Slow Is Fast: Why Insurtech Is a Bet Worth Making | FreeS Fund Interview

How did assessing a car's driving risk become a business?

When the hype fades, truly competitive products are more likely to surface. At the turn of this century, China's banking industry completed its large-scale data consolidation and launched online banking — marking the financial sector's transition from electronification to informatization. Internet finance, which began with third-party payments, entered the digitalization phase around 2015. In the years since, fintech has continued to evolve, navigating tighter and looser regulatory cycles, gradually shedding its glamour and arriving at a moment that truly tests the core of its products.

Fintech and insurtech products aren't distant from our daily lives: Why is auto insurance for new energy vehicles more expensive than for gas-powered cars? If you use your private car to drive for DiDi and get into an accident, will the insurance company pay out? How do insurers set prices? When shopping on e-commerce platforms, what determines the cost of return shipping insurance? These questions all touch on fintech.

What new changes are happening in the insurtech space, and what entrepreneurial opportunities exist? Zhao Xin, founder of Qijing Technology, has over 20 years of experience in finance and insurance across China and the US. She is a certified underwriter, financial risk manager, and associate of the Society of Actuaries. After earning her master's in mathematics from the University of Wisconsin, she joined Milliman, an international actuarial and consulting firm, as an actuarial consultant. She went on to work at Fortune 500 companies including Liberty Mutual and USAA. Upon returning to China, Zhao joined Deloitte Consulting and, as an industry expert for the China Banking and Insurance Regulatory Commission, actively contributed to planning and calculations related to China's auto insurance market rate reform.

To productize technical solutions for the insurance sector and apply them more effectively across the industry, Zhao founded Qijing Technology in 2017. Starting with the auto insurance market, Qijing uses big data risk control technology to precisely distinguish individual risk differences between vehicles, filtering out insurable cars from the "bad business" that insurance companies are reluctant to cover — allowing these owners to obtain appropriate coverage at fairer prices. As its risk control system has continuously improved, Qijing has made insurance more efficient and equitable.

Pengqi Liu, Executive Director at FreeS Fund, spoke with Zhao Xin about:

- Why she decided to start a company, and what opportunities she saw

- Why she chose to enter through the auto insurance market

- What trial and error the company experienced along the way

- When people's lives become digital faster than the insurance industry, what should insurance do?

- After the Personal Information Protection Law took effect, how does the insurtech industry solve compliance issues?

- How large is the market Qijing wants to enter? Why is Qijing positioned to succeed in insurtech?

- What is the pace of insurtech market development, and what types of talent does it need?

Reader Giveaway We welcome your thoughts in the comments. Through November 17, the five most thoughtful commenters will receive a LAMY pen from Qijing Technology (orange or white packaging, shipped randomly).

/ 01 / Why Start a Company?

What Opportunities Did You See?

Pengqi Liu: From an entrepreneur's perspective, what differences have you observed between Chinese and international fintech in recent years? What innovation opportunities exist there?

Zhao Xin: Qijing's industry can be categorized as either insurance innovation or enterprise services. Abroad, whether in autonomous driving insurance, health insurance innovation, or cross-industry SaaS enterprise services, there are many highly valued startups. But in China, most directly copied models have not been particularly successful. Some attribute this to strict regulation limiting innovation, but I don't think regulation is the main factor — it's directly related to where the industry is in its development.

Before founding Qijing to empower the industry through SaaS, I had already been back in China from the US for several years, and noticed significant differences in consulting approaches. I once participated in a major consulting project delivered primarily by a US expert team. Their approach was: since you hired us for consulting, we'll give you these advanced American practices directly. But this approach completely failed — Chinese clients wanted localized technology and experience, and would not accept simply importing American practices.

On the surface this seems like an isolated case, but it's actually an inevitability stemming from different stages of enterprise development. American companies have had longer to develop mature management systems; even across different industries, internal processes are largely similar, and software needs are comparable. So enterprise technology services mainly "slice by function" — financial software, sales software, HR software, and so on.

In China, customer needs vary enormously. We're in a stage of rapid development where electronification wasn't finished before informatization arrived; internet finance had barely started before digitalization and intelligence came along. Every enterprise is urgently responding to various demands, presenting "a thousand enterprises, a thousand faces" in management processes.

For technology-enabled services to succeed, they must be rooted in specific industries and segmented scenarios, providing solutions for particular industries. Only by refining granularity can solutions be packaged into products with clear boundaries and consensus, avoiding endless customized development. This may seem counterintuitive, but we firmly believe that using big data technology to empower markets requires rooting in more vertical, more segmented domains to achieve scalable replication that meets China's market needs.

Coming back to my original motivation for founding Qijing: in implementing intelligent algorithms and solutions, I found that customized consulting solutions were difficult to reuse. Small and medium insurers had varying customization needs but couldn't afford millions or tens of millions in consulting fees. Even when they gritted their teeth and paid, they lacked sufficient manpower and expertise to execute solutions effectively over the long term, unlike large companies.

Therefore, the industry needed productized solutions — at least semi-automated ones — to truly generalize common components into tools and systems. So founding a technology company to drive industry digitalization was the natural next step.

/ 02 / Why Enter Through the Auto Insurance Market?

Pengqi Liu: There should be many directions for digitalization in insurance. Why did you choose auto insurance? Most property insurers aren't actually doing well — beyond the top few, most aren't profitable. In recent years new vehicle sales, especially traditional gas-powered cars, have slowed. Wouldn't that impact the market space?

Zhao Xin: When an insurance product is growing rapidly, grabbing channels and sales may be enough — technology empowerment is nice to have but not essential. But after markets become fully competitive, it becomes about efficiency. If you want to climb higher, digitalization may be the only path left.

We chose insurance industry digitalization as our focus and auto insurance as our entry point not because we believed it had the fastest overall growth, but because this market is particularly suitable for applying and promoting digital solutions.

Within the auto insurance sector, new energy and freight logistics are fast-growing, high-risk incremental markets, while traditional gas-powered auto insurance is a stable stock market with negative growth. This allows us to validate innovative solutions in incremental markets, then test them in stock markets to see if we're "swimming naked." If digital empowerment is done right, stock markets are large enough; if new technologies need validation, incremental markets are complex enough with high growth. The two markets validate each other, enabling horizontal replication and solid promotion of digital solutions without being misled by surface-level high growth.

Currently, auto insurance products offered by insurers are clearly mismatched with market demand. In traditional gas-powered vehicles, many insurers choose to engage in price wars and fee competition, making life difficult with poor profits. In new energy, ride-hailing, and freight logistics, some insurers lag in digitalization, lack confidence in risk assessment, and fear blind entry will lead to losses.

Therefore, when Qijing provides technology empowerment, we started with high-risk, "unwanted" commercial truck insurance. Compared to the hundreds of millions of private cars, these tens of millions of trucks are certainly a small segment. This business received little attention when private auto insurance was racing for scale. But now that everyone is competing on refinement, commercial truck insurance has grown larger, testing risk judgment accuracy and digitalization efficiency — creating an opening for Qijing's products.

/ 03 / Trial and Error in Entrepreneurship: From Comprehensive to Focused

Pengqi Liu: You mentioned replicability. Has this been solved in Qijing's current business model? Was your positioning accurate from the start, or did you gradually iterate to find it?

Zhao Xin: The replicability issue is now solved. But when the company was founded in 2017, we did take some detours. Initially, we wanted to build a comprehensive system that would digitize the entire business decision process — budgeting, pricing, even policy issuance.

But we quickly discovered the industry wasn't ready for so much decision-making to be digitized at once; the step was too large to accept. We had to first digitize the most critical and most universal link — "risk screening" — without touching other decision processes, to minimize impact on business and management workflows and smoothly enter the market.

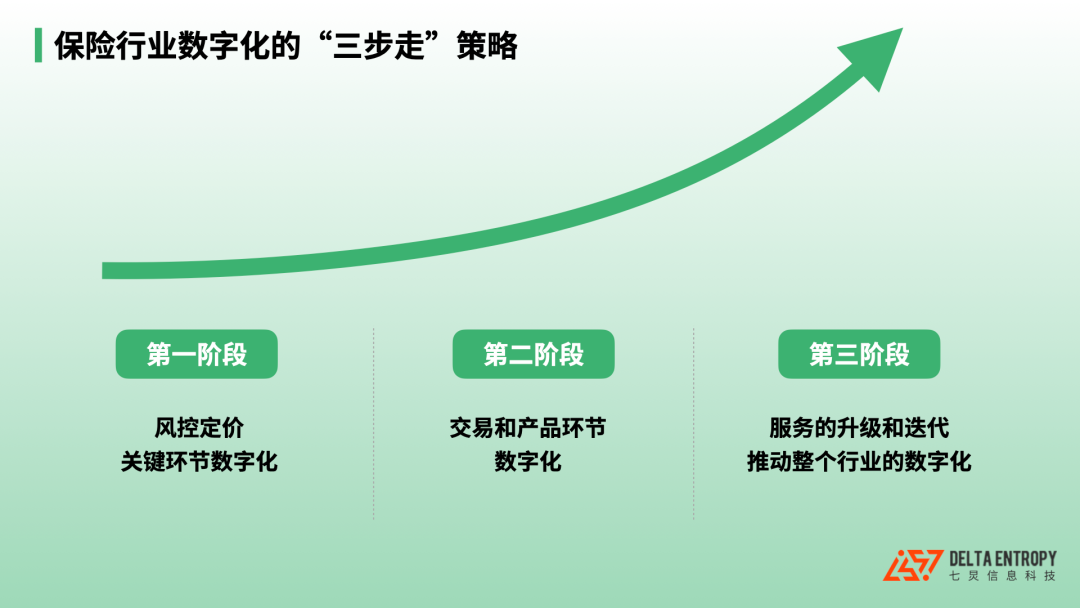

In recent years, our understanding of the underlying logic of industrial internet digital transformation has continuously deepened. Combining industry research center and national think tank white papers with industry specifics, we've mapped out a "three-step" digitalization strategy:

Phase One: Digitalization of the critical risk control and pricing link. First, without changing major business processes, help insurers digitize the most critical "pricing and risk control" link, empowering them through shared risk control services.

Phase Two: Digitalization of transaction and product links. Through Phase One results, demonstrate that innovation brings controllable risk, then use technology and data support to achieve product collaboration and facilitate insurance transactions.

Phase Three: Service upgrades and iteration, driving industry-wide digitalization. Finally, through continuous integration of technology and industry needs, iterate to meet customers' digitalization demands.

In Phase One, the goal is to provide "plug-and-play" standard risk control products for the insurance industry. Qijing launched a convenient auto insurance product where insurers simply input license plate information to receive accurate vehicle risk assessments, without affecting existing business processes. Market acceptance for this product has been strong — it has achieved tens of millions of calls, covers over 30 insurance entities, and has a customer renewal rate exceeding 90%.

In Phase Two, the focus shifts from solely addressing insurer needs to more effectively and precisely connecting customers with insurance, jointly defining insurance products.

Take IoT as an example: based on extensive data, Qijing designed an extended warranty product based on equipment IoT, achieving precise individual equipment risk cost prediction. Through insurance products, expensive used machinery transactions become smoother, no longer hindered by buyer quality concerns.

Phase Three is the ultimate stage of digital transformation, aiming to automatically implement risk identification, product matching, and transactions, connecting the full digital ecosystem.

When insurance gradually keeps pace with digitalized life, life becomes more convenient — Taobao's return shipping insurance gives us a glimpse of this future. Return shipping insurance eliminates buyers' concerns about losing shipping fees, improving transaction convenience and completion rates. Insurtech companies precisely calculate premiums through data analysis and real-time calculation, ensuring fairness and reasonableness. Insurance exists quietly yet powerfully, dramatically improving buying and selling experiences.

Of course, achieving similar integration and innovation in auto insurance, critical illness, medical, and other major insurance types still has a long way to go — and that is precisely what we're working toward.

/ 04 / When People's Lives Become Digital Faster Than Insurance, What Should Insurance Do?

Pengqi Liu: During the previous fintech boom, people mentioned insurance industry digital transformation. Now under the pandemic, its importance has been reinforced again. In your view, will insurance digitalization become a sustained transformation?

Zhao Xin: Insurance industry digitalization can be understood as technological innovation that brings progress and impact to insurance markets, companies, and services. Specifically, if you've bought a new energy vehicle in the past year, you may have noticed premiums are considerably higher than for gas-powered cars. If you have friends in logistics and freight, you may sense how difficult it is for truck drivers to buy insurance. This mainly occurs because the insurance industry as the supply side and the client demand side have become mismatched.

As the digital era arrives, people's lives have become digital faster than the insurance industry. In the past, the standards insurance used to measure a vehicle's risk level and set prices might only include brand and model, personal or commercial use, number of seats, tonnage, and similar dimensions. Simple demand meant simple insurance. But today, the same sedan model might be used for commuting or for ride-hailing. The same small truck might haul flour for its owner's bakery or take freight platform orders for moving services all day without stopping. This creates enormous challenges for insurance risk assessment.

What Qijing Technology aims to do is solve the problem of how insurance keeps pace with complex and diverse customer needs. We digitize vehicle usage scenarios, supplementing risk assessment with actual driving information such as mileage, area, time, routes, violations, overloading, fatigue driving, and more — enabling more accurate vehicle risk assessment, better meeting users' protection needs, and making insurance fairer and more effective.

/ 05 /

After the Personal Information Protection Law Took Effect,

How to Solve Compliance Issues?

Pengqi Liu: Qijing Technology masters more dimensional data, which also means greater responsibility for data privacy. How does the team address compliance?

Zhao Xin: The Personal Information Protection Law means stricter requirements for big data applications. But for us, which already followed data privacy requirements, compliance isn't difficult. Breaking down the legal provisions, compliance requires three aspects: data sources are compliant; storage and transmission links are secure; data use has clear authorization. These three aspects were already principles that insurance, as a strictly regulated industry, needed to follow.

Additionally, Qijing's core goal is relative prediction and judgment of individual risk compared to other risks. We focus on whether one vehicle's driving risk is relatively higher or lower than others, assessing relative comparisons like long-term driving time, violation frequency, and so on. Specific sensitive information like the owner's ID number, home address, phone number, or even their exact location at a specific time — we don't use these.

/ 06 /

How Large Is the Future Market?

Why Can Qijing Succeed at This?

Pengqi Liu: How large is the market Qijing is entering? How high is the ceiling?

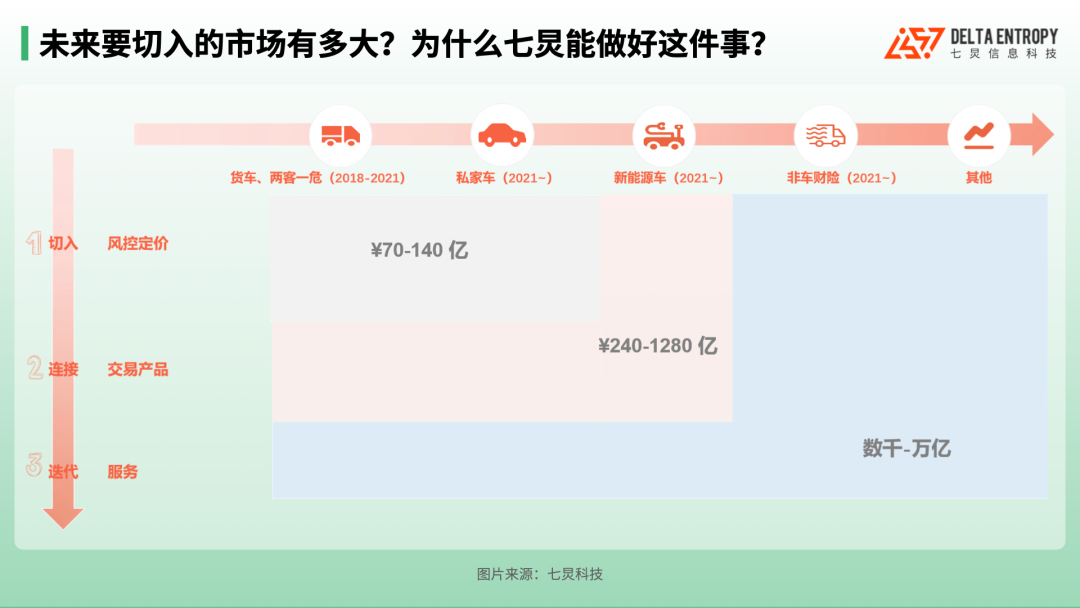

Zhao Xin: From a vertical business perspective, Qijing will start with risk control, then move to products, then services. From a horizontal product perspective, we'll start with highest-risk commercial trucks, then new energy vehicles, then other non-auto insurance products.

Based on our calculations, as we gradually expand from the upper left to lower right of this map, we'll progressively penetrate markets of hundreds of millions, billions, tens of billions, and hundreds of billions. There's still a long road ahead; we won't be overly optimistic — validation cycles will be relatively long.

Pengqi Liu: How do we extend from the current risk control market of tens of billions to a future market of hundreds of billions? On one hand, is this underlying logic sound? On the other hand, why Qijing Technology specifically?

Zhao Xin: First, the underlying logic: insurance industry digitalization follows the same approach as other industries' digitalization — starting with the most critical link's digitalization, cutting into transactions and connecting multiple links, continuing to iterate, and gradually upgrading to industry digitalization. This underlying logic has been validated by many industries and is widely recognized as the universal logic for industrial digitalization. We've carefully measured and calculated the revenue share we can capture in each link — the market is large enough.

What we need to consider is: Why Us? In Phase One, we've proven with facts that we can do risk control well. Now we're validating Phase Two: whether transaction and product linking is our strength. For this, we've done POCs (Proof of Concept): increasingly, insurance intermediary companies, like the insurance industry itself, are shifting from extensive operations to hoping risk control can increase their business quality and corresponding returns. We've talked with them one by one and validated that the model works.

Logically, because we do risk control, we have detailed knowledge of over 30 insurance companies and certain influence over their product pricing. So when we cut into transactions, insurers can fully trust our judgment of business quality. Agencies, having both cooperative and competitive relationships with insurers, may not easily win such trust. After our screening, insurers accept more smoothly. Without Phase One as foundation, if a third party like us jumped directly into brokering transactions, the success rate would be very low.

What we do is somewhat like the pork business. When restaurants buy whole hogs directly, they still need someone to process and cut them. If wholesalers first process pork into ribs and ground meat, profit margins are higher and many restaurants prefer it. In Phase One, we're like the cutting specialists hired by large chain restaurants. After our technology gains broad recognition, in Phase Two we can directly help wholesalers process and sell to smaller restaurants. We both greatly increase wholesalers' revenue and provide numerous restaurants with high-quality ribs and ground meat.

/ 07 /

The Pace of Insurtech Market Development

Pengqi Liu: Qijing was founded in 2017 — it's been five years. How do you perceive the industry's development pace? Compared to when you started, is the industry developing faster or slower?

Zhao Xin: When the company was founded, we caught the tail end of the previous insurtech boom. The core team understood both insurance and algorithms, and had some case studies, so we very smoothly obtained angel round funding. Objectively speaking, if we were entering the market from scratch now, it might not be so easy. Three years after founding, in 2020, we validated the complete policy and claims cycle for risk control, had detailed actual data, and completed a second funding round in 2021.

Although our speed in completing each milestone has gradually increased, being in the midst of it, we're particularly aware that insurance digitalization can't be rushed — every iteration cycle requires patient validation. For auto insurance, a policy covers one year; if a major accident occurs, from vehicle damage to final claim completion may take one to two years. Before 2019, every customer was relatively difficult to acquire.

But once products are validated, the flywheel effect becomes very obvious. Ninety percent of our customers were acquired in the past two years. Now, while continuing to replicate Phase One results, we're beginning to cut into product and transaction links, entering another phase requiring validation. By next year, transaction business should grow again. Iteration cycles no longer need two or three years, but certainly won't be completed in just a few months.

Our direction of effort is to make validation cycles shorter. Once we establish cooperation with customers, relationships become very long-term, building solid bilateral effects.

/ 08 /

What Talent Does the Insurtech Industry Need?

Pengqi Liu: From what I've heard, succeeding at what you're doing is quite complex — requiring industry knowledge, business understanding, and finding suitable technology to solve problems, very interdisciplinary. This actually fits FreeS's investment style well; we also believe interdisciplinary directions are where innovation and strong competitive moats emerge.

Tech talent is already scarce, and in a relatively niche track like insurance, how does Qijing solve the talent problem? Do you have your own selection logic?

Zhao Xin: This gets to our difficulty. When I first started, I thought core teams of insurance talent plus tech talent would suffice, so I tried finding tech talent in the internet industry and business talent in insurance companies.

But I later discovered that simply adding insurance people and tech people together doesn't achieve insurtech innovation. What we need are people with basic appreciation for both insurance and technology, who are excellent in one area, and also resilient in innovation — really hard to find.

Bumping along to where we are now, the team continues to develop, and members who have stayed demonstrate cross-disciplinary characteristics: actuaries with decades in insurance who have done both algorithms and business; entrepreneurs from auto manufacturing who started selling parts and took their companies public; platform architecture veterans from gaming who get excited for half a day calculating their family's auto insurance prices; MBAs who started as coders, became product managers, then transformed into key account sales. Everyone comes together with reverence for insurance and determination to improve the industry, doing what's right rather than what's easy.

If you have firm conviction in fintech innovation, can endure solitude, and have expertise in sales, algorithms, development, project management, product design, or operations — welcome to join Qijing. Together we'll explore using technology to make fair and effective protection more accessible! Interested candidates please send resumes to HR@deltaentropy.com

Join Qijing If you have firm conviction in fintech innovation, can endure solitude, and have expertise in sales, algorithms, development, project management, product design, or operations — welcome to join Qijing. Interested candidates please send resumes to HR@deltaentropy.com

Reader Giveaway We welcome your thoughts in the comments. Through November 17, the five most thoughtful commenters will receive a LAMY pen from Qijing Technology (orange or white packaging, shipped randomly).

▲ Li Xiang x Feng Li: The "Monopolistic Success" and "Gradual Dilemma" of the Dollar | Feng Li Column

▲ How Will Humans Work in the Future? | FreeS Report 26

▲ Financial Transformation Begins: How to Build the Next "Hundsun"?

▲ Building Virtual Idols, the Pitfalls and Barriers | FreeS Interview