Four Years On, Revisiting Cross-Border E-Commerce | Frees Fund

Focus on long-term value, and business will endure.

"

Hai Huang, Executive Director, FreeS Fund

Email: hai@freesvc.com

Hai Huang focuses on investments in consumer and retail sectors. He led and participated in investments in Club Factory, Saturnbird Coffee, Vphoto, and other projects. He holds an MS in Management Science and Engineering from Stanford University and a BS in Mathematics from The University of Hong Kong.

"

On October 11, 2019, Club Factory announced a $100 million Series D round led by Qiming Venture Partners and several other domestic and international funds, becoming India's third-largest e-commerce company. FreeS Fund, the lead investor in Club Factory's Series A, made an outsized follow-on investment.

Here, we share our thinking on cross-border e-commerce over the past four years. Compared with four years ago, the entrepreneurial landscape and competitive dynamics of cross-border e-commerce today are markedly different. Based on our continuous follow-up and reflection during this period, we have developed new insights and understanding of this space. We also attempt to answer: standing in 2019, what opportunities remain in cross-border e-commerce?

01

Why did we pay attention to this space four years ago?

From FreeS Fund's founding in 2015, cross-border e-commerce has been one of our key focus areas. At that time, the daigou (overseas purchasing) industry was booming, while "cross-border e-commerce" was not yet a hot topic among investors. Our willingness to place bets stemmed from our thinking at the time.

That year, a major backdrop was the mobile internet era reaching mass adoption. The demographic dividend that had long fueled China's mobile internet growth was gradually dissipating, and concerns about hitting a traffic ceiling were becoming reality.

TalkingData's "2015 Mobile Internet Industry Development Report" noted that "by the end of 2015, device scale reached 1.28 billion, with quarterly growth of 3.2%," and that "growth in active mobile terminals is gradually slowing, with user saturation approaching; quarterly user growth in 2016 is expected to fall below 3%."

New user demographics urgently needed to be discovered, and increasingly more domestic attention began turning overseas. Compared with domestic markets, overseas user acquisition costs were lower then, making "going global" one of the new directions for entrepreneurs. Data from the Ministry of Commerce showed that in 2015, China's non-financial outward direct investment hit a historical high, exceeding $1 trillion for the first time.

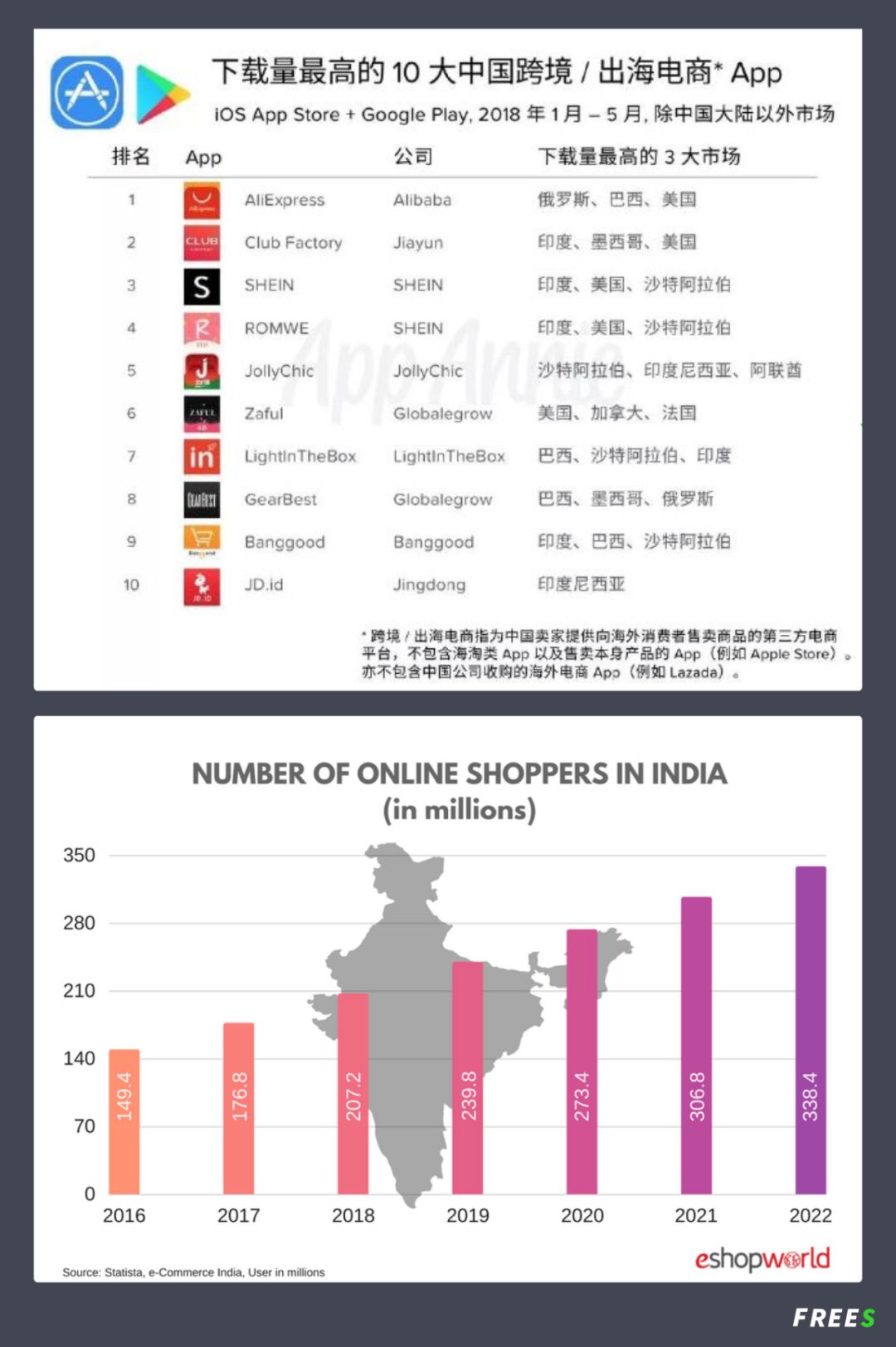

At the time, we found that export e-commerce targeted both mature markets like the US and UK, and emerging markets like India and the Middle East. In emerging markets where e-commerce was still underdeveloped, there remained vast untapped fertile ground in terms of total potential consumers. In key battlegrounds including India, Chinese and American giants were still in a state of chaotic competition.

This objectively meant that market structure remained open, and the competitive ecosystem was relatively friendly to startups, since a few giants had not yet monopolized the market.

Domestically, we were accustomed to startups taking sides to grow. Whether Tencent-aligned or Alibaba-aligned, these binding relationships largely stemmed from relatively closed commercial ecosystems where giants had built powerful traffic moats. There did not exist a data-rich, open system that allowed companies to easily acquire users.

Overseas, the situation was different.

Due to constraints from Western commercial culture and legal systems, Amazon, eBay on one side and Google, Facebook on the other — e-commerce giants and traffic giants — had not formed alliances, nor did they have any investment relationships. The relative independence of e-commerce platforms and traffic platforms gave startups excellent room to grow. With a very high ceiling, this overseas competitive landscape was favorable for Chinese startups.

Meanwhile, Google and Facebook, the two advertising giants, had very mature advertising systems and richly dimensional user data. As long as you had a clear understanding of target users, you could acquire them on Google and Facebook at a certain cost. While acquisition costs varied by country, this was a scalable user acquisition method at the early stage, with stable and controllable ROI.

Beyond this, after entering the mobile internet era in 2010, Chinese companies' overall operational capabilities had developed substantially based on innovation explosions in mobile internet. Overseas markets were not as advanced as China in operational methodology. Many Chinese startups employed flexible tactics, adapting domestic experience to overseas markets.

Based on this industry analysis, FreeS Fund invested in early-stage cross-border projects including Club Factory and PatPat during 2015-2016. If you're interested in FreeS Fund's investment thinking at that time, please refer to our 2015 report "FreeS Research Report No. 1: Opportunities and Future of Export Cross-Border E-commerce."

02

New observations on cross-border e-commerce after four years

In 2015, few investors were paying attention to cross-border e-commerce. By 2019, not only domestic and international giants including Alibaba and Amazon were doubling down on emerging markets, but cross-border e-commerce startups including our portfolio companies were also showing their edge. Based on four years of continuous follow-up and reflection, we have developed new insights and understanding:

▍China's supply chain advantages persist

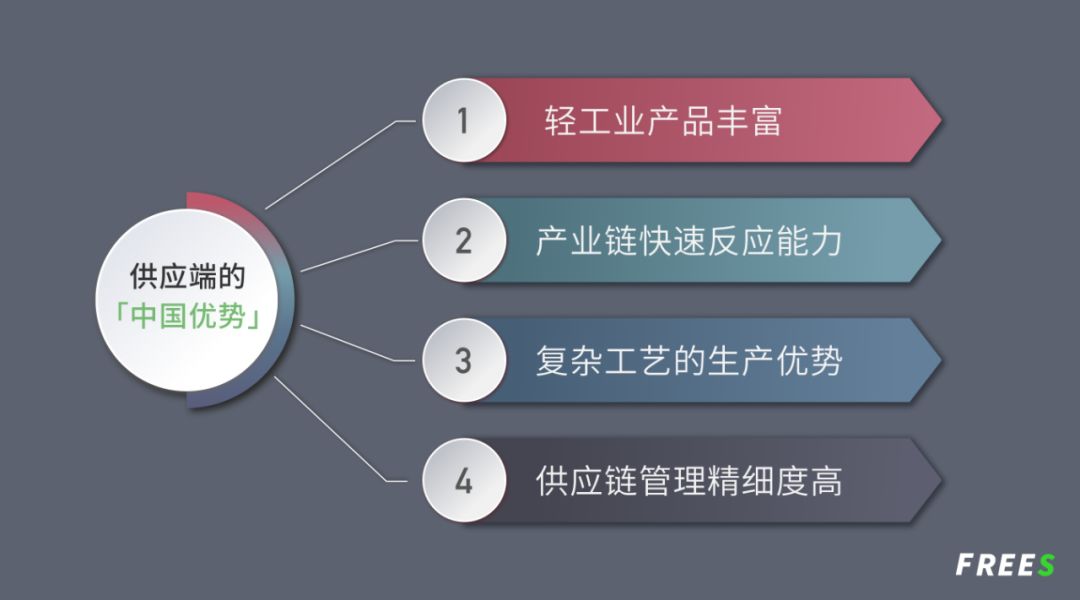

In recent years, pessimistic voices about Chinese manufacturing have frequently emerged based on the US-China trade war and rising labor costs. Based on two core factors analyzed below, we believe that while production relocation does occur, China's systematic advantages in manufacturing remain unshakable (see "Li Feng Column 14: Why We Should Be Grateful for Chinese Manufacturing"). Chinese e-commerce exports to the world remain a long-term trend.

- Supply-side category richness

China's light industrial product variety is the highest globally.

"Made in China" is no longer synonymous with cheap. It means more SKUs and greater variety than foreign alternatives can offer, satisfying diverse overseas consumer needs. This is especially true for non-standard categories like apparel, home goods, shoes and bags, and accessories that naturally require variety.

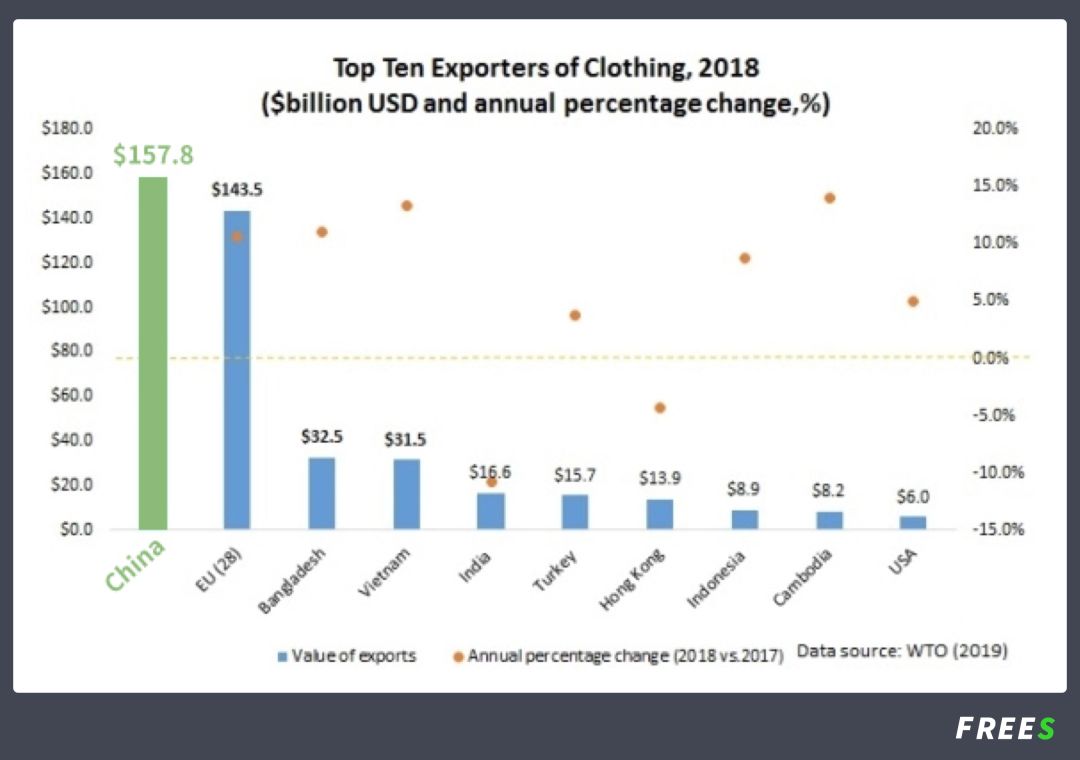

As shown below, in 2017, China's total apparel exports ranked first globally. Aside from being roughly on par with second-place EU (comprising 28 countries), it far exceeded all other countries from third place onward.

Like the foundation of Taobao's prosperous ecosystem — abundant long-tail small merchants, typified by small and medium-sized light industrial enterprises in the Jiangsu-Zhejiang region — they can produce sufficiently diverse products to meet global consumer needs. This foundation is crucial for cross-border e-commerce, especially non-standard categories (apparel, shoes, bags, etc.).

- Some manufacturing process accumulations are hard to replace in the short term

Take the apparel industry: for basic categories like white shirts and T-shirts — tending toward standard products without complex style, fabric, and accessory design — production can indeed be poached by countries with lower labor costs. When processes are easily copied and learned, labor cost becomes the core variable in production, so basic style relocation is indeed a trend.

However, labor cost is often not the most important consideration in production. For some non-standard style items, the richness of the upstream and downstream ecosystem for corresponding styles, fabrics, and accessories is a more critical factor. Moreover, many relatively complex processes cannot be quickly mastered by overseas production line workers. Therefore, when the entire ecosystem has accumulated sufficient time, relocating the complete upstream and downstream supporting facilities and process knowledge becomes very difficult.

▍The essence of cross-border e-commerce: technology improves supply-demand matching efficiency

Four years ago, we mostly understood cross-border e-commerce from the angle of China's unique advantages. Four years later, having seen more consumer retail projects and thought more deeply, we increasingly feel that cross-border e-commerce is simply about meeting overseas consumer demand. Judging whether a cross-border e-commerce project is investment-worthy is essentially the same as judging any retail project. We've also become increasingly clear that whether cross-border e-commerce, domestic e-commerce channels, or consumption upgrade brands, all must fundamentally conform to the common laws of retail.

A retail company's core lies in understanding both supply and demand ends:

- Consumer end: strong insight into what users need;

- Supply chain end: whether you can provide more efficient solutions, offering consumers low-priced goods while guaranteeing quality.

This was actually a weak point for Chinese teams. Because they don't live locally, their understanding of local consumers is limited, so they need even more to use technological capabilities to improve matching efficiency — similar to how the ByteDance team doesn't need artificial preset assumptions about user preferences, but simply learns and understands user preferences automatically from data.

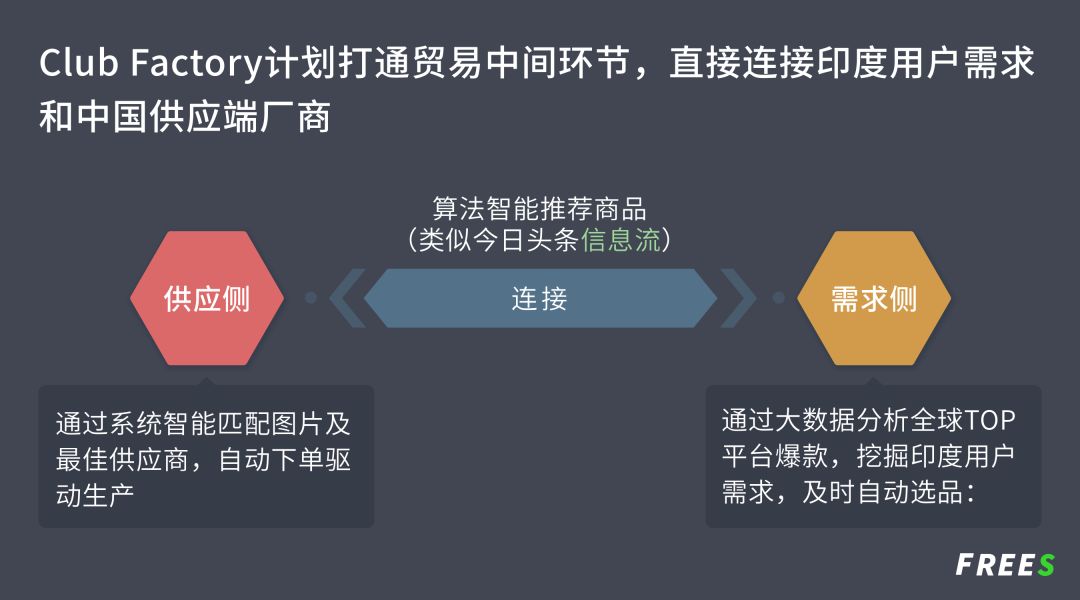

Take Club Factory, a FreeS Fund portfolio company. Its biggest advantage over Indian domestic giants lies in capturing Chinese manufacturing advantages, enabling factory-to-consumer sales to some degree, cutting out lengthy middlemen. And the key to achieving this "direct sales" model was using technology to effectively solve supply-demand matching.

Simply put, through front-end data analysis, Club Factory predicts which items will sell well in India; for each such item, it must be able to find supply resources on the back end. Thus, supply-demand matching is the key to the entire process.

Club Factory achieved this matching entirely through automated machine processes. If relying on human labor, it couldn't have grown into an e-commerce company managing over 10 million SKUs simultaneously. Without technology supporting automatic product matching, identification, and listing, the entire large-scale non-standard product operation business model wouldn't exist. (Regarding "supply-demand relationships" and "deconstructing Club Factory," please refer to Feng Shu's course module on "Model Innovation" in the Chaos University App.)

The particularity of overseas markets: few focus on long-term user value

If we observe this industry from a longer time dimension, we find an interesting phenomenon — this is a market where leaders change every two to three years. What does this mean? Many companies go from prosperity to decline in not very long.

Pioneers in cross-border e-commerce entered as early as the 2000s.

In an era when overseas logistics were not smooth, early cross-border sellers mainly dealt in virtual products like game cards. As logistics developed, more entrepreneurs gradually tried physical cross-border shipping. LightInTheBox was the industry's first US-listed company. But good times didn't last; as user retention rates dropped and customer acquisition costs rose, LightInTheBox's market value declined year by year.

Cross-border e-commerce (Globalegrow) is the industry's only evergreen tree and currently its only A-share listed company, with annual cross-border e-commerce sales exceeding RMB 10 billion.

Worth pondering: this industry exceeds RMB 1 trillion in scale, so it should accommodate enough companies — but why is there only this one listed company on the entire A-share market?

First-generation cross-border e-commerce players mostly gradually declined during development, failing to achieve long-term value. This is also why this industry had few followers years ago — its sustainability was questionable.

This is actually not due to intrinsic industry reasons, but more the limitations of practitioners themselves. A common problem among many cross-border e-commerce companies is crude and simplistic tactics, excessive reliance on paid acquisition for new customers, poor retention of existing users, resulting in short lifecycles.

In recent years, entrepreneurs have gradually recognized these problems and focused more on long-term value. Take Club Factory: in the Indian market, it insists on using the app as its transaction scenario, rather than emphasizing the more easily convertible web端 — inserting single-item ads in Facebook feeds for one-page e-commerce was the money-making formula for many sellers back then. Club Factory broke away from the short-sighted thinking of "only caring about traffic, not retention" that characterized many previous cross-border e-commerce players, and the app is undoubtedly the best environment for operating and retaining users.

Through these cognitive iterations, our confidence in the industry's prospects has further strengthened. Therefore, in Club Factory's 2018 Series C and 2019 Series D rounds, FreeS Fund continued to follow on, even making an outsized follow-on investment in the latest Series D round to further increase our ownership stake.

Standing in 2019, what opportunities remain in cross-border e-commerce?

Will new opportunities continue to emerge?

One obvious fact is that we are no longer in the industry's initial萌芽 stage. Many countries and regions, especially in Asia — India and Southeast Asia, which are relatively close to China and have huge market potential — already have numerous startups and even giants like Alibaba and Amazon deeply rooted and fiercely competing. Giants are investing massive resources, treating India and Southeast Asia as must-win markets, while leading startups have reached the scale of mid-to-late stage PE financing.

In this situation, what differentiated space and细分赛道 do latecomers still have to切入?

We have two suggestions:

First, leverage platform dividends to reduce customer acquisition costs.

Pay attention to social media dividends. Domestically, a batch of fast-moving consumer goods brands in the cosmetics industry have rapidly risen in the past year by deeply exploiting content dividends on platforms like Douyin — I analyzed this in my previous article "Startup Brand Breakthrough: From Traffic Thinking to Content Thinking."

The overseas logic is similar. In Part 1 of this article, I also mentioned Facebook and YouTube, as well as newer generation platforms Snapchat and Instagram, are open platforms with fewer constraints — for example, if Douyin content contains prompts guiding users to follow WeChat, the likelihood of being banned is high, but no similar problems exist overseas.

One specific case: as Snapchat's penetration in the Middle East market continues to increase, and Snapchat has not yet systematically monetized there, some e-commerce startups have exploited this customer acquisition洼地, achieving rapid customer acquisition and growth in the Middle East starting from 2018.

Second, focus on categories, forming repurchase through quality and service advantages.

Have very good judgment about categories; you can focus on and deeply dig into a category you excel at and are familiar with. The cross-border e-commerce market is vast. Focusing on a single category suitable for export (supported by logistics with Chinese production advantages) to form quality and service advantages can also achieve considerable profitability, such as wedding dresses, wigs, and auto parts that are lightweight and not easily damaged in shipping. For example, PatPat, another cross-border e-commerce company in FreeS Fund's portfolio, focuses on children's clothing in European and American markets and has also achieved rapid development in recent years.

Summary

1. Cross-border e-commerce, at its core, is about meeting overseas consumer demand and must fundamentally conform to the common laws of retail — namely, control of supply-demand relationships.

2. The methodology for entering cross-border e-commerce lies in making correct choices regarding market, business model, and building core moats.

3. Focus on long-term value for business to endure.

(Welcome to read, share, and like. For republication on other official accounts, websites, or mobile apps, please reply "republication" to learn republication rules and contact "Feng Xiaorui" (id: freesfund) for authorization. Copyright belongs to FreeS Fund.)

▲ FreeS Research Report (I): Opportunities and Future of Export Cross-Border E-commerce

▲ Li Feng Column 14: Why Should We Be Grateful for Chinese Manufacturing?

▲ Startup Brand Breakthrough: From Traffic Thinking to Content Thinking