Panning for Gold in the Light: Where AI Goes Next, Through the Eyes of a Tech Investor

Stand in the light, and stand there with more founders.

Lately, "optics" has become the most crowded buzzword in the secondary market.

Optical modules, CPO (Co-Packaged Optics), thin-film lithium niobate, all-optical switches — they've all taken turns trending, sending a batch of previously obscure companies soaring on heavy trading volume. A joke making the rounds: you want to stand in the light, not have the light just standing there.

This isn't an A-share exclusive narrative. In April 2026, Lightelligence listed on the Hong Kong Stock Exchange, becoming the "world's first AI optical computing IPO." And at this year's COMPUTEX, Jensen Huang shared the stage with Marvell's CEO, clearly pointing to "connectivity" as the next decisive battleground for AI infrastructure — the very domain where optics operates. He called Marvell "the next trillion-dollar company" on stage, a single sentence that ignited the entire optical communications sector.

As an early-stage investment firm that's been deploying in optics for years, our read is this: optics isn't a "universal cure" for AI, but as large models push compute, power consumption, and real-time performance to their limits simultaneously, optics has become increasingly difficult to bypass.

In this industry research report, we try to address a few questions:

- In optical communications, what's real demand and what's just concept?

- How far away is optical computing, really?

- And in this wave of opportunity, where do Chinese companies stand?

Interactive giveaway:

When do you think optical computing will become reality? Share your thoughts in the comments. By 17:00 on July 16, 2026, the two most thoughtful commenters will each receive a book recommended by Feng Shu.

We continue to track technological developments in optics. If you're a founder or practitioner in this space, feel free to reach out to the author Yang Yongcheng at yangyongcheng@freesvc.com.

/ 01 /

Putting the Optics Story on One Map: From Materials and Chips to Communications and Computing

The optics chain is long, with many technical branches. Materials, chips, devices, modules, communications, interconnects, and computing nest within one another, and several concepts are often conflated. Before diving into this report, we need to place them back onto the same map.

"Optics" chain roadmap.

If you compressed the entire chain into one sentence, it would roughly be: first create the light, then write information onto it, transmit it between different devices, and finally receive and restore it; one step further, you directly use light to perform computation.

Following this chain downstream, the furthest upstream is materials and light sources. Lasers generate light; materials like silicon, indium phosphide, and thin-film lithium niobate respectively guide, emit, or modulate light, affecting device speed, loss, and integration approach. Below that are optical chips and devices, including modulators, detectors, wavelength-division multiplexers, optical phased arrays, etc. — respectively responsible for loading signals onto light, receiving light, combining or splitting different wavelengths, and controlling light direction.

Optical devices like lasers, modulators, and detectors, packaged together with electrical chips like drivers and DSPs and their interfaces, constitute optical modules. They connect host equipment to optical fiber, handling the conversion between electrical and optical signals. In other words, optical modules aren't a separate technical path — they're the core "interface" in optical communication systems.

Optical communications refers to a larger system: using light to transmit information. In the past, light was already widely used for transoceanic, metropolitan, base station backhaul, and inter-data-center communications; in the AI era, it has moved further into servers, GPUs, and even between chips on the same board. These shorter-distance, higher-density applications are typically called optical interconnects. Optical modules, CPO, and LPO address how light enters devices and gets closer to chips; all-optical switches are responsible for directly switching optical paths in the network.

Optical computing takes one more step forward. Optical communications solves how to move data faster; optical computing asks whether we can have light do the "computing" itself. The former still serves information transmission; the latter uses physical properties of light like propagation, interference, and diffraction to perform operations. They share some underlying materials, chips, and manufacturing capabilities, but face different problems and are at different industrial stages.

The various "optics" concepts in the market today can basically all be understood by placing them back on this chain.

/ 02 /

AI Isn't Running Out of Compute — It's Hitting a Traffic Jam

Most people assume AI's bottleneck is compute, that GPUs (Graphics Processing Units) aren't enough. But what hit the ceiling first wasn't "compute" — it was "connect."

I. The Memory Wall and PCB (Printed Circuit Board) Physical Limits

Think of each GPU as a factory. Training large models is about continuous movement and coordination among tens of thousands of factories. What actually stalls the production line usually isn't any single factory's capacity — it's the road between factories. The first wall is the memory wall.

To alleviate it, the industry developed HBM (High Bandwidth Memory), stacking memory layers like a sandwich — effectively spreading a line's thickness into a plane, with capacity jumping accordingly. But circuit boards themselves have limits: today's AI server boards are already stacked to roughly several dozen layers, while phones manage only six to eight, nearing the ceiling. Even the "electronic cloth" used in these laminated boards has been hyped into a hot theme in the secondary market.

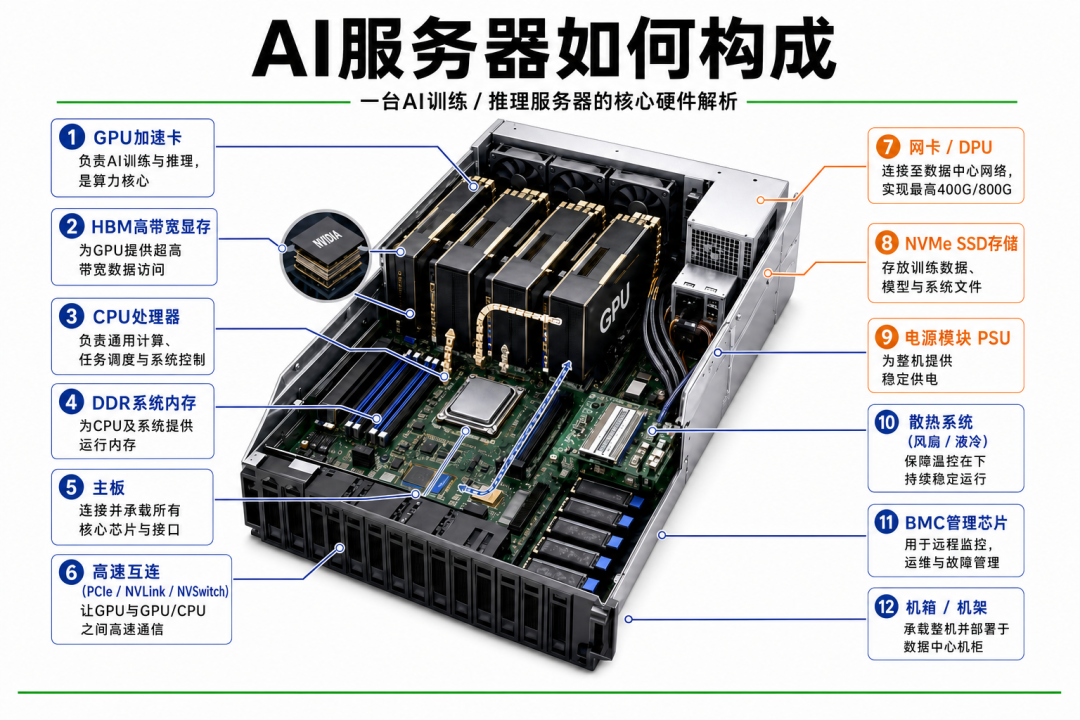

Core hardware composition of AI training and inference servers. GPUs, HBM, CPUs, and DDR handle computation and data access; PCIe, NVLink, NVSwitch, etc. manage high-speed interconnects; NICs, storage, power, cooling, and management modules together support full system operation.

II. Three Layers of Interconnect Simultaneously Under Pressure

More tricky: this isn't one road congested — it's three layers of roads simultaneously gridlocked.

Interconnect between servers, industry-called Scale-out;

Interconnect within one server, between multiple GPUs, called Scale-up;

And further in, interconnect between chips on the same board, called Scale-in.

At all three layers, electrical approaches are increasingly struggling.

A telling comparison: copper cables in boards typically only stably transmit about three centimeters, and within a chassis merely several meters, while optical fiber remains composed at a hundred meters or even several kilometers; on power consumption, one copper interconnect takes roughly fifteen watts, while an optical interconnect takes about five.

So rather than optics suddenly becoming hot, it's the electrical path that first approached its own physical ceiling.

III. Why NVIDIA Got "Impatient"

NVIDIA's recent moves illustrate the point well: it has successively invested in industry chain companies like Marvell, Lumentum, Coherent, and partnered with Corning. NVIDIA and other AI compute giants have proposed technical paths including CPO, MicroLED (Micro Light-Emitting Diode), micro-ring modulators, OCS (Optical Circuit Switch). A giant that originally only did compute is now personally directing optical communications for a simple reason: its demand is there, and existing suppliers' pace can't keep up.

When the chain leader gets impatient, the entire industry is forcibly ignited. The demand is real, but technical paths haven't converged, and the mud-slinging is equally real — not lacking those coming to "ride the optics wave."

Some choose the opposite direction. Rather than painstakingly connecting thousands of chips, make an entire wafer into one giant chip, letting most computation happen internally to bypass the interconnect hurdle. The representative doing this is Cerebras in the United States. But this is a purely electrical chip path, with non-trivial costs in heat dissipation and yield, ultimately unable to bypass other physical limits.

Yet one thing almost no one doubts: everyone has identified the same exit — optics.

/ 03 /

Why Optics, Specifically?

Why optics can take this baton starts with a basic physics fact.

Photons have no mass, so they're inherently superior to electrons in speed, power consumption, and signal-to-noise ratio. The simplest proof: submarine cables can send signals across thousands of kilometers to the other shore — something electricity can't do.

This is also our underlying conviction for betting on optics for ten years without wavering: in many links of communications and computing, light's physical endowment is simply better than electricity's.

In fact, optical communications is already everywhere — we just don't usually feel it. Transoceanic submarine cables, metropolitan area networks, backhaul between base stations of various generations, and even interconnections between servers in data centers — fundamentally, all run on optical fiber. But AI has introduced new demands this round: inside servers, between chips — these short-distance scenarios where electricity used to suffice now need to switch to light.

So how is the signal loaded onto light? In essence, two paths: one is having the light source carry the signal itself; the other is having the light source shine steadily, then adding a "modulator" behind it to alter it. The latter path uses silicon photonics, the current mainstay, but single-wave rates basically top out at 200G. To go higher, you need a new material called thin-film lithium niobate, an almost unavoidable option for hitting 1.6T, 3.2T high rates. On this line, Chinese teams have moved relatively ahead, and we've invested in one company.

But there's another layer of uncertainty in optics' incremental role in AI infrastructure, and it comes from AI itself. Right now, the biggest demand side for compute is training, with companies stacking GPU clusters; but the next step, inference — how big and how to build dedicated data centers for it — no one can say for certain. If intelligent agents and on-device assistants really take off, with increasingly stringent low-latency requirements, that would push optics demand even higher; but if inference mainly reuses existing training clusters, the increment would be much smaller. This uncertainty is an important reason why optical communications is "hot yet chaotic."

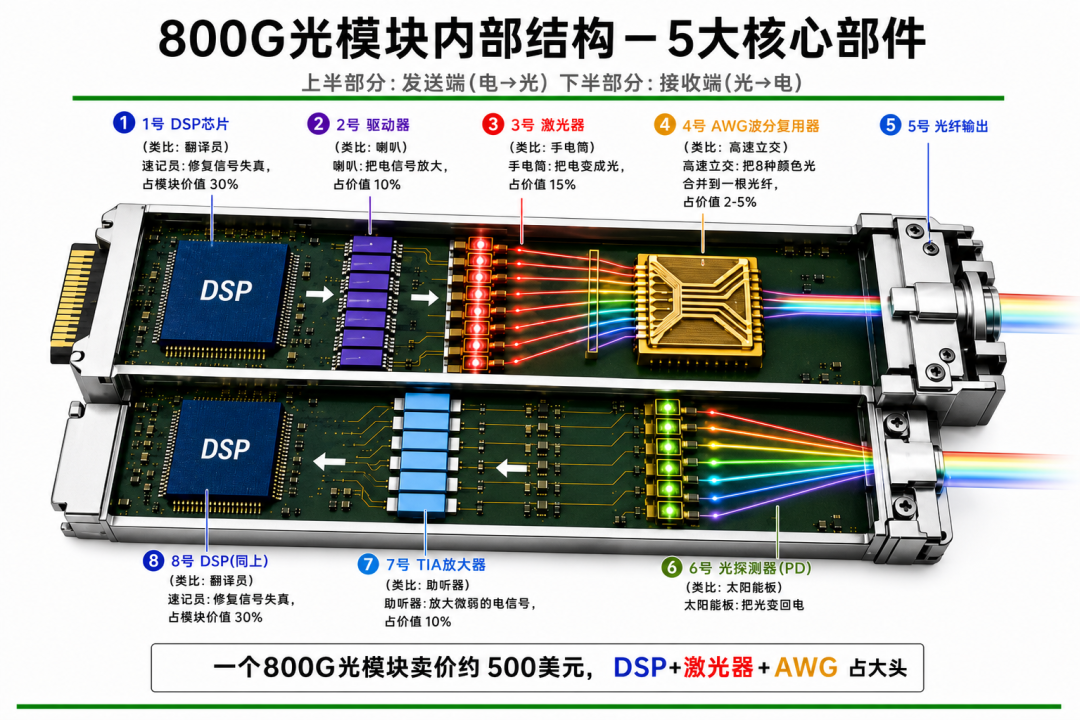

There's also an unavoidable hard bone in optical modules, called DSP (Digital Signal Processor), equivalent to the "CPU" of optical communications, specifically dedicated to straightening out signals that got distorted or blurred — without it, high-speed signals are simply unrecognizable. The problem is this chip is both expensive and power-hungry, accounting for roughly one-third of optical module cost and nearly half its power consumption. Delivery lead times for high-end DSPs have stretched to nearly a year, and they're basically held by two American companies: Marvell and Broadcom.

800G optical module internal structure schematic. The transmit and receive ends respectively complete electrical-to-optical and optical-to-electrical conversion, with main components including DSP, driver, laser, AWG wavelength-division multiplexer, photodetector, and TIA amplifier, etc.

To be frank: we aren't being choked by anyone's executive order — our own technology simply hasn't reached that level yet. It's too complex, a chip with very high technical complexity and difficulty; we still need some time to catch up on high-end optical DSPs.

The broad direction of optics is doubted by almost no one; but which specific path to take, who succeeds first — far from consensus.

So in this still-unclear landscape, where exactly does China stand?

/ 04 /

On This Board, China Stands on the "Creation" Side for the First Time

I've been asked before: Is optical chip yet another "domestic substitution" direction?

My answer: no. It's different from the story we're familiar with. Back when we looked at GPUs, the essence was domestic substitution — NVIDIA had already broken out overseas, and we were chasing from behind; but today, looking at the new directions in optics, such as CPO, LPO (Linear-drive Pluggable Optics), thin-film lithium niobate, OPA (Optical Phased Array), etc., China and overseas started from the same starting line simultaneously. From the current position, we're not at a disadvantage this time — some links are even further ahead, like thin-film lithium niobate chips. Of course, in the technical areas where we lead, there often isn't a clear "anchor," meaning no overseas benchmark to reference. Many peers might see this as uncertainty and risk, but in my view, this is precisely a good thing — because it means you're the first.

Being the first to eat the crab means you have the chance to grab the biggest, best crab.

Currently in the AI optical interconnect track, there are two types of players. One is the several optical module leaders that have risen most sharply in the secondary market — they're mainly producing traditional optical modules already in mass production, with demand primarily coming from NVIDIA's data center builds, essentially continuing to grow within an existing large market. In this traditional pluggable optical module market, the major-player landscape is already relatively stable, with little opportunity for new entrants like startups; but in new directions, startups and giants basically stand at the same starting line, and because they're more focused and faster-decisioning, they actually have a window period.

The optics board is large, and over the years we've deployed along technical paths one by one, investing in relevant entrepreneurial teams for each key route.

FreeS Fund's investment layout in optics.

First, the most closely watched: optical computing. We first invested in Lightelligence in 2017; it listed on the Hong Kong Stock Exchange this April, taking a photonic-electronic hybrid route — using light to accelerate the matrix multiplication that weighs heaviest in AI, with remaining operations handled by electrical chips. Another company we invested in in 2022, LightStandard, takes a different path, using silicon photonics plus phase-change materials to combine storage and computation into a single unit for "compute-in-memory," with the benefit of smaller unit size and lower power consumption. For the same thing, we've bet on two different routes.

The second line is thin-film lithium niobate. As mentioned earlier, going toward 1.6T, 3.2T rates, this material is almost unavoidable. Whether upstream wafers or chip design, Chinese teams have been ahead these past few years; Anpai Xinyan, which we invested in in 2021, is one of them.

The third line is OPA, optical phased array. Its principle is somewhat like the flat-panel antenna in 5G, using phase to control light direction without relying on mechanical rotation. This has two major applications: one is all-optical switch OCS, the other is solid-state LiDAR, with the latter beginning to ship in vehicles this year. There aren't many teams globally that can pull this off; Lice Technology, which we invested in in 2019, is one of them.

Beyond these three, in silicon photonics we invested in Luowei Technology, which takes the FMCW (Frequency-Modulated Continuous Wave) route; in optical modules we invested in AfaLight; and in metalenses we invested in Xuanxiang Technology. Connecting these together, from optical interconnects to optical computing, from materials to devices, we have positions on almost every key route in optics.

Of course, we're not at the forefront of every line. Like that hard bone DSP — as mentioned earlier, our technology hasn't reached that level yet. In terms of category completeness, we're probably the most complete; but to say every category is top-tier, definitely not yet — that takes time. But precisely because the direction is right and the layout is complete, I'm confident in the final outcome.

And in this entire layout map, what excites us most is still the diamond in the crown. What's truly new about optical computing, and why are we willing to bet two routes on its future?

Betting on a Further Future

Optical communications uses light to "deliver" data faster; optical computing goes one step further — it simply hands the "computing" itself over to light.

Today's AI computing relies on thousands of electrical chips multiplying and adding around the clock, consuming power and generating heat; while light moves fast and consumes almost no energy. If light could shoulder those most repetitive, most burdensome computations in AI, theoretically it would be both faster and more efficient. So optical computing is one step beyond optical communications — its ceiling is higher, but also further and harder.

Today most so-called optical computing has actually only taken a small step: using light to replace the multiply-accumulate operator, swapping in light for the most core step, while the overall computational topology and architecture remain identical to electrical chips. The true next step is using light's physical properties themselves to complete an entire computation. This sounds mystical, but there's actually a simple example.

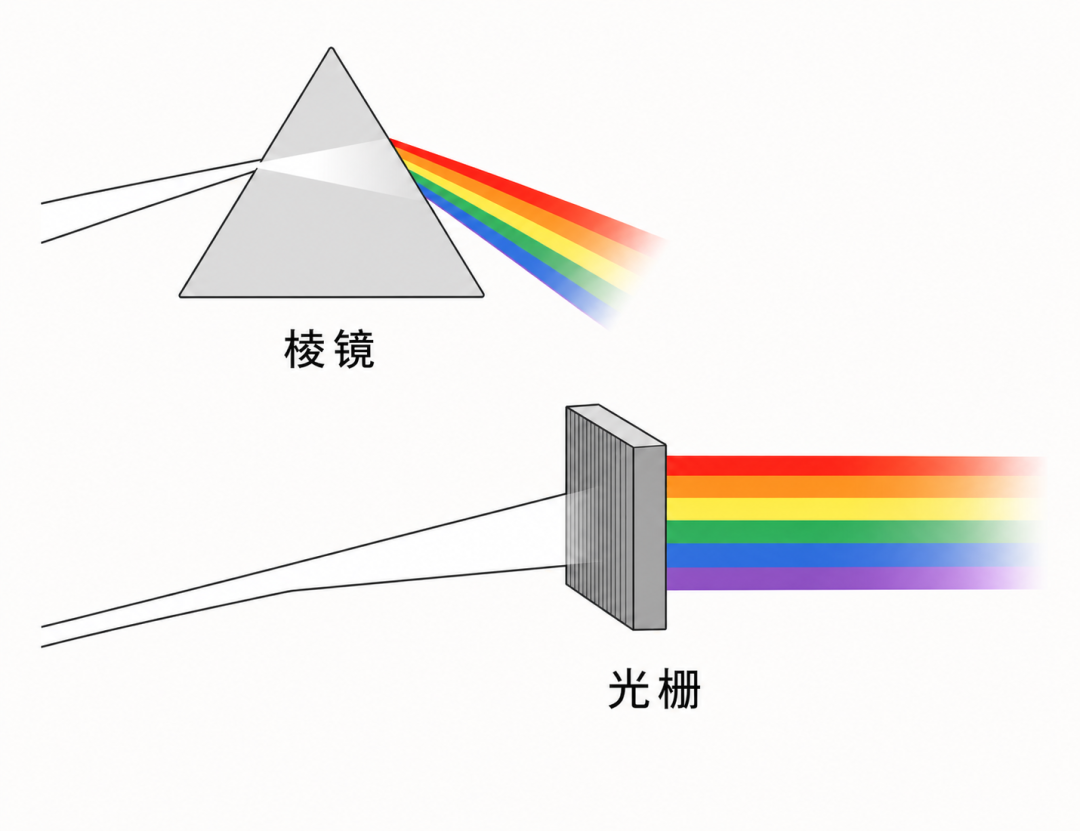

Any waveform can be decomposed into a superposition of sine waves at different frequencies — that's the Fourier transform, algorithmically a matrix operation; while a beam of white light passing through a prism separating into various colors, this utterly ordinary phenomenon, is essentially the prism doing that calculation for you, and you read the result at the exit. Prisms, gratings, metalenses and similar devices are "physical computers" that consume no power.

White light, after passing through a prism or grating, is decomposed into light of different frequencies. Optical devices use their own physical structure to directly complete frequency decomposition; input the optical signal, and read the result at the exit.

But this path is still early, with clear shortcomings. Implementing computation directly through light's physical structure means model parameters are固化 in the device — unchangeable after training, like a photo that's developed and fixed. So it's only good at fixed, unchanging tasks, like a certain type of image recognition; it can't swap models on demand like general-purpose GPUs, making it more suitable for edge devices and fixed-scenario small tasks. Expecting optical computing to replace the electrical compute market dominated by NVIDIA GPUs today is still premature.

So why did we dare to bet early? Because for this kind of hard tech, the direction is almost never wrong — the suspense is only who, and when, makes it work. Like silicon carbide: its first principles were established very early, but when it was made, downstream hadn't yet emerged, no one used it; early companies had to survive on other products until new energy vehicles' high-voltage platforms emerged, demand arrived, and then they took off.

Optics is somewhat more fortunate than silicon carbide, because the AI application scenario is visibly right there.

Companies that grind forward bit by bit on technology have a very distinctive valuation curve shape. For many years early on, it stays flat at very low levels, often with valuations under two billion; but once first principles are validated by the market and single-product sales exceed one hundred million, there's only a very short one or two round window in between, and valuation shoots straight past ten billion. After that, the question isn't whether it's expensive — it's that you simply can't get allocation at all.

Connecting the entire map above, what we want to do is actually quite clear. Grounded in the present, establishing positions in optical communications, optical interconnects, optical chips — areas already happening; while also looking to the future, pre-positioning for further directions like optical computing.

The era of optics has just begun. We want to stand in the light, together with more founders.

Illustrations in this article were AI-assisted, using tool: ChatGPT