Li Xiang x Li Feng: From Purified Water to Unsweetened Tea — A Case Study in China's Consumption Upgrade | Li Feng Column

In consumer markets, the boundary between services and retail is growing increasingly blurred.

This column comes from an in-depth conversation between Li Xiang and "Uncle Feng" on the High Energy podcast. Li Xiang is the curator of the In-Depth Conversations book series and editor-in-chief of Dedao App. The battle for refrigerator space is heating up, and beverage sales are about to hit peak season. In some convenience store drink coolers, the prime real estate is now occupied by sugar-free tea — once mocked as the "worst-tasting drink" around.

The sugar-free tea boom also shows up in financial reports: in 2022, Nongfu Spring's tea beverage segment, led by East Leaf Tree (Oriental Leaf), generated 6.906 billion yuan in revenue, up 50.8% year-over-year. Tea beverages were also Nongfu Spring's only category in 2022 to grow faster than the same period in 2021, with revenue share rising from 15.4% to 20.8%.

In Uncle Feng's view, the rise of East Leaf Tree and Genki Forest represents a textbook case of consumption upgrading: on one hand, a health dimension upgrade from low-sugar to sugar-free; on the other, a price dimension upgrade from 1 yuan to 5 yuan. And on the beverage track, consumption upgrading has been happening all along.

In their nearly hour-long discussion, Li Xiang and Uncle Feng moved from bottled water to beverages to coffee, dissecting the true face of domestic consumption upgrading and the trend shifts behind it: lower-tier markets have begun brand-oriented consumption upgrading, consumer demand has shifted from "endless variety" to "curated selection," and the boundaries between service and retail are increasingly blurred...

We've edited and excerpted portions of the podcast, hoping to offer fresh perspectives. We welcome you to continue observing and exploring with us. You can also head to the Xiaoyuzhou app or Apple Podcasts, search for and subscribe to High Energy to listen to the full episode.

Engagement Giveaway

What new observations and discoveries do you have about today's consumer market? Leave a comment and share — we'll give curated gift packs to the 2 users with the most likes and the 3 users with the most thoughtful comments (deadline: 5 PM, June 5). Each curated gift pack includes: one copy of In-Depth Conversation: Wu Jun, one bag of Methuselah low-fat chicken sausage, and one box of Methuselah lemon-flavored energy-control wafer bars.

/ 01 / On the Beverage Track, Consumption Upgrading Has Been Happening All Along

Li Xiang: Welcome to High Energy. In this episode, I'll be discussing bottled water and the beverage industry with Uncle Feng. He's also invested in some bottled water and beverage startups, so I wanted to get his take on this topic.

Li Feng: For this episode's industry observation, let's start with water and talk about the consumption phenomena happening in China and the trend shifts behind them. Let me start with a few simple examples and interesting observations. We once conducted thousands of user surveys and found that Chinese consumers made a noticeable shift from drinking purified water to drinking natural water during 2015-2016.

▲ Image source: CBNData

Li Xiang: Specifically, Nongfu Spring pushes natural water, while Wahaha pushes purified water, right?

Li Feng: Right, Nongfu Spring is natural water. This shift mainly happened between 2015 and 2016 — a clear consumption upgrade, with bottled water price points rising from 1 yuan to over 1 yuan or even 2 yuan.

▲ Image source: FoodTalk

We did many user surveys at the time. Most users could clearly distinguish whether they were buying purified water or mineral water — they had a clear consumption upgrade awareness. But there was one brand, C'estbon, where quite a few users weren't sure if it was purified water or mineral water. The reason: among most purified water brands, C'estbon was one of the few that used hard bottles and hard caps. Nestlé and Wahaha purified water bottles are very thin. Natural water and mineral water, taking Nongfu Spring as an example, both use hard bottles and caps. So many users would think C'estbon is mineral water, or at least not perceive it as purified water. This was a very interesting phenomenon in the bottled water upgrade process — a user perception shift caused by packaging.

Li Xiang: Packaging created this differentiation.

Li Feng: Before 2018, when we bought drinks more expensive and more satisfying than mineral water, sugary tea beverages and cola were our typical choices, around the 3 yuan range. In 2018-2019, we shifted from drinking cola to so-called healthier sugar-substitute sparkling water.

Li Xiang: The most typical example is Genki Forest.

▲ Image source: Genki Forest Tmall flagship store

Li Feng: Right. Going from cola to sugar-substitute sparkling water was actually consumption upgrading, moving from the 3-yuan price range to 5 yuan. In 2022, I observed a very noticeable consumption shift: young colleagues went from drinking sugar-substitute sparkling water to drinking 0-sugar, 0-calorie pure tea beverages, with East Leaf Tree as the typical product.

Let's simply assume that sugary equals unhealthy and sugar-free equals healthy. We went from the most unhealthy, most sugary drinks, to sugar-substitute sparkling water, to sugar-free — in roughly just 4-5 years. From a health concept perspective, that's basically the end of the road.

This is a very typical consumption shift. From this case, we can see that Chinese consumers, especially young consumers, after forming definite consumption awareness and concepts, transition from less professional to professional very quickly. Similar situations are also happening in the cosmetics industry, and may become increasingly common.

In cosmetics, consumers moved from expensive products with complex chemical ingredients, to affordable alternatives with simplified ingredient lists, to very professional, specific, relatively pure-ingredient semi-medical, semi-beauty products — also in just a few years, users rapidly shifted from one end to the other.

This proves several things are happening in China:

First, the proportion of young Chinese consumers receiving higher education is already very high. Their ability to determine what they want and understand what products are good for them is improving rapidly.

Second, China's internet penetration is very high, so in China's consumer market, information channels are increasing, information professionalism is improving, and information symmetry is improving very quickly. What consumers see offline, they can almost all buy online.

These factors are driving very fast consumption iteration. The time and space for intermediate states are greatly compressed — very interesting.

Li Xiang: Actually, in the iteration process from cola to sugar-substitute drinks to pure tea beverages, the products themselves didn't change that much, right? It's more that consumers' consumption concepts and professionalism changed?

Li Feng: Yes, it very typically reflects domestic consumption upgrading. By category, consumers went from purified water to mineral water, to high-sugar beverages, then to low-sugar beverages, to sugar-free beverages — roughly that process. By price dimension, from 1 yuan to 1.5 yuan, 2 yuan to 3 yuan, 5 yuan. This is very typical consumption upgrading along two dimensions.

/ 02 / From Luckin Coffee to Sam's Club: Lower-Tier Markets Begin Brand-Oriented Consumption Upgrading

Li Xiang: Two years ago, Dedao CEO & co-founder Tuo Buhua observed a phenomenon. She noticed that young colleagues around her weren't really drinking water anymore. The office had a water dispenser, but few young colleagues would pick up a cup and get some water. If they wanted to drink something, they'd order Luckin Coffee or milk tea.

Li Feng: Speaking of Luckin, what everyone's been discussing a lot recently is its "comeback." What's characteristic of Luckin's development? It's now number one in scale among Chinese coffee chains, with nearly 30% being franchise stores.

Luckin had two very important expansions — one before its scandal, and one from late 2020 to now. This recent expansion mainly opened up third-tier cities and below, developing franchise stores. Its franchise store ratio rose significantly. Lower-tier city franchising and improved operational efficiency helped Luckin's performance improve rapidly over the past two years, with overall annual operating profit turning positive for the first time.

Luckin's large-scale expansion into lower-tier stores over the past two years solved part of its growth problem. This fully demonstrates that China's lower-tier markets have begun a brand-oriented consumption upgrade.

Consumption upgrading has several levels. We just talked about how water has had different consumption upgrades throughout. And branding means going from being able to buy pretty good things, to wanting to buy pretty good things that also have a certain brand.

If you live in a Chinese county-level city and want to treat a friend to a drink, you could find a local or cheaper chain coffee shop. But because you saw coconut latte or cheese latte on Xiaohongshu, you might spend a few extra yuan to buy them a branded, freshly ground coffee — that's Luckin's lower-tier market.

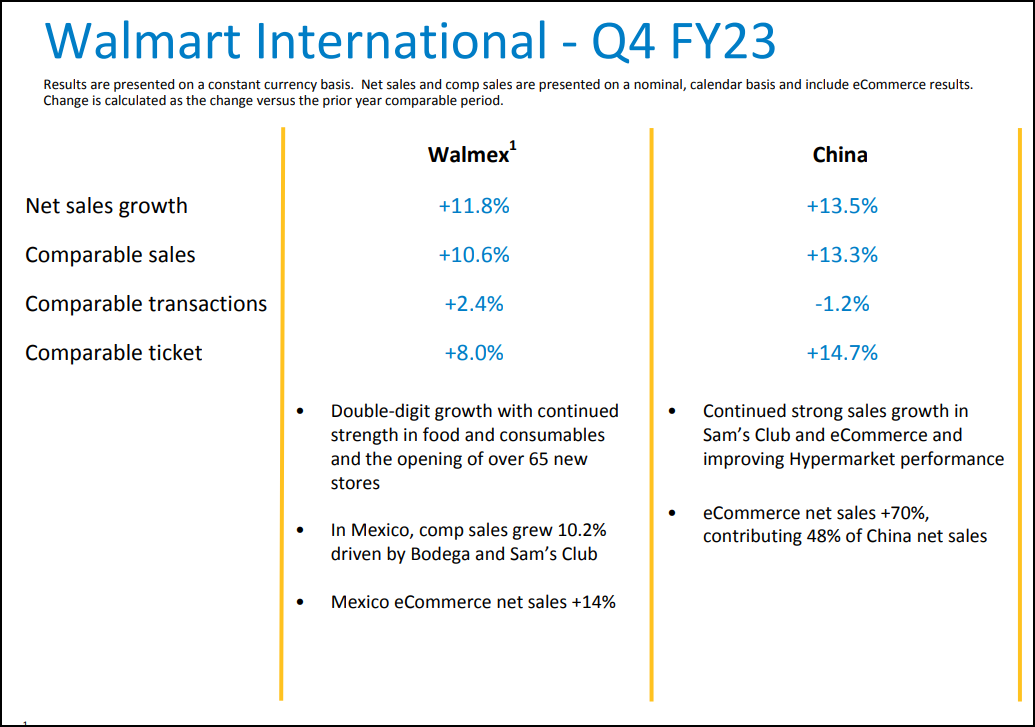

Over the past few months, two very notable directional news items have echoed this lower-tier market brand upgrade phenomenon. One is Carrefour's large-scale store closures, while Walmart achieved relatively good growth in China last year, especially in Q4 FY2022 (November 1, 2022 - January 31, 2023), with net sales growing 13.5%.

Walmart's growth data is thought-provoking. Both were among the earliest batch of supermarkets to enter China. Carrefour closed stores on a large scale, while Walmart actually achieved growth. Walmart's main growth in China came from its Sam's Club membership stores.

Sam's Club stores have relatively large space and fewer SKUs. A Sam's Club has about 4,000 SKUs, while medium-sized supermarkets and large supermarkets typically have about 10,000+ SKUs.

In October 2021, Sam's Club exceeded 4 million paid members across China. What does this mean? Over a decade ago, going to the supermarket was still a pleasure for many people. At that time, we hadn't fully entered a stage where necessities were completely satisfied. Seeing endless variety gave us a sense of satisfaction.

▲Image source: East Money

▲Sam's Club. Image source: China Business Network

People still go to supermarkets today, but endless variety no longer feels fresh. Look at Sam's — it curates a small selection of quality SKUs.

Today's consumers want efficiency, not abundance. This is probably the defining urban consumption trend of the past decade or so. And Sam's is the epitome of consumption upgrade. Consumers want better products, plus exclusive, special items. Even at slightly higher prices, many find them acceptable.

Li Xiang: How many cities is Sam's in now?

Li Feng: Over twenty. That brings me to the second news item I wanted to mention — Sam's Club is expanding aggressively into prefecture-level and even county-level cities this year. Sam's is going downmarket too.

We used to think consumption patterns mainly shifted in tier-one and new tier-one cities. But looking at Sam's expansion plans for this year, quite a few new stores are headed for lower-tier cities.

Of course this "downmarket" move is relative to tier-one — Luckin Coffee went much deeper, since it's an impulse purchase with some brand recognition. Sam's represents a new lifestyle and living choice for urban populations, and now it's moving below tier-one into tier-two and tier-three cities. That's its main expansion story this year.

Connect these consumption phenomena together and you can see a possible trend.

When we talk about boosting domestic demand today, one crucial factor is brand upgrade in lower-tier markets. This may also be a driver, a consumption trend powering China's domestic demand.

Li Feng: Of course this connects to infrastructure in the economic structure, including new infrastructure — digital infrastructure. Brand upgrade also relates to policy goals like addressing township issues, revitalizing county economies, and narrowing urban-rural income gaps. When the state builds out this infrastructure, it greatly accelerates brand upgrade in lower-tier markets.

Li Xiang: For companies, this creates opportunities for scale and chain expansion.

Li Feng: Yes, and there's a very special phenomenon here. Over the past three years, especially the past year, some retail and service sectors that previously had low chain penetration have seen it increase.

Over the past three years, scattered mom-and-pop shops struggled. Chain brands with stronger risk resilience survived. They had brand recognition and could seize the moment to expand on the supply side, because supply had contracted. It's an interesting phase-specific phenomenon.

Li Xiang: COVID actually had an unexpected consequence — it gave companies that had been concentrated in certain regions the impulse to expand outward. Because COVID taught them not to put all their business in one fixed region.

The Boundary Between Service and Retail Is Blurring

Li Feng: Speaking of Luckin and Sam's, there's another interesting phenomenon that's very important in Chinese consumption — the boundary between service and retail is increasingly blurred.

Walmart disclosed in its earnings that in Q4 fiscal 2023 (November 1, 2022 — January 31, 2023), e-commerce net sales accounted for 48% of total net sales in China. That's already quite high among large supermarket chains here. Meanwhile, e-commerce net sales grew 70% year-over-year.

▲Q4 e-commerce net sales accounted for 48% of Walmart China's total net sales, with 70% growth. Image source: Cross-Border E-Commerce Headlines

If we make an interesting comparison between Sam's Club and Luckin, you'll find that Sam's, originally a pure retail format, has taken on service characteristics, while Luckin, originally in services, has taken on retail characteristics.

Sam's Club was 100% retail, and now it's added e-commerce delivery. Compared to cafés that provide leisure space, over 90% of Luckin's coffee sales are in e-commerce form — users order online and choose delivery or pickup, which leans retail.

Going forward, as we develop domestic demand, with the help of internet development and infrastructure buildout, China's retail sector will carry many service characteristics, while China's service sector will carry many retail characteristics. This is something I find very special and remarkable about China.

The easiest example to understand is restaurants. Restaurants have dining environments, service, and evaluation metrics. But when restaurants add delivery, they extend toward retail. Because of high internet penetration, changing lifestyles among young people, China's urban structure, population density, and other factors — looking ahead, almost all efficient retail in China will likely carry service characteristics.

Another example is Freshippo, also an important emerging format. Freshippo is a large supermarket with home delivery service, and it can also prepare fresh seafood, steak, and other hot food for customers on the spot. This is a very typical case of retail adding service characteristics.

We can see this change very clearly from larger trends too. Over ten years ago, in China's department store and shopping mall formats, experience and retail were roughly 30-70. Experience included parent-child entertainment, cinemas, beauty and hair salons, and other eat-drink-play formats.

Around 2016, when Alibaba proposed the "new retail" concept, it became 40% experience, 60% retail. By pre-pandemic times, the ratio in malls had already reached 50-50.

Offline department stores used to rely more on rich product variety; now they rely more on bringing in stores that deliver good experiences and services. For example, you watch a movie, have a meal, feel good, and stroll around — riding that satisfied feeling, you end up buying things.

From every angle, China's retail sector is starting to carry service characteristics to enhance experience, while China's service sector is starting to carry retail characteristics to improve efficiency. In emerging categories in China's consumption sector going forward, most will probably exhibit this pattern.

Li Xiang: Uncle Feng has unintentionally defined "new retail" very clearly. Before, when people talked about new retail, everyone had their own interpretation. From what I'm hearing, new retail is combining retail and service, then applying digital means.

Li Feng: Yes. When something becomes fully digitized, it may not correspond to its original concrete form, but it corresponds at an abstract level. Take Taobao — everyone calls it a shelf-style department store. When you shop on Taobao, it's like browsing a department store.

Today there's an emerging format: livestream e-commerce. At an abstract level, livestream e-commerce puts experience and service into retail. During a livestream, someone demonstrates and explains products to you — just like when you go to a department store, someone carries your bags, a guide tells you which floor to go to, and takes you to brands you might like.

In a sense, livestream selling adds experiences and services that can be provided on the internet into the retail industry. Livestreaming is just one form — in China, there will be all kinds of ways to combine retail and service differently going forward.

▲Saturnbird's "Force Flight" coffee shop. Image source: Zhihu

Saturnbird's Force Flight coffee shop in Shanghai is another case. Starbucks already did well extending toward retail, selling all kinds of things in stores — coffee cup derivatives, desserts, tea, and so on.

According to Starbucks' fiscal 2022 annual report (ended October 2), retail business accounted for roughly 20% of total sales, while Saturnbird's offline café retail share far exceeds this figure.

Li Xiang: Because Saturnbird Force Flight's retail transaction value is higher than single coffee orders.

Li Feng: Yes. It uses retail to drive service. Thanks to the brand built through online business, the offline store was popular from day one. And because it opened offline stores, Saturnbird's retail business gained service characteristics.

Customers can experience offline-exclusive No. 8 series flavors and see Saturnbird's pour-over coffee capabilities, which supports Saturnbird's retail pricing range.

Take One or Two Extra Steps, and Consumer Brands Will Compete in New Directions

Li Xiang: Coffee market competition is fierce today — besides Luckin, there's MANNER, Cotti, Lucky Cup...

Li Feng: In March 2023, we did a statistical survey of China's coffee chain industry and found that chain penetration among the top ten coffee brands wasn't high: Luckin ranked first with over 9,000 stores, Starbucks second with over 6,000, but by tenth place it was only in the few hundreds.

A Meituan report, 2022 China Coffee Consumption Insights, mentioned that Shanghai already has nearly 8,000 cafés. You could say Shanghai alone has about as many cafés as Luckin has nationwide.

Starbucks and Luckin are two sides of the same coin. Starbucks provides lots of environmental experience for customers, and environment was heavily affected by COVID. Luckin, whether in store placement, efficiency, or cost control, is well-suited to delivery service. Most Luckin stores are relatively small with no seating. During the pandemic, users who wanted coffee but didn't need to drink it in-store might choose Luckin.

In recent years, Starbucks has also been going downmarket, actively expanding stores in cities below tier-two. Lower-tier city users have more leisure time and higher disposable income ratios — they have time to sit in stores and consume.

Li Xiang: Right, so Luckin's store strategy in lower-tier cities is actually different from tier-one cities. I've been to some Luckin stores in lower-tier cities — they're mainly large stores.

▲Image source: Zhihu

Li Feng: I also think that in lower-tier cities, users probably need more service and environment elements.

Li Xiang: I'm actually a bit worried about Starbucks. Starbucks' brand and various concepts are all quite good, but its pricing is indeed high relative to competitors.

Li Feng: This is the same logic as Walmart versus Sam's. Walmart is the world's largest retailer and entered China earliest, but in China, whether it's China Resources, Yonghui, or RT-Mart, all can outcompete Walmart on value. Sam's positions a notch higher, making it harder to get squeezed out.

Li Xiang: HEYTEA has already made moves to lower prices, and Chicecream has also launched cheaper ice cream lines — they're all exploring downward.

Li Feng: Let's stick with the Sam's example. Sam's has some product distinctiveness, a certain premium, and consumers accept it. If a product itself has little uniqueness, it's hard to command high prices in China.

We mentioned this at the very beginning: consumers today are more educated, and the internet has made information more symmetrical. Combine these two factors, and it's very difficult to charge a premium for no reason.

Li Xiang: Right, basically if you can't prove your product is sufficiently differentiated, you have to join the "race to the bottom."

Li Feng: But you want to "race" toward an emerging direction, to go one or two steps further. For example, following this same consumer logic, we invested in a special medical food company called Maslath.

Special medical food is like prescription medicine — when the body needs specific nutritional supplements, doctors prescribe these special foods. Beyond special medical food and nutrition-fortified products, Maslath makes two other types: one is low-GI food, meaning foods with a slower glycemic index that don't cause rapid blood sugar spikes; the other is energy-control food, where the ratios of key nutrients are relatively balanced, so you don't gain weight easily.

We had looked at the healthy food track before and almost gave up on it entirely. In users' eyes, all healthy food gets compared to snacks. Once users compare it to snacks, it can never taste as good as snacks.

▲ Image source: 36Kr

At the time, I discussed this with Maslath's founder, Tang Liming, for a long time. Eventually, he helped me understand the logic: start with sensitive populations first, like users concerned about diabetes and high blood sugar. Let these users first experience the product's professionalism. During that experience, they'll discover that healthy food can taste as good as snacks, and they'll find that remarkable.

▲ Image source: Sam's Club

Later, FreeS Fund made a sole investment in Maslath's Series A, and continued to double down in the A+ round. In 2022, Maslath's energy-control chicken breast sausages entered Sam's Club and ranked among the top monthly sellers, praised as both healthy and tasty. Maslath's lemon-flavored energy-control wafer bars, low in sugar and high in protein, are quite popular in our FreeS Fund office. (P.S. — Leave a comment below; reader perks include wafer bars~)

A key logic of healthy food is this: medicines or health supplements should move closer to the experience and taste of food, rather than food moving toward medicine. Nongfu Spring's tea beverage revenue grew over 50% in 2022, now accounting for more than 20% of total revenue. Oriental Leaf persisted for 12 years, and was even named one of China's ten worst-tasting drinks. The product first positioned itself on the functional side, waiting for consumers to gradually shift toward healthy beverages. Once consumers recognized it as a healthy product, it could "move back" toward being relatively good-looking and good-tasting, becoming popular.

Li Xiang: Nongfu Spring was smart — they also made sweetened tea drinks, Tea π.

Li Feng: Right, so in consumer goods, positioning is extremely important. Especially positioning a consumer brand based on shifts in consumer awareness — this is crucial.

05 The Essence of Retail: Localization + Supply Chain

Li Xiang: We were just talking about Walmart and Sam's Club. When I travel on business, I notice that every region or market has a local supermarket that does extremely well — like Pang Donglai in Henan, and often more than one per province. Why does this phenomenon exist? Can it be changed?

Li Feng: There's a certain rationality to it. There's a simple, enduring essence in retail: you need both localization and an excellent supply chain, and the two need to work together. The product mix needed in different regions of China — east, west, south, north — varies. Preferences have regional differences. Without enough regional differentiation, it's basically hard to do well locally.

China's new retail, or retail formats with substantial offline elements, typically needs several characteristics:

- First, a sufficiently large urban population, so the market is big enough;

- Second, the city can't be too large, housing prices need to be relatively reasonable, so the share available for consumption is high;

- Third, there need to be many small streets, making it convenient to shop;

- Fourth, residential and work areas can't be too separated, otherwise each format can only do half a day's business, with obvious tidal effects;

- Fifth, the climate should be warm, suitable for street shopping.

So places like Changsha, Xiamen, Chengdu, Shanghai, Shenzhen, and Fuzhou — because they have many young people — are more likely to give birth to distinctive new retail brands that combine online and offline.

Li Xiang: Besides Saturnbird, you haven't invested in any other coffee chain brands?

Li Feng: Correct. Mainly because offline service formats are difficult to manage, so building something like Haidilao is very hard. There's an interesting comparison here: Haidilao was profitable in 2022, while Helen's taverns lost money in 2022.

Both Haidilao and Helen's took cost-cutting and efficiency measures, but the timing was different. After the first wave of COVID was controlled in 2020, Haidilao was relatively optimistic about the future and massively expanded in Q3 2020. Because of continuous COVID impacts, Haidilao then started closing stores from the second half of 2021.

Haidilao's cost-cutting and efficiency measures took effect in 2022. It especially benefited after the December 2022 reopening. Helen's may have had the opposite rhythm — expanding in 2021, only starting to cut costs and improve efficiency in 2022.

Li Xiang: My impression is that Haidilao truly pulled away from other leading restaurant chains during the pandemic, with its overall scale moving upward.

Li Feng: Haidilao was already growing before the pandemic. Haidilao's previous expansion plan was similar to Luckin Coffee and Sam's in one respect: the stores it added from 2019 to 2021 were mainly in cities below the second tier. Haidilao is a classic case of a service industry brand moving downmarket.

Li Xiang: Some industries, companies, and brands were affected by the pandemic. For example, camping — during the pandemic, camping became very popular. After the pandemic ended, camping took a significant hit.

Li Feng: Video conferencing, camping — these experienced short-term rapid growth during the pandemic. After the pandemic, some habits persist long-term and become lifestyles, while others don't stick as easily. For example, in the US, many companies and employees still choose to work from home after the pandemic. But in China, remote work didn't become a long-term trend.

Reader Perks In today's consumer market, what new observations and discoveries do you have? Feel free to share in the comments. We'll give selected gift packs to the 2 users with the most likes and the 3 users with the most thoughtful comments (deadline: 5 p.m. on June 5). The selected gift pack includes: Detailed Talks: Wu Jun (1 book), Maslath energy-control low-fat chicken sausages (1 bag), and Maslath lemon-flavored energy-control wafer bars (1 box).

▲ Li Xiang x Li Feng: Why Did ChatGPT Emerge Today? What Happens Next? | Li Feng Column

▲ 40 Years of 3D Printing: How Far From Niche Technology to Mass Application? | FreeS Report 31

▲ Li Xiang x Li Feng: The Dollar's "Monopolistic Success" and "Gradual Dilemma" | Li Feng Column

▲ Why Are Chinese and American VC Drifting Apart? | Li Feng Column

Star the FreeS Fund WeChat Official Account for timely business insights delivered to your inbox