Our Three Years: Experimenting, Exploring, and Pushing Forward

Still believing in the mission, still hoping to create value.

Marking the final close of FreeS Fund's RMB Fund I (hereafter "Fund I") as our starting point, by late May of this year FreeS Fund will have completed its first full three years. We're still a young firm. What have we grown into during these three years, and what twists and turns have we navigated? Looking at the present, how do we view the industries and sectors we've focused on? And looking ahead, how will we position Fund II? Below is our retrospective and outlook.

01

Fund I: The Modest Goal, Largely Achieved

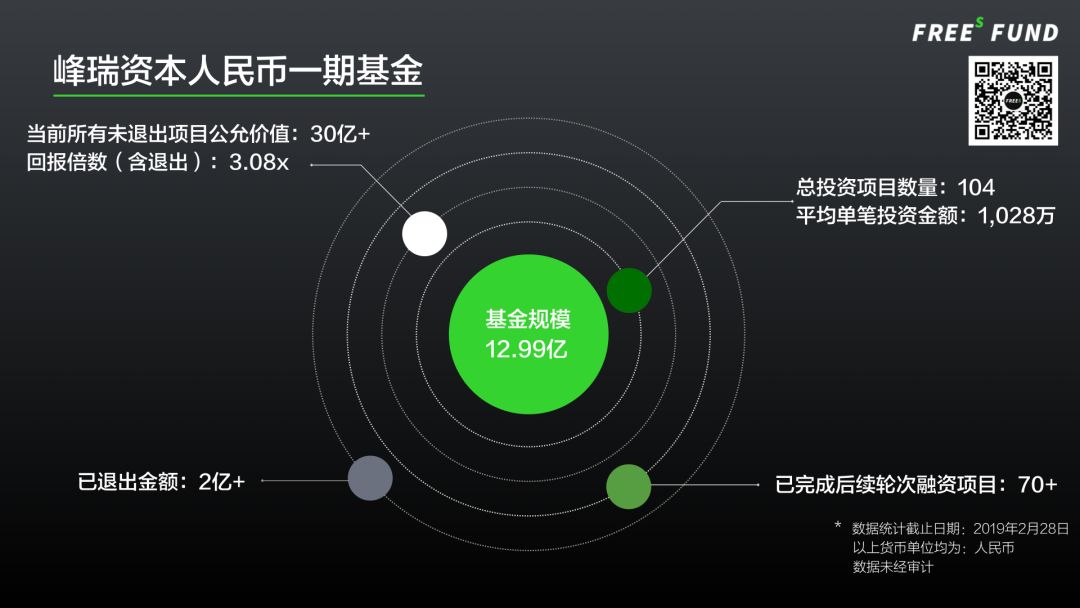

Three years ago, we set ourselves a target: Fund I needed to deliver at least a 3x return. Three years later, we've largely hit that modest goal.

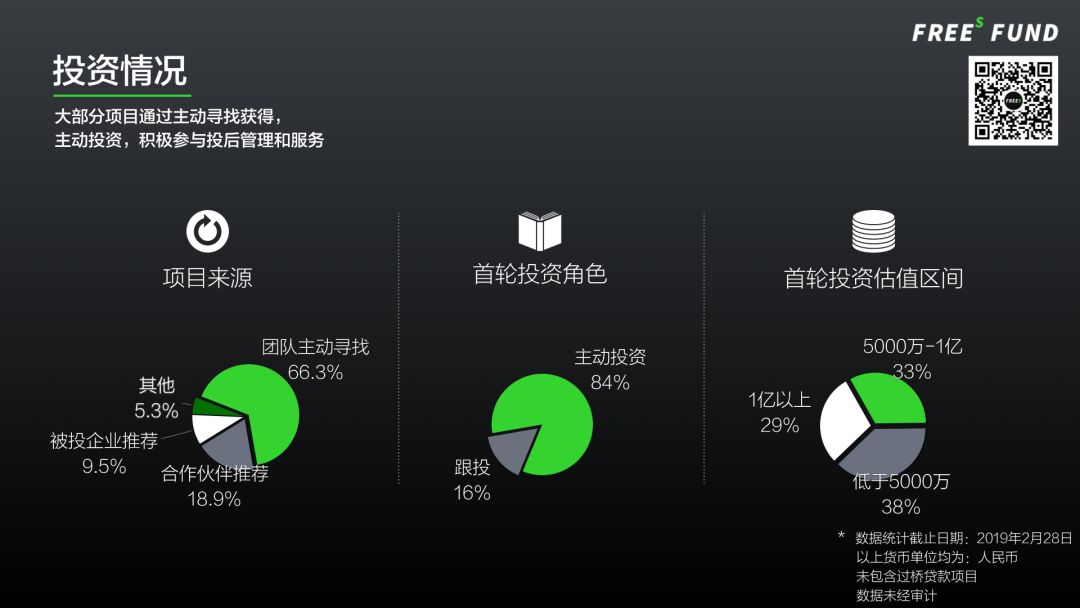

From the portfolio perspective: over the past three years, Fund I invested in 104 companies, with an average check size of around RMB 10 million, ranging from RMB 2 million to RMB 30 million per deal. By initial investment stage, angel rounds accounted for two-thirds of projects, with Pre-A and Series A making up the remaining third. Sectors covered consumer, deep tech, and enterprise services. Proactive sourcing by our team was the primary deal flow channel, representing two-thirds of total investments. We led or invested solo in over 80% of deals.

To date, approximately 70% of portfolio companies have completed follow-on financing. Sixteen companies have achieved valuations exceeding RMB 1 billion. FreeS Fund has also been actively involved in portfolio management and services, holding board seats in over three-quarters of invested companies.

On the people side, the profile of our portfolio CEOs is shown above: post-80s and post-70s generations make up the bulk, with post-80s as the main force at 59%, and post-70s at 34%. The majority (61%) have overseas study or work experience. Seventy-one percent hold master's degrees or higher, including 29% with PhDs, postdocs, or professorships. Less than one-third have been entrepreneurs for fewer than three years; over 40% have more than five years of entrepreneurial experience. Serial entrepreneurs account for 43%, and one-fifth have started three or more companies.

As of end-February 2019, Fund I's return multiple was 3.08x, with an IRR of approximately 70%. Of course, these are paper returns. Given that Fund I is no longer making new investments and most portfolio companies are still growing, we expect the final return multiple to be even better.

From a fund operations perspective, Fund I's DPI is currently quite substantial. To date, FreeS Fund has completed full or partial exits from seven projects, plus one project currently in exit closing, with cumulative exit proceeds approaching RMB 300 million.

By September 2019, when the fund enters its harvest period, I believe FreeS Fund will have ample opportunity and confidence to generate even greater returns for our LPs through various exit mechanisms.

02

Behind the Numbers: Five Principles We Stuck To

Behind these figures, I think, lie five principles. First, diversified allocation across investment directions to mitigate sector cyclicality. Second, paying attention to China's rising technological innovation force — a capability we've newly developed. Third, cross-disciplinary investment capability, emphasizing both expertise and intersectionality. Fourth, staying research-driven, analyzing coolly, and judging independently. And finally: embracing change, driving change, and valuing people. Let me explain each in turn.

▍Diversified allocation to mitigate sector cyclicality. The best way to fight cycles is through diversification. Diversification means actively seeking quality investment opportunities in sectors where we have existing familiarity, understanding, and resource advantages, while simultaneously learning quickly and venturing into entirely new industries. Moreover, at different stages of economic development and industry maturation, we should maintain an open mind toward different directions.

Turning the clock back to over three years ago, when FreeS Fund was newly established, beyond leveraging my accumulated resources in TMT, I also entered deep tech and enterprise services — areas where I had zero prior knowledge — amid considerable controversy. Forcing myself to learn chip investing and biotech investing was genuinely painful, like going through university all over again. Today, tech and enterprise services account for nearly 60% of FreeS Fund's investment allocation. Tech projects in particular have jumped from 0% three years ago to nearly 40%, now roughly on par with consumer investments.

The value growth curves across our three major sectors — consumer, tech, and enterprise services — show that growth momentum and pace vary significantly by sector each year. In year one, consumer-leaning projects showed better growth. In year two, both consumer and tech heated up simultaneously. In year three, after two years of accumulation, compounded by policy tailwinds, tech became wildly popular in capital markets; by year-end, enterprise services began emerging as the new hotspot.

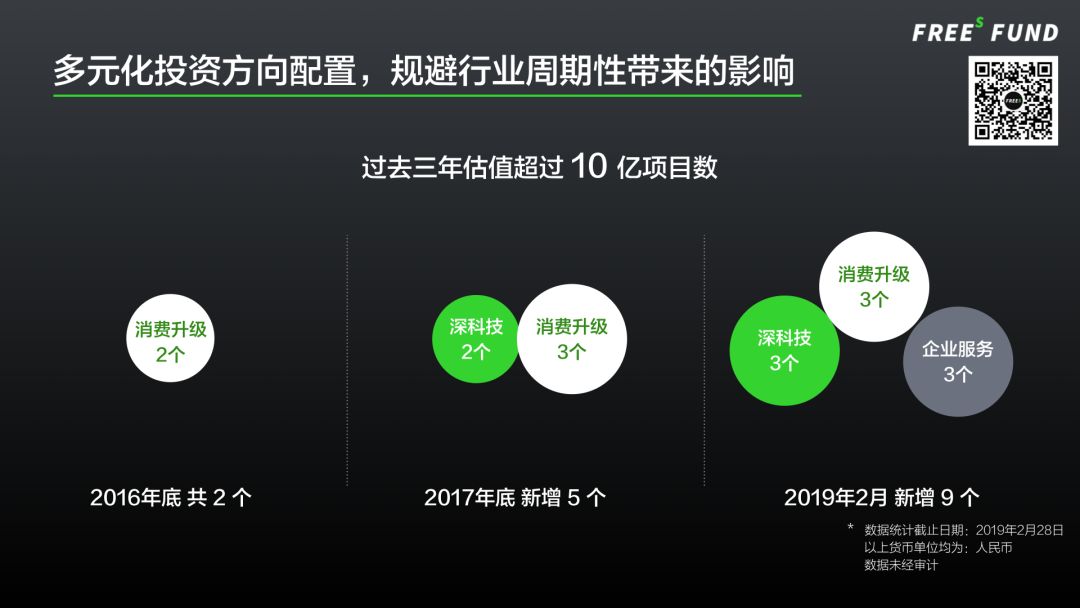

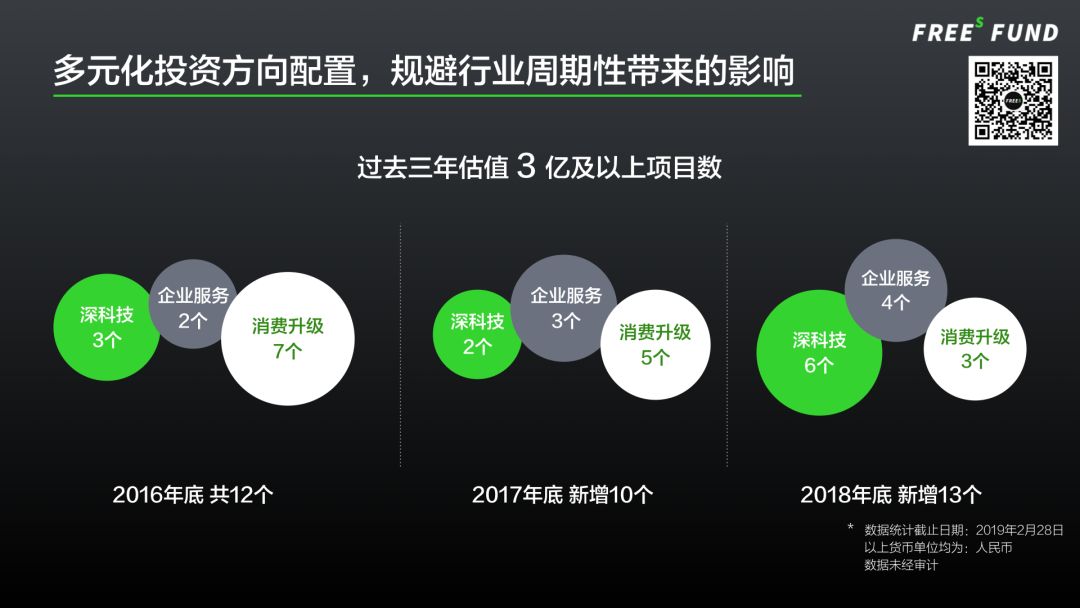

Thanks to our diversified allocation, even in 2018 — which most considered a winter — our portfolio companies' growth and development pace didn't slow; if anything, they performed slightly better than the previous two years. In 2018, Fund I added nine new portfolio companies valued above RMB 1 billion, and 13 more companies crossed the RMB 300 million valuation threshold.

Additionally, I'm gratified that among the 35 projects currently valued above RMB 300 million, over 20 are in directions I never participated in or led during my pre-FreeS Fund investing career, including chips, industrial automation, industrial internet, new materials and energy, and medtech. These represent capabilities we've newly developed over the past three years through continuous expansion of our perimeter.

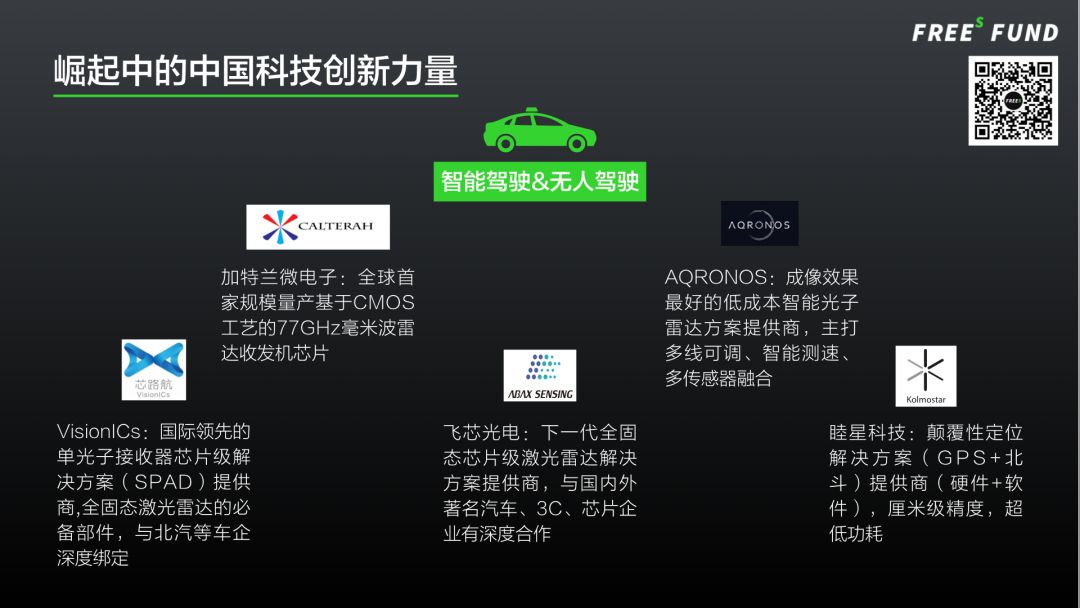

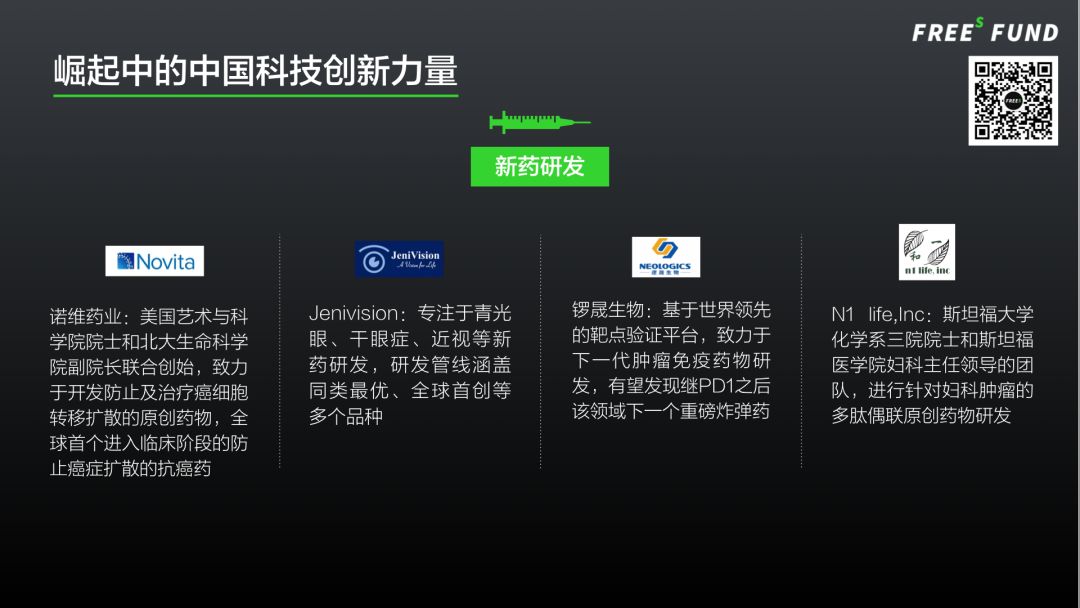

▍Paying attention to and investing in China's rising technological innovation force. Three years ago, we were complete novices in tech. Three years later, from new materials and energy/environmental to chips and sensors, extending to IoT, and onward to medtech, FreeS Fund has built out its investment map across numerous sub-sectors.

Spotlighting China's Rising Tech Innovation

(Swipe left or right to see more photos)

We're also proud to back companies that are "globally leading" in their fields. A few examples:

- In new materials, FreeS Fund invested in QingTao Development, the world's first company to mass-produce solid-state lithium batteries;

- In synthetic biology, we invested in Bluepha, the world's only provider of all types of PHA bioplastics;

- In semiconductors, we invested in NextVPU, whose AI vision processor chip N171 set new world records across multiple parameters; and Calterah Microelectronics, another FreeS Fund portfolio company, became the first in the world to mass-produce 77GHz mmWave radar transceiver chips based on CMOS process technology.

- In medtech, Novita developed the world's first anti-cancer drug to prevent cancer metastasis that entered clinical trials; Singleron Genomics signed an exclusive global licensing agreement with Yale University for microfluidic single-cell processing patents, aiming to apply breakthrough single-cell analysis technology to clinical testing, health management, and drug development; and XtalPi is a world-leading, computation-driven drug discovery company that has partnered with pharmaceutical giants including Pfizer and Roche.

These projects may not shine as brightly as TMT star deals, but because they address hard needs in industrial upgrading, they've become important forces driving growth in their respective sectors — and have delivered rapid business development and strong equity appreciation. Today, the tech investments in FreeS Fund I have an IRR of roughly 80%, outperforming our consumer and enterprise services portfolios.

It's worth noting that tech doesn't fail easily, because it's fundamentally about technology transfer and application — the initial value is already there. Though tech projects have longer growth cycles and more visible trajectories, they also mean long-term, steady returns.

▍Cross-disciplinary investment capability: depth and intersectionality. Any industry that looks massive today was built through cross-boundary innovation; breakthroughs mostly happen at the intersection of disciplines. Biology + data and computation, biology + electronics (automation, sensors), chips + algorithms, biology + materials, chips + consumer scenarios, consumer + data... FreeS Fund has seen many such innovative projects in the past three years, and invested in quite a few. Some examples:

- Club Factory, sometimes called "the Taobao of India," is full-stack, consumer-facing AI — consumer (supply chain) + data + AI;

- XtalPi and Bluepha, mentioned above, are also typical cross-disciplinary projects: the former is cloud computing + AI + pharmaceuticals, the latter is AI + computation + biology.

This means at FreeS Fund, it's now common for at least two specialized investment teams to jointly evaluate a project's value.

Second, different industries and technology directions all go through cycles — underlying innovation, widespread adoption, and application innovation. Take GPS: from GPS getting smaller, more accurate, and lower-power, to GPS being put into smartphones, to the emergence of DiDi and Uber — that's how it evolved across different stages. For any given direction, different investment theses and analytical frameworks are needed at different stages and cycles.

FreeS Fund's investment team is multidisciplinary by design. When innovation is cross-boundary, you need a composite team with different know-hows — from technology to application to consumer — to judge a project together. And when industries and technologies are at different stages, you need know-how from previous stages and different directions to make cross-cycle judgments. We believe this is a meaningful advantage for the fund's overall investment and target selection.

However, wanting to maintain both diversity and specialization in every direction is hard because teams need to complement each other's growth rather than constrain it. Put bluntly: you can't use TMT investment thinking to constrain pharma or chip investments. Companies grow at different speeds, need different resources, and founders have different capability profiles.

▍Research-driven, calm analysis, independent judgment. FreeS Fund encourages thinking and sharing, demands deeper industry research than others, and makes investment decisions based on calm analysis and independent judgment.

Staying calm and making independent decisions in a rapidly changing market close to money isn't easy. Honestly, we have to resist a lot of temptation. Many times we see opportunities to make money quickly, and we're certain we could profit from speculation. But after a few years, my feeling is: forcing myself, or talking myself into short-term investments is hard. What feels more comfortable is this: if it's not an opportunity I genuinely believe in for the long term, no matter how much money it could make short-term, I pass.

Over the past three years, my team and I actively passed on some hot sectors and some very famous projects. There was definitely struggle and wavering in this process. The upside is that this experience pushes us harder to make long-term judgments — looking 5 or even 10 years out. It's a conviction.

Don't go where the crowds are. As a result, FreeS Fund is arguably a firm that doesn't chase fads. If deep tech counts as a fad now, it was far from one when we decided to bet on it three years ago.

▍Embrace change, drive change, value people. Investing ultimately comes down to people. Over the past three years, our team has grown with the fund. Several colleagues have been promoted to take on greater responsibilities. Others have left to explore new directions — starting their own companies, or joining startups.

Going through these three years, in internal management and team evolution, I've personally moved from worrying about change, to accepting change, to actively driving change. Looking back, change is always happening; things always need constant iteration. Understanding that the fund and every team member are constantly evolving means accepting that people may evolve in different directions, and thus make different choices and decisions. What's more important is holding to our original intention: letting a team that has grown together continue to evolve together. Facing all change, the key isn't to worry about it, but to ensure the change is the right change, a good change.

As the fund's investment directions expanded and its advantages and resources accumulated, FreeS Fund opened a Shanghai office in early 2019 to better serve and support outstanding entrepreneurs in East China. In the past six months, we've also been fortunate to attract several partners and young talent to join.

In hardware technology and related enterprise services, FreeS Fund added a partner with over 20 years of experience in smart hardware, chips, automation, and other specialized fields, who has also served in executive roles at well-known internet and smart hardware companies. We've also attracted young Silicon Valley tech development talent with excellent educational backgrounds.

In biotech and healthcare, I'm very glad to have brought on board a partner with over 10 years of entrepreneurship and investment experience in biology-related fields, as well as young talent with strong educational backgrounds and experience in China's new drug R&D industry.

In internet and consumer, FreeS Fund was also fortunate to attract investment partners with rich industry experience and successful entrepreneurial track records, to strengthen our internet DNA.

Together with our existing team, they form FreeS Fund's 20-plus-person professional investment team. Despite different generations, geographies, and professional backgrounds, we will work together to identify outstanding projects in the three investment areas above, and serve our portfolio companies well.

On fund operations and management, I invited a work partner I had collaborated with for 5 years, and convinced him to give up an executive position and stock options at a listed company to join FreeS Fund.

Additionally, the large-project team that FreeS Fund established three years ago — responsible for late-stage project IPOs and exits, as well as fundraising for late-stage project-specific funds — has made significant progress under the leadership of existing partners, contributing substantially to the fund.

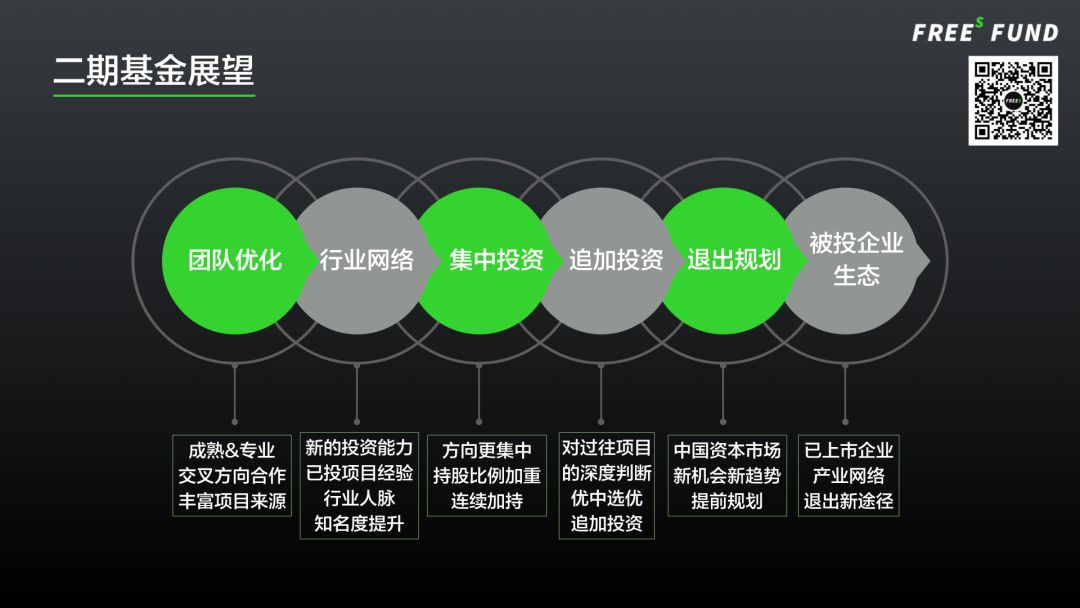

Fund II: Three Commitments, Some Changes and Reflections

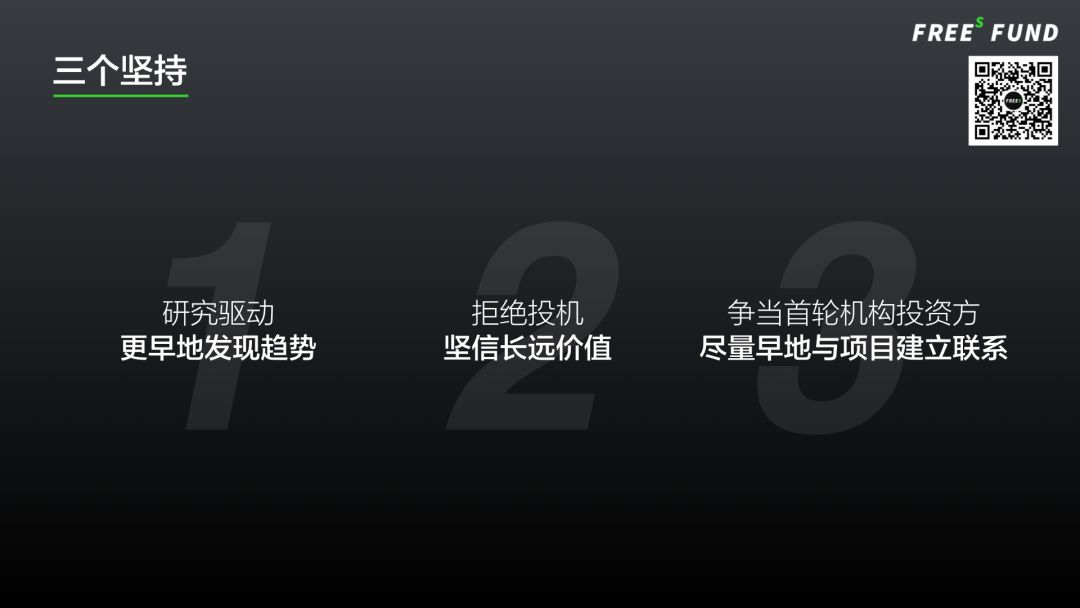

Compared to Fund I, there are three things we'll stick with. First, we remain research-driven, hoping to identify trends earlier. Second, once we've identified a trend, we firmly believe in long-term value and reject speculation. Third, we want to establish relationships with projects as early as possible, striving to be the first institutional investor in early-stage deals.

On investment direction, internet+ related projects will make up a slightly smaller proportion in Fund II, while tech and healthcare will continue to increase their share. Looking at invested projects, tech is approaching half, and healthcare has exceeded 20%.

Having gone from zero to one with Fund I, FreeS Fund has accumulated a portfolio and resources in biopharma, new energy and new materials, and semiconductors, developed the team's investment capabilities, established initial industry networks and influence, and learned lessons from portfolio companies. Therefore, in these more familiar directions, Fund II will invest with greater conviction in individual projects.

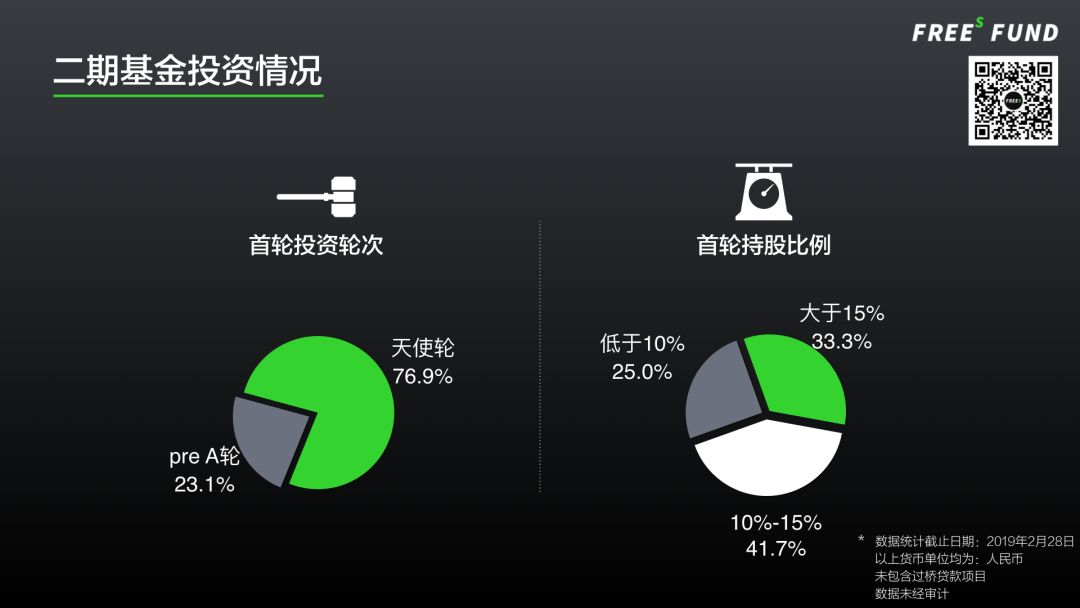

Beyond its principle of active investing, Fund II continues FreeS Fund's pattern of leading rounds as the first institutional investor at a high rate. At the same time, our ownership stake in first rounds has risen significantly — projects where we hold more than 10% now account for three-quarters of our portfolio, and those where we hold more than 15% represent roughly one-third.

Next, I'll share our thinking on five major sectors: industrial internet, finance, consumer, healthcare and education, and technology.

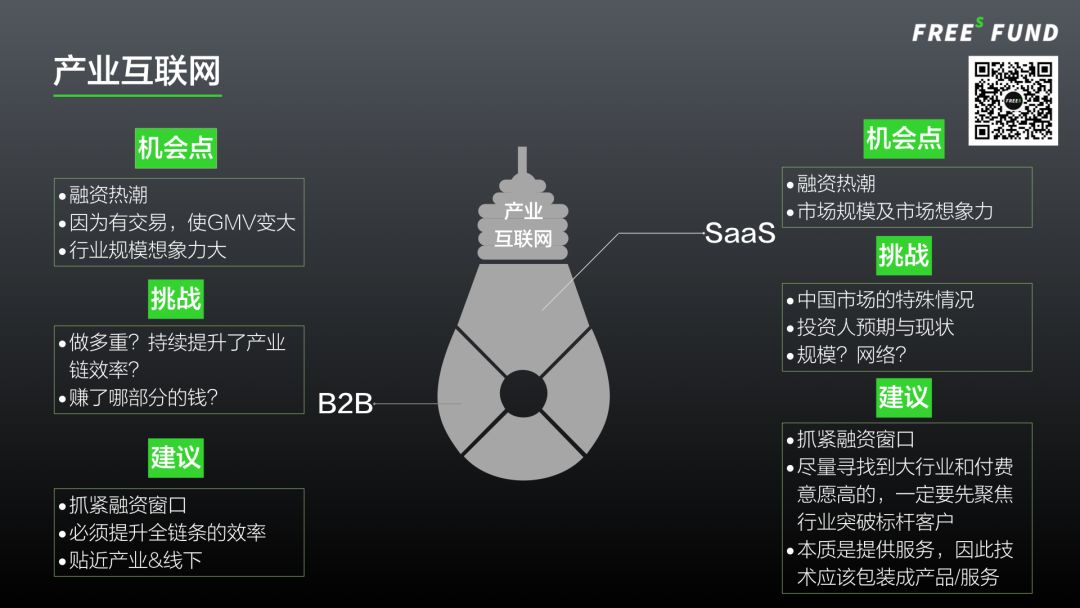

Enterprise services is seeing an investment boom — that's obvious to everyone. I want to focus on the challenges. The US went through three waves in SaaS and enterprise services: software-ization, cloud-ization, and then intelligence and big data built on top of cloud. These three waves produced numerous public companies and industry giants. That brought many benefits: cultivating talent, educating the market, and providing more exit channels.

China's enterprise services market, however, hasn't fully experienced any of these three waves. Whether in resource and talent accumulation or exit channels, we're far behind. For enterprise buyers, they're being exposed to software-ization, intelligence, and mobile-ization all at once, and choosing among similar products is difficult. This means entrepreneurs need to be steady and methodical, but also possess exceptional sales capabilities — a "grind it out" mentality is probably necessary.

Three pieces of advice: seize the funding window; try to find industries with large market size and high willingness to pay, and work hard to land benchmark clients; rather than explaining why your technology is superior, focus on delivering the service itself — what problems the technology actually solves.

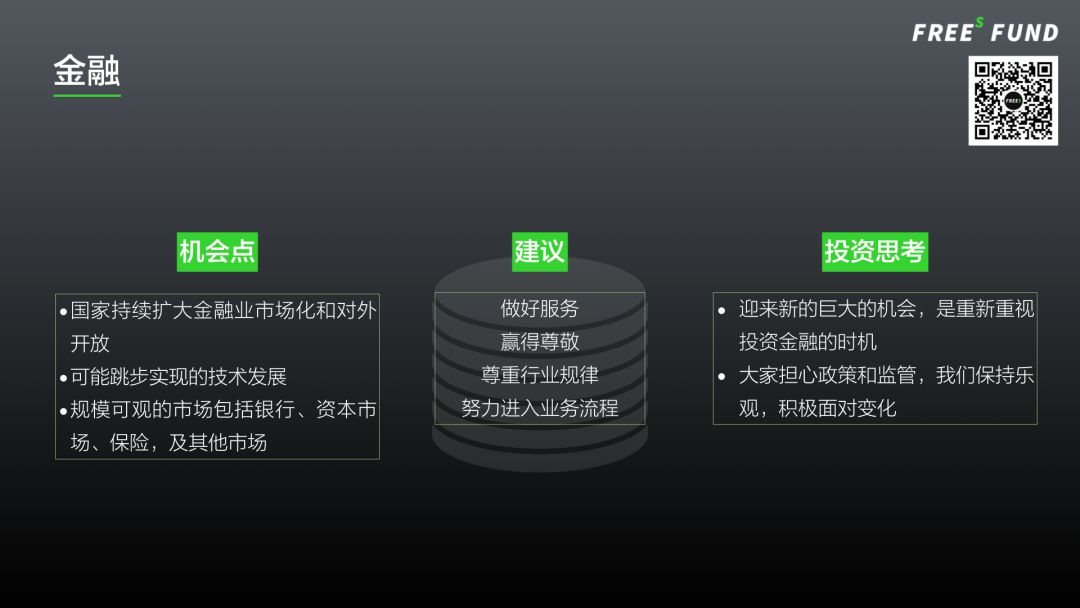

Now is a good time to refocus on financial investments. The financial industry has enormous scale and momentum, and it was also the industry that produced the most listed companies over the past five years (2013 to 2018) — bar none. 360 DigiTech, an early FreeS Fund investment, listed on NASDAQ on December 14, 2018.

2018 saw multiple regulatory policies in finance, but we believe that rather than worrying about regulation and constraints, it's better to stay optimistic and face changes proactively. In a regulatory cycle, from the perspective of policy direction and survival pressure, China's licensed financial institutions — including banks, capital markets, and insurance — are all facing asset structure adjustments. These correspond to tens of trillions and even hundreds of trillions in assets and related markets, representing long-term opportunities spanning more than three to five years. Helping these large institutions with their structural transformation is an excellent entry point. The key is respecting industry rules, embedding in business processes, and earning respect.

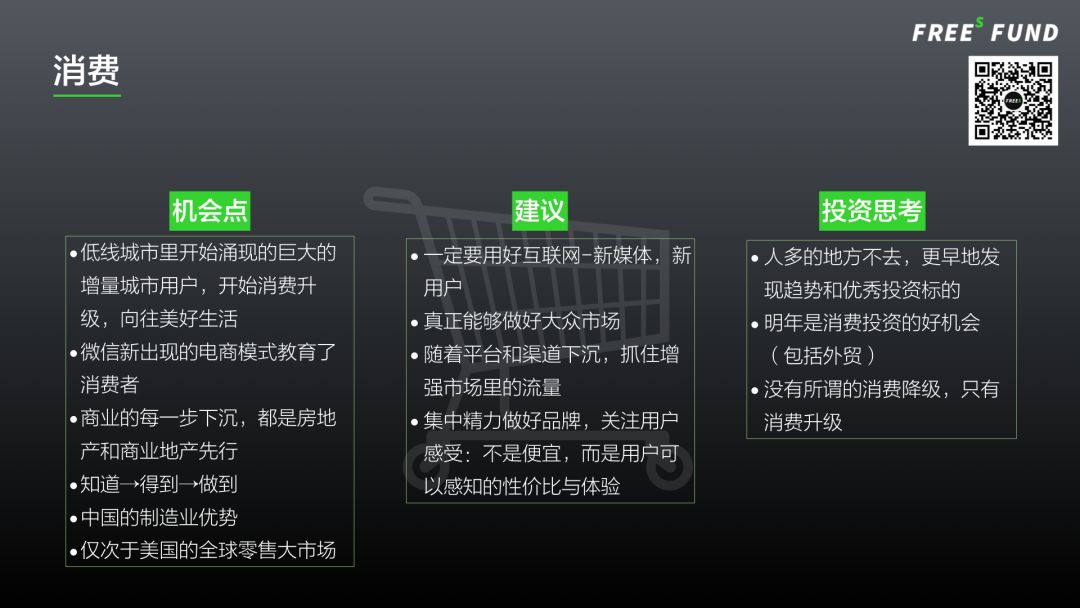

There's only upgrading, no downgrading; consumption down-market is the biggest opportunity. The gap between supply and demand usually means opportunity. Aspiring to a better life, seeing interesting things that represent that better life, but frustrated by expensive and not necessarily good offline options, not knowing who to buy from — so you "buy cheap but not necessarily bad" (this explains WeChat official accounts turning to e-commerce, social commerce, influencer commerce, and Moments commerce). Then to "buy what everyone knows but isn't expensive" (formerly VIP.com and Jumei International, now second-hand luxury going down-market and known brands' off-price and inventory sales). Then to "buy what you know is good and offers great value, though not necessarily the cheapest" (brands and channels going down-market together). This has been China's sequential process of activating tier-1/2, tier-2/3/4, and lower-tier city markets, with each stage corresponding to roughly 100 million, 200 million, and 500 million urban residents respectively.

So this is the activation with the most new users ever, and the biggest market opportunity for brand coverage and down-market expansion. Brands that recognize this trend and can execute the right down-market strategy will see tremendous year-over-year growth. But the hardest questions are: what makes a good brand? How do you go down-market? How do you adjust products? And conversely, will any brands start from lower-tier cities and break upward?

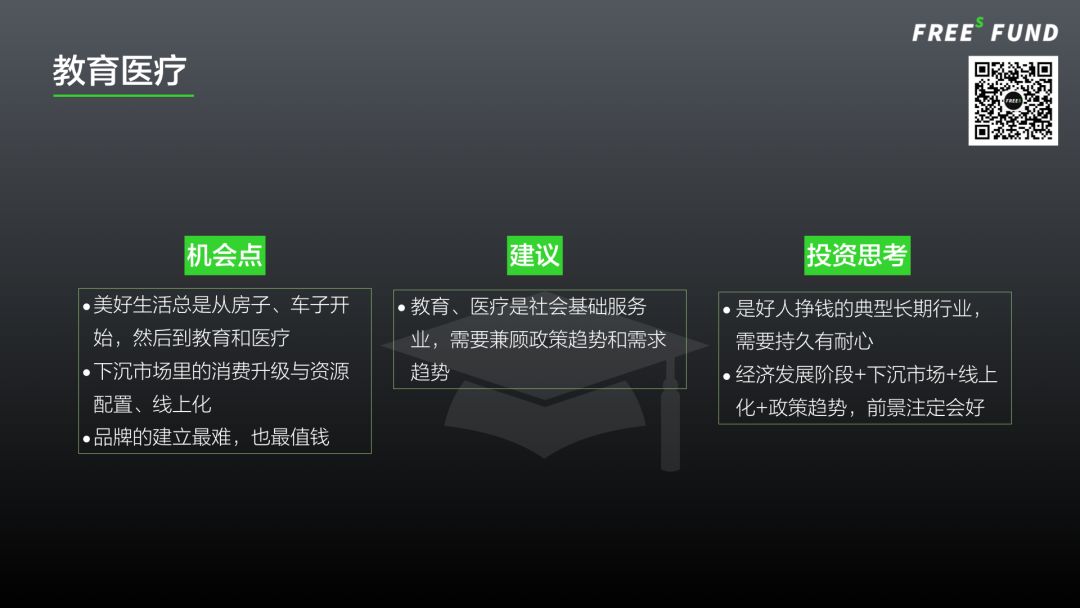

Education and healthcare need to balance idealism with commerce. People's aspirations for a better life mostly start with housing, then cars, then other physical goods representing that better life. This holds true across tier-1 through tier-7 cities. Similarly, as people age, individual and household spending shifts to three major areas: finance, education, and healthcare. I've already analyzed finance above. Like finance, education and healthcare are foundational social services that need both social and commercial value. So they require longer accumulation periods and a better balance between idealism and commerce. The upside is that when they truly become brands, their moats are very high.

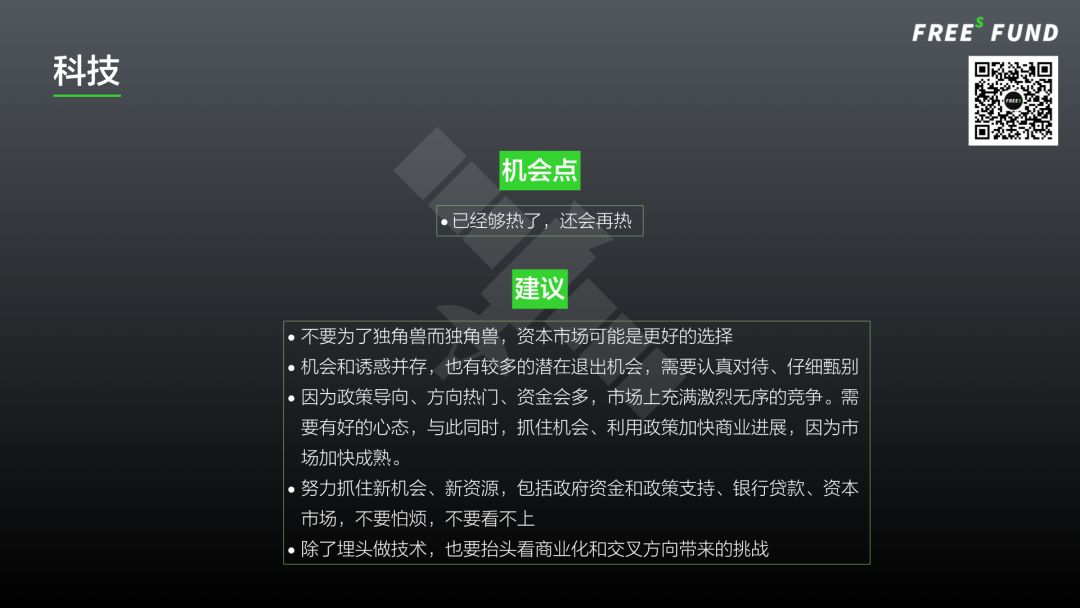

Technology is already hot enough, and with the STAR Market, it will get even hotter — you need the right mindset. FreeS Fund has been investing in deep tech since its founding; technology projects already account for 40% of our portfolio. The STAR Market's rise will catalyze an investment boom in tech. In this prosperity, CEOs will face many temptations: partnerships, investments, even M&A. I have two suggestions: first, take the STAR Market seriously — it's a brand-new capital market opportunity that China is offering right now for special economic policy reasons. Second, I don't advocate inflating valuations too high in the primary market, only to find you can't realize that value. Respecting industry development patterns and your own growth trajectory is the best choice.

Entrepreneurship is hard — maintain "heroism"

Finally, I want to say that capital is not a cold money-making machine, and neither is business. FreeS Fund has invested in many companies that combine social and commercial value — beyond commercial value, they also strive to create social value and make society better. Let me share a few typical cases.

Beyond commercial value, also striving to create social value.

(Swipe left/right to see more)

Over the past five years, Onion Math's Onion Teaching Assistant Initiative has cumulatively provided teaching support to over 40,000 rural teachers at more than 3,000 rural schools across 22 provinces nationwide.

NextVPU's "Angel Eye" glasses for the visually impaired have held 387 global experience events across 283 cities worldwide, with cumulative participants exceeding 45,081. The total kilometers walked by users traveling with Angel Eye could circle the Earth 52 times.

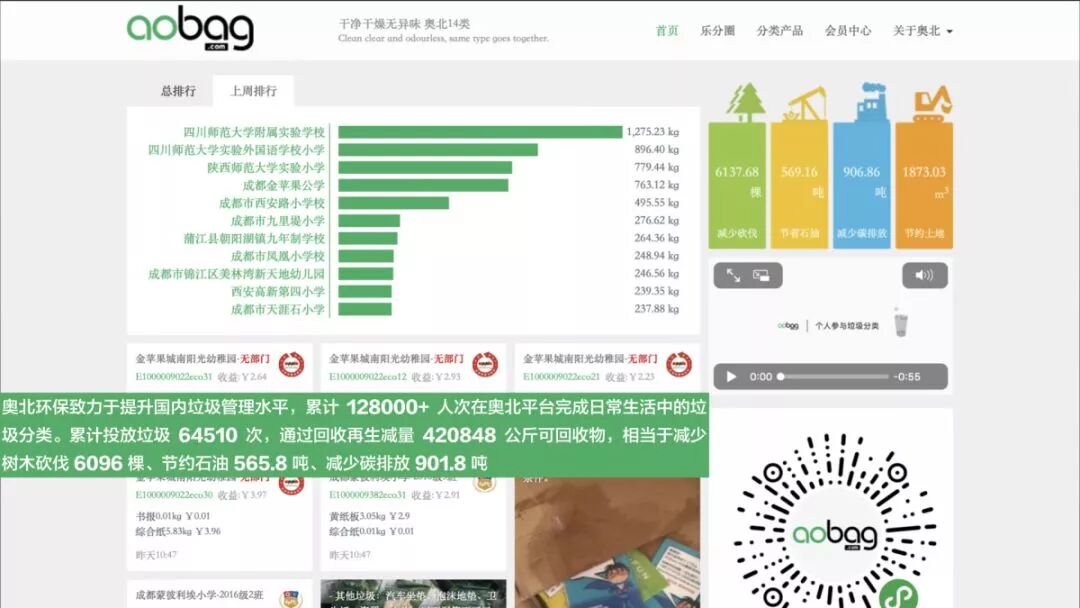

In waste recycling, Aobag is dedicated to improving China's waste management. To date, over 128,000 people have completed daily waste sorting on the Aobag platform, with 64,510 waste drop-offs, recycling 420,848 kg of recyclable materials — equivalent to saving 6,096 trees, conserving 565.8 tons of petroleum, and reducing carbon emissions by 901.8 tons.

The tumor big data platform Haalthy has cumulatively served over 30,000 lung cancer patients nationwide, with its collaborative projects accelerating the clinical development of lung cancer-related new drugs by over 20% annually.

There are many more examples like these. Starting a company is already hard enough, especially in the volatile, up-and-down year of 2018. In an environment widely acknowledged as difficult, our founders still hold onto their ideals, still want to create value, and still insist on doing the right thing and doing it better. We are honored to walk alongside them.

To close, I'll borrow from Romain Rolland: "There is only one heroism in the world: to see the world as it is and to love it."

(Disclaimer: Funds carry certain investment risks and are suitable for qualified investors with strong risk identification, assessment, and tolerance capabilities. Risks in venture capital fund management and operation include: legal and policy risks, force majeure risks, technical risks, operational risks, market risks, risks related to investment targets and projects, risks related to guarantee measures and credit, asset loss risks, fund operation risks, fundraising failure risks, investment target risks, tax risks, liquidity risks, distribution timing risks, early termination risks, management risks, equity transfer risks, fund custody risks, business operation risks, and other risks.)

▲ We Want You! FreeS Fund 2019 Spring North America Roadshow

▲ FreeS Fund Is Hiring Investors | Do What's Right, Not What's Easy

▲ Li Feng Column | A 2 Trillion Market and 10 Trillion in Output Value: Why We're Bullish on China's Chips?

▲ Li Feng × Li Xiang: Strip Away the Emotion — What Does China Look Like in 2019?

▲ Be Long-Term Greedy, Be a True Hero | FreeS Fund 2019 CEO Annual Meeting

▲ Tang Ning × Li Feng: Truly Great Companies Are Bound to Be Controversial | FreeS Fund 2019 CEO Annual Meeting