Expansion or Store Closures: Reassessing Offline Opportunities | Li Feng Column

From "Store Opening Boom" to "Store Closing Wave": Reassessing Offline Opportunities

Not long ago, Haidilao announced that it would gradually shut down 300 stores by December 31, 2021. This is seen as the largest wave of store closures since the company's IPO.

Haidilao wasn't alone. Starting around mid-year, several major chain restaurant brands became embroiled in large-scale closure controversies. While commentary has focused on the pitfalls of rapid expansion under COVID-19, this may also be an opportunity to re-examine offline opportunities in our new pandemic-normal.

Before diving in, a few perspectives to share:

-

During the pandemic, using the rent dividend period to expand against the trend was a common choice for leading restaurant chains. But opportunities conceal risks. In the process of rapid expansion, companies are prone to mistakes — errors in evaluating and selecting locations, organizational structures and talent pipelines that can't keep pace with expansion speed, and so on. The result is underperformance. This risk was amplified by an environment where restaurant consumption recovery fell short of expectations.

-

The restaurant industry is like this; other industries are similar. When companies race to capture territory during industry downturns and rapidly increase market share, they inevitably bear the uncertainty that comes with fast expansion. If they fail the test, rapid expansion backfires. There are two sides to every coin.

-

We need to judge whether offline development gained through this window period represents only short-term dividends. Different industries have different answers. Over the past year, many internet-born brands have increased their offline presence. This was essentially rapid offline expansion completed during the pandemic window, helping brands accelerate their omnichannel buildout. But like chain restaurants, they face the same challenge after completing offline expansion: whether the omnichannel sales growth brought by COVID-19 is merely a short-term dividend. We may not have a clear answer until after 2022.

-

We cannot infer from the "wave of store closures" in offline food and beverage services that offline expansion is unnecessary, or wholly deny the value of counter-trend expansion. It only proves that simply "opening stores at high density" during a window period makes it difficult to convert short-term dividends into long-term advantages. During a market dividend period, rapid expansion is a strategic response that was reasonable at the time. But when economic and market conditions change, choosing to close some stores is also a necessary adjustment to cyclical changes. If deep-seated problems can be solved in the process, it's also an opportunity to strengthen on an already enlarged plate.

-

In the social consumer retail sector, offline importance should not be questioned because of "store closure waves." For brands to develop sustainably, online-only isn't big enough, and offline-only isn't big enough either.

-

In the past, retail brands could be "big first, good later." As long as you had sufficient advantage in one link, scale could grow rapidly. After growing big through some advantage in the retail channel, brands could patch things up later. Now it's different. Consumer entrepreneurship relying on single-point advantages is no longer enough to sustain growth, so you can only be "good first, then big" — at minimum, "good and big simultaneously."

-

Current competition between enterprises, especially in saturated markets, depends importantly on who understands the entire chain better, who achieves higher relative efficiency across the full chain and pushes it to the limit — that's who becomes more competitive. So to be "good" means constantly breaking through efficiency bottlenecks, whether in services or retail. Second, compared to the past when companies could win market favor simply by delivering good value, today's consumers have higher and more comprehensive demands, requiring stronger product development capabilities — products need to be "better, more beautiful, with stronger spiritual added value."

Hoping this brings you a different angle for thinking about these issues.

▲ Source: Haidilao Hotpot Weibo

01 The "Bottom-Fishing" Opportunity That COVID-19 Brought to Offline

To understand what "shutting down 300 stores" means, we need some comparison. "300" represents about 19% of Haidilao's total global stores as of end-June this year, equivalent to 55% of Haidilao's net new stores added in 2020.

To understand the "closure wave," we need to start with the "expansion wave."

Before this round of closures, Haidilao experienced more than two years of continuous expansion. Before 2019, Haidilao's total global stores approached 470. In 2019 alone, store count increased 65%. 2020 saw even more acceleration, with 544 new stores — nearly 1.8 times the number opened in 2019.

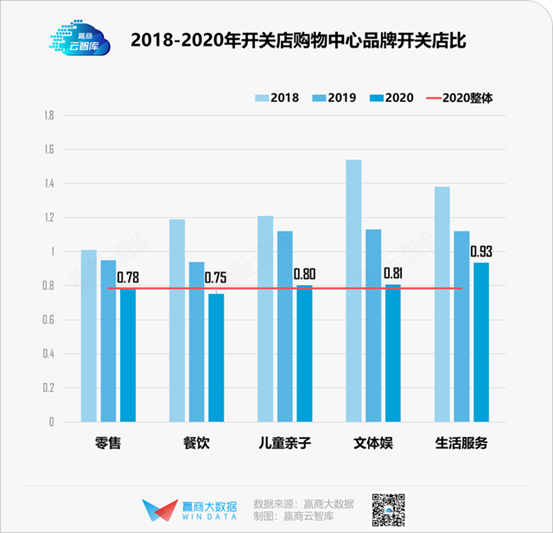

A key precondition for this acceleration was the pandemic's impact. COVID-19 brought "crisis" to many industries. Winshang Cloud Think Tank once surveyed 1,080 shopping centers over 50,000 square meters across 21 cities, finding that in 2020, nearly 78,000 stores closed while about 61,000 opened, for an overall opening-to-closing ratio of 0.78.

▲ Source: Winshang Big Data

This fully demonstrates the two sides of "crisis."

On one hand, for many businesses and small merchants with weaker risk resistance, sustained uncertainty from COVID-19 forced them to terminate leases and cease operations.

On the other hand, early in the pandemic, shopping malls and street-facing shops saw large numbers of vacant spaces — supply increased while demand decreased, and commercial rents fell. For leading enterprises that already counted "expanding coverage" as a key strategic direction, a rare "bottom-fishing" opportunity emerged.

Even pre-pandemic, Haidilao enjoyed relative rent advantages; malls typically offered favorable rents hoping to draw foot traffic through Haidilao's presence. Its strong brand power gave it even more bargaining leverage during the pandemic. According to a research report from Zhongtai International in October 2021, Haidilao's rent costs were only about 4%, roughly 10 percentage points lower than industry peers.

In this ebb and flow, it wasn't just Haidilao — restaurant chains using this rent dividend period to expand against the trend became an industry-wide phenomenon. A white paper from the China Chain Store & Franchise Association showed that in 2020, China's restaurant market chain penetration rate increased from 13.3% in 2019 to 15.0%.

Worth noting: restaurant chains' counter-trend expansion also won recognition from much capital. You may recall that this year, chain noodle shops received successive capital investments, with Chinese fast-casual brands represented by noodle shops riding a financing wave. Given China's restaurant industry still has considerable room for chain penetration growth, the investment logic around chain noodle brands is fundamentally sound.

And hot pot, because it puts all raw materials and flavor satisfaction into one solution, is the category most likely to break through the ceiling of Chinese restaurant chain penetration. So by this logic, for the hot pot industry, "counter-trend expansion" was arguably a wise choice at the time. We discussed this in October's Hot Noodles + Hot Capital: Can They Create a Chinese "McDonald's"? | FreeS Daily Business Thoughts.

Stories always hold surprises; opportunities often conceal risks.

02 The Challenges of Offline Counter-Trend Expansion

From "expansion wave" to "closure wave," the turning point came within a year.

In fact, as early as May this year, another hot pot giant, Xiabuxiabu, announced it would close 200 loss-making stores. Xiabuxiabu founder He Guangqi stated that losses were mainly due to serious site selection errors at some stores.

This aligns with Haidilao's November announcement. Haidilao attributed underperformance to errors in evaluating and selecting "locations" amid rapid expansion, along with existing talent pipeline development speed being unable to keep pace with location coverage expansion.

According to Haidilao executive director and chief strategy officer Zhou Zhaocheng, three dimensions were considered in selecting which stores to close: "First, whether the external commercial district and foot traffic can support store operations; second, whether surrounding store density is too high; third, whether the single store's financial data is in a ramp-up period and whether short-term profitability has room for improvement."

This partly reflects how chain restaurants' business logic differs from the internet industry. The scale effects championed by the internet cannot be simply applied to the restaurant industry.

The restaurant industry has a saying: "One hurdle at a hundred stores, another at a thousand." When companies race to capture territory during industry and market downturns and rapidly increase market share, they inevitably bear the uncertainty of fast expansion. Rapidly increasing store counts tests chain restaurants' organizational structure, operational management, and talent pipeline capabilities. If they fail this test, rapid expansion backfires. There are two sides to every coin.

Beyond internal company factors, the broader environment also contributed to the "closure wave."

Many of the 300 stores announced for closure were opened in 2020 and 2021. On November 9, Haidilao executive director and co-CEO Yang Lijuan told Caijing in an interview: "In March 2020, COVID-19 was stabilizing. When we reopened in April and May, recovery was relatively fast, plus stores were easy to find and [rent] terms were favorable — we thought it might be an opportunity and wanted to seize it. We didn't expect the pandemic to recur and last this long."

Restaurants represent the single largest industry collection in social consumer retail. From 2015 to 2019, restaurant industry growth exceeded both total retail sales and GDP growth. The industry's four-year compound growth rate was 9.7%. If COVID-19 had been a short-term event, in a high-growth track where companies seized a rare window, the story might have developed differently.

However, pandemic recurrence brought more persistent impact to restaurants than imagined.

According to National Bureau of Statistics data, from January to December 2020, national restaurant revenue was 3.9527 trillion yuan, down 16.6% year-over-year; from January to October 2021, restaurant revenue was 3.7211 trillion yuan, essentially flat with January-October 2019's 3.6932 trillion yuan.

In other words, two years into the pandemic, consumer spending power has yet to return to "year-over-year growth" trajectory, remaining merely "essentially flat." Against this backdrop of restaurant consumption recovery falling short of expectations, once companies are insufficiently cautious in rapid store expansion, negative chain reactions follow: high-density store openings cannibalize single-store profits, table turnover rates decline, and net profits decrease.

Another predictable development: once offline consumption capacity recovers to certain levels, small merchants (or mom-and-pop shops) that lacked risk resistance during the pandemic or closed temporarily due to uncertainty will spring back "like grass in spring." Notably, compared to convenience stores with chain penetration around 23%, "mom-and-pop shops" scattered across streets and alleys still maintain substantial market share. According to Beijing Daily, citing 2017 survey data, "mom-and-pop shops" contributed 40% of all retail channel shipment volume.

Similarly, while many small restaurants are modest in scale, they often distinguish themselves through distinctive flavors and maintain certain advantages in operational efficiency and management costs. Meanwhile, because China's restaurant market is extremely segmented by consumption scenario and spending capacity, once overall consumption markets warm, small shops will find new room for survival and development.

03 How to View Counter-Trend Expansion: Long-Term Opportunity or Short-Term Dividend?

Of course, it's worth emphasizing that any judgment we make now is, to some extent, "Monday morning quarterbacking." In the circumstances at the time, seizing counter-trend expansion opportunities was industry consensus. It was very difficult to accurately predict COVID-19's duration or whether there would be recurrences. This was a completely new challenge for everyone; all were dynamically adjusting and responding amid change.

But from "expansion wave" to "closure wave," this process leaves us with a question: how should we view counter-trend expansion? If we face similar circumstances again, how should we judge whether this is a long-term opportunity or short-term dividend?

As "Monday morning quarterbacks," whether what Haidilao and others faced was a long-term opportunity or short-term dividend, you likely have your own judgment now. But if we broaden our view, does this mean counter-trend offline expansion in other industries under COVID-19 follows the same logic and leads to the same results?

Let's take food and beverage social consumer goods, which account for about 40% of total retail sales.

In April this year, we explored in Li Feng: Will Consumer Investment Stay Hot in 2021? | FreeS Research Institute that 2020's consumer track was very hot, importantly because major offline retail brands' "dormancy" gave internet-born brands opportunities to occupy offline shelf space — especially small and medium enterprises with online buzz and brand recognition that happened to have new products.

Over the past year, many internet-born brands have increased offline presence. This was essentially rapid offline expansion completed during the pandemic window. The "rent dividend" from COVID-19 attracted not only Haidilao but also emerging coffee brands, new tea drinks, new Chinese-style pastry shops, beauty collection stores, and others that rose rapidly.

Take Chicecream (Zhong Xue Gao) as an example. Ice cream consumption has impulsive and casual characteristics, with offline purchase frequency far exceeding online. After building strong brand momentum online, starting in 2020, Chicecream strengthened offline channels beyond national online sales — deploying in supermarkets, convenience stores, and emerging retail terminals, opening flagship and pop-up stores, building out omnichannel sales. According to public data, Chicecream's omnichannel sales grew 300% year-over-year in the first four months of 2021.

▲ Source: Chicecream Weibo

Chicecream hosted a yellow rice wine ice cream private tasting event in Shanghai.

For these internet-born brands, the pandemic window similarly accelerated their omnichannel buildout. But like chain restaurants, after completing expansion they face the same challenge: whether COVID-19-driven omnichannel sales growth is merely a short-term dividend, and how to convert it into long-term opportunity.

The importance of offline experience is gradually increasing. For a long time, users were accustomed to seeing products offline then comparing prices online; now user behavior has shifted to being "planted with grass" online, then consuming offline. But competing offline enters traditional brands' home turf. A key advantage of established brands is their national supply chain.

If you've been paying attention, you'll notice that convenience store freezer ice cream prices have noticeably increased this year — more varieties exceeding eight or even ten yuan, with high new product ratios besides the price increases. This means offline competition is intensifying.

The same goes for sparkling water. In 2021, convenience store sparkling water brands and new products have become dizzying. Among them are international giants that lay dormant for a year during the pandemic, as well as new brands that quickly followed.

So to judge whether offline development gained through the window period is merely short-term dividend requires a longer view. By next summer, will these new brands still occupy top-three positions in consumer mindshare? After all, fundamentally, what matters isn't shelf space but consumer mindshare — who can maintain a place in consumers' hearts after intense competition.

If new brands can emerge from this fierce offline elimination round, they've made it. We may need until 2023 to fully clarify the results and significance of this 2020 "window period" growth.

/ 04 / While Prediction Is Hard, These Things Are Certain

▍Offline Expansion Is Important and Necessary

Beyond Haidilao and Xiabuxiabu, well-known new tea drink brand ChaYanYueSe also announced on November 10 that it had temporarily closed nearly 100 stores in Changsha, stating this was the third wave of concentrated temporary closures this year. The first two occurred early this year and during the late-July COVID-19 recurrence. ChaYanYueSe stated that temporary closures in some overly dense areas will become normal, "as the company must bear the results of sharply reduced foot traffic from COVID-19."

Of course, we cannot infer from the "closure wave" in offline food and beverage services that offline expansion is unnecessary, or wholly deny counter-trend expansion's value. It only shows that simply "opening stores at high density" during a window period is insufficient; more must be done to convert short-term dividends into the beginning of long-term advantage.

Returning to Haidilao's example: alongside the closure announcement, Haidilao announced implementation of a "Woodpecker Plan" to address operational difficulties. "Woodpeckers are good at finding pests beneath tree bark; we hope to use the woodpecker spirit to find and improve deep-seated management problems." According to Haidilao, these closures are not "permanent" — some lower-traffic, underperforming stores will be reopened after adjustments when timing is appropriate.

Thus we can see that during market dividend periods, rapid expansion is a strategic response that was reasonable at the time. But when economic and market environments change, choosing to close some stores is also a necessary adjustment to cyclical changes. If deep-seated problems can be solved in the process, it's also an opportunity to strengthen on an already enlarged plate.

And for other social consumer brands, one view is certain — online-only isn't big enough, and offline-only isn't big enough either.

According to latest data released by the National Bureau of Statistics on November 15, in the first 10 months this year, online retail sales of physical goods grew 14.6% year-over-year, accounting for 23.7% of total social consumer retail sales. That is, in physical consumer goods, online channels account for about one-quarter, while offline holds three-quarters. Therefore, for any medium-sized or larger enterprise, an omnichannel development path is essential.

In October this year, we also discussed offline importance with "Squirrel Dad" in Dialogue with Zhang Liaoyuan: Two Years After IPO, How Does Three Squirrels Think About Next Steps? | FreeS Interview. Dad shared his thinking on offline importance: "From zero to one for a brand, online efficiency is highest; but most of people's living radius is still offline, to take a brand from one to ten, you still have to go offline."

For many internet-born brands, the importance of full-domain reach is increasingly prominent — they want consumers to think of them first when consuming a category, and also want consumers to be able to see and buy them first.

So in the social consumer retail sector, offline importance should similarly not be questioned because of "closure waves."

▍How to Convert Short-Term Dividends into the Beginning of Long-Term Opportunity?

So for entrepreneurs, how can short-term dividends be converted as much as possible into the beginning of long-term opportunity?

Before Hong Kong stock market opening on November 12, Haidilao announced plans to place 115 million shares through an old-for-new placement, raising approximately HK$2.337 billion net. The company intends to use about 30.0% of the net proceeds to enhance supply chain management and product development capabilities.

Haidilao's response to this crisis may offer entrepreneurs some inspiration.

- From "big first, good later" to "good first, then big," or at least "good and big simultaneously"

In the past, retail brands could be "big first, good later." Back then, retail was still in rapid development both offline and online; as long as you had sufficient advantage in one link, scale could grow rapidly. This link could be supply chain, product strength, or traffic. After growing big through some advantage in the retail channel, brands could patch things up later.

But now it's different — you can only be "good first, then big." China's retail industry has matured considerably; both consumer and supply chain maturity have greatly improved, with fierce competition both offline and online. Entrepreneurship relying on single-point advantages is no longer enough to sustain growth, so you can only be "good first, then big" — at minimum, "good and big simultaneously."

- To be "good first, then big" or "good and big simultaneously," what does "good" mean?

"Good" has rich connotations; we won't exhaustively cover them today, but mainly look at two measurement dimensions.

First is full-chain efficiency.

Current competition between enterprises, especially in saturated markets, depends importantly on who understands the entire chain better, who achieves higher relative efficiency across the full chain and pushes it to the limit — that's who becomes more competitive. So to be "good" means constantly breaking through efficiency bottlenecks, whether in services or retail.

Second is product strength.

Today's consumers have significantly improved independent thinking ability and information acquisition efficiency compared to the past. Compared to when companies could win market favor simply by delivering good value, today's consumers have higher and more comprehensive demands. You need to do everything possible to make them recognize that you're genuinely worth the money or even exceeding value in many aspects.

So product development capability requirements are higher, manifested in products that are "better, more beautiful, with stronger spiritual added value." This requires companies to emphasize co-creation space and emotional appeal.

First, co-creation space. Haidilao's fancy sauce bar falls in this category. On Xiaohongshu, you can see all kinds of user-created notes showing how they mixed special dipping sauces or new ways to eat. Another example is Saturnbird (San Dun Ban). Saturnbird's ultra-instant, convenient characteristics give consumers rich operational possibilities — various ways to drink: iced, warm, hot; with water, oat milk, sparkling water, cocoa milk, or with ice cream, etc. This creative participation increases brand freshness and experience; consumers feel they participated in the creation process rather than being boxed in or limited.

▲ Source: Saturnbird Weibo

Second, emotional appeal. As social consumption levels rise, we've long since left behind material scarcity eras, with higher requirements for products' spiritual attributes — for example, greater emphasis on environmental attributes, personalization degree, and more connection with values that brands convey.

For more on this, you can click Breaking Consumer Industry Involution: Is the Secret "Making It Expensive"? | Li Feng Column for more of our thinking.

Discussion In this piece, we've shared our research on offline consumption. We especially welcome you to share your observations and thoughts in the comments: How do you view the future of offline chain brands?

Contact Us

We always look forward to meeting more innovators in the consumer sector. Welcome to send your BP to bp@freesvc.com. We also welcome those interested in consumer investment to join us at hr@freesvc.com.

FreeS Report 25: From China's Dietary Structure, Viewing Food Investment

Hot Noodles + Hot Capital: Can They Create a Chinese "McDonald's"? | FreeS Daily Business Thoughts

"Interconnection" Begins: What Are the Long-Term Impacts for Consumer Brands? | FreeS Daily Business Thoughts

Li Feng: Will Consumer Investment Stay Hot in 2021? | FreeS Research Institute