Farewell to Tradition, Decoding Complexity: How Can the Insurance Industry Transform and Upgrade? | FreeS Fund Fintech Venture Capital Summit Transcript

How Can Insurtech Serve the 800 Million People Without Coverage?

As personal wealth has grown, Chinese households' investable assets surpassed 200 trillion RMB in 2019. Meanwhile, with China allowing foreign financial firms to enter as wholly-owned enterprises, the launch of stock market registration-based IPOs, and the gradual adoption of innovative technologies like blockchain and AI in finance, China stands at the starting line of a new wave of financial innovation.

We believe that truly outstanding companies will have the opportunity to participate in this fintech innovation wave and contribute their value.

How to seize the trillion-dollar opportunity brought by this structural shift? FreeS Fund has partnered with Silicon Valley Live, CreditEase Wealth Management, and Plug and Play to launch the FreeS Fintech Venture Summit 2020, featuring four online themed livestreams and one offline FreeS-exclusive Fintech Open Day.

Today, we're sharing the fourth installment of the "FreeS Fintech Venture Summit 2020" series, focused on insurtech. The traditional, complex insurance industry holds massive opportunities for upgrading. Currently, the industry's digitization remains in a relatively early stage. Whether considering insured entities, overall insurance business processes, or the transformation of agent systems, there remains substantial room for digitalization to play a role. Product innovation oriented toward customer needs, built on digital foundations, is equally worth exploring.

In this livestream hosted by Weili Dong, FreeS Fund's North America head, Pengqi Liu, FreeS Fund investment VP, traced the development of insurtech and interpreted trends and opportunities in the space. Qingfeng Zhang, founder of FreeS portfolio company Aixuan Technology, shared his thinking and practice on insurtech. They discussed: how to capture opportunities from the insurance industry's transformation and upgrading, and how to solve product homogenization problems to meet incremental market demands.

Before diving in, a few key takeaways:

- The insurtech industry has three main characteristics that interact with each other: comprehensive business digitization using innovative technologies as tools; a shift from relatively closed systems toward building open, collaborative, win-win ecosystems; and insurers moving from top-down market strategies to strategies grounded in underlying customer needs and service.

- Insurance companies' digital transformation remains in a very early stage, with many opportunities still available.

- One inflection point for the insurance industry came in 2013 with the emergence of internet insurers represented by ZhongAn; another came around 2017 with the establishment of the China Banking and Insurance Regulatory Commission (CBIRC) and its emphasis on "insurance should be insurance." These changes truly ushered in a great era for insurtech development.

- The companies most likely to scale are those capable of connecting different players across the entire insurance ecosystem and outputting complete solutions for the whole ecosystem, rather than merely providing single-point technology outputs.

- Using technology to precisely measure risk can serve as a means to address product homogenization and user demographic homogenization. For service homogenization, using technology to manage chronic diseases represents an extremely effective breakthrough point.

- The underlying moats of insurtech companies include three aspects: capability, data, and superior algorithms. Capability comprises four components: actuarial pricing capability, risk control and underwriting capability, sales capability, and investment capability. Beyond capability, data is needed. Taking health insurance as an example, three types of outcome data are required: data accumulated from the insurance industry's claims practice, medical insurance data, and physical examination data.

Below is the essence of the conversation, which we hope will be helpful. On October 17, from 9:00 AM to 12:30 PM, the "Fintech Exclusive Open Day" will take place. We've already received registrations from hundreds of attendees and sent out the first wave of offline invitations.

If you'd still like to join, please scan the QR code to register before 9:00 AM on October 14 (the Fintech Exclusive Open Day offers both offline and online participation options).

Contact Us

Fintech has been a focus area for FreeS since our founding. We've invested in over 10 companies in related directions, including consumer finance, supply chain finance, wealth management and asset management, as well as new technologies related to financial big data and insurtech. Entrepreneurs and industry experts are welcome to reach out:

Pengqi Liu, VP at FreeS Fund

We also look forward to those interested in joining our investment team (contact: hr@freesvc.com).

**/ 01 / **

The Development History of the Insurance Industry and Drivers of Change

▍Why does the most complex insurance industry present upgrade opportunities?

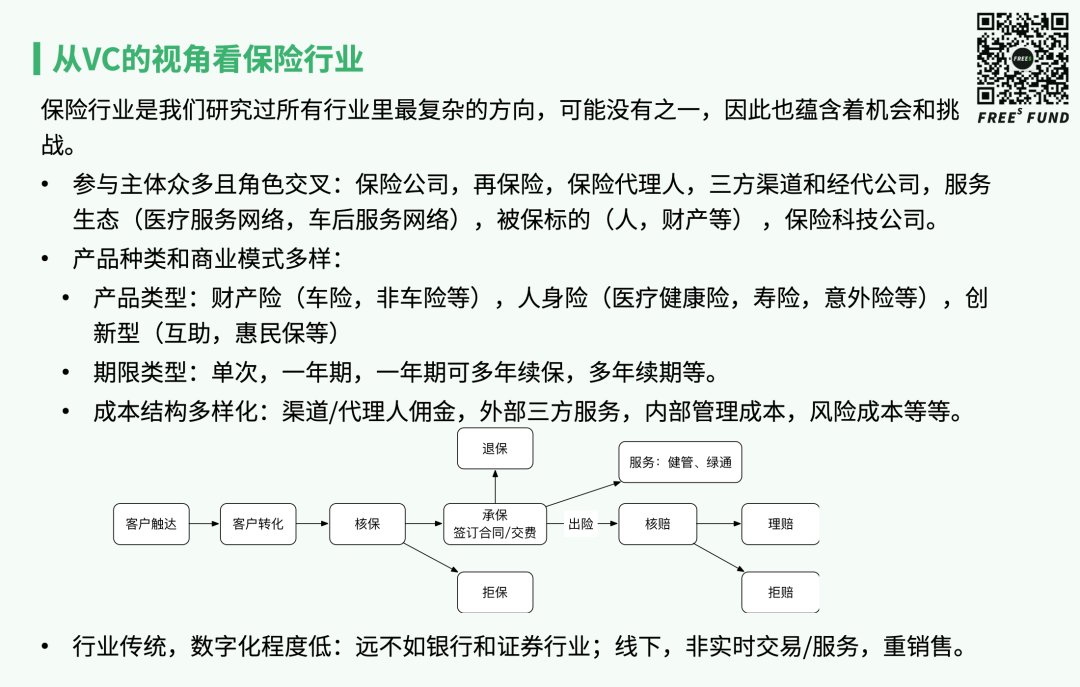

FreeS began paying attention to the insurance direction around 2019, focusing on identifying entrepreneurs and projects in the industry. After extensive research, insurance may be the most complex industry we've ever studied. Why do we say this?

First, the insurance industry chain involves numerous roles, including insurance companies, sales channels, insurtech companies serving insurers, service networks, and more. Second, the origin and purpose of insurance is to help us diversify various risks, so insurance is naturally relevant to all industries, leading to particularly diverse and rich insurance product types and business models.

Although insurance sits within the broader fintech sector, it remains relatively traditional compared to banking and securities. The industry's informatization and digitalization levels are low, with substantial non-real-time transactions and service environments, and heavy reliance on sales.

It is precisely because of the insurance industry's complexity and relative traditionalism that massive upgrade opportunities exist.

▍What trends have emerged in the insurance industry?

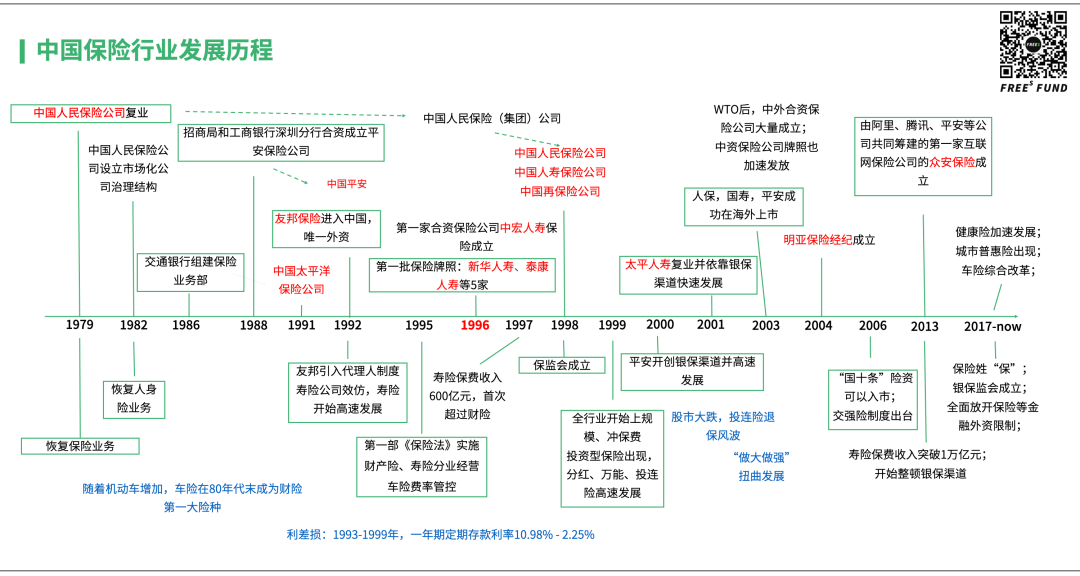

Roughly 200 years ago during the late Qing dynasty, as Chinese ports opened, China's insurance market was born. 1979 marked the starting point of modern China's insurance industry. After resuming operations, China's insurance industry developed very rapidly overall, especially with the establishment of the China Insurance Regulatory Commission (CIRC) in 1998, which ushered in a development climax for the insurance market.

In the preceding years, changes in China's insurance industry were primarily model-related, with genuine innovations involving new technology being relatively scarce. Looking at results, for example, the auto insurance market entered a state lacking innovation in recent years, driven purely by sales and price wars. Life insurance also once evolved into a wealth management product form that "competed" with banks for household deposits.

One inflection point for the insurance industry came in 2013 with the emergence of internet insurers represented by ZhongAn; another came around 2017 with the establishment of the CBIRC and its emphasis on "insurance should be insurance." It was these changes that truly ushered in a great era for insurtech.

Before 2017, much like internet finance back then, when we discussed insurtech innovation, we basically only talked about internet insurance.

But the difference between internet insurance and internet finance is that innovation in internet finance existed across the entire front, middle, and back offices — comprehensive innovation across channels, funding sources, and asset sides. Internet insurance, however, might simply mean selling insurance over the internet, merely a process of channel digitization.

Within internet insurance, genuine innovation based on internet scenarios themselves was very scarce. Scenario-based insurance like aviation accident insurance and return shipping fee insurance had relatively minor impact on insurance's overall market. To this day, the online penetration rate of overall insurance sales remains far below 10%.

But we've also seen some positive trends, such as Huize's IPO this year, and the rapid development and scaling of channels like Ant Group, Waterdrop, and WeSure. Some new-generation internet insurance technology companies have also emerged in the industry.

After 2017, the most significant macro policy change was the merger of the banking and insurance regulators and the proposal that "insurance should be insurance."

"Insurance should be insurance" emphasized that insurance must return to its roots — it exists to guard against risk, not to compete with banks for customers. After this shift, innovation in the insurance industry mainly manifested in two areas: health and medical insurance, and auto insurance.

First, looking at health and medical insurance. The combination of medical reform and changes in the insurance domain made health and medical insurance a very hot direction. ZhongAn launched its "Zunxiang e-Sheng Million Medical" product in 2016, becoming a market "blockbuster."

Health and medical insurance continues to evolve, with city-based inclusive insurance recently emerging as a new direction. Thus, health and medical insurance is a meaningful and vibrant field.

Turning to auto insurance. As mentioned earlier, auto insurance has entered a stage of stock competition. The auto insurance market is large, roughly 500 billion RMB, but the three insurers PICC, Ping An, and CPIC hold over 60% market share, while other small and medium-sized property insurers are basically in a state of thin profits or losses.

This year, the comprehensive auto insurance reform officially launched, with mandates to cut costs, improve efficiency, and raise quality. Whether it's the development of auto insurance itself or the broader business transformation of these property insurers toward new non-auto lines, it's clear the auto insurance sector has entered a period of disruption.

▍How is the insurance industry approaching digital transformation?

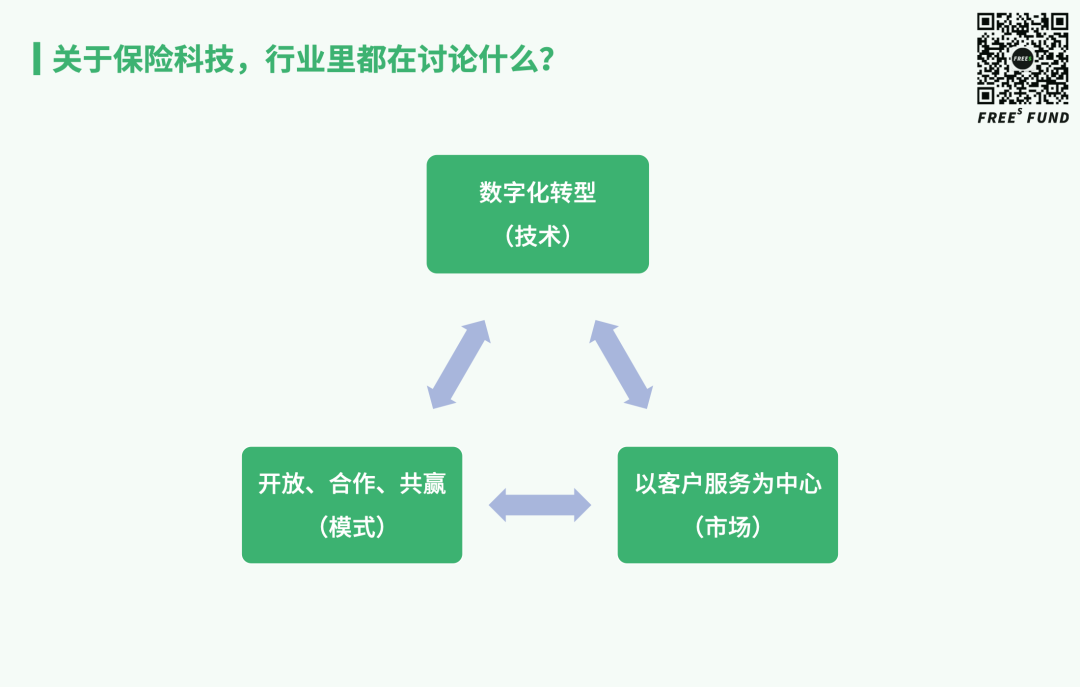

Broadly speaking, the insurtech sector has three main characteristics that interact with and reinforce one another:

- Comprehensive business digitization driven by innovative technologies.

- A shift from relatively closed operating models toward open, collaborative ecosystems built on mutual benefit.

- A pivot from top-down market strategies to approaches grounded in underlying customer needs and service delivery.

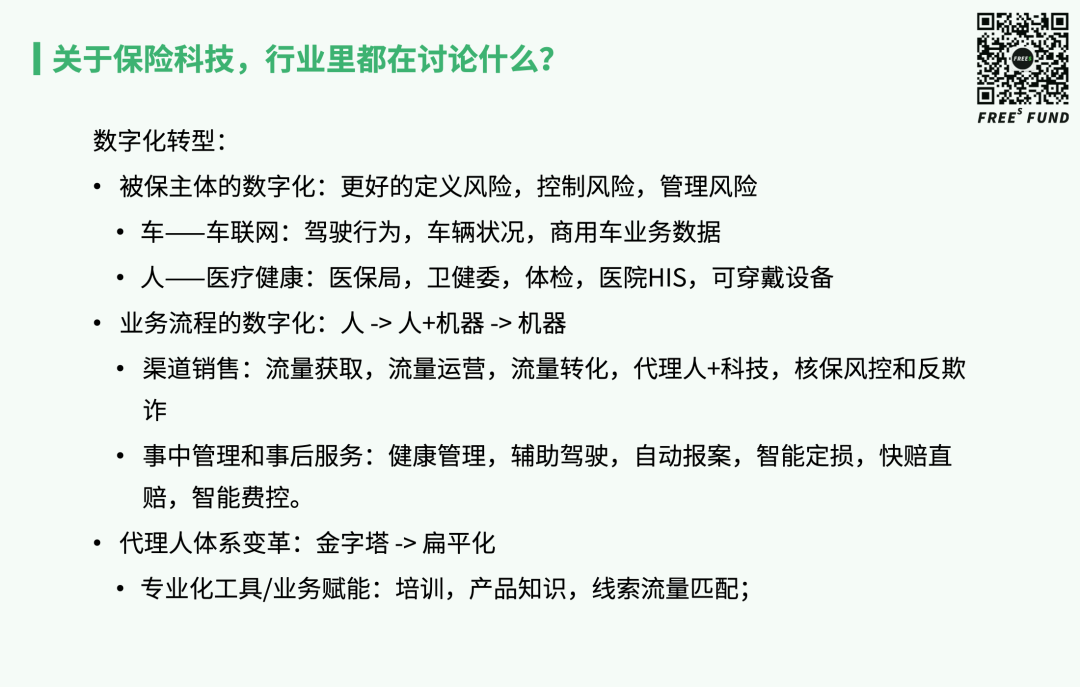

Let's start with digital transformation. For the insurance industry, digitization is still in a relatively early stage.

First, the digitization of insured subjects remains sorely inadequate.

Take the vehicle in auto insurance. At the point of underwriting, insurers know the model, age, and the driver's claims history — but they know very little about the actual condition of the vehicle or the driver's behavior.

For health insurance, beyond the age and gender used to reference mortality and critical illness tables, insurers lack deeper understanding of individual health status.

The degree of digitization is a critical factor affecting product innovation for vehicle- and person-related insurance. Without digital understanding of these subjects, you cannot define risk, let alone help customers control and manage it. More fundamentally, without the ability to define risk for different subjects, you cannot create corresponding insurance products.

Second, there's the digitization of overall insurance business processes.

On the sales front, digital tools can improve conversion efficiency for direct-to-consumer channels. There may also be opportunities in tools for agents — the "To A" segment. Upfront, underwriting risk control and anti-fraud capabilities can be embedded.

Post-underwriting, there's substantial work to be done both during and after the coverage period. Risk management and health management investments can be made, such as family doctors or second opinion services. For auto insurance, monitoring commercial vehicle driving risk could be an important approach.

When claims actually occur, operations and settlement can become more digital and intelligent — automatic reporting, intelligent damage assessment, fast and direct claims payment, and so on.

End-to-end process digitization helps the industry accumulate data, reduce costs, and improve timeliness, while delivering better service experiences to customers.

Third, there's growing discussion about transforming the agent system.

Can this system evolve from its current pyramid structure toward greater flattening?

The trend toward flatter agent structures is already quite pronounced. Once agents break away from the pyramid, they'll need more professional tools and capability support — enhanced training, product configuration knowledge, customer profiling, and demand matching, all aimed at improving efficiency.

▍How is the insurance industry's operating model changing?

As mentioned earlier, the insurance industry involves many participants, but their endowments differ significantly.

Insurers hold valuable licenses, yet sales remain painful for small and mid-sized property insurers. Different players also vary considerably in their capacity to invest in innovation.

Tech companies may have strong technical capabilities, but often lack understanding of specific insurance business scenarios and the internal interest dynamics of the insurance system. This creates major challenges when choosing business models and executing on the ground.

A positive trend is that within the insurance ecosystem, insurers are shifting from pure risk transfer roles toward comprehensive service provider models. They're beginning to collaborate closely with external partners across sales channels, risk control, product design, and service networks to deliver integrated solutions to customers.

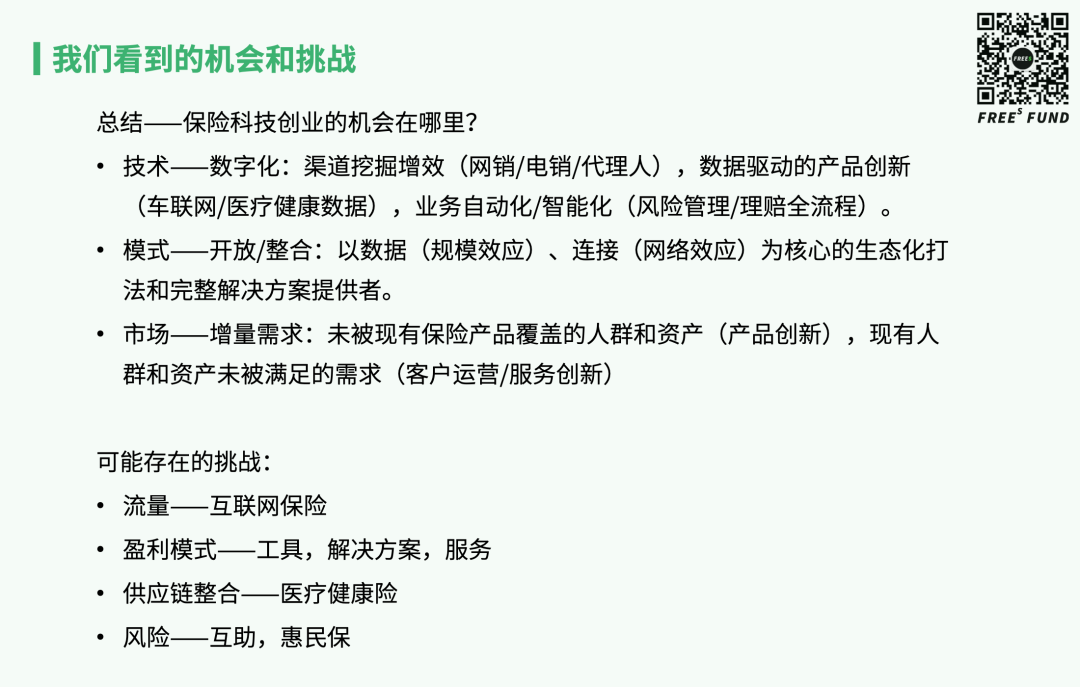

Thus, the opportunity for insurtech companies lies in providing services to insurers across product development, distribution, claims, risk control, and risk management.

Currently, the companies we see as most likely to scale are those capable of connecting different players across the insurance ecosystem and delivering complete solutions rather than single-point technology outputs.

For health insurers, this means effectively integrating data from hospital systems, pharmaceutical manufacturers, health management services, and data collection devices. For auto insurers, it means unifying the post-sale vehicle service market, vehicle operations market, and connected vehicle data onto a single platform for holistic service innovation.

▍How is the insurance industry's service model changing?

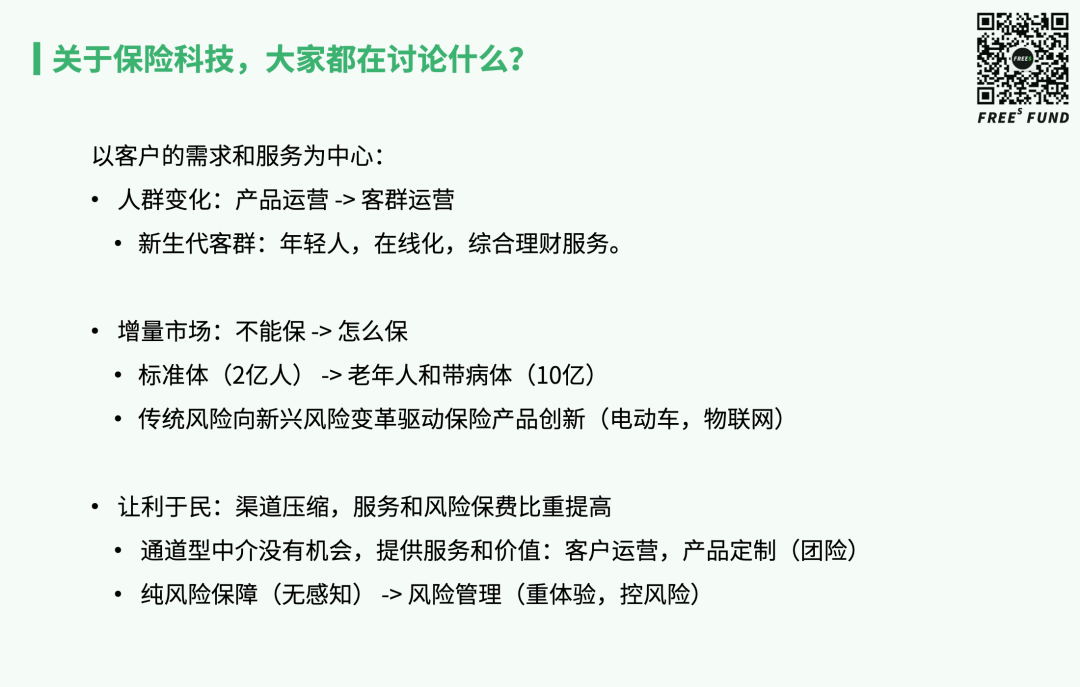

The entire insurance industry is now emphasizing customer-centricity in needs and service. Three examples illustrate this.

First, demographic shifts are pronounced. The population targeted by insurance sales is growing noticeably younger. Compared to older generations, these young people have more diverse demands. They likely want more online-native experiences, and they need insurers to move from single-product operations toward holistic customer segment operations. Beyond selling insurance products to these young people, should insurers also meet their broader wealth management needs?

Second, incremental market demand deserves attention. How can previously uninsurable populations be brought into coverage? Health insurance has primarily covered healthy populations. But in reality, truly healthy people represent a minority — there's a vast population of sub-healthy individuals, those with pre-existing conditions, and the elderly who remain unserved. This currently uninsurable segment represents an incremental market of 800 million people. Are there opportunities to serve them?

As society continues to evolve, new risk protection needs constantly emerge — related to electric vehicles, IoT integrated with various industries — creating substantial innovation opportunities. So many insurtech companies aren't just focused on traditional insurance, but also exploring whether new forms present innovative possibilities.

Finally, it's worth emphasizing that adjusting cost and fee structures to benefit consumers has become an inevitable trend across insurance products.

Both channel tiers and channel fees are being further compressed. Money that previously went to channels is increasingly being redirected into products — either to fund customer services or as part of risk premiums.

For intermediary-type insurtech companies, pure pass-through businesses likely face limited future prospects. They need to excel at customer operations, and even reverse product customization, to serve their user bases well.

Insurance was difficult to sell for an obvious reason: it was essentially "a piece of paper," and we hoped that piece of paper would never actually be used.

So there's a major trend in insurance products: post-underwriting, insurers need to embed more service components like health checkups and chronic disease management. These services improve customer experience while helping insurers manage and control risk, reducing ultimate payouts — which also benefits insurers' own operations.

▍How does the insurtech sector address challenges around traffic, profit models, and supply chains?

Finally, let's discuss the potential challenges FreeS Fund sees in the insurtech space.

One concerns traffic. Traffic costs have risen sharply in recent years. For direct-to-consumer internet insurance startups, the question is how to break through in such an expensive traffic environment with giants occupying key positions. We're seeing some companies experiment with social media and private domain traffic.

Another challenge involves profit models, which connects to the open, integrated model mentioned earlier.

Some insurtech companies may only provide a tool to customers. More advanced ones might offer solutions. The most capable can deliver complete services. This maps directly to business models: whether you can only charge tool usage fees, or whether you can take revenue shares from business performance. The model determines how much value you can actually deliver to customers.

We're also seeing that as more services get bundled into insurance products, insurers need stronger supply chain integration capabilities. For health insurance, can you effectively connect hospitals, pharmaceutical manufacturers, health management services, internet hospitals, and other resources? This integration capability is a critical dimension for evaluating insurtech companies.

One final point, and this is something FreeS Fund considers across financial services generally: financial businesses are inherently tied to risk. When exploring innovative models, never lose sight of the underlying risks, and never cross regulatory red lines.

What opportunities and challenges exist in health insurance? How can startups enter?

▍The gap in medical insurance payment is the underlying logic for commercial insurance development

Dong Weili: From an entrepreneur's perspective, what opportunities and challenges do you see in health insurance?

Zhang Qingfeng: Let's start with the fundamental drivers of health insurance growth.

Overall, the opportunity in health insurance stems from China's large population: once basic medical insurance reaches a certain coverage level, third-party solutions are needed to address medical payment gaps.

At present, China's basic medical insurance may be approaching its payment ceiling. In 2019, China's medical insurance revenue was roughly 2.4 trillion yuan, with payouts around 2 trillion yuan. We've made projections in the past: at China's current GDP level, we can probably sustain medical insurance payouts up to 2.5 trillion yuan.

In healthcare, how do we define whether a country's medical security policy gives its people a sense of well-being? Generally speaking, when out-of-pocket payments by patients to medical institutions account for 10% to 20% of total costs, that's considered one important marker of well-being.

In China, medical insurance payments account for roughly 40% to 50%, with most of the remainder paid directly by patients to hospitals, while commercial insurance covers a relatively small share.

Suppose one day China's total medical payments reach 10 trillion yuan, with medical insurance covering about 2.5 trillion. According to the "well-being line," consumers pay 20% out of pocket—that's 2 trillion yuan.

Subtracting this 4.5 trillion from the total, there's still a gap of 5.5 trillion yuan. This gap is the underlying logic for the development of commercial insurance, city-wide insurance, mutual aid plans, and similar products. New models may emerge within this space to address roughly 3 to 4 trillion yuan of the payment shortfall.

In recent years, health insurance has developed very rapidly, with compound annual growth rates exceeding 30%. In a market approaching trillion-yuan scale, such high growth is bound to attract considerable attention.

However, health insurance has consistently faced the challenge of homogenization throughout its development—a problem that remains unresolved to this day. Homogenization manifests across three dimensions: products, users, and services.

First, product homogenization. One consequence of completely homogeneous products is price wars. Smaller companies, in order to compete with large insurers, have no choice but to offer lower prices—a practice that poses significant long-term risks to the entire industry. In homogeneous competition, the weapon smaller companies can use to break through is innovative products, because large companies hold absolute control over distribution channels.

Second, user homogenization. The population we currently underwrite is still concentrated primarily among healthy individuals. Unhealthy people, the elderly, those in special occupations, and those with insufficient payment capacity are all outside our underwriting scope. Many users' needs are actually quite diverse, but the products we offer are singular and homogeneous, resulting in our only being able to underwrite a homogeneous user base—most users' protection needs go unmet.

Third, service homogenization. Health insurance has two major segments: one is critical illness insurance, which focuses primarily on disease payouts; the other is medical insurance, which is based on medical expense reimbursement. Medical insurance is a very service-heavy product. The insured must engage in medical behavior, creating service needs ranging from physician guidance, referral navigation, to medical assistance and so on. But the services currently offered by the insurance industry for medical insurance are highly homogeneous.

When all three forms of homogenization exist simultaneously, the entire industry enters a scenario of price competition. Yet insurance—health insurance in particular—underwrites the risk of disease onset; this cannot be solved by taking risks.

▍How to Solve the Homogenization Problem?

Dong Weili: I'd like to ask you, how can technology and products be used to solve the homogenization problem?

Zhang Qingfeng: Solving homogenization requires high standards for both technology and data.

Let's start with how to address user homogenization and product homogenization.

Take the elderly as an example. According to data we have, the elderly account for over 60% of medical insurance payouts, while their actual share of the population is relatively low.

Entering old age, most people develop chronic conditions—issues with blood sugar, blood pressure, blood lipids—and these conditions are mostly overlapping. Every elderly person's overall physical condition differs; the risks they face are difficult to homogenize.

At this point, powerful technical capabilities and computing engines are needed to measure each elderly person's risk. This way, some insurance companies can underwrite insurance targeted at the elderly, thereby solving the user homogenization problem. We can even break down elderly people's chronic conditions and have different insurance companies underwrite different aspects.

China will have roughly 400 million elderly people in the future; assuming 200 million of them must be insured, this market is sufficiently massive. In the US market, the elderly occupy the most central portion of health insurance premium income and payouts.

Another example: if someone develops Type 2 diabetes, can they be insured like an ordinary person?

We believe that technically, it is possible to enable Type 2 diabetics to be insured. Based on data and models we have, we've concluded that some Type 2 diabetes patients have lower mortality rates and incidence of core diseases than ordinary people. We don't yet know the causal relationship, but we roughly speculate that after a person develops Type 2 diabetes, in the process of self-management, they prevent the elevation of a series of indicators including blood sugar, blood pressure, and blood lipids, resulting in lower mortality and core disease incidence than ordinary people.

These populations can actually be regarded as high-quality underwriting targets; insurance companies can use products designed for ordinary people to underwrite these patients. Behind this service, technological breakthroughs are needed—separately measuring risk for each individual Type 2 diabetes patient. After individual measurement, each company can leverage its own distinctive strengths and advantages.

We've observed that there are many regional insurance companies in the US, and they operate very well. Because medical insurance is, to a certain degree, highly fragmented—it is very service-heavy and has relatively high requirements for measuring individual risk.

Therefore, using technology to precisely measure risk can serve as a means to solve product homogenization and user population homogenization.

As for service homogenization, using technology to manage chronic conditions will be a very effective breakthrough point.

As hardware technology improves, with consumer authorization, we can collect large amounts of data and track users' daily behavioral habits—all of which can play crucial roles in future product development and chronic disease services.

China has a strong 5G foundation, massive data transmission and processing capabilities, and government willingness to support the productive use of data as a factor of production. These foundational conditions can help the insurance industry solve homogenization problems. The insurance industry may begin solving homogenization problems starting roughly in the next two to three years, but the entire process will take a considerable amount of time.

Aixuan Technology has been seeking breakthroughs in this area in recent years, and has achieved breakthroughs across multiple populations: the elderly, diabetes patients, specific risk populations, regional populations, and so on.

▍The Underlying Moat of Insurance Technology Companies: Capability, Data, Super Algorithms

Zhang Qingfeng: What is the underlying moat of insurance technology companies? I believe it encompasses three aspects: capability, data, and super algorithms.

Capability includes four components. The first is actuarial pricing capability. The second is risk control and underwriting capability. The third is sales capability. The fourth is investment capability. In the insurance industry, especially for life insurance companies, after receiving premiums, there's also the matter of investment—obtaining greater investment returns while ensuring safety. We need to think about how to better solve the investment capability problem when insurance companies may be managing assets in the tens of trillions in the future?

Beyond capability, data is also needed. Taking health insurance as an example, it requires outcome data from three sources.

First, data accumulated from the insurance industry's claims practice. For instance, according to data accumulated by the insurance industry, the average age at death for China's insured population is roughly 79, while for the general population it's 74. Industry-accumulated data and models are most suitable for helping with product pricing.

Second, medical insurance data. Currently, in-hospital data is relatively less helpful for health insurance pricing because it lacks population base data; medical insurance precisely contains population base data, which can serve as a basis for pricing. However, critical illness insurance products generally have premium payment periods of 10 or 20 years, with lifetime coverage as the main form. Critical illness actuarial work requires relatively long-term closed medical insurance data to make predictions for future decades.

Third, physical examination data. Physical examination data has relatively smaller impact on pricing, but is extremely valuable for risk control, underwriting, and building entire risk control systems.

With data in hand, matching super algorithms are still needed.

Whether in investment, sales, risk control, or actuarial pricing, when dealing with massive data, without strong super algorithm capabilities and artificial intelligence capabilities, it's difficult to be defined as a technology company. You're not facing toward the future, only toward today—you won't be able to respond to the major transformation facing the global insurance industry in the future. The next three years are a window period; China may lead the transformation of the insurance industry, particularly health insurance.

▍Compliance Risks to Watch When Using Medical Insurance Data

Dong Weili: For an insurance sector startup, what challenges will it encounter regarding data, and how can it build its own technical moat after obtaining data?

Zhang Qingfeng: Data has very different application value across different domains of the insurance industry. Beyond investment and sales, actuarial work and risk control are also very important components of the insurance industry.

Actuarial work is risk pricing. In actuarial work, we advocate not overusing data, especially personal data, but rather using it through federated modeling and compliant authorization. The essence of actuarial work is probability prediction, so it doesn't need personal element information including personal names, ID numbers, phone numbers, or home addresses. Actuarial pricing is prediction after statistics, so it only needs to perform effective calculations within legal and regulatory constraints, using data from partners, government, and medical insurance.

Regarding underwriting risk control, we need to know specific customers' risk conditions before they apply for insurance. There are many authorization conventions for this worldwide. When we say authorization, we generally mean two-way authorization: one is consumer authorization of insurance institutions, service institutions, and technology institutions; but more importantly, it's consumer authorization of the institutions providing data.

In China, except for government-authorized units such as health departments and hospitals, medical insurance data calls involve considerable policy compliance risks. Patients can authorize their in-hospital medical records and corresponding data, but medical insurance data is settlement data between the state or government and medical insurance centers—it's not entirely the patient's property. Therefore, using medical insurance data carries legal compliance risks. However, some local governments can, through policy, allow data to be used by third parties with consumer authorization.

To summarize, in risk control and technical data usage: first, emphasize compliance; second, emphasize effectiveness. Effectiveness doesn't mean the more factors you have the better, but rather the more factors with high relevance, strong predictiveness, and rich information the better.

Preview

On October 17, 9:00 AM – 12:30 PM, the "Fintech Open Day" will meet you. If you'd still like to get on board, please scan the code to register before 9:00 AM on October 14 (the Fintech Open Day is open to both in-person and online participation).

(Scan the code to register now~)

Contact Us

Fintech has been a direction FreeS Fund has paid close attention to since its founding. We have invested in more than 10 companies in related directions, including consumer finance, supply chain finance, wealth management and asset management, as well as new technologies related to financial big data and insurance technology. Entrepreneurs and industry experts are welcome to connect with us:

Pengqi Liu, Vice President, FreeS Fund

We also look forward to investment-interested friends joining us (contact: hr@freesvc.com).

▲ How to Build the Next "Hundsun"? The Financial Transformation Is Underway

▲ FreeS Report 19 | The Tipsy Era: Where Are the Opportunities for Low-Alcohol Beverage Startups?

▲ Galaxies in Your Eyes: A Visual Guide to the Rise of Colored Contact Lenses | FreeS Research

▲ Navigating Black Swans: Conversations with Six Founders

▲ Entering Our Sixth Year, FreeS Fund Is Hiring Investors | Doing What's Right, Not What's Easy