Li Feng Column | The ICO Bubble: Origins and Future

Why is this round of currency bubble certain to burst?

In this sixth column installment, we're talking about cryptocurrency.

From 2017 through the 2018 Lunar New Year, digital currencies seemed unstoppable. Hordes of investors piled in, hoping to profit from the crypto boom, and prices for digital currencies including Bitcoin and Ethereum surged. But recently, Bitcoin and Ethereum have suffered sharp declines — a sign that a classic bubble is about to burst.

To be clear, I'm not here to bash digital currencies. On the contrary, I've been consistently bullish on crypto and blockchain since I started investing in projects like Coinbase and Ripple back in 2012. Full disclosure: I don't personally trade or mine coins. This past Lunar New Year, I did grab a Bitcoin red envelope worth about 100 RMB.

Currency fluctuations follow their own patterns. Based on my observations of digital currencies since 2012 and my analysis of the previous crypto cycle, I'd like to explore a few questions from an economic perspective:

- What triggered this round of the bubble?

- ICOs began as a fundraising method within a small, closed circle of digital currency insiders — how did they become a tool for "harvesting leeks" (exploiting retail investors)?

- This bubble is already deflating — how exactly will it pop?

- What happens after it bursts?

Share your thoughts in the comments below.

▍A year ago, ICOs were a fundraising method within a small digital currency circle, with reasonable valuations and amounts

ICOs were conducted on blockchain-based platforms, with high barriers to entry — they were the exclusive domain of digital currency insiders.

In the early days, ICOs looked like a normal fundraising method, similar to equity crowdfunding. In the first two months of 2017, Ethereum was still trading below 100 RMB, and a typical ICO would raise about 5,000 to 10,000 ETH — roughly one million RMB.

For an early-stage project with a business plan, that was a reasonable and cheap amount.

▍Ethereum lowered the barrier to ICOs, and Ethereum-denominated valuations and token prices exploded

In November 2015, Ethereum introduced the ERC-20 token standard (token, usually translated as "代币," maps to team value or serves as a proof of stake). This made Ethereum like an open-source Android system that allowed anyone to build applications — Ethereum allowed anyone with a project idea and funding needs to develop tokens on its platform. If a token met the standard, it could be publicly sold to raise funds for the project, and this sale process required no third-party oversight — it could execute automatically.

This made it much easier for people outside the digital currency circle to participate in ICOs.

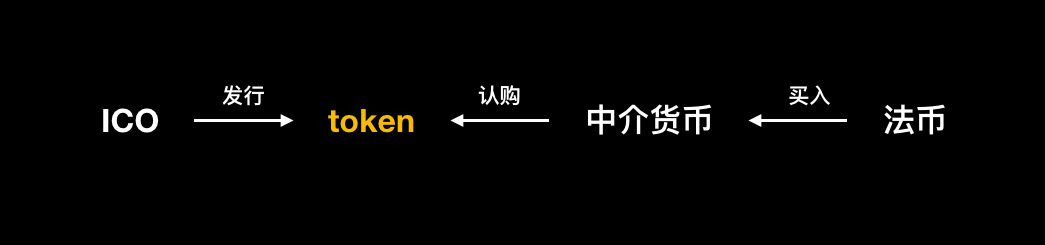

▲ As shown: on one side, people obtaining tokens through ICOs; on the other, investors using fiat currency to buy intermediary currencies, then subscribing for tokens.

For those bullish on an ICO project and wanting to invest, you couldn't directly purchase the project's tokens with fiat currency. You needed an intermediary currency to bridge the gap.

Given that Bitcoin and Ethereum accounted for the highest share of financing currencies supported by ICOs, with the two combined representing over 90% (Source: National Internet Finance Security Technology Expert Committee, "Report on Domestic ICO Development in the First Half of 2017"), this meant investors used real money to buy Bitcoin and Ethereum, sent the coins to the smart contract address published by the project team, and the smart contract automatically distributed the project's tokens to the investor — only then was the transaction complete.

So when outside money wanted in — when demand for buying Ethereum with fiat suddenly surged — the prices of intermediary currencies like Bitcoin and Ethereum were inevitably pushed up.

This process has already played out, especially over the past year, with gains so frenzied they triggered a new wave of digital currency mania.

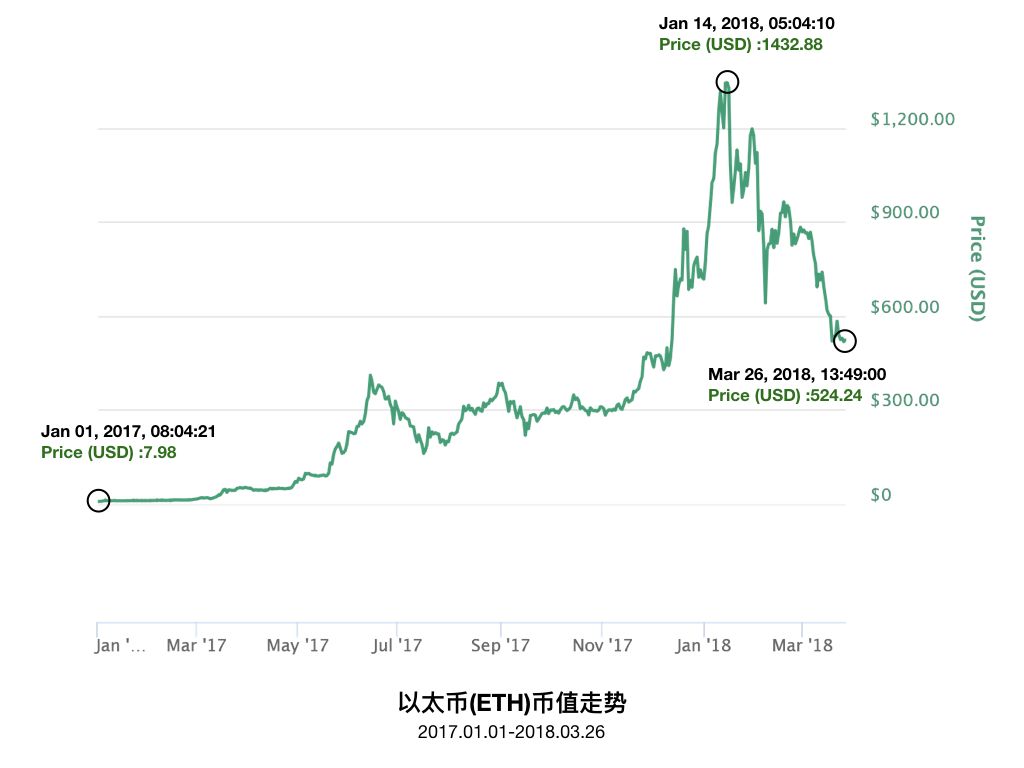

From the start of 2017 through mid-February 2018, Bitcoin's price rose 10x in one year. But compared to Ethereum, that's nothing.

In 2017, Ethereum's value rose over 100x: from $7.98 on January 1, 2017 to over $800 by December 2017, and breaking through $1,432 in January 2018. (Ethereum is currently trading around $520.)

Ethereum's wild ride:

▲ Ethereum (ETH) price movement, 2017.01.01–2018.03.26 (Source: CoinMarketCap)

Since Ethereum serves as the valuation base for projects launching ICOs on its platform, when Ethereum surged, the valuations of these projects — and the prices of the tokens they issued — all rose together.

▍ICO mania: what began as a fundraising method for digital currency insiders gradually became speculation

As tokens skyrocketed, the paper gains for ICO issuers became substantial — after all, their cost basis for holding tokens was nearly zero. Many projects hadn't even started building yet; they'd merely written a white paper and told a business model story.

Meanwhile, early participants who had used fiat to buy tokens at low prices could sell high, capturing the spread and harvesting a windfall.

One get-rich-quick story after another thrust cryptocurrency, originally something extremely niche within insider circles, into the spotlight before billions of people as a "shortcut to wealth."

Like countless commodity bubbles before it, it activated and exploited human greed and desire, while greed and desire in turn fed its flames, ultimately pushing it toward madness.

Everyone wants a piece of easy money. So more and more people wanted to profit from token appreciation. And once this wheel started rolling, it became hard to stop. Ethereum rose rapidly, ICO fundraising amounts grew enormous, and soon reached unreasonably inflated valuation ranges.

By mid-2017, a project that hadn't even started building could raise tens of millions of dollars. That no longer looked reasonable — it started to look like greedy arbitrage.

▍The game of speculative (investment) costs widens the gap between fiat entrants and ICO issuers, and a downward cycle begins

Imagine a giant seesaw, with ICO issuers on one end and people using fiat to buy intermediary currencies on the other. Initially, roughly equal numbers sat on both sides.

But soon, people realized that sitting on the ICO end was clearly cheaper — just tell a story — and the profit temptation was clearly greater. Gradually, more people crowded onto the ICO end than the fiat end.

The seesaw began to tilt, sloping toward the ICO side. The total token supply on the seesaw kept increasing, but fresh capital entering from the fiat side couldn't keep up.

Once supply-demand balance breaks, with fewer new entrants, the price of the intermediary currency — the hinge — stops rising first. Then token prices follow, falling and even dropping below issuance price.

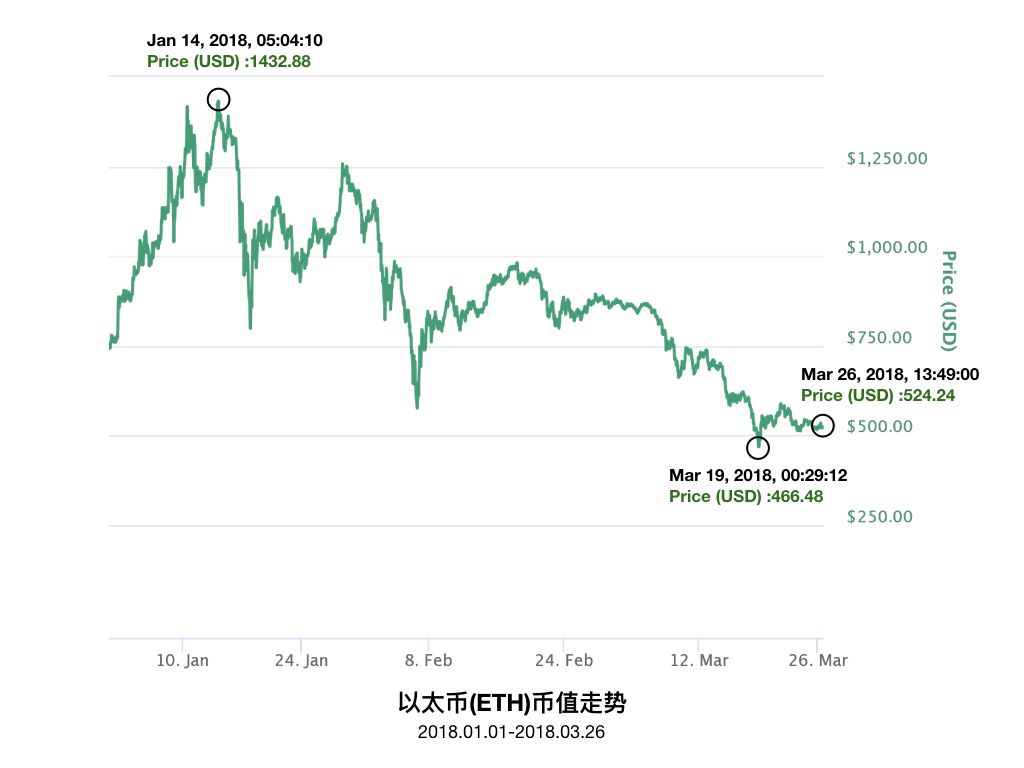

In fact, if we look at intermediary currency Ethereum's price, after breaking through its high above $1,400 in January 2018, it hasn't risen for nearly two months, and has been declining.

Ethereum's price movement over the past two months:

▲ Ethereum (ETH) price movement, 2018.01.01–2018.03.26 (Source: CoinMarketCap)

If everyone on the seesaw believes Ethereum's trend will continue downward, what will they do? They'll rush to harvest whatever arbitrage remains while they can, then jump off and exit.

Two types of people leave. First, those who entered relatively early with fiat — since current prices are still above their entry price, exiting now means they don't lose money.

The second group is ICO issuers. What they can do is quickly convert tokens back to intermediary currency, then exchange that for fiat to exit. This intermediary currency doesn't have to be the same one that fiat entrants originally used to buy tokens. They can choose a more liquid, relatively more resilient intermediary currency. For example, if they initially bought with Ethereum and Ethereum looks weak, they can switch to Bitcoin.

Two types of people remain on the seesaw. First, those who genuinely believe in digital currency's value and, to preserve value, try to convert their tokens into the most resilient currency and wait to see what happens. The second group is the "leeks" — retail investors who bought at high prices and can't bear to cut losses, or who reacted too slowly to exit in time and got trapped.

▍The currency bubble is already bursting, and prices may well fall below mining costs

I suspect this round of bubble bursting may happen very quickly, and prices could fall very low, because many people's cost basis is extremely low — especially for many ICO issuers, whose cost basis is close to zero. Without cost constraints, no matter how far prices fall, these people still have some arbitrage space.

This differs from the 2013 downturn. Back then, media coverage had propelled Bitcoin, previously obscure and unable to break $15, to suddenly surge past $1,000. The bubble promptly burst, prices halved, and at one point fell to around $500. But fortunately, holders at that time had to incur some cost to obtain Bitcoin — their cost basis was close to mining costs, so they only earned the spread between price and cost. Thus, when prices fell near mining costs, people stopped receiving adequate rewards, mining ceased, and supply and demand gradually rebalanced.

This round, prices could easily fall far below mining costs. Only after washing out these near-zero-cost holdings, bringing everyone's cost basis back to a reasonable equilibrium, and reestablishing foundational consensus, can prices begin climbing upward again.

The above analyzes short-term price movements.

▍On the meaning of bubbles

Even good companies experience dramatic price swings or drops below issuance price when bubbles burst. The existence of ICOs means ICO startup CEOs experience the pressures and challenges of secondary markets (price volatility) prematurely.

However, bubbles aren't entirely bad. Companies that truly create value gain funding and resources during this bubble, and will emerge after it bursts. This is inevitable in every bubble cycle. Similar stories played out in the 2013 digital currency wave — I'll share more on that another time.

Summary

1 This wave of digital currency mania was primarily driven by Ethereum's smart contract functionality, which lowered barriers to ICOs.

2 Get-rich-quick myths stimulated the public's nerves, drawing in more and more ordinary investors. They used fiat to buy intermediary currency ETH, then subscribed for tokens issued by projects. As participation grew and demand outstripped supply, ETH prices rose, token prices followed, and investors made money.

3 The bubble has already started bursting, and many investors (especially retail) will suffer heavy losses. Because another class of players in the market has extremely low cost bases — without cost constraints, no matter how far prices fall, these players still have arbitrage space. Those who get trapped are the momentum chasers who entered hoping to make a quick buck.

4 Bubbles aren't entirely bad — truly valuable projects will surface.

(Feel free to share to Moments. For reprint requests, please reply "转载" to learn reprint rules and contact FreeS Little Rui [ID: freesfund] for authorization. Copyright belongs to FreeS Fund.)

Li Feng's Column | What was the secret behind history's only successfully transformed major power?