Frees Fund Report 18: Reflections Amid the Stock Market Rally — Where Are the Opportunities in Fintech? | Frees Fund

Our money is rushing toward new financial assets.

On July 23, A-share trading volume once again broke through one trillion yuan, marking the sixteenth consecutive trading day above that threshold. On one hand, the across-the-board surge reflected euphoric market sentiment; on the other, debate continued over whether this was a structural bull market or a full-blown rally.

Yet some trends had already become fairly clear. For instance, product issuance by domestic institutional investors, particularly public funds, was accelerating — equity fund issuance in the first half of 2020 jumped 224% year-over-year; securities firms were seeing notably higher account openings; and institutional investors representing long-term capital, such as insurers and pension funds, were entering the stock market at a faster clip.

Meanwhile, over the past quarter, a flurry of policies had been rolled out:

- March 1: The new Securities Law took effect, fully implementing the registration-based IPO system

- April 1: Foreign ownership caps on securities firms and fund management companies were formally lifted nationwide

- April 9: The State Council issued guidelines on building more robust market-based mechanisms for factor allocation

- June 12: The CSRC and related bodies released rules for ChiNext reform and the pilot registration-based IPO system

- June 27: News emerged that the CSRC planned to grant securities licenses to commercial banks

- July 15: A State Council executive meeting announced the removal of industry restrictions on insurance funds' financial equity investments

- July 19: The People's Bank of China and CSRC approved interconnectivity between the interbank and exchange bond market infrastructures

Regardless of how long this bull market lasts, there is no doubt that under policy guidance, the asset allocation of the entire population is in the midst of a long-term transformation. In fact, this shift did not begin with the current surge — the asset transition has been imminent for some time.

Over the past several years, FreeS Fund has been tracking innovation in fintech. Based on our observations and investment experience in this space, we will explore three key questions in this piece:

- Why is China at the starting point of an asset transformation wave? What factors are driving this transition?

- Looking at the past 50 years of U.S. capital markets, what structural opportunities exist in asset management and wealth management?

- Drawing on American experience and Chinese realities, what trends will shape domestic capital market development? What entrepreneurial (and investment) opportunities lie in fintech?

Before diving in, here are four conclusions:

- Driven by the triple forces of individual asset allocation demand, a shifting macroeconomic growth engine, and financial institution business transformation, the asset transition of societal wealth is an inevitable trend.

- China's capital market today closely resembles that of the U.S. in the 1970s. Drawing on decades of American capital market development, and with the boost of technological and financial innovation, the majority of Chinese household capital will likely flow into equity-based financial assets — primarily stocks, funds, and insurance.

- Using manufacturing innovation as an analogy for capital market evolution, we find that industrial upgrading follows a similar logic: division of labor, digitization, automation, intelligence, and personalization are trends highly likely to materialize.

- Given the massive market created by asset transformation and the transformation pressure on licensed financial institutions, fintech entrepreneurial opportunities in China far exceed those in the U.S. FreeS Fund will focus on innovation in asset management and wealth management.

This article will address the following questions in turn:

1. China at the New Starting Point of the Asset Transformation Wave

2. The Turning Point in U.S. Capital Markets: 1970

2.1 1920s–1960s: A Chaotic Germination Period

2.2 1970s: The Year of Inflection

3. China's Capital Market Today Resembles 1970s America

3.1 Funding side: The growing scale and wealth management needs of middle-class clients

3.2 Asset side: The shift from infrastructure and manufacturing to high-tech, high value-added sectors

3.3 Financial institutions and regulation: Cutting off old paths, building new ones

3.4 Changes underway in China's capital market

4. U.S. Financial Innovation Cases from the 1970s Onward and Their Relevance

4.1 1970s: The rise of asset management capabilities and Vanguard's emergence

4.2 1990s: The rise of wealth management and Charles Schwab's successful transformation

4.3 2000s opportunities: Robo-advisors, quantitative investing, and risk management

4.4 Summary of U.S. capital market development from 1970 to present

5. Innovation Opportunities in China's Capital Market Fintech

For your reference, in hopes of offering a different analytical angle. We look forward to continued exchange with entrepreneurs and industry experts in finance. Please contact Pengqi Liu, Vice President at FreeS Fund, at pengqi@freesvc.com. You may also add FreeS Fund's WeChat account (ID: freesfund) to reach us.

Fintech in the Asset Transformation Wave By Pengqi Liu (pengqi@freesvc.com)

**/ 01 / ** One Conclusion: China Stands at a New Starting Point of the "Asset Transformation Wave"

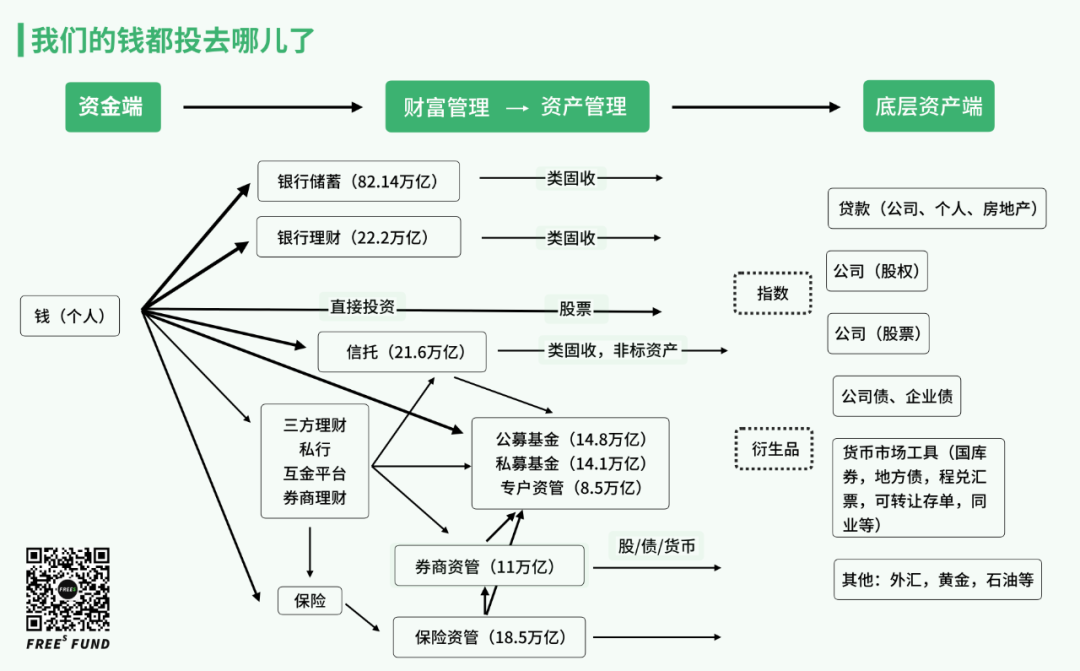

Let's first use a simple diagram to understand the concept of asset allocation. In essence, the money in our hands flows through various financial intermediaries — banks, securities firms, insurers, funds, trusts — to ultimate funding recipients. Asset allocation refers to the process by which this capital, through different types of financial institutions, takes various forms (loans, bonds, stocks, etc.) and proportions, and is deployed into underlying assets (real estate, corporations, local government debt, etc.).

So where has our money actually been allocated?

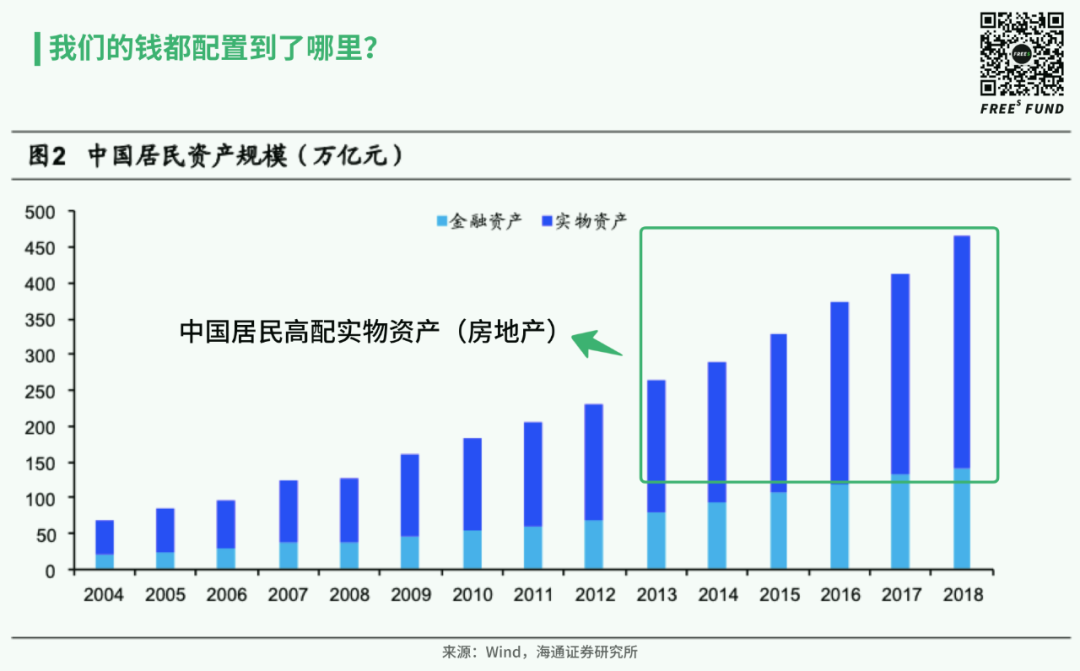

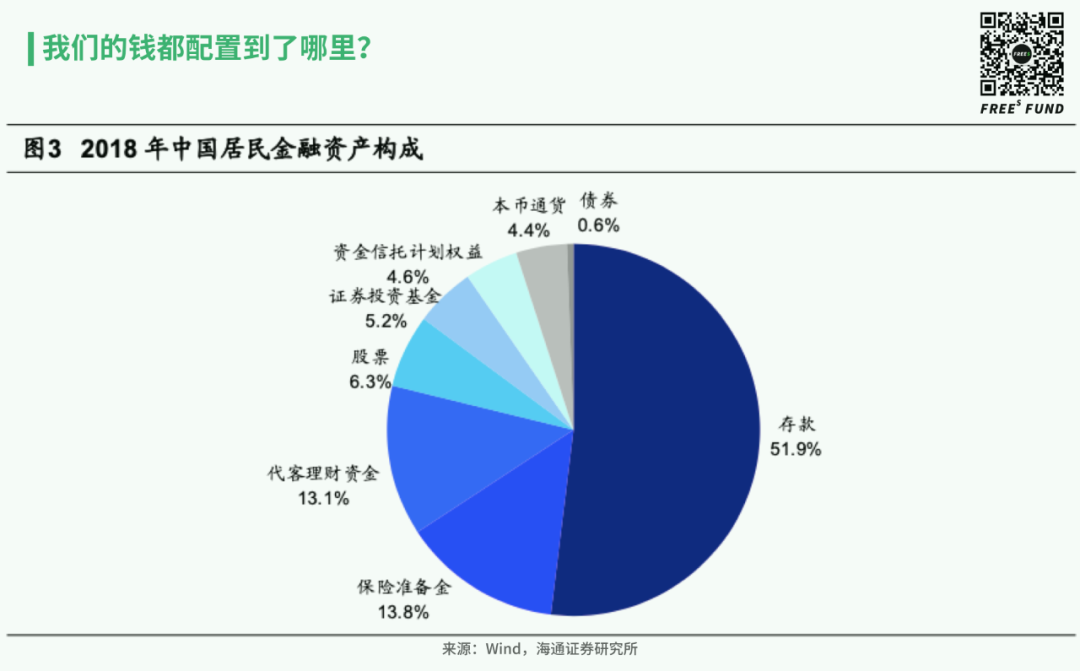

At the top of the list are real assets, primarily real estate. According to estimates by Haitong Securities Research Institute, as of end-2018, real estate accounted for approximately 70% of Chinese household wealth, while financial assets comprised roughly 30% — with half of that in principal-protected financial products, namely deposits.

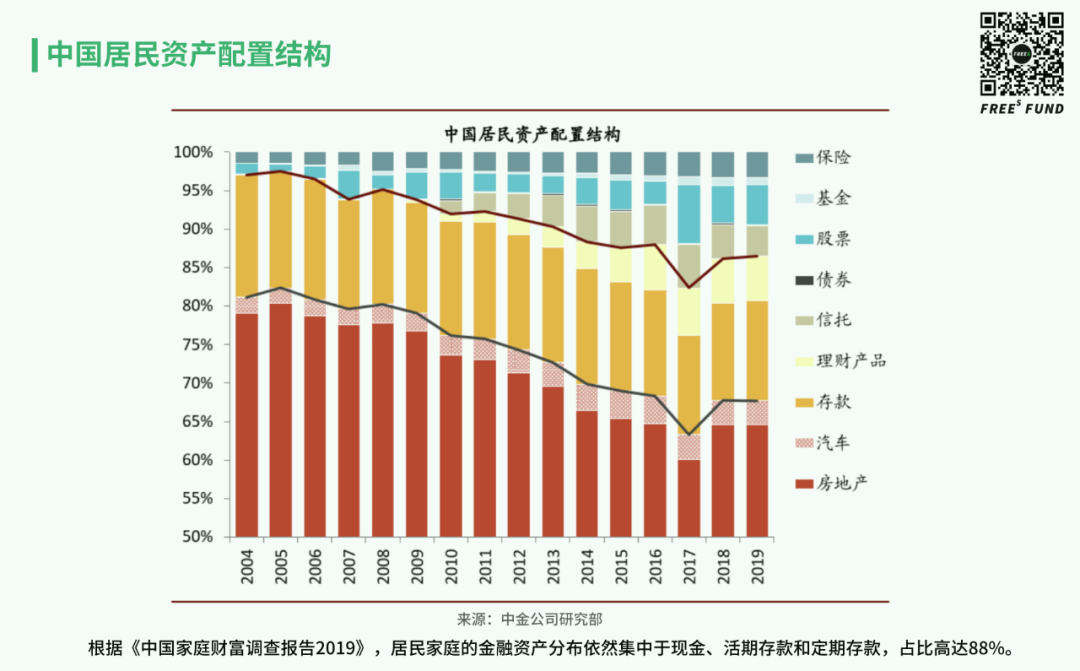

A survey of over 30,000 urban household balance sheets conducted by the People's Bank of China in October 2019 across 30 provinces, autonomous regions, and municipalities yielded similar results: financial assets accounted for a low share of household assets at just 20.4%.

Despite differing statistical definitions and data sources, both point to a similar conclusion: Chinese household assets are overly concentrated in real estate, with financial assets accounting for a relatively small share.

This situation is almost exactly the inverse of the United States. Data from Haitong Securities Research Institute shows that as of 2018, approximately 70% of U.S. household assets were financial assets, with stocks and investment funds at 32%, insurance and pensions at 23%, and real estate at just 24%.

Looking back at history, American household asset allocation also underwent a transition from real estate to financial assets. We believe that the American capital market of today is, in all likelihood, China's tomorrow. This implies that going forward, our capital deployment will increasingly shift from real estate and principal-protected assets (indirect financing) toward equity-type risk assets (direct financing, stocks, bonds, etc.).

This is our forecast for China's "asset transformation." Going further, we believe that within this hundred-billion-yuan-scale reallocation of assets lies enormous opportunity. And right now, we stand at the new starting point of China's asset transformation wave.

To validate this view, let us look back at history together and examine how American capital markets completed their asset transformation over the past several decades.

Food for Thought

Q: When robo-advisors emerged in the U.S., China also saw companies built around the robo-advisor concept, but mainstream opinion at the time largely dismissed them as "unreliable." Why? Feel free to hit "Like" at the end of this article, and reply "finance" in our official account backend to receive our preliminary answer.

**/ 02 / ** The Turning Point in U.S. Capital Market Development: The 1970s

▍1920s–1960s: A Chaotic Germination Period

Before the 1929 crash, U.S. capital markets were in a chaotic germination period. On one hand, the economy was growing rapidly, massive amounts of capital were flooding into the stock market, and equity investment had become an important investment vehicle for the American public. On the other hand, behind the stock market boom, high leverage and margin trading were all the rage. Against the backdrop of universal banking, banks took the lead in launching mutual funds, using leverage to inflate a bubble. Speculation dominated, and the entire market was exceptionally overheated.

After the 1929 crash, the U.S. entered the Great Depression. During the economic correction, a series of major laws were enacted to strengthen regulation:

The Glass-Steagall Act of 1933 gradually established the separation of financial industries. The Securities Act of 1933 and the Securities Exchange Act of 1934 set rules for stock issuance and trading. The Investment Advisers Act and the Investment Company Act, introduced in 1940, regulated investment advisers and investment funds respectively.

These laws provided initial regulation for the two major fields of wealth management and asset management. Thereafter, the U.S. entered an era of separated operations.

During this strong regulatory cycle, banks basically had no wealth management business. Securities firms could only conduct traditional commission business and rarely participated in asset management. In the same period, having lived through the economic crisis, people's concerns about uncertainty grew stronger, demand for property protection increased, and funds and insurance became more attractive.

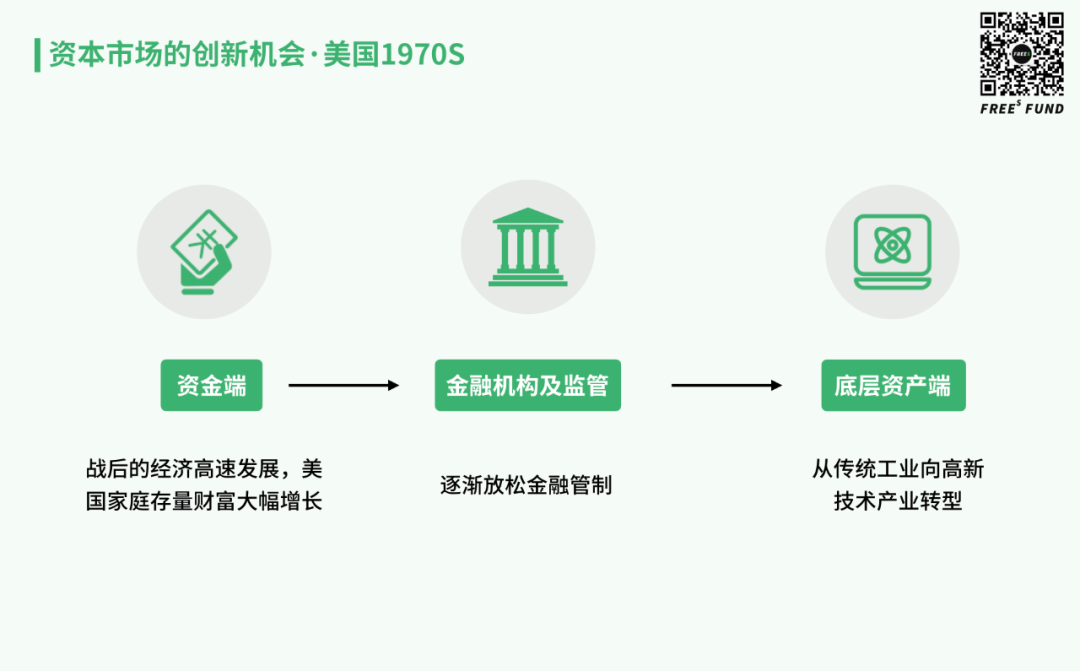

▍The 1970s: The Turning Point

Why were the 1970s a turning point? Let's look at three aspects — the capital side, the underlying asset side, and financial institutions and regulation.

- Capital side: Post-war rapid economic development led to massive growth in U.S. household wealth

After the 1970s, America's "Baby Boom" generation (those born between 1946 and 1964) began entering young adulthood. In 1978, U.S. per capita GDP reached $10,587, breaking the $10,000 threshold for the first time. The population base with wealth management needs and the demand itself rose substantially.

And the "401(k) plan" introduced in the early 1980s (where companies establish accounts for employees, which are then managed by professional asset management firms and can be invested in most financial products on the market including mutual funds, bonds, and stocks) essentially channeled enormous amounts of money into long-term investment in financial markets. This gave enormous impetus to the development of the U.S. asset management industry, particularly the fund industry, and catalyzed the vigorous growth of the wealth management industry.

- Underlying asset side: Transition from traditional industry to high-tech industry

From the mid-1960s to the early 1970s, affected by internal and external political and economic turmoil, the U.S. experienced successive dollar crises, economic development was hindered, and the country was mired in deep stagflation.

To address the unfavorable situation, in 1971 the U.S. government began implementing the "New Economic Policy," introducing a series of measures including tax cuts and economic restructuring. The U.S. economy began transitioning from traditional industry to high-tech industries (such as electronic computers), catalyzing rapid development in the securities market.

- Financial institutions and regulation: Gradual deregulation of financial controls

At the same time, the U.S. government gradually relaxed financial controls — liberalizing exchange rates and interest rates, broadening the scope of business operations for institutions, and allowing different financial sectors to cross over in their business activities.

Take interest rate liberalization as an example. After the separation of industries in the 1930s, the proportion of interest income for U.S. commercial banks rose year by year. After the 1970s, the U.S. gradually liberalized exchange rate and interest rate controls, and the degree of financial marketization continuously increased. Under the dual pressure of narrowing interest spreads and a relaxed regulatory environment, intermediary businesses represented by wealth management began developing rapidly, and non-interest income rose sharply.

The liberalization of securities commissions produced similar results. The 1975 amendment to the Securities Exchange Act triggered a commission price war in the securities industry, with all parties drastically cutting commissions to compete for high-net-worth clients. Brokerage revenue as a proportion of total operating income for securities firms continuously declined, forcing them to begin developing diversified businesses such as wealth management and asset management.

China's Capital Market Today Closely Resembles the U.S. in the 1970s

Why do we say this? Let's follow the same logic as above and compare point by point.

Capital side: The scale of middle-class clients and wealth management demand has increased significantly

In January 2020, the National Bureau of Statistics announced that China's total GDP in 2019, converted at the annual average exchange rate, reached $14.4 trillion, with per capita GDP reaching $10,276, breaking the $10,000 threshold. Like the U.S. in the 1970s, this important milestone means that the scale of high-net-worth clients in China is growing larger, and correspondingly, wealth management demand is also increasing significantly.

So where is this capital appropriately directed?

We can see that yields on fixed-income products have been consistently declining. Take Yu'e Bao as an example: its seven-day annualized yield once broke through 6%, and its assets under management peaked at 1.69 trillion yuan in 2018. However, its yield has now basically fallen below 1.5%, lower than the benchmark one-year bank deposit rate. From 2017 to 2019, Yu'e Bao's AUM also showed a consistent downward trend, at 1.58 trillion, 1.13 trillion, and 1.09 trillion yuan respectively.

Affected by the COVID-19 pandemic and other factors, in Q1 2020, as of March 31, Yu'e Bao's AUM was 1.26 trillion yuan, 170 billion yuan higher than at the end of 2019. This shows that against the backdrop of global financial market volatility and risky asset fluctuations, people simply don't know what products to put their cash into — residents face an asset shortage in their allocation.

Against the multiple backdrops of liquidity flooding, declining yields on fixed-income-like products, the shutdown of P2P lending, and the real estate cycle peaking, how the middle class should allocate assets has become an obvious question.

Asset side: Transition from infrastructure and manufacturing to high-tech, high value-added industries

Over the past forty-plus years, especially since reform and opening up, the driving forces of China's economic development have mainly come from infrastructure, real estate, and full-factor, full-chain manufacturing. These industries mostly carried lower investment risk and had relatively good return guarantees. Their corresponding financing method was primarily the bank-dominated indirect financing system — that is, the model of taking deposits and making loans to channel money into the aforementioned industries.

This was the logic by which the financial system supported real economic development over past decades, and it did indeed drive China's sustained high growth. However, as economic development enters the new normal, we are transitioning from infrastructure and manufacturing to high-tech, high value-added industries.

The question before us is: Can private enterprises and small and medium enterprises in industries including 5G, AI, big data, industrial internet, and new energy — all within the scope of "new infrastructure" — rely on the traditional indirect financing loan model to develop, as infrastructure and manufacturing industries did in the past? In fact, it's not that easy. Moreover, if this is merely mandated in the form of policy targets, the results will likely be discounted.

Therefore, developing a direct financing system is an inevitable choice. The launch of the STAR Market and the registration-based IPO system also reflect the state's desire to bring high-quality assets aligned with new industrial directions into the market, encouraging more capital to enter capital markets through diversified channels and improving investment and financing efficiency.

More high-quality companies going public can also provide excellent investment targets for residents, allowing them to share in the dividends of corporate growth.

Financial institutions and regulation: Cutting off old paths and building new ones

In recent years, to better support the transition in financing methods, a series of policy measures can be summarized in two points — cutting off old paths and building new ones.

The most typical measure is interest rate liberalization. Interest rates are the anchor for all assets; interest rate liberalization is the foundation for the marketization of all types of financial assets. Through the LPR (Loan Prime Rate) reform, the interest rate spread that originally supported bank profits — the most important source of bank revenue — has been made market-based and more flexible. After spreads narrowed, banks could no longer make easy money through traditional business, and were compelled to develop other new businesses.

There's also the gradual implementation of new asset management regulations. Let's look at a few examples:

In March 2020, the China Banking and Insurance Regulatory Commission (CBIRC) issued the Measures for the Administration of Insurance Asset Management Products, which clarified that: the balance of non-standardized debt assets invested by all combination products managed by the same insurance asset management institution shall not exceed 35% of the net assets of all combination products managed by it at any point in time.

Recently, the CBIRC also raised the maximum proportion of insurance funds that can be allocated to equity assets from the previous 30% to 45%.

The purpose of this series of regulations is precisely to "encourage insurance asset management institutions to raise funds through the issuance of insurance asset management products to support economic structural transformation, support market-oriented, rule-of-law-based debt-to-equity swaps, and reduce corporate leverage ratios."

In May 2020, the Measures for the Administration of Trust Company Fund Trusts (Draft for Comments) also restricted the proportion of investments in non-standard debt assets, clarifying that the total amount of all collective fund trusts invested in non-standard debt assets shall not exceed 50% of the total paid-in trust of all collective fund trusts at any point in time.

Given that fund trusts have traditionally been "heavy users of non-standard assets," these regulations will have significant impact on the industry. On one hand, this will to some extent cut off "restricted industries" that sought to use trusts for financing, such as real estate. On the other hand, it will also accelerate the transformation of trust companies.

At bottom, whether cutting off old paths or building new ones, everything serves one purpose — serving the transformation of assets.

Changes happening or about to happen in China's capital markets

Whether it's our personal capital allocation needs, the needs of macroeconomic development momentum, or the business transformation needs of financial institutions, all are basically converging at the same intersection, making asset transformation an inevitable trend.

Money will inevitably flow into new financial assets.

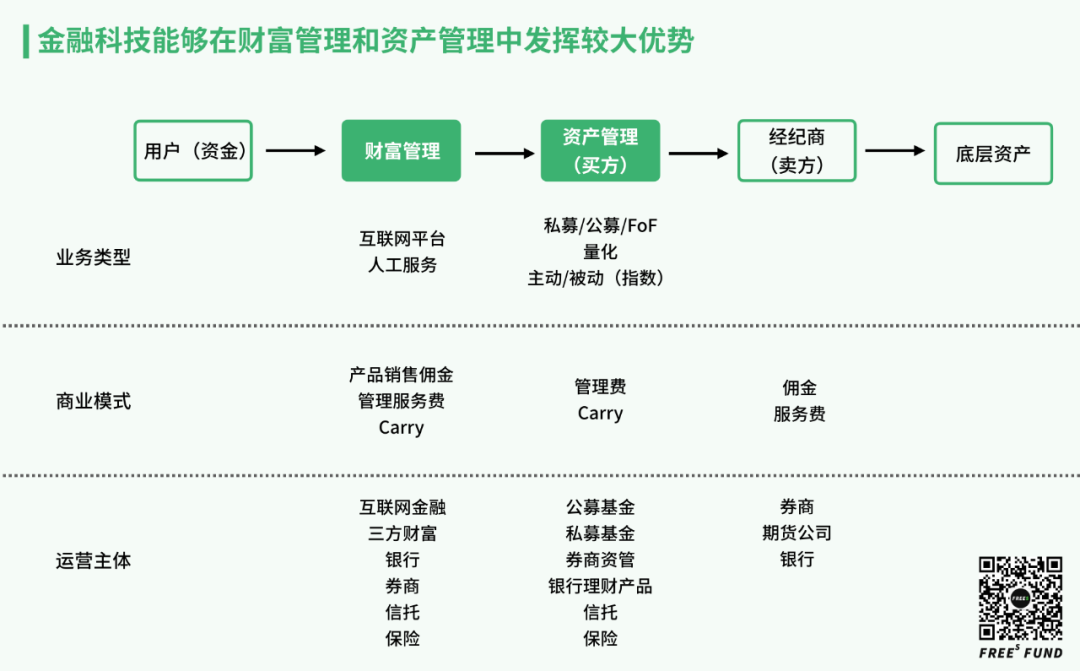

Change often breeds opportunity. As two important links in the financial industry chain, how should wealth management firms and asset management firms seize this opportunity?

Asset management firms are primarily responsible for taking underlying investable assets — think of them as raw materials — and processing them into financial products in various forms to meet market demand.

Clients with capital can invest in and purchase these financial products through wealth management firms, otherwise known as distribution channels, thereby achieving efficient capital allocation while injecting much-needed funding into the underlying assets.

Therefore, the capabilities of wealth management and asset management institutions directly determine the efficiency and scale at which money flows into these new asset classes. And fintech is bound to play a significant role in this process.

To summarize: if wealth management previously served mainly ultra-high-net-worth individuals, then in this new environment, advisory services need to address the growing mass of upper-middle-net-worth clients. On the asset management side, there needs to be a greater variety of products catering to different levels of return, risk, and liquidity — while these asset managers' internal operations and risk management capabilities must be strengthened.

Next, let's look back at the history of the US asset transformation to see what changed in American capital markets after the turning point of the 1970s, and which companies seized the opportunity.

US Financial Innovation from the 1970s to Today: Cases and Lessons

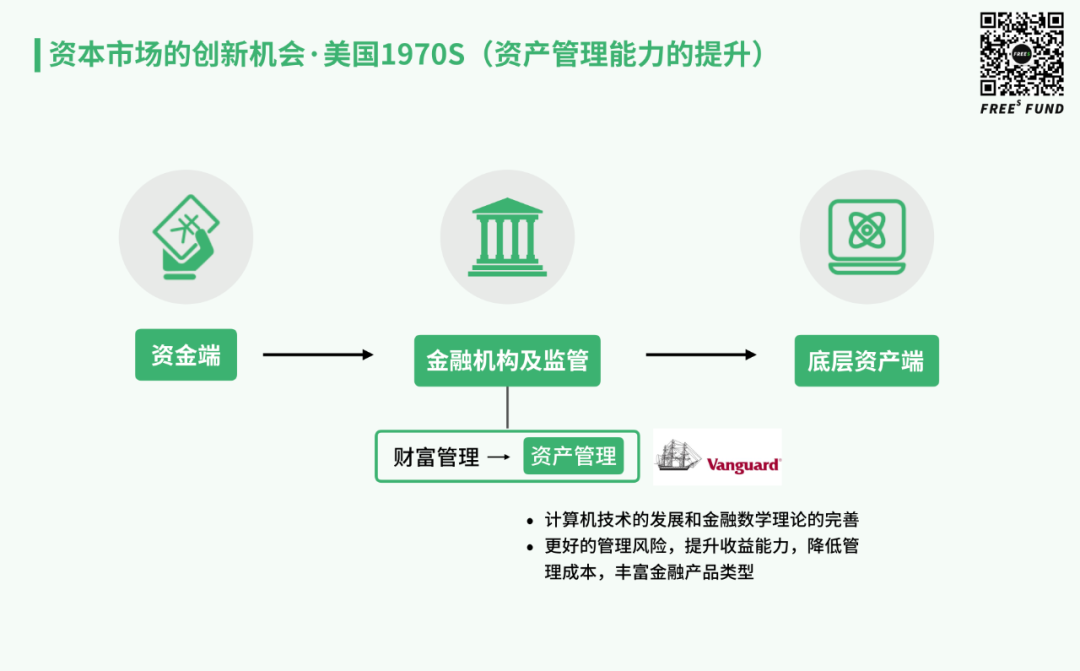

1970s: The Rise of Asset Management Capabilities

Benefiting from advances in computing technology and the refinement of financial mathematics, the wave of financial innovation that began in the 1970s brought significant improvements to asset management capabilities — better risk management, enhanced return generation, lower management costs, and a richer variety of financial products.

A few representative examples:

-

1971: NASDAQ was established, built on the Securities Dealers Automated Quotations system

-

1971: The first quantitative index fund was launched by Barclays Investment Management

-

1972: The first money market fund was created

-

1972: Foreign exchange futures were introduced, the world's first exchange-traded derivative. Interest rate futures, stock index futures, and options followed

-

1977: Barclays issued the first actively managed quantitative fund

-

From the 1970s onward, structured debt instruments (mortgage-backed securities, asset-backed securities) grew rapidly, and corporate bond issuance (high-yield bonds) expanded dramatically

-

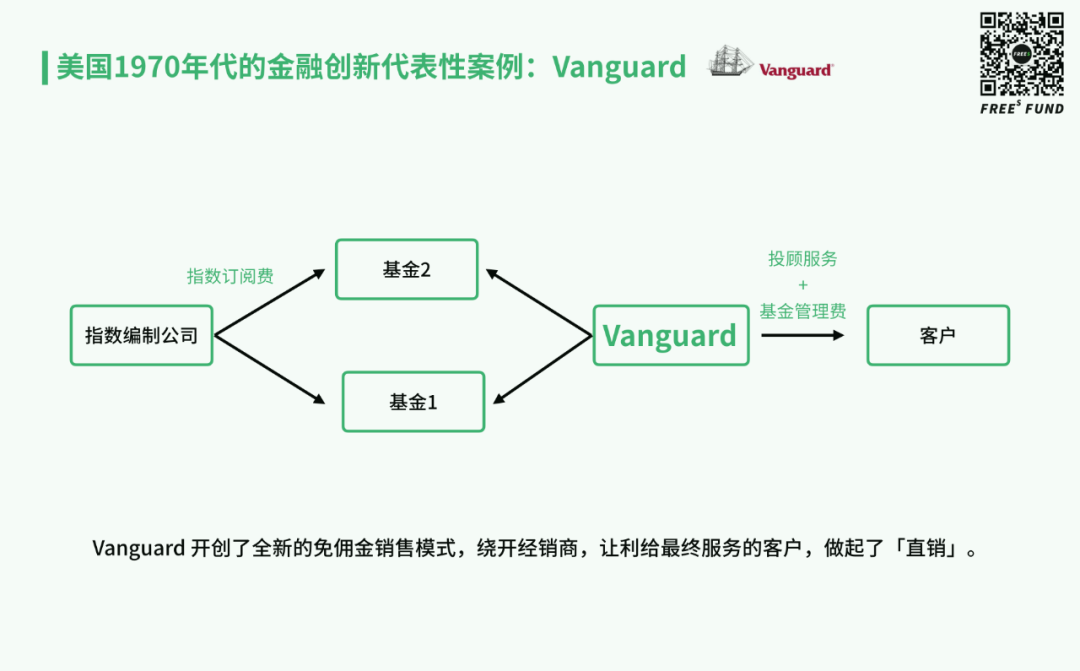

Case Study: Vanguard

Vanguard is one of America's largest fund management companies — the Vanguard Group, the world's largest mutual fund provider and second-largest ETF provider, and an asset manager renowned for its index investing.

As of 2019, Vanguard managed 319 mutual funds with total assets under management of approximately $5.7 trillion — a figure exceeding the combined total of all funds in China.

Vanguard's origins trace back to the Wellington Fund, founded in 1929, which evolved into the modern group structure in 1975. Beyond managing traditional funds, it pioneered a crucial model innovation.

At the time, the dominant fund distribution model in the US resembled China's current situation: channel sales, where fund companies paid commissions to distributors who then sold to end clients. But Vanguard was unwilling to share profits with intermediaries. It created an entirely new no-load sales model, bypassing distributors entirely and passing the savings to end clients — essentially going "direct."

Yet direct sales carry their own costs: building brand recognition and customer acquisition capabilities. Eliminating commissions was one lever; lowering management fees was another. To sustain low operating expenses, Vanguard pursued an index fund-centric strategy, launching its first index fund in 1976 (the Vanguard 500 Index Fund tracking the S&P 500). It was betting that index funds would become a major asset class.

The 1982 bull market and the 401(k) program turbocharged asset growth. By building and defending its low-cost moat, Vanguard won its bet. Entering the 1990s, as its fund offerings expanded and its wealth management footprint deepened, stock market funds including the S&P 500 Index Fund helped propel Vanguard to become one of the world's largest fund companies.

- Lessons from Vanguard

First, capital market development follows similar logic everywhere. Initially, retail investors trade actively. Then, as actively managed funds outperform retail investors, institutionalization rises, market maturity and efficiency improve, indices climb, and index funds inevitably become the primary vehicle for market participation.

Second, long-term capital inflows contribute enormously to the asset management industry — life insurance, annuities, and similar products become important allocation categories.

Third, changes in cost and distribution fee structures are critical to product innovation. Index funds effectively outsource investment research and risk management services. This creates opportunities for "pick-and-shovel" companies serving asset managers — B2B fintech service providers. A quintessential example is MSCI, whose core business model provides index subscriptions and research analytics services.

MSCI trades at roughly 50x P/E with exceptionally high gross and net margins; subscription revenue accounts for 74% of total revenue. If China can produce companies of this type, they would make highly attractive investment targets.

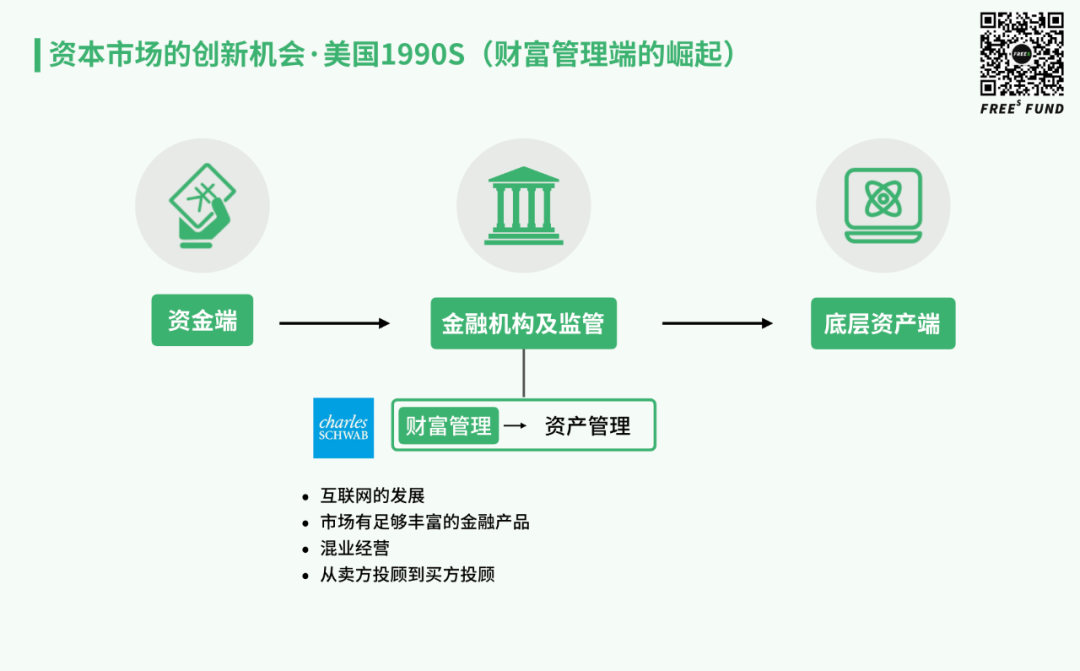

1990s: The Rise of Wealth Management

If the 1970s and 1980s saw computing technology drive upgrades in product design and risk management capabilities — with American financial innovation concentrated on the asset management side — then from the 1990s onward, the internet progressively closed the distance between consumer-facing platforms and institutions, creating the necessary preconditions for wealth management's ascent.

Additionally, the continued development of asset management firms brought sufficiently diverse financial products to market. This both reduced transaction costs and expanded market capacity, giving wealth management greater room to operate and the ability to attract and retain quality clients.

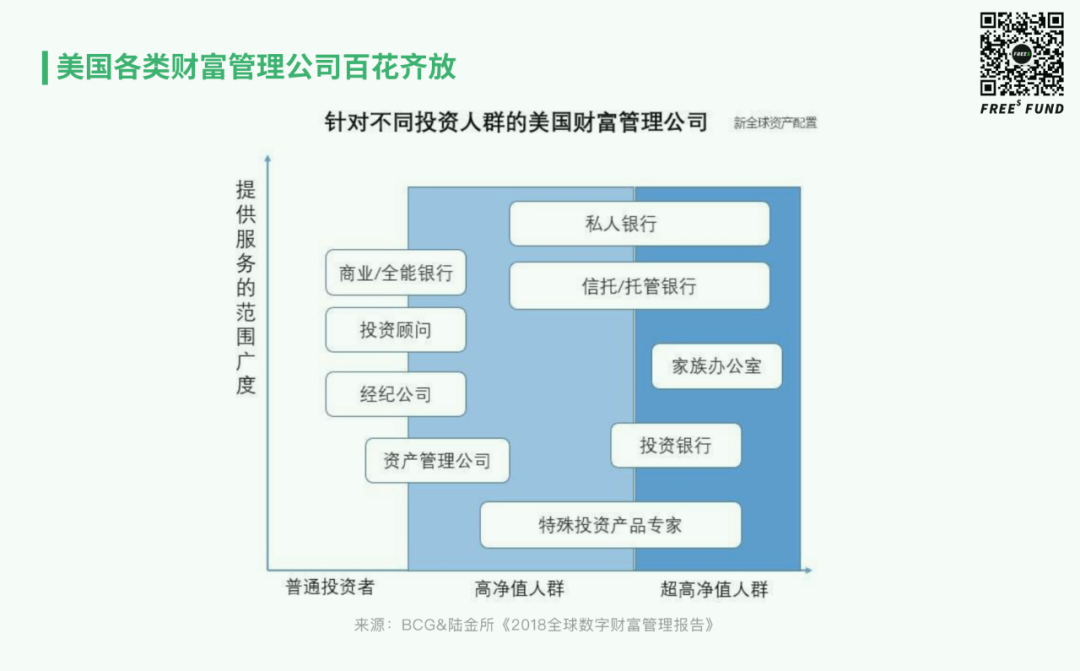

Another catalyst was the 1999 Gramm-Leach-Bliley Act, which once again permitted commercial banks to combine with investment banking operations, making multi-asset-class services more accessible. Various wealth management participants flourished — asset managers, broker-dealers, banks, independent advisors, private banks, family offices — each serving distinct client profiles, but collectively presenting a vibrant, multi-faceted landscape.

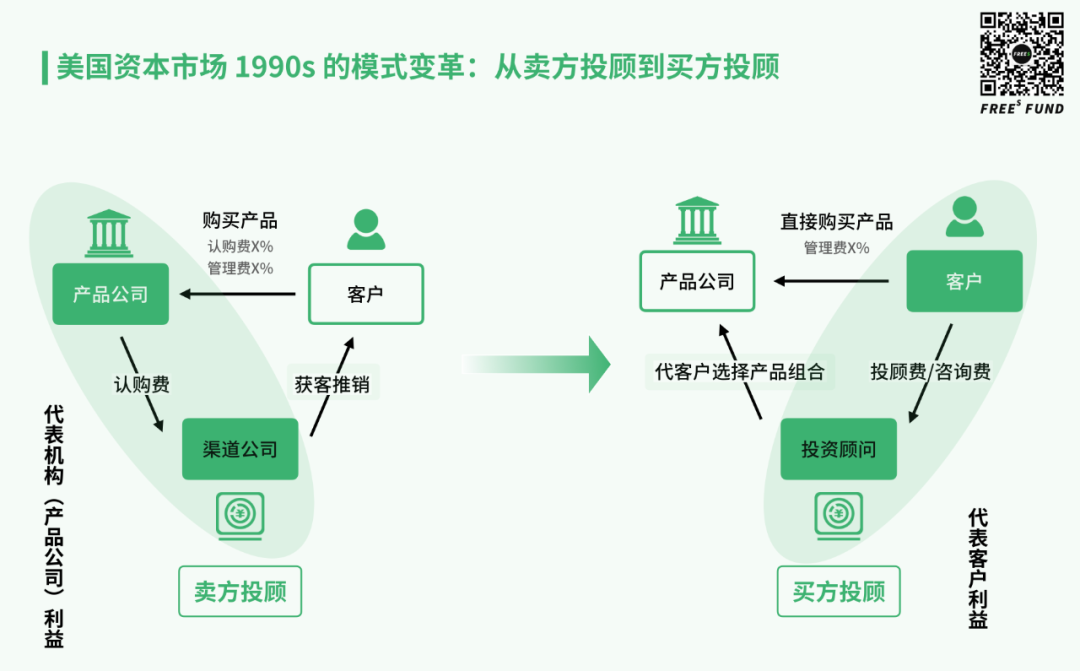

This environment also catalyzed an important model shift: from product-pushing to client-centered advisory.

As mentioned earlier, Vanguard's no-load fund model effectively eliminated traditional broker intermediaries. This objectively produced two consequences:

One, clients gained direct access to an increasingly rich array of products.

Two, as financial products multiplied rapidly and financial risks intensified, people grew dissatisfied with platforms' one-sided product pushing — the "seller's advisory" model. They urgently needed third-party investment advisors operating from the client's interests to help construct portfolios. Thus emerged and developed "buyer's advisory."

The earliest buyer-side advisors emerged around the 1970s, when insurance and securities agents and brokers gradually left institutions like commercial banks and insurance companies to establish or join independent broker-dealers, becoming independent agents. Free from institutional constraints, they had more latitude to recommend diverse products, but also had to build and maintain their own client bases. They began charging advisory fees rather than sales commissions, aligning their interests with those of their clients.

This trend accelerated after the 2008 financial crisis. Once-golden brands collapsed like dominoes, and large numbers of insurance and securities agents and brokers left their former employers to become independent. Today, there are over 13,000 registered investment advisor firms in the US, serving more than 43 million clients, over 90% of whom are individual investors.

For these buyer-side advisors to strike out on their own, strong client relationships are a prerequisite. But relationships alone aren't sufficient — they also need solid professional service capabilities and support from underlying asset supply chains.

However, not all independent advisors possess such strong professional capabilities. This gave rise to the TAMP (Turnkey Asset Management Program) model. By providing front-office independent agents with a "middle-office" system covering portfolio construction, trading, and product supply chains, TAMPs allow these advisors to concentrate on what they do best — developing and maintaining client relationships — thereby significantly improving their productivity and value-add.

- A Representative Success Story: Charles Schwab

Founded in 1971, Charles Schwab started out as a traditional brokerage. When fixed commission rates were abolished in the US in 1975, Schwab joined the discount brokerage race, slashing commissions by 70% to win customers. To sustain growth at such low commission levels, Schwab invested heavily in R&D — automating securities trading, enabling online order entry, and building out information systems to drive down transaction costs and protect margins.

This strategy paid off. By the end of 1985, Schwab had established nearly 100 physical branches, serving 1.2 million clients with $7.6 billion in assets under management, making it the largest discount broker in America. It listed on the NYSE in September 1987.

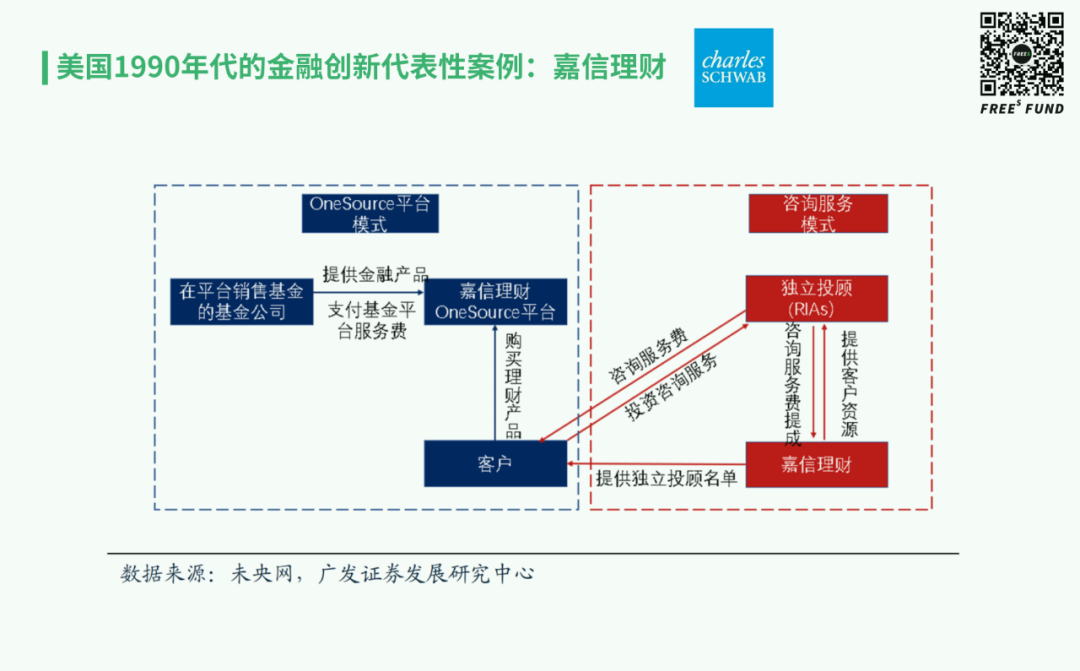

Shortly after going public, Schwab began pivoting toward wealth and asset management. Around 1990, it made two pivotal moves:

First, it created the OneSource platform (similar to Alipay's fund marketplace or East Money's fund supermarket), offering centralized mutual fund trading with no transaction fees for investors, while charging fund management fees to asset managers.

Second, leveraging OneSource, it strategically deepened partnerships with independent investment advisors, providing them with practice-building platforms and asset allocation tools. Investors paid advisory fees directly to the RIAs, with Schwab taking a cut as the platform provider.

From this point on, Schwab's revenue gradually shifted toward asset management fee splits and interest income, with trading commissions becoming a smaller share.

By the end of 2008, Schwab's total platform assets reached $3.25 trillion, of which $1.55 trillion was in TAMP accounts — representing 41.3% of the entire US TAMP market. It stands as an excellent case study of a brokerage successfully transforming into a wealth and asset management firm.

- Lessons from Charles Schwab

Drawing on the US experience, we can infer that fee-based advisory services represent one of the most viable paths for capital markets to develop effectively, aligning the interests of clients, wealth management firms, and asset managers. Huatai Securities Co., Ltd.'s successful acquisition and IPO of AssetMark further validates capital market confidence in this direction.

However, the development of fee-based advisory doesn't happen overnight. Timelines vary across markets, and three necessary conditions must be in place:

First, you need a sufficiently rich product offering. Second, you need a large base of educated clients. Third, you need professional service capabilities.

If asset management firms are responsible for producing products that meet diverse needs, then TAMP platforms can provide RIAs with professional support and product supply, helping them serve clients efficiently and with high quality.

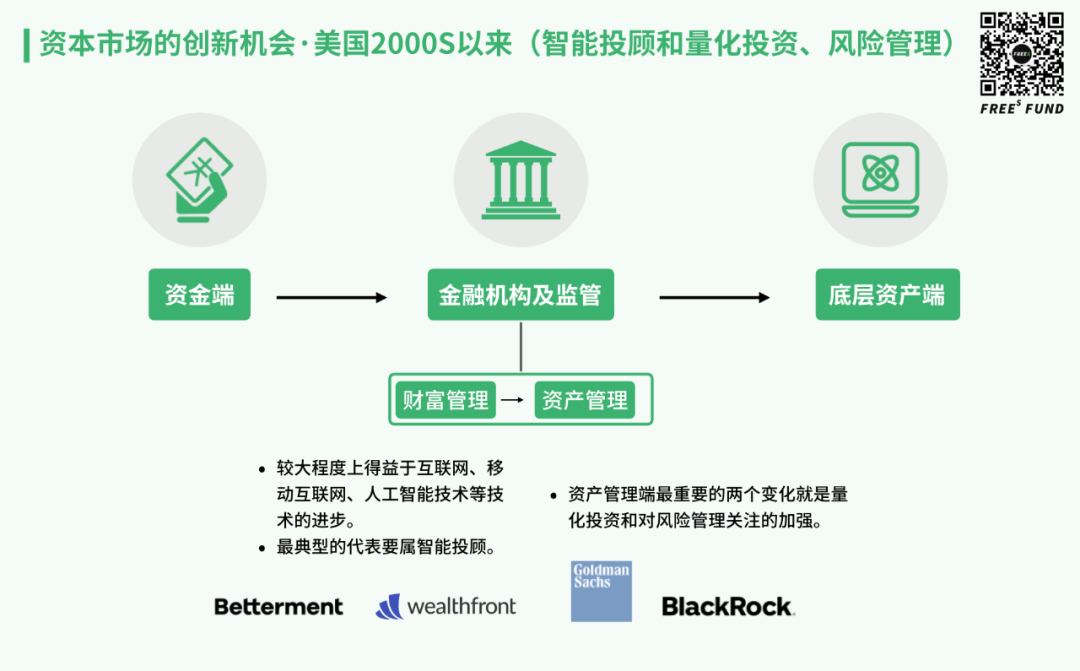

2000s: Robo-Advisors, Quantitative Investing, and Risk Management

- Wealth Management: Robo-Advisors

After 2000, innovation on the wealth management side was less about the essence of finance and more driven by technological advances — the internet, mobile internet, and AI. The quintessential example is the robo-advisor.

The pioneers were Betterment and Wealthfront. Both offered fully automated services covering client assessment, asset allocation recommendations, trade execution, and ongoing account maintenance.

Take Betterment: in theory, after logging in, users simply fill in personal information — age, income, retirement status, investment goals, and expectations — and the platform automatically generates a scientific, secure, effective, long-term stock and bond allocation plan. Users can see projected returns, risk coefficients, time horizons, and allocation percentages. Clients can also adjust stock-bond ratios within certain ranges based on their risk tolerance.

Robo-advisors offer two main advantages:

First, they lower the barrier to advisory services, reaching ordinary investors at lower fees. Second, by leveraging online behavior, they can better identify client risk preferences and respond more quickly.

As traditional financial institutions began pouring more resources into new technologies, many fintech companies were overtaken. After all, for many, entrusting investment decisions entirely to machines still feels uncertain at current technology levels. As a result, hybrid human-machine investment products became the industry mainstream.

In October 2016, Betterment launched Betterment for Advisors, expanding from its original consumer-facing business to serve B2B clients.

This service targets independent financial advisors, allowing them to build customized offerings for clients through Betterment, including portfolio options from Goldman Sachs and Vanguard. Through Betterment for Advisors, investment advisors can escape the manual drudgery of document and report preparation, freeing up more time for client communication.

- Asset Management: Quantitative Investing and Risk Management

After 2000, the two most important developments on the asset management side were quantitative investing and heightened attention to risk management.

Quantitative investing replaces human subjective judgment with mathematical models, using computer technology to uncover excess returns and formulate automated trading strategies. It dramatically reduces the impact of investor emotion and irrational decision-making.

Notable examples include Renaissance Technologies, founded in 1988 by a group of PhDs in mathematics and natural sciences, along with the more familiar names: Bridgewater, AQR, Citadel, and Two Sigma. Today, quantitative funds have become the mainstream of US hedge funds.

The second characteristic of this era was strengthened focus on risk management.

The first decade of the 21st century brought the dot-com bust in 2000 and the 2008 financial crisis, driving unprecedented attention to risk management among financial institutions. MSCI's 2004 acquisition of Barra — now the most widely used risk assessment tool among global financial institutions — was mentioned earlier.

Top global asset managers also built their own risk management systems, such as BlackRock's Aladdin and Goldman Sachs' SecDB. Taking Aladdin as an example, investors can use it to adjust portfolio characteristics, simulating specific market conditions or historical scenarios to project how portfolios would perform under those circumstances. Currently, asset managers overseeing more than $20 trillion globally use this system. SecDB is also credited with helping Goldman Sachs weather the 2008 financial crisis better than competitors.

It's also worth noting that with the evolution of data and AI technology, alternative data and intelligent investment research have begun playing increasingly important roles in the fiercely competitive US asset management industry.

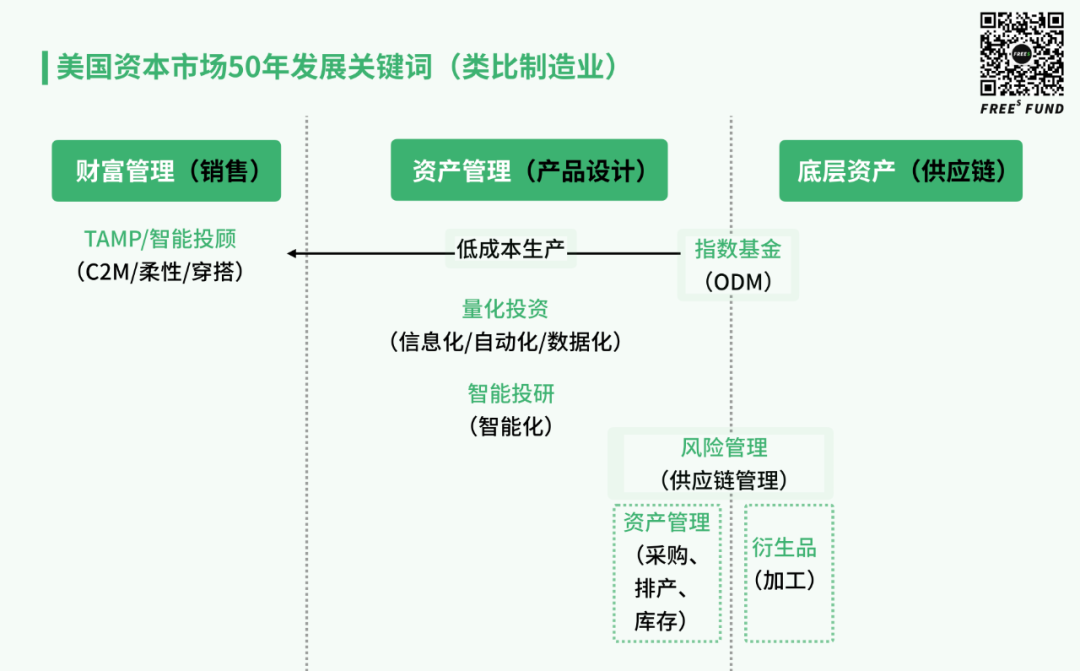

Summarizing 50 Years of US Capital Market Development

- Capital Market Development Logic Resembles Manufacturing Supply Chain Upgrades

Looking back at US capital market innovation and development since 1970, we can draw an analogy with structural upgrading in manufacturing.

Simply put, index funds are somewhat like ODMs (original design manufacturers) in manufacturing, providing outsourced research and risk control services. Quantitative investing can be understood as the automation process in manufacturing. Risk management maps to supply chain management — akin to procurement, production scheduling, and inventory risk control in manufacturing production. Similarly, when back-end supply chains (underlying assets) are sufficiently digitized and product design (asset side) is sufficiently rich, front-end sales (wealth management) can better achieve C2M (customer-to-manufacturer) — more precise, more flexible — enabling services represented by TAMPs and robo-advisors to be more effectively deployed.

Of course, this analogy isn't strictly precise, but the logic of manufacturing supply chain development can help us better understand how US capital markets evolved over the past five decades.

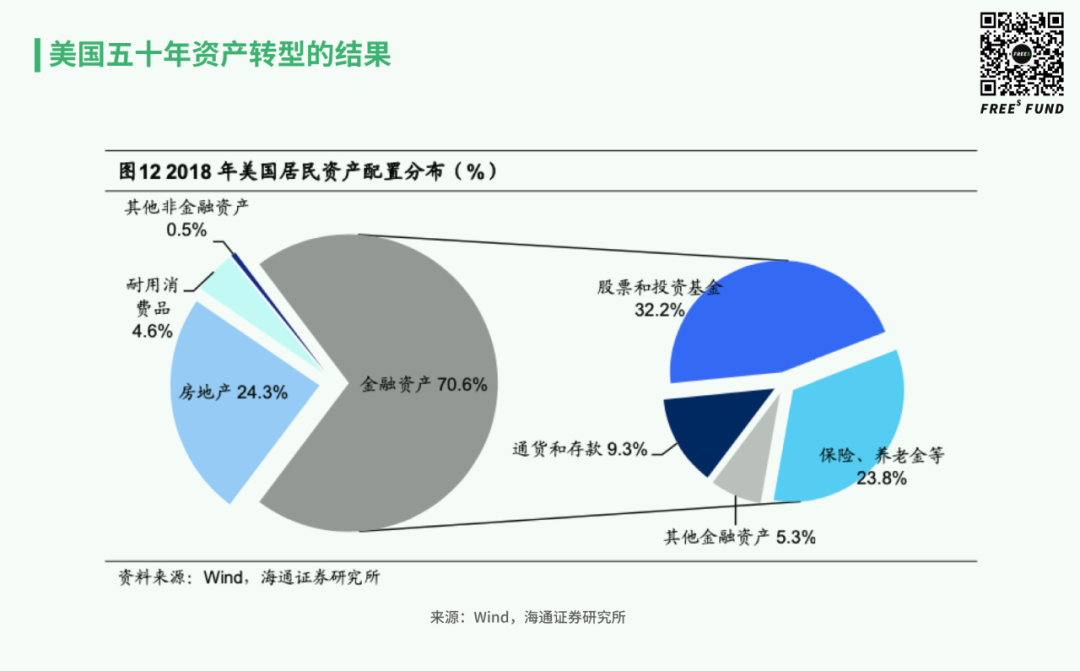

- The Outcome of Fifty Years of Asset Transformation in America

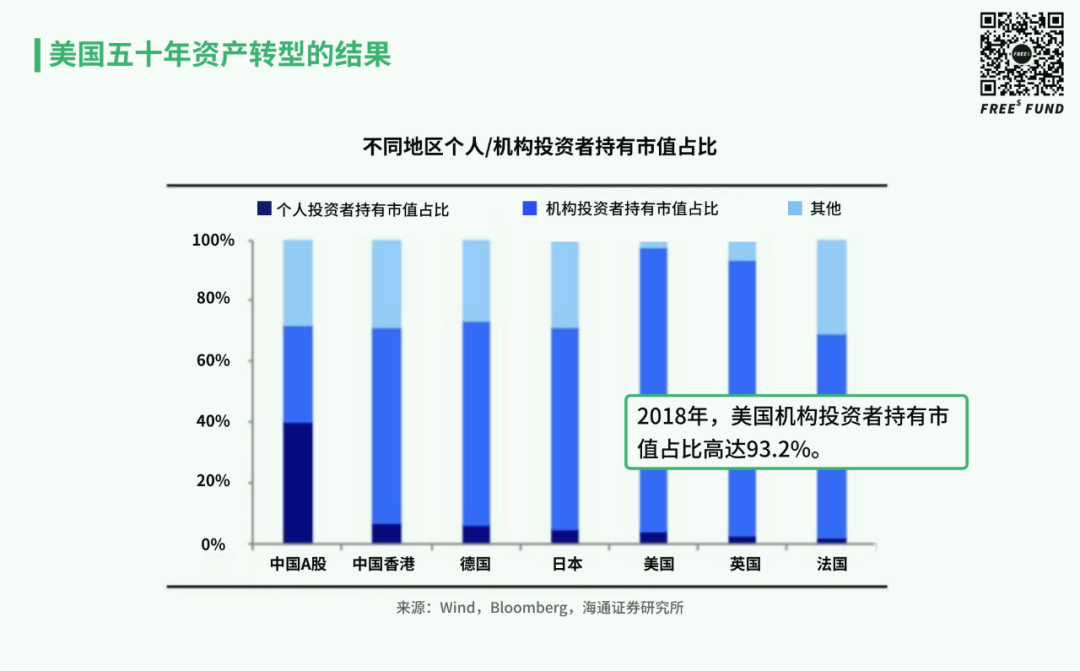

As of 2018, US household asset allocation was roughly 70% financial assets and 30% real estate and other assets. Financial assets were primarily distributed across stocks, funds, and insurance. Notably, according to Haitong Securities research, as of mid-2018, US institutional investors held 93.2% of total stock market capitalization, while individual investors held less than 6%. Mutual fund assets reached 114% of GDP (versus 14% in China).

From the 1970s and 1980s, when money flowed primarily into real estate, to today, where household financial assets far exceed other asset categories — America completed this asset transformation over several decades.

Innovation Opportunities in China's Capital Markets and Fintech

Since its founding, FreeS Fund has continuously tracked the fintech sector, having invested in over a dozen companies spanning consumer finance, supply chain finance, wealth management, asset management, financial big data, and insurtech.

We believe that as China's capital markets gradually open up, fintech entrepreneurship opportunities in China will far exceed those in the US.

This is partly thanks to China's massive market, its still rapidly expanding economy, and its fast-growing middle class.

On the other hand, it also stems from fundamentally different development logics for fintech in the two countries. In US capital markets, institutionalization was completed before the arrival of next-generation information technology. Competitive pressure meant most innovation emerged from within financial institutions themselves. Chinese financial institutions, by contrast, have long grown up under licensing and entry protections. They now simultaneously face intensifying market competition, foreign entry, and pressure from technological upgrading. Relying on external third-party fintech companies to rapidly achieve transformation and upgrading has become the mainstream approach — and this is the primary structural reason we are bullish on this direction.

Returning to our topic today, faced with this historic asset transformation opportunity, we believe the changes currently underway or inevitably coming in the future will concentrate in two main areas:

- Asset management: Providing products that meet clients' varying needs for returns, risk, and liquidity, while enhancing institutions' internal operations and risk management capabilities.

- Wealth management: Comprehensively upgrading service capabilities oriented toward client needs, particularly advisory services for the new middle class.

Specifically, on the asset management side, actively managed institutions and products will remain mainstream in the short to medium term. Because retail investors exist in large numbers, most funds still have the ability to outperform the market. Therefore, quantitative investment tools and better investment research/pricing and valuation/risk control/cross-asset risk management capabilities will become focal points for most financial institutions. This will involve applications including trade execution and management, financial engineering and quantitative computing, and new technologies such as AI and big data.

From a longer-term perspective, however, passive index investing will inevitably become mainstream. The main problem currently is the insufficient variety of available index products. Therefore, specialized index compilation companies targeting the China market have opportunities to grow. At the same time, financial derivatives as effective risk hedging tools have gradually begun to be accepted by the market and regulators, but domestic talent accumulation remains limited, and demand for system tools will become increasingly urgent.

One additional point merits special attention. The opening of financial markets increases market activity and efficiency while also amplifying risk, placing higher demands on regulatory capacity. To meet compliance requirements, financial institutions' own operating costs will rise — this is clearly evident from the EU's MiFID II and GDPR regulatory frameworks, and domestically, regulatory intensity may only be stronger. Therefore, whether for regulatory departments or financial institutions' self-inspection, using new technological means for intelligent regulation, compliance monitoring, and regulatory reporting is likely to become a major trend.

On the wealth management side, China still has a longer road ahead. However, we see some clear changes.

For example, starting in 2019, the state successively issued two batches of fund advisory licenses, allowing advisors to charge based on management fees and excess returns rather than product sales commissions — sending an important signal to the market.

Meanwhile, traditional financial institutions represented by banks and securities firms have begun actively deploying in wealth management, establishing wealth management subsidiaries and wealth management companies. Yet they simultaneously face problems including asset scarcity, sales-orientation, and weak client service capabilities.

Therefore, developing a TAMP model suited to China's national conditions and market structure in the B2B direction, leveraging advisory resources to help clients with asset allocation services including insurance, will gradually become mainstream.

Additionally, intelligent advisory combining scenarios and demographic characteristics, as well as models such as open banking utilizing banking license resources, are also worth exploring.

However, we also recognize that China still lacks mature investors with asset allocation awareness. So the transition of wealth management to a buyer-advisory model will not happen quickly. Perhaps combining investor education with the wealth management transformation is also a viable path.

Major traffic platforms are also entering the fray. For instance, in April 2020, Ant Group partnered with Vanguard to launch a buyer-oriented intelligent advisory service, setting a benchmark for the industry. This also raises the bar for entrepreneurs in related fields — innovative companies must attempt to develop distinctive and differentiated services.

Finally, what cannot be avoided is that fintech companies face numerous challenges in implementation. Because the sector is close to money, clients have strong payment ability, and industry digitalization is high, numerous teams from within and outside the industry have attempted to enter this space. But many have more or less encountered problems in industry understanding, sales resources, market timing, client needs, business models, user awareness, upstream and downstream relationships, moral hazard, regulatory compliance, and so on.

Overall, we continue to believe that opportunities always outweigh challenges. Truly excellent companies will have the chance to participate in this trillion-yuan-scale asset transformation wave and contribute their value, helping China's capital markets develop more stably and healthily, and bringing continuous vitality to the real economy.

Reference

- EY, Global Asset Management Industry Report 2019

- BCG, Global Asset Management Report 2019 — The Next Decade of Asset Management: Can the Glory Continue?

- BCG, Global Digital Wealth Report 2019-2020

- Haitong Securities, The Era of Property Speculation Fades, Increase Allocation to Financial Assets

- Essence Securities, The Buyer-Advisory Model as the Key to Breaking Through Wealth Management Transformation

- Orient Securities, US Commercial Bank Wealth Management: Glimpsing the Evolution of Non-Interest Income

- GF Securities, Wealth Management Special Topic: Lessons and Insights from Charles Schwab

- Yiou, China Wealth Management and TAMP Business Model Research Report

- Quanye Planet, Decisive 2025: Outlook for Financial Institutions' Retail Wealth Management

- Quanye Planet, 45 Years of Charles Schwab: The Internet Broker in an Era of Transformation

- Wangjing Boger's Snowball Original Column, Bogle and the Complete History of Vanguard Group's Entrepreneurship

- New Global Asset Allocation, Xu Yang, From Breakdown to Establishment: The Development and Transformation of US Wealth Management

- New Global Asset Allocation, Xu Yang, Seeing the Big Picture from the Small: Charles Schwab and the Rise of Wealth Management and Advisory

- Yang Delong Says Finance, Yang Delong, Overseas Fund Development History Series: The Development of the US Fund Industry

- Sina Finance Opinion Leader Columnist, Dai Zhifeng, How Is the Asset Management Industry Being Reshaped by Fintech?

- Haitong Quantitative Team, Fund Advisory Series (I): Global History of Advisory Development

Discussion Questions

Q: When intelligent advisory emerged in the US, some companies in China also emerged with intelligent advisory concepts, but mainstream opinion at the time mostly viewed them as "unreliable." Why?

Welcome to click "Like" at the end of this article, and reply "finance" in our official account backend to receive our preliminary answer.

Reader Benefits

We welcome you to share your views on China's capital markets or fintech in the comments section. By 21:00 on July 31, the 6 readers with the most thoughtful comments will each receive a FreeS Fund customized notebook.

Contact Us

We look forward to continuous exchange with entrepreneurs and industry experts in the financial sector. You are welcome to contact Pengqi Liu, Vice President of FreeS Fund, at pengqi@freesvc.com. You may also add FreeS Fund's WeChat account (ID: freesfund) to connect with us.

FreeS Report 16: The Truth About Early-Stage Healthcare Investment and China Speed | Frees Fund

FreeS Report 15: Life's Gamble — The Adventurous Journey of Drug R&D | Frees Fund

▲ FreeS Report 13: To Understand China's Consumption Upgrade, First Look at Japan 40 Years Ago

▲ FreeS Report 10: The Bestselling Snacks That Survived Economic Cycles All Share One Secret