FreeS Fund Report 19 | The Age of Tipsiness: Where Are the Opportunities in Low-ABV Alcohol Entrepreneurship?

Is this a market driven by long-term trends, or one poised for rapid near-term growth?

Fruit-flavored, fizzy alcoholic drinks couldn't be hotter this summer. Last week, Nongfu Spring joined the fray following its Hong Kong IPO. How did the low-ABV beverage trend emerge, and what shape will it take in the Chinese market?

We traced the logic behind viral hard seltzer White Claw's explosive 2019 rise in the US, and analyzed how Japanese centenarian brand Suntory expanded its ready-to-drink cocktail portfolio in a mature alcohol market to become the industry leader.

We hope you find it illuminating.

Contact Us

We remain bullish on innovation in food and beverages. We welcome candidates with industry backgrounds to join us (hr@freesvc.com), and business plans are always welcome (bp@freesvc.com).

Low-ABV Alcohol Industry and Case Studies

By Huang Hai, Jiao Yingzhu (jiaoyingzhu@freesvc.com)

How Did Hard Seltzer Develop Into a New Category?

In food and beverages, innovation never sleeps.

One day in 2012, Nick Shields, fifth-generation scion of Boston's venerable craft brewery Boathouse Beverage, sat at a bar worrying about his beer business.

At the time, the US had over 4,000 craft breweries large and small. Beer production and sales climbed year after year, but competition intensified. To make matters worse, beer faced a "squeeze effect" from wine and spirits.

By observing women's drinking habits at bars, Nick found inspiration. He noticed groups of women would sit together for hours, each nursing a low-ABV vodka soda, knocking back several without getting drunk.

This rudimentary cocktail recipe — two ounces of vodka with soda water, mixed over ice and garnished with lemon or lime — was crisp and refreshing. Nick wondered: could he create a similar low-ABV drink using craft brewing methods?

After repeated experimentation and process refinement, he replaced the malt essential to beer fermentation with cane sugar, and charged the bottles with abundant carbon dioxide so bubbles rushed out upon opening. This alcoholic sparkling water clocked in at just 6% ABV but was remarkably low-calorie at 140 calories per can — healthy enough to appeal to the weight-conscious.

Nick named his creation Spiked Seltzer, adopting a siren as the brand's associated image, targeting young women who enjoyed drinking. Spiked Seltzer launched in 2012 at $8 for a six-pack, with sales rocketing upward year after year; roughly 70% of buyers were women.

▲ Spiked Seltzer six-pack

In 2016, AB InBev, with its keen commercial instincts, acquired Spiked Seltzer from Nick. Multiple breweries entered the fray, including White Claw, which we'll analyze in depth.

By production method, alcohol is generally classified into three categories: distilled spirits, fermented beverages, and mixed drinks. Both distilled and fermented beverages tend to be high in calories due to sugars produced during manufacturing.

Spiked Seltzer and its ilk, based on modified beer brewing processes, reduced calories while offering diverse flavors. Subsequent brands followed similar formulations — so closely that the Brewers Association recently published a dedicated Hard Seltzer brewing guide.

Strictly speaking, however, hard seltzer traces back to the 1980s–1990s: Bacardi, one of the world's largest spirits producers, launched Breezer; Hooper introduced Hooch; Two Dogs' Lemon Brew hit shelves. The most representative brand was arguably Zima, launched by Coors Brewing in 1993. This malt-based alcoholic beverage sold over 1 million cases in its debut year, yet experienced turbulence and was discontinued in 2008.

One major reason for Zima's decline was ridicule for being overly feminized. David Letterman famously mocked Zima as a "sissy drink." Hard seltzer similarly attracted a large female user base and risked being tagged as "feminine" — the brand that shattered this stereotype, which we'll analyze next, was White Claw.

▲ White Claw's sales exploded in the US in 2019.

Before dissecting White Claw, let's summarize the characteristics and advantages of alcoholic sparkling water as an everyday beverage — this will help explain why low-ABV drinks could rise so dramatically.

First, lower alcohol content dramatically lowers the barrier to consumption. By Chinese standards, beverages below 0.5% ABV qualify as non-alcoholic. The industry generally labels drinks between 0.5%–7% ABV as low-alcohol beverages. The former category includes Heineken and Suntory's alcohol-free beers; the more mass-market latter includes Rio cocktails.

Lower ABV expands the addressable drinking population while reducing costs, giving producers greater pricing flexibility.

In the US, the legal drinking age is 21, and supermarkets and department stores require age verification for alcohol purchases, whether spirits or low-ABV drinks. Yet many under-21 college students drink at parties regardless.

Second, low-ABV beverages can offer diverse flavors and textures to satisfy young consumers' appetite for novelty. Fruit flavors dominate alcoholic seltzers, letting consumers choose according to preference. Moreover, alcoholic sparkling water suits social scenarios like home gatherings and picnics — light drinking enhances atmosphere without excessive alcohol intake.

▲ By production method, alcohol falls into three major categories.

Third, low-ABV alcoholic sparkling water satisfies both health-conscious consumers watching their calorie intake and gluten-intolerant individuals seeking gluten-free options. Popular low-ABV sparkling waters abroad feature zero sugar, zero carbs, and low calories — with all calories coming from the alcohol itself. White Claw, for instance, contains roughly 100 calories per can. This proves highly attractive to those dieting or managing their physique. Additionally, gluten-free positioning suits the 3.1 million Americans following gluten-free diets.

To deepen understanding of low-ABV beverages, this article selects White Claw and Suntory as representative cases from the mature US and Japanese alcohol markets respectively, analyzing their product and competitive strategies in different market contexts.

White Claw's Viral Rise: Beer Replacement, Clever Positioning, and Viral Social Media Content

In 2016 — the same year AB InBev acquired Spiked Seltzer — White Claw launched in the US.

Its producer was Mark Anthony Brands, North America's largest ready-to-drink alcohol manufacturer, a 48-year-old company that found its second growth curve with White Claw. White Claw contained 5% ABV, just 100 calories per can, zero sugar, and no gluten. Six-packs ran $8–10, available in six flavors including black cherry, mango, and lime.

▲ White Claw's low ABV, low calories, and affordable price made it a staple at young people's parties and outdoor gatherings.

After three years of growth and accumulation, White Claw swept across America in summer 2019. Per Nielsen data, White Claw reached $1.5 billion in US sales last year, capturing 60% of the alcoholic sparkling water market — single-handedly igniting the entire category. Alcoholic sparkling water jumped from under 1% of US alcohol sales in 2018 to 2.5% in 2019, independently establishing itself as a new alcohol category. Correspondingly, the number of alcoholic sparkling water brands in the US rose from 20 in 2018 to over 80 in 2019.

In 2019, The New York Times wrote: "If you see another brand of alcoholic sparkling water in the fridge, you'd still call it a White Claw." In other words, White Claw = alcoholic sparkling water.

So what did White Claw, the upstart in alcoholic sparkling water, do right? How did it ascend to become synonymous with the category?

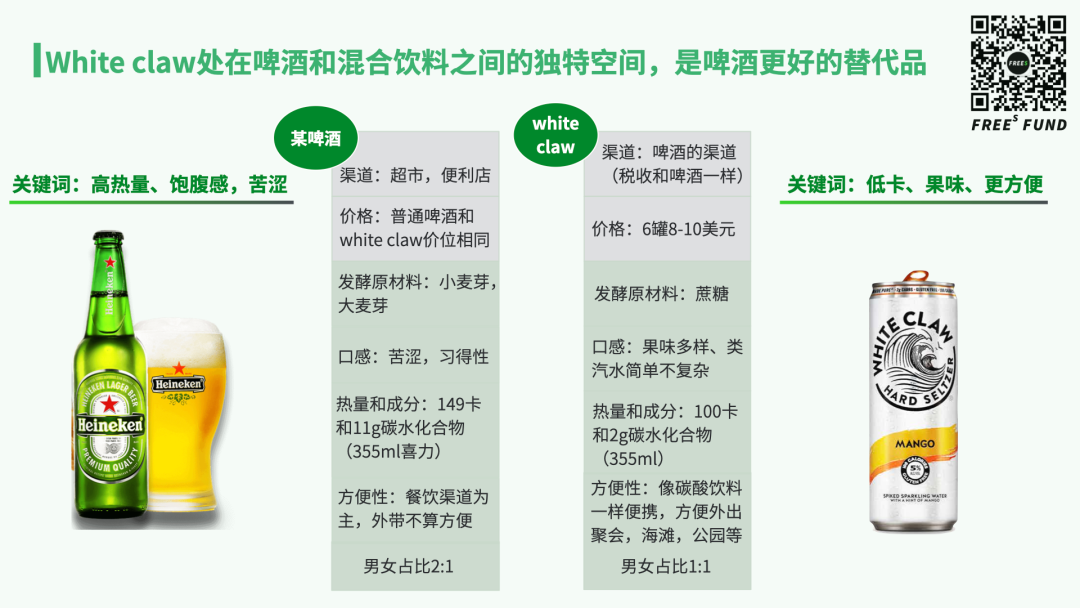

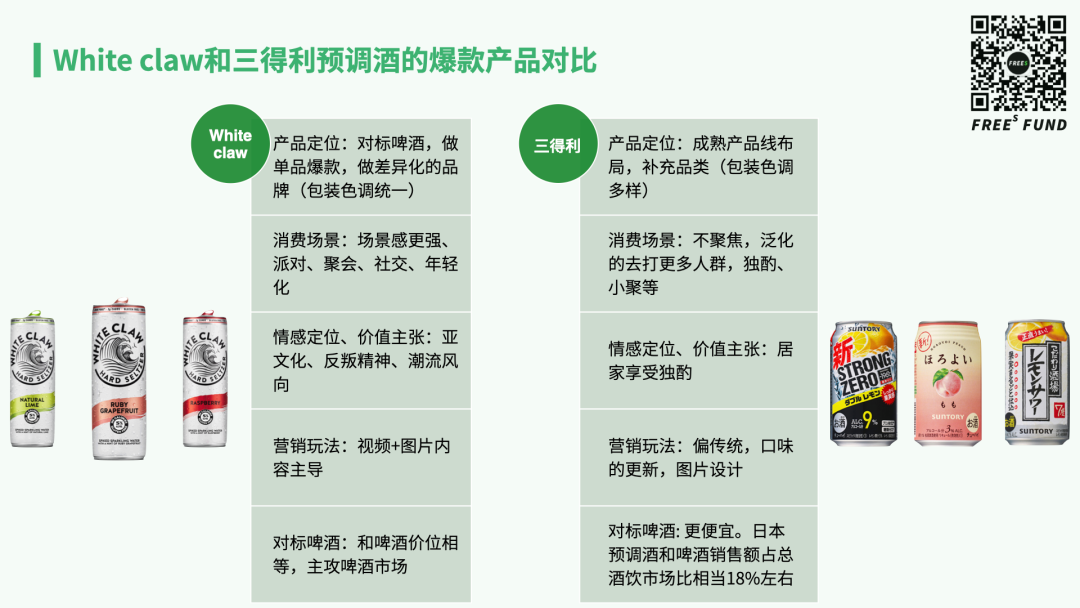

First, compared to beer and other alcoholic beverages, White Claw occupied a unique position between beer and mixed drinks, largely able to substitute for beer in social settings.

From a product positioning standpoint, White Claw's consumption scenarios mirror those of beer — crowded parties, campus events, outdoor sports, pop concerts — tightly woven into American social life. Its price point matches ordinary beer, yet it's more approachable on the palate, blending in rich fruit flavors with a soda-like taste. Meanwhile, its aluminum can packaging makes it effortless to bring to beaches, parks, and pools.

Moreover, beer carries a masculine connotation, with a male-to-female user ratio of roughly 2:1. White Claw, by contrast, targets a young, gender-neutral audience. This shows up in both its product and content design. Take content design: White Claw's video content projects a youthful, natural, healthy, and energetic lifestyle — appealing equally to men and women.

▲ White Claw's unique position between beer and mixed drinks.

Second, White Claw's rise owed much to video and image-based传播 on the internet, connecting product value to American spirit, youth culture, and values — creating resonance.

White Claw shone particularly bright on YouTube. In June 2019, Trevor Wallace, a 27-year-old comedy influencer, posted a viral video about White Claw. Two months after the video dropped, White Claw experienced nationwide stockouts. The nearly five-minute clip has racked up 5.09 million views as of September 14, 2020.

▲ Trevor Wallace's viral YouTube video about White Claw.

The video spawned countless quotable lines that netizens clipped and circulated. For example:

- "Ain't no laws when you're drinking Claws" (pointing to rebellion, rule-breaking. The legal drinking age in America is 21, yet the average college freshman is 18.)

- "You don't like White Claw? Well, I guess you don't like America." (tying product value to American spirit)

- "You drink Truly [the #2 selling hard seltzer]? Yeah, well I have an Android phone." (American humor flexing market dominance)

White Claw's sense of trendiness and quality made it a form of social currency among young people. Trevor's persona — lighthearted, funny, a voice-of-authority for white guys — was catnip to American youth. His animated delivery of internet "memes" that American kids instantly got drove widespread propagation of the brand's distinctive character.

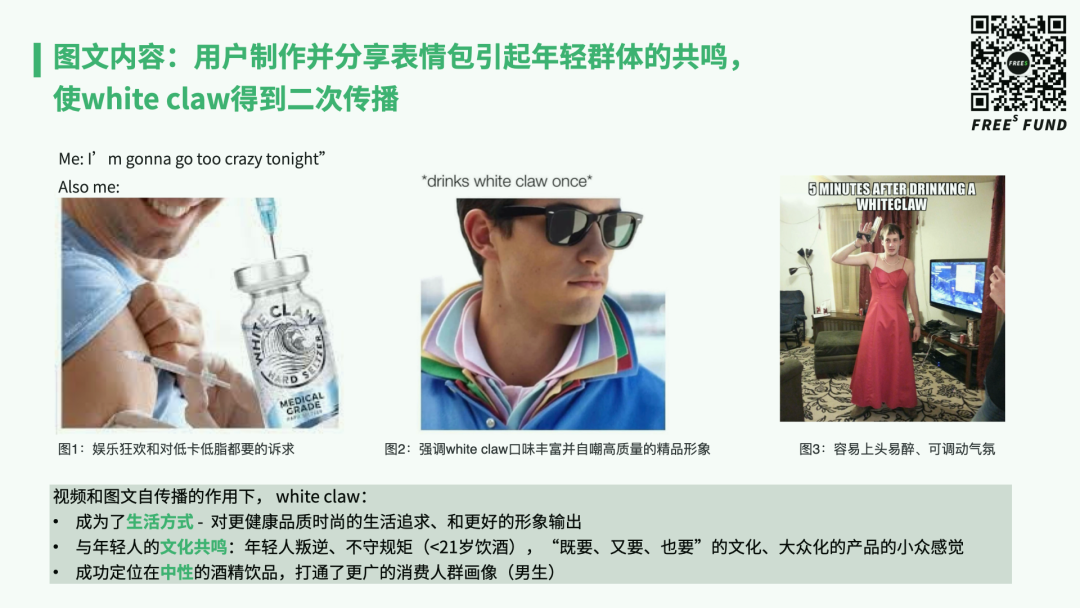

On the image front, social media users spontaneously created and shared countless memes about partying and drinking, helping White Claw achieve secondary传播 while once again exporting a lifestyle of youthful rebellion, self-assuredness, and rule-flouting.

▲ User-generated content fueled White Claw's secondary propagation.

Take the three images above. The first reads, "I'm getting absolutely wrecked today." The image then points to the effect of drinking White Claw — comparable to injecting stimulants — while still satisfying low-cal, low-fat demands.

The second says, "How it feels after drinking White Claw once." You see a handsome guy in a blue polo with a multicolored collar underneath. Analysts suggest this image carries two layers of meaning: first, the person is mimicking White Claw's bottle design — pale blue body with streaks of color representing rich fruit flavors; second, White Claw drinkers look polished on the outside but are secretly drama queens who love playing it cool.

The third reads, "My state five minutes after finishing a White Claw." The guy wears a skirt and brandishes a toy gun. Implying the product gets you drunk fast and easily pumps up the atmosphere.

To summarize, White Claw's breakout rests on three main factors:

- Strong positioning. As a beer alternative, alcoholic sparkling water sits between beer and mixed drinks, largely able to substitute for beer in social settings.

- Brand resonance with American youth culture, where young people find identity affirmation.

- A gender-neutral image that attracted a broader consumer base, shattering the preconception that "alcoholic sparkling water" was feminine.

Much like beer, White Claw's primary sales channels remain offline retail and on-premise consumption. Constrained by legal requirements, e-commerce's share of online alcohol sales has stayed around just 1%.

03

Suntory: Seizing Every Niche, Full Product Line Deployment

In America, emerging categories are often led by upstart brands. Spiked Seltzer and White Claw in alcoholic sparkling water are textbook examples.

Japan's alcohol market, by contrast, has virtually no new brands built by new companies. Century-old giants dominate — Suntory, Asahi, and Kirin posted 2019 revenues of roughly RMB 149.8 billion, 137 billion, and 124.1 billion respectively, forming a near-monopoly in Japan. Fourth-place Sapporo Breweries trailed far behind at just RMB 21.2 billion.

In alcohol-saturated Japan, the market breaks down by subcategory into beer, wine, spirits (whiskey, shochu, sake), and ready-to-drink (RTD) beverages, among others. In 2019, Japan's alcohol retail market reached RMB 571.8 billion. Spirits claimed 25% of sales due to higher unit prices, while beer and RTD held roughly comparable shares at 18% and 16%.

The three giants — Suntory, Asahi, and Kirin — each excel in different arenas. Asahi has long reigned as beer sales champion; its Asahi Super Dry alone captures 19.9% of Japan's total beer sales. But in spirits and RTD, Suntory dominates with 53% and 40% market share respectively. Spirits serve as the base for RTD. In 2014, Suntory acquired American company Beam Inc., becoming the world's third-largest spirits group.

Next, we'll use Suntory — Japan's RTD leader — to examine the consumption landscape for ready-to-drink beverages. RTD refers to pre-mixed drinks combining base spirits with fruit juice. Similar to alcoholic sparkling water, Suntory's RTD lineup features relatively low alcohol content, ranging from 3% to 9%.

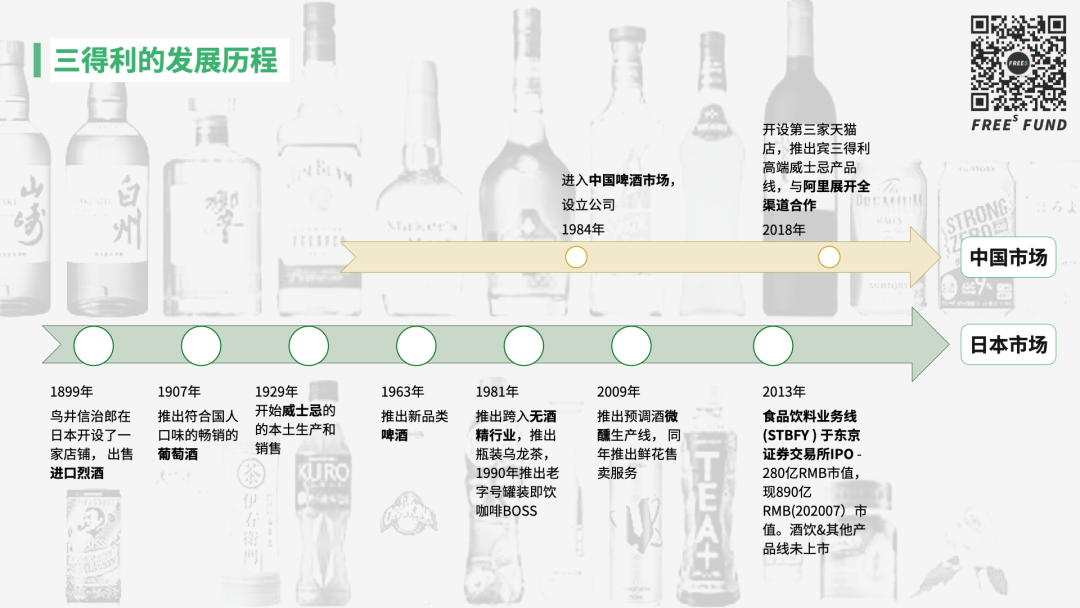

Founded in 1899, Suntory operates three divisions: food and beverages, alcoholic beverages, and health foods. In 2019, Suntory's annual revenue approached RMB 150 billion, with roughly 56% from food and beverages — where water represents the largest subcategory, somewhat reminiscent of recently listed Nongfu Spring. Another 34% came from alcoholic beverages, approximately RMB 50 billion in scale.

▲ Suntory's century-plus history.

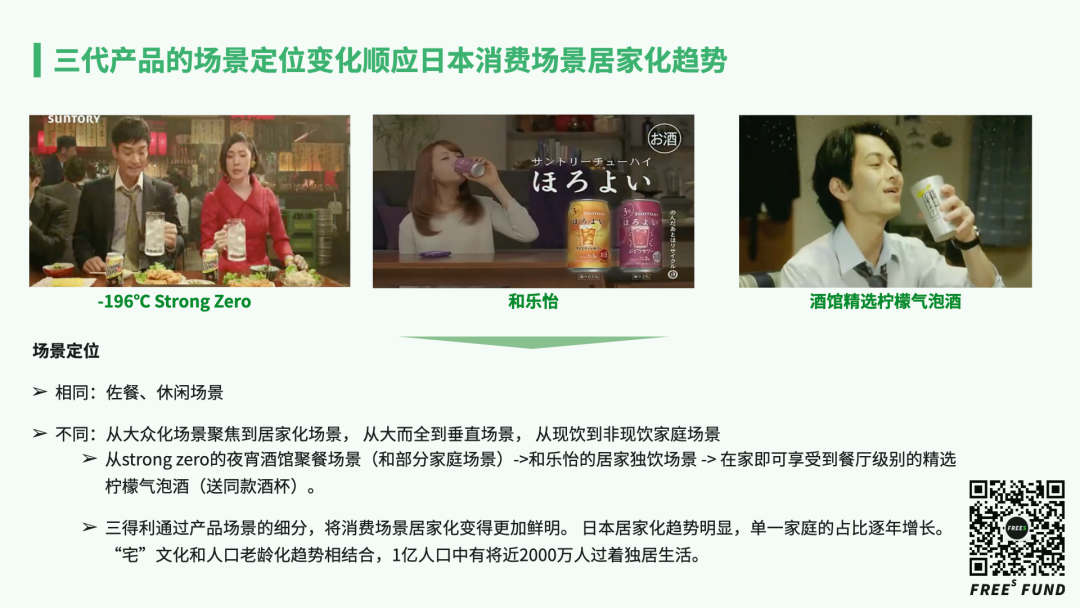

For its first 80 years, Suntory dug deep into spirits, wine, and beer. In 1981, it launched bottled oolong tea. In 2003, its food and beverage division listed in Tokyo. In 2009, Suntory introduced the RTD sub-brand Horoyoi in Japan — what many Chinese consumers know as "Weixun" (微醺, "tipsy").

Horoyoi comes in flavors like white peach, grape, and plum wine soda, in 350ml cans, all at just 3% ABV. Unlike White Claw's emphasis on zero-sugar and low-calorie selling points, Horoyoi focuses on fusing fruit juice with low-alcohol content — smoothing out alcohol's bite while delivering rich fruit flavors. When Suntory officially brought Horoyoi to China in 2019, it immediately became a beloved网红 product.

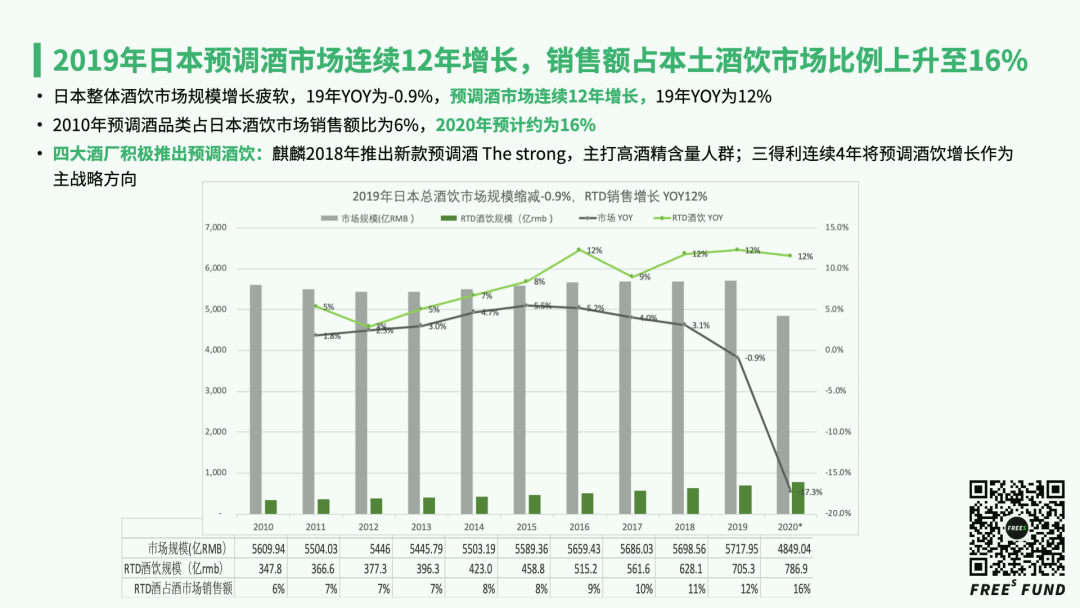

Suntory has designated RTD as the primary growth driver for its alcoholic beverage division for four consecutive years. Consider this: in a Japanese alcohol market that's overall sluggish and no longer growing, with beer transitioning from maturity to decline, RTD is the only category to achieve 12 consecutive years of growth. To a large extent, it's eating beer's lunch.

In 2010, RTD accounted for just 6% of Japan's alcohol beverage sales; this year, that figure is expected to hit 16%. In 2019, RTD sales grew 12% year-over-year — a substantial number in a country with stagnant population growth.

▲ In a sluggish, no-longer-growing Japanese alcohol market, with beer moving from maturity to decline, RTD is the only category to achieve 12 consecutive years of growth.

Facing such a market, Suntory's approach is a full-product-line strategy — deploying across every subcategory, even launching multiple products within the same subcategory to meet diverse consumer demands. In the RTD segment, this holds true as well.

Beyond the 3% ABV Horoyoi, Suntory fields a product called Strong Zero, its bottle emblazoned with a bold "9%" — targeting users who crave both fruit flavors and alcohol kick. Additionally, Suntory offers a bar-select sparkling lemon shochu, emphasizing restaurant-grade quality, available in both 7% and 9% ABV. These three hit products account for 73% of Suntory's RTD sales.

▲ Against Japan's increasingly pronounced solo-living trend, promoting home drinking and solo enjoyment follows the current.

From Strong Zero to Horoyoi to the bar-select sparkling lemon shochu — though all three target leisure scenarios, subtle shifts underlie them: from bar settings to home settings, then to enjoying better products at home.

Behind this scene-positioning evolution lies Japan's unmistakable solo-living trend, with one-person households growing year by year. Against this backdrop, championing home drinking and relishing solo imbibition is simply riding the wave.

▲ A Suntory ad targeting solo-drinking occasions.

After Suntory's RTDs achieved massive success in Japan, other breweries entered the same market. Kirin, for instance, launched its own RTD brand, The Strong, in 2018.

04

What Opportunities Exist in China's Alcohol Market?

This year, numerous domestic companies have launched low-ABV products. Craft brewery Panda Brew introduced a sub-brand called Chill, using vodka as its base, with a focus on zero-sugar, low-calorie formulations at 3% ABV. Nongfu Spring also made a high-profile debut with three TOT sparkling beverages, including a rice wine flavor containing less than 0.5% alcohol.

It's still too early to analyze or predict the prospects of these domestic low-ABV beverages. We're equally curious: will China produce a White Claw or Suntory-caliber low-ABV brand? And what core capabilities are needed to build one?

Before tackling these questions, let's examine China's alcohol market.

By volume, beer dominates absolutely, accounting for 76% of sales. Baijiu represents less than 18% by volume, but commands a staggering 66% of sales value due to higher price points. From 2015 to 2018, China's overall alcohol market saw declining sales, with 2020 market size estimated at roughly 1.1 trillion RMB.

We believe this trillion-RMB industry offers substantial room for innovation and new approaches. Baijiu is highly mature, dominated by major incumbents — a sector where barriers grow with time, making it difficult for startups to penetrate. Beer has also reached saturation in China, with volume declining for five consecutive years, though market value has held steady thanks to premiumization and higher average selling prices.

Data shows RTDs command merely 0.18% of China's alcohol sales volume and roughly 0.2% of sales value. If RTD大众化 — mass-market adoption of RTDs — becomes a confirmed trend, significant opportunities await.

On one hand, RTDs can address drinking needs that beer fails to satisfy, potentially winning over female consumers. On the other, they may convert non-drinkers — people who previously consumed juice or carbonated beverages — into light drinkers.

The success of White Claw and Suntory RTDs in the US and Japan validates both possibilities.

▲ A product comparison between White Claw and Suntory.

Indeed, from a consumer perspective, the lower alcohol content of hard seltzers and RTDs dramatically reduces the barrier to entry — even infrequent drinkers can enjoy them easily. The abundant carbonation and fruit flavors satisfy broad taste preferences. Additionally, to serve both on-premise and retail needs, hard seltzers and RTDs use can packaging, making them convenient to drink and carry while maintaining a quality perception.

Notably, our research into White Claw and Suntory RTD distribution reveals they rely primarily on off-premise retail channels rather than on-premise venues like restaurants. Specifically, White Claw's sales come mainly from physical retail — grocery stores, convenience stores, liquor shops (Drizly), supermarkets (Walmart), and specialty grocers (Trader Joe's). Similarly, retail channels comprising hypermarkets and supermarkets account for 97% of Suntory RTD sales.

By contrast, China's alcohol market — whether baijiu or beer — carries strong social attributes and tight restaurant-scene associations. Looking at domestic beer's current state, retail and on-premise channels split volume roughly equally. On-premise consists mainly of restaurants, bars, and nightlife venues; off-premise comprises supermarkets, hypermarkets, convenience stores, and other online and offline channels. The online-to-offline ratio is 1:9.

This channel structure likely means low-ABV startup brands face a choice: either burn capital on heavy investment to build retail distribution, or invest effort into navigating on-premise channels like restaurants. Given the fragmented nature of restaurant outlets, the latter demands strong offline management capabilities.

To summarize: in the long term, some portion of beer market share will be captured by low-ABV products like hard seltzers or RTDs. Based on their trajectory in the US and Japan, this is expected to unfold over the coming decade.

The challenge is that at this stage, offline channels' dominance is hard to change. Yet attracting young consumers requires strong online content and communication capabilities. Channels are offline; content and brand building are online. (FreeS Fund has previously analyzed how content ecosystem evolution shapes consumer entrepreneurship — see our past articles for more.). Thus, low-ABV alcohol entrepreneurship is a demanding track, requiring teams to excel both online and offline.

"Drink less, buy more" somewhat captures the core commercial logic of the low-ABV alcohol sector. But realizing this logic demands considerable effort in marketing and consumer education.

Key Takeaways

1. In product positioning, White Claw more directly targets beer, with emotional positioning focused on young people's social scenarios: gatherings, outdoor activities. Accordingly, its marketing strategy leverages KOLs and social networks to reinforce product selling points and communicate value propositions to young consumers. Suntory, by comparison, further segments its target demographic and consumption scenarios, purposefully launching RTDs with varying ABV levels and flavors that align with Japan's social trends — championing home drinking and relishing solo imbibition.

2. China's RTD market remains in a very early stage. Baijiu and beer respectively dominate the high-ABV and low-ABV segments. Beer is the traditional king of low-ABV alcohol, but consumption has peaked. Mass-market beer is declining; overall market size is maintained mainly through rising price points. Some beer market share being captured by RTD/low-ABV categories — this happened in the US and Japan, and is likewise the trend in China.

Discussion

Which approach holds more promise: adding alcohol to beverages, or making alcohol taste like beverages?

Share your thoughts in the comments. By 9:00 PM, September 20, we'll select the 6 most thoughtful commenters to receive custom FreeS Fund notebooks.

We're Hiring Investors | Beijing, Shanghai, Shenzhen — Three Sectors

We're seeking investors in Beijing, Shanghai, and Shenzhen for biopharma, deep tech, and consumer/TMT. If you have industry background and interest in investing, join us — or refer excellent candidates. Send resumes to hr@freesvc.com. Please use subject line: Application for "[Specific Position]" — "[Work Location]"

For full details: Year Six and Counting: FreeS Fund Is Hiring Investors | Doing What's Right, Not What's Easy

▲ Three Squirrels' Zhang Liaoyuan: A Once-in-20-Years Brand Opportunity — How to Win in Three Steps | FreeS Fund 2020 CEO Annual Meeting

▲ FreeS Report 17: What New Opportunities Are Emerging in the Ancient Jewelry and Accessories Industry? | FreeS Research Institute

▲ How Did Saturnbird Surpass Nestlé and Starbucks to Become #1 in Instant Coffee During 618? | FreeS Research Institute — Learning from Investment

▲ 2020: Consumer Brand Entrepreneurship Enters an Era of Multiple Simultaneous Growth Drivers | FreeS Research Institute

▲ Mid-Game During Singles' Day: What Did Chicecream, Saturnbird, Plant Voice, and Huasheng Haoche Get Right?

▲ The Category Logic Behind the Hype — Using Coffee Industry Investment as an Example

▲ Breaking Through as a New Brand: From Traffic Thinking to Content Thinking | FreeS Research Institute

▲ From the Rise to the Settling: Is E-Commerce Livestreaming a Feature or a Business Model? (Part 1) | FreeS Research Institute

Where Is the Endgame for E-Commerce Livestreaming? | FreeS Research Institute