The Hammer and the Dance: Where Healthcare Investment Goes Next Under COVID-19 | FreeS Fund

The unexpected arrival of COVID-19 turned out to be a shot in the arm for the healthcare industry.

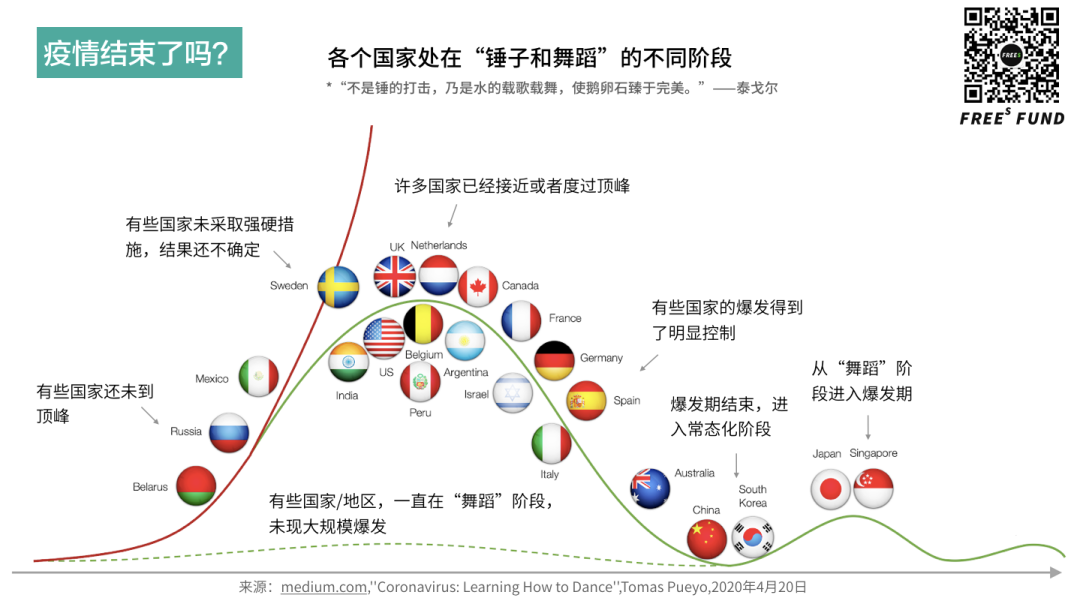

Tagore once wrote, "It is not the hammer's blows, but water's song and dance, that polishes the pebble to perfection."

COVID-19 continues to exert its lingering force, while countries and regions find themselves at different stages of the "hammer and the dance."

China's COVID-19 prevention and control situation has further consolidated its positive trajectory, with response efforts transitioning from emergency mode to normalized operations. Yet looking globally, the pandemic continues to spread. While European and American countries have passed their peaks, reopening economies makes a second wave of infections increasingly likely. South America, Africa, India, Russia, and other regions remain in periods of rapid outbreak. The virus knows no borders; the world shares the same fate. Humanity faces an enormous challenge.

In this piece, we will review how COVID-19 spread globally, examine the pandemic's impact on the biopharmaceutical industry, and explore investment opportunities in the post-pandemic era.

Before diving in, here are a few key takeaways:

- The COVID-19 outbreak unexpectedly gave the healthcare industry a shot in the arm, with market sentiment and capital supply both helping to ease the growing pains of an adjustment period.

- The accumulation and breakthrough of underlying technologies will be the next hotspot in biopharma.

- First-in-class drugs developed independently by Chinese companies will become a focal point for both industry and market attention over the next five years.

- The healthcare industry has entered the big data era, which will truly transform how we intervene against disease, manage health, and understand life itself.

We hope this offers fresh perspectives. We welcome continued exchange and discussion. Feel free to reach out to Yikai Wang at yikai@freesvc.com.

/ 01 / Defeating the Pandemic Globally Will Depend on the Healthcare Industry

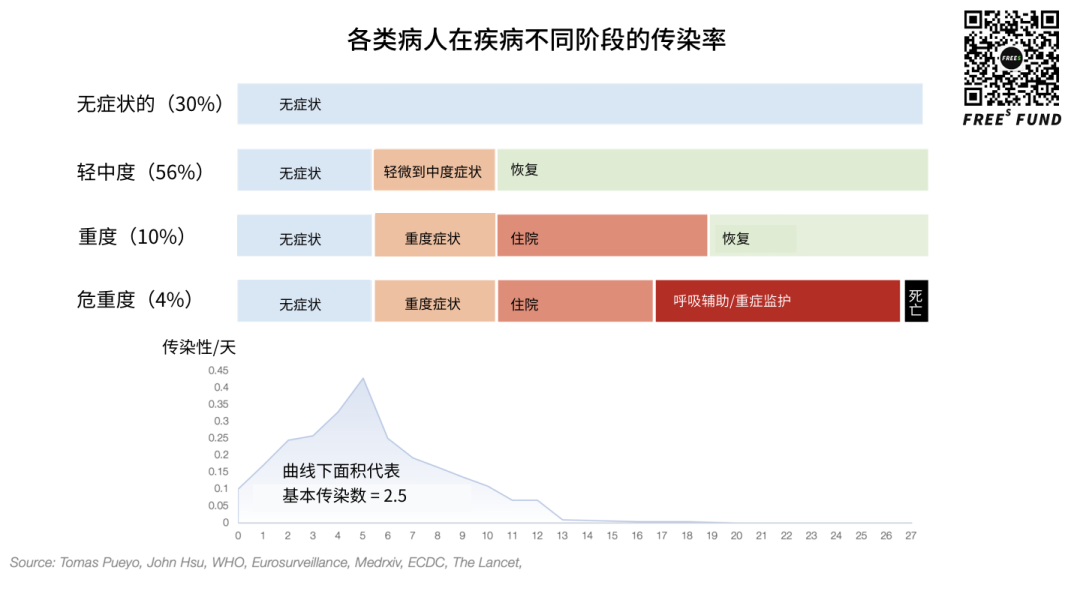

The novel coronavirus is slightly more contagious than SARS and considerably more so than the flu, with severe case and mortality rates far exceeding those of influenza. Once patient numbers surge, causing healthcare system overload and medical staff infections, a vicious cycle forms that further drives up mortality.

When facing the spread and ravages of a novel virus, the "four earlys" principle — early detection, early reporting, early isolation, early treatment — applies universally. From the January 23 lockdown of Wuhan to contain the outbreak there, to controlling the situation in Hubei province, to coordinated prevention and control elsewhere, and then to the early February deployment of makeshift hospitals to ensure "all who should be admitted are admitted, all who should be treated are treated" — by around February 4-5, China's new case numbers had peaked and begun to decline.

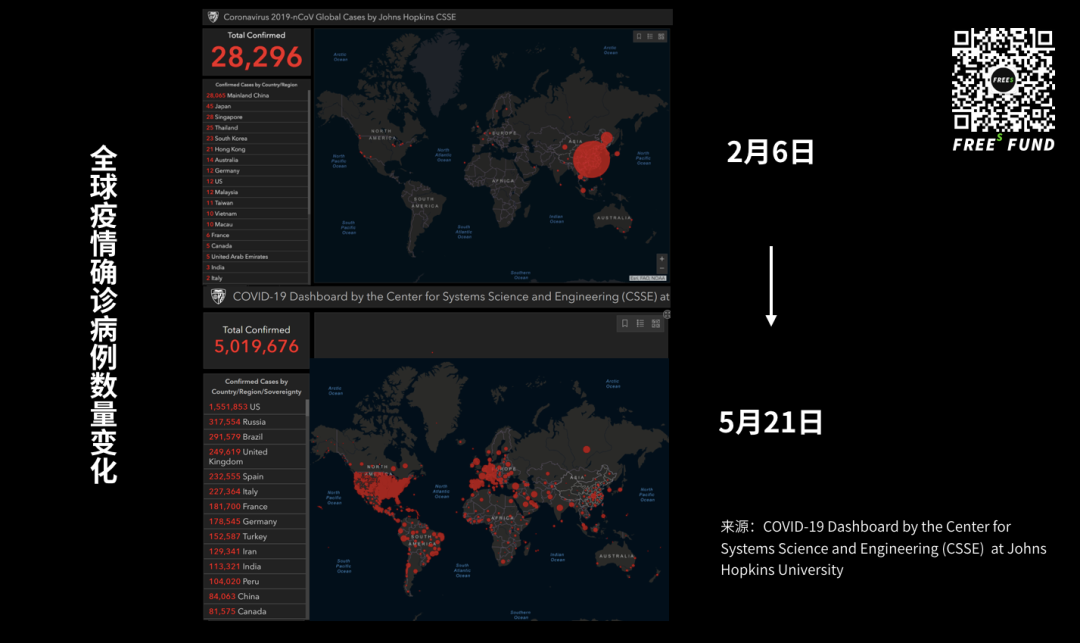

Regrettably, the pandemic still exploded globally. This was partly determined by the virus's own characteristics — for instance, patients are highly contagious even when asymptomatic or experiencing mild symptoms — and partly due to differences in national conditions and public sentiment, making it difficult for other countries to implement the thorough social distancing measures seen in China. Under these circumstances, if the virus does not die out on its own, the hope for ultimate containment and global return to normalcy rests on the healthcare industry.

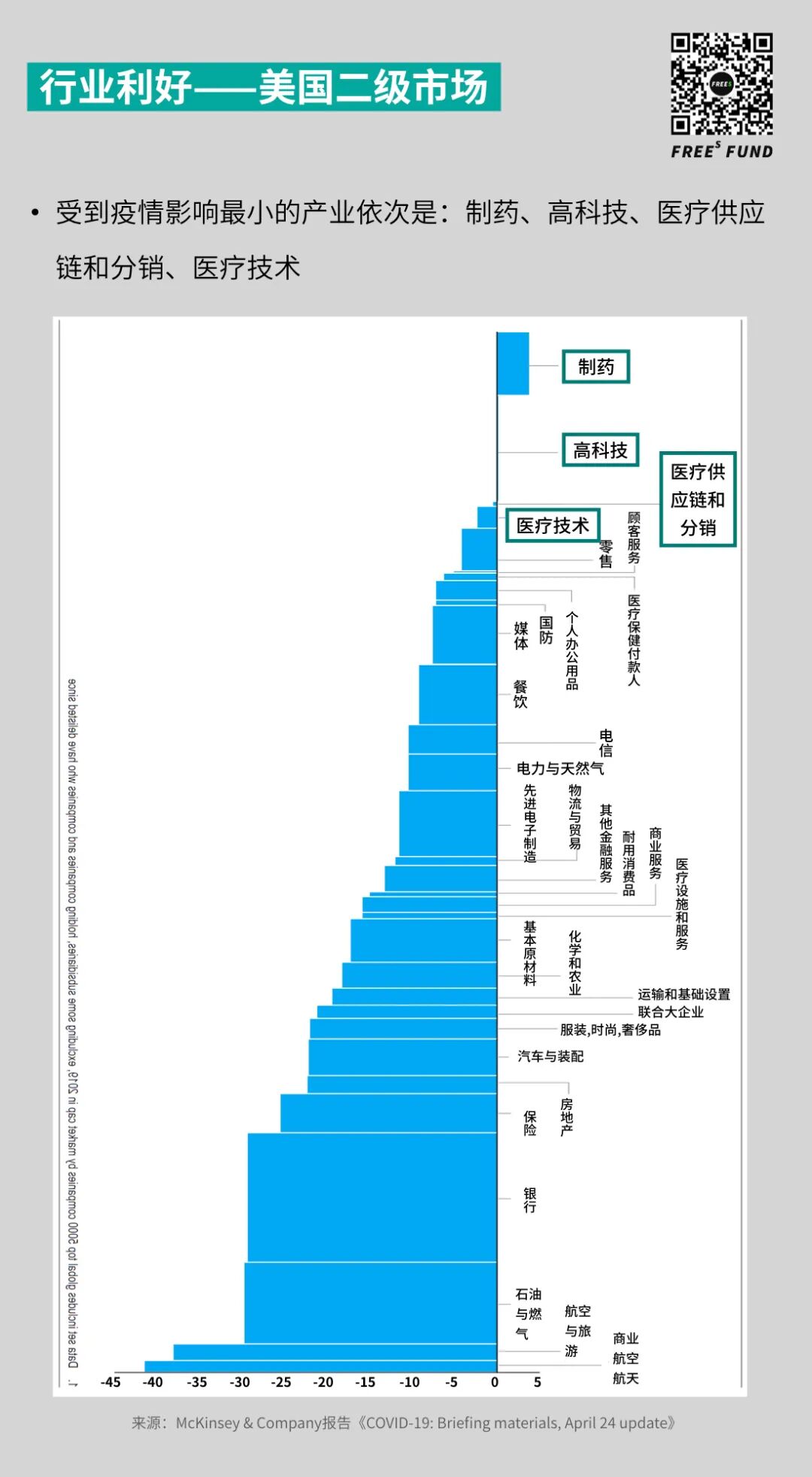

Whether in Shenzhen and Shanghai, New York, or stock markets worldwide, the pharmaceutical sector has been the least impacted by the pandemic, with the strongest resilience. Companies related to epidemic prevention materials and drugs have even risen against the trend. This reflects, to some degree, the market's stress-driven panic and its reliance on the healthcare industry.

Moreover, while routine R&D work has slowed or been interrupted due to social distancing, COVID-19-related research and clinical trials have grown exponentially. According to statistics, COVID-19-related papers numbered 11 at the end of last year, increasing to 8,276 by late April; registered clinical trials numbered fewer than 10 at the end of January, exceeding 2,000 by the end of April; and regulatory agencies worldwide accelerated approval of hundreds of COVID-19 test kits for epidemic prevention and control.

Such large-scale global mobilization and formidable R&D capabilities have given humanity its first opportunity to race against viral spread, yielding increasingly deep understanding of the virus's origins, transmissibility, detection, pathology, treatment, and prevention. Over the past few months, humanity has made positive progress in antiviral drugs, critical care interventions, and preventive vaccines — undoubtedly easing panic and stabilizing market expectations.

Discussion

Q: Specifically for the biopharmaceutical industry, will the US and China decouple? Feel free to hit "Like" at the end of this article, and reply "医药" in the WeChat official account backend to see our preliminary answer.

/ 02 / Healthcare Weaknesses Exposed by the Pandemic and the Path to Domestic Substitution

The healthcare industry has provided powerful tools and weapons for our response to the virus. At the same time, this sudden pandemic has been a comprehensive test of every nation's healthcare system.

Looking back to when the outbreak first began, we completed viral isolation and sequencing at the first opportunity, identifying the novel coronavirus as the cause of this unexplained pneumonia. Nucleic acid test kits were then developed, enabling effective patient differentiation and diagnosis. Simultaneously, we conducted a series of research studies on the virus's structural characteristics, infection mechanisms, possible intermediate hosts, and potential therapeutic drugs, making positive progress and promptly providing information and reference for countries worldwide responding to COVID-19 — earning broad recognition from international peers.

Compared to fighting SARS in 2003, our prevention and control capabilities and treatment standards have advanced enormously. However, while affirming these achievements, we should also soberly recognize certain shortcomings in the healthcare industry.

▍Insufficient reserves of innovative drugs, with clinical trial systems needing improvement.

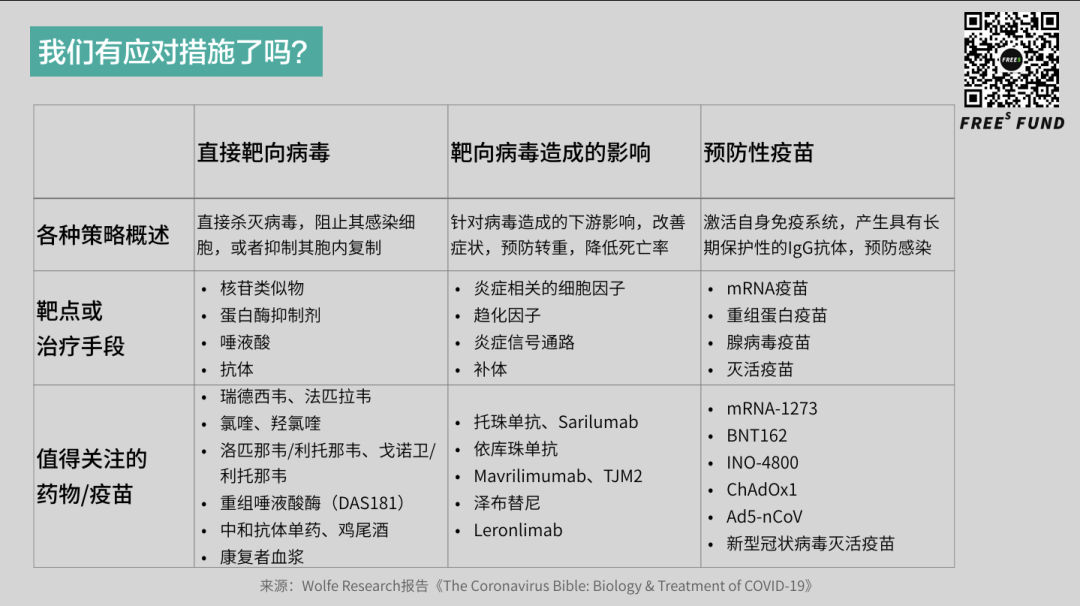

By the end of April, over 260 drugs were in development globally for COVID-19 treatment, more than half of which were not originally developed for COVID-19 — including repurposed approved drugs and indications expanded for unapproved drugs. Even so, the vast majority of drugs are being developed and advanced by European and American companies. Only around 50 involve Chinese companies, such as domestic innovative drug enterprises including Hengrui Medicine, BeiGene, Innovent, Ascletis, Junshi, I-Mab, and Harbour BioMed.

Notably, while we have few innovative drugs available for COVID-19, the number of clinical trials conducted has far outpaced other countries. According to statistics, by the end of April, China had over 400 COVID-19 clinical centers, far exceeding the US's 22; China had launched over 700 clinical trials, while the US had only 300-plus.

However, among these 700-plus clinical trials, the National Medical Products Administration had approved fewer than 10. The vast majority were investigator-initiated, with many having insufficient rationale and less-than-rigorous trial design. Such a large number of clinical trials consumes substantial clinical resources, causing potentially meaningful trials to be delayed or even unable to complete due to insufficient patient recruitment.

In response to this chaos, the State Council issued an emergency notice on February 25 to regulate and halt such practices. Additionally, thanks to the "compassionate use" mechanism, remdesivir was first used to treat COVID-19 in the United States, while this system still needs further development and improvement in China.

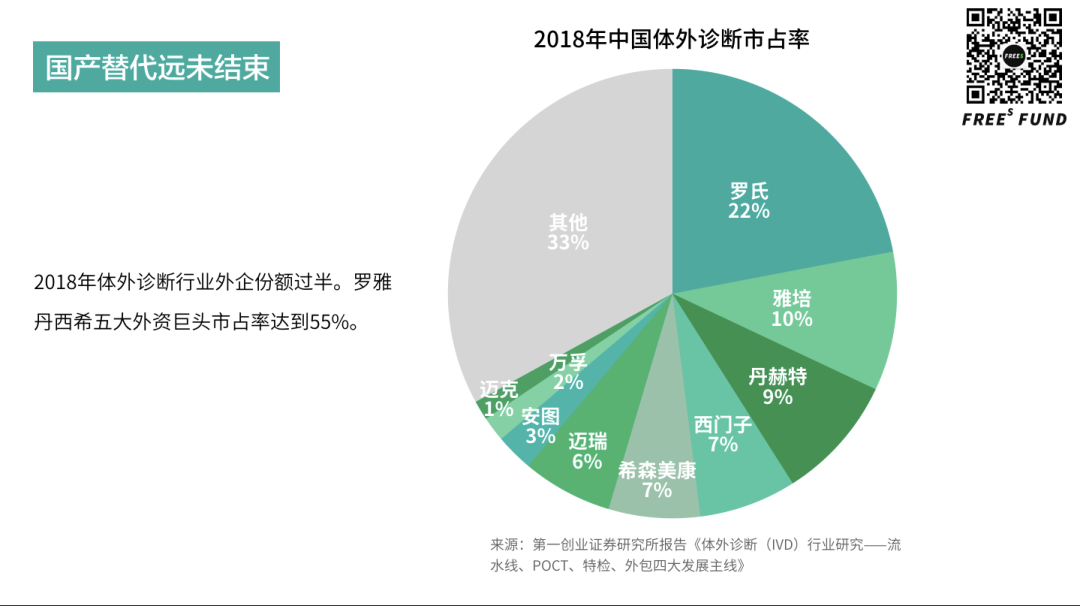

▍Limited rapid nucleic acid testing capacity, with high-end consumables and equipment largely dependent on imports.

Nucleic acid testing falls in the molecular diagnostics field. Although in 2018 domestic Chinese companies accounted for approximately 70% of PCR diagnostic reagent production, high-end materials are heavily import-dependent, with normal supply even harder to guarantee during the pandemic; for PCR instruments, imported brands hold 80% market share.

Furthermore, since the outbreak began, the nucleic acid testing we have used has largely relied on laboratories or clinical testing centers, with limited point-of-care testing (POCT) capacity. Addressing this issue, the Central Leading Group for COVID-19 Response convened a meeting on May 7, calling for concentrated efforts on key breakthroughs to accelerate nucleic acid testing capacity — particularly pushing for expanded production of rapid nucleic acid testing equipment with short turnaround times and no laboratory requirement.

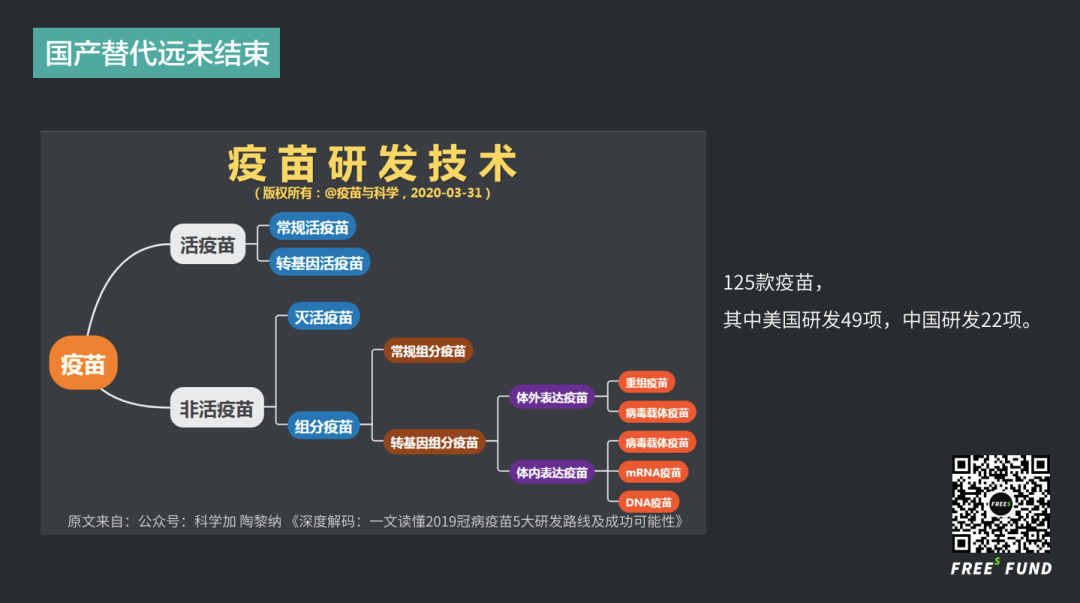

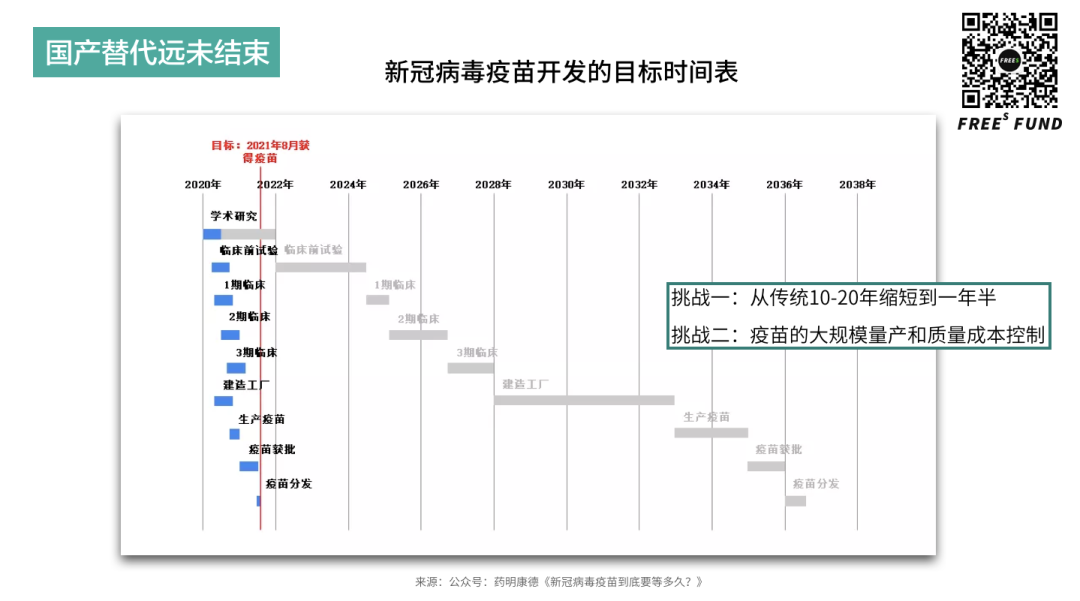

▍Novel vaccine platform technologies difficult to scale, with bottlenecks in mass production and quality/cost control.

By the end of April, 125 COVID-19 vaccines were in development globally, with China developing 22 — fewer than the US's 49. Our progress with inactivated vaccines has been relatively rapid. CanSino Biologics, in collaboration with the Institute of Biotechnology of the Academy of Military Medical Sciences, has also advanced their adenovirus vector vaccine (Ad5-nCoV) to Phase II clinical trials.

Vaccine efficacy is one aspect; whether mass production and quality/cost control can be achieved is another challenge. Beyond their own manufacturing capabilities, major European and American vaccine companies have CMO partners like Catalent, Emergent, and Lonza with mass production capacity. According to Johnson & Johnson, their COVID-19 adenovirus vector vaccine in development is projected to reach 1 billion doses in capacity, with market price controlled below $10 per dose. Unlike the traditional 10-20 year vaccine development cycle, countries hope to ensure vaccine availability within 1 to 1.5 years in response to this pandemic — an enormous challenge for vaccine R&D, production, and distribution.

Additionally, mRNA vaccines, an emerging platform technology that has gained prominence in the past two years, are highly promising. While domestic companies are also exploring this direction, the R&D system remains insufficiently developed and production capabilities relatively weak.

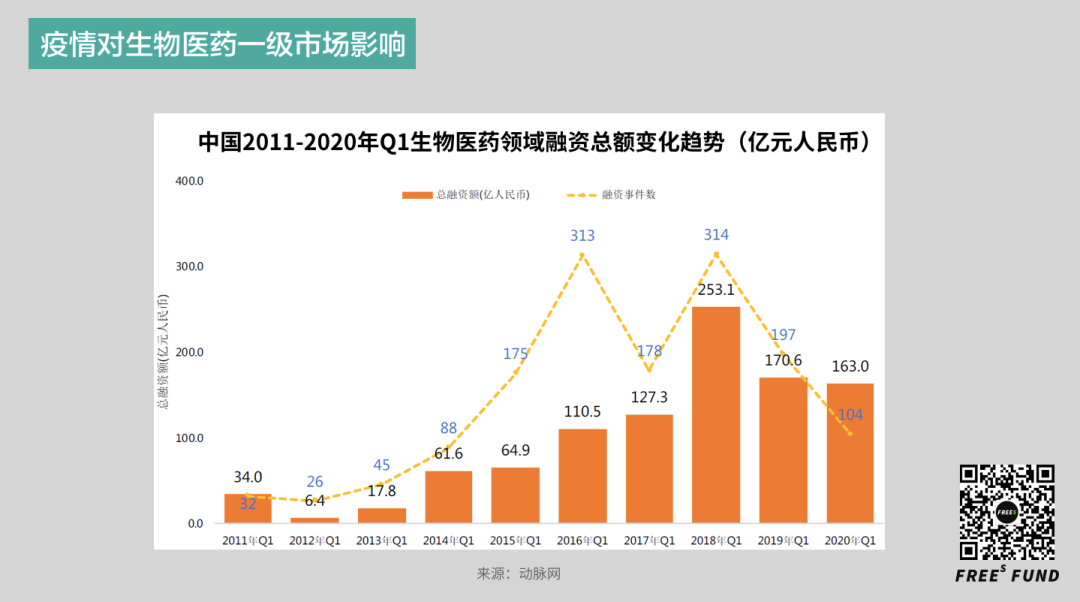

Starting from 2013, with the introduction of a series of national policies and regulations, the pace of domestic substitution in healthcare accelerated, and primary market financing surged. According to statistics, healthcare industry primary market financing grew rapidly from 3.9 billion yuan in 2013 to 99.2 billion yuan in 2018 — a 25-fold increase in five years.

On one side, numerous companies clustered around popular targets or products for fast-follower innovation; on the other, fundraising tightened starting in 2018, primary market financing became more difficult, project valuations compressed, and domestic substitution entered an adjustment period.

Against this backdrop, the COVID-19 outbreak unexpectedly gave the healthcare industry a shot in the arm, with both market sentiment and capital supply helping to ease the growing pains of the adjustment period to some degree.

According to VBData, in Q1 2020, 634 investment events occurred across the new economy sector, down 44.5% year-over-year; total transaction value was 119.1 billion yuan, down 31.3% year-over-year. The healthcare sector was not immune — Q1 financing events numbered 104, down noticeably from 197 in the same period last year. However, this quarter saw a relatively large number of major financing transactions, with total financing reaching 16.3 billion yuan, nearly on par with Q1 2019. By quarter's end, four additional pharmaceutical companies had listed on the STAR Market, with Zai Lab becoming the first loss-making company to apply for listing under the fifth set of standards, making it the first unprofitable listing on A-shares.

Additionally, according to ChinaVenture Research Institute statistics, the VC/PE fundraising market warmed in April, with the healthcare industry becoming a capital focus in both primary and secondary markets. In April, the healthcare sector completed 57 transactions, ranking first among all industries; transaction scale exceeded 9 billion yuan; and three more companies went public.

If ample primary market capital supply and diversified secondary market exit channels can help the domestic substitution path proceed more steadily and further, then the gaps revealed during the pandemic point the direction for next-step industry development and capital deployment.

03 The Next Wave of Healthcare Investment Opportunities: From Fast-Follower to Original and Systemic Innovation

While continuing to support domestic substitution, FreeS Fund is also very optimistic about original innovation in biopharma.

In recent years, domestic biopharmaceutical companies have primarily developed me-too drugs — new drugs with independent intellectual property rights targeting targets already validated abroad, with efficacy comparable to first-in-class counterparts.

Developing me-too drugs requires less investment, shorter timelines, and has higher success rates — a first step in the pharmaceutical industry's upgrade from generics to innovative drugs. However, as more companies participate and validated targets remain relatively limited, clustering around the same targets has emerged, with serious product homogenization, difficulty competing globally, and rapidly diminishing investment returns.

In the next stage, capital will increasingly favor higher-risk, higher-return first-in-class products. Beyond investment returns, this judgment is based on two additional considerations.

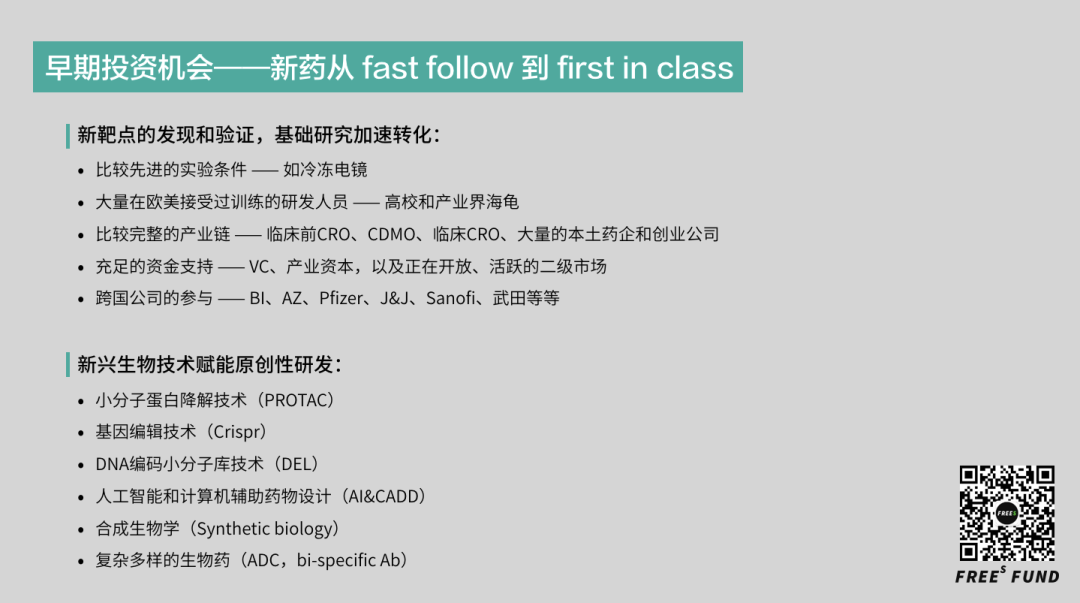

From an industry accumulation perspective, ample R&D funding has given us world-class scientific research infrastructure; multi-year talent recruitment programs have attracted large numbers of researchers who received systematic training in Europe and America to return and conduct basic and translational research; and as multinational pharmaceutical companies have outsourced substantial R&D and production work to China — from preclinical CRO to clinical CRO to CDMO — the domestic new drug R&D industry chain has become quite complete.

From market competition and corporate strategy perspectives, if innovation from China offers lower costs and higher efficiency, its attractiveness to multinational pharmaceutical companies will exceed that of US domestic options. Leading domestic new drug companies, after generating profits from existing products, will also be more willing to invest more in and support original innovation — as this is the foundation and source of their long-term competitiveness.

Based on the above analysis, we believe that first-in-class drugs independently developed by Chinese companies will become a focal point for industry and market attention over the next five years.

As biotechnology accumulates and breaks through, Europe and America have seen the emergence of numerous so-called platform companies, attracting investor attention and pursuit. Such companies are typically built on a general-purpose technology with the continuous ability to generate innovative products; they often focus on intellectual property generation and preclinical/early clinical research, with clinical-stage development primarily handled by closely partnered large companies. Moderna, the global leader in COVID-19 mRNA vaccines, is such a platform company based on mRNA synthesis and delivery technology, focused on developing mRNA medicines.

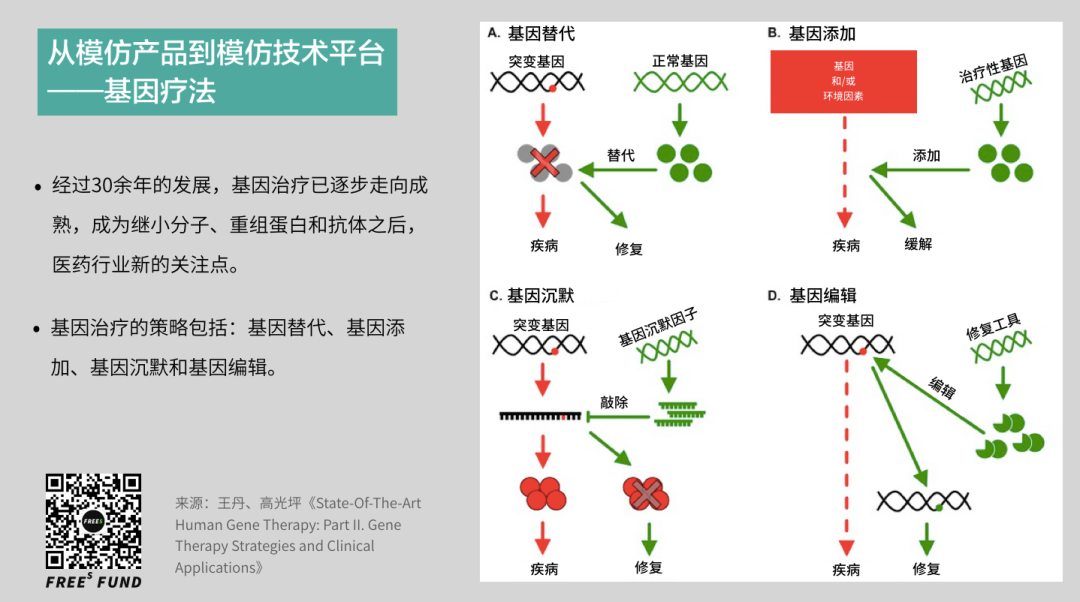

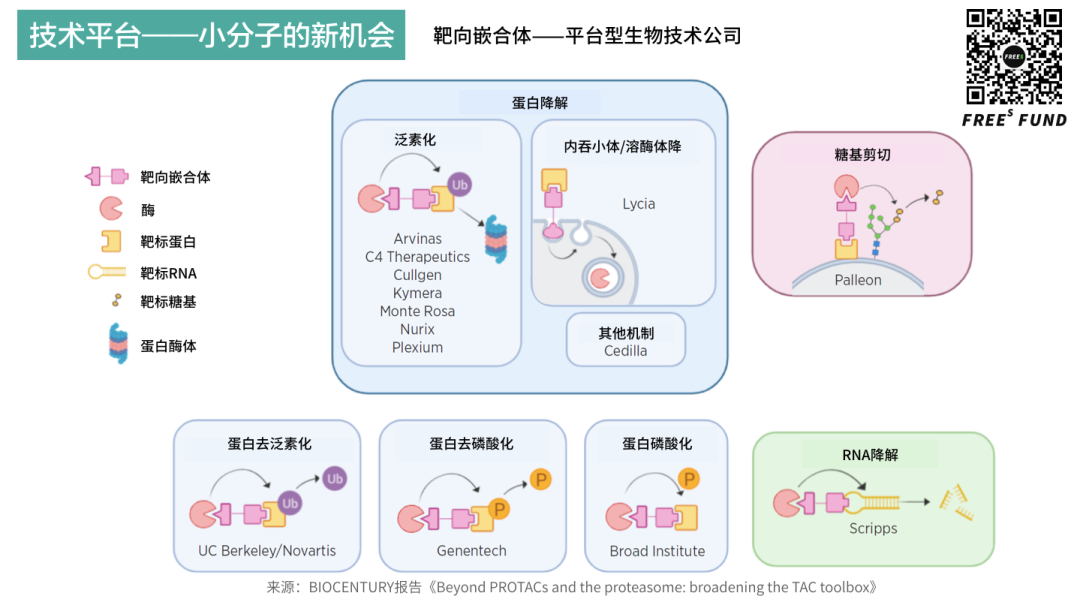

Beyond mRNA, novel biotechnologies including gene therapy, small nucleic acids, viral and non-viral vector drug delivery, and protein degradation have also spawned numerous star companies with notable performances in capital markets and M&A transactions.

Unlike developing a first-in-class drug for a new target, platform companies often require the integration of multiple underlying technologies, with higher demands for systemic innovation and industrial chain collaborative innovation. For mRNA vaccines, for example, both mRNA optimization and synthesis and lipid nanoparticle research and preparation are needed — ultimately, a stable, controllable, scalable manufacturing process route is essential for drug approval.

As more domestic companies begin to lay out in this direction, with systemic innovation and domestic substitution proceeding simultaneously, China's healthcare industry will turn a new page.

04 The Healthcare Industry Enters the Big Data Era

The pandemic will eventually pass, but its changes to people's lifestyles will persist. The impact and disruption to offline healthcare during the pandemic has instead become a catalyst for internet healthcare to capture user mindshare and cultivate user habits. That internet healthcare has entered an accelerated development phase is now industry consensus.

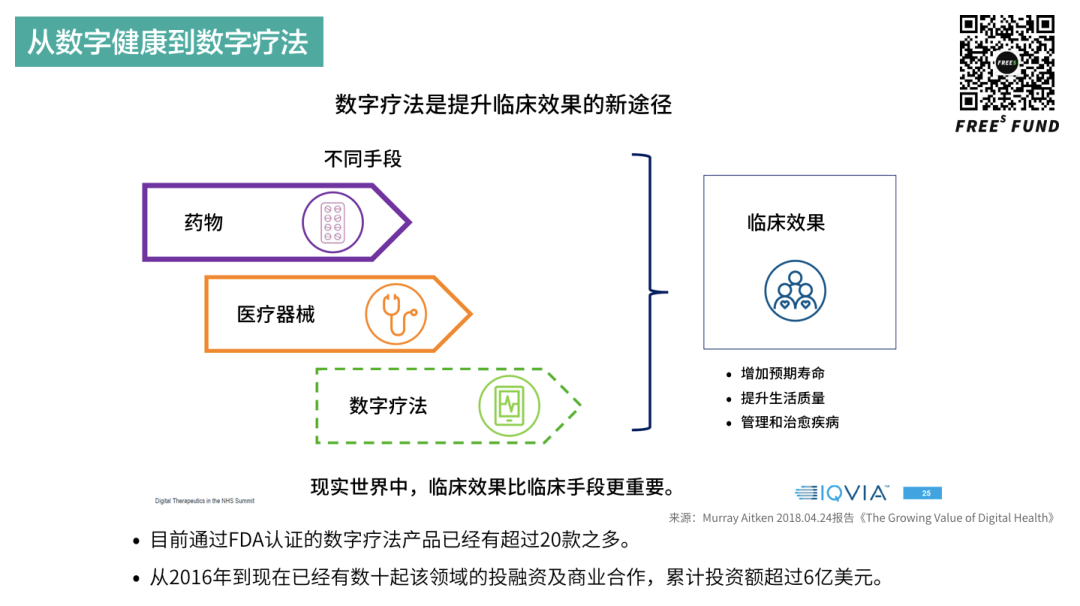

At the same time, digital therapeutics are quietly rising. Thanks to rapid technological advances, digital therapeutics are software-based therapies that help patients prevent, manage, or treat disease. Combined with traditional drugs and medical devices, digital medicine will bring more efficient, more accessible treatment approaches.

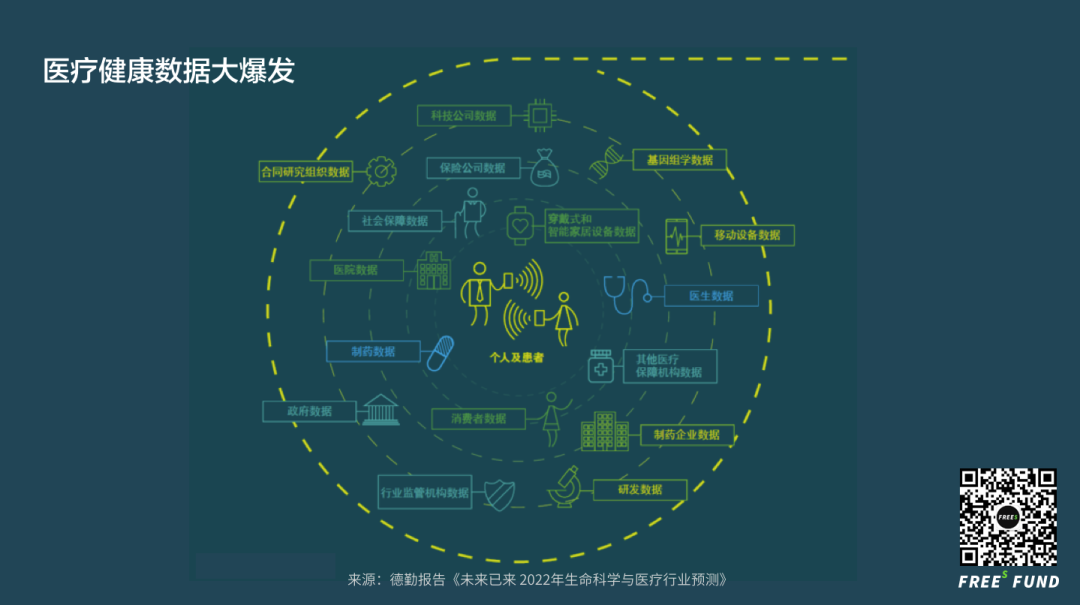

If we view this trend through the lens of data, virtually all health-related information has become digitized and datafied. From human genomic and other omics data, vital signs monitoring data, disease onset and diagnosis/treatment data, real-world data, to pharmaceutical R&D data, physician and hospital data, insurance company data, and social security and regulatory data — healthcare and health-related data will become important production factors and core corporate assets.

Big data plus artificial intelligence have enormous application prospects in diagnosis, treatment, prognosis, health management, medical insurance pricing, actuarial science, drug sales, and new drug R&D — and this will truly transform how we intervene against disease, manage health, and understand life itself.

Beyond deep mining and application, there remain many issues to address regarding data rights confirmation, open sharing, free flow, and data security — which also contain numerous investment opportunities. Of course, the healthy and sustainable development of data as a production factor requires necessary government regulation and Chinese data science reaching internationally leading levels as foundation and backing — particularly so for the healthcare big data industry.

05 Closing Thoughts

Facing social isolation during the pandemic, many raised the question: "Human right or human left?" This brings to mind the famous lines by the great Hungarian poet Sándor Petőfi: "Life is dear, love is dearer. Both can be given up for freedom."

Of course, a poet living in the first half of the 19th century could hardly have imagined that even when facing such a vicious virus as COVID-19, humanity has both the capability and the will to defend free life and love. Undoubtedly, this confidence comes from a strong healthcare industry. We shall see.

Summary

1 The COVID-19 outbreak unexpectedly gave the healthcare industry a shot in the arm, with both market sentiment and capital supply helping to ease the growing pains of the adjustment period to some degree.

2 The next wave of investment opportunities in healthcare lies in the shift from fast-follower innovation to original innovation and systemic innovation.

3 The healthcare industry has entered the big data era, which will truly transform how we intervene against disease, manage health, and understand life itself.

Discussion

Q: Specifically for the biopharmaceutical industry, will the US and China decouple? Feel free to hit "Like" at the end of this article, and reply "医药" in the WeChat official account backend to see our preliminary answer.

(Feel free to read, share, and hit "Like." For reprint permission, please reply "转载" to learn reprint rules, and contact FreeS Little Rui [ID: freesfund] for authorization. Copyright belongs to FreeS Fund.)

▲ FreeS Report 16: The Truth About Early-Stage Healthcare Investment and China Speed | FreeS Fund

▲ FreeS Report 15: Life's Gamble — The Adventurous Journey of Drug Development | FreeS Fund

▲ One Chart to Understand Changes and Opportunities in China's Industrial Chain | Li Feng Column

▲ One Chart to Understand Globalization or Deglobalization | Li Feng Column

▲ After the Pandemic, a New Era for "Good Companies" | FreeS Fund