Li Feng Column 11: The Middle Path for New Retail | Frees Fund

The Three Axes of Understanding New Retail

This is the 11th installment of our column. Let's continue our discussion on new retail.

We've already talked about one major shift happening in Chinese retail: for the first time, urban consumers in China can buy offline products with the same cost-performance ratio, same brands, same styles, and identical quality as online.

Under this trend of online-offline integration, we've recently seen the strategic partnership between Starbucks and Alibaba. The former has perfected offline retail; the latter commands a massive online empire. Together, they're building Starbucks "new retail smart stores." In other words, we'll soon be able to get Starbucks delivered. Today, I'd like to share some recent thoughts:

- What is the "middle path" of China's new retail, and how did it emerge?

- For retail companies or brands, how do you address all consumer needs along a single chain?

- What does the future of new retail look like?

I hope we can exchange ideas and discuss. Feel free to share your thoughts at the end.

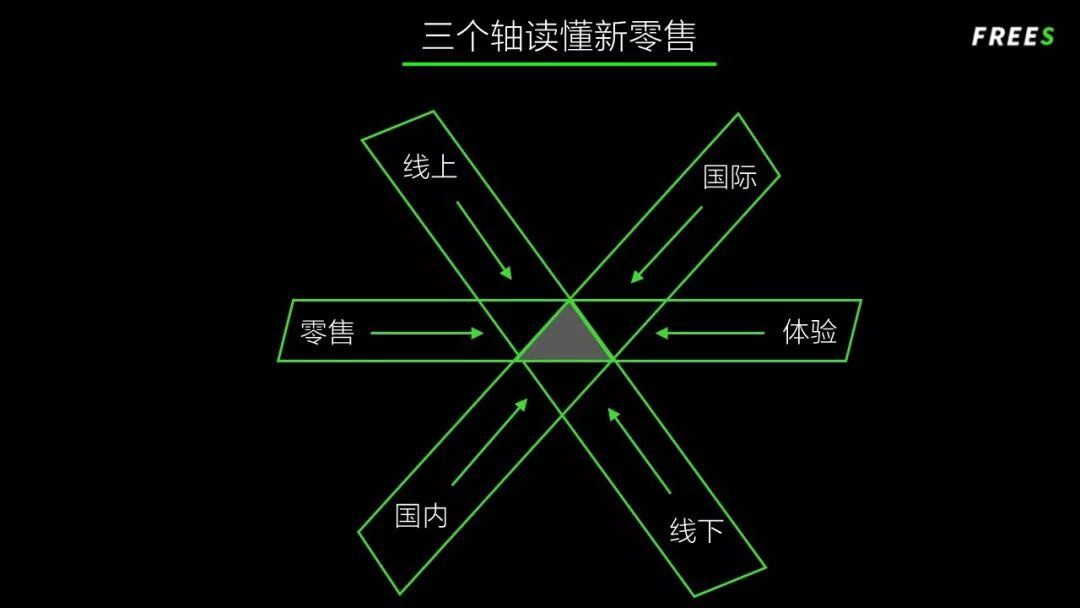

Three Axes for Understanding New Retail

I think the chart above explains most retail phenomena we've seen lately. For the past decade, retail formats and brands stayed put in one quadrant of this chart — offline stayed offline, online stayed online; retailers stayed on the industrial-goods end, while experience-oriented businesses focused on services; international brands emphasized their global identity, while China-centric brands highlighted local characteristics.

You could place every brand you can think of into one quadrant: Walmart and 7-Eleven are offline, Tmall and Ele.me are online; Nestlé and Maxwell's instant coffee sit 100% at the retail-industrial corner...

So what's changed today? A small shift probably started with Starbucks. In previous discussions about Starbucks, the most concentrated question was: why no delivery yet? Delivery is typical experience economy — not you going to the product, but the product and service coming to you. That's the difference between retail and experience.

Now Starbucks is finally doing delivery. You can see it moving from offline toward online, from retail toward experience in this quadrant.

Take Freshippo as another example. As a supermarket, it should have stayed put in retail like Walmart, running stores. But it invested enormous effort in in-store experiences. Or it should have focused on brick-and-mortar offline retail, but instead poured huge resources into online ordering and three-kilometer-radius delivery.

In other words, as a typical new retail representative, Freshippo didn't stay at the polar position of offline and retail. It moved toward the center of the quadrant, doing all four — retail, experience, online, and offline — simultaneously.

The same applies to product identity. What we used to think was definitely A, gradually shifted toward B. No brand can stay in one place forever.

When FreeS Fund invested in tea brands, we tended to believe pure tea was typically China-centric. But what took off first was new-style tea drinks — tea like lattes (milk + coffee blends), such as fruit + cheese, or milk + tea + sugar combinations, increasingly appearing in the market. We could no longer place them at the "China-centric" pole of that axis.

We could draw many more such axes.

For instance, in terms of brand classification, some brands leaned more toward marketing, others more toward supply chain. Now they're also gradually moving toward the middle. We can call this the middle path of new retail, or the trend of centralization.

How Did This Middle Path of New Retail Emerge?

The fundamental reason is that retail is full-chain competition. From the consumer's perspective, the essence of change is this: addressing all consumer needs along a single chain.

Take Starbucks again. In Starbucks stores, consumers can buy coffee beans, ground coffee, or freshly made coffee. Freshly made splits into machine-brewed, pour-over, and premium barista pour-over. Add delivery, and Starbucks can say it satisfies all coffee needs and scenarios for people. Conveniently, all of these can be solved by one supply chain, making it highly efficient.

The premise for one brand solving multiple user needs is consistent cost-performance ratio and brand perception. When we say "same products, same quality, same price online and offline," we mean making you believe that the same brand's products, whether through online or offline channels, offer the same high cost-performance ratio at the same quality and price.

With consistent perception, you won't obsess over channels. So terms like "online channel" and "offline channel" should become obsolete. They're not separate; they're converging.

The future of new retail is more diverse consumer needs and more complete consumption scenarios. Consumers themselves don't need to think about who to find online versus offline — it's the same category of need, the same brand relying on the same supply chain to provide all solutions.

What Else Does Full-Chain Competition Bring?

Moving toward the middle path means using one chain to string together consumers' different needs across different scenarios. At the same time, it requires companies to reduce costs and improve resource utilization efficiency at every link of the chain.

In less developed retail eras, the industry had enough links where single-point breakthroughs and efficiency gains could win users and profits. Those good old days when startups could dominate by excelling at one point are gone. Only by aggregating efficiency gains across multiple points into a total efficiency advantage across a longer chain can startups create value.

For example, a vegetable seller who honestly ran a shop at the neighborhood entrance might not lose business to the vegetable store next door. What really threatens this business is likely a company that does both online and offline, selling both fresh groceries and prepared food.

This business is brutal. Winners compete on only one thing: efficiency. And this isn't single-point efficiency — it's full-chain efficiency.

Any company doesn't necessarily need to run faster than others. As long as you have efficiency others can't match, even just 5% higher, and you don't die, you can keep growing and gradually eat away others' market share. Just as Amazon in America may consume the entire retail world, with no retailer able to stop its sweeping advance.

In long-term efficiency competition, retail enterprises have only one core competency: quality supply (we'll elaborate on this in the next installment). What essentially grows from this is called brand.

Brand is ultimately the core of consumer cognition. For the vast majority of products, consumers lack sufficient professional judgment ability and the time cost to make professional judgments. Therefore, the core purpose of brand is to reduce both of these costs.

Brand formation is very special. It ultimately embodies a process of values transmission. Values are created by founders, then passed down through various media, advertising, product information, until perceived by consumers.

If the values ultimately perceived by consumers are strong, consumers' willingness to pay brand premium and their loyalty are high, and vice versa.

Now, informatization and (mobile) internet pose a major challenge to brands: content, channels, and products are increasingly rapidly becoming one thing. Founders' good deeds and original intentions are more perceivable by consumers than before. The downside is that your mistakes are also more easily perceived by consumers, and hard to hide through information asymmetry.

Though companies have different characteristics, when a company grows to a certain scale and affects enough people, it's essentially been selected by everyone. The process of a company growing larger is the process of being gradually selected by the market.

Integration Has Just Begun

Right now, integration is still in very early stages. Whether all brands want to move toward the middle, we needn't rush to conclusions. What we can already see is that many companies originally at opposite ends of the quadrant have found various ways to move toward the middle to better satisfy consumer needs.

For example, MUJI originally sold pure industrial goods, but it opened hotels, adding experiential elements to user consumption.

Another example: Haidilao's business scope now includes something new — self-heating hot pots. These were very popular over the past year.

Self-heating hot pots add experiential elements to retail. You buy it from a convenience store, tear open the packaging, put ingredients in the upper container, add water, then activate the heating pack, place it in the lower container, add water, cover it, and wait 15 minutes for it to boil before eating. The whole process has strong ritual — a typical example of moving an industrial product from the retail end toward the experience end.

Moving toward the center of the quadrant is the path most brands will definitely take for the foreseeable future. Though many brands positioning themselves as doing only one quadrant, small-and-beautiful businesses, will still exist. They have their own market space and way of surviving.

Two preconditions for brands moving toward the quadrant's center: one, infrastructure like delivery, express logistics, and retail reach is already largely mature. China has many large cities with extremely high population density. We will certainly become the country with the world's best last-mile logistics. This special urban structure enables China to birth many wonderful business models, such as Luckin Coffee.

The other precondition for brands moving toward the center relates to supply chain — the brand's ability to control the full chain. We'll explore retail supply chain in the next installment.

Today, we're in the early days of new retail. Efficiency competition poses major challenges for brands in reconstructing people, goods, and places. You can imagine what the ideal state looks like: you need to satisfy both online and offline needs (using the same chain), you need to solve both retail problems — having both industrialized products and experiential elements — and in terms of positioning, you need both distinctive characteristics like China-centric elements while also catering to as many people as possible, trending toward the popular.

The problems to solve here are numerous and complex, so not all new retail forms we see fit this middle path. This means many new retail companies we see will need adjustment, evolution, and may also be eliminated. At the same time, it means retail entrepreneurs need more skills, more comprehensive capabilities to adapt to the current integration trend.

Summary

- The future of new retail is satisfying more complete consumer needs and more complete consumption scenarios.

- Brands' ability to control the full supply chain, together with the improvement of society's retail infrastructure, are the two preconditions for the centralization trend.

- Retail is full-chain efficiency competition. To satisfy consumers' more comprehensive needs today, staying at any end of the quadrant is insufficient. A typical new retail company must do online, offline, retail, experience, marketing, and supply chain all together.

Today's Question

Q: Currently, the middle path is an explanation method where induction works better than deduction. What brands or formats do you think fit this trend?

Feel free to leave a comment at the end and share your insights.

(Feel free to share to Moments. For reprint, please reply "reprint" to learn reprint rules and contact Feng Xiaorui [ID: freesfund] for authorization. Copyright belongs to FreeS Fund.)

Li Feng Column | US Dollar and HK Dollar Rate Hikes, and the Unicorn Winter

▲ Li Feng Column | The US-China Tech Rivalry, China's Secret Weapon

▲ Li Feng Column | What Was the Secret Trick the Only Successfully Transforming Major Country in History Grasped?

▲ Li Feng Column | A 2 Trillion Market and 10 Trillion Output Value, Why Are We Bullish on Chinese Chips?

▲ Li Feng Column | The Essence of New Retail, in These 10 Characters

▲ Li Feng Column | Lipton 120 Years Ago, Walmart 50 Years Ago, MUJI 30 Years Ago — How I Think About Consumption Upgrade and New Retail

▲ Li Feng Column | The Origin and Future of ICO

▲ Li Feng Column | From iPhone X, Smart Speakers to New Drug R&D, Environmental Monitoring — How I View Technology Innovation

▲ Li Feng Column | Shared Bikes Entering the IoT Track, Where Does the Data War Go Next?