FreeS Report 20 | Learning from History: Why We're Bullish on Industrial Robots?

A Brief History of Industrial Robot Development in Germany, Japan, and the US, and China's Opportunity

Industrial robots have reached their best moment for growth. According to data from China Customs and Zhiyan Consulting, in 2019 China exported industrial robots for the first time in greater numbers than it imported — 105,604 units exported versus 60,723 units imported.

As the world's largest manufacturing nation, China is benefiting from innovation-friendly policies and the advancement of AI technology. We believe China will eventually produce world-class industrial automation enterprises. What patterns govern the emergence of these companies, and how will they develop?

History offers guidance. By analyzing the development of industrial robots in the US, Germany, and Japan, we identify three common factors shaping the industry: macro environment and policy, labor availability, and sector-specific demand.

Compared to Germany, China's conditions for industrial robot takeoff bear greater resemblance to Japan's. Whether measured by GDP composition, labor structure, or robot installed base, China today looks much like Japan around 1990. The difference: Japan's robot growth entered a plateau after 1990. In our view, China's robot industry will enter a new high-growth phase after 2020.

So how specifically can startups enter this field on the verge of explosive growth, build moats, and win? We studied the rise and fall of the "Big Four" in industrial robotics. Their trajectories offer lessons for Chinese industrial robot companies.

This article explores:

- Why is China at an opportune moment for developing industrial robots?

- Why did industrial robots, first born in the US, take off first in Japan and Germany?

- Beyond automotive and 3C electronics, which other industries hold automation opportunities?

- What can China's industrial robot industry learn from the "Big Four"?

Before diving in, three preliminary conclusions:

- Whether viewed through macro policy, labor composition, or demand-side factors, China currently possesses the conditions for industrial robot development.

- Lessons Chinese industrial robot companies can draw from the "Big Four": core technology must come first, and the more fundamental the technology, the greater the advantage; product versatility matters greatly; synergy and scale effects deserve attention; software improves gross margins; the biggest moat is industry moat — sector-specific know-how is essential; extend the service chain both vertically and horizontally.

- In large markets such as logistics, home appliances, and textiles, automation levels and robot deployment remain mismatched with industry scale. These sectors hold enormous potential for industrial robot growth.

Learning from History: A Study of Industrial Robots

By Yao Yuan (yaoyuan@freesvc.com)

I. Why Did Industrial Robots, Born First in the US, Take Off First in Japan and Germany?

01 Why Industrial Robots Didn't Develop in the US

The world's first industrial robot was born in America. In 1961, American company Unimation introduced Unimate, a 1.8-ton robotic arm installed on an assembly line at a General Motors plant in New Jersey. Its function was simple: remove hot castings from die-casting machines and weld them onto car bodies, freeing workers from this dangerous and health-hazardous task.

Yet industrial robots did not see widespread adoption in the US. Main reasons include:

Early industrial robots were functionally limited, performed poorly, and cost too much. The first-generation Unimate sold for $35,000 — roughly equivalent to a worker's lifetime wages at the time — yet could only handle simple welding of large parts, while manufacturing workers earned just $2 per hour. Weak customer purchase intent was hardly surprising.

Additionally, the US had abundant labor. During the 1960s-70s when industrial robots emerged, American manufacturing employment hit historical peaks, driven by the post-WWII baby boom. During this same period, US unemployment climbed to near 10%, according to Wind and Huajin Securities Research Institute data. Machines replacing humans would only further reduce jobs. The US government had little policy incentive to support robot industry development.

02 Why Did the Robot Industry Take Off in Japan and Germany?

Both Germany and Japan built their first industrial robots based on Unimate. Since American robots couldn't sell domestically, US robot companies traveled worldwide to promote their products. Some German and Japanese companies purchased American robots and then modified them.

Why were Germany and Japan so enthusiastic about industrial robots?

A crucial factor: both countries faced labor shortages.

As fellow WWII defeated nations, Japan and Germany had lost many young adults in the war. During the 1960s-70s, the working-age population (15-64 years) as a share of total population trended downward in both countries. Unemployment rates ran below 4% in Germany and under 2% in Japan — the latter partly due to Japan's lifetime employment system. By comparison, US unemployment hovered around 10%, significantly higher.

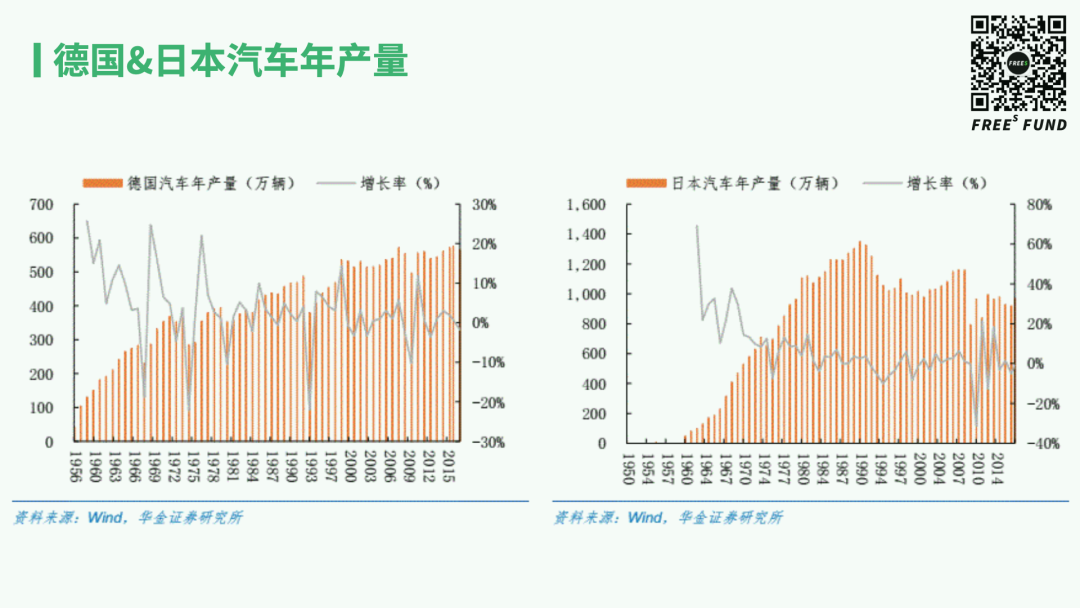

Second, the automotive industry's rise.

During the 1960s-70s, German and Japanese auto sales surged. German annual auto production grew from under 2 million to nearly 4 million vehicles; Japanese output climbed from under 1 million to over 6 million. Downstream industries rose alongside.

Against this backdrop, Japanese and German governments strongly supported robot industry development.

The German government launched the "Improvement of Working Conditions Program," which mandated that certain toxic, hazardous jobs must use machines to replace humans.

Japan's policy support was even more aggressive, offering loans, subsidies, and cash incentives directly to robot companies and factories using robots, while establishing robot research labs to support related industry research.

In summary, labor shortages, automotive industry revitalization, and policy support combined to launch German and Japanese industrial robots.

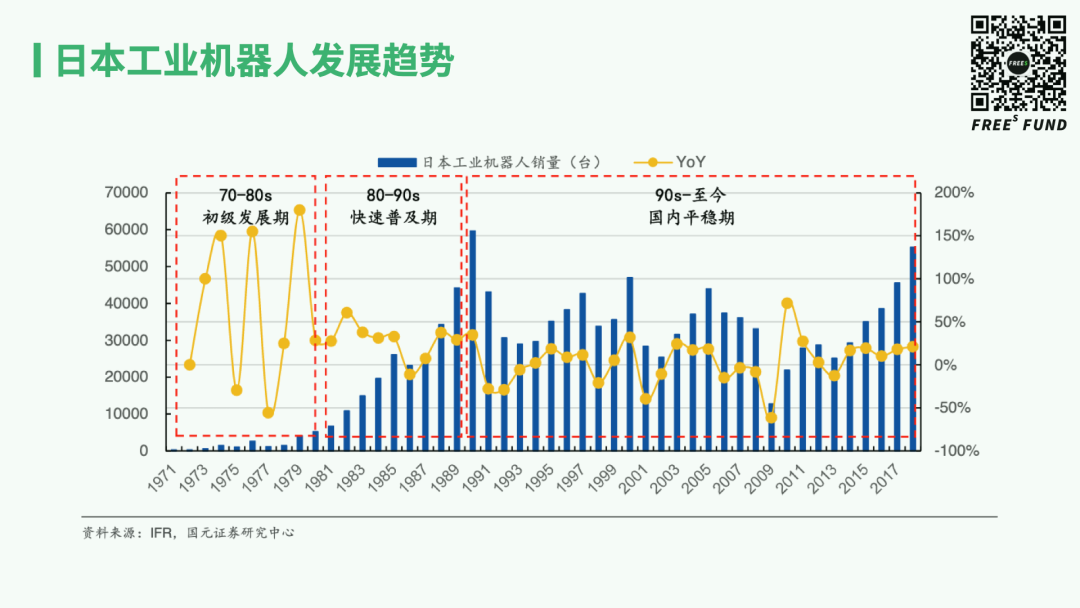

03 Japan's Example: Trends in Industrial Robot Development

Japan's industrial robots passed through three development stages: initial growth from 1970-80s, rapid adoption from 1980-90s, and stable growth after the 1990s. 1990 marked the pivotal year — the watershed between rapid growth and plateau.

Japan's industrial robot boom closely tracked developments in automotive and semiconductor industries.

As noted, automotive was a key driver. One index captures this relationship: the dynamic correlation coefficient between auto production growth rate and industrial robot shipment index growth rate. The higher the coefficient, the stronger the positive correlation. According to National Bureau of Statistics and Huajin Securities Research Institute research, Japan's auto production growth and robot shipment growth showed very high correlation. The dynamic correlation coefficient averaged 0.41 from 1984-2017, peaking around 0.9 near 2010.

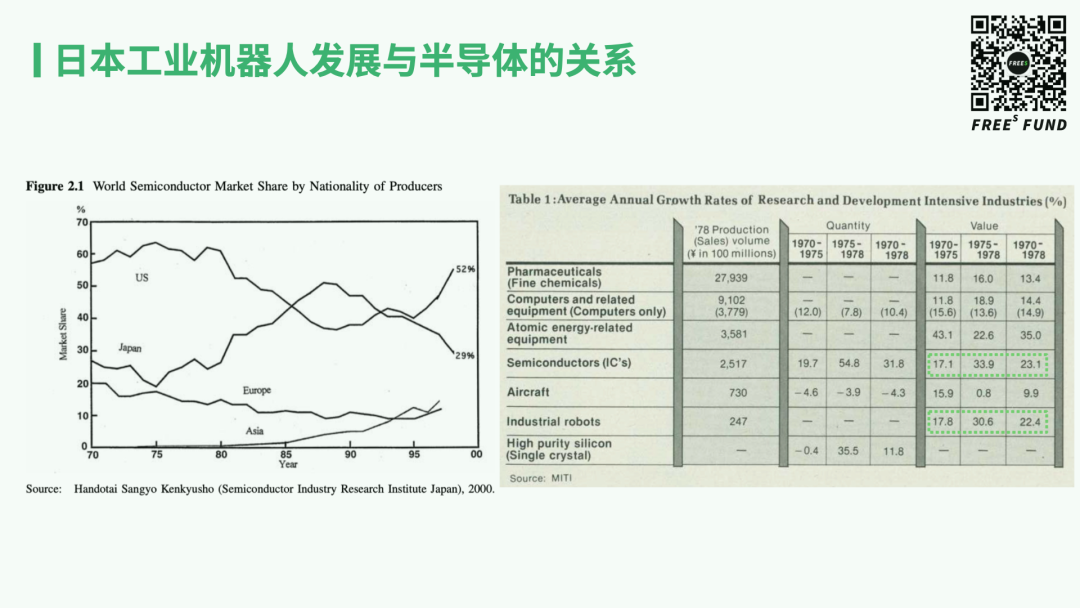

Semiconductors also significantly promoted industrial robot development.

In the 1970s, Japan's semiconductor (IC) industry and industrial robot industry saw remarkably synchronized growth rates — both climbing from roughly 17% to about 30%, then declining to around 20%.

Japan's global semiconductor market share rose continuously from the 1970s through the 1990s, peaking in the 1990s. The 1990s marked both the apex of Japanese industrial robots and the apex of Japanese semiconductors.

FreeS Fund Perspective

History shows that three factors shaped industrial robot markets in Germany and Japan: macro environment and policy, labor availability, and industry demand. The US in the 1960s-70s lacked these conditions; Japan and Germany possessed them, so their industrial robot industries took flight.

II. Why Is China at a Good Moment for Developing Industrial Robots?

01 Conditions China Possesses for Industrial Robot Industry Development

Compared to Japan and Germany, has China's moment for industrial robot development arrived?

Policy. China's manufacturing upgrade hinges heavily on automation and intelligent transformation. Recent trends toward domestic substitution and the rollout of "new infrastructure" have also provided policy tailwinds for industrial automation.

For instance, new infrastructure sectors — intercity high-speed rail and urban transit networks, EV charging stations, ultra-high-voltage power transmission, and big data centers — all require machine-for-human solutions that align with cost-cutting and efficiency imperatives. AI, another pillar of "new infrastructure," also has direct applications in industrial automation.

Second, labor. According to Wind and Northeast Securities data, from 2013 to 2018, China's working-age population share declined year over year, manufacturing wages rose steadily, and average robot prices trended downward — dipping below average manufacturing wages around 2013–2014. Machine substitution carries a clear cost advantage in China.

Third, demand.

China is already the world's largest auto market and is now gaining massive incremental demand from new energy vehicles. NEV R&D, design, and production will all deeply apply automation and intelligent technologies; the supporting infrastructure — charging stations, transmission lines — also requires automation solutions.

5G represents another major incremental market. The commercialization and widespread adoption of 5G will drive hardware refresh cycles. Beyond phones, smart hardware — watches, bands, earbuds — will see huge new shipment volumes.

Moreover, as the world's largest manufacturing country, China needs industrial robot solutions across sectors beyond automotive and 3C.

Overall, whether viewed through the lens of policy, labor, or demand, China currently possesses the conditions for industrial robot development.

02 China's Robot Development Trajectory Resembles Japan's

After comparing the conditions for industrial robot development in China versus Japan and Germany, we find that China today looks much like Japan around 1990 — whether measured by GDP composition, working-age population, or industrial robot density.

First, GDP composition.

In 2019, the GDP share of China's three major industries roughly matched Japan's from the 1970s–1980s, about a 30-year lag. In 2019, China's primary industry accounted for 7.1% of GDP, secondary industry nearly 40%, and tertiary industry about 53%. In Japan from the 1980s–1990s, the respective shares were below 5% for primary industry, below 40% for secondary industry, and 60–70% for tertiary industry.

Behind this sectoral shift lies a key driver of structural evolution: robots liberating workers to flow into services.

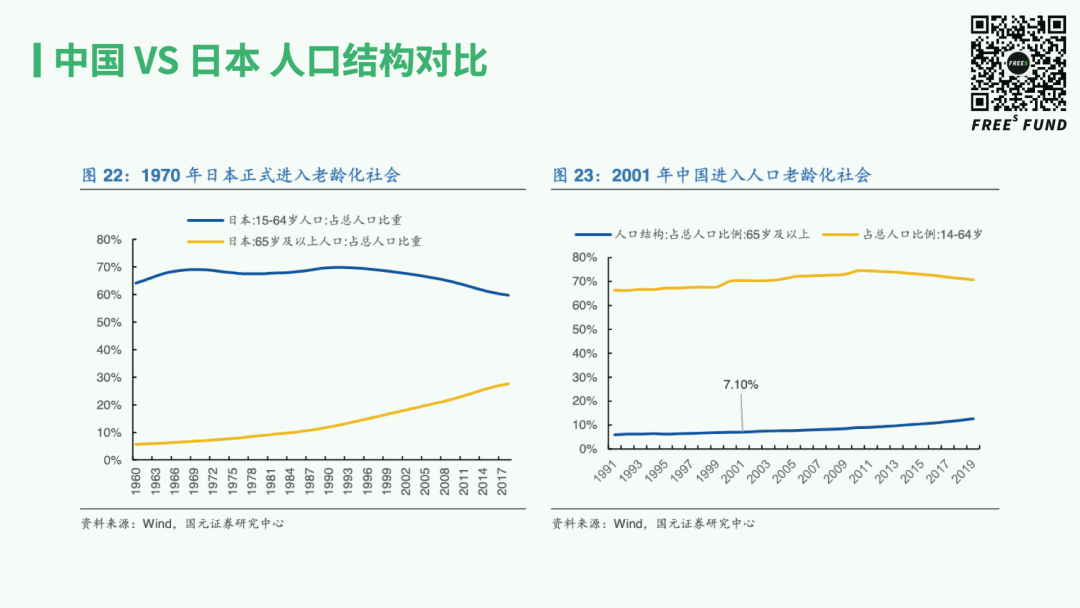

The second indicator: working-age population comparison.

Per the UN's Population Ageing and Its Socio-Economic Consequences, a region enters an aging society when the population aged 65 and above exceeds 7%, and an aged society when it exceeds 14%.

In the early 2000s, China's 65+ population share crossed 7%; by 2017, it exceeded 10%. In Japan, these thresholds were reached in the early 1970s and mid-1980s respectively. Like GDP composition, China's current labor force structure resembles Japan's from over 30 years ago.

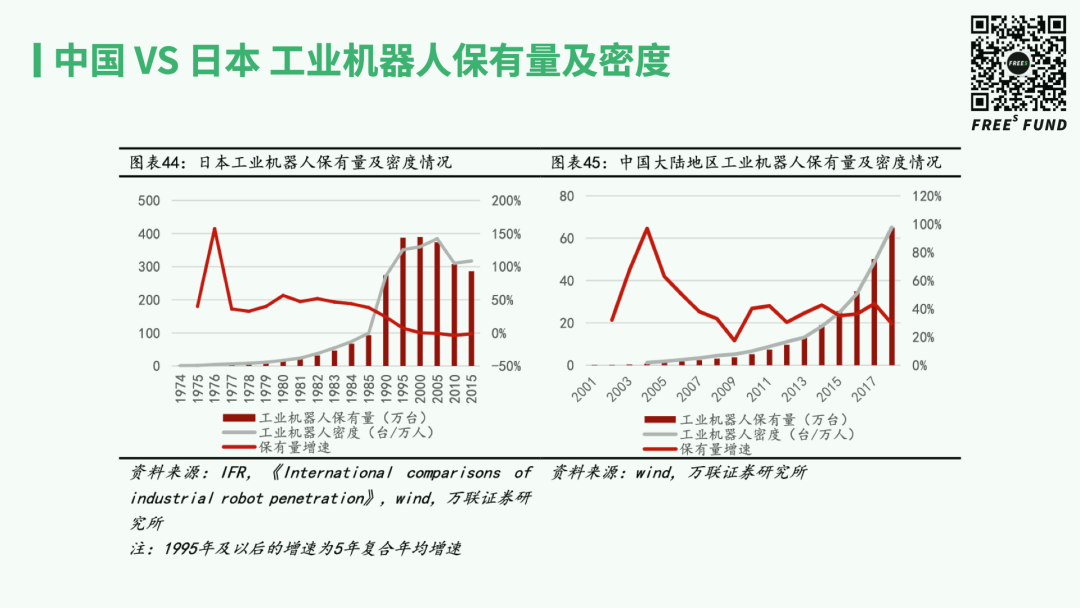

The third indicator: industrial robot density. In 2018, China's industrial robot density was 65.2 units per 10,000 workers, close to Japan's level around 1990.

The trajectories of Chinese and Japanese industrial robot development also show parallels.

Looking at sales volume changes, China's industrial robots started from near zero in 2000, took off around 2010, and by 2018–2019 entered a period of stabilization and pullback — equivalent to Japan's transition from peak to plateau around 1990.

We generally divide China's industrial robot development into four phases:

2000–2009: Early stage. The transfer of Western 3C manufacturing to China created demand for automation solutions.

2010–2012: Rapid growth period, driven by booming automotive and 3C industries.

2013–2017: High-speed growth period. 2013 was the "4G era" launch year; users needed to replace hardware across categories. Explosive 3C growth pulled industrial robots along with it.

2018–2019: Pullback and adjustment period. State subsidies for robotics declined, and 3C demand weakened. According to CAICT data, 2019 domestic mobile phone shipments totaled 389 million units, down 6.2% year over year. Some users were holding out for 5G before upgrading.

So, will China's industrial robots follow Japan into a plateau? Our preliminary answer: after 2020, China's industrial robots will enter a new period of high-speed growth.

03 Why Will China's Industrial Robots Enter a New High-Growth Period?

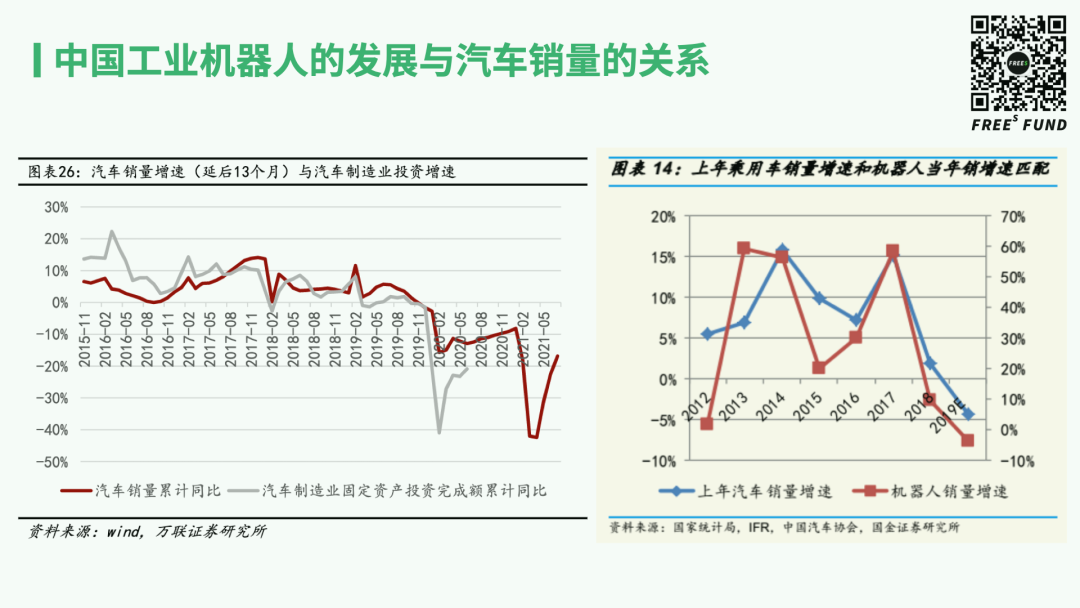

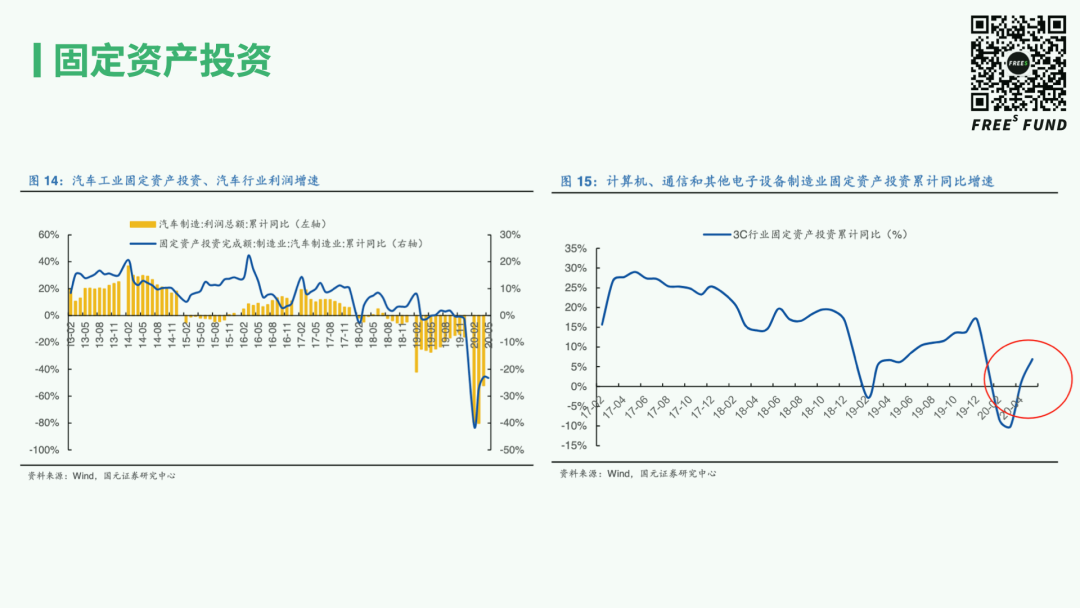

First, let's examine the relationship between industrial robot sales, auto sales, and auto manufacturing investment growth.

Comparing auto manufacturing investment growth from 2015–2020 with auto sales growth (lagged 13 months), you'll find the trajectories track remarkably closely.

A significant portion of auto manufacturing investment goes to industrial automation. This linkage effect means auto sales and robot sales are tightly correlated. From 2012 to 2018, prior-year passenger vehicle sales growth closely matched current-year robot sales growth.

In 2020, the recovery rhythms of industrial robots and autos also aligned closely.

Since the start of 2020, industrial robots have warmed up, with monthly output showing clear recovery. According to Wind and Shanghai Securities Research Institute data, during 2018–2019, China's monthly industrial robot output had fluctuated mildly or even declined slightly. The year-over-year change in monthly output is more telling: from September 2018 to September 2019, monthly output was consistently negative year over year, turning positive again from late 2019 onward.

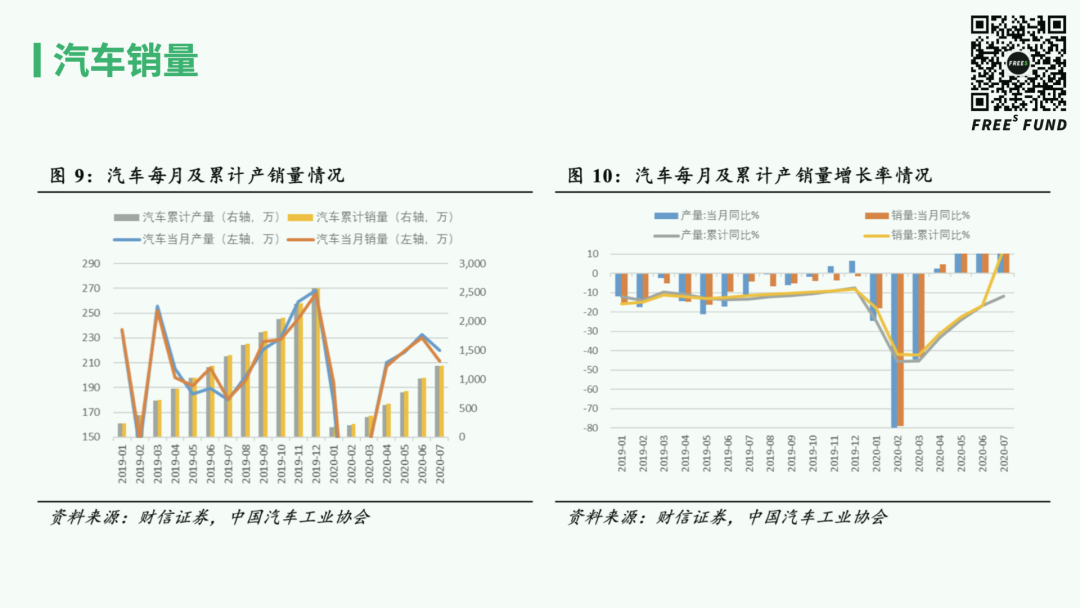

Let's look at auto sales over the same period.

From January 2019 to March 2020, China's monthly and cumulative auto production and sales were mostly negative year over year, with January–March 2020 particularly brutal. April saw year-over-year growth turn positive, with May–July showing more pronounced gains.

A major factor behind the auto rebound is new energy vehicles. China's NEV monthly production and sales year-over-year growth was consistently negative from H2 2019 until July 2020, when it finally turned positive. July–September saw very rapid NEV sales growth: 19.3% in July, 25.8% in August, and 67.7% in September.

It's not just NEVs — even conventional vehicles saw a major rebound this year compared to 2018–2019. According to statistics from SAIC-GM's Buick brand, September wholesale sales reached 98,722 units, up 28% year over year, hitting a 24-month high.

The synchronized recovery of industrial robots and autos confirms that rising auto sales are indeed driving robot sector revival.

As numerical proof, fixed asset investment in the auto industry has been recovering since February this year, and much of that FAI flows into industrial automation.

Now let's look at the 3C sector.

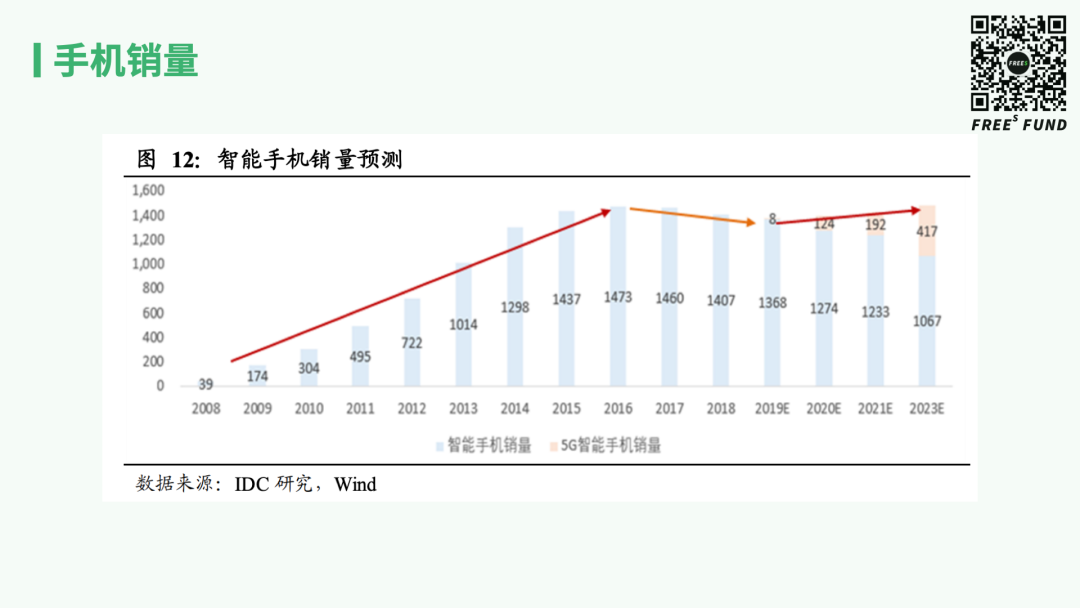

As mentioned earlier, 3C experienced a pullback and adjustment in 2018–2019. According to IDC's smartphone sales forecast, global smartphone sales will rise, with 2020 expected to reach 1.4 billion units and year-over-year growth turning positive. The incremental volume will come mainly from 5G phones. 2019 was the "5G era" launch year, stimulating replacement demand. According to CAICT statistics, from July 2019 to November 2020, 5G phone shipment share rose from 0.2% to 68.1%.

Beyond driving smartphone demand, 5G will also accelerate upgrades across other smart hardware — meaning factories need new production lines and new automation solutions.

Moreover, 5G dramatically boosts signal transmission speeds. With 5G, critical enabling capabilities for robotics — data volume, speed, and latency — all improve significantly across multiple dimensions.

Currently, we see many industrial robot projects concentrated in the 3C sector. The main reasons are:

Compared to countries like the US, Japan, and Germany, China's 3C industry remains relatively under-automated. Second, China is a massive 3C consumer market, creating ample room for industrial robot applications. Another important factor: 3C products and their manufacturing processes evolve rapidly. Different technical solutions and processes for production and inspection constantly require new automation solutions, providing startups with a steady stream of commercial opportunities and market entry points.

Overall, beyond macro factors like policy and labor, the demand-side drivers for China's industrial robot development include:

- First, new markets created by new energy, 5G, and new infrastructure have indeed given industrial robots substantial room to operate.

- Second, this year's pandemic has accelerated the "machines replacing humans" trend, with the public more keenly aware of the importance of automation.

- Additionally, AI development will open more application scenarios for industrial robots.

FreeS Fund Perspective

Whether looking at policy, labor, or demand-side factors, China now has the conditions in place to develop industrial robots. China's current industrial robot development resembles Japan's around 1990. The difference is that after 2020, China's industrial robots will enter a new period of rapid growth. In the existing market, many problems that industrial robots previously couldn't solve can now be addressed thanks to technological advances.

04 Beyond Automotive and 3C: What Other Industries Hold Opportunity?

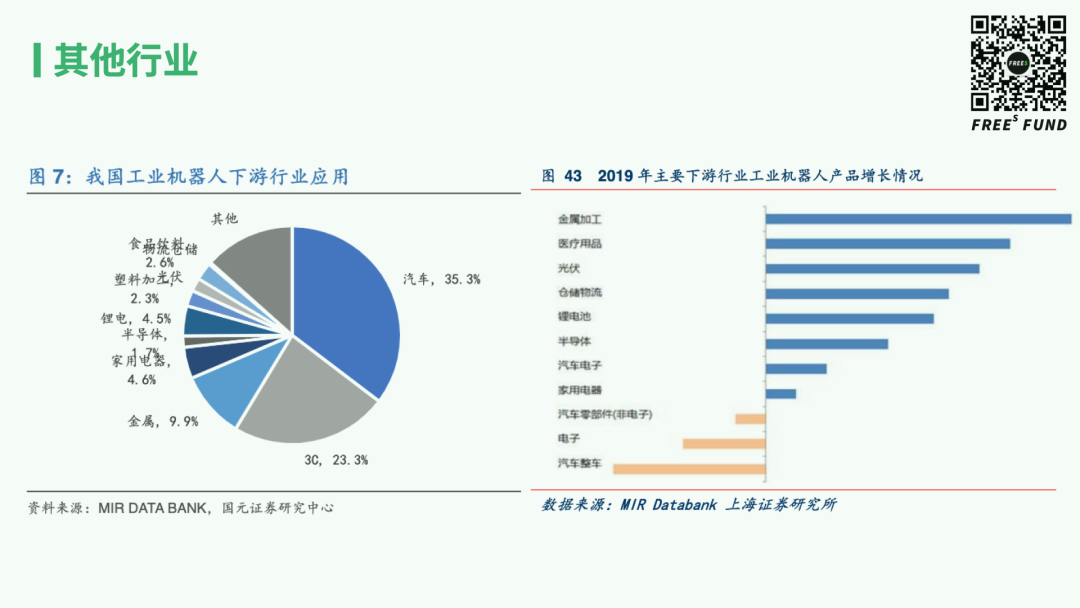

In China, industrial robot adoption varies considerably across industries. The automotive and 3C sectors mentioned above have essentially reached maturity, with widespread robot deployment.

FreeS Fund portfolio company Yifei Automation is a company actively building automation solutions across 3C, consumer goods, pharmaceuticals, and logistics. Yifei focuses on industrial robot R&D and manufacturing, holds nearly 100 national patents, and is currently one of China's largest parallel robot companies — also one of the few Chinese robot brands to make it into Fortune 500 supplier lists. (Click here to read "How to Invest in Industrial Robots? | FreeS Research — Learning from Investment")

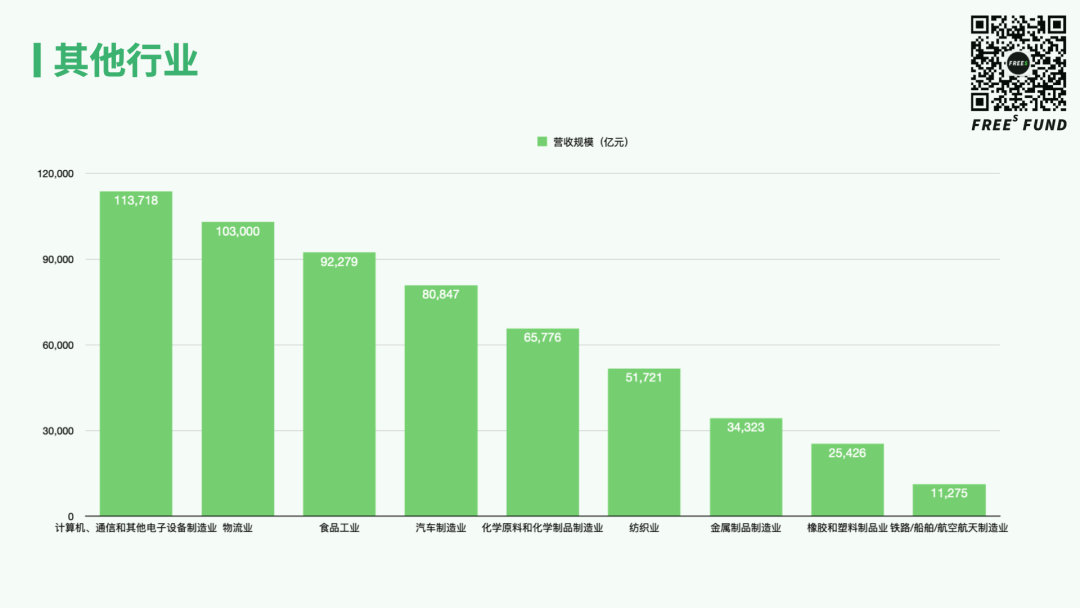

In many industries such as logistics, home appliances, and textiles, robot sales remain far below their sector scale.

When we rank China's manufacturing subsectors by output value and compare this to industrial robot sales ratios, we can see at a macro level that automotive, 3C, and metals show basic alignment between sector scale and robot sales. But in massive industries like logistics, home appliances, and textiles, robot sales fall far short of sector scale. These industries therefore hold enormous potential for industrial robot development.

Industrial robot density also reveals growth potential for robot adoption across different Chinese industries.

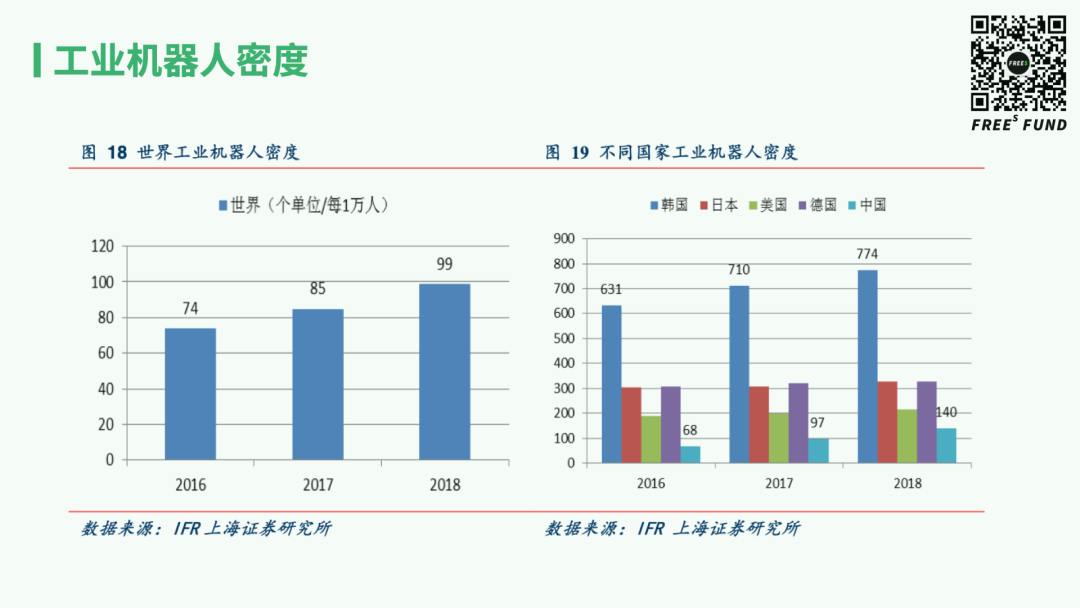

In 2018, the global average industrial robot density was 99 units per 10,000 workers. China stood at 140 units per 10,000 workers — while still trailing Japan, Germany, and the US, it has already surpassed the global average. (South Korea is an outlier with a relatively concentrated industrial structure.)

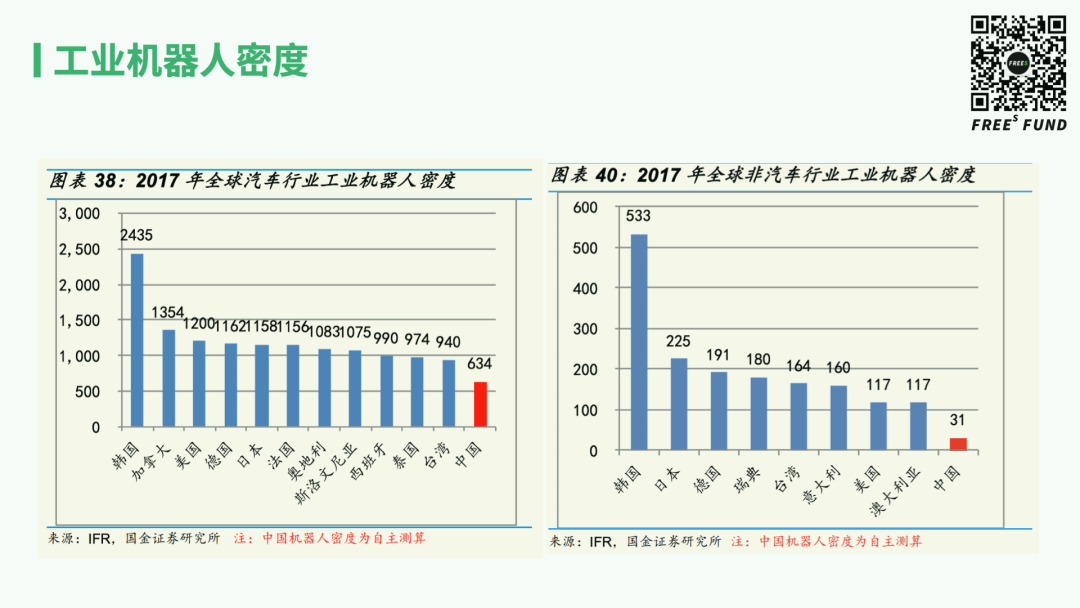

Comparing 2017 global automotive industry robot density, the US, Germany, and Japan had roughly double mainland China's density. In non-automotive sectors, US, German, and Japanese density was approximately 4-7 times that of mainland China.

This shows that outside automotive, China's manufacturing automation remains relatively low.

▍Robot Applications in Logistics

China's logistics network is highly developed, with relatively low labor costs and leading transport efficiency. But in warehousing and management, the gap with countries like the US and Japan remains significant — still heavily reliant on human labor with low automation levels.

Warehousing has become one of the most active application areas for industrial robots, including transport, sorting, loading and unloading.

FreeS Fund portfolio company Covariant.AI focuses on warehouse automation solutions. Covariant.AI has developed a platform combining camera-equipped robotic arms, specialized grippers, and ample computing power, excelling at grasping items in warehouses. Its intelligent warehouse robots can pick and sort over 10,000 different items in a customer's facility with 99% accuracy. Wired reported that "Covariant.AI hasn't yet developed robots as adaptable and flexible as humans, but it has clearly succeeded in applying reinforcement learning research to industrial environments."

▍Robot Applications in Home Appliances

Similar to logistics, China's home appliance industry has very low automation levels, presenting massive opportunities for industrial robots.

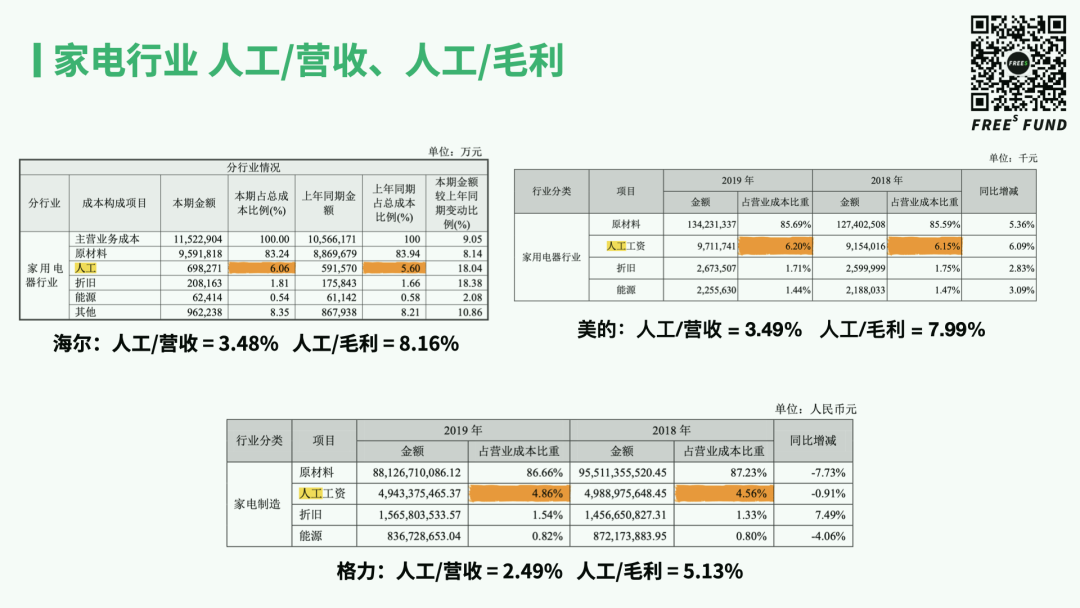

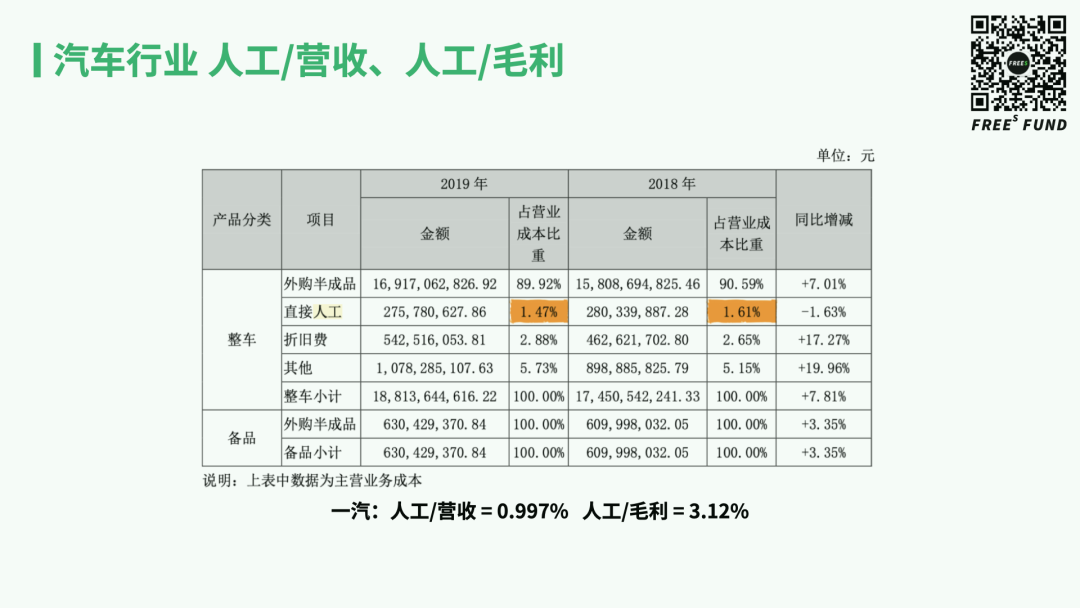

We analyzed the labor-to-revenue and labor-to-gross-profit ratios in the financial reports of the three home appliance giants (Haier, Midea Group, and Gree). Lower ratios indicate higher automation. We found these three companies' labor/revenue ratios range from roughly 2.49% to 3.49%, and labor/gross-profit ratios from about 5.13% to 8.16%.

Compared to the automotive industry, which makes full use of industrial robots, home appliance automation remains relatively low. Take FAW: its labor/revenue ratio is about 0.997%, and labor/gross-profit ratio about 3.12% — far below the home appliance sector.

FreeS Fund portfolio company Haiyan Automation is a company deeply rooted in home appliance automation solutions. The company focuses on machine vision and AI applications in intelligent manufacturing, with solutions including appearance defect detection, high-precision measurement, component inspection, positioning and assembly. It currently holds a leading position in the home appliance sector and has expanded into steel, home furnishings, and automotive components.

▍Textiles: Massive Room for Automation

China's textile industry is large in scale but currently low in automation. Technology suited to textiles would unlock very substantial market space.

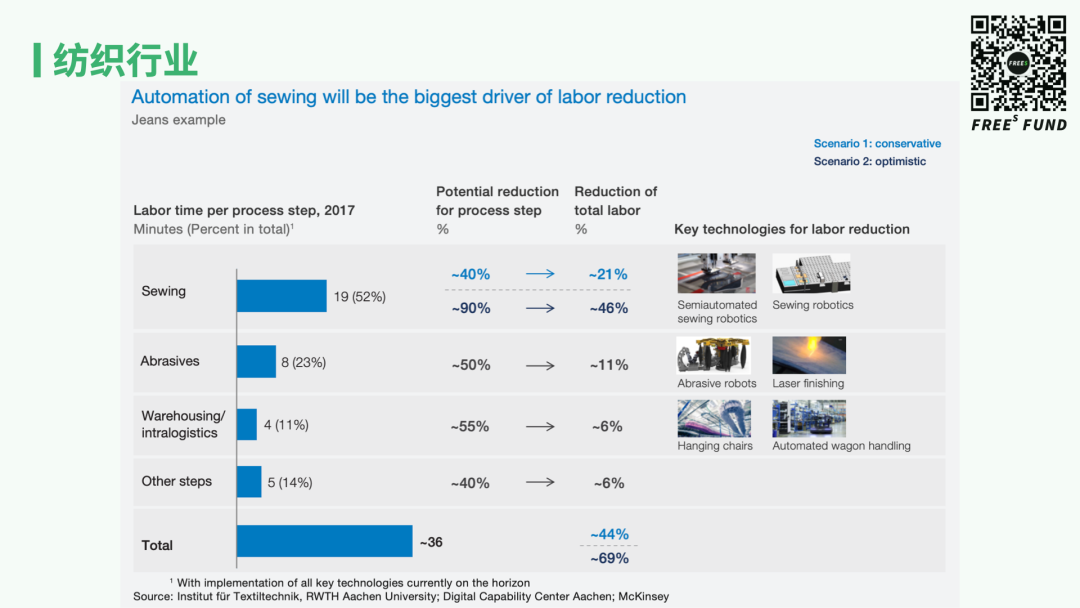

In textiles, sewing is the most difficult process to automate because garment materials are flexible and irregular. Other processes — cutting, washing, dyeing, etc. — can all be automated.

According to research from Institut für Textiltechnik and other institutions, solving sewing automation would yield the most significant efficiency gains, reducing labor by 21%-46%.

In other subsectors, we also see industrial robot opportunities. For example, FreeS Fund portfolio company Xingzhixing focuses on wall-climbing robots, with core technical expertise in magnetic adhesion and high-pressure water jet-based wall-climbing robot bodies and components, plus extensive industry experience in shipping and petrochemicals. Through long-term co-development with benchmark customers, Xingzhixing has launched industry-leading comprehensive solutions that fully meet customer needs.

III. What Can China's Industrial Robot Industry Learn from the "Big Four"?

01 The History of the "Big Four"

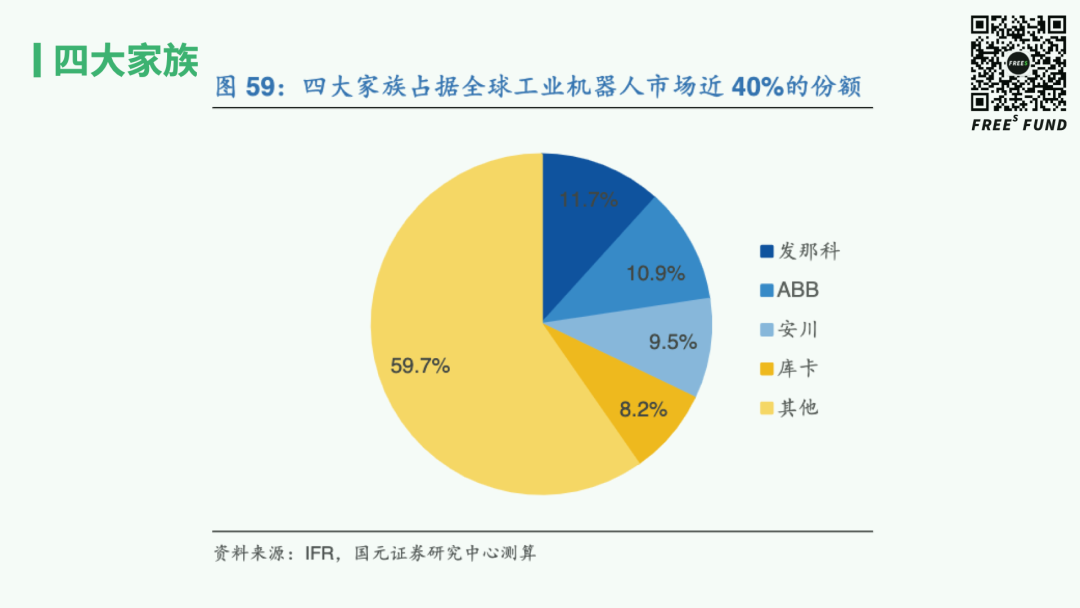

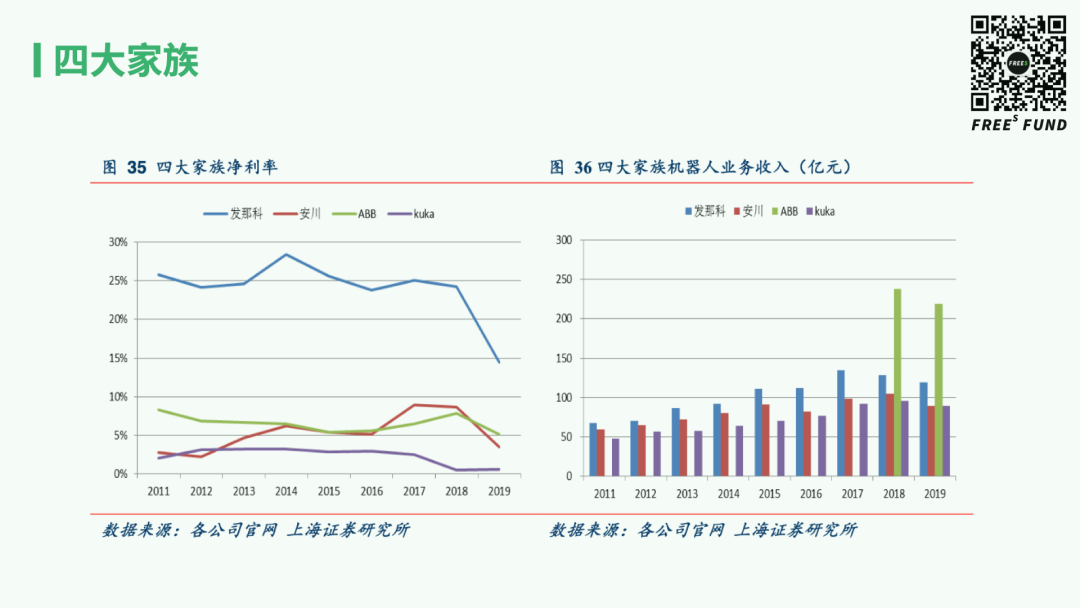

Any discussion of industrial robots must address FANUC, ABB, Yaskawa, and KUKA — the "Big Four." They hold roughly 40% global market share, and even higher in China at nearly 50%.

Let's trace the history of the "Big Four."

FANUC was founded in 1956 and became the world's leading CNC systems manufacturer, reaching the top position among CNC integrators by 1971. FANUC has three core businesses: industrial automation, robots, and intelligent tools — all centered on CNC systems, creating synergies and scale effects. FANUC's CNC products still hold over 50% global market share, with many competitors purchasing and using its CNC technology.

Swiss-Swedish company ABB is a massive industrial conglomerate with two main businesses — electrification and industrial automation — which gives it high revenue. Its core products are electric motors and automatic control systems. ABB used to have a power grids business, which was spun off in 2018.

Yaskawa Electric was founded in 1915 and was Japan's first company to manufacture servo motors. With over a century of accumulated motor technology, it pioneered the concept of mechatronics.

KUKA was established in Germany in 1898. In 1973, it developed the FAMULUS industrial robot based on modifications to the American Unimate. KUKA took system integration in the automotive sector to the extreme — starting with robot bodies and extending upward into components.

Let's look at their founding technologies first. FANUC started from the most fundamental technology in industrial robots — CNC systems. Yaskawa and ABB mainly focus on controllers and motors. KUKA started from welding equipment and primarily builds robot bodies, making it the purest robot manufacturer of the four.

Now consider their industrial chain positioning. Besides reducers, FANUC, Yaskawa, and ABB are involved in nearly all components related to industrial robots, while KUKA basically only makes controllers and robot bodies.

02 Why can FANUC maintain high gross and net margins? What are KUKA's strengths and moats?

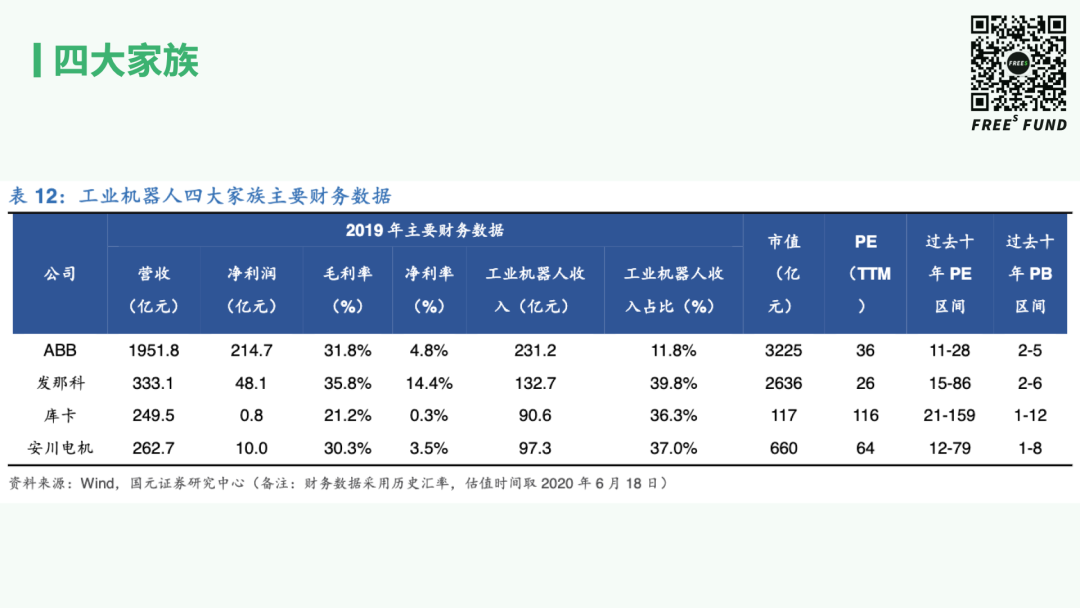

Having traced their histories, let's look at the "Big Four's" key 2019 financial data.

ABB has more diversified businesses and significantly higher revenue than the other three, but industrial robots account for only 11.8% of its sales. The other three have similar industrial robot revenues, with that segment representing 30% to 40% of total sales.

But the "Big Four" show considerable divergence in net and gross margins. FANUC leads by a wide margin in both, while KUKA "pales in comparison" with a net margin of just 0.3% — barely profitable at all.

This pattern has persisted for years. Data compiled by Shanghai Securities Research Institute shows that from 2011 to 2019, FANUC's net margin consistently outpaced Yaskawa, ABB, and KUKA. In 2018 and 2019, KUKA's net margin was so low it was practically negligible.

What drives FANUC's high margins?

This owes much to several of FANUC's operating principles.

First, never build customized products — only produce standardized, general-purpose products. This principle, established by FANUC founder Seiuemon Inaba, is baked into the company's DNA. FANUC places enormous emphasis on generalization, standardization, and scale.

Second, with the exception of reducers, components (control systems and servo systems) are largely made in-house, raising technological barriers.

Third, components are shared across different product lines, and downstream customer bases for different products are strongly interconnected.

These principles create synergies and scale effects, enabling FANUC to achieve higher margins. At the same time, its substantial high-margin software business pushes its net margin far above peers.

FreeS Fund Perspective

What we can learn from FANUC: First, core technology matters — and the more fundamental the technology, the greater the advantage. FANUC's CNC technology for machine tools sits at a more foundational layer than the motor technologies of ABB and Yaskawa Electric. Second, emphasize product generalizability. Third, synergies and scale effects are crucial. Additionally, software can improve a company's margins.

Despite its weak profitability, KUKA — one of the "Big Four" — has formidable strengths.

KUKA has gone deep into automotive manufacturing, where it is undisputedly number one in automation. Virtually every major automaker is its customer.

KUKA does several things well: First, it provides customers with full-lifecycle services, expanding vertically to cover engineering design, process planning, project management, after-sales service, and every other stage. Second, it builds complete production lines for customers, expanding horizontally — rather than selling point solutions, it sells robots across the entire production line, which also creates certain synergies.

FreeS Fund Perspective

For Chinese industrial robot companies, KUKA's lesson is that industry expertise matters enormously. In downstream integration and applications, the biggest barrier is industry-specific know-how — you must have deep domain knowledge, customer relationships, and so on. You need to lengthen your service chain, both vertically and horizontally. Vertically means adding service stages; horizontally means broadening your product portfolio.

Closing Question

What opportunities do you see in the industrial robot sector?

Feel free to leave a comment below, or continue the conversation with us. Contact: Yao Yuan, Vice President at FreeS Fund, yaoyuan@freesvc.com

▲ Philanthropy, Calls to Action, Bottom Lines, and Temptation: A Startup's Playbook for Public Crises | FreeS Business School

What Did Minister Miao Wei Actually Say About Chinese Manufacturing? | FreeS Research

Li Feng Column 14: Why Should We Thank Chinese Manufacturing?

How to Invest in Industrial Robots? | FreeS Research — Learning from Investing

FreeS Report 19 | The Era of Pleasant Buzz: Where Are the Opportunities in Low-ABV Alcohol Startups?