Li Xiang x Li Feng: The Dollar's "Monopolistic Success" and "Gradual Dilemma" | Li Feng Column

Can the U.S. Actually Bring Manufacturing Back?

This column is drawn from an in-depth conversation between Li Xiang and Feng Shu on the podcast "High Energy." Li Xiang is the curator of the Detailed Conversations book series and editor-in-chief of Dedao App.

The conversation took place in mid-October. At the time, we sensed a widely shared consensus — the ebb and flow of COVID, regional conflicts, Fed rate hikes, capital market turbulence... the world was deep in a fog of uncertainty. Meanwhile, we realized that when people confront various uncertainties, emotions tend to get amplified while genuine consensus remains scarce. Even faced with the same facts, people may interpret them in completely opposite ways.

Over the course of more than two hours of wide-ranging discussion, Feng Shu and Li Xiang shared their views on the current macro situation, talked about how Fed rate hikes affect capital markets and the RMB exchange rate, and looked back at history to explore how dollar dominance came about. Their conversation also touched on two hotly debated topics: the reshoring of U.S. manufacturing, and globalization versus deglobalization. What's interesting is that part of the answer to whether U.S. manufacturing reshoring can succeed happens to lie hidden within the dollar's "exorbitant privilege."

We've excerpted portions of Feng Shu's contributions from the podcast episode, hoping to offer one lens for observation. For the full version, please head to Xiaoyuzhou App or Apple Podcasts and search for "High Energy" to listen. Going forward, Feng Shu and FreeS Fund will be deeply involved in producing the "High Energy" podcast. We'll use this format to share our observations and thinking about the business world. You're also welcome to follow the "FreeS Fund" WeChat account — as always, we'll push first-hand industry research and investment insights there, plus edited text selections from the "High Energy" podcast.

Welcome to search for "High Energy" on Xiaoyuzhou App or Apple Podcasts to listen to the full episode

Welcome to search for "High Energy" on Xiaoyuzhou App or Apple Podcasts to listen to the full episode

Giveaway We welcome your thoughts in the comments section. The 5 most thoughtful commenters will receive a copy of The Rise and Fall of American Growth by Robert J. Gordon.

01

Why do Fed rate hikes have such a large impact?

To answer this, we first need to look at what effects interest rates bring.

First, interest rates directly affect corporate borrowing costs. When rates rise rapidly, the cost of borrowing money rises just as fast. Suppose the Fed raises the federal funds rate to around 4%. This 4% is the base rate, the minimum rate, while actual corporate borrowing rates might reach 6% or even 8%. This is why rate hikes cause economic activity to contract.

Second, changes in the benchmark rate affect capital flows and the velocity of money in capital markets. The logic is simple: the choice between allocating to stocks or bonds mainly depends on expected returns. If Treasury yields rise quickly, to the point where the returns from Treasuries clearly exceed the average dividend yield of blue-chip stocks (referring to large, established industrial and financial stocks with stable long-term growth), capital will naturally flow from the stock market to the bond market. When you can get 3% to 5% from a relatively low-risk bond, you probably won't buy stock in "Coca-Cola" and the like. After all, no matter how "blue-chip" the latter may be, they can't escape market volatility. So a lot of money gets reallocated from stocks back to bonds.

Additionally, when interest rates rise, capital tends to sit in low-risk places like banks rather than circulating back into the economy. This reduces the velocity of money.

Finally, if dollar rates rise faster, those holding multiple currencies may shift more of their time deposits from other currencies into dollars to ensure better stable returns. This is why Fed rate hikes have driven the dollar index sharply higher, putting pressure on the exchange rates of non-dollar currencies like the RMB.

The last time the dollar index broke 100 was two years ago. Around May 2020, as COVID raged globally, a striking phenomenon emerged in economic terms — except for the dollar, nearly all assets including stocks, bonds, gold, and cryptocurrencies were falling. The backdrop for both episodes of dollar strength was similar: against a surge in uncertainty, market demand for safety remained elevated, everyone wanted to hold cash, and the dollar became the safe-haven asset of choice.

This is why Fed rate hikes affect global economies and global currency exchange rates.

02

Why is the dollar so dominant?

Currency serves three main functions: medium of exchange, store of value, and investment/financing. Whether as a transaction currency, reserve currency, or investment/financing currency, the dollar is currently dominant in all three.

Data from SWIFT (Society for Worldwide Interbank Financial Telecommunication) shows that in December 2021, in global payment currency rankings by value, the U.S. dollar, euro, and British pound ranked top three with shares of 40.51%, 36.65%, and 5.89% respectively, while the RMB rose to fourth globally with 2.7%.

IMF data shows that in Q1 2022, total global foreign exchange reserves were $12.55 trillion, of which dollar-denominated assets were $6.88 trillion, accounting for 58.88%.

Yet against these figures, U.S. GDP accounted for less than a quarter of global GDP in 2021.

So how did the dollar become so dominant? Let's roughly trace the dollar's history.

The first established international monetary system in human history was actually the gold standard, created under Britain's leadership. At that time, alongside the establishment of the first global trading system, having a globally circulating and recognized standard of value became important. From silver-based, to gold and silver together, to gold standard as consensus, the development of precious metal currencies also went through a process.

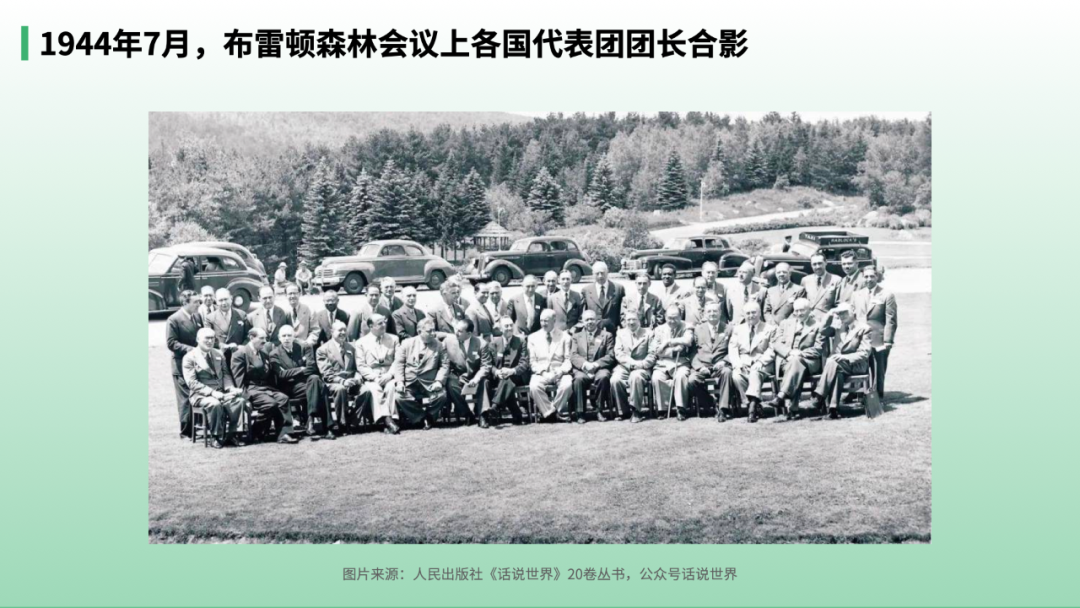

By World War I and World War II, America encountered a crucial period for its national rise. During both wars, the U.S. mainland was almost entirely spared from conflict except for a few islands. Instead, thanks to its powerful industrial production and organizational capabilities, it earned enormous wealth by selling weapons and materials. After WWII, America reached its peak in gold reserves, holding nearly 70% or more of globally circulating gold. These massive gold reserves supported the birth of the "Bretton Woods system." The basic content of this system was that the dollar was directly pegged to gold, while other countries' currencies were pegged to the dollar, and could exchange gold from the U.S. at the official price of $35 per ounce.

However, as postwar economic recovery proceeded, new problems emerged. Everyone needed large amounts of dollars, leading to severe dollar overissuance, and the U.S. gradually became unable to maintain convertibility at the 35:1 ratio. In July 1971, the seventh dollar crisis erupted. The Nixon administration announced "new economic policy" on August 15 of that year, suspending the obligation for foreign governments or central banks to exchange dollars for gold with the U.S. In December 1971, marked by the Smithsonian Agreement, the Fed refused to sell gold to foreign central banks. The dollar was essentially decoupled from gold, and dollar expansion was no longer constrained by gold convertibility.

Although the "Bretton Woods system" collapsed, over the three postwar decades, America's political, economic, and military power continued to expand. The dollar's credit was guaranteed by its strong national power, maintaining absolute dominance in all three functions — transaction, store of value, and investment/financing. Particularly in the 1970s, after Saudi Arabia signed the petrodollar agreement with the U.S., binding the dollar to oil, not only could America itself print money to freely buy oil, but it also created additional international demand for dollars, further cementing the dollar's position. At this point, the dollar solidified its throne as world currency, and America truly possessed the seigniorage rights of a world currency.

03

What happens when a country gains seigniorage rights over a world currency?

What does gaining seigniorage rights over a world currency mean? Let me give an imperfect analogy, mainly for easier understanding. It's like there's a lottery shop downstairs from my home. Initially, I went there and bought a ticket, and found I'd won two million. So, having tasted the sweetness, I went every month, and every time won two million. Such temptation is too hard to resist. After that, whenever my family encountered economic difficulties, I'd go buy lottery tickets, and started expecting bigger prizes — five million, or even larger amounts. Of course, this is just an analogy. But we can see that starting from the 1980s, whenever America encountered major or minor financial or economic crises, it would use quantitative easing — simply put, printing money to solve problems.

We can also see that after gaining seigniorage rights over a world currency, three characteristics emerged in America's economic development: first, deindustrialization; second, becoming the main driver of global trade system development; and finally, the rapid rise of finance and services as a share of the national economy.

To some extent, because "when in doubt, print money" — once you can print enough money to buy everything you want, why bother producing things yourself? Just buy from other countries. Compared to manufacturing, what a "wealthy landlord" needs more are people to help manage the money, and those providing nearby services. And the reason to promote globalization is that America can obtain more and better products at lower prices, so even if many Americans' incomes haven't grown much, they can maintain a decent standard of living.

So reading this far, some might ask: why in recent years does America seem to no longer be a staunch supporter of globalization, sometimes even playing the role of "destroyer" of the world multilateral trading system, and vigorously pushing for manufacturing reshoring? Others might ask: since petrodollars are so important for America to maintain its world currency status, why has it repeatedly sanctioned Iran and Russia, essentially pushing roughly one-third of global oil and natural gas trade out of the dollar system? This seems to run completely counter to everything that happened before.

Why would a country with seigniorage rights do things that theoretically it shouldn't? There are certainly many reasons behind this. One conclusion we can draw is that although the dollar looks very strong, this "strength" derived from seigniorage is often unstable.

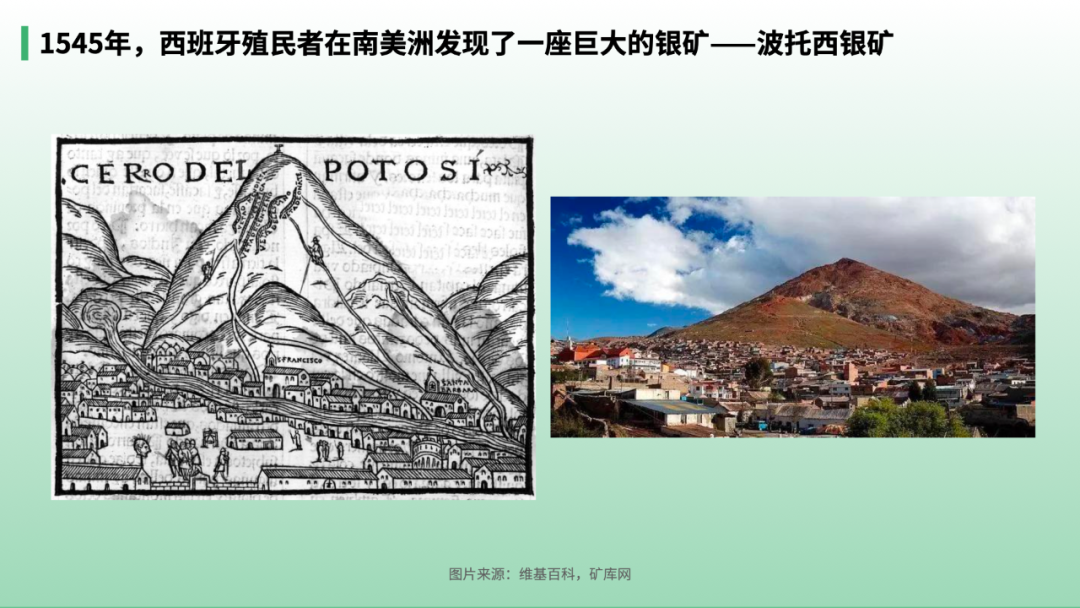

Let's look at Spain's example. In the Age of Discovery, Spain also came close to possessing world seigniorage rights. The global monetary system at the time was a precious metals system, with silver as the main currency. Before the colonial era, Europe's silver mainly came from local sources, with low production, often falling into shortage. In the 16th century, Spanish colonizers discovered multiple giant silver mines in Central and South America. After these giant mines were successively exploited and shipped back to Spain along sea routes, for a time, most of the silver circulating globally was in Spain.

But because silver came too easily, this massive windfall made Spain profligate. The three major characteristics we mentioned above that appeared in America after gaining seigniorage rights also played out in Spain at that time. Spain's handicraft industry was crowded out; industrial goods and daily necessities were no longer painstakingly produced domestically, but simply bought from other countries, which drove the development of manufacturing and service industries in surrounding European countries. Additionally, Spain's financial industry and military also developed — the former to serve the money, the latter to help it gain more colonies.

However, easily obtained wealth also became the gravedigger of the Spanish dynasty. Wealth narcotized the Spanish; they missed the Industrial Revolution. Wealth was not used to upgrade domestic industrial capacity, and they gradually fell behind in industrial and commercial development. As colonies were later eroded by other powers, Spain gradually declined.

So, seigniorage is honey in the medium term; in the long term, if the contradictions exposed in the process cannot be properly managed, today's honey may become tomorrow's poison.

04

To what extent will rate hikes drag down U.S. and global economic growth?

In 2022, inflation suddenly heated up, becoming a global problem. According to statistics from Tang Duoduo, director of the macro research division at the Institute of Economics, Chinese Academy of Social Sciences, as of May, over 40 economies globally had monthly year-on-year CPI exceeding 10%, and over 80 economies had CPI exceeding 5%.

To suppress high domestic inflation, the Fed raised rates continuously and aggressively. According to statistics from Wang Jun, a council member of the China Chief Economist Forum, since the Fed began a new rate hike cycle in March 2022, five rate hikes have cumulatively totaled 300 basis points, setting a record for the most intensive and aggressive Fed tightening since 1981.

For a country holding seigniorage rights over a world currency, due to excessive reliance on money printing, inflation is to some extent inevitable; the question is what ultimately triggers it.

Reading this far, you might wonder: since America has frequently resorted to quantitative easing whenever encountering economic or financial crises since the 1980s and 1990s, why didn't large-scale inflation occur before?

There are multiple reasons. Let's discuss one of them.

America has long had many ways to export inflation outward. Let's pull back slightly. Going back to the 1980s and 1990s, America's "deindustrialization" wave actually produced at least two results: on one hand, domestic industry's share rapidly decreased and manufacturing declined; on the other hand, with globalization, the industrialized portion was transferred to Southeast Asian and Central and South American countries.

These recipient countries were beneficiaries of globalization, their economies developed, and America similarly solved its inflation problem through globalization. Simply put: you have the ability to print more money, I have the ability to make things cheaper and cheaper. China is a typical representative of this. Thus, America balanced domestic prices by importing cheap, good-quality foreign goods. So the inflation triggered by printing more money and the decline in goods prices offset each other.

However, in recent years the RMB has been continuously deepening exchange rate marketization reforms. One result of this is that the RMB has to some extent freed itself from active or passive pegging to the international central currency, increasing exchange rate flexibility, and thus the RMB's function of absorbing large-scale U.S. inflation has weakened.

Additionally, we mentioned earlier that "petrodollars" were crucial for cementing the dollar's international currency status. Massively exporting dollars to countries needing to buy oil was also one of its methods for lowering inflation. But in recent years, "de-dollarization" in oil trade has been gradually advancing, and multiple petrocurrency systems are developing. This path for exporting inflation has also been weakened to some extent.

Inflation's impact on the U.S. economy is enormous. America's current economic growth mainly relies on domestic consumption and financial markets. Rate hikes cool the economy through two channels: increasing corporate borrowing costs, and reducing the frequency and efficiency of capital circulation. However, if inflation can truly be controlled, American citizens' relative income, consumer confidence, and spending levels may not decline and could even rise. Theoretically speaking, the locomotive driving its economic development would still have power. Conversely, if consumption and services, which contribute 80% to GDP, have problems, the U.S. economy would very likely enter recession. Once America's massive consumer market falls into recession, its pulling effect on global economic development would also weaken, thereby affecting the global economy.

05

Can America's "Entity Return" strategy succeed?

Let's state the conclusion first: difficult.

An important production factor in manufacturing is labor. Looking back at history, workers mainly came from two sources: one was conversion from agriculture, the other was large-scale immigration.

In China in the 1970s and 1980s, industrial productivity mainly came from the countryside. Through the household responsibility system, rural productivity was liberated, greatly improving agricultural efficiency; and with the rise of township enterprises, labor in the fields could be trained and converted locally. But today, young people coming to work in cities are mostly post-95s or post-00s; unlike the previous generation, they generally prefer service industry work over manufacturing. (Welcome to click One Chart to Understand Changes and Opportunities in China's Industrial Chain to review the evolution of China's industrial structure since 1978)

America faces a similar situation. In 2021, U.S. finance and services reached $18.4 trillion, accounting for 80% of total GDP, while industry's share was around 18%. A practical problem facing "entity return" is how to persuade people in services to return to factories. Data shows that the share of U.S. manufacturing employment has been on a downward trend overall since 2000; for the three years 2015-2017, U.S. manufacturing employment share had fallen to 8.8%, 8.3%, and 8.5%, and in 2019 this figure was 8.4%.

Can automation fully replace workers? This involves another interesting proposition: the timing of technological revolution. Technological revolution is most likely to occur when labor costs are high enough but not too high, because at this point adopting new technology is cost-effective. Additionally, technological substitution is difficult to leap directly to full substitution — just like the development history of AI.

So overall, to bring manufacturing back still requires finding enough workers, and these workers need to possess machine production skills. This whole affair, compared to seigniorage or other financial methods, is clearly hard work. It requires the entire country's resource allocation and education system to be able to accommodate industrial structure returning to industrialization. As we've seen in the business world: suppose a company is accustomed to doing business with 90% gross margin; when it switches to business with 19% gross margin, even the smartest company globally would have to shed a layer of skin.

Currently, China continues to maintain its position as the world's largest manufacturing country. Data from the Ministry of Industry and Information Technology shows that China's manufacturing value-added as a share of global total rose from 22.5% in 2012 to nearly 30% in 2021, with manufacturing value-added roughly equivalent to the combined total of the U.S., Germany, and Japan.

06

"Locality" and "Globalization"

In recent years, everyone has been paying close attention to topics of deglobalization and regional supply chains.

Let's look back at the Age of Discovery. The Age of Discovery was a product of the Industrial Revolution, creating large-scale global trade systems. As early as the Age of Discovery, product supply chains frequently changed.

Take cotton as an example: who was responsible for producing raw materials, who for textile manufacturing, who for sales — division of labor in the global trade system was not fixed. The book Empire of Cotton introduces how European countries reshaped the cotton industry in a short time.

Once, India and China were world-class cotton textile manufacturers; Indian weavers' products once dominated intercontinental trade — high-quality cotton textiles were sold globally, especially to Europe. After the First Industrial Revolution, in the late 18th century, the use of the water frame provided technical support for the takeoff of Britain's textile industry. India was "assigned" to retreat from textile producer back to cotton producer. Under conditions at the time, it couldn't compete with textile machines, nor could it use them. Because labor in India was extremely cheap, compared to investing in machines, factory owners found hiring people more cost-effective. Additionally, India had soil and climate suitable for cotton growth, so in the global trade system for cotton, India instead assumed the role of cotton cultivation.

Behind this is a story full of aggression, and also a cross-section of the globalization process in the cotton industry. The spatial arrangement of the global cotton industry has constantly changed, with new global divisions of labor following. Later, Britain's cotton industry lost global position; by the 20th century, Asia's cotton industry became the world's fastest-growing, and the cotton industry returned to its main place of origin.

To conclude, from a macro perspective, since the establishment of the global trade system, it has consistently advanced in terms of rationality of division of labor and efficiency improvement. Though it has experienced redistributions and iterative ups and downs that look similar to today's, it has continued marching forward on the path of globalization.

(Welcome to click "Read Original" at the bottom left of this article to listen to the full audio of Feng Shu and Li Xiang's conversation.)

Giveaway We welcome your thoughts in the comments section. The 5 most thoughtful commenters will receive a copy of The Rise and Fall of American Growth by Robert J. Gordon.

▲ One Chart to Understand Changes and Opportunities in China's Industrial Chain | Li Feng Column

▲ One Chart to Understand Globalization or Deglobalization | Li Feng Column

▲ Li Xiang × Li Feng: Remove the Emotions — What Did China Look Like in 2019?

▲ Li Xiang × Li Feng: 200 Million New Urban Residents' Consumption Awakening — Who Will "Harvest" It?

▲ In the Future, How Will Humans Work? | FreeS Report 26

▲ The Human Body's "Smartest" Organ — How to Further Explore It? | FreeS Research Institute

▲ 2022, Where Are the Next-Gen New Consumption Opportunities? | Li Feng Column

▲ Why Are Chinese and American VC Drifting Apart? | Li Feng Column