How to Capture Category Dividends in Consumer Entrepreneurship? | FreeS Research

How to Lead the Pack?

Anyone following consumer entrepreneurship has likely come across the term "category dividend."

The dividends in consumer sectors come in many forms, spanning everything from policy to distribution channels. But the biggest dividend of all isn't the traffic dividend people talk about so often — it's the category dividend.

Today's discussion centers on exactly that:

- What exactly is a category dividend?

- How does a category dividend form?

- How can consumer entrepreneurs and investors capture it?

We hope this offers a fresh perspective.

Entrepreneurs and industry experts are welcome to continue the conversation with the author, Yingzhu Jiao (jiaoyingzhu@freesvc.com). We're also looking for people with industry backgrounds interested in consumer investing to join our team (hr@freesvc.com).

A Brief History of the Beauty Industry

By Yingzhu Jiao (jiaoyingzhu@freesvc.com)

Feng Li (feng@freesvc.com)

**/ 01 / **

Incremental Markets: Where Category Dividends Live

What kinds of sectors or industries have category dividends? Here's a starting thesis: an industry has experienced one or more inflection points and is maintaining or entering a phase of growth.

Incremental markets typically mean bigger and more abundant opportunities. When an industry is expanding from small to large, the gap between discovered demand and fulfilled demand creates entrepreneurial opportunity.

To determine whether a category or its sub-segments currently sit in an incremental or stock market, compare its year-over-year growth rate for a given period against China's total retail sales of consumer goods during the same period:

- At or below the national total retail sales growth rate? It's a stock market.

- Above the national total retail sales growth rate? It's an incremental market.

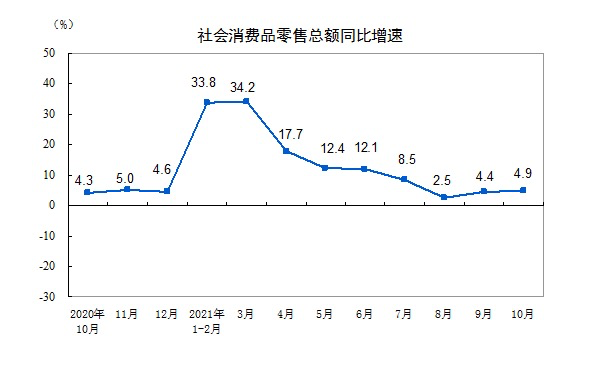

For example, National Bureau of Statistics data shows that from January to October 2021, China's total retail sales of consumer goods reached 35.8511 trillion yuan, up 14.9% year over year.

▲ Image source: National Bureau of Statistics

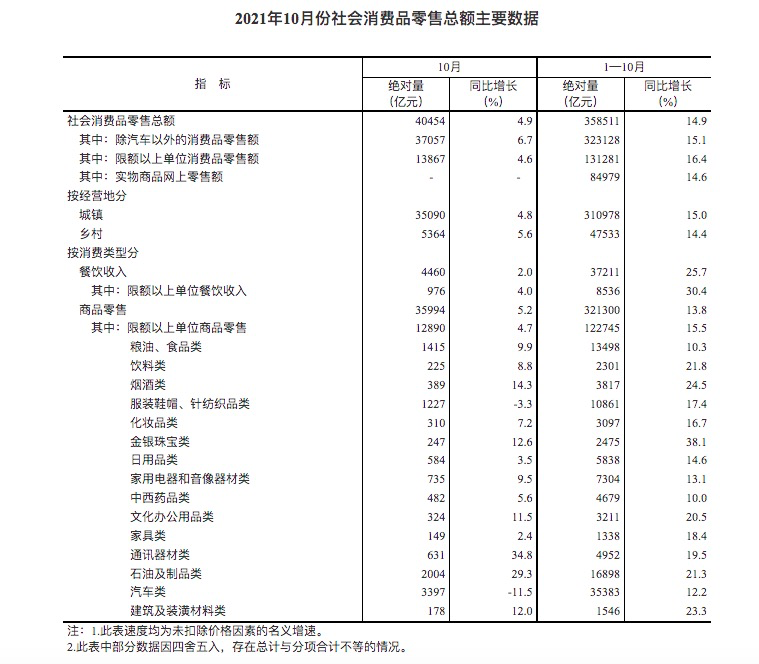

Take cosmetics during the same period: domestic cosmetics retail sales hit 309.7 billion yuan, up 16.7% — beating the 14.9% overall retail growth rate and signaling clear incremental momentum. China has, in fact, become the world's fastest-growing cosmetics market.

What does a stock market look like? Consider automobiles. From January to October 2021, auto retail sales grew 12.2%, below the overall retail growth rate. Meanwhile, data from the China Automobile Dealers Association showed 8.4342 million used cars traded nationwide in the first half of 2021, up 52.89% year over year — suggesting China's auto market was gradually entering a replacement-driven stock phase.

▲ Image source: National Bureau of Statistics

That said, supply-demand dynamics are constantly shifting, and stock and incremental markets frequently nest within and transform into each other.

▲ Image source: China Association of Automobile Manufacturers

Even though the auto industry as a whole entered stock-market territory in 2021, new energy vehicles within it were forming their own incremental market. According to the China Association of Automobile Manufacturers' October monthly briefing, cumulative vehicle sales from January to October 2021 reached 20.97 million units, down 9.4% year over year — but NEV sales hit 2.542 million units, surging 134.9%.

▲ Image source: China Association of Automobile Manufacturers

**/ 02 / **

What Is a Category Dividend? The Case of Colored Contact Lenses

As noted, category dividends represent the biggest dividend in consumer sectors. Let's look at two examples.

When people started embracing healthier eating and seeking low- or no-sugar diets, sugar-free flavored sparkling water emerged and took off. That's a category dividend.

Or consider how prolonged mask-wearing during COVID shifted women's makeup focus from full-face to eye makeup, sparking explosive growth in colored contact lenses and eyeshadow within cosmetics. That's also a category dividend.

Beyond sugar-free sparkling water and colored contacts, sub-segments that have grown against the headwinds in recent years — nuts, coffee, and others — have typically ridden category dividends.

Compared to the traffic dividend, which gets mentioned just as often in consumer entrepreneurship but whose competitive moats are easily eroded, category dividends offer distinct advantages:

- Longer, more stable dividend periods.

- The largest addressable market among all dividend types.

Next, we'll use colored contact lenses — a consumer sub-segment enjoying a category dividend — to examine what characteristics and potential it showed before that dividend formed.

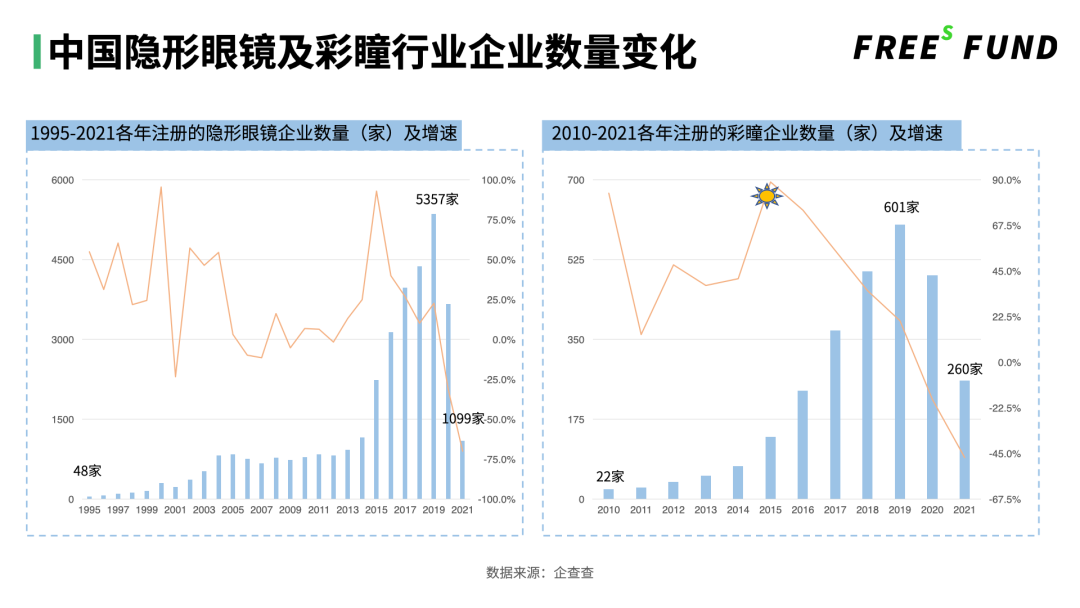

Let's start with the data. According to GfK, China's contact lens sales reached 10.67 billion yuan in 2020, up 1.14% year over year, with colored contacts accounting for 70% of that. Forward Industry Research Institute data shows that while penetration exceeds 30% in some countries and regions, China's colored contact penetration sits at roughly 8% — leaving substantial room for growth.

The Tmall Contact Lens Industry Consumer Insights White Paper, published in July 2021, noted that colored contact lens sales grew 83% year over year in the first half of 2021. MobTech forecasts China's colored contact market could reach 50 billion yuan by 2025, with China poised to become the world's most important market.

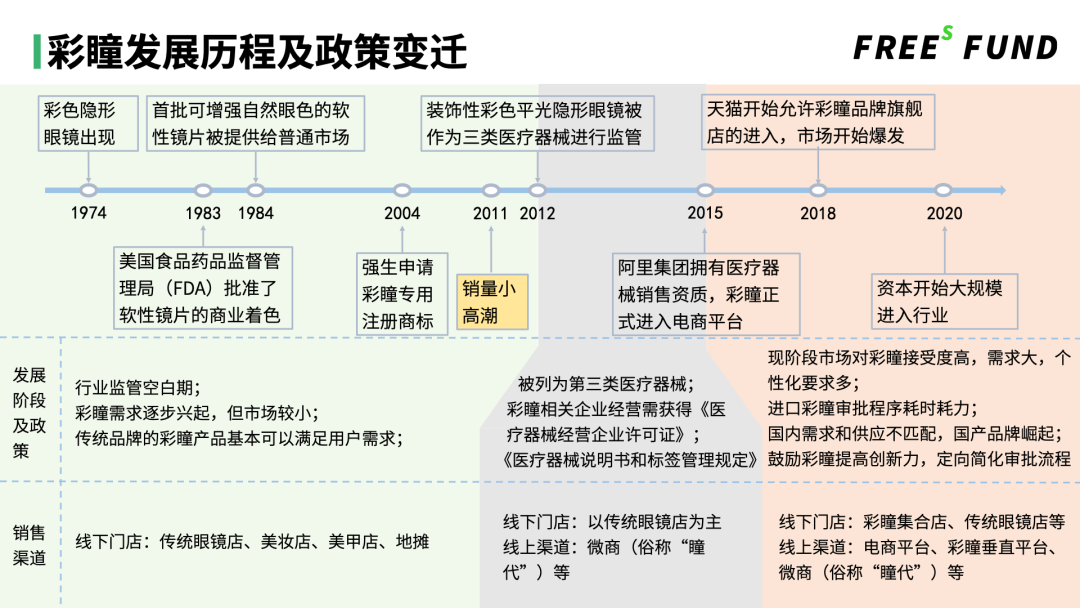

Before this rapid growth, the industry had nearly 40 years of history. Colored contacts first appeared in the 1970s to cosmetically enhance post-surgical eye appearance. They didn't gain traction as consumer products in China until 2011, when they sparked a small sales surge and began their decade-long takeoff.

That decade can be roughly divided into three phases based on market conditions.

- 2011: Riding the wave of Japanese, Korean, and "non-mainstream" culture, demand for colored contacts emerged in China. Yet industry regulation was nonexistent — consumers could freely buy colored contacts at night markets, cosmetic shops, and other informal venues.

- 2012–2015: Colored contacts became regulated as Class III medical devices. Companies needed medical device manufacturing licenses and other regulatory approvals to sell publicly. Domestic brands could only reach consumers through traditional optical shops and WeChat commerce, while Japanese and Korean brands, unaffected by domestic policy, gradually captured China's main colored contact market.

- 2015: Alibaba obtained medical device sales qualifications, bringing colored contacts onto e-commerce platforms. That year, colored contact business registrations grew 80%. Though growth slowed in 2019–2020, the overall number of enterprises continued rising.

Let's examine how the category dividend formed by looking at demand-side, supply-side, and channel-side changes over that decade:

▍Demand Side

- Compared to the more diverse eye colors in Western populations, East Asian irises tend toward uniformity (brown, black). Over the decade, influenced by Western, Japanese, and Korean pop culture, Chinese demand for diverse eye colors gradually rose.

- Myopia among Chinese youth climbed steadily. By 2019, approximately 460 million people in China wore corrective lenses. Myopia rates among high school and university students exceeded 87%, showing trends of high prevalence, earlier onset, and greater severity.

- As beauty consumers upgraded their daily makeup routines, daily disposable contact lenses — often the first step in many people's makeup process — shifted from consumer goods to everyday fast-moving consumer goods, strengthening consumption resilience. More consumers began prioritizing aesthetics alongside vision correction. A 2019 Online Colored Contact Lens Consumer Insights Report by Yicai Business Data Center (CBNData) and Alibaba Health found that 32.9% of colored contact buyers had no myopia and purchased purely for appearance.

- Starting in 2020, COVID shifted many consumers' makeup focus to eye makeup, making colored contacts a key element of eye looks. (This represents a relatively shorter-term dividend.)

▍Supply Side

- Mature contract manufacturers. Early colored contact brands relied primarily on Taiwanese, Japanese, and Korean OEMs and manufacturer-branded OEMs. Starting in 1992, Hydron's parent company built factories in mainland China. Subsequently, domestic supply chains like Jilin Realcon, Gansu Kangshida, and Hebei Xinshikang developed and matured over the decade, becoming the main OEMs for China's colored contact market today.

- Material upgrades. From early PMMA and RGP to hydrogel and silicone hydrogel. Most Chinese colored contacts now use hydrogel. While domestic adoption of this material once lagged foreign markets by 40 years, it has now matured.

- Process upgrades. Coloring techniques became thinner, more vivid, and safer. Comfort, pattern innovation, and fit all improved significantly, better matching growing user demands. Additionally, many Chinese colored contact brands use Taiwanese OEMs, where mechanization has advanced in recent years. For example, injection molding allows preset parameters and high-pressure injection of liquid monomers for mass production, greatly improving efficiency for short-cycle products like daily disposables.

▍Channel Side

- Expanded marketing channels. According to reports from Chuangkr and other industry sources, Alibaba obtained Class III medical device sales qualifications and opened to colored contacts in 2015. In 2018, Tmall began allowing colored contact flagship stores. Colored contacts started selling as FMCG on e-commerce platforms. The openness of content platforms like Douyin, Xiaohongshu, and Weibo further expanded brands' marketing reach. This is particularly noteworthy because, like cosmetics, colored contacts are especially well-suited to video as a medium for demonstration and viral spread.

▲ Image source: Douyin

The above makes clear that over the past decade, colored contacts seized multiple upgrade opportunities — consumption upgrading, category upgrading, and digital upgrading — methodically building their category dividend.

The underlying logic enabling this series of upgrades: mature supply chains improved product capabilities, and upgraded products were then amplified and promoted through the abundant traffic and content channels of the internet era.

▲ Image source: Kilala

In the colored contact space, FreeS Fund invested in Kilala's Pre-A round in early 2020. Over the past year and a half, we've watched Kilala grow rapidly in the face of an enormous category dividend.

**/ 03 / **

How to Find Category Dividends Proactively

Consumer entrepreneurship and investing based on category dividends share one difficult challenge: being proactive.

Everyone now knows coffee is hot, colored contacts are a big opportunity, and zero-sugar sparkling water is fair game. That's all fine. The hard part is recognizing these as promising new categories or categories undergoing major change before they gain widespread acceptance.

The same holds for entrepreneurs. A dividend becomes a dividend precisely because I see it and others don't. If everyone sees it or has it, what kind of dividend is that?

To some extent, when a category's dividend is just beginning to show — like a lotus tip emerging from the water — it represents a rare window. Large companies tend not to take notice or prioritize it. Domestic instant coffee brands like Saturnbird captured substantial dividends; Starbucks only launched its freeze-dried instant coffee this year.

Similarly, when an industry undergoes major change, it creates important entrepreneurial timing, because large companies must learn from scratch too — putting them, in some sense, nearly at the same starting line as startups.

Not all category dividends are equal; they vary in magnitude across sectors.

Let's compare sugar-free sparkling water and colored contacts.

Sugar-free sparkling water has indeed turned a corner, enjoying a major dividend from consumers' pursuit of healthier lifestyles. But beyond that, its sales channels, marketing methods, and so on haven't changed substantially.

Colored contacts, by contrast, saw simultaneous changes across supply chain, product, marketing methods, and sales channels. As mentioned, colored contacts evolved from Class III medical devices to consumer goods to FMCG — three distinct turns. Brands also continuously iterated and frequently updated manufacturing processes, marketing approaches, and sales channels. Some launched patented technologies to build technical moats. Meanwhile, new demographic segments contributed upward incremental growth. All these changes叠加 together, giving early movers who captured the category dividend a chance to enjoy a relatively long and stable dividend.

To summarize: in theory, from a consumer investment and entrepreneurship perspective, when an industry undergoes obvious change and sits in an incremental market, category dividends are usually there for the taking.

But practice shows that different entry methods and sub-segment characteristics create meaningful variation among category dividends — their duration and stability can't be generalized.

Staying proactive is key to capturing them.

Join the Conversation In this piece, we've shared our thinking on category dividends. We'd also love to hear your observations: What other approaches help entrepreneurs capture category dividends? What sub-segments do you see category dividends in? Contact Us Entrepreneurs and industry experts are welcome to continue the conversation with Yingzhu Jiao (jiaoyingzhu@freesvc.com). We're also looking for people with industry backgrounds interested in consumer investing to join our team (hr@freesvc.com).

▲ 3 Biotech Companies Raise Over 1 Billion Yuan Combined | FreeS Family Funding News · Oct–Nov ▲ In the Booming Cross-Border E-Commerce Sector, What Infrastructure-Level Opportunities Exist? | FreeS Interview ▲ "There Will Come a Moment When Technology Defeats Human Experience" | FreeS Fund Dialogue Transcript ▲ Expand or Close Stores? Re-examining Offline Opportunities | Feng Li Column ▲ FreeS Report 22: Can New Materials Save the Footwear and Apparel Industry? | FreeS Research Institute