Early-Stage Medical Aesthetics Investment Shifts Toward Underlying Technology | FreeS Research

Self-Pampering Psychology or Appearance Anxiety? Exploring the Underlying Drivers of the Trillion-Yuan Medical Aesthetics Industry

In Greek mythology, Pygmalion was a sculptor who carved an ivory statue based on his ideal vision of feminine beauty, then fell deeply in love with his own creation. Moved by this devotion, Aphrodite brought the statue to life. Modern medical aesthetics technology has turned people into Pygmalions of a sort — redefining and sculpting their ideal faces through hyaluronic acid injections, picosecond lasers, Thermage, and Hi-Body treatments, among countless other methods.

In its 2019 China Medical Aesthetics Industry Trends Research Report, iResearch noted that China's medical aesthetics market grew from 64.8 billion yuan to 176.9 billion yuan between 2015 and 2019, representing a compound annual growth rate of 28.7%. According to the Gen Z Trend Beauty Consumption Insights Report, jointly published by CBNData and Tmall International in 2020, the top five most popular skincare ingredients among Gen Z (those born between 1995 and 2009) were amino acids, hyaluronic acid, niacinamide, collagen, and salicylic acid. This consumer enthusiasm has carried over to secondary markets, where medical aesthetics stocks such as Bloomage Biotech and Imeik Technology have each surpassed 100 billion yuan in market capitalization.

Why is the medical aesthetics industry so hot? What broader trends does this reflect? In this article, we'll explore:

- How did the medical aesthetics industry develop?

- What exactly are the core products in this space: hyaluronic acid and botulinum toxin?

- What pivotal moments shaped the trajectories of industry giants Allergan, Bloomage Biotech, and Imeik Technology?

- In terms of business model, is Bloomage Biotech positioning itself as the Huawei of medical aesthetics?

- What will be the next blockbuster medical aesthetics product?

First, our overarching thoughts on the industry:

1. The medical aesthetics industry has technical moats; attention has shifted from its service attributes to its underlying technology

Overall, the medical aesthetics industry has meaningful barriers in technology and manufacturing processes, spanning microbial fermentation as well as materials science and synthesis. For example, producing hyaluronic acid requires expertise in strain selection, fermentation formulation and process control, plus cross-linking chemistry and related materials science.

Moreover, different applications and demands impose distinct requirements on materials and their associated synthesis techniques. These require continuous experimentation and accumulated know-how. Sometimes these explorations take years.

In earlier years, investment in medical aesthetics concentrated on the midstream segment, where the focus was on the industry's service attributes — medical aesthetics and consumer healthcare institutions. Later, attention shifted downstream to customer acquisition channels and traffic platforms.

With the listings of Bloomage Biotech, Imeik Technology, and other medical aesthetics stocks, the upstream segment has garnered more attention. Investors now prioritize underlying technology — from injectables and equipment to materials synthesis, microbial fermentation, and tool platforms. FreeS Fund also focuses on researching and uncovering innovative technologies and products in the upstream medical aesthetics space. For instance, in 2020, Bluepha — a synthetic biology company and FreeS angel-round portfolio company — partnered with L'Oréal to develop functional skincare products. Memtech, another FreeS-backed biotech cosmetics company, is developing scalp care functional ingredients and products based on cutting-edge protein peptide technology.

2. The trend toward M&A and consolidation in China's medical aesthetics industry is just emerging

The expansion of industry giant Allergan demonstrates one viable path for medical aesthetics companies: not going it alone, but pursuing acquisition and consolidation within the industry.

China's medical aesthetics leaders such as Bloomage Biotech and Imeik Technology have only just "come of age," and the trend toward M&A and consolidation is only beginning to surface. These Chinese giants sit upstream, controlling core raw materials and industry discourse. Judging by market penetration and other metrics, they have growth potential far beyond what Allergan has achieved.

3. Single-technology, single-product opportunities remain enormous

Most medical aesthetics giants — Allergan, Bloomage Biotech, and others — built their success on single technologies (such as hyaluronic acid synthesis and cross-linking) and single products (such as hyaluronic acid and botulinum toxin). We believe single-technology and single-product plays still hold tremendous promise, with the potential to birth the next "Bloomage Biotech." That said, discovering the next "hyaluronic acid" or "botulinum toxin" may be a once-in-decades opportunity.

What's notable is that this represents a classic cross-disciplinary innovation direction (biology + consumer). We believe virtually all innovation today is cross-boundary, with breakthroughs occurring at the intersection of disciplines. We welcome entrepreneurs and industry experts to continue the conversation with us (lei@freesvc.com). We also welcome candidates with industry backgrounds and interest in biopharma or consumer investment to join our team (hr@freesvc.com).

A Brief Introduction to Medical Aesthetics

By Lei Wang (lei@freesvc.com)

/ 01 /

The History of the Medical Aesthetics Industry

The formal name for the medical aesthetics industry is "Medical Aesthetics." It was originally defined internationally as the use of surgery, drugs, medical devices, and other medical techniques by clinical physicians or specialists to alter a patient's appearance, including facial features and body contours.

During World War I and World War II, reconstructive surgery emerged to help soldiers with limb disabilities and other survivors reintegrate into society. This drove the development of the global medical aesthetics industry. At the time, there were no dedicated plastic surgeons; some general surgeons transitioned into plastic and orthodontic work, shifting from the fine art of surgical life-saving to working on faces.

Following the Korean War and the Great Leap Forward's backyard furnace campaign in late 1957, China saw a sharp rise in burn patients. Hospitals across the country established burn and plastic surgery departments, cultivating a generation of plastic surgery talent. Even so, China's current pool of plastic surgeons remains quite small.

/ 02 /

What Categories Does the Medical Aesthetics Industry Include?

Beauty supplements, services at spa and slimming centers/medical aesthetics clinics, even color cosmetics — all fall within the broad umbrella of "pan-medical aesthetics." However, under China's official classification, medical aesthetics is divided into four main categories: cosmetic surgery, cosmetic dermatology, cosmetic dentistry, and cosmetic traditional Chinese medicine.

Cosmetic surgery covers procedures like rhinoplasty and breast augmentation. It has stringent standards and requirements for facility licensing and practitioner qualifications; these surgeries must be performed by certified plastic surgeons in hospital plastic surgery departments or equivalent settings.

Compared to cosmetic surgery, cosmetic dermatology faces relatively looser regulation. Botulinum toxin, hyaluronic acid, and other skin-improving injectables, as well as photoelectric treatments for superficial skin concerns, all fall under this category.

Orthodontics and teeth whitening belong to cosmetic dentistry. Cosmetic traditional Chinese medicine encompasses cupping, internal and external herbal treatments, and various other therapeutic approaches.

/ 03 /

Why Has the Medical Aesthetics Industry Heated Up in Recent Years?

Why has the medical aesthetics industry become so hot in recent years?

First, upstream technology has advanced by leaps and bounds, steadily improving the safety of medical aesthetics procedures.

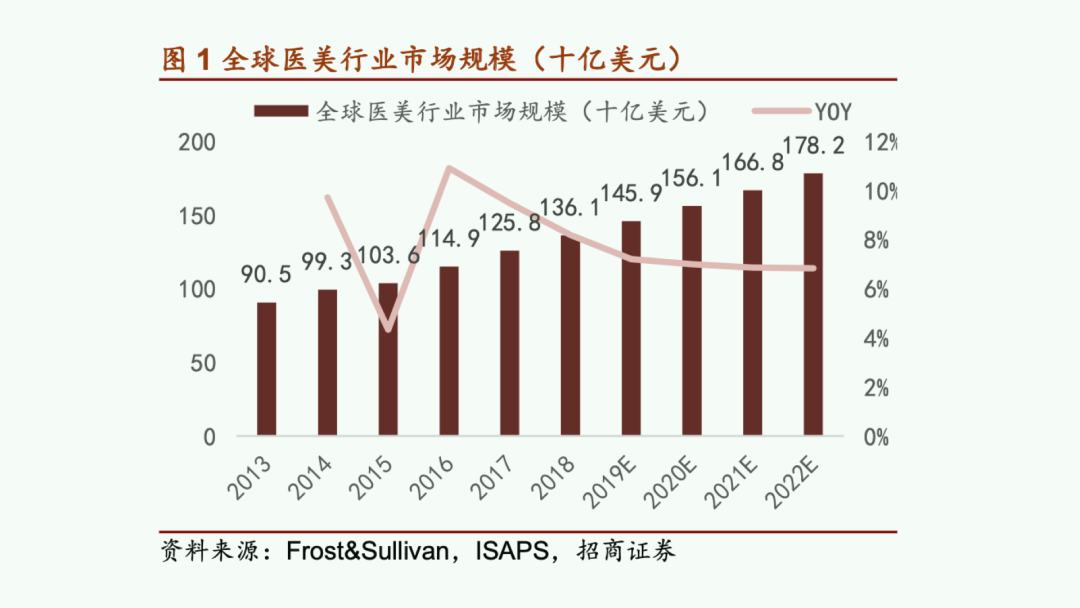

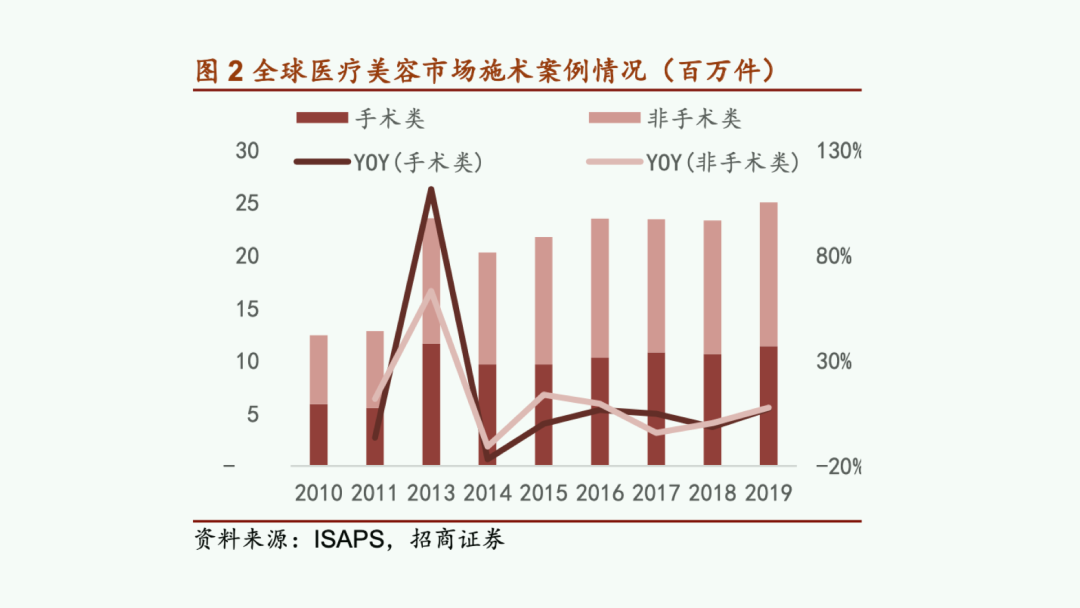

Second, the middle class has expanded rapidly, and many consumers have grown comfortable spending several thousand yuan on a single hyaluronic acid injection. According to a research report from China Merchants Bank, the global medical aesthetics market surpassed one trillion yuan in 2019. Within the industry, non-surgical procedures grew at a CAGR of 9.7%, while surgical procedures grew at 8.6%.

Additionally, whether driven by positive "self-pleasure" motivations or negative "appearance anxiety," consumer attention and demand for beauty enhancement and anti-aging have risen continuously. Baidu Index data shows that from December 2013 to May 2021, search volume for "medical aesthetics" climbed from roughly 140 to over 1,800, peaking at over 2,900.

/ 04 /

Differences Among China, US, and South Korea Medical Aesthetics Markets

The United States, China, and Brazil together account for nearly half of the global medical aesthetics market. According to a report from third-party research firm Frost & Sullivan, China became the second-largest medical aesthetics services market in 2018, capturing approximately 13.5% of global market share. By 2019, China's medical aesthetics market had reached 176.9 billion yuan.

Medical aesthetics users and their product preferences differ substantially between China and the US. Chinese consumers are predominantly under 35 — it's common to see post-95s sharing their medical aesthetics experiences on mainstream social platforms. American consumers, by contrast, are mostly over 35. In terms of products, US users favor "lifting" and "skin tightening" anti-aging treatments. Chinese consumers undergoing surgical procedures concentrate on breast augmentation, rhinoplasty, and double-eyelid surgery — primarily appearance-altering rather than age-related concerns.

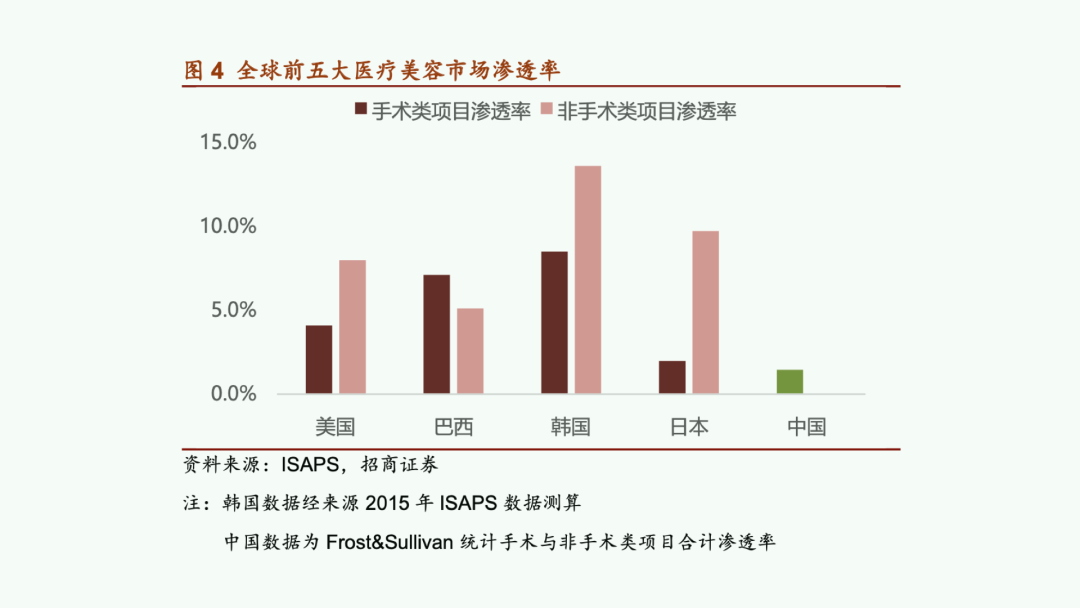

Compared to the US, South Korea, and Brazil, China has lower medical aesthetics market penetration. According to calculations by ISAPS (International Society of Aesthetic Plastic Surgery) and China Merchants Securities: in South Korea in 2015, surgical procedures had penetrated to nearly 9% of medical aesthetics consumers — meaning 9% of those who had undergone beauty treatments had gone under the knife — while nearly 14% had received non-surgical injectable treatments. In 2018, China's medical aesthetics penetration was just 1.45%. Frost & Sullivan data from 2019 showed this rising to 3.6%, still far below South Korea, the US, and other countries. This indicates substantial potential across both surgical and non-surgical segments in China's medical aesthetics market.

/ 05 /

Surgical vs. Non-Surgical Products

Surgical procedures include breast augmentation, liposuction, eyelid surgery, abdominoplasty, rhinoplasty, and other projects that alter a consumer's overall facial appearance. Non-surgical procedures include Botox, hyaluronic acid fillers, hair removal, and non-surgical fat reduction — all relatively minimally invasive treatments.

The advantages and disadvantages of surgical and non-surgical procedures are fairly well-defined. Generally, non-surgical options involve less trauma, lower per-session cost, faster recovery, and lower risk, though their effects don't last as long. Surgical procedures, meanwhile, tend to carry higher price tags, require longer recovery periods, but deliver longer-lasting results.

In China's medical aesthetics market, total consumption of surgical procedures falls below that of non-surgical treatments. However, surgical products generate significantly higher overall revenue and gross margins than their non-surgical counterparts. As a result, licensed cosmetic clinics or hospitals may prioritize recommending surgical procedures to consumers.

/ 06 /

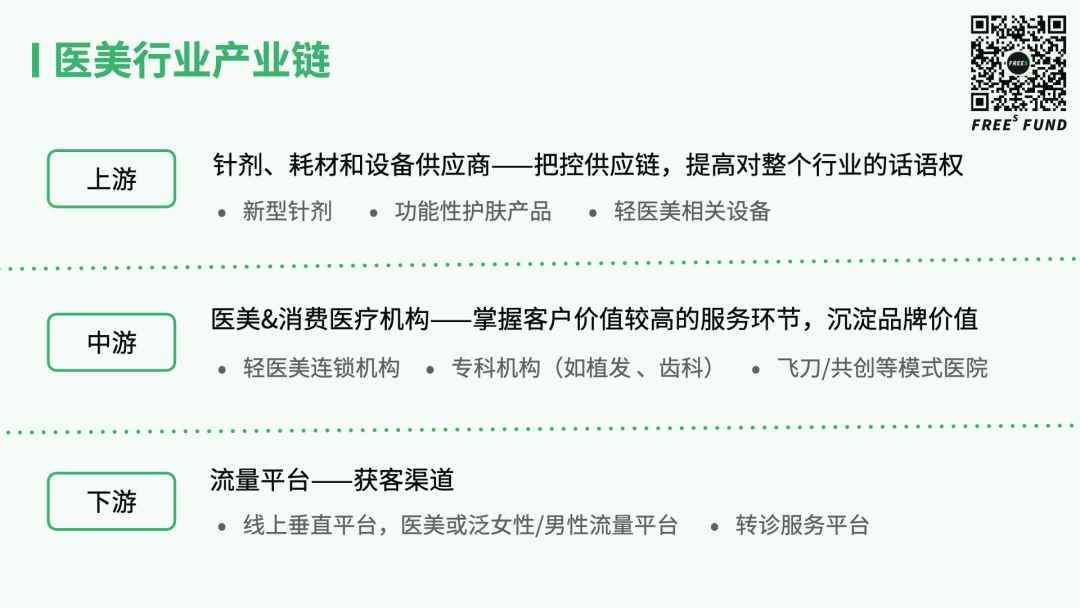

The Medical Aesthetics Industry Chain

Having covered the industry's development history and market size, let's walk through the upstream, midstream, and downstream segments of the medical aesthetics value chain.

The upstream segment comprises injectable, consumable, and equipment suppliers like Bloomage Biotech. Their products include various novel injectables, functional skincare products, and light medical aesthetics devices. These companies strengthen their voice across the industry by controlling supply chains.

The midstream segment refers to medical aesthetics and consumer healthcare institutions — light medical aesthetics chains, specialized clinics (hair transplants, dentistry, etc.), and innovative models like "flying knife" arrangements (where doctors perform surgeries at other hospitals during their off-hours) or co-creation hospitals. The midstream controls the high-value service touchpoints with customers and can build brand equity.

The downstream segment consists mainly of traffic platforms, including online vertical platforms and referral service platforms. They control customer acquisition channels for the medical aesthetics industry.

Broadly speaking, upstream and downstream players in medical aesthetics enjoy stronger profitability, while competition among midstream institutions is more intense.

In earlier years, investment in medical aesthetics concentrated heavily on the midstream. Investors focused on the industry's service-sector characteristics, primarily evaluating medical aesthetics and consumer healthcare institutions. Later, attention shifted downstream to customer acquisition channels and traffic platforms.

With the IPOs of Bloomage Biotech, Imeik Technology, and other medical aesthetics stocks, the upstream segment gained greater attention. Investors began emphasizing underlying technology — from injectables and equipment to material synthesis, microbial fermentation, and tool platforms. FreeS Fund also focuses on researching and uncovering innovative technologies and products in the upstream medical aesthetics space. For example, in 2020, FreeS Fund's angel-round portfolio company Bluepha, a synthetic biology firm, partnered with L'Oréal to develop functional skincare products. Another FreeS-backed company, biotech cosmetics firm Meimu Technology, is developing scalp care active ingredients and products based on cutting-edge protein peptide technology.

/ 07 /

Core Upstream Products: Hyaluronic Acid and Botulinum Toxin

Within the upstream medical aesthetics segment, there aren't many well-known domestic or international companies. Global leader Allergan historically operated in both ophthalmology and medical aesthetics before spinning off its eye care business to focus exclusively on aesthetics. Major Chinese players include Bloomage Biotech, Haohai Biological Technology, and Imeik Technology.

These upstream companies primarily produce two product categories: botulinum toxin and hyaluronic acid.

Botulinum toxin is classified as a pharmaceutical product requiring Phase III clinical trials. Hyaluronic acid falls under consumables, with relatively high industry concentration and strong profitability. Compared to these two leading medical aesthetics products, photoelectric devices account for a very small share of consumption.

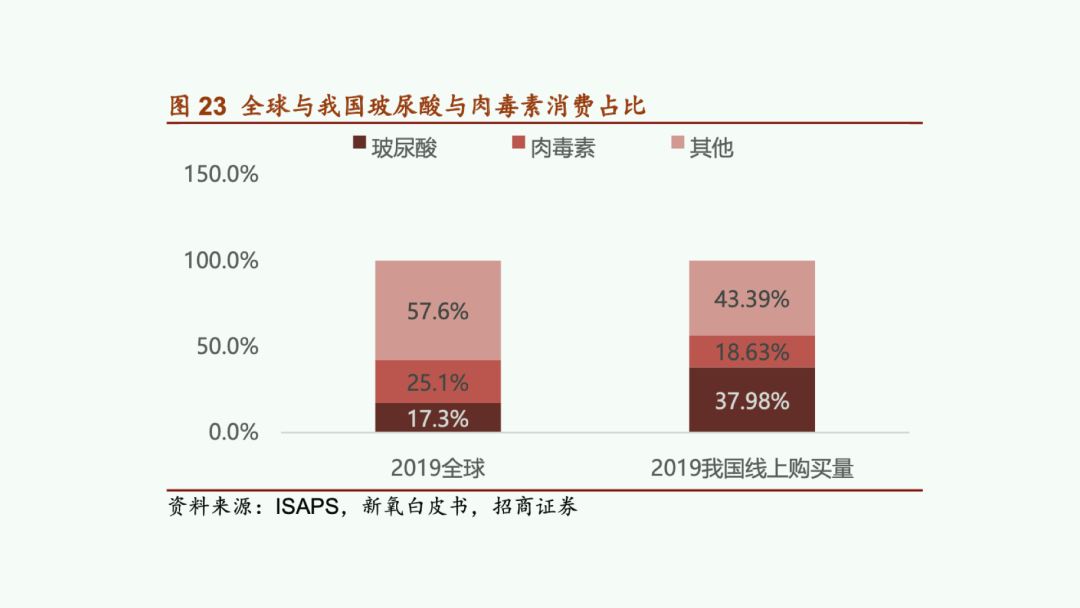

Data from ISAPS, So-Young White Paper, and China Merchants Securities Research shows that in 2019, hyaluronic acid and botulinum toxin accounted for 17.3% and 25.1% of global medical aesthetics consumption respectively. Chinese and global consumers show notable differences in their purchasing patterns for these two products. In 2019, global botulinum toxin consumption surpassed hyaluronic acid at 25.1% versus 17.3%, while in China, hyaluronic acid consumption (37.98%) far exceeded botulinum toxin (18.63%).

What makes hyaluronic acid and botulinum toxin so appealing?

▍ Hyaluronic Acid

Hyaluronic acid's scientific name is hyaluronan — a transparent, naturally occurring polysaccharide with a gelatinous crystalline structure. Polysaccharides are abundant in human connective tissue and the dermis. It's relatively natural, with moisturizing, lubricating, and skin-nourishing properties, and can promote skin absorption of certain nutrients.

▲ A novel hyaluronic acid product launched by Bloomage Biotech. Image source: Bloomage Biotech official website

American scientists first discovered hyaluronan in bovine vitreous humor in 1934. In the 1980s, Japanese company Shiseido began using microorganisms to synthesize hyaluronic acid. In China, Bloomage Biotech has developed its own microbial synthesis platform. Hyaluronic acid production technology has become one of Bloomage's core competencies. Looking ahead, microbial synthesis represents the long-term future direction for the hyaluronic acid industry.

Beyond synthesis technology, another critical production technique is cross-linking. Single-chain hyaluronic acid molecules are rapidly metabolized by enzymes in the human body. To use this natural substance for body filling, hyaluronic acid must first be cross-linked into harder, more resilient, and less easily metabolized high-molecular-weight forms.

Currently, many medical aesthetics companies focus R&D around this single molecule. Compared to pharmaceutical or biotech firms researching numerous molecules, these aesthetics companies show less diversity. However, developing such products involves exceptionally high barriers to entry.

Depending on molecular size, elasticity, and hardness, hyaluronic acid can be deployed across different applications. Single-molecule or small-molecule hyaluronic acid is primarily applied topically for hydration and moisturization. Cross-linked, harder, more elastic hyaluronic acid is mainly injected for filling, adding facial volume and resilience.

In the hyaluronic acid market, the dominant giant is Allergan. Before acquiring hyaluronic acid technology in 2007, Allergan was best known for Botox, its botulinum toxin product. After 2002, Allergan executed a series of acquisitions in the medical aesthetics space. Bloomage Biotech was the earliest entrant into China's hyaluronic acid industry, securing first-mover advantage and becoming a global giant in hyaluronic acid raw materials. Bloomage's prospectus reveals that Shanghai Yushi Medical Technology, Harbin Sanlian Pharmaceutical, Jiuzhou Tong Group, and other companies purchase hyaluronic acid from Bloomage. We'll analyze the development trajectories of domestic and international medical aesthetics giants in detail below.

▍ Botulinum Toxin

Botulinum toxin is a toxin produced during the growth of Clostridium botulinum. It's a neuromuscular transmission blocker — initially used only in clinical treatment, such as injecting botulinum toxin to treat cervical dystonia, with no aesthetic applications.

▲ Before-and-after results using Botox. Image source: Botox official website

In 1992, Allergan acquired the patent for botulinum toxin production and developed Botox, a wrinkle-inhibiting product. For example, injecting botulinum toxin into the masseter muscle causes surrounding muscles to contract, keeping the masseter relatively still during chewing and gradually slimming the face. Similarly, injecting it into the forehead blocks motor signals from reaching forehead muscles when you raise your eyebrows, hiding frown lines.

▲ Botox product image. Image source: Botox Hong Kong official website

However, botulinum toxin is an extremely potent natural toxin — among the deadliest substances on Earth. One milligram of purified crystalline botulinum toxin can kill 200 million mice. Consequently, China classifies botulinum toxin as a biological weapon. Lanzhou Institute of Biological Products is one of the few domestic enterprises qualified to research and produce botulinum toxin. According to the company's website, as early as March 1934, the Republican-era Central Health Administration approved establishing the Northwest Epidemic Prevention Office in Lanzhou (predecessor of Lanzhou Institute). After the outbreak of the War of Resistance Against Japanese Aggression, the office specialized in producing vaccines, blood products, and toxins for supply to over ten provinces.

Currently, Type A botulinum toxin dominates medical aesthetics applications, with relatively fixed molecular structure. However, once injected into muscle, botulinum toxin follows a certain metabolic cycle, typically requiring re-injection every 6 to 12 months.

Presently, manufacturers including Allergan are developing slower-release or faster-release botulinum toxin products to meet user preferences for either quicker dissipation or longer-lasting effects. Developing such products demands high biotech capabilities, typically involving the addition of different proteins to botulinum toxin to modify protein activity.

▍ Other Products

Upstream medical aesthetics products also include implantable fillers and photoelectric devices. Both categories currently represent small markets in China, likely under RMB 1 billion. Most implantable fillers in the Chinese market are imported from South Korea. Going forward, growing awareness of skin management and increasing demand for anti-aging solutions may drive growth in the photoelectric device sector.

/ 08 /

Case Studies: Allergan, Bloomage Biotech, Imeik Technology

Currently, multiple medical aesthetics companies trade on China's A-share market, including Bloomage Biotech, Imeik Technology, Haohai Biological, and Huadong Medicine, among others. However, China's medical aesthetics industry remains in an early development stage, with ample room for improvement in product sophistication, technical content, and variety.

Based on 2019 revenue, Allergan's medical aesthetics product revenue was several multiples that of Bloomage Biotech, Imeik Technology, and Haohai Biological combined. If China can fully unlock the potential of the world's second-largest medical aesthetics market, and if these companies can continue delivering strong products, they face enormous growth runway — and the medical aesthetics track holds opportunity for new entrants as well.

How did Allergan, the giant of the medical aesthetics industry, rise to prominence? What lessons does its trajectory hold for China's medical aesthetics sector? And what distinguishes the development paths of Bloomage Biotech and Imeik Technology in China?

▍Allergan: From Eye Drops to "Aesthetics Empire"

▲ Image source: Allergan China official website

Allergan is the world's largest medical aesthetics company. Many Chinese medical aesthetics firms aspire to benchmark against it, claiming they want to become "China's Allergan."

Allergan began as an Irish company. In 1948, Irish pharmacist Gavin Herbert developed an antihistamine eye drop named Allergan. In 1950, he founded Allergan Pharmaceuticals, continuing to develop novel eye drops and expand its ophthalmology portfolio. By 1965, Allergan had expanded into overseas markets including New York, becoming an international pharmaceutical company.

In 1989, after Oculinum — the world's first botulinum toxin product — received FDA approval for treating strabismus and blepharospasm, Allergan recognized its potential to inhibit neuromuscular transmission. The company acquired Oculinum and rebranded it as Botox.

Subsequently, Allergan continuously expanded Botox's applications, such as for wrinkle reduction and facial slimming, and built its business around this growth. Over the following decades, Allergan executed more than thirty acquisitions in the aesthetics segment, constructing an increasingly vast "aesthetics empire."

In 2002, Allergan divested its eye drop and contact lens businesses to focus exclusively on aesthetics, consolidating and acquiring hyaluronic acid fillers, dermal fillers, and eyelash growth serums.

In 2020, AbbVie acquired Allergan for $68 billion, becoming the world's fourth-largest pharmaceutical company. According to a 2019 Chemical & Engineering News report, the acquisition would bring AbbVie nearly $16 billion in annual sales, with the majority of revenue contribution coming from hyaluronic acid and botulinum toxin products.

▍Bloomage Biotech: The Huawei of Medical Aesthetics?

▲ Image source: Bloomage Biotech official website

In 2001, China Bloomage International Investment Group invested in Bloomage Biotech's predecessor (Shandong Freda Biotech Engineering Co.) and acquired its microbial fermentation technology. According to a 2019 Global and China Hyaluronic Acid (HA) Industry Market Research Report by third-party research firm Frost & Sullivan, Bloomage Biotech is the world's largest producer and seller of hyaluronic acid, with a 38.96% market share by sales volume in 2019 — exceeding the combined market share of the second through fifth ranked global companies.

Bloomage Biotech is a biotechnology and bioactive materials company focused on functional sugars and amino acid substances that benefit human health. In some respects, Bloomage Biotech resembles the Huawei of medical aesthetics. Just as Huawei possesses core chip technology and controls everything from chips to processors, communications technology, and hardware devices, Bloomage Biotech holds core bio-fermentation technology, extending from its fermentation platform to crosslinking technology platforms and downstream into a range of injectable and filler products.

In recent years, Bloomage Biotech has also developed hyaluronic acid derivatives and expanded toward consumer-facing products, including injectable HA, topical HA fillers, and skincare brands like Biohyalux (润百颜) that incorporate hyaluronic acid ingredients.

On January 7, 2021, China's National Health Commission formally approved Bloomage Biotech's application to recognize sodium hyaluronate (i.e., hyaluronic acid) as a new food raw material, permitting its use in ordinary food products. After securing its food additive license, Bloomage Biotech launched an HA food brand called "Hey Zero" (黑零). As reported by Guangming Online, this marked the formal entry of hyaluronic acid food products into the era of domestic production.

If Bloomage Biotech's food business develops successfully, it will carry hyaluronic acid into far broader domains. Bloomage Biotech has taken another step toward becoming "Huawei."

As its full-industry-chain capabilities have gradually come together, Bloomage Biotech has also begun pursuing horizontal expansion through a series of acquisitions — purchasing innovative companies such as French firm Revitacare and Dongying Foste Biotech Engineering. This development approach bears some resemblance to Allergan's strategy.

▍Imeik Technology: Deep Focus on Verticals with Distinct Product Advantages

▲ Image source: Imeik Technology official website

Imeik Technology is an innovative company in the field of biomedical soft tissue repair materials, listed on China's A-share market in September 2020. The company focuses primarily on injectable dermal filler products and thread lifting (线雕) products, and has not yet directly expanded into consumer-facing distribution.

According to Imeik Technology's 2020 annual report: "The company's full-year performance growth was driven primarily by solution-type injectable products centered on Hearty (嗨体). In 2020, this product category achieved operating revenue of RMB 447 million, representing year-over-year growth of 82.85%."

"Hearty" is Imeik Technology's flagship product — hyaluronic acid injected into the neck to smooth out neck wrinkles. Currently, Hearty is the only Class III medical device approved in China specifically targeting neck wrinkles. The product builds upon hyaluronic acid's functions by adding carnosine, which has strong antioxidant properties.

Furthermore, Hearty has expanded hyaluronic acid's application from the face to the neck. Going forward, new products targeting the legs or other body parts may emerge in the market.

What Will Be the Next Breakout Product in Medical Aesthetics?

Beyond hyaluronic acid and botulinum toxin, what other products show promise in today's medical aesthetics market?

One category includes supplementary products such as collagen and poly-L-lactic acid (PLLA).

Collagen is suitable for small-area transplantation and supplementation, triggering collagen proliferation to provide skin support. Collagen sources fall into two categories: human-like recombinant and porcine-derived. Several upstream medical aesthetics companies are already developing products around collagen. Could collagen become the industry's next breakout product?

Then there's poly-L-lactic acid. The recently popular "youth injections" (童颜针) use PLLA as a raw material for large-area filling. Imeik Technology's Class III PLLA device is currently in registration and application stage. Once approved, it will become China's exclusive Class III youth injection.

Another category comprises facial support materials.

Highly crosslinked large-molecule hyaluronic acid and bone-structural materials can compensate for facial changes caused by bone loss. Highly crosslinked large-molecule HA uses more crosslinking agents during manufacturing, resulting in higher crosslinking density, firmer overall texture, less diffusion, and stronger cohesiveness after injection — making it suitable for facial sculpting. However, the durability of these materials remains insufficient, leaving substantial room for improvement.

FreeS Fund portfolio company Meimu Technology, a biotech cosmetics firm, is developing scalp care active ingredients and products based on cutting-edge protein peptide technology. These products activate cellular activity by providing skin with source protein peptides. From its founding, Meimu Technology established a biotech raw material R&D platform, pursuing brand innovation starting from the most fundamental raw material level. The company now controls the entire process from raw materials to production to finished product efficacy and safety assessment.

Meimu Technology's founder holds a PhD in biochemistry and molecular biology from Peking University, and previously held key R&D positions at Procter & Gamble (the world's largest consumer goods company) and Novozymes (a global leader in industrial enzymes and microorganisms). He brings substantial experience in biomedicine, cross-disciplinary cosmetics R&D, and product development bridging industry, academia, research, and medicine.

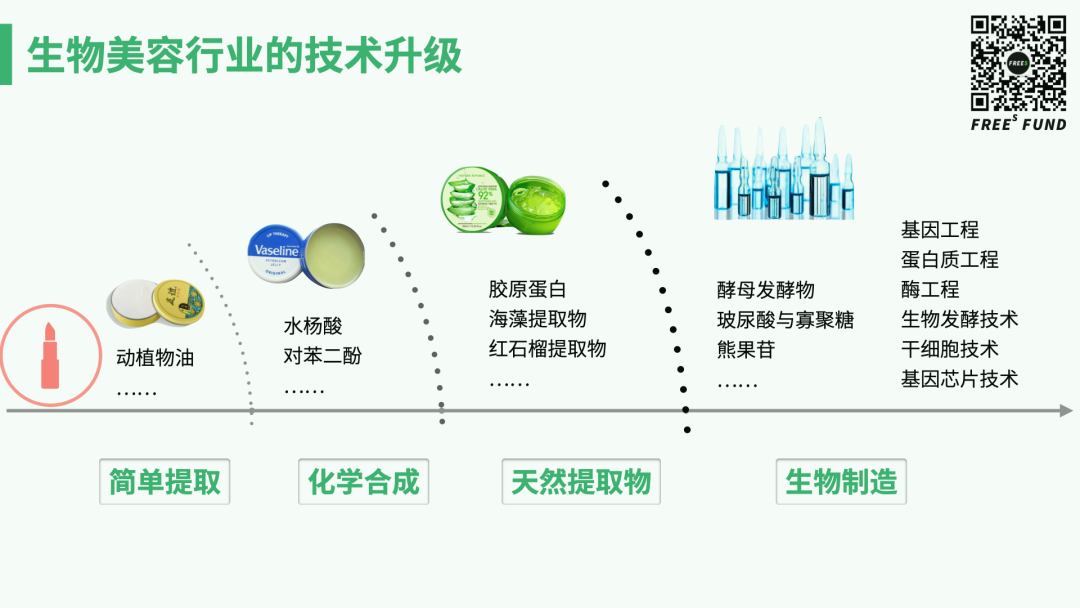

The trend we observe is that technologies used in the bio-beauty industry have evolved from simple extraction to chemical synthesis to natural extracts, and are now undergoing a technological upgrade toward biotech applications. This technological advancement itself may give birth to new brands.

Such bio + consumer cross-disciplinary projects represent one of FreeS Fund's key focus areas. We believe that innovation today is almost entirely cross-disciplinary, and breakthrough innovations frequently occur at the intersection of disciplines.

Beyond Meimu Technology, FreeS Fund's angel-round portfolio company Bluepha collaborated with L'Oréal in 2020 to jointly develop functional skincare products. Bluepha is a molecular and materials innovation company built on "biotechnology + industrial internet." The company is committed to creating commercially imaginative innovative products through bio-computation and testing platforms, including the only plastic capable of degrading in natural environments (including seawater), industrial hemp components for combating anxiety and pain, and hangover remedies to address the alcohol metabolism genetic deficiency prevalent among East Asian populations.

What Will Be the Next Breakout Product in Medical Aesthetics?

1. Medical aesthetics has technical barriers; the industry is shifting from a services focus to underlying technology

Overall, the medical aesthetics industry possesses technical and process barriers involving microbial fermentation technology as well as materials science and synthesis techniques. For example, producing hyaluronic acid requires expertise in strain selection, fermentation formulation conditions, and process control — alongside crosslinking-related materials science and synthesis capabilities.

Moreover, different application scenarios and demands impose varying requirements on materials and their associated synthesis technologies. Medical aesthetics companies must continuously explore and accumulate know-how through this process. Sometimes these explorations span years.

In earlier years, medical aesthetics investment concentrated primarily in the industry's midstream, with greater attention to the sector's services attributes — mainly medical aesthetics or consumer healthcare institutions. Later, investors began looking downstream at customer acquisition channels and traffic platforms.

With the listings of companies like Bloomage Biotech and Imeik Technology, the upstream segment has gained increasing attention. Investors now place greater emphasis on underlying technologies — from injectables and equipment to materials synthesis technology, microbial fermentation technology, and tool platforms. FreeS Fund also focuses on researching and uncovering innovative technologies and products in the upstream medical aesthetics industry. For example, in 2020, FreeS Fund's angel-round portfolio company Bluepha, a synthetic biology enterprise, collaborated with L'Oréal to jointly develop functional skincare products. FreeS Fund's portfolio company Meimu Technology is developing scalp care active ingredients and products based on cutting-edge protein peptide technology.

2. The trend toward acquisition and consolidation in China's medical aesthetics industry is beginning to emerge

The development history of medical aesthetics giant Allergan's expansion of its commercial footprint demonstrates one viable path for medical aesthetics companies: not relying on going it alone, but rather pursuing acquisition and consolidation within the industry.

Chinese players like Bloomage Biotechnology and Imeik are still in their early stages, and China's medical aesthetics industry is only just beginning to show signs of acquisition and consolidation. These domestic giants sit upstream in the value chain, controlling core raw materials and wielding significant industry influence. Judging by metrics like market penetration, their growth potential compared to Allergan remains vast — far beyond what most imagine.

3. Single-technology, single-product plays still hold enormous promise

Most medical aesthetics giants, whether Allergan or Bloomage Biotechnology, built their empires on a single technology (such as hyaluronic acid synthesis or cross-linking techniques) or a single product (such as hyaluronic acid fillers or botulinum toxin). We believe single-technology and single-product opportunities remain promising — there's still room for the next "Bloomage Biotechnology" to emerge. That said, discovering the next "hyaluronic acid" or "botulinum toxin" may be a once-in-decades opportunity.

Galaxies in Your Eyes: A Visual Guide to the Colored Contact Lens Boom | FreeS Research

Join Us

We are seeking investors in biotech, deep tech, and consumer/TMT across Beijing, Shanghai, and Shenzhen. If you have an industry background and an interest in investing, we'd love to hear from you — and we welcome referrals to strong candidates as well. (For full job descriptions, please click the "Read More" link at the end of this article.) Please send your resume to hr@freesvc.com. Email subject line: Application for "[Biotech / Tech / Consumer] Investor" — "[Preferred Location]"

We are also recruiting interns for investment research, legal, finance, HR (portfolio management direction), and video content operations. Interested students are welcome to apply. (For full job descriptions, please click the "Read More" link at the end of this article.)

Internship duration: 3–5 months, 3–5 days per week on-site. Based in Beijing preferred.

Please send your resume to hr@freesvc.com.

Email subject line: Position Applied For — Name — School — Major — Minimum Internship Commitment (x months) — Days per Week (x days) — Earliest Available Start Date