One Chart to Understand Globalization vs. Deglobalization | Li Feng Column

A Piece of History, Two Industries, Eight Companies: Understanding the Global Supply Chain

The globalization of the pandemic has cast a shadow over the globalization of supply chains.

On April 10, Larry Kudlow, chief economic advisor to the White House, called on American companies in China to consider leaving the country during a U.S. media interview—while also emphasizing the stimulus: the U.S. government was willing to pay for their relocation costs.

That same day, news broke that Japan was also urging its companies to withdraw from China. Reports stated that the Japanese government had decided to allocate $2 billion to support Japanese firms moving back to Japan, with an additional $200 million budgeted to help them relocate to other countries.

So what actually determines where global supply chains stay or go? We can break this down into three questions:

- Can the U.S. really bring manufacturing back?

- Can Japan achieve its goals of reshoring and diversifying manufacturing?

- With both the U.S. and Japan focused on "decoupling from China," is China really so easy to move away from?

Before diving in, here are a few points to consider:

- The U.S. "manufacturing reshoring" strategy has been in place for over a decade, with very limited results to show for it. Looking at the subtle博弈 between companies like Apple, Tesla, GE, and 3M and the government, what the U.S. government says has relatively little impact on corporate decisions. What's interesting is that when government priorities conflict with corporate goals, the government has chosen to protect corporate interests.

- Setting aside Japan's new "decoupling" initiatives, regardless of trade wars or pandemics, the outward migration of lower-value-added, labor-intensive supply chains is unstoppable. Fortunately, China's industrial structure has been continuously adjusting and optimizing toward higher value-added production—which is the top priority for China's supply chain development right now.

- Post-pandemic, large enterprises will definitely increase the globalization of their supply chains and sales markets in their business decisions. In this process, from market scale to supply chain structure, length, and completeness, China remains one of the most attractive countries.

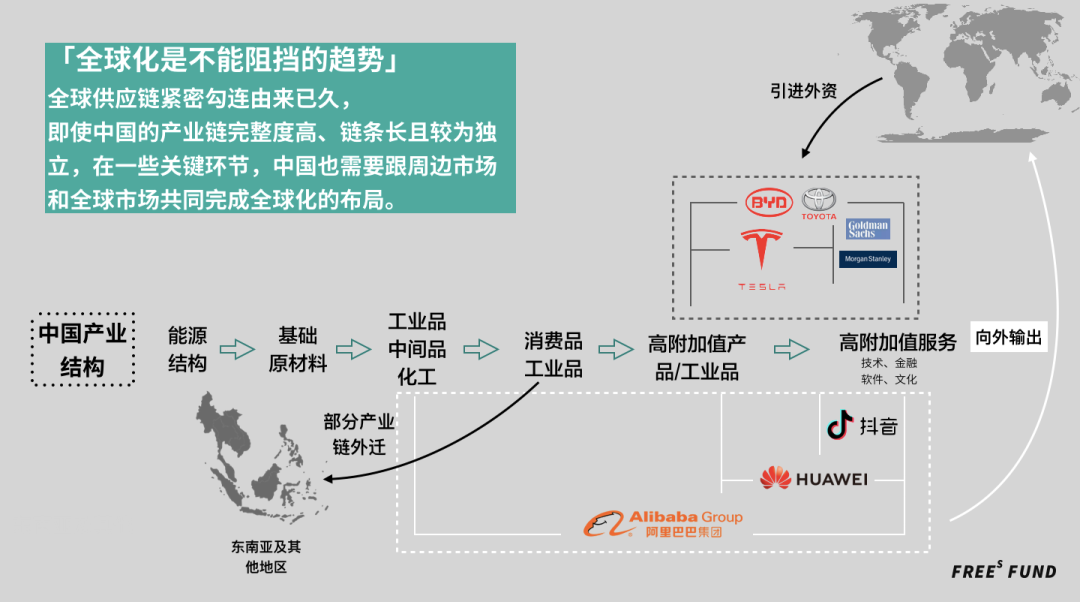

- Global supply chains have been tightly interconnected for a long time. Even though China's supply chain is highly complete, lengthy, and relatively self-contained, in certain critical links China still needs to work with neighboring and global markets to complete its globalization布局.

We hope this offers some food for thought. Feel free to share your thoughts with us at the end.

Charts by: Chen Feng

/ 01 /

Can the U.S. really bring manufacturing back?

▍Looking back: The "manufacturing reshoring" strategy has been in place for over 10 years, with very limited results.

From a growth rate perspective, in most years between 2008 and 2017, U.S. manufacturing growth failed to keep pace with overall U.S. economic growth. In 2009, U.S. manufacturing growth plummeted to -7.6%. Aside from a relatively high growth rate of 5.3% in 2010, growth in other years remained below 2.0%.

In terms of manufacturing's share of the U.S. economy, from 2008 to 2015, the value added by U.S. manufacturing as a percentage of GDP never returned to the pre-financial crisis level of 12.8%, and was far below the higher level of around 15% seen in the early 21st century.

Moreover, there simply aren't that many Americans willing to work in manufacturing anymore. The share of U.S. manufacturing employment has been on a downward trend since 2000. In 2015–2017, this figure dropped to 8.8%, 8.3%, and 8.5% respectively.

Consider this:

If 60–70% of Apple's production and sales were in Europe and the U.S., how much would Apple be affected right now?

If the pandemic had happened a year earlier, how much would Tesla's sales, market cap, and production have been affected? (At that time, nearly 100% of Tesla's production capacity was in the U.S., with 90% of sales in Europe and the U.S.)

▍Looking at the present: The U.S. government has difficulty interfering with how companies operate.

Let's look at what recently happened in the U.S. In March 2020, to combat the spread of COVID-19, President Trump invoked the Defense Production Act as a "wartime president," demanding that U.S. companies ramp up production of masks and medical protective equipment.

General Electric was named to produce ventilators and breathing equipment. 3M was required to increase N95 mask production and give "America first" priority in mask sales, and was even asked to stop exporting masks to countries like Canada.

The result? 3M initially resisted, refusing to supply masks only to the U.S. The final compromise was to both increase supply to the U.S. and not restrict exports.

So you see—even during the extraordinary circumstances of fighting a pandemic, large enterprises still have considerable bargaining power when facing government demands.

Another recent event: A Financial Times teardown video of Huawei's P40 phone revealed that American vendors including Qualcomm, Qorvo, and Skyworks provided RF components. Similarly, an analysis of components in Huawei's nova6 5G showed seven components sourced from the U.S. These are Huawei's latest models, meaning that despite U.S. government suppression and sanctions against Huawei, well-known American hardware manufacturers continue to maintain business relationships with the company.

Tesla is equally "willful." Despite escalating U.S.-China trade tensions and government calls for "manufacturing reshoring," Tesla built its first factory outside the U.S. in Shanghai, China. Not only that, it put achieving 100% "localization" of vehicle parts on this year's agenda.

▍Going further: Corporate interests and government意愿 are not fully aligned. When the two conflict, what the U.S. does with its large companies is to grant exemptions, letting them operate outside the rules.

For example, the additional tariffs on Chinese exports to the U.S. were intended to create obstacles for China and win orders for domestic U.S. companies. Instead, they touched the interests of large enterprises like Apple and GE.

Multiple major U.S. companies applied for tariff exemptions, though they needed to prove they met criteria set by the Office of the United States Trade Representative: whether the product could only be obtained from China; whether additional tariffs on the product would cause severe economic harm to the applicant or other U.S. interests; and whether the product was related to or strategically significant for Chinese industrial policies.

In September 2019, Apple submitted 15 tariff exemption applications, 10 of which were approved. In late March 2020, another Apple product—the Apple Watch—received a tariff exemption, meaning Apple would not have to pay the 7.5% tariff when importing finished Apple Watches from China.

Besides Apple, another company that recently received an exemption from the U.S. government was GE. On April 7, 2020, Reuters reported that GE had obtained U.S. government approval to supply engines for China's C919 large passenger aircraft.

What happened to Apple and GE shows that when corporate interests conflict with government意愿, the U.S. government yields and lets companies "make money"—even when their partners are countries the U.S. seeks to压制.

▍Why do multinational corporations like Tesla, Apple, and GE risk confronting their governments to do business with China? The reason is simple: they must take the Chinese market seriously.

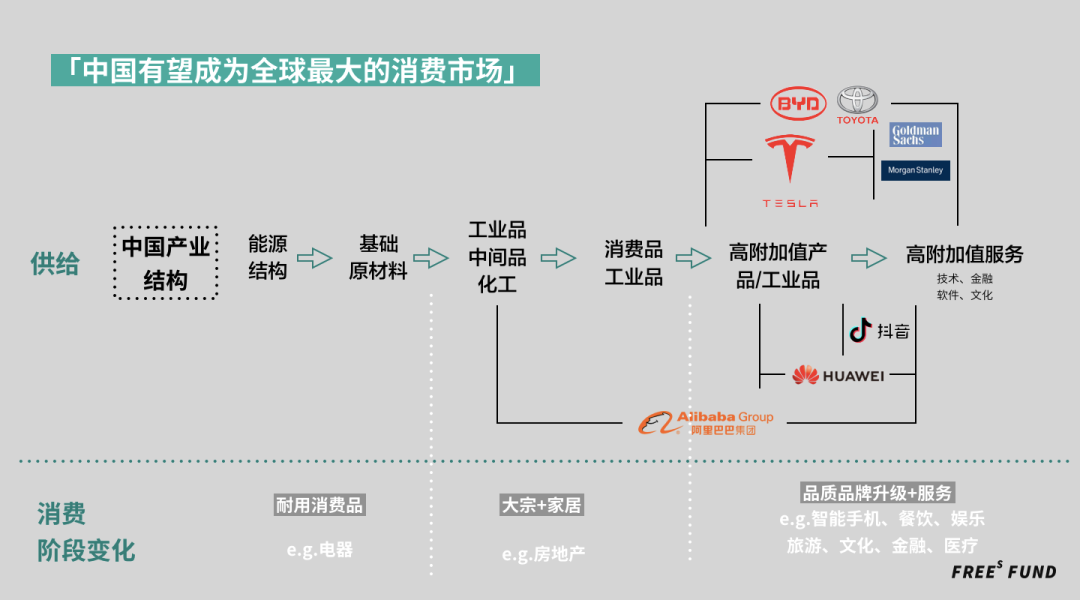

In many industries and sectors, China is already the world's largest single market. This is an irresistible attraction.

Data from research firm Canalys shows that in Q1 2012, China surpassed the U.S. to become the world's largest smartphone market for the first time, and has held the top spot ever since.

In 2009, China became the world's largest new car market. Six years later, in 2015, China also claimed the top spot globally for new energy vehicles. According to projections from the Ministry of Commerce, by the end of 2020, China's vehicle ownership is expected to surpass that of the U.S., making it number one in the world.

The rapid growth in China's passenger and freight transport demand is also driving an explosion in the aviation market. The International Air Transport Association expects that within five years, China will replace the U.S. as the world's largest aviation market.

With some optimism, in 2020 China could very well surpass the U.S. to become the world's largest single consumer market. Last year, China's total retail sales of consumer goods were 3% behind the U.S. Given that China has already begun recovering from the pandemic while the U.S. epidemic situation remains severe, if the pandemic's impact on U.S. retail consumption exceeds that on China by more than 3%, then—without considering growth rates and other factors—China could become the world's largest single consumer market in 2020. Even accounting for growth rates, the U.S. GDP growth rate in 2019 was 2.3%, while China's was 6.1%.

So, when we discuss whether supply chains will flow back to the U.S., a question large enterprises must face is: do they want to make money in China, which is the world's largest market in almost every important industry?

A quick thought exercise:

Q: Compared to before the pandemic, how might the U.S.-China trade war differ after the pandemic?

Give us a "like" at the end of this article, then reply "globalization" in the backend to get our answer.

/ 02 /

With both the U.S. and Japan focused on "decoupling from China," is China really so easy to move away from?

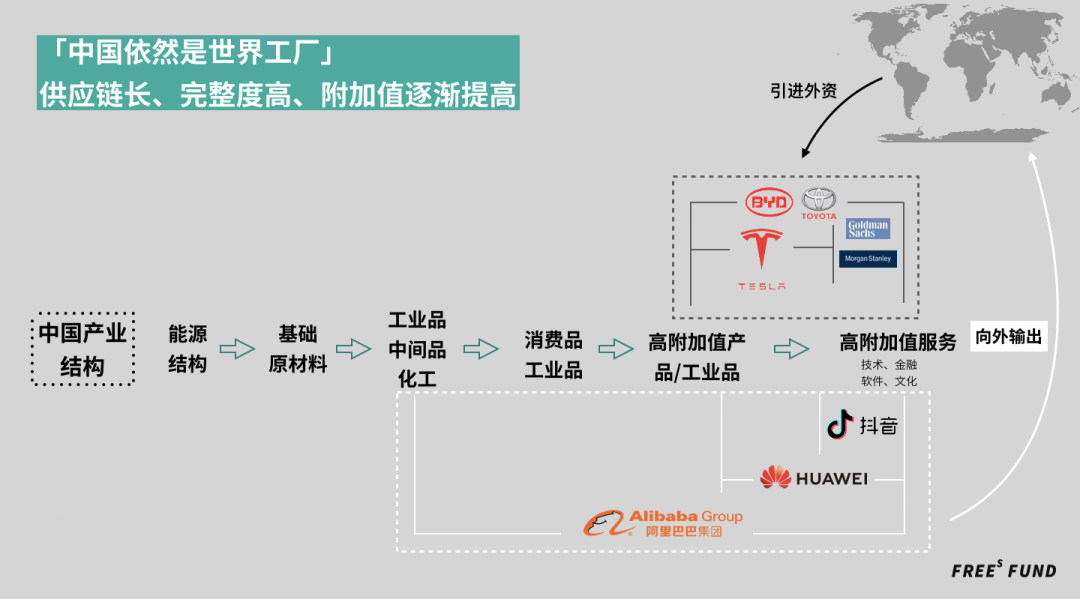

▍China's supply chain is unavoidable: "Bigger," "Thicker," and "More Value-Added"

From the emergence of township enterprises around 1984 to today, Chinese manufacturing has developed for nearly 40 years and now embodies the characteristics of being the world's largest, most complete, and longest. After China's manufacturing output first surpassed the U.S. to become world number one in 2010, it has never lost that top position. This makes it difficult for any country's pillar industries to bypass China in their supply chains.

While "getting bigger" and "getting thicker," China's industrial structure has also been "adding value": beyond scale, it has taken on high-value-added precision processing. (We'll break down the evolution of Chinese manufacturing in a future piece.)

Take the auto and mobile phone industries, widely considered the most difficult to manufacture.

China has long been firmly established as the world's largest auto producer. According to marklines data, of the approximately 90.87 million vehicles produced globally in 2019, China accounted for 28.3%.

China also has one of the most complete automotive supply chains and highest localization ratios. We have over 100,000 auto parts enterprises, basically achieving full coverage of 1,500 types of auto parts. On the other hand, the world's top 50 tier-one and tier-two parts suppliers have all established factories in China; the world's top ten tier-one foreign suppliers have deployed over 400 production plants and R&D facilities in China.

This powerful automotive supply chain is what gives Tesla the confidence to propose changing its localization ratio from 30% to 100% this year. China is probably the only country that can achieve this goal in such a short time. The rapid construction and approval of Tesla's Shanghai factory earlier already highlighted "China speed."

Mobile phone brands also favor Chinese supply chains. In recent years, Apple has accelerated moving its supply chain to China. Despite the U.S.-China trade war, looking at the composition of Apple's top 200 global suppliers in 2019, the number and proportion of Chinese factories still increased noticeably. In 2018, Apple had 778 factories globally, with 356 in mainland China (45.76%); in 2019, of Apple's 807 global factories, 383 were in mainland China (47.46%).

China's contribution to the mobile phone supply chain has long exceeded mere contract manufacturing. China already has several world-class mobile phone brands including VIVO, OPPO, Xiaomi, and Huawei. In 2019, domestic brands occupied 3 of the top 5 global smartphone manufacturers, with Huawei's shipments and market share both surpassing Apple's. This shows that the R&D and manufacturing capabilities of China's mobile phone supply chain have been continuously developing and improving.

▍During the pandemic, China's supply chain helped foreign companies resume production

As the pandemic spread globally, affecting over 200 countries and regions, many countries successively fell into shutdowns. Apple's and Tesla's Chinese supply chains, to some extent, helped them hedge risks and improve efficiency.

Due to the global pandemic, Apple lowered its revenue forecasts. Foxconn, Apple's largest assembler, also announced that Q1 2020 revenue fell 12% year-over-year.

As China gradually resumed work and production, we've also seen some positive turnaround news.

Based on Q1 preliminary disclosures from four suppliers shared by Apple and Huawei, Luxshare Precision Industry Co., Ltd.'s net profit grew 55–60% in Q1 2020, Avary Holding's March 2020 revenue grew 19.4%, Goertek's Q1 2020 net profit grew 40–60%, and Lens Technology expected profit of 879–884 million yuan (compared to a loss of 96.96 million in the same period last year).

The reasons, on one hand, were the fulfillment of pre-pandemic inventory orders; on the other hand, likely because production resumed in China, taking orders from regions where the pandemic was climbing and work had stopped.

Tesla similarly benefited from China's supply chain.

Currently, Tesla's U.S. factory has shut down, and it's even been embroiled in controversy over laying off contract workers. However, in China, Tesla's Shanghai factory—completed in early January 2020—resumed production on February 10, becoming one of the first auto companies nationwide to return to work. That same day, Tesla's tier-one supplier Shanghai Lingang Joyson Safety Systems Co., Ltd. also resumed operations.

Tesla's efficient resumption of work in China also received support and protection policies from national and local governments for important supply chains. According to statistics, since March 6, Tesla Shanghai factory's resumption rate has exceeded 91%, with production capacity even surpassing pre-pandemic levels.

A quick thought exercise:

Q: Currently, foreign trade is in a difficult period with weak external demand. In your view, will foreign trade "dip first, then rebound" this year?

Give us a "like" at the end of this article, then reply "globalization" in the backend to get our answer.

/ 03 /

"Decoupling from China" and "Globalization"

▍Behind "decoupling from China" lies concern about over-dependence on China's supply chain

As described above, as a manufacturing powerhouse, China has established a relatively comprehensive set of industrial categories, with long and highly complete supply chains and high technological value-added. Countries worldwide benefit from this, but may also be severely hurt by it.

Take Japan as an example. Since 2007, China has been Japan's largest trading partner. According to statistics from the Japan External Trade Organization, in 2018, Japanese enterprises' cumulative investment in China reached $108.2 billion, ranking first among all countries. Due to this pandemic, China's mask exports to Japan were somewhat affected, and Japan realized that strategic medical supplies like masks should not be overly dependent on imports. According to previous disclosures from Japan's Ministry of Health, Labour and Welfare, 70% of masks sold in Japan came from China.

Whether encouraging manufacturing to return or spending effort to relocate manufacturing elsewhere, the goal is to optimize supply chains to make them more complete, independent, and diversified.

Concentrating supply chains in one country is like putting all your eggs in one basket—very risky.

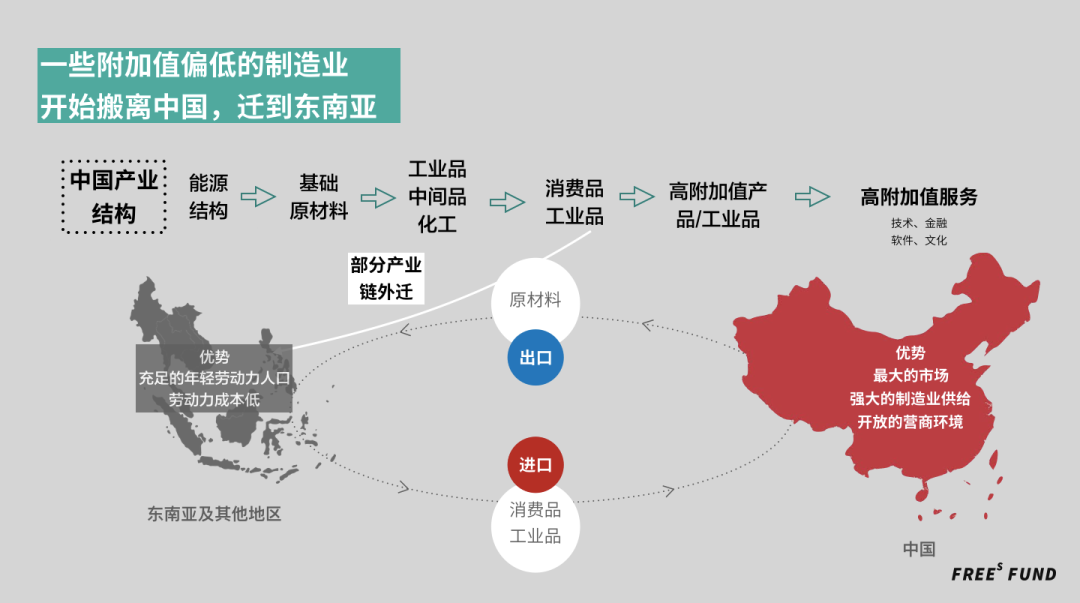

▍Going to Southeast Asia: Since relocation cannot be stopped, what should we keep?

In recent years, some lower-value-added manufacturing has indeed begun moving out of China to emerging countries in Southeast Asia.

Frankly, this is something we can neither stop nor deny the rationality of.

As China's population structure ages, young people are decreasing, and with rising labor costs, we no longer have advantages in undertaking large-scale, low-value-added, extremely labor-intensive production. Meanwhile, emerging countries in Southeast Asia have cheaper labor and sizable young populations.

So regardless of trade wars, pandemics, or policies encouraging corporate relocation, this portion of supply chains could potentially be transferred.

However, this relocation process may be much more difficult and slower than many imagine.

First, it's hard to imagine that in the present and for a considerable time after the pandemic, large enterprises would be willing to reduce efficiency and increase investment to move. For a considerable period going forward, the primary goal of multinational enterprises should be maintaining growth, while supply chain relocation requires significant capital investment and requires companies to endure short-term efficiency reductions.

Even if the government pays for relocation costs, this is still an unprofitable business decision. To return to the growth track as quickly as possible, the most efficient approach right now is to not make waves—to stay in place and collaborate within the already-formed, interdependent global supply chain.

Second, from a medium- to long-term perspective, China's "largest and most complete supply chain" is the result of adapting—actively or passively—at different historical stages. This is difficult for other countries or regions to replicate. Beyond the extreme uniqueness of its historical formation, considering the massive total labor force involved, the entire chain is difficult to migrate to other countries in a short time.

Furthermore, the overall competitiveness of China's market is a powerful pull for foreign enterprises investing in China. China has one of the world's top consumer markets and powerful manufacturing capabilities—essentially occupying both production and consumption ends. Placing factories close to the market is a rational choice for enterprises. Additionally, we have open policies and business environments, and continuously improving and upgrading infrastructure.

If what's relocating is cost-extremely-sensitive, low-value-added production and processing—that is, labor + manufacturing—then what we need to grasp is value-added + manufacturing: continuing to optimize supply chain structure, increase value-added, so that we can produce increasingly expensive products within the manufacturing chain, and continuously improve quality and efficiency.

If we look one step further, what we need are productivity drivers for the next cycle. Like the steam engine of the 18th century, or computers in 1960s America.

▍The business world is destined to be global

Business is profit-driven. Setting aside emotions, politics, and other factors, and considering purely from a business perspective, it's absolutely correct for enterprises in various countries to fully utilize advantages everywhere, making supply chains thoroughly globalized and diversified to ensure stability and security.

After all, with布局 in multiple countries and regions, at least everything won't completely shut down simultaneously when a specific crisis hits. As Apple CEO Tim Cook said in a recent media interview: "There's always unpredictable things happening. We've gone through earthquakes, tornadoes, fires, floods, tsunamis, and SARS."

I believe that after this pandemic, all medium- to large-sized enterprises, especially multinational corporations, will have deeper understanding and appreciation of globalization, and will value it even more.

One week before news broke of Japan encouraging supply chain relocation, on April 2, the pure electric vehicle R&D joint venture between Toyota and BYD was established. The joint venture is registered in Shenzhen, with Toyota and BYD each contributing 172.5 million RMB, each holding 50% of the company's shares.

This cooperation, combining Japanese and Chinese technology and experience, can be seen as a footnote to business globalization. The electric vehicles produced by the joint venture will be developed based on BYD's technology, then sold under Toyota's brand.

It also illustrates three things.

One, for Japanese automakers, China's new energy vehicle market is very attractive, so Toyota is increasing investment in China.

Two, China's electric vehicle technology and supply chain are already in a globally leading position. Toyota is already among the most top-tier enterprises in the auto industry in terms of technology, sales, and management. Its choice of Chinese technology for EV R&D also indirectly confirms this point.

In new energy vehicles, batteries—which account for the highest cost share at about 42%—China has the world's number one and number three players in CATL and BYD. For IGBT, the core technology of new energy vehicles, China has also achieved supply chain autonomy, with BYD Microelectronics, CRRC Times Electric, and Starpower Semiconductor. Additionally, BYD has independently developed an industry-leading three-in-one e-platform. Simply put, this technology integrates several important EV-related components into one, minimizing component space, lowering costs, and maximizing vehicle performance. Toyota's choice of Chinese technology for EV R&D also indirectly confirms these technological advantages.

Three, with foreign ownership permitted (in October 2018, BMW Brilliance opened the precedent for joint venture automakers to be foreign-controlled), Toyota still chose a 1:1 equity ratio to cooperate with a Chinese automaker. This shows that when exploring cooperation possibilities, Chinese and Japanese enterprises had equal bargaining chips, because equity ratios reflect each party's contribution to the joint venture.

To some extent, this is the result of structural optimization in China's automotive supply chain. It shows that China's importance in the automotive supply chain is rising, enabling us to attract top international automotive brands to establish operations in China and cooperate with Chinese enterprises as equals.

/ 04 /

Will extreme sanctions happen? If they do, what happens to us?

Rhetoric around "deglobalization" and "decoupling from China" has emerged from time to time in recent years, but will decoupling really happen? If countries worldwide apply maximum pressure on China, what impact would this have on China's supply chain?

We answer this with one contemporary example and one historical episode.

For the present, let's again use Huawei. Over the past year, Huawei's sanctions and封锁 by the U.S. have been plain for all to see. In the world's most difficult industry, facing maximum pressure from the world's most powerful country—what has been the impact on Huawei?

Teardowns show that Huawei's latest phones, the P40 and nova6 5G, contain 2 and 7 American components respectively, with cost shares that are practically negligible. By contrast, before the trade war, Huawei's 2018 core supplier list had 92 companies, with American suppliers being the most numerous at 33.

This means that since the U.S. restricted Huawei from importing American technology, the number of American components in Huawei phones has been continuously decreasing. While accelerating "de-Americanization," the trade war has also spurred Huawei to increase R&D efforts to achieve supply chain localization or substitute with diversified suppliers.

Earlier, Huawei Consumer Business CEO Richard Yu stated in a media interview: Huawei's supply chain can operate without using American components; Chinese enterprises' capabilities are growing stronger, and we're giving domestic companies more opportunities. Taking the Huawei P40 as an example, the 210 components provided by China for it already account for 60.7% of costs.

Historically, we've also experienced the worst-case scenario.

Around 1990, due to special circumstances, China was once subject to joint sanctions from Western countries. An anti-China wave swept globally, and political, economic, and military relations and cooperation between China and many countries including the UK, France, the U.S., and Japan were cut off.

Facing comprehensive sanctions, Deng Xiaoping's stance was: "Of all countries in the world, China is the least afraid of isolation, the least afraid of blockade, and the least afraid of sanctions."

The result: we traded one year of difficulty for 20 years of miraculous high-speed economic growth.

In that sanctioned year, China's GDP growth rate was 3.8%, the lowest since reform and opening up. But after that, our GDP growth curve rose all the way, maintaining approximately 10% growth for nearly 20 years. Even though at that time, as a country we were still very weak—China's total GDP that year was equivalent to just one Chinese city today: Suzhou (which ranked sixth in China's 2019 GDP, first among non-municipalities and non-provincial capitals).

The 1990 blockade and sanctions also brought an unexpected result. With foreign economic and trade relations cut off, unable to buy, the only option was to find ways to be self-sufficient—creating the long supply chain of Chinese manufacturing. This also laid a solid foundation for China to become the world's factory.

So you see, when we were still weak and the international environment was extremely poor, we could still turn crisis into opportunity and solve problems. Today's international situation and economic environment, though complex and full of uncertainty, is something we can certainly overcome and win development from.

Summary

1 The U.S. "manufacturing reshoring" strategy has been in place for over a decade, with very limited results. Looking at the subtle博弈 between companies like Apple, Tesla, GE, and 3M and the government, what the U.S. government says has relatively little impact on corporate decisions. What's interesting is that when government priorities conflict with corporate goals, the government has chosen to protect corporate interests.

2 Setting aside Japan's new "decoupling" initiatives, regardless of trade wars or pandemics, the outward migration of lower-value-added, labor-intensive supply chains is unstoppable. Fortunately, China's industrial structure has been continuously adjusting and optimizing toward higher value-added production—which is the top priority for China's supply chain development right now.

3 Post-pandemic, large enterprises will definitely increase the globalization of their supply chains and sales markets in their business decisions. In this process, from market scale to supply chain structure, length, and completeness, China remains one of the most attractive countries.

4 Global supply chains have been tightly interconnected for a long time. Even though China's supply chain is highly complete, lengthy, and relatively self-contained, in certain critical links China still needs to work with neighboring and global markets to complete its globalization布局.

Discussion Questions

Q1: Compared to before the pandemic, how might the U.S.-China trade war differ after the pandemic?

Q2: Currently, foreign trade is in a difficult period with weak external demand. In your view, will foreign trade "dip first, then rebound" this year?

Give us a "like" at the end of this article, then reply "globalization" in the backend to get our answers.

▍Coming Up

Next, we'll also explore the historical impact the pandemic may cause, the pandemic's impact on investment and capital markets, and innovation opportunities driven by "new infrastructure" stimulus under the pandemic.

Follow FreeS Fund's WeChat official account (id: freesvc)

▍References

- "White House and 3M Reach Truce, U.S.-Canada 'Mask Dispute' Ends Happily?", The Paper

- "Trump Orders General Motors to Produce Ventilators Under Defense Production Act", AutoQa

- "The Rise and Fall of U.S. Manufacturing: Does 'Reshoring' Work?", Caijing Baoshe

- "Exclusive Interview with Cao Dewang: Why Must Manufacturing Supply Chains Stay in China?", The Beijing News

- "Morgan Stanley: This Crisis Will Slow, Not Accelerate, Supply Chain Relocation from China", China Economic Weekly

- "Will Japanese Companies Leave China? Japan External Trade Organization Survey: Nearly 10% of Japanese Enterprises in South China Discuss Moving Out of China's 'World Factory'", International Investment Bank Research Report

- "478.3 Billion Yuan! Global Investment in China Accelerates, U.S., Japanese, and German Companies Refuse to Leave China's Market!", Jinshi Data

- "Japan Mask Shortage, One Box Sold for 3,145 Yen! Now Announces Resumption of Chinese Mask Imports", Jinshi Data

- "China's Relations with Japan", Huanqiu.com

- "2019 Global Top Five Smartphone Manufacturer Rankings Released, Huawei Takes Second", CNMO

- "U.S.-China Trade Momentum Shifts, Apple Supplier Supply Chain Center Shifts", EO Intelligence

- "International Air Transport Association: China Will Replace U.S. as World's Largest Aviation Market", 10jqka.com.cn

- "Ministry of Commerce: China's Vehicle Ownership Expected to Surpass U.S. by Year End", Beijing Daily

- "GE Obtains U.S. Government Approval to Supply Engines for China's C919 Large Aircraft", Two Engines Power Control

- "Trade Friction Series Report No. 6: Which Tariffs May Ultimately Be Exempted?", Sina Finance

- "Tesla to Achieve 100% Localization by Year End, Who Will Be the Next Supplier?", Yicai

- "Microsoft Approved to Sell Software to Huawei, But Huawei Still Awaiting Google GMS", ITHome

- "Foreign Teardown of Huawei P40 Reveals: Proportion of American Components Hits New Low, Only RF Module Uses [U.S. Parts]", Qu Dong Zhi Jia

- "Huawei First Releases Core Supplier List: Cooperates with 33 American Manufacturers", Securities Times

- "How Did China Withstand Western Sanctions Pressure in the Early 1990s?", Guancha.cn

- "Why Did Toyota Choose BYD?", EO Intelligence

(Welcome to read, share, and give us a "like." For reprints, please reply "reprint" to learn reprint rules, and contact Feng Xiaorui [ID: freesfund] for authorization. Copyright belongs to FreeS Fund.)

2020: The Travel Industry's Reshuffle and Restart | Frees Fund After the Pandemic: Education's Life-or-Death Elimination Round | Frees Fund After the Pandemic: The New Landscape for Fresh Food, Catering, and Food | Frees Fund After the Pandemic: A New Era for "Good Companies" | Frees Fund Li Feng Column 16 | Fresh Retail: Learning Early-Stage Investment from the Secondary Market Li Feng's New Year Outlook | One Chart to See 2020 China Opportunities