Is the Internet Destined to Have a Next New Platform? | FreeS Research

Will the new decade that began in 2021 be a better one for entrepreneurship?

Monopoly and innovation are classic themes in the world of venture capital.

Not long ago, antitrust issues surrounding internet platforms once again sparked widespread discussion. Back in 2020, we at FreeS Fund conducted some internal research focused on the monopoly and fragmentation of traffic platforms, and how each generational shift in these platforms affects industries across the board.

Standing at the start of 2021, the process and findings of this internal research help answer two questions to some degree: Is 2021—and the next 5 to 10 years—a good time to start a company? Compared to the past five years, will internet entrepreneurship become easier or harder now and in the five years ahead?

Before diving in, here are our preliminary conclusions:

- There will always be new internet platforms. Whether in China or the US, in markets with free competition, once a platform reaches monopoly stage from a traffic-structure perspective, various subjective and objective factors will collectively break that monopoly. A single platform gradually fragments into multiple platforms—this is a great opportunity for entrepreneurs. (So the question becomes: what's next?)

- The alternation between old and new traffic platforms is typically accompanied by changes in traffic structure, traffic medium, and platform architecture. Every shift in internet traffic structure and format usually signals enormous opportunities and challenges. (So, will the opportunities be offline or online, tech-focused or cross-sector?)

- Inflection points in infrastructure development play an important role in driving changes to internet traffic and related business models. Whoever better grasps the opportunities brought by infrastructure transitions is more likely to capture greater user time.

- From the PC era to the mobile internet era, and now to the video era, the sequence in which business models form in each era is relatively consistent. When a new medium begins to consume large amounts of user time, new content and services gradually migrate into it. The general sequence is: lighter information and gaming industries enter first, then shift toward heavier, higher-time-consumption industries, and finally to very heavy industries closely integrated with offline life.

Below is the detailed analysis. We hope it offers some useful insights. Wishing you a smooth year ahead—and as we often say: stay true to your original intentions, keep your ideals alive, keep working hard, and there's always hope.

Internet Traffic Platform Research: There Will Always Be New Internet Platforms

By Shao Shili, Chen Zinan, Cao Jiarui, Cai Yufei

Advised by Li Feng

I. The Sign of an App Reaching Maturity: Dilution of Young Users, "Adultification" of the User Base

Let's first review the development of social platforms in China and the US.

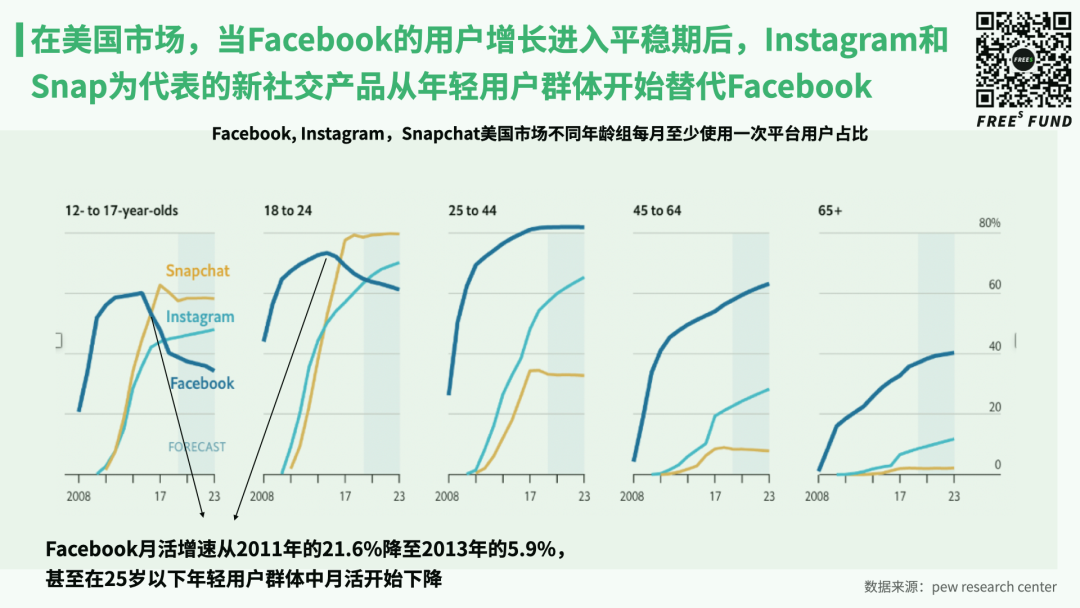

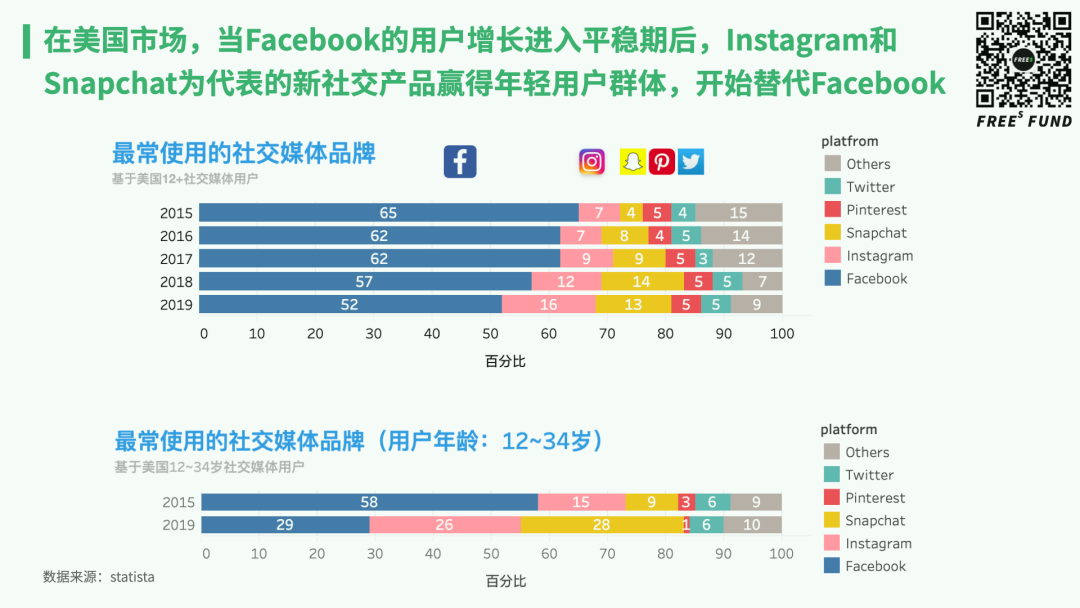

01 US: What Does the Data Say About How Facebook's Share Was Eaten by Snapchat and Instagram?

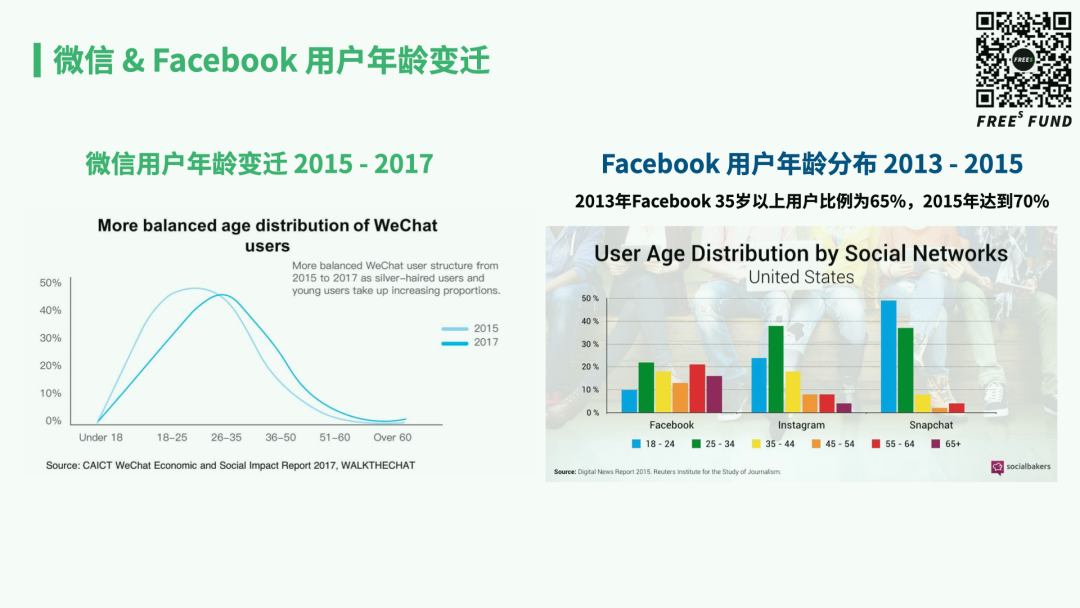

Facebook, the largest social platform in the US, launched in 2004 and has been around for 16 years. If we divide its development stages by growth data, 2013 stands out as unusual. That year, Facebook's monthly active user growth in North America dropped from 21.6% in 2011 to 5.9% in 2013, with Q1 2013 quarter-over-quarter growth nearly hitting zero—marking Facebook's entry into maturity in the North American market.

By 2016, Facebook's penetration among young users (under 25) was successively surpassed by two new social platforms: Snapchat (founded 2010) and Instagram (founded 2011).

The logic behind this shift boils down to two factors:

-

First, technology—specifically the development of 4G infrastructure in the US at the time, which played an important role in changing internet traffic and related business models. Declining network costs drove 4G penetration; faster speeds enabled new media formats. This meant new opportunities.

-

Second, changes in media content. Alongside 4G penetration, users—especially young users—began consuming more image and video content on mobile networks. Image- and video-based social products emerged, with Snapchat (video) and Instagram (images) as standouts. Specifically, Instagram offered an image-centric social experience from launch, and introduced the video-format Instagram Stories feature in 2015. Similarly, Snapchat initially focused on image-based instant messaging, then launched video chat in 2014.

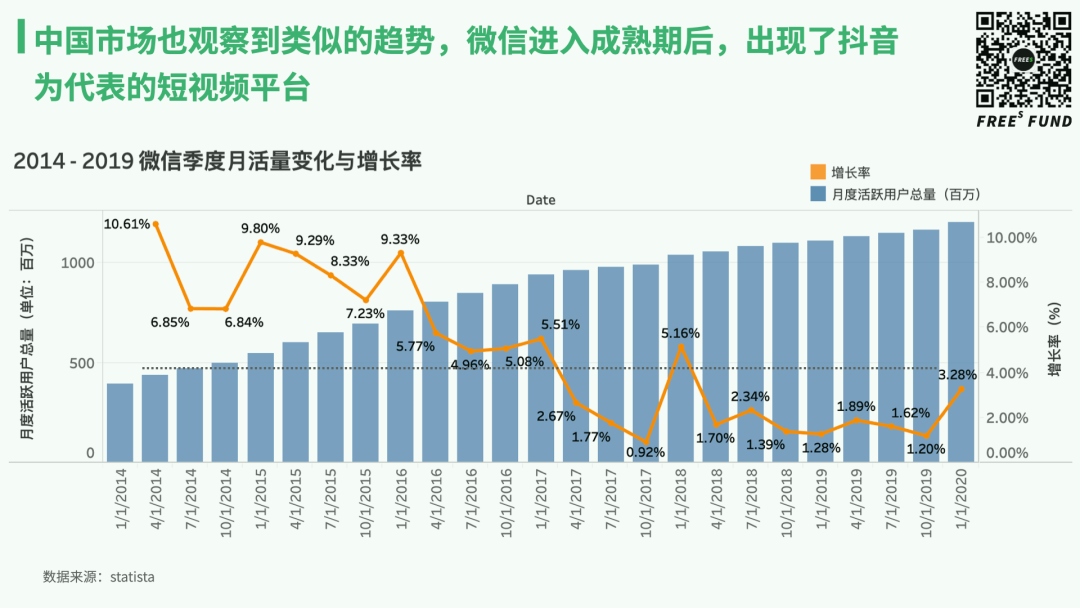

02 China: WeChat Enters Maturity as Douyin and Kuaishou Rise

Looking at China, WeChat as a super app followed a similar trajectory to Facebook. In 2016, WeChat reached 826 million monthly active users, with Q1 2016 quarter-over-quarter growth notably dropping below 5%—WeChat had entered maturity.

Meanwhile, new technological infrastructure and new media content also began to drive change.

According to the Ministry of Industry and Information Technology's 2016 telecommunications report, China added 340 million 4G users in 2016, reaching 58.2% penetration. The emergence of zero-rated data plans effectively lowered data costs, and users began consuming more video content on mobile networks. Short video apps represented by Kuaishou and Douyin emerged, with the latter seeing rapid user growth and gradually eroding WeChat's usage time.

03 The Price of Super App Growth: Young People Flee

If we analyze the age demographic shifts of Facebook and WeChat users, we find:

In the early growth phase of super apps, both supply and demand sides typically experience rapid growth simultaneously. Later, as the user base expands from young (25 and under) to older demographics, growth gradually flattens. When growth no longer has sufficient room, a certain degree of monopoly often emerges, and the platform begins considering monetization.

When super apps break out of their niche and achieve monopoly, they often face attrition among young users. The reasons behind this include, but are not limited to, two aspects:

-

As older users such as parents join, young users find that the platform is no longer the optimal place to communicate with peers. A February 2018 Guardian interview with young people identified parents and advertising as the problems. One respondent said, "Once parents are on it, it loses its original appeal";

-

The influx of users across all age groups typically accelerates platform commercialization. Increased commercialization makes young users feel disrupted—seeing ads that are inappropriate or unappealing.

This is the critical stage where change germinates. The under-25 demographic is the most crucial force driving the alternation between old and new platforms. Whoever wins the young becomes the new king of social. Conversely, whoever loses the young falls from the throne.

In fact, this isn't just a headache for Facebook and WeChat. Will the new traffic platforms that replace them and win young users' favor inevitably face the same fate?

Let's take Douyin as an example. Douyin was originally a platform for "little brothers" and "little sisters" to show themselves off. Later, as its user scale expanded, Douyin launched the tagline "Record a Beautiful Life," encouraging users of all ages to create content. Driven by this expansion strategy, the age coverage of users rapidly broadened, and the user base gradually "adultified."

As seen in the data below, from July 2017 to February 2018—a mere six months—Douyin's domestic user share under 24 dropped from 51.9% to 31.8%, while the 25-35 share grew from 28.2% to 46.8%. Compared to Facebook and WeChat, in today's more developed internet environment, Douyin's "adultification" came much faster.

In summary, we can draw two conclusions:

- A major sign of an app entering maturity is the evening out of age distribution across demographics. Platform growth stagnation is often accompanied by user adultification, a process that typically lasts 3-5 years.

- Platform expansion strategies usually create partial vacancies in the young user market, giving new platforms opportunities.

Discussion

Compared to the past five years, is internet entrepreneurship harder or easier now?

Share your thoughts in the comments, and reply with the keyword "startup" on the FreeS Fund WeChat official account (ID: freesvc) to see our preliminary thinking.

II. 50%: The Data Watershed Brought by Monopoly Status

Above we discussed the logic behind traffic platform transitions. But does this change have a critical data inflection point that can serve as a reference for future prediction?

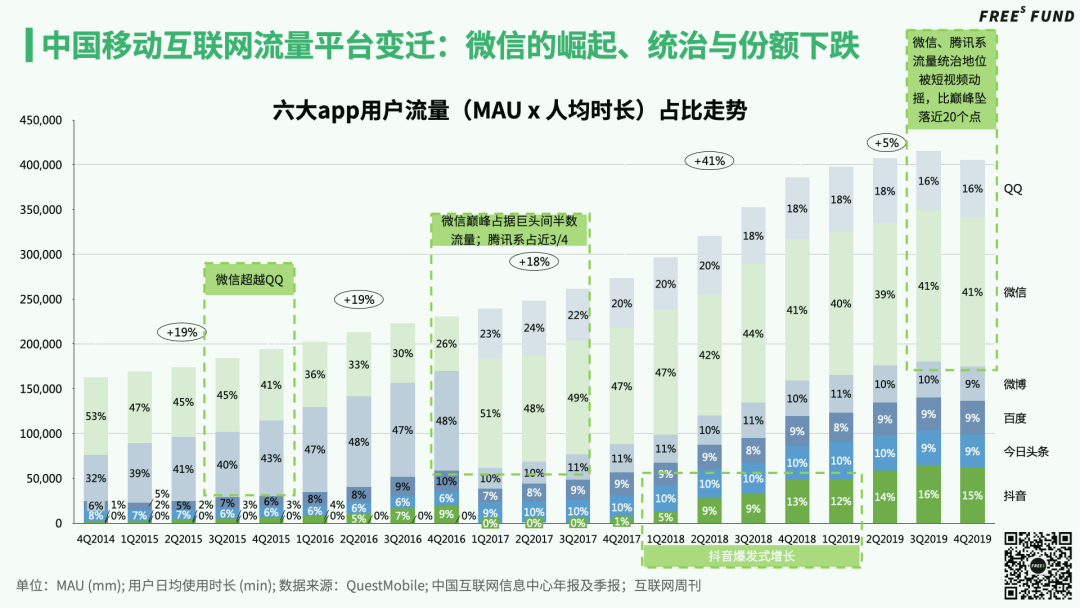

As shown above, we used a special statistical approach: treating "total users × average usage time per person" as a total traffic pie, then looking at each app's "total users × average usage time" as a percentage of that total traffic pie. From this chart, we can see how internet platform traffic distribution has evolved since 2014.

Why calculate it this way?

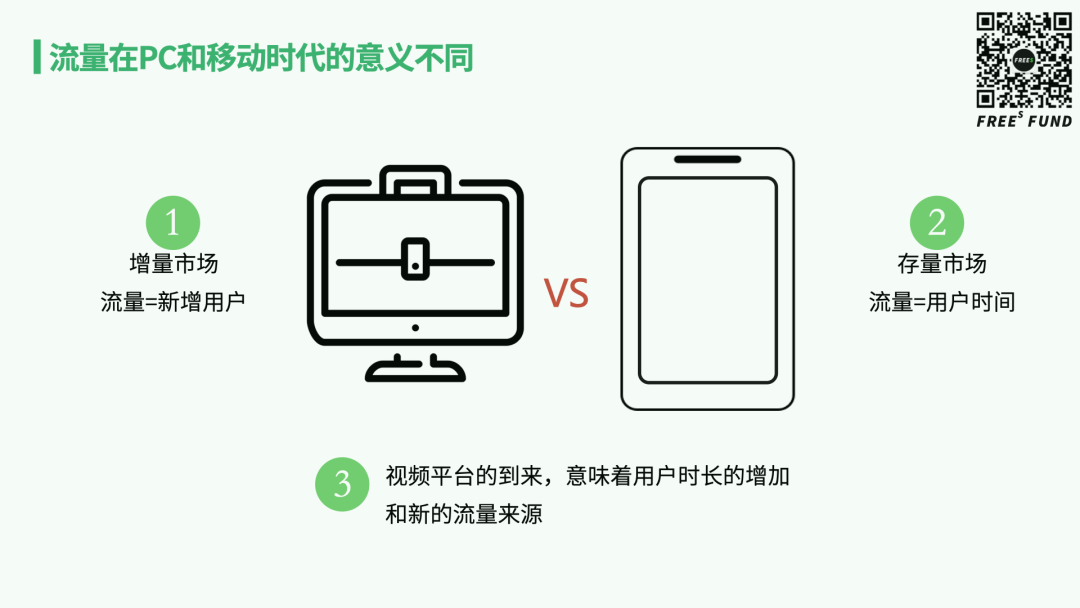

Here's the simple explanation. Before 2013, our standard metric was an app's "number of users / total internet population" because the PC era was a growth market — it was all about acquiring new users. But as we entered the mobile internet era, we moved into what's called a stock market. Customer acquisition costs kept rising, user growth hit ceilings, and the value of new users to business growth fell behind that of increasing existing users' time spent. So user time became a key metric for stock markets.

Especially in the video era, users became more efficient at utilizing fragmented time, and increased time spent became a new source of traffic. That's why we chose "total users × average usage time per person" as our measurement standard.

Let's first look back at WeChat's data. For WeChat, we can identify several important inflection points.

The first was Q4 2015, when WeChat's traffic share among major platforms reached 43%, surpassing QQ (41%) for the first time. This can be seen as a landmark moment marking the formal arrival of the mobile internet era.

The second was around 2016, when WeChat and QQ combined accounted for nearly 75% of platform traffic, essentially controlling the absolute gateway to internet traffic.

Just one year later, the inflection point arrived. As Tencent's traffic platform users aged, young users' adoption of Douyin exploded. In Q4 2017, Douyin's traffic share was merely 1%. It rapidly climbed in 2018 — from 5% to 9% to a peak of 13% in Q4 2018 — then stabilized around 15% through Q4 2019.

You can see that from WeChat's rise to Tencent's dominance of traffic gateways, to Douyin's entry and explosive growth, this all happened within just three years. By end of 2019, Tencent's traffic dominance had been shaken by short video, with its traffic share falling nearly 20 percentage points from its peak.

So what was the critical threshold in this process? 50%.

In 2017, once WeChat's share hit 50%, a monopoly formed. And once a monopoly forms, as we said, whether from commercialization-driven experience changes or shifts in user behavior, the share tends to decline — whether due to internal subjective reasons or being objectively "carved up" by competitors.

Beyond social and related fields, does this pattern hold? We also looked back at e-commerce industry data.

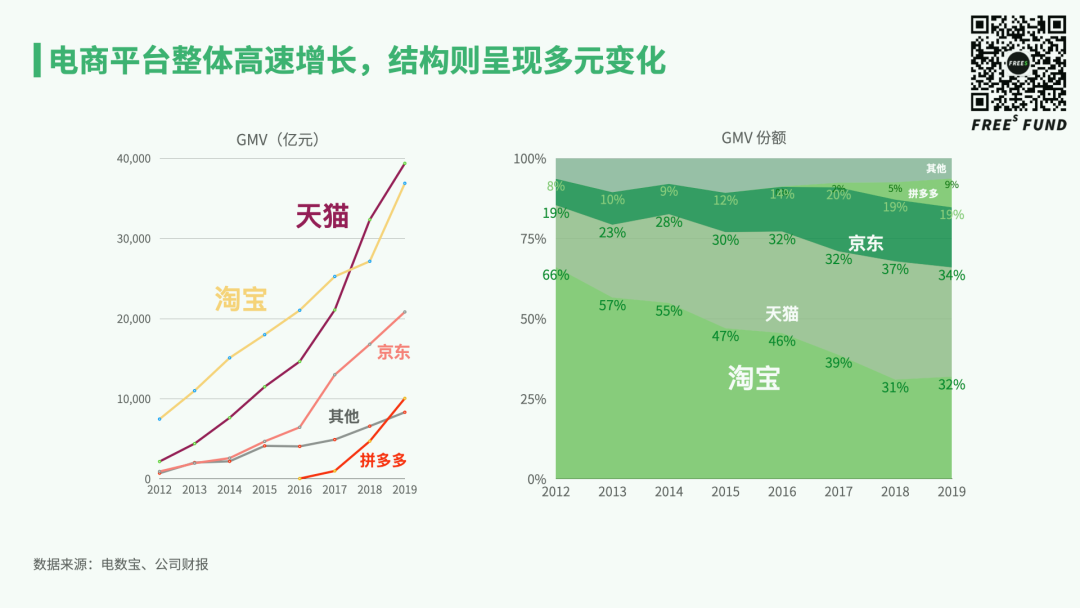

In fact, as early as 2012, when we began investing in the first batch of internet brands including Three Squirrels, the most frequently asked question was: will e-commerce platforms become monopolized? The GMV share chart above shows that e-commerce platforms also struggle to maintain monopoly.

If you observe the e-commerce industry over the past decade, you'll likely recall that starting from Q3 2012, there was an 18-month period that was the coldest for e-commerce investment. The result was that most B2C e-commerce companies exited after 2013. Also in 2013, among trackable benchmarks, Alibaba was almost completely monopolistic.

The chart above also shows a very contradictory picture. The GMV curve on the left shows Alibaba's platforms growing extremely rapidly — by growth rate among the fastest. But the GMV share chart in the middle still announces that its monopoly is being shaken: in 2012, Alibaba's market share approached 90%; by 2019, it had fallen to 66%. Taobao's share was cut in half, dropping from 66.1% to 31.9%, while Tmall's share doubled from 19.3% to 34.1%.

Beyond this internal "reshuffling," the main winners of share from Alibaba's e-commerce empire were JD.com and Pinduoduo. From 2012 to 2019, JD.com's market share doubled. Pinduoduo rose from 2017 onward, carving out 9% share by 2019.

The e-commerce industry finally began shifting from single dominance to multi-platform coexistence. This is beneficial for entrepreneurs.

So we say: everyone wants to monopolize, but the internet always has new platforms. For investment institutions, the key question is: who's next? How to find them?

To answer this, we look to the past for answers, examining the industry opportunities behind the evolution of these traffic platforms.

III. From PC to Mobile to Video: How Did Industry Opportunities Sequentially Emerge Across Different Waves?

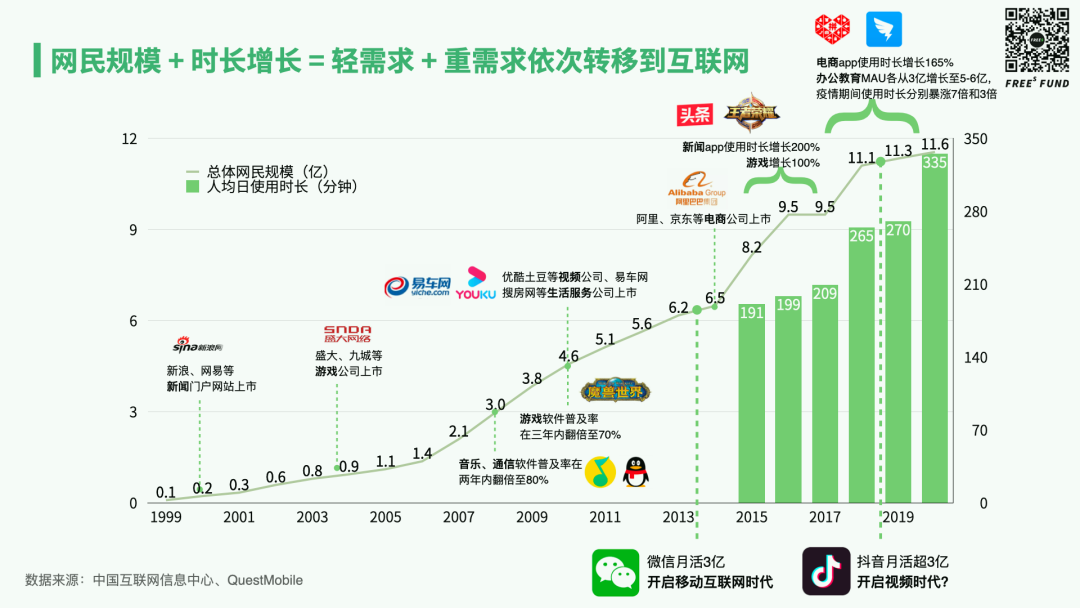

When a traffic platform begins to reach monopoly status, new traffic platforms tend to emerge. We've divided the past 20 years into three eras — PC era, mobile era, and video era — breaking each down to see what entrepreneurship and investment opportunities sequentially developed after each new traffic platform appeared, and whether patterns exist behind this.

Based on public data, we created the chart below. From 1999 to 2020, China's internet population and per capita usage time have consistently climbed.

01 PC Era

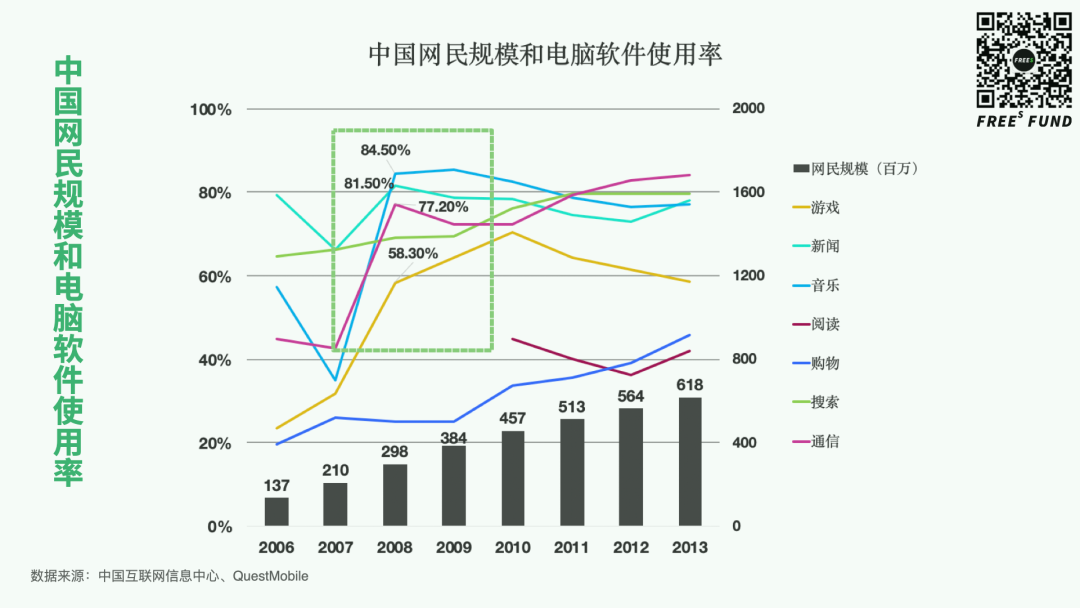

Looking first at the PC era, overall, the earliest to develop were news portals like Sina and NetEase, most going public around 2000. Then came gaming companies like Shanda and NCTY. From 2007 to 2010, relatively lighter entertainment services — games, music, video — began rising.

In the chart above, the light blue and green lines represent news and search respectively — the two industries that developed earliest in the PC era, with the highest market penetration. Between 2007 and 2009, you can see the blue, rose, and yellow lines suddenly spike, representing music, communication, and games — people began satisfying entertainment needs online.

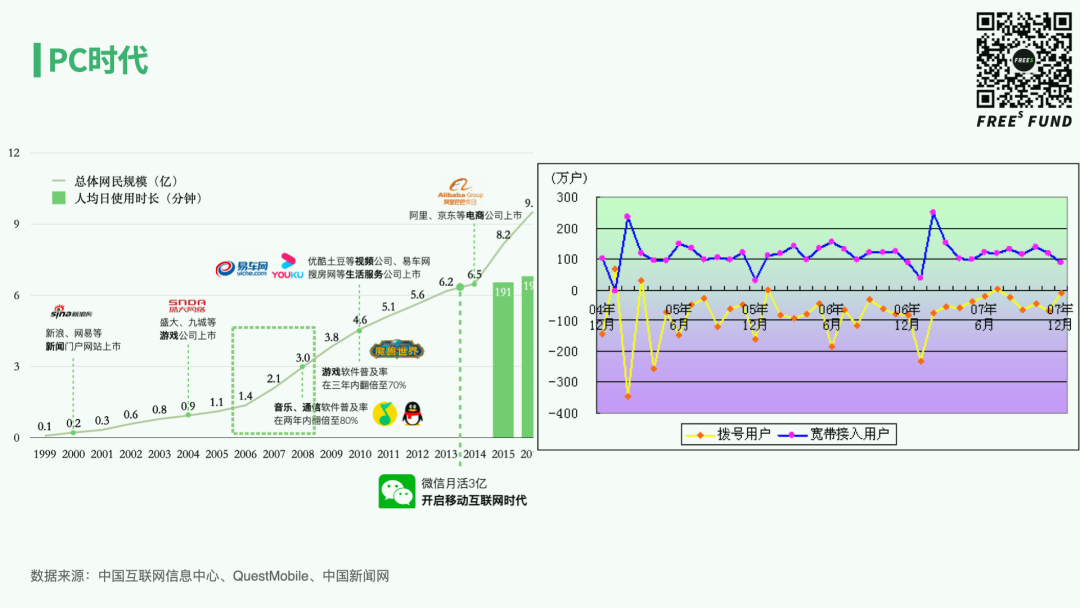

A major backdrop behind this, beyond continuously growing internet population, was broadband replacing dial-up internet.

According to the 2007 National Communications Industry Development Statistical Bulletin released by the Ministry of Information Industry, 2007 saw the largest increase in mobile users. In that same year, dial-up internet users among basic telecom enterprises decreased by 6.957 million to 19.49 million, while broadband internet access users increased by 15.611 million to 66.464 million — the gap between the two continuously widened.

Better network stability also provided foundation for these entertainment needs to migrate. Further along, the dark blue line representing shopping shows online shopping demand beginning rapid growth from 2009, accelerating the internet's pace into retail.

In early 2012, then-Chief Engineer of the Ministry of Industry and Information Technology stated that China had 156 million broadband access users, with over 84.4% above 2 Mbps; internet population reached 513 million, and 3G users hit 128 million.

From 2013 onward, WeChat's monthly active users reached 300 million, marking the opening of the mobile internet era. In 2014, after Alibaba, JD.com, and other last major PC-era e-commerce companies went public, the domestic market formally entered the mobile internet era.

02 Mobile Era

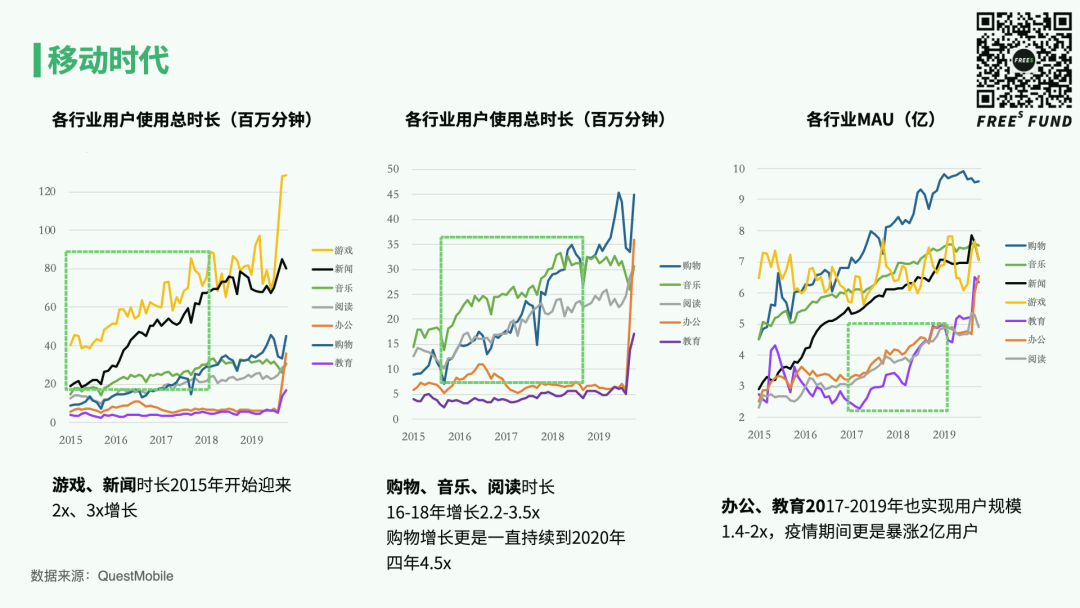

In the mobile internet era, traffic shifts resembled the PC era. As shown in the left chart above, the first two industries to develop were news and games. Within two to three years, both industries achieved two- to three-fold leaps in user time spent.

From 2016 to 2018, as shown in the middle chart above, we removed news and games. Beyond these two industries that still led far ahead in user time, the second wave of rapid growth came to three industries: shopping, music, and reading — achieving two- to four-fold growth within two to three years. Shopping in particular continued growing through 2020, increasing 4.5-fold in four years.

The most recent wave of growth occurred from 2017-2019, concentrated in office and education — the orange and purple curves in the right chart above — with user scale nearly doubling in three years. Growth during the pandemic was even more dramatic, surging by 200 million users. Of course, after market popularization is complete, whether these two industries hit growth ceilings within two to three years remains to be seen.

To summarize, the mobile era resembled the PC era: both moved from games and news, or information and games, to shopping, music, and reading, then to office and education — that is, from lighter needs fulfillable through information, to heavier needs with longer time spent, to very heavy needs with high offline life integration.

03 Video Era

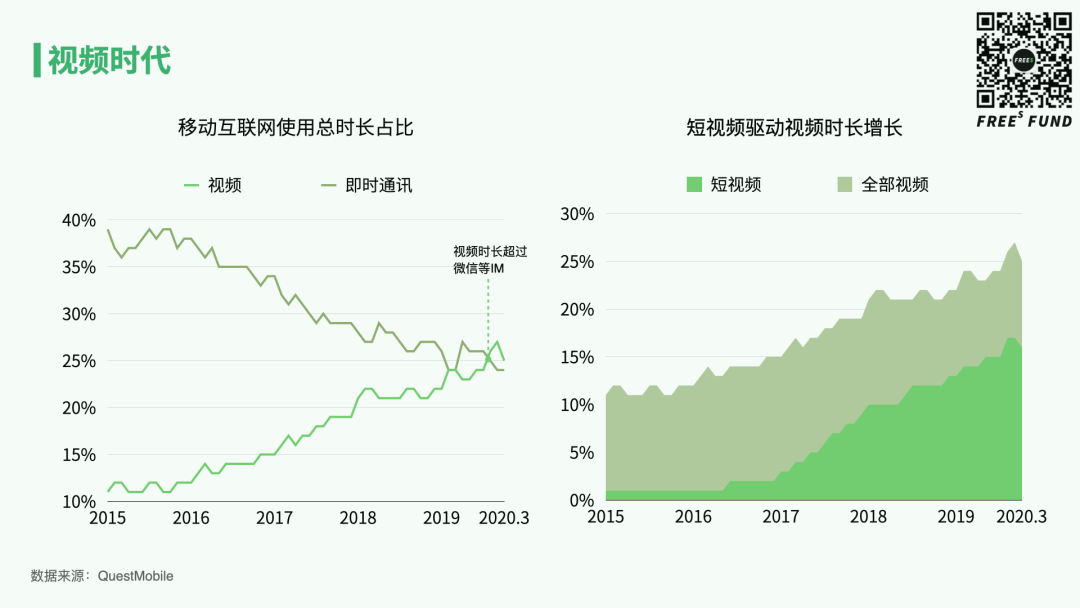

Just as WeChat's monthly active users surpassing 300 million opened the mobile internet era, Douyin's monthly active users surpassing 300 million in June 2018 marked the opening of the video era.

We can see that after entering the video era, the shares of video and instant messaging in total mobile internet usage time have also been shifting:

- Instant messaging apps like WeChat and QQ fell from nearly 40% of total mobile internet time in 2015 to around 25% in recent years, while video climbed from just over 10% in 2015 to 25% by Q1 2019.

- Short-video platforms including Douyin and Kuaishou saw sustained growth in user time after 2017. Around 2018, short video accounted for half of all video time growth. Since then, short video has occupied an increasingly dominant position within the video landscape.

- In early 2020, video surpassed instant messaging in time spent — another milestone in the video era.

In the current video-plus-new-platform stage, we believe the sequence of business model formation will be broadly consistent with the PC and mobile eras. When a new medium begins capturing massive amounts of user time, new content and services naturally migrate into it step by step.

It's also worth noting that with the development of infrastructure like 5G, whoever better seizes the opportunities created by infrastructural shifts is more likely to capture greater user time.

IV. New Characteristics of Today's Traffic Market, and the Opportunities Behind Them

01 The Particularity of the Current Stage: Traffic Structure, Traffic Medium, and Platform Structure Are All Changing Simultaneously

As mentioned earlier, a defining event in Q4 2019 was video surpassing instant messaging in its share of total mobile internet user time. Beyond platform structure changes, this reflected shifts in both traffic structure and traffic medium.

The change in traffic structure means WeChat's monopoly dividend has diminished.

The change in traffic medium refers to the shift from text-and-image as the dominant information format for over 20 years toward video.

In the text-and-image era, we went through portals, vertical portals, forums, blogs, Weibo, and WeChat Official Accounts, but the essence was still writing on the internet. The content entrepreneurs who built successful accounts mostly came from traditional media or were quality content creators from internet media.

However, when video traffic began surpassing instant messaging traffic, we didn't yet have a definitive answer about who could create good video content, because this field hadn't undergone sustained competitive selection.

The triple transformation of platform structure, traffic structure, and traffic medium will create enormous opportunities.

During transitions, good content is extremely scarce. Even platforms don't know where the best video content will come from, so despite any monopolistic intentions, true monopoly is impossible. This pressure of scarce quality supply and uncertain supply sources theoretically weighs more heavily on incumbents than on newcomers. That's why we saw news of ByteDance investing in five web novel platforms over roughly half a year.

Another phenomenon: compared to short video, discussion of mid-form video noticeably increased in 2020. Why? One reason is that as users spend more and more time with video, they no longer remain satisfied with entertainment alone. They gradually need to consume content and services across more domains — news, work, learning, e-commerce, finance, education, travel, and so on. This is also why we believe Bilibili grew so rapidly in the past year: it offers content of varying lengths and natures, satisfying diverse video content needs across age groups and demographics.

Of course, this contains the potential for new business models to emerge. Take the video project "Paperclip" that FreeS Fund invested in during the 2020 pandemic as an example.

We invested in Paperclip not only because it started producing video content early, is a quality content supplier, and excels at video-based content expression. More importantly, it began using video to redo, in a broad sense, knowledge and education-related work.

I previously discussed with Luo Zhenyu that Dedao essentially used audio — a distinctive medium — to create the knowledge-payment business model during the WeChat Official Account era. That was genuine innovation. Now, entering the video era, when traffic structure, medium, and platform structure are all changing simultaneously, new forms of Dedao will inevitably emerge — new knowledge-payment models, or new knowledge education systems.

Paperclip's experiments align with this trend. In mid-December 2020, they released their first paid interactive video course, embedding learning and interaction within video itself. This could incubate new business models for education or knowledge payment. During this window when all platforms need quality content supply, they can more easily obtain platform traffic and resource support.

Overall, however, the video-related entrepreneurship we see today remains in the very earliest stage of video transforming industries. The future holds promise.

02 From People Finding Products to Products Finding People: Traffic Becomes Increasingly Precise and Segmented

Against the macro backdrop of simultaneous changes in traffic structure, traffic medium, and platform structure, another notable shift is that traffic is becoming increasingly precise and segmented.

In the past, people found products. Users came with determined needs and some brand impression. So the merchant strategy was: spend heavily to rank first in your category on platforms like Tmall, and regardless of what users searched for in that category, you'd appear at the top with plenty of platform-allocated traffic.

Now it's products finding people, with traffic completely fragmented. First, users don't need to remember as much. Second, when users buy something, it's not necessarily because they recognize the brand — it's often because a streamer recommended it, or a Douyin influencer dropped a link.

From the platform perspective, user profiling is becoming increasingly granular. Every like, save, and comment you make on Xiaohongshu may be used by the system to tag and interpret your preferences and interests. More tags mean more precise targeting. A common experience: if you view a consumer brand on a certain platform, you'll receive recommendations for related brands and products for a long time afterward. Taobao's redesign last year, placing "Guess You Like" and "Recommended" at the forefront, reflected this platform mechanism change — it's no longer recommending brands, but products.

The result is that the narrower your product positioning, the better your traffic kickstart from platforms may be. But on the flip side, as traffic becomes more precise, the free traffic of the past largely disappears. Nearly every piece of traffic is bought, yet it may not ultimately be profitable.

For products, another challenge is that as traffic structure and platform logic tilt more toward products — especially precise, niche, high-certainty products — this helps niche products go from 0 to 1, but breaking out beyond that becomes extremely difficult. Traffic structure, platform logic, and sales methods all become unfavorable to breaking out of core audiences.

So how many companies can make money going from 0 to 1, and how many can make money going from 1 to 10? These are profoundly challenging questions. Still, the future is always bright. As we've always believed, China will inevitably produce the world's largest international brands across all categories. The process will simply be more painful than before — though fortunately, the final outcome may exceed anything we can imagine today.

Discussion

Compared to the past five years, is internet entrepreneurship today harder or easier?

Share your thoughts in the comments. You're also welcome to reply with the keyword "创业" on the FreeS Fund official account (ID: freesvc) to see our preliminary reflections.

Learning Early-Stage Investing from the Secondary Market: Where Are the Opportunities and Timing for Consumer Entrepreneurship? Where Is the Future of Livestream E-Commerce? Learning from the History of TV Shopping to Find New Brand Opportunities | FreeS Research Where Is the Endgame for Livestream E-Commerce? | FreeS Research From Boom to Settling: Is Livestream E-Commerce a Feature or a Business Model? (Part 1) | FreeS Research Li Feng Column 15 | How Long Can Livestream E-Commerce Stay Hot? What Makes the Low-ABV Alcohol Markets in China, the US, and Japan Completely Different? | FreeS Research FreeS Report 19 | The Tipsy Era: Where Are the Opportunities for Low-ABV Alcohol Entrepreneurship? Understanding the Secret Behind Instant Noodles' Explosive Popularity in 4 Minutes | FreeS Daily Business Musings FreeS Fund's Li Feng: For Consumer Brands, 0 to 1 Is Easy; 1 to 10 Is Hard | 10/31 Closed-Door Session Registration Galaxies in Your Eyes: Understanding the Rise of Colored Contact Lenses in One Chart | FreeS Research

▲ Three Squirrels' Zhang Liaoyuan: A Once-in-20-Years Brand Opportunity — How to Win in Three Steps | FreeS Fund 2020 CEO Annual Meeting ▲ Surpassing Nestlé and Starbucks During 618 to Become #1 in Instant Beverages: What Did Saturnbird Do Right? | FreeS Research — Learning from Investing