Amid the GPT Frenzy: Anxiety and Breakthroughs in China's Chip Market | FreeS Research --- The launch of ChatGPT has ignited a global AI race, and chips — the silicon foundation of this revolution — have become the most scrutinized bottleneck in China's tech ecosystem. For domestic semiconductor players, this moment is charged with both urgency and opportunity. ## The Anxiety: Caught in the Supply Chain Squeeze China's AI chip landscape is dominated by a handful of players, with NVIDIA holding roughly 90% of the market for training chips. The U.S. export controls, tightened in October 2022 and again in 2023, have systematically choked off access to NVIDIA's most advanced GPUs — the A100 and H100, then the cut-down A800 and H800 workarounds. Each restriction has sent ripples through China's AI infrastructure buildout. The anxiety runs deeper than procurement headaches. Training large language models demands massive clusters of high-bandwidth, high-memory chips working in lockstep. China's domestic alternatives remain one to two generations behind on process nodes, interconnect bandwidth, and software ecosystems. The gap isn't merely hardware; it's the accumulated decades of compiler optimization, framework integration, and developer familiarity that NVIDIA

It's been nearly a year since the CHIPS Act took effect. How is China's chip industry doing?

Chips are both the crown jewel of industrial manufacturing and a bargaining chip in great-power competition. In August 2022, the U.S. government signed the CHIPS and Science Act of 2022, sending shockwaves through China's chip market. Since then, U.S. restrictions on China in the semiconductor domain have steadily escalated. This January, Japan and the Netherlands also reached agreements with the U.S. to impose export controls on semiconductor equipment to China. Companies like Samsung Electronics, SK Hynix, and TSMC have been forced to make difficult choices in this "chip war."

China Customs data shows that from January to February 2023, China's integrated circuit imports totaled 67.6 billion units, down 26.5% year-over-year — a steeper decline than the 15.3% drop for all of 2022. 2022 also marked the first year in nearly two decades that China's IC imports had fallen. Nearly a year after the Act took effect, what impact has it had on mainland China's chip market? Has the recently proposed European Chips Act further intensified these effects?

In a podcast collaboration between What's Next | Tech Matters and High Energy, FreeS Fund partner Yongcheng Yang joined hosts Can Liu and Diane to discuss the current state of China's domestic chip R&D industry, exploring these questions:

- Why does the surge in large language models directly boost the chip market? Will this wave transform the chip landscape?

- What factors allowed NVIDIA to stand out during this AI boom?

- How should Chinese tech companies properly address chip anxiety and overcome weaknesses in chip design?

- What substantive impact has the U.S. CHIPS Act had on the global chip industry?

We've edited and excerpted portions of the podcast, hoping to offer fresh perspectives. We welcome you to continue observing and discussing with us. You can also head to the Xiaoyuzhou app or Apple Podcasts, search for and subscribe to What's Next | Tech Matters or High Energy to listen to the full episode.

We look forward to continuing the conversation. If you also follow the chip industry or are building a startup, feel free to reach out to FreeS Fund partner Yongcheng Yang at yangyongcheng@freesvc.com.

Engagement Giveaway What do you think about China's chip market? Does your industry have chip anxiety? Share your observations and thoughts in the comments. By 5:00 PM on June 21, we'll give Dedao reading cards to the 2 users with the most likes and the 3 users with the most thoughtful comments (reading cards valid through November 30, 2023).

Why Do Large Models Boost the Chip Market?

Can Liu: After most major domestic tech companies tried their hand at large models, they started turning their attention to chips. Why does the surge in large models directly boost the chip market? What's the logic behind it?

Yongcheng Yang: In the past, things at the application layer could be continuously accumulated and iterated. You could start with a foundational model and keep improving it, gradually refining it as data and use cases grew. But for current application scenarios, demand for GPT-like capabilities has exploded.

Previous small models tended to be more domain-specific, developing in an incremental way. But in the large model space, without massive computing power, the model simply can't run. On the compute side, large models require enormous one-time resource investments, consuming huge quantities of GPU chips.

As Qi Lu put it, the current moment of large model popularity is like a gold rush. Everyone recognizes that AI has many advantages, but where exactly it will first take off, and what its timeline curve will look like — we're all uncertain. We know the gold is definitely there, but who will find it? And where, and what kind?

When the specific path is unclear, what heats up first are the tools for mining gold — we need people selling shovels. GPU chips are the gold-mining tools of the large model era. Many technologies follow this pattern, but for GPT, "shovels" aren't enough. GPT requires such vast amounts of general-purpose data and such high compute requirements that without a baseline configuration of computing power, you get nothing. So it needs lots of "excavators," lots of industrial equipment to develop effectively.

So from the perspective of large models' chip demands: first, the explosion in demand is extremely rapid; second, the volume needed is enormous.

Diane: I've spoken with friends at major Silicon Valley companies, and they believe the "window of opportunity" for startups to enter the large model space has basically closed. Even at well-resourced large companies, departments are constantly competing for compute resources. So for startups, trying to build large models now would likely require prohibitively high costs.

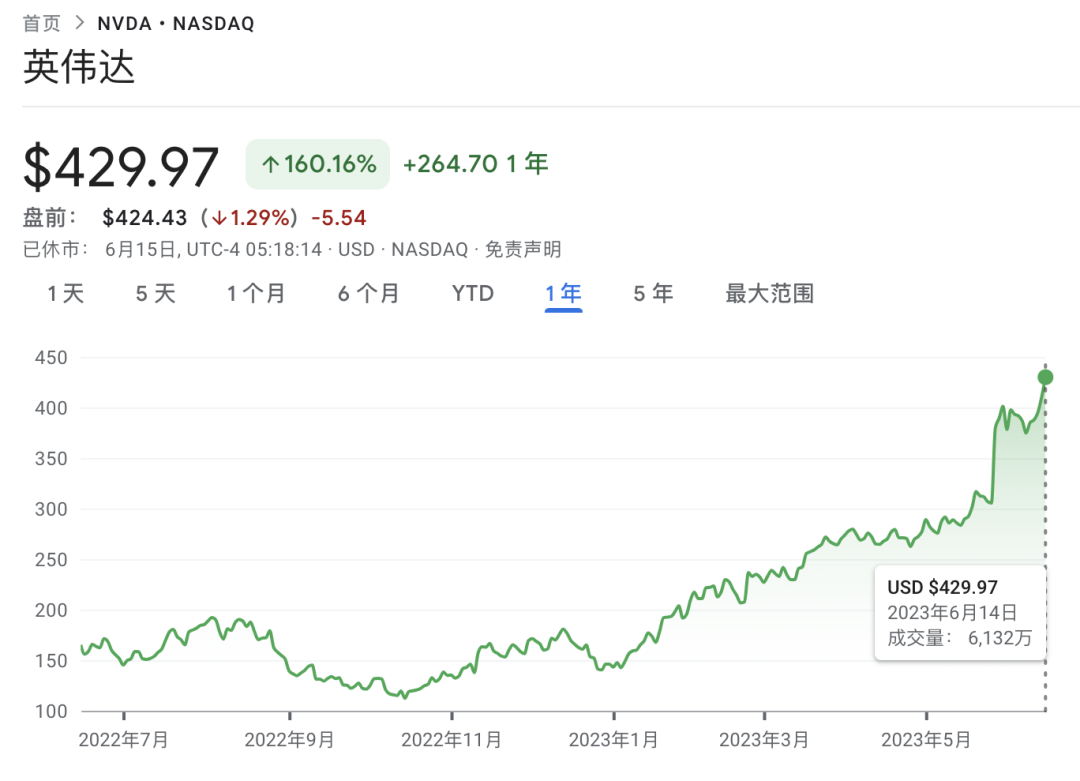

Can Liu: From last year to this year, the chip industry hasn't been in a very strong position. When we discussed automotive chips last year, we noted that chips weren't in a particularly hot cycle. So why in this GPT wave has NVIDIA been the first to break out and perform so well?

▲ NVIDIA's market cap changes over the past year. Image source: Google Finance

Yongcheng Yang: Several factors: First, NVIDIA laid the groundwork earliest. Second, its technology is extremely strong. Third, its ecosystem is more mature. It's leading across three dimensions: related software, development environments, and graphics algorithms.

"Getting in early" matters enormously. In the chip industry's development, beyond core players, you need participants in algorithms, services, board cards (printed circuit boards that control hardware operation), and other roles. Everyone promotes and competes with each other, and this also forms some explicit or implicit industry standards.

NVIDIA entered earliest and was also very strong, so many rules in the industry are extremely well-suited to NVIDIA. Getting in early lets you occupy an exceptionally good, forward-leaning position.

Beyond NVIDIA, How Much Opportunity Do Other Competitors Have?

Can Liu: Perhaps precisely because NVIDIA's performance has been so standout, companies have realized that NVIDIA's chips place a certain burden on their R&D costs. Overseas, for example, Microsoft has a team working on self-developed chips. There have been reports that Microsoft is developing chips on a 5nm process node.

Will NVIDIA, now benefiting from the large model boom, see future revenue decline as subsequent competitors enter?

Yongcheng Yang: Major tech companies building chips or crossing into new domains — this isn't the first time, and it won't be the last. But in the next 5 to 10 years, I don't think the position of specialized chip companies is so easily shaken.

Let's first assume these companies have no problem with chip manufacturing capability. Compared to NVIDIA, what's the advantage of major tech companies?

From a product definition perspective, they understand their own needs better — they're clearer about what algorithms are needed for internet services or application software. So if a major company builds a chip to run its own applications, and it shows higher efficiency or better performance, that's not surprising.

But the flip side is that it may face a generality problem. In product definition and development, major companies typically lean toward designing for their own services. It's not easy to abstract the needs of society as a whole, the entire IT industry, into common requirements and then gradually implement them. Even if they recognize these needs, they have to make trade-offs in implementation — it's difficult to balance on the product definition dimension.

The second dimension: every company has its own DNA. Especially once a company becomes a giant, it's like someone who's completed their PhD — they've already established their own specialization.

This specialization isn't entirely about technical barriers, because technical capabilities have hard metrics. What's hard are the softer aspects: product definition, management, operations, setting KPIs — these differ greatly between industries. For a company to transform from an internet company into a chip company, that's hard to achieve in a short time.

One example illustrates the difference between chip companies and internet companies. Some leading domestic chip companies will issue press releases about a chip being "successfully lit up" — meaning that after first tape-out, electrical current flows through the chip smoothly, indicating the chip is functional, though its features haven't been tested yet. In the chip industry, this is considered major progress.

If we switch to an internet company manager's perspective, someone might ask: can't you iterate faster? From internet practitioners' viewpoint, chip manufacturing efficiency seems low. This cultural clash actually happens every day.

The chip industry requires sustained investment. The hardest part is continuously iterating based on market and demand changes — each iteration is very costly. So the companies that can do CPU architectures and server architectures are basically just a handful. In the mobile industry, too, only a countable few. Doing chip hardware well isn't easy.

How Should Domestic Companies Respond to Chip Anxiety?

Can Liu: Recently I saw a report from Cambricon, which makes general-purpose intelligent chips, and I think domestic companies do have reserves in this area. When we talk with friends, some worry whether our chips aren't good enough yet, whether capacity is insufficient.

How do you think Chinese tech companies, especially those involved in AI computing, should properly respond to chip anxiety?

Yongcheng Yang: While the industry doesn't believe the U.S. will completely cut off chip supply, what will this affect?

First, it affects efficiency — your computational efficiency will decline. Second, it affects cost. Originally, a task that required just two board cards with an A100 chip (NVIDIA's high-end GPU) might now need 4 or 5 board cards with an A800 chip (the "budget alternative" to the A100).

But in the Chinese market, this isn't a fatal problem. The reason is that the companies using this computing power are all internet giants — they are both customers for chips and providers of AI algorithms. We may not be using the most advanced technology in our infrastructure, but our accumulated scale won't decline, and the market remains in our hands.

No path of development is ever completely smooth. Especially as a追赶者 [catch-up player], you need to prepare for a "protracted war." But this doesn't mean companies like Cambricon need to fight alone. Behind them, there needs to be both macro-level resource coordination and support from the investment chain.

There aren't many successful catch-up cases globally. First, in the short term, global chip production capacity is limited, so we need to concentrate resources to accomplish big things — directing more social resources toward chip companies. Second, and most crucially, we need persistence. Under the broad goal of building national industry, we need to think about how to solve chip anxiety.

Due to U.S. sanctions, Europe and other regions are more inclined to build independent industrial chains. For catch-up players, this is positive news — it provides opportunities to validate their products.

Diane: I previously watched your conversations with several portfolio companies, where you mentioned Japan's restrictions on exporting chip materials to South Korea. Could you share that story?

Yongcheng Yang: For a period, Japan restricted exports of key materials needed in display panel and semiconductor chip manufacturing to South Korea. Japan held a relatively large share of global production for these materials, many of which relate to fine chemicals. (For more thoughts on underlying semiconductor materials, click to read Discovering New Opportunities from the Periodic Table: Tech Entrepreneurship Has More Room for Imagination | FreeS Fund Dialogue)

▲ In 2019, Japan announced strengthened export controls on South Korea, focusing on three chemical products: fluorine polyimide, photoresist, and high-purity hydrogen fluoride (etching gas). Image source: Yangtze River News screenshot

Manufacturing equipment is a strength of Chinese manufacturing. However, China entered the chip industry relatively late, and equipment manufacturing lagged behind — this is where we're being most choked. Still, our foundational capabilities are there. We've gradually overcome many things we were previously choked on, so China still has significant opportunities in chip manufacturing equipment.

Relatively speaking, equipment is easier to reverse-engineer. Even in the worst-case scenario, we can disassemble existing lithography machines and study their construction. Even if reverse-engineered equipment performs much worse, there's always something to learn from it. But chips are very difficult to reverse-engineer through disassembly, and once made, if problems arise, they're hard to redesign.

China already has some布局 [positioning] and capabilities in chip design. For example, Huawei's HiSilicon can design and produce most of the major chips used in phones.

The flip side of being choked on the equipment end is that China's foundries have an opportunity to overtake on the弯道 [curve]. Why didn't chip manufacturing equipment companies develop as well before? Because equipment lacked opportunities to be tested in practice. If foundries adopt domestic chip manufacturing equipment, it's an opportunity to solve backup solutions. In the medium to long term, we may be able to solve the chip manufacturing equipment problem.

Looking at the materials end. Japan's semiconductor materials, including specialty gases and silicon wafer materials, largely come from China. China's total chemical product output ranks among the top globally, providing considerable raw materials to the world. So choking on materials is actually mutually damaging. The current problem for Chinese chip materials is insufficient refinement and purity, and low gross margins. Fine chemicals involve knowledge and technical issues, and also require practical experimentation to improve.

We need strategic定力 [resolve] and to fight a protracted war. I'm relatively optimistic — China will be able to solve the chip anxiety problem in the future.

Liu Can: In the chip materials field, FreeS Fund has also invested in related companies. As Chinese chip materials become more refined, domestic materials will gradually gain advantages. Specifically, which materials?

Yongcheng Yang: There are some new materials being invented and expanding their applications. For example, because of new energy vehicles, people have learned more about silicon carbide and gallium nitride.

Additionally, there are some newly developed materials, such as the next-generation semiconductor material — gallium oxide. Some Chinese universities and startups are already very close to Japan in materials R&D, and our talent积累 [accumulation] is no less than Japan's.

Another example is in the optical device field. FreeS portfolio company Aipai Xin Yan is working on thin-film lithium niobate materials. Thin-film lithium niobate is gradually being recognized by the industry as the best optical material, particularly for optical piezoelectric materials. Using thin-film lithium niobate to make modulators can achieve better performance than traditional silicon photonics and III-V semiconductors.

Liu Can: Let me imagine boldly — could thin-film lithium niobate become a much better optical material than silicon?

Yongcheng Yang: For light, thin-film lithium niobate is much better than silicon. But in terms of optical applications, silicon remains the most foundational material.

Light itself is a type of electromagnetic wave, a high-frequency electromagnetic wave with very excellent properties. In optical applications, the world's best communication systems, including high-capacity communications in data centers, all use optical signals for transmission.

For a long time, when humans have tried to control light, we haven't found a material suitable for controlling optical signals the way silicon controls electrical signals. In the future, we may be able to better control light through thin-film lithium niobate or other materials.

04 When Will We Have Our Own Lithography Machine?

Liu Can: Lithography machines are crucial for chip manufacturing. Currently there's a lot of attention on this, and it's widely considered very difficult — when will China be able to independently develop lithography machines? If we continue to be choked, will it affect China's chip process nodes?

Yongcheng Yang: It's hard to have a definitive answer. In lithography machines and other scientific developments, there are always偶然 [contingent] factors. Furthermore, China's ultimate breakthrough in chips may not necessarily be limited to lithography machines.

For advanced process nodes like 7nm, 5nm, or even the 2nm, 3nm that some people mention, different manufacturers have different definitions of what constitutes a given nanometer process. TSMC's industry standards differ from Intel's. Objectively speaking, reaching the most advanced nodes is somewhat more difficult.

But for processes above 8nm, we've basically solved the technology — now it's more about solving production capacity. Mature process nodes already cover most application scenarios, such as home appliance market demand. The chip-related industrial chain won't collapse. Combined with our massive market scale, even if we're not running first, we're in the first tier.

Liu Can: Then for 2nm, 3nm processes, if they're not serving the home appliance industry, what industries do they serve?

Yongcheng Yang: Smaller, higher-process chips are mainly used in digital circuits, more specifically CPUs. CPU structures are very complex and require higher integration to reduce cost and power consumption. But for other RF devices and optical devices, they don't need to reach nanometer levels — sub-micron is sufficient.

The reason high-process chips are getting so much attention now is mainly because we're being choked. But in terms of overall industry share, current demand for high-process chips isn't actually that large.

Liu Can: If we look from the design end, is global chip design dominated by the U.S.? China also has some companies布局 [positioned] in the EDA (electronic design automation) field. Around 2014, when the domestic semiconductor wave rose, there were already startups working on this. But we still have shortcomings in chip design — how should we break through?

Yongcheng Yang: From my observer's perspective, systematically replacing the U.S. in chip design is quite challenging. There's a view in the industry that software development isn't the big problem. What's key is having people who understand underlying physics, people who understand mathematics, and who are also very familiar with foundry processes. Only such people can do chip design well.

From the chip design perspective, what's the biggest problem these companies will face?

Being strangled in competition. On one hand, there are administrative, unreasonable measures from competitors or certain countries. But there's another reason that's easily overlooked: if you overly pursue profit, that will also strangle these startups. For Chinese semiconductor startups, especially those with their own brands on the design end, profitability perhaps shouldn't be an important goal in the company's early stages.

The semiconductor industry has developed to where it is today, and we're somewhat behind. There are several reasons at different levels.

First, the semiconductor industry will likely enter a phase of declining demand. The dividends of globalization are being impacted and squeezed by both subjective and objective factors. Overall industry demand declining is clearly not a good time for entrepreneurship. As a catch-up player, startups can hardly compete with existing giants in technology and other aspects.

Additionally, what did the global semiconductor market do in the last round of development? Consolidation. Giants formed monopoly situations by acquiring small companies. Competing with giants, small companies are far weaker in resource utilization efficiency and control. If a company has a single product line, a niche product with small market volume, achieving profitability becomes even harder.

In Europe's semiconductor market, large companies frequently acquiring small companies, with small company founders benefiting and successfully exiting, is common. China's semiconductor market is still in a phase of百家争鸣 [a hundred schools contending]. From a commercial perspective, most chip companies are still difficult to make profitable. Moreover, China's semiconductor market hasn't yet formed a healthy acquisition culture.

FreeS Fund has invested in many chip companies, and everyone is working hard to achieve profitability. But we should still take追赶技术 [catching up on technology] and合理布局产业 [rationally laying out industry] as primary goals. From an industry development perspective, I hope chip companies won't care too much about profitability early on. But this doesn't depend only on the chip companies themselves — it also involves the entire industry's认知 [understanding] and national policy orientation.

The globalized, market-competition-based regulatory situation currently doesn't exist in the semiconductor industry. This means that beyond pursuing profitability, we need to change our thinking and pay more attention to technology progress itself.

05 The CHIPS Act Has Been in Effect for Nearly a Year — What Impact Has It Had on the Global Chip Industry?

Liu Can: When policy supports industry development, perhaps there shouldn't be硬性要求 [hard requirements] for the profitability or revenue of companies at different development stages. What's more important is laying a solid industrial foundation and building up talent accumulation.

Looking back at the CHIPS Act that the U.S. introduced in 2022, despite its advantages in certain segments of the supply chain, its fundamental purpose was still to bring more of the chip industry back onshore through legislation. From your perspective, has it had any real impact on the global chip industry today?

Yang Yongcheng: As the global industrial hegemon, the U.S. has attracted many fabs to set up operations through administrative subsidies and market competition. But how exactly are these subsidies allocated? Who gets them? How confident can a fab be about actually receiving the money? And can they afford the price they'll have to pay? There was news this year that the U.S. is requiring companies receiving more than $150 million in subsidies to share "excess profits" with the government — are chip companies actually willing to do that?

I've always believed that using administrative means to attract these companies to the U.S. could lead to problems. Why did the most formidable companies in home appliances and light manufacturing leave the U.S. in the first place? Fundamentally, because the efficiency of its industrial environment is very low.

Fabs are, to a large extent, a chemical industry — you need to deposit material layer after layer, apply photoresist, and so on. If the U.S. wants to retain chip manufacturing, it needs a lot of labor. But how many Americans are actually willing to work in the chip industry? The market already made this decision years ago. After industries like automotive left the U.S., there was no reversal of that trend.

When competing through direct commercial means, China is not at a disadvantage in the semiconductor industry. What hurts us most are direct administrative orders, like the sales ban on China — that causes us direct damage.

Liu Can: So the CHIPS Act isn't the main reason for the poor performance we're seeing in the global wafer market right now — is that the right way to understand it?

Yang Yongcheng: It's mainly due to overall demand decline. In semiconductors, the American economic model is fabless — these are asset-light businesses that can make money relatively faster, simpler, and smarter, so American industry achieved overflow through this approach. Meanwhile, we're doing the hardest work in the supply chain.

Other countries also have their own roles and capabilities in the industry chain. Japan, for example, excels at producing semiconductor materials. Technology, markets, supply chains, equipment, materials — China and the U.S. both have these things, so everyone participates and benefits from it.

But now the situation is that the U.S. has "flipped the table." The reason: even though I'm making easy money, I'm worried this can't continue. To ensure our own security, we need to rebuild or accelerate the development of our weak points, especially in semiconductors. Fundamentally, this is being forced to reinvent the wheel. Before, we could just purchase components across the entire supply chain. Now we can't.

What's interesting is that as American allies, Europe and Japan have also panicked and want to build their own complete semiconductor industries. So to some extent, the U.S. has broken the chain that originally supported high-speed global economic development.

There's another factor. We discussed this in a previous episode: one of the major pillars of the semiconductor industry, particularly consumer products, hasn't seen many new categories emerge. Demand for new categories has temporarily hit a ceiling. (For more discussion on chip demand, see "The Entrepreneurial Challenges and Opportunities Behind the 'Chip Shortage'" | FreeS Research · Chip Series)

Because of this panic, everyone is reinventing the wheel. Currently, Europe accounts for 10% of global chip capacity, and they've stated they want to increase this to 20% by 2030 — very ambitious. But my guess is that they're mainly playing defense, trying to prevent European semiconductor companies like Infineon Technologies and STMicroelectronics from being lured away by U.S. policy.

So who will be left standing at this point? Companies that don't develop entirely according to traditional market rules might survive. To put it simply: in a disaster year, it's not necessarily the strongest who survive — it's those who consume less or those who are fighting for survival.

06 Will AI-Driven Chip Demand Change the Underlying Chip Market?

Diane: In this wave of AI, we're using more underlying computing power, more chips — do you think this counts as something that could change demand at the foundational level of the chip market?

Yang Yongcheng: For the chip industry as a whole, I don't think it will have that large of an impact.

Looking at the history of AI development, every innovation has made people ecstatic. The times when it most easily finds application and makes new breakthroughs are definitely when it's solving problems that humans struggle with — but up to now, there haven't been enough of these cases. We're still looking for such points, and many people aren't yet convinced that AI's current capabilities can shoulder this responsibility.

Another factor is that when demand explodes, capacity is insufficient, so everyone expands production. But after expanding capacity, people discover that from the demand side, there isn't actually that much demand. So on this point, I have some doubts about its development.

Before a technological revolution happens, before something like GPT emerges, we always underestimate its potential because we can't predict that it will create a new hotspot. But it definitely will, and we inevitably overestimate it — like the uncertainty principle. If we could measure it accurately, the world wouldn't be like this anymore, and it wouldn't be as interesting.

Liu Can: After talking with you today, my biggest takeaway is that whether you're an entrepreneur in China's semiconductor industry or looking at established giants across global supply chains that have already formed competitive advantages — if everyone wants to take one more step forward, we can all have a bit more confidence, because there are still many niche segments in this industry where people can advance further.

Of course, current political turbulence will have unpredictable impacts on this industry. But considering our current foundational capabilities and talent accumulation, from the perspective of China independently developing chips, we have confidence that there will be better development in the future.

Yang Yongcheng: Overall, I'm very confident in China's semiconductor industry. When observing these startups, different stages and different parts of the chain have different characteristics, so we need to maintain objective strategic resolve. The home appliance and mobile phone industries also grew this way — it's a process.

I once told entrepreneurs something: everyone hopes opportunity goes to the prepared person, but in reality, the true entrepreneur is probably the one who wasn't prepared. So when we encounter problems, we need to firmly believe that we can solve them and succeed, and firmly believe that we will keep trying.

Interactive Giveaway What do you think about China's chip market? Does your industry have chip anxiety? Welcome to share your observations and thoughts in the comments. By 17:00 on June 21, we will give Dedao reading cards to the 2 users with the most likes and the 3 users with the most heartfelt comments (reading cards valid until November 30, 2023).

3D Printing at 40: How Far From Niche Technology to Mass Application? | FreeS Report 31

Li Xiang × Li Feng: Why Did ChatGPT Emerge Today? What Happens Next? | Li Feng Column

Was Elon Musk Right? Will LiDAR Make It Into Cars? | FreeS Research · Chip Series

The "Chip Shortage": Entrepreneurial Challenges and Opportunities | FreeS Research · Chip Series

Star the FreeS Fund WeChat account for timely business insights.