FreeS Report 14: Cosmetics Keep Getting Pricier, But Is Your Face Really Worth a Million? | Frees Fund

Optimistic about startups carving out a slice of the mass-market cosmetics pie.

In FreeS Report Issue 14, we're talking about the beauty business.

Humans have been chasing beauty for over a million years. Looking pleasant never hurts, but is your face really worth a million?

A 50ml bottle of Estée Lauder Advanced Night Repair sells for 850 RMB. A 30ml bottle of Pechoin Sancha Flower Youth Revitalizing Essence goes for 179 RMB. Both主打 hydration and skin activation. Both are born from the same Intercos Suzhou factory.

The luxury brand cosmetics you pay dearly for and the affordable domestic alternatives may not differ all that much in raw materials and formulations. So why such a gap in retail price? From mountains of raw materials piled in bags at the factory to the gram-measured, multi-functional products in our hands, cosmetics pass through production, brand, agency, and channel — how does each layer add its markup? Before you spend big to make yourself more beautiful this year, you might want to read this.

Here's what we'll cover:

- The Past and Present of Cosmetics 1.1 Global market analysis 1.2 The evolution of cosmetics industries in Europe, America, China, Japan, and Korea 1.3 How are international brands made?

- Secrets of Production 2.1 What's really going on inside contract manufacturers? 2.2 Why do startup cosmetics companies have supply chain opportunities in China?

- Changes in Distribution 3.1 How have cosmetics purchasing channels evolved? 3.2 American millennials and Gen Z: the网购-loving消费主力军 3.3 The selling power of social media

- Summary: Bullish on startups carving out share in the mass cosmetics market

Share your thoughts in the comments below. If you're interested in the beauty market, feel free to reach out to our investment colleague Qianhui Sun at qianhui@freesvc.com

Cosmetics Industry Research

By Qianhui Sun (qianhui@freesvc.com)

01 The Past and Present of Cosmetics

Cosmetics need no introduction. They're the magical species that transform you instantly — from hair oil to body lotion, from facial care to oral cleaning, from makeup to fragrance. They make you cleaner, prettier, more confident.

In fact, humans have been tirelessly pursuing beauty for over a million years.

In distant primitive societies, some Egyptians and Arabs revealed their love of beauty early on. During tribal rituals, they would apply animal fats to their skin to make it appear lustrous.

In China, cave murals from the Neolithic period also record traces of cosmetics.

After the Renaissance, the sprouting of the modern cosmetics industry owed much to a 17th-century ruler of France's Bourbon dynasty — Louis XIV.

▲ Louis XIV's high heels.

This Louis-Dieudonné de Bourbon was a veritable fashion king. The first pair of high heels to hit the ground with a clatter — one popular version traces them to Louis XIV. He was short in stature and had his cobbler add thick heels to appear tall and imposing. After an illness caused his hair to fall out, he was forced to wear wigs — and wigs became fashionable. Not fond of bathing, he favored perfume instead, fueling the rise of France's perfume industry.

1.1 Global Market Analysis

Today, the cosmetics industry commands massive scale. In 2016, the global cosmetics market totaled nearly $220 billion — roughly equivalent to Alibaba's market cap at the time. Asia-Pacific, Western Europe, and North America ranked as the top three markets. Euromonitor predicts that by 2021, the US will become the largest cosmetics market, followed by China and Japan.

Cultural influences create fascinating differences in category structure across countries. Though skincare dominates in all major markets (UK, Germany, US, Japan, and China), its share in Western countries is less than half that in Asian countries. Asian consumers have a particular fondness for whitening products, while fragrance is the darling of the Western world. Perfume accounts for 20% of cosmetics sales in Western countries but less than 2% in Asian markets.

1.2 The Evolution of Cosmetics Industries in Europe, America, China, Japan, and Korea

The development paths of Western and Asian cosmetics industries diverge dramatically.

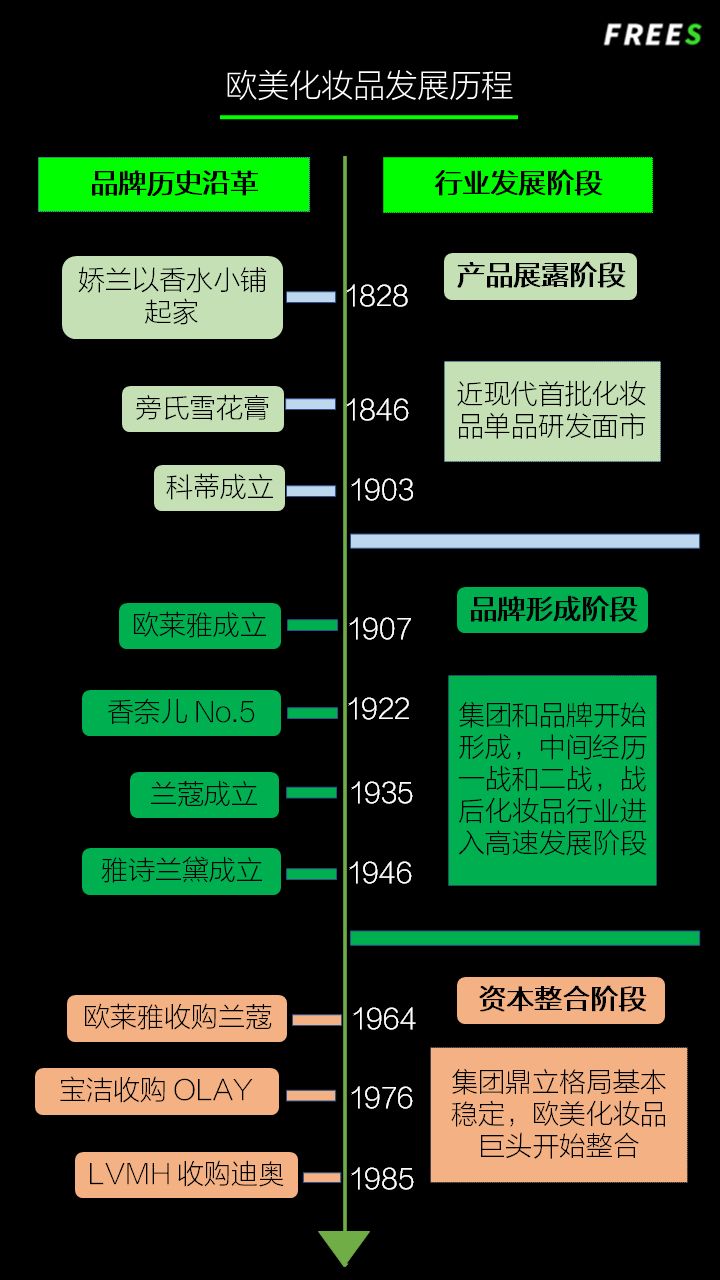

The Western cosmetics industry evolved through three stages: local single-product incubation → brand creation → group mergers and acquisitions. In Europe, fueled by Louis XIV's influence, the cosmetics market flourished amid the fragrance of French perfume.

Spared from wartime destruction, the US cosmetics market developed rapidly during World War I and World War II, emerging as a rising star that rivaled Europe in scale.

Today, Western cosmetics is mapped around giants like L'Oréal, Estée Lauder, Procter & Gamble, and LVMH, which dominate the vast majority of the premium cosmetics market.

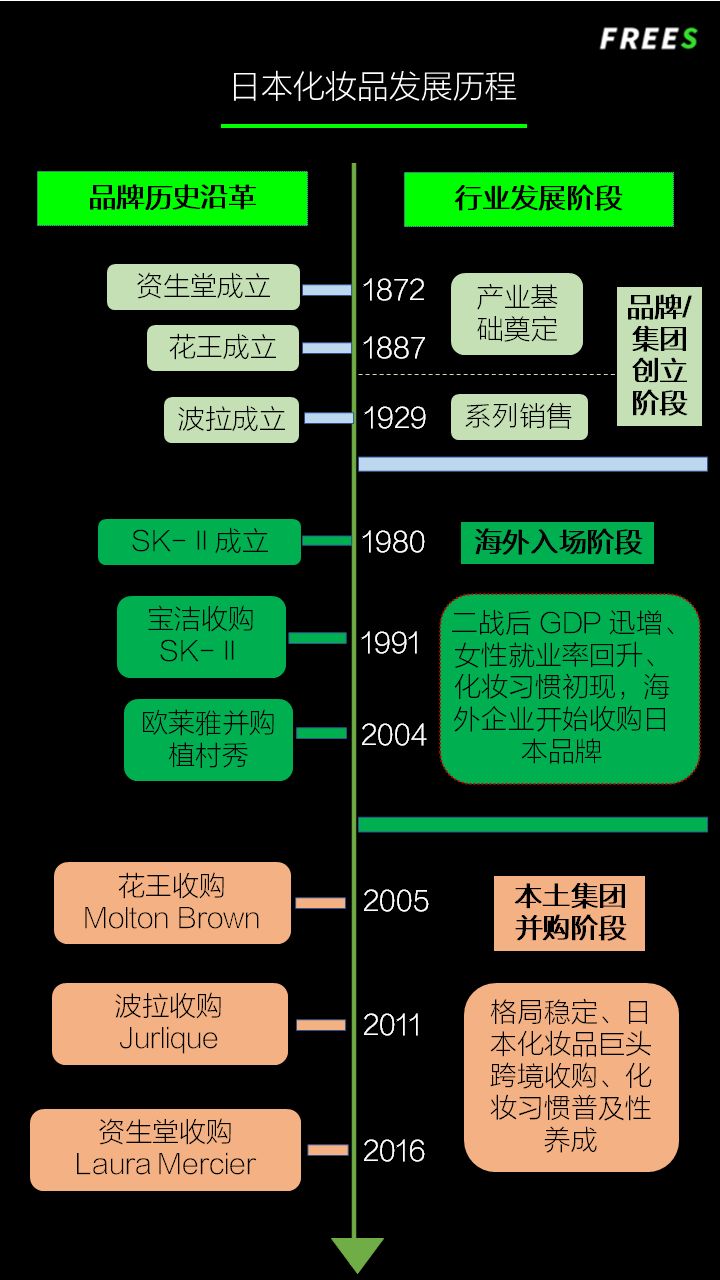

Japan's cosmetics market tells an inspiring story of local brand creation → acquisition by Western brands → resurgence of local brands & group mergers and acquisitions.

Shiseido, Kao, and Lion were founded as early as the late 19th century, but it wasn't until the 1950s, after World War II, that Japanese cosmetics brands began their rapid growth, eventually forming the three major cosmetics groups: Kao, Shiseido, and Pola.

Although overseas companies continued to swallow Japanese brands over the following half-century, local brands have accumulated sufficient strength in the past decade and begun to strike back. From 2010 to 2016, Shiseido successively acquired American natural makeup brand Bare Escentuals, premium makeup brand Laura Mercier, and premium skincare brand ReVive; Pola acquired American skincare brands H2O+ and Jurlique; Kao acquired British luxury bath brand Molton Brown.

China's cosmetics market has ancient roots. As early as the Shang and Zhou dynasties, cosmetics were widely used in the imperial court, accumulating rich beauty formulations. Later, they spread among the common people. The Southern Dynasties folk ballad Mulan contains the line "facing the mirror,粘贴花黄" (applying decorative yellow patches before the mirror).

China's modern cosmetics industry began in the early 20th century, passing through four stages: "small workshop initial production → influx of overseas brands → development of local brands → industry consolidation." We'll find opportunities to deeply analyze the Chinese cosmetics market later.

1.3 How Are International Brands Made?

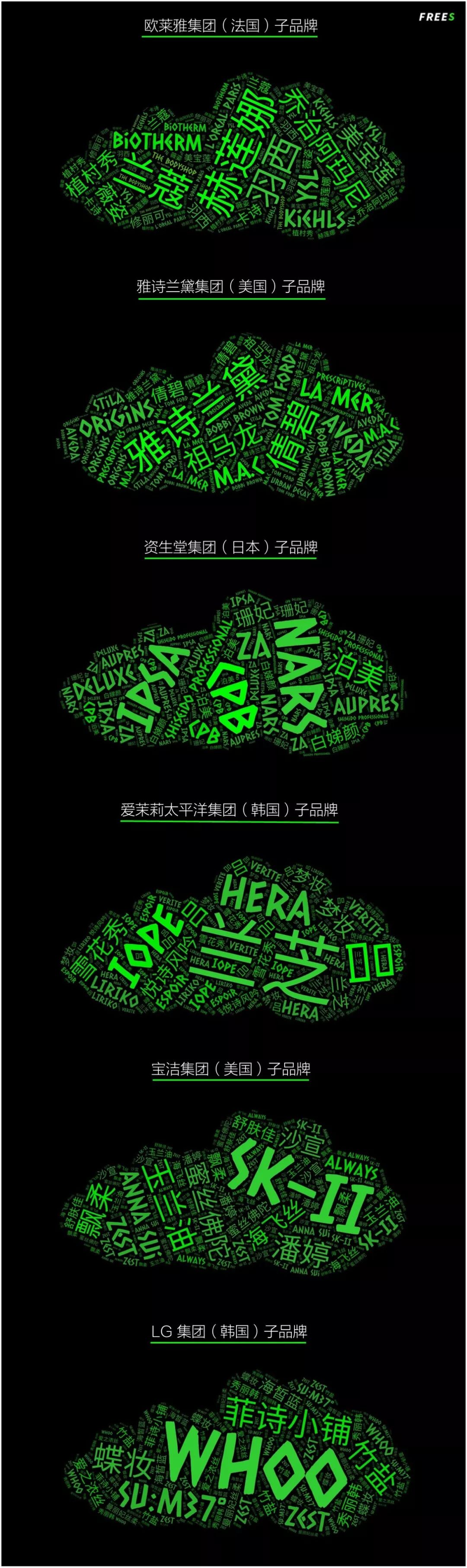

Today, the cosmetics industry has developed into a globalized industry dominated by group operations and brand-driven strategies. Major cosmetics groups have established their dominance: France's L'Oréal, America's Estée Lauder, Japan's Shiseido, Korea's Amorepacific, and others.

The premium cosmetics market is highly concentrated and primarily direct-operated. The premium cosmetics of L'Oréal, Estée Lauder, LVMH, and Chanel together account for roughly 70% of global sales. By contrast, mass cosmetics is relatively less concentrated, with strong local brands in every country.

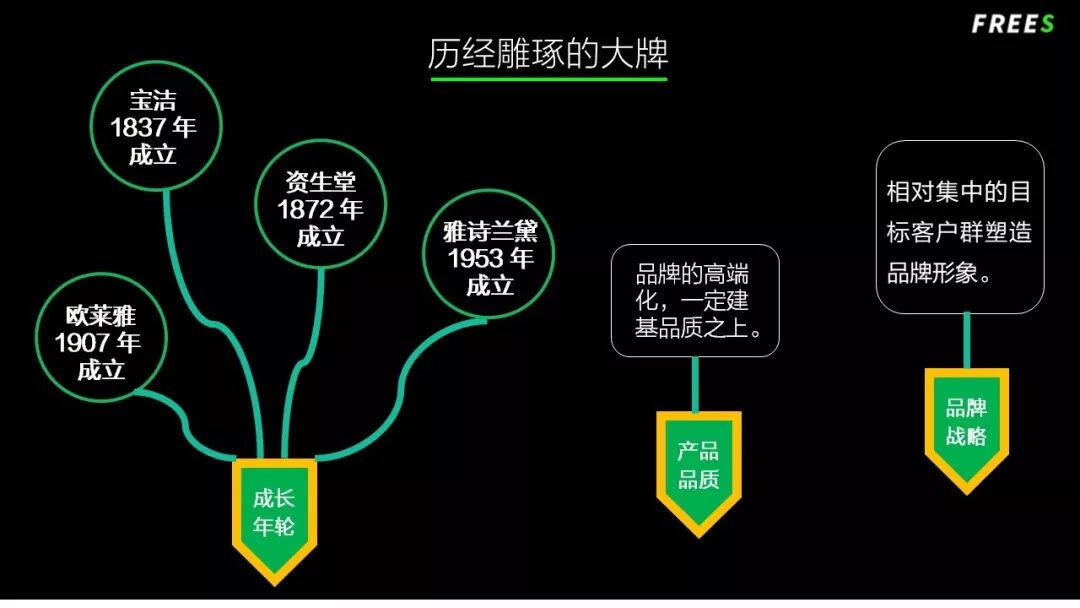

A close look at the growth history of cosmetics giants reveals that cultivating a major brand always takes time. Procter & Gamble, Shiseido, L'Oréal, and Estée Lauder were founded in 1837, 1872, 1907, and 1953 respectively.

Product quality is a necessary condition for brand premiumization. Major groups have maintained relentless investment in product R&D, design, and monitoring to sustain high quality. In 2015, Procter & Gamble, L'Oréal, Shiseido, and Estée Lauder invested 12.89 billion, 5.85 billion, 1.3 billion, and 700 million RMB respectively in R&D.

In terms of brand strategy, relatively concentrated target customer segments have helped major groups shape and maintain their brand image.

External incubation and capital operations such as acquisitions and mergers have further turbocharged group operations. According to incomplete statistics, over 200 M&A deals have occurred in the cosmetics industry from 2012 to the present.

To expand their product lines and meet consumers' growing demand for personalization, beauty giants have been sniffing out niche, creative companies that attract emerging consumer groups. L'Oréal's acquisition of Carol's Daughter, an American organic makeup brand for people of color; Revlon's purchase of nail care brand Mirage Cosmetics; and Estée Lauder's buyout of Rodin olio lusso, a top-tier American skincare brand — all served this purpose.

Meanwhile, advances in biotechnology have driven major groups to swallow up tech companies with core equipment and proprietary technology. Examples include American cosmeceutical brand SkinMedica's acquisition of mineral makeup brand Colorescience; Canadian pharmaceutical giant Valeant's purchase of medical aesthetics device maker Solta Medical; and Estée Lauder's merger with GlamGlow, a British premium skincare brand that holds patents for advanced facial masks.

Beyond that, channel integration has been a major catalyst for M&A. By acquiring e-commerce brands, traditional retailers can gain deeper insight into consumer pain points, desires, and delights. American retail giant Target's acquisition of online beauty retailer DermStore and Macy's purchase of specialty beauty retailer Blue Mercury were both aimed at injecting fresh channels into the traditional department store environment.

Market expansion is another key reason large groups aggressively pursue territory. For foreign cosmetics groups, acquiring local brands in other countries breaks down import barriers and efficiently captures local distribution channels. For example, L'Oréal acquired MG (美即) and Interconsumer Products to break into the Chinese and Kenyan markets respectively; Japanese beauty brand Kose purchased makeup brand Tarte to expand into the American premium color cosmetics market; and organic beauty producer Hain Celestial acquired personal care manufacturer Belvedere to expand into the Canadian market.

In the coming years, capital consolidation will remain one of the defining themes of the cosmetics industry.

FreeS Fund Perspective (freesvc)

- The premium market is solid, making it difficult for premium-focused cosmetics startups to rise. Developing high-end cosmetics requires substantial R&D investment, and established luxury brands have built up user loyalty through years of cultivation.

- Capital consolidation will remain a major theme in the cosmetics industry over the next few years. High fragmentation drives frequent M&A activity. Giant cosmetics groups expand product lines, integrate channels, and open new markets through acquisitions. The rise of younger consumers and the trend toward personalized consumption have made niche brands more valuable.

/ 02 /

Deconstructing the Cosmetics Supply Chain: Secrets of the Production End

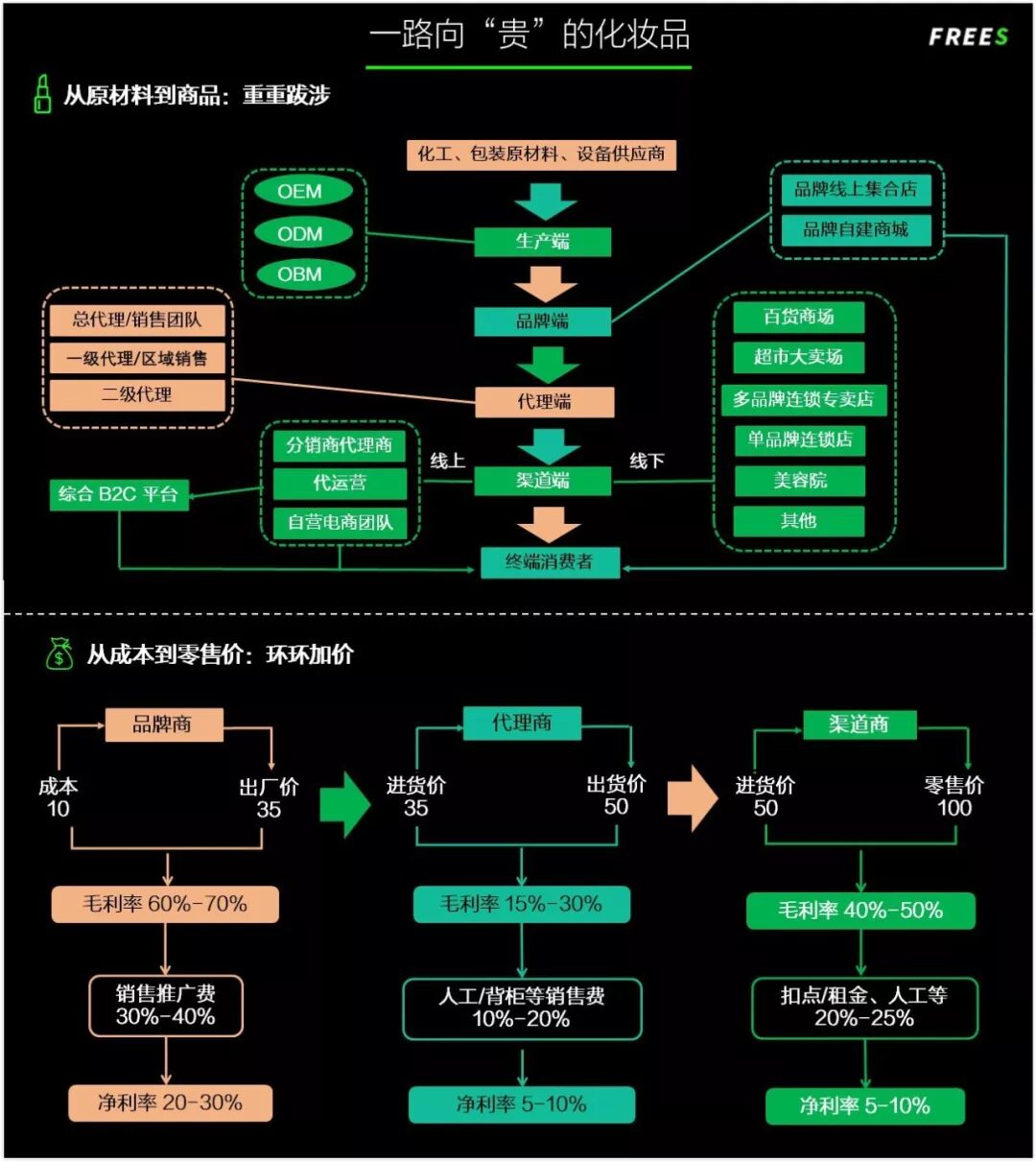

The cosmetics industry supply chain is mainly divided into production, brand, agency, and channel segments.

Brand-side concentration is relatively high, with international and domestic brands dominating the premium and mass markets respectively. The agency segment, as the middle hub of the supply chain, has been flattening amid industry competition driven by brand diversification and the rise of e-commerce.

The division of labor in the cosmetics supply chain has given rise to two typical enterprise types: "R&D-oriented" and "channel-oriented."

Next, let's look at the R&D and production links of "R&D-oriented" enterprises.

/ 2.1 /

What's Really Going On in Contract Manufacturing?

Most products and brands use contract manufacturing (i.e., OEM/ODM) models. Only a handful of cosmetics giants — such as Procter & Gamble, L'Oréal, Estée Lauder, and Shiseido — build their own factories and handle production in-house. They maintain skincare, color cosmetics, and personal care product lines, while simultaneously pursuing brand differentiation strategies to create multi-dimensional, tiered portfolios.

There are two common types of contract manufacturers. One is the Original Equipment Manufacturer (OEM), which inherits the product formulation developed by the client, procures raw materials according to the brand's specifications, produces samples, and — once samples pass inspection — takes on bulk production orders.

The other is the Original Design Manufacturer (ODM), which independently conducts formulation R&D and trial production based on the client's brand positioning and product planning. In this model, the contract manufacturer's R&D capability is the core competitive advantage, while the brand mainly plays a white-label role.

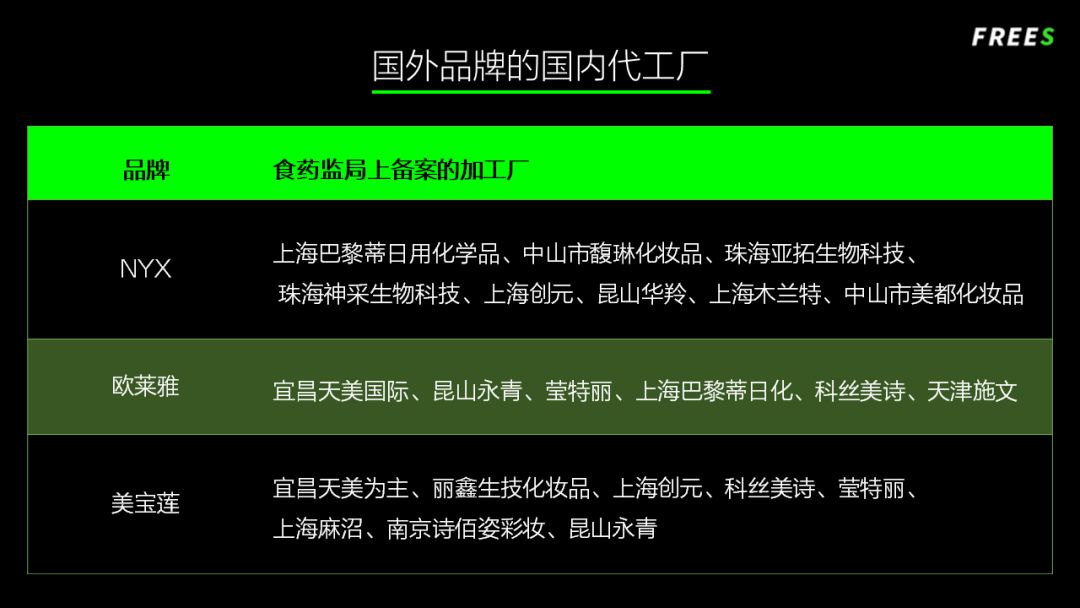

One interesting but unsurprising fact: those Western drugstore color cosmetics we happily buy — products from brands like L'Oréal, Revlon, NYX — are quite possibly 100% made in China.

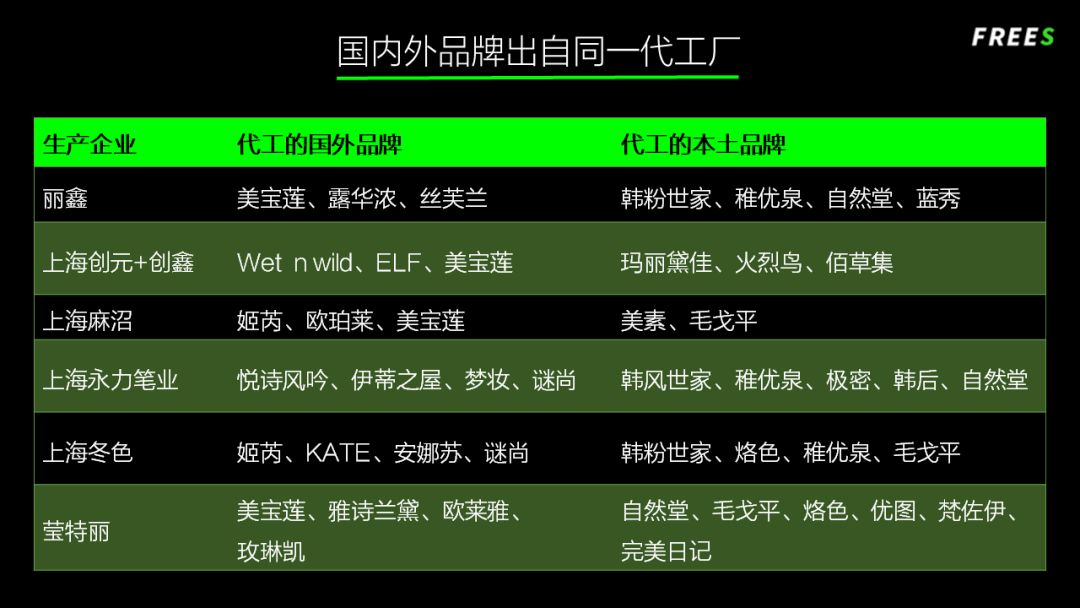

Meanwhile, some products from foreign brands like Maybelline, Anna Sui, and Estée Lauder, as well as familiar domestic brands like Chando, Herborist, and Maysu, may come from the exact same contract manufacturer.

Among numerous contract manufacturers, Italy's Intercos, South Korea's COSMAX and Kolmar, and China's Nox Bellcow have emerged as leading international cosmetics R&D and production enterprises. In 2016, their revenues were €450 million (RMB 326 million), KRW 756.96 billion (RMB 436 million), KRW 667.47 billion (RMB 385 million), and RMB 1.21 billion respectively.

Next, we'll use Intercos and COSMAX as examples to analyze what makes these top contract manufacturers exceptional, where they fall short, and what opportunities this creates for small and mid-sized cosmetics production enterprises.

/ 2.2 /

Why Is the Supply Chain Opportunity for Startup Cosmetics Companies in China?

Intercos is Europe's largest cosmetics producer, with 40% of the world's well-known cosmetics brands as its clients. It places heavy emphasis on creativity and R&D — nearly 20% of its staff work in creative roles, and half of that team specializes in R&D.

It also maintains its own formulation and product portfolios: 527 color cosmetics and 690 skincare products (2015 data).

Its subsidiary CRB, focused on skincare R&D and contract manufacturing, is a royal-appointed factory for European aristocracy, frequently called upon by luxury brands like La Prairie and La Mer.

COSMAX is a South Korean publicly listed company integrating research, development, and production, with its own color research institute and fragrance research institute.

Its production raw materials are centrally procured within the group, and its factories scattered worldwide share formulations and equipment to ensure product quality consistency.

However, its weakness is long production cycles. Completing the full process — raw material transport, sampling, packaging confirmation, design, trial use, and market launch — typically takes 4-6 months. Its rationale for building factories abroad is primarily to adapt to local markets, shorten response times, and react quickly.

Beyond long production cycles, these large top-tier contract manufacturers generally suffer from high production costs, low communication efficiency due to too many clients, and difficulty meeting diverse consumer demands through large-batch production.

Yet cosmetics' paying customers are increasingly young people who prioritize value-for-money and personalization.

Moreover, new-generation cosmetics — especially color cosmetics — have pronounced product timeliness. A hit lipstick shade may lose its heat within months, requiring brands to choose flexible supply chains that can rapidly respond to market changes based on user feedback.

All of the above creates opportunities for China's small and mid-sized cosmetics production enterprises.

China has over 5,000 cosmetics production enterprises, with small and mid-sized companies accounting for 90% of the total. Though numerous and mixed in quality, years of collaboration with internationally renowned brands have produced a large crop of Chinese contract manufacturers with mature technology, stable quality, and strict quality control.

Currently, among the 21 cosmetics manufacturing companies listed on the NEEQ (New Third Board), at least 5 specialize in OEM/ODM business. For example, Nox Bellcow (835320) in Zhongshan, Guangdong is a professional cosmetics production enterprise focused on mask, skincare, wet wipe, and non-woven fabric OEM/ODM processing, capable of producing over 5 million facial masks and 500,000+ cream products daily, with revenue exceeding RMB 1 billion for three consecutive years.

▲ In contract manufacturing facilities, raw materials in large bags.

Compared to top-tier contract manufacturers, they have lower labor costs, more responsive communication and coordination, greater ability to provide personalized products and services, and can quickly adjust product plans based on client feedback to adapt to market demands.

FreeS Fund Perspective (freesvc)

- Another reason the premium cosmetics market is solid and difficult for premium-focused startups to crack: large OEM/ODM companies possess significant R&D advantages and strong control over the premium market, making it hard for small contract manufacturers to compete.

- Startup mass-market cosmetics brands' future supply chain opportunity lies in China. Chinese cosmetics OEM/ODM enterprises have strong upgrade willingness, low market concentration, and significant long-tail effects. Years of collaboration with internationally renowned brands have produced a large crop of contract manufacturers with mature technology, stable quality, and strict quality control — offering good quality at low prices that align with the value-for-money consumption trend, with flexible supply chains characterized by short production cycles and fast refresh rates.

/ 03 /

Changes on the Channel End

Retail channels for cosmetics globally are trending toward diversification.

Offline, department store counters have held the top spot among sales channels since color cosmetics first entered the market. Though their revenue share has declined in recent years amid a broader retail downturn, counters will maintain their core position in color cosmetics (especially premium color cosmetics) and mid-to-high-end skincare retail, thanks to their indispensable roles in experiential and customized services, brand building, and product display.

Supermarkets and hypermarkets are also major retail channels, though they primarily sell personal care products and mass-market skincare items.

CS stores (customer service stores) offering a multi-brand, one-stop shopping experience — such as Sephora and chain drugstores — have grown rapidly in number, mainly selling open-shelf cosmetics.

Single-brand specialty stores are the rising stars of offline channels. The format originated with The Body Shop in the UK; comparable overseas models include Kiehl's in the US, L'Occitane in France, and Etude House in South Korea.

In recent years, as global offline cosmetics retail sales have declined overall, e-commerce channels including B2C and C2C — built on the foundation of e-commerce — have surged in momentum, making online channels a battleground no brand can ignore.

/ 3.1 /

Have Cosmetics Purchasing Channels Changed Over the Years?

Next, let's turn our attention to the United States, the world's largest cosmetics market.

In recent years, traditional offline retail channels have struggled under the weight of consumer migration online, making store closures a dominant theme in American retail.

According to statistics, total US retail store closures reached 6,985 in 2017, up 229% from 2016. A recent example: Italian color cosmetics brand Kiko Milano filed for bankruptcy protection with a US court in January 2018, closing most of its American stores.

Half of these closures were due to brands going bankrupt or shutting down entirely; the other half came from retailers undertaking large-scale store portfolio restructuring to adapt to new consumption habits.

Amid the general malaise of offline retail, those retailers with strong financials, flexible sales channels and locations, and a willingness to experiment with new retail concepts became the ones breaking through. Of the roughly 3,400 new retail stores opened in the US in 2017, the fastest-growing formats were "dollar stores" Dollar General Corp. (NYSE: DG) and Dollar Tree Inc. (NASDAQ: DLTR).

The rise of e-commerce channels in the US is also undeniable. According to CPC Strategy, 96% of Americans have shopped online, 80% have made an online purchase in the past month, and 35% of millennials say they can't live without Amazon — giving some sense of Americans' obsession with e-commerce.

/ 3.2 /

Millennials and Gen Z: The Consumer Main Force That Champions Online Shopping

America is a consumption-driven economy. Influenced by consumption attitudes, residents tend not to save money, with the savings rate remaining in the single digits for the long term. Consumption has steadily contributed 60%-70% of GDP, providing a clear boost to the economy.

At the same time, economic development gives individuals more money to spend. American consumer spending largely tracks the economic cycle — during prosperous times, per capita GDP, disposable income, and consumer demand all rise steadily. In 2016, US per capita GDP reached $57,420, roughly 6-7 times China's per capita GDP, which had only reached the level of US per capita GDP from the late 1970s.

Stable population growth is also an important factor supporting the US consumer industry. The US is one of the very few developed countries where population continues to grow steadily; from 1920 to 2010, the US population tripled. With this increase, mass consumer goods and real estate have both benefited.

More importantly, a youthful population structure injects greater growth elasticity into consumption. The US demographic structure is relatively stable, with the 15-64 age group consistently comprising 60%-70% of the total population. Young people have stronger consumption impulses and purchasing power, bringing vitality to the development of the US consumer industry.

Among this cohort of shopping enthusiasts, millennials have drawn particular attention. Since the late 1990s, millennials have risen to become the primary consumer group.

They value cost-effectiveness and have stronger rational consumption awareness. Influenced by the普及 of the internet and smart devices, their shopping channels have diversified, with online shopping becoming the wave of the era. According to Deloitte, millennials (born 1980-2000) and Gen Z (born after 2000) generally allocate about 60% of their total budgets to online consumption.

Moreover, the explosion of digital media — born alongside the internet — has also profoundly influenced young people's consumer behavior.

According to a US mobile user behavior report, from 2013 to 2015, overall time spent on digital media in the US grew by 49%. Among users aged 18-24, daily time spent on mobile apps exceeded three hours, with the most commonly used apps including YouTube, Facebook, Facebook Messenger, Instagram, and Snapchat.

So what impact has the rise of social media had on the cosmetics industry?

/ 3.3 /

The Selling Power of American Social Media

Looking at the global history of cosmetics marketing, the industry tends to be swept up in a hurricane whenever media undergoes transformation and renewal.

For example, in post-WWII America, media innovation centered on television contributed enormously to the cosmetics industry's development. Especially after the introduction of color television in the mid-1950s, the explosion of Hollywood films became a major driving force for the entire American cosmetics industry (particularly color cosmetics).

In Japan, Shiseido was the first to learn from the West, securing the sole sponsorship of a high-rated TV music program targeting young women in 1958. Around the same time, POLA began investing heavily in television advertising. From 1950 to 1966, the Japanese cosmetics market grew from $25 million to $317 million, a compound annual growth rate of 17% over sixteen years.

In South Korea, from the early 2000s, the Korean Wave centered on K-dramas swept across Asia and globally, with hit dramas repeatedly propelling on-screen cosmetics to peak popularity — such as "Missing You" lip colors, "My Love from the Star" lip shades, and "Gong Hyo-jin" eyebrow pencils. After the 2014 broadcast of My Love from the Star, the same cosmetics featured in the drama sold out on major e-commerce platforms; most of these products came from brands under South Korea's Amorepacific Group, including IOPE, Laneige, and Hanyul. That same year, Amorepacific's revenue reached $3.681 billion, up 29.89% year-over-year.

These cases are no coincidence. In the mobile internet era, the cumulative effect of mobile-ization and new media's rise has accelerated information dissemination, making entertainment marketing an important factor in driving rapid cosmetics brand development.

Data shows that social media has enormous influence on American consumers' cosmetics purchase decisions. A 2016 Facebook report found that 53% of beauty product purchase decisions were influenced by beauty experts' social media shares, while 44% were influenced by brands' own social media presence.

Major American social media platforms affect the beauty industry in different ways.

For instance, YouTube is an incubator for beauty KOLs. Blogger Michelle Phan's natural makeup tutorial uploaded in 2007 racked up 40,000 views in just one week. Currently, the ratio of beauty bloggers to beauty brands on YouTube is approximately 14:1.

According to NPD Group, 92% of beauty consumers in Europe and America draw inspiration from demonstration videos by opinion leaders on YouTube. Among the seven most popular video categories on YouTube, aside from gaming and comedy videos, review videos, tutorials, vlogs, ranking videos, and unboxing videos all pave the way for spreading beauty information.

Compared to YouTube, Instagram functions as a new digital marketplace. Instagram can generate demand and create blockbuster products. Compared to celebrities in TV commercials, an ordinary person on Instagram who seems similar to you recommending a product feels more authentic and reliable — you're more inclined to believe that, like these ordinary people, you'll become equally charming after using the product.

Unlike the overt product sharing and recommendations on YouTube and Instagram, selfie platform Selfie provides a new channel for product reviews. In the looks economy era, selfies have become an indispensable part of life. Products that give people a "filtered" feeling in front of the camera — such as contour creams and concealers — have seen sales surge. Products for creating facial shadows and contours have also begun trending.

Given social media's massive influence, leveraging it to build cosmetics brands has become a natural next step.

Monetizing traffic has become a common tactic for beauty KOLs launching new color cosmetics brands. Emily Weiss, former styling assistant at Vogue magazine, started her personal blog Into the Gloss in 2010, sharing beauty tips and product reviews. A year later, the blog had reached 10 million monthly active users. The most popular feature was "The Top Shelf," where Weiss interviewed well-known designers, models, artists, and fashion editors. In October 2014, Weiss launched her own color cosmetics brand Glossier, rolling out a full product line driven by hit products, with prices ranging from $10 to $40.

When it came to brand building, Glossier used Instagram as both a marketing platform and a testing ground, leveraging its community to gather user needs and feedback for developing new products — a strategy that yielded strong user retention. At the same time, Glossier adopted an agent system where every customer could become a KOL, which significantly encouraged word-of-mouth marketing and drove 70% of online sales.

In 2015, Kylie Jenner of the Kardashian family took a similar approach, launching her personal brand Kylie Cosmetics. The manufacturer behind Kylie Jenner, Seed Beauty, also handled production for Colourpop Cosmetics. Colourpop boasted a rich, professional production line with fast turnover, high output, and low inventory, and was known for skillfully using social media to sell makeup. The brand regularly invited the most prominent beauty bloggers on YouTube and Instagram to promote Colourpop products, amplifying its influence on social networks and accumulating 5.6 million Instagram followers.

Beyond new brand launches, some established makeup brands also doubled down on social media to find new growth engines. Take NYX, an American professional makeup brand founded in 1999, which emphasized simultaneous online and offline operations. While maintaining a premium product line in select department stores and an affordable line in beauty specialty retailers (CVS Pharmacy, Target, Ulta, etc.), NYX also used social media platforms like Instagram and YouTube to launch new products and build awareness with the help of multiple beauty bloggers and makeup artists. P.S., many NYX products are "Made in China."

A similar case is e.l.f., founded in New York in 2004 by American father-son duo Alan Shamah and Joey Shamah. The brand primarily targeted millennials seeking value, with most products priced below $6. Its sales channels included 19,000 retail stores across the U.S. (Walmart, Target, CVS Health, etc.) and major e-commerce platforms.

These cases make it clear that booming makeup sales are a global phenomenon, social media is the new driving force with rising penetration, and makeup is propelled by quality, occasion, and trend dynamics — making it well-suited for multi-channel sales.

FreeS Fund Perspective (freesvc)

- Offline consumption remains robust, even as spending shifts online, with diversified omni-channel presence.

- Content platforms and social media like YouTube, Facebook, and Instagram have captured Americans' — especially young Americans' — time, making digital marketing a powerful tool for cosmetics marketing in the U.S.

- Amid a revival of rational consumption consciousness, millennial consumers place greater emphasis on value for money.

- When shopping, millennial consumers habitually reference KOL recommendations, making social interaction-driven traffic a new customer acquisition channel for emerging brands. This means brands need to communicate fully with consumers and adjust product strategy based on demand.

/ 04 /

Conclusion: Optimistic About Startups Carving Out Share in the Mass Cosmetics Market

Cosmetics is a mature market. The high-end segment is firmly entrenched, with major cosmetics groups commanding the lion's share of market share, making it difficult for startups focused on premium cosmetics. However, as young people become the mainstream consumer demographic and personalized consumption becomes an overt trend, niche brands have an opening to break through.

Furthermore, looking at the two most critical links in the cosmetics industry value chain — production and distribution — startups stand a chance to grab a slice of the mass cosmetics market.

Although startup cosmetics companies often lack sufficient capital to deeply invest in R&D, China has already produced a large crop of technically mature, high-quality, low-cost, and responsive contract manufacturers. They are better equipped to adapt to consumers' increasingly personalized needs and can serve as the production backbone for startup cosmetics companies.

On the distribution side, millennial consumption habits require startups to recognize the influence of e-commerce and social media on purchase decisions. Brands that continuously expand their touchpoints for consumer communication and interaction, and that can quickly satisfy consumers' latest demands, have an opportunity.

Notably, mastering the "influencer economy," managing both online and offline channels, and generating enough traffic to build brand momentum have become the breakthrough points for emerging brands to enter the beauty market.

(Feel free to share to Moments. For republication on other official accounts, websites, or mobile apps, please reply "republication" to learn the rules and contact FreeS Fund for authorization. Copyright belongs to FreeS Fund.)

FreeS Report 13: To Understand China's Consumption Upgrade, First Look at Japan 40 Years Ago

FreeS Report 10: The Common Secret Behind Snack Hits That Have Survived Economic Cycles

FreeS Report 9: How Can Sportswear Brands Achieve Brand Upgrade?

FreeS Report 8: Will the Matcha Industry Produce the Next Starbucks?

FreeS Report 7: Four Major Directions for Healthcare Data Entrepreneurship in China

FreeS Report 5: We've Collected So Much Health and Medical Data — How Far Are We From Living Well?

FreeS Report 4: The SaaS Explosion — Opportunities, Logic, and Challenges

FreeS Report 3: Is an Online IKEA Possible? — Investment Opportunities in Home E-commerce

FreeS Report 2: Investment Outlook for the Healthcare Industry in China and the U.S.

FreeS Report 1: Opportunities and Future of Cross-Border E-commerce Exports