Li Feng Column 12: A Speculation on the Endgame of China's New Retail | Frees Fund

Short-term: traffic. Medium-term: efficiency. Long-term: supply chain.

In this 12th column installment, we're talking about the battle for supply chains in new retail.

We've already discussed the profound changes underway in Chinese retail: for the first time, "same product, same quality, same price online and offline" has become possible in China. When we zoom out to look at innovation, setbacks, and endgames in retail over a longer time horizon, one thing is unavoidable: regardless of whether it's "new" or "old," retail is always a competition for efficiency across the entire chain, and a competition for high-quality supply chain resources.

China possesses an almost unimaginable depth of industrial chain technology. Roughly 70% of global production capacity for major consumer goods probably sits here. In the coming years, China has the opportunity to produce countless world-class consumer brands — but the precondition is that retail companies must get close to, control, and even create the highest-quality supply chains.

Today, we're merely standing at the starting line of new retail. On the core competitiveness and endgame of new retail, I've broken it down into three questions:

- In the marathon toward new retail, what is the long-term competitive advantage for consumer goods companies?

- Where are China's high-quality supply chains today? What impact will "same product, same quality, same price online and offline" have on China's retail supply chains?

- As the era of full-chain competition arrives, how do retail supply chains upgrade?

Share your thoughts at the end.

▍In the long run, retail's core competitiveness is owning quality supply

In consumer industries, short-term competitiveness is traffic, medium-term is efficiency. Long-term, what is the core competitiveness? Brand, certainly — but the most important thing has to be "supply chain" that is "high-quality and capable of upgrading."

What this means: a consumer brand can get sales moving in the short term through traffic; once volume is up, it needs to figure out how to improve efficiency; the essence of improving efficiency comes down to who can control or create the best supply chain.

What does controlling a quality industrial chain look like? Take Tesla. Tesla's batteries are made by Panasonic. The way it works with Panasonic is through a dedicated joint-venture factory, where Tesla calls the shots on production requirements. The degree of control is obvious.

Another consumer company with tight supply chain control is Apple. There's a Chinese company called AAC Technologies (HK: 02018) that makes acoustic components for Apple, with several production lines dedicated exclusively to Apple.

How does Apple control this critical supply chain? All the control software and computers on these lines belong to Apple; the ERP system is Apple's too. The AAC person in charge of production frequently receives emails from Apple saying something is off at a certain point on a certain line, then Apple opens permissions so the AAC production lead can go check on-site. Additionally, Apple has about twenty engineers rotating through on-site presence. Simply put, in principle, everything except the equipment and workers belongs to Apple.

Beyond controlling supply chains, companies that scale also need to be able to create quality supply.

Take New Oriental. In China's massive test-prep industry, New Oriental became one of the few large enterprises. I worked there for seven years, and one observation and conclusion is that it got many people who weren't originally teachers to become teachers — and they became hugely popular.

Its approach: using market-based methods plus a bit of inspirational appeal, it recruited large numbers of young graduates from Tsinghua University, Peking University, and other top schools, even North American returnees, then through systematic training turned these people whose original life trajectory wasn't teaching into full-time New Oriental teachers.

This is using a specific method to turn supply that wasn't previously supply into supply, and into a company advantage. While creating value for society, the company builds moats. Going further: as long as you have quality supply, you don't need to worry about demand.

Years ago, I invested in many C2C companies and reached a similar conclusion: all platforms that match bilateral supply-demand relationships are, at their core, competing on supply, not demand.

Apply this logic to retail brands and markets, and it's the same. On the road to new retail, whether you're doing channels, platforms, or brands, whether you're selling products or services, put aside all the trendy stuff — as long as you're in a bilateral retail business, what you're ultimately fighting for is quality supply, and what you're fundamentally solving is supply chain problems.

On one hand, you have to believe that within China's manufacturing sector, many excellent companies will seek to upgrade themselves; on the other hand, in the process of their improving production capacity, management, technology, and efficiency, whoever gets close to them at the front end, using sales volume and traffic thinking to bring them along in upgrading, will in the long run build very powerful enterprises.

All powerful, scaled retail companies, including IKEA and Muji, monopolize supply chains for their core categories — supply chains that produce almost exclusively for them, and upgrade and evolve together with them.

Xiaomi is also typical. It has traffic at the front end, efficiency in the middle, and at the back end, Xiaomi and the Xiaomi ecosystem bring along a massive array of intermediate industrial chains to upgrade together with it.

▍As the era of full-chain competition arrives, how do retail supply chains upgrade?

Since supply chains are paramount, then where are China's high-quality retail supply chains today? What impact will "same product, same quality, same price online and offline" have on China's retail supply chains?

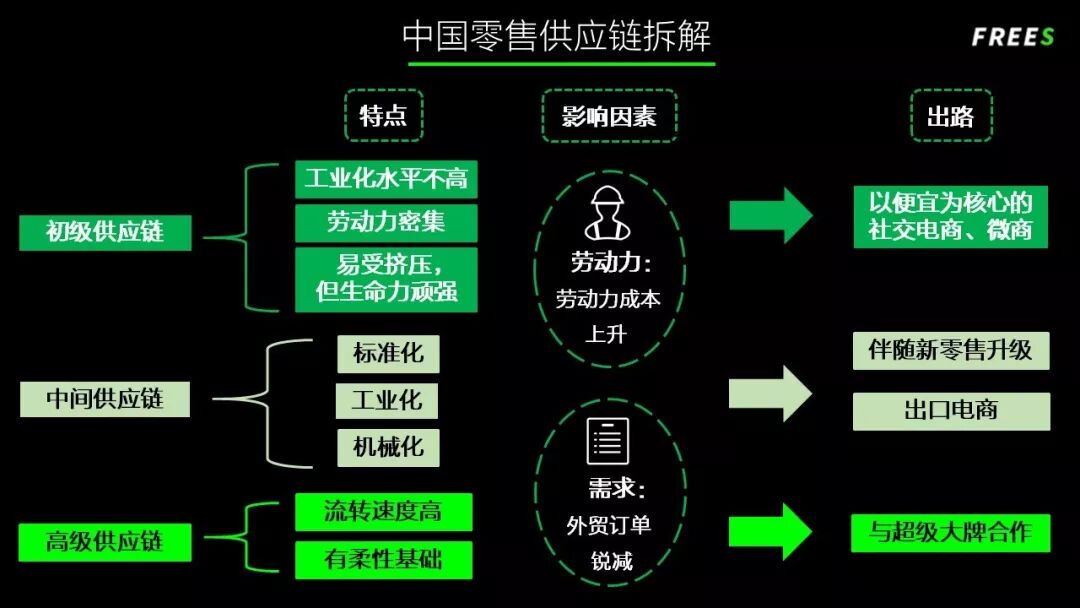

We can divide China's current supply chains into three categories:

- Primary supply chains

Production supply chains most vulnerable to squeeze. In other words, these have neither achieved good industrialization, nor good standardization, nor good cost-performance ratio, while also facing pressures like rising labor costs. However, just as China has vast numbers of retail endpoints, primary supply chains remain widely distributed and stubbornly resilient across China to this day.

- Intermediate supply chains

Can be understood as mid-tier supply chains that have achieved standardization, industrialization, and mechanization. Their production capacity is guaranteed, management relatively mature. They have opportunity to upgrade, but may also migrate under pressure factors like labor shortages and shrinking foreign trade orders.

- Mature supply chains

The ideal supply chain capability for new retail: high turnover speed, fast response, with some flexibility foundation. They generally partner with super brands (like Zara, Uniqlo), through ecosystem design departments' extreme refinement and testing, ultimately producing high-quality products with generous materials, cheap pricing, and strong experience.

China's retail supply chains over the past decade or so have faced their most direct problems related to two things: demand and labor.

Here's an example of demand forcing retail supply chain change. Go back ten years. The world financial crisis that began in 2007 started becoming visibly felt in China in 2008. One harder-hit industry was foreign trade, which forced China's decades of accumulated industrial chains to seek new outlets, making them willing to support e-commerce sellers whose prospects were then unclear or even not very promising. That year, China's e-commerce industry grew explosively.

In the current environment and consumption cycle, China — as the country producing roughly 70% of global daily consumer goods — so-called export-oriented, production and processing enterprises again face challenges and squeeze: foreign trade growth is relatively sluggish, China's labor costs have risen quickly.

This way, factories' survival space gets compressed quite severely; some can only automatically die off. Like ten years ago, they need to find every possible way to find outlets — distribution channels and methods that can purchase their products.

The cheapest we-commerce and social commerce are two major outlets for primary supply chains.

The populations they reach include, very importantly, users completing their first e-commerce purchase via smartphone. In other words, they likely weren't previously PC users, nor had they bought anything on e-commerce platforms like Taobao, Tmall, or JD.com.

These people can be analogized to the populations e-commerce first reached around 2010. In principle, you only need sufficiently high cost-performance ratio, or sufficiently low prices, and they will compare with offline retail of insufficient quality and products that haven't yet achieved cost-performance ratio, then smoothly convert into we-commerce and social commerce users. This is also why social commerce and we-commerce that open with cheapness can achieve explosive user growth in short timeframes.

However, accompanying new retail's rapid expansion, penetration, and下沉, when good quality at low prices is no longer a problem, or when massive amounts of affordably priced branded products are pushed before users, one challenge these cheapest we-commerce and social commerce may face comes down to: can their supply chains upgrade?

Q1: After new retail achieves full coverage, these mobile e-commerce users initially attracted by extremely low prices in we-commerce and social commerce — whose users will they become? Or put another way, when good quality at low prices isn't a problem, what will users buy?

New retail is one of the main outlets for intermediate supply chains. Like MINISO, and Xiaomi's Mijia Youpin mentioned earlier, after achieving volume, the supply chains they occupy are this intermediate layer with certain standardized quality standards and production capabilities. Intermediate supply chains, through combination with new retail, also begin to have upgrade possibility, further gaining flexible capabilities like rapid adjustment, rapid design, and rapid feedback.

This is also new retail's special significance in China today: on one hand, those supply chains with quality production capacity facing pressure from emerging channels need to find more outlets. On the other hand, brands' demand for quality supply chains will only grow. The two enable each other.

Additionally, intermediate supply chains have another very typical outlet: cross-border e-commerce.

During the last financial crisis, though foreign trade was affected, a small wave of cross-border e-commerce companies still emerged, including LightInTheBox, etc. In this cycle, China will also birth a relatively large number of export e-commerce companies. Take Club Factory and Patpat, which FreeS Fund invested in — both are based on China's supply chains with quality production capacity, building direct sales channels whose customers are foreign middle classes.

These relatively good intermediate supply chains, trained over decades, when facing people becoming expensive, people hard to hire, even migration to other cheaper-labor countries like Southeast Asia, have extremely strong motivation to cooperate with new formats and new opportunities to make an upgrade, turning themselves into quality foreign trade producers.

This is another open question we leave today:

Q2: Besides new retail and export e-commerce, where else can the quality production capacity of this supply side go — with both production capability, design capability, and relatively strong data-based management capability?

Correspondingly, there's also a smaller question:

Q3: At this stage, primary supply chains surviving by adapting to low-price products and new channels, new outlets — from a medium-term view or looking toward the distant future, will they be eliminated or persist?

One advantage of China is that time always moves fast; one year of development and change can equal many years in other countries. Now, China's retail has experienced e-commerce's baptism, also experienced commercial real estate's rapid development, and offline retail formats' reflection, adjustment, and reshaping, heading toward a highly competitive and highly marketized mature market.

What hasn't changed is retail's logic — short-term is traffic or sales volume, medium-term is efficiency, long-term is competing on supply chains. What essentially grows from this is called brand.

This fierce battle of new retail — time will give us the answer.

Summary

1 In consumer industries, short-term competitiveness is traffic, medium-term is efficiency, long-term core competitiveness is owning quality supply. The method is: either you master quality supply chains, or you create quality supply chains.

2 New retail's special significance in China today: on one hand, those supply chains with quality production capacity facing pressure from emerging channels need to find more outlets. On the other hand, in the fierce battle of new retail, brands' demand for quality supply chains will only grow. The two enable each other.

Today's Questions

Q1 After new retail achieves full coverage, those mobile e-commerce users initially attracted by low prices in we-commerce and social commerce — whose users will they become? Or put another way, when good quality at low prices isn't a problem, what will users buy?

Q2 Besides new retail and export e-commerce, where else can the quality production capacity of this supply side go — with both production capability, design capability, and relatively strong data-based management capability?

Q3 At this stage, primary supply chains surviving by adapting to low-price products and new channels, new outlets — from a medium-term view or looking toward the distant future, will they be eliminated or persist?

Welcome to leave comments at the end, sharing your insights.

(Feel free to share to Moments. For reprint, please reply "reprint" to learn reprint rules, and contact Feng Xiaorui [ID: freesfund] for authorization. Copyright belongs to FreeS Fund.)

▲ Li Feng Column | The Middle Path of New Retail

▲ Li Feng Column | US Dollar and Hong Kong Dollar Rate Hikes, and the Unicorn Winter

▲ Li Feng Column | The US-China Tech War, China's Secret Weapon

▲ Li Feng Column | What Was the Trick That the Only Successfully Transformed Great Power in History Grasped?

▲ Li Feng Column | A 2 Trillion Market and 10 Trillion Output Value, Why Are We Bullish on China's Chips?

▲ Li Feng Column | The Essence of New Retail, in These 10 Characters

▲ Li Feng Column | Lipton 120 Years Ago, Walmart 50 Years Ago, Muji 30 Years Ago — How I Think About Consumption Upgrade and New Retail

▲ Li Feng Column | The Origin and Future of ICO

▲ Li Feng Column | Mi Meng with 8 Million Followers and Martin Luther from 500+ Years Ago — How I Think About Content Entrepreneurship

▲ Li Feng Column | From iPhone X, Smart Speakers to New Drug R&D, Environmental Monitoring — How I View Technology Innovation

▲ Li Feng Column | Shared Bikes Enter the IoT Track, Where Does the Data War Go Next?