FreeS Report 17: What New Opportunities Will Emerge in the Ancient Jewelry and Accessories Industry? | Frees Fund

From Chow Tai Fook to Pandora and APM: Decoding the Growth Logic of Famous Jewelry and Accessories Brands.

In 1953, Marilyn Monroe swayed across a Hollywood musical, belting out "Diamonds Are a Girl's Best Friend." For the half-century that followed, the public's enthusiasm for diamonds never cooled—and gold, silver, and crystal accessories enjoyed similarly enduring appeal. Today, China's jewelry and accessories market alone exceeds 700 billion RMB in total size. Globally, by 2018, high-end jewelry consumption per capita in China, the US, and Japan had all reached maturity, while emerging markets like India remained in a growth phase.

Though jewelry occupies minimal real estate in an overall outfit, it's arguably the most powerful piece for elevating temperament and shifting style—not merely the finishing touch, but a statement of personality and even status. Yet compared to the price of a lipstick, the thousands or tens of thousands that fine jewelry commands makes women considerably more cautious and selective in their choices. The typical approach: hold onto one or two expensive, value-retaining pieces, while periodically buying trendy, season-appropriate fashion accessories.

Looking back at China's jewelry history, brand development has essentially tracked evolving consumer mindsets. The motivation for purchasing jewelry has gradually shifted from traditional wedding occasions to self-indulgence ("self-gifting") for women. Brands serving different functions have evolved across materials, retail channels, and supply chains in varying degrees.

In this report, we analyze several key companies in the jewelry and accessories industry's development—including Chow Tai Fook, Pandora, and APM—and use them to explore the opportunities and challenges facing brands amid ongoing change.

We hope this offers fresh perspective. We welcome continued dialogue with entrepreneurs and industry experts in the consumer space: reach us at hai@freesvc.com, or add FreeS XiaoRui on WeChat (ID: freesfund).

2020 Jewelry and Accessories Research Report

By Huang Hai (hai@freesvc.com) and Jiao Yingzhu (jiaoyingzhu@freesvc.com)

/ 01 / The Jewelry and Accessories Industry Spectrum

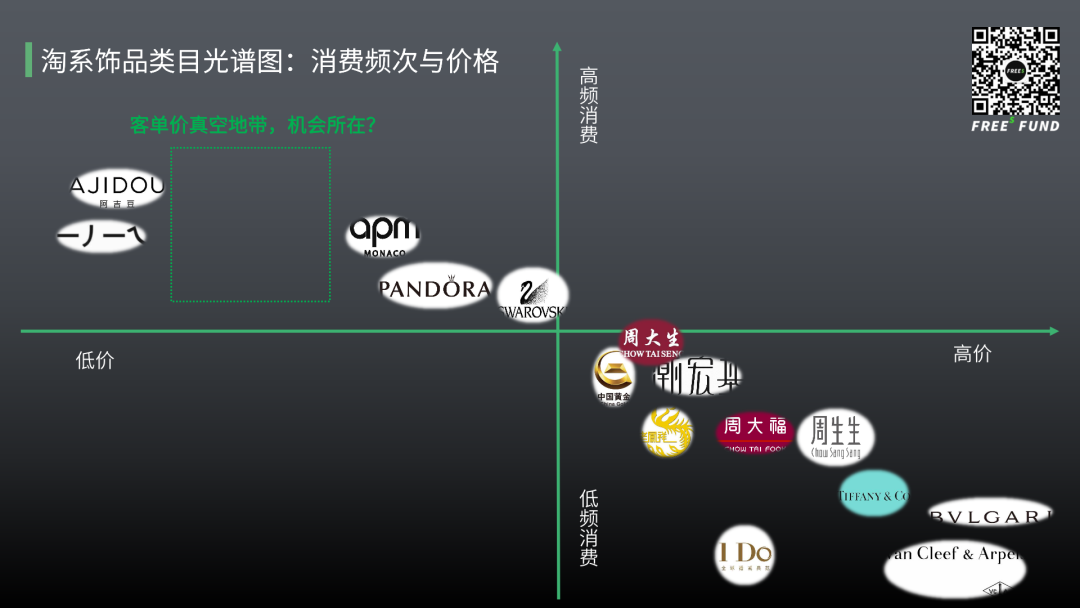

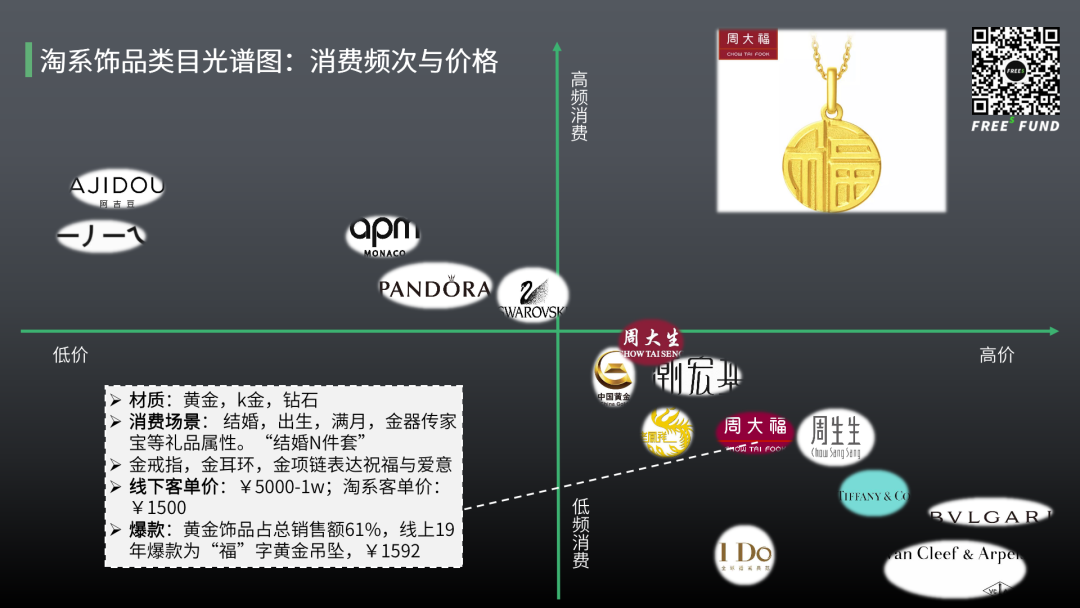

The majority of China's jewelry and accessories industry revenue still comes from offline channels, though consumption is gradually shifting online—creating omnichannel diversity. On Alibaba's platforms alone, the jewelry and accessories category reached over 60 billion RMB on Taobao and Tmall in 2019. The category broadly splits into fine jewelry and fashion accessories at roughly a 6:4 ratio—fine jewelry accounting for over 40 billion RMB, fashion accessories approaching 30 billion.

One fundamental distinction between the two is average order value, which is determined by material. A single gold piece can run into the tens of thousands; established fine jewelry players like Chow Tai Fook target classic fixed-consumption scenarios such as weddings and gift-giving.

Fashion accessories are far more accessible, ranging from several dozen to around a thousand RMB. Notably, despite the 20-billion-plus fashion accessories market on Taobao's ecosystem, market leader Swarovski only captures 1.3 billion, second-place Pandora sits below 1 billion, and the largest domestic emerging brand ZENGLIU is in the hundreds of millions—illustrating the extreme fragmentation.

Tmall's 2019 Double 11 data confirms this dispersion: Swarovski ranked first with 175 million RMB in sales, the only category brand to cross 100 million; Pandora came second at nearly 100 million; ZENGLIU third at several tens of millions.

The content-ification of e-commerce has, to some extent, boosted online jewelry sales. FreeS Fund has previously discussed how video-driven trends have propelled categories like cosmetics. Similar to lipstick, jewelry and accessories emphasize visual coordination and lend themselves well to video and livestream presentation. In 2019, the category's overall growth on Tmall reached 50%.

More specifically, we can segment the industry across dimensions like material, gold content, craftsmanship, and price point:

First, fine jewelry: materials primarily diamonds, pure gold, jadeite, and emeralds, with value-retention properties, typically priced above 3,000 RMB. However, high-ticket jewelry sales require substantial trust; thus brands like Chow Tai Fook and Tiffany & Co., with annual profits in the billions, still derive most revenue from offline.

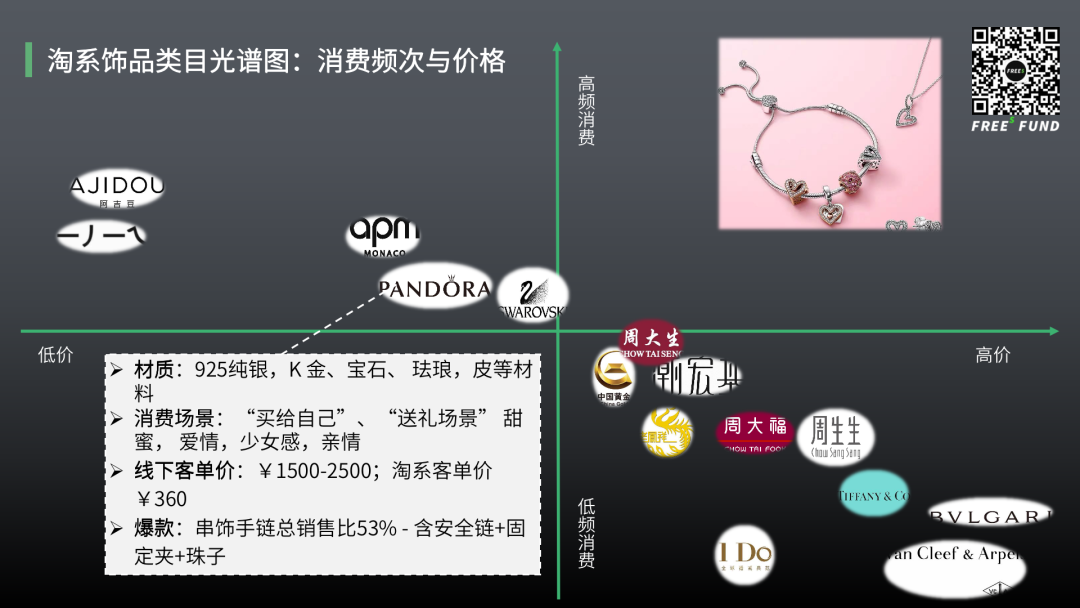

The 500–3,000 RMB range serves as a transition zone, where value retention diminishes as price decreases. Materials shift to silver, silver-plated gold, and K-gold. Representative brands include Swarovski, Pandora, and APM. Interestingly, these brands tend to carry foreign origins—or carefully cultivate a foreign "persona." Foreign brands hold certain advantages in this mid-to-high price band; a similar pattern exists in cosmetics.

From a gross margin perspective, non-value-retaining products actually outperform gold. Gold, as a precious metal directly tradable in markets, has relatively transparent pricing that leaves little room for margin manipulation. By contrast, crystal- or silver-focused brands like Swarovski, Pandora, and APM achieve gross margins of 70–80%.

Third, accessories below 500 RMB: this band uses widely available or even overcapacity materials like alloys, copper, stainless steel, and glass. These pieces compete through constant style and design iteration, also commanding high margins.

Of course, lower price points aren't universally optimal. In the several-dozen-RMB range, Taobao hosts numerous small and medium merchants where brand attributes remain weak: consumers focus on design and appearance without material expectations, often discarding pieces after a few uses—yet repeat purchase rates don't match cosmetics or apparel.

Price band determines purchase frequency and audience size; brand appeal drives customer loyalty. The investment opportunities we watch for find dynamic balance among these core elements.

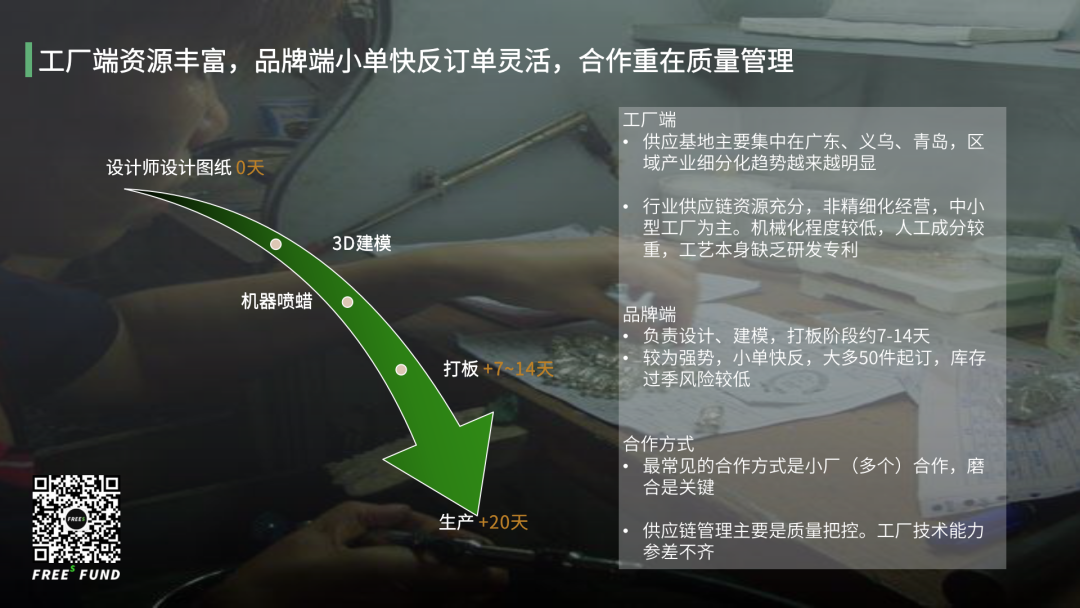

Having examined demand-side segmentation, let's turn to supply chain and production barriers. Most products and brands in jewelry and accessories use OEM/contract manufacturing; only a handful of jewelry giants like Chow Tai Fook and Lao Feng Xiang have built in-house factories and supply chains for vertically integrated production.

Brand-side fragmentation has created opportunities for China's small and medium accessories manufacturers. The typical cycle from designer sketch to production runs about 20 days.

In typical Chinese small-commodity production hubs like Yiwu, Guangdong, and Qingdao, numerous non-refined small and medium factories cluster together—plentiful, uneven in quality, mostly with sales under 100 million RMB. The craftsmanship itself carries no R&D patents, requiring brands to invest considerable effort in coordination, quality control, and design alignment when partnering with them.

Because jewelry features diverse styles, irregular shapes, and complex setting techniques, the industry is unlikely to achieve full mechanization or assembly-line production. Human labor must remain involved in the process, with labor costs sometimes exceeding raw material costs.

Under these conditions, brands and factories tend toward small-batch, quick-turnaround collaboration. Many products have low minimum order quantities, with some as low as 50 pieces. Fortunately, accessories carry less seasonal inventory risk than apparel—unsold items can still sell next quarter.

/ 02 / How China's Century-Old Jewelry and Accessories Industry Has Evolved

We can trace the industry's evolution through three companies' development in China: Chow Tai Fook, Pandora, and APM.

Founded 80-plus years apart (1929, 1982, and 2011 respectively[1]), these three represent distinct approaches and positioning across generations:

- Chow Tai Fook: traditional gold-material-driven, occupying conventional wedding and family/child-rearing consumption scenarios

- Pandora: created new consumption scenarios through its blockbuster "charm bracelet"

- APM Monaco: focused more squarely on women's self-indulgence, with highly distinctive signature brand element—the six-pointed star

We've observed that younger companies emphasize fashion over value retention.

Each of these representative companies maintains core product lines or categories: Chow Tai Fook with various gold pieces, Pandora with silver bracelets, APM with its six-pointed star collection. Regardless of approach, establishing core product lines tightly aligned with relevant scenarios proves critical for brand recognition.

As previously noted, material differences yield the highest average order value but lowest gross margin for Chow Tai Fook, while silver-focused Pandora and APM both achieve 70–80% margins. Meanwhile, Pandora and APM generate similar China-region revenue, around 2 billion RMB each, though APM shows stronger growth momentum while Pandora has begun hitting bottlenecks.

Phase One: Chow Tai Fook

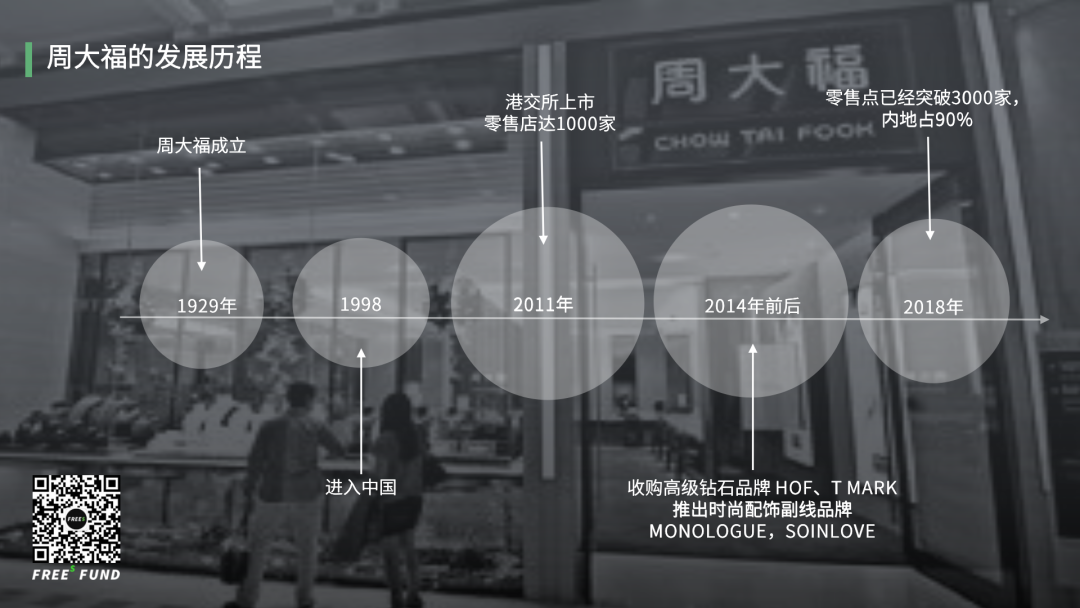

As a nearly century-old jewelry brand, Chow Tai Fook currently operates close to 4,000 retail points in mainland China, capturing nearly 10% market share—making it China's top jewelry brand. Analyzing its business offers direct insight into the industry's overall trajectory.

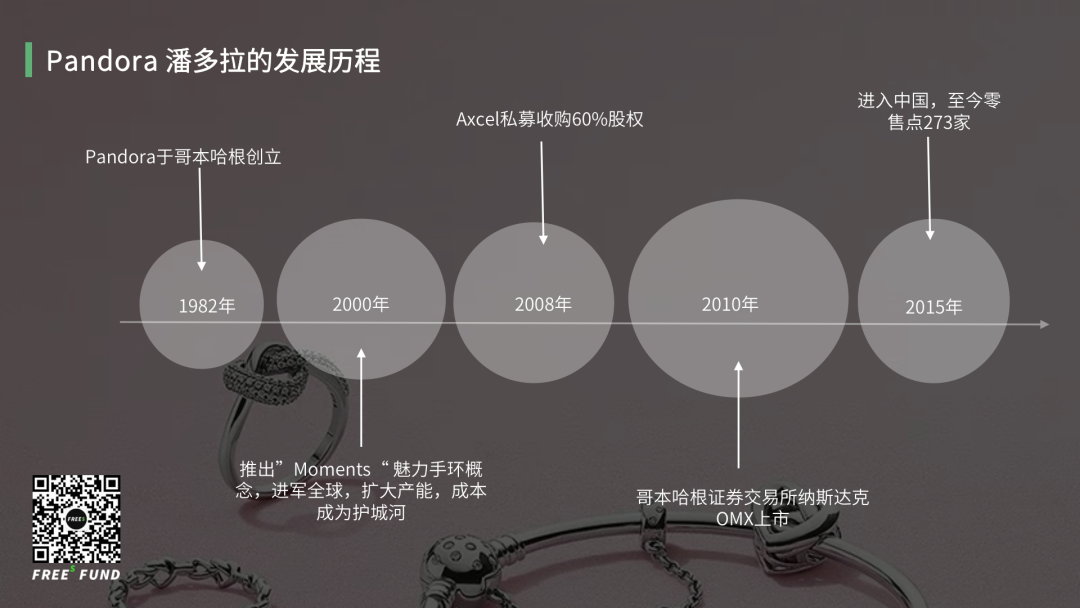

Two particularly important milestones mark Chow Tai Fook's development. The first was its 2011 Hong Kong Stock Exchange listing, with 1,000 retail points—more than 80 years after its founding. The long wait stemmed largely from a 2003 policy change: mainland China abolished its gold production and circulation approval system in favor of business registration, effectively opening the mainland gold market only from that year.

The second key period came around 2014. Through acquisitions of premium diamond brands HOF and T MARK, Chow Tai Fook gradually launched fashion accessory sub-brands targeting millennials, such as MONOLOGUE and SOINLOVE, focusing on accessible luxury jewelry.

If the first milestone reflected decades of industry leadership, the second revealed this established player's anxiety—insufficient brand youthfulness.

This anxiety is widely shared among similar brands: younger consumers feel little resonance with traditional gold jewelry. Gold products comprise roughly 60% of Chow Tai Fook's sales; the name immediately evokes gold associations. As of 2019, the brand's most popular online item remained a ~3-gram gold fortune-character pendant.

As of July 2020, Chow Tai Fook's market cap sits around 80 billion HKD, making it the world's second most valuable jewelry retailer—trailing only Tiffany & Co., acquired by LVMH for $16.2 billion.

Two primary factors support this valuation:

First, mainland China revenue performance. In FY2019, Chow Tai Fook reported approximately 59.3 billion RMB in revenue with 6.87% net margin. The main growth driver came from mainland China, contributing 63.7% of sales with 15.3% growth; Hong Kong and Macau combined for only 36.3% with comparatively modest 8.4% growth.

Second, online revenue performance. As noted, the jewelry category exceeds 40 billion RMB on Alibaba platforms. Leveraging accumulated brand momentum, Chow Tai Fook has achieved over 40% annual online sales growth for four consecutive years, reaching 2.8 billion HKD in FY2019 online sales—with Taobao ecosystem sales accounting for nearly half. This spans approximately 70 e-commerce platforms, with millions of followers on both Taobao and JD.com.

Beyond financials, Chow Tai Fook's industry position rests on three pillars:

One, it sets industry standards. From its founding, it created the "pure gold" (足金) concept, later establishing Hong Kong gold jewelry purity standards and providing reference prices for the Shanghai Gold Exchange. This standard-setting experience has helped expand its market share.

Two, with gold resources historically scarce in China and diamond raw materials entirely import-dependent, Chow Tai Fook has built absolute upstream procurement control.

Three, through in-house factories and self-operated channels—integrated from mining, processing, and design through to retail, with self-operated channels comprising 60%—it has elevated overall gross margin levels.

Phase Two: Pandora

Compared to century-old enterprises like Chow Tai Fook and Lao Feng Xiang, Copenhagen-founded Pandora has merely 40-plus years of history, listing on NASDAQ OMX Copenhagen in 2010.

Pandora launched its "Moments" charm bracelet concept in 2000, going global and achieving household-name status. The bracelet has three components: bracelet, charm, and clip. Users layer different charms onto the base bracelet to create personalized commemorative meaning.

The charm bracelet's success established Pandora's core bracelet-and-charm category, exceeding 50% of total sales. Undeniably, Pandora's bracelet charms redefined accessories. Its blockbuster logic can be summarized in three points:

First, Pandora identified distinctive brand positioning through its marketing logic: a commemorative-meaning jewelry brand. It worked to convince consumers that each bracelet, through free charm combinations, could reflect uniquely personal experiences and memories—creating user-driven customization that powerfully stimulated purchase desire. Simply put, it constructed new consumption scenarios in consumers' minds.

From a supply chain perspective, this represents a particularly interesting highlight: establishing effective connections between customer demand, production, and fashion coordination. In simpler terms, upgrading front-end positioning while simultaneously reengineering back-end supply chain processes. For a consumer startup, this capability is crucial during the 0-to-1 phase.

Second, based on this product positioning, it created multiple consumption scenarios: birthday self-gifts, partner love expressions, commemorative dates through numbers and letters, memorializing events through special shapes like baby carriages.

Finally, Pandora invested early in digitalization, with competitively positioned average order values—each charm around 360+ RMB—and offered 3/6/12-month interest-free installment plans across e-commerce platforms, lowering psychological barriers. At one point, repurchase rates reached 70–80%. In FY2019, Pandora's Alibaba sales exceeded 30% of total China-region sales.

Of course, every coin has two sides; Pandora's bracelet was both blockbuster and constraint.

In overall market purchasing power, Chinese women's accessory purchases by piece ratio roughly runs necklaces:earrings:bracelets:rings at 4:3:1:1—necklaces and earrings combined account for nearly 80%.

Pandora has aggressively expanded its necklace, earring, and ring proportions in recent years, yet data shows bracelets still comprise roughly 60% of its category mix, while demand-heavy necklaces and earrings sit at only about 10% each—meanwhile, DIY charms don't integrate easily with necklaces and earrings.

This bracelet concentration limits Pandora's overall brand scale expansion. Once the window for using a small category to drive larger categories passes, momentum becomes difficult to sustain. One could say Pandora's rise came from bracelets, and its stagnation does too.

Product revenue provides the most direct reflection: starting 2017, Pandora's revenue began declining, with FY2019 global sales reaching 22.161 billion RMB, down 8% year-over-year—the brand showing clear fatigue.

▍Phase Three: APM Monaco

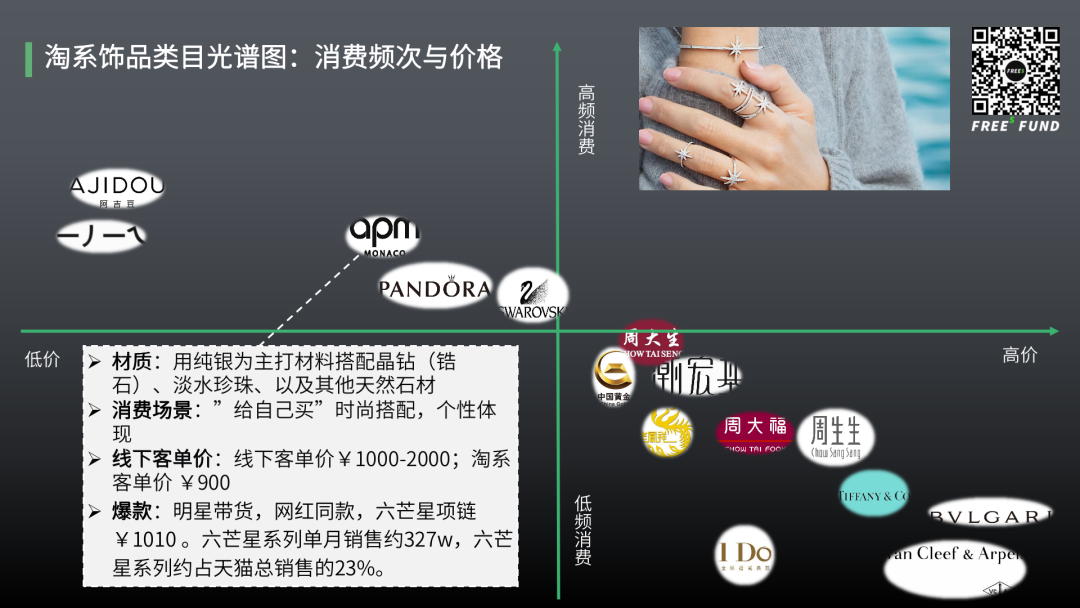

APM Monaco founder Ariane Prette is European, having lived in Hong Kong for many years and engaged in trade of Chinese jewelry to Europe. After the 2008 financial crisis cratered cross-border trade, the Prette family pivoted in 2011 to design-focused sterling silver jewelry.

From the start, the brand cleverly employed a "originating from Southern France" image and concept for packaging, establishing fashionable positioning early on. As of end-2019, it operated 300+ directly managed stores globally, with 200+ in China—essentially making it a China-market-focused jewelry brand.

APM Monaco likewise has its blockbuster—the six-pointed star collection, whose design element became the brand's signature, widely applied across bracelets, earrings, necklaces, and other products. This collection accounts for approximately 23% of its Tmall total sales, making it the brand's most popular series.

This approach is quite astute: Van Cleef & Arpels, Tiffany, Bulgari and other jewelry brands all maintain their own iconic, highly visually recognizable elements.

Unlike Pandora's commemorative-scenario focus, APM Monaco more directly serves women's self-indulgence needs—purchases for oneself and close friends. Marketing relies on celebrity and influencer promotion; in 2018 it launched the APM Monaco × Yao Chen jewelry collaboration, boosting brand awareness and sparking discussion waves on Xiaohongshu.

Of course, aesthetic judgment varies individually, so visually positioned products must evolve faster than trends to remain at fashion's forefront. Simply put: having chosen the path of continuously leading trends and fashion requires sustained investment in new-release speed and style iteration.

Thus we observe: diamond-and-gold players like Tiffany and Chow Tai Fook might launch one or two collections annually; Pandora follows holidays and scenarios with 7–8 release cycles per year; while APM adds one new theme and four new collections monthly, with 35–40 new SKUs hitting stores monthly—full-chain update from product design through production to retail in just one month.

The APM Monaco team clearly recognizes that consumers buy fashion pieces not for the material, but for how the product makes them feel about themselves—the aforementioned "self-indulgence" need. APM focuses on silver, avoiding gold entirely, yet pushes average order values above 1,000 RMB through tone and fashion sensibility.

At 1,000 RMB for silver products, the price isn't low—but silver costs roughly 1% of gold, giving APM Monaco ample profit room. Though unlisted, we estimate from public information that it enjoys gross margins no lower than 75% and net margins approaching 20%.

/ 03 / Summary: What New Opportunities Exist in This Industry?

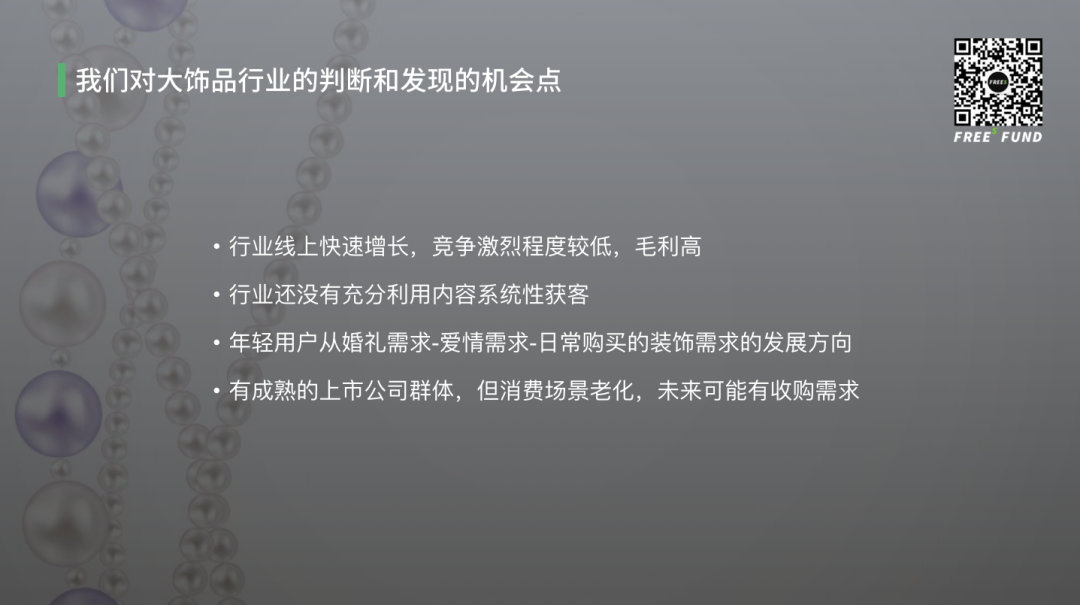

Overall, jewelry and accessories present a market of simultaneous opportunity and challenge.

Despite the category's high-margin characteristics, from an SKU management perspective it more closely resembles fast-fashion apparel, with demanding requirements for continuous new releases and SKU management capability.

Such industries exhibit fragmentation, non-standardization, and long-tail dynamics—making sustained success from one or two styles unlikely. Strong product iteration and relatively high inventory turnover requirements apply. For startups, cutting in with limited SKUs to find a blockbuster may more readily achieve 0-to-1 breakthrough. Beverages and lipstick, benefiting from "blockbuster supremacy" characteristics, have become standout new domestic brand categories in recent years.

Second, from a demand perspective, jewelry and accessories more closely resemble cosmetics, satisfying women's desires for beauty, self-indulgence, and self-expression. Like cosmetics, brands initially tend to build awareness through "grass-planting" (content seeding) on platforms like Xiaohongshu and Douyin. However, compared to cosmetics, jewelry and accessories are relatively lower-frequency, with less spontaneous user-generated content—we've yet to see startup success cases systematically acquiring customers through content ecosystems. Even Tmall's top-ranked domestic emerging brand ZENGLIU, despite early establishment and strong design, more closely resembles a typical "Taobao brand." Further leveraging video formats to showcase product distinctiveness and storytelling will become the breakthrough point for emerging brands entering jewelry and accessories.

Notes:

- APM Monaco was founded by Ariane Prette in 1982, originally as an OEM providing original designs, building mature design and supply chain capabilities serving European jewelers. The Prette family pivoted to design-focused sterling silver jewelry in 2011.

Reader Engagement If you've read this far, we welcome your thoughts on the jewelry and accessories industry in the comments. We'll gift the 6 most thoughtful commenters a Juno&Co. "Multi-Use Sculpting Powder"—like jewelry and accessories, it's in the business of enhancing beauty. (Deadline: 9:00 PM, July 24.)

Contact Us We look forward to continued exchange with entrepreneurs and industry experts in the consumer space. Reach us at hai@freesvc.com, or add FreeS XiaoRui on WeChat (ID: freesfund).

FreeS Report 16: The Truth About Early-Stage Healthcare Investment and China Speed | FreeS Fund

Double 11 at Halftime: What Did Zhong Xue Gao, Saturnbird, Botaniera, and Huasheng Haoche Do Right?

The Category Logic Behind the Hype—Using Coffee Industry Investment as Example

Startup Brand Breakthrough: From Traffic Thinking to Content Thinking | FreeS Fund

Where Is the Endgame for E-Commerce Livestreaming? | FreeS Fund