The Category Logic Behind the Hype — Using Coffee Industry Investment as an Example

Most business happens below the surface.

"

Hai Huang, Executive Director, FreeS Fund

Email: hai@freesvc.com

Hai Huang focuses on investments in consumer and retail sectors. He has led and participated in investments in Club Factory, Saturnbird Coffee, Vphoto, and other projects. Huang holds an MS in Management Science and Engineering from Stanford University and a BS in Mathematics from The University of Hong Kong.

"

In a changing consumer environment, we can find investment opportunities in many niche categories.

Nestlé launched instant coffee in China in 1989. Starbucks opened its first Beijing store in 1999. Coffee has had a 30-year history in China, yet it has developed at an unprecedented pace in just the past two years.

Luckin Coffee went public at Lightspeed. Coffee chains like Coffee Box and Fisheye Coffee have raised hundreds of millions of yuan in cumulative funding. On the other side, beverage giants including Nestlé, Coca-Cola, and even Nongfu Spring have entered the coffee market with ready-to-drink products. The only offline retail format maintaining rapid growth — convenience stores — has also gotten into the freshly brewed coffee business. Beyond the familiar FamilyMart and 7-Eleven, you may have noticed recent news that Sinopec, with its 50,000 convenience stores, has joined the coffee-selling ranks.

But most of the business happens beneath the surface. Over the past two years, Luckin has attracted the most attention, yet the freshly brewed coffee market it belongs to, despite rapid growth, still only accounts for 15-20% of China's coffee market. The relatively unremarkable instant coffee segment still holds 60-70% market share. In this article, we try to break down the real consumer landscape of China's coffee industry, and what kinds of innovations actually stand a chance. Additionally, we attempt to examine the category selection logic for consumer goods through the lens of coffee.

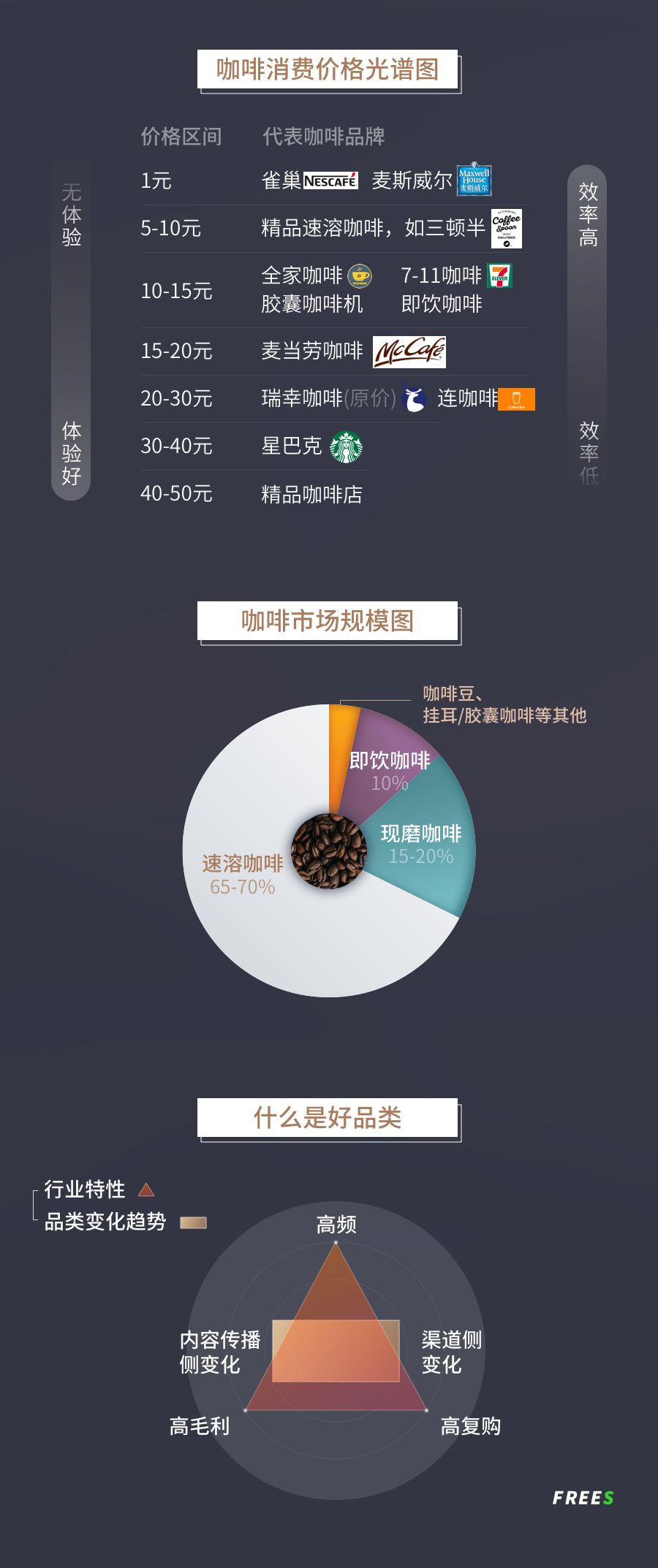

China's Coffee Consumption Map

Coffee consumption scenarios — including purchase methods and price tiers — are among the most diverse and rich in the consumer goods industry.

By price, China's overall coffee market map looks roughly like this: If you want to spend one yuan on coffee, you get Nestlé 3-in-1. If you want to spend 5-10 yuan, you choose upgraded instant products like Saturnbird. If you want to spend 10-15 yuan on a cup, excluding various promotions, convenience stores like FamilyMart and 7-Eleven offer freshly brewed and ready-to-drink coffee. The self-service coffee machines and office capsule machines that were popular for a while also fall in this category. If you want to spend 15-20 yuan on a cup[1], you can also choose McDonald's coffee.

In the 20-30 yuan price range, you have Coffee Box and Luckin. Luckin's original price exceeds 20 yuan, but through discounts and group-buying promotions, the actual revenue per cup including shipping may be slightly above 10 yuan. In first-tier cities, boutique coffee shops emphasizing higher quality than Luckin have also emerged, priced in the low 20s. Moving up, Starbucks occupies the 30-40 yuan zone. There are also premium boutique coffee chains priced above 40 yuan.

Analyzing this consumption map, we can see: at every price point, for every consumer group, there's a way to drink the coffee they want. As investors, what we need to consider is: which consumption tier has the largest consumer base and market in China? What changes are happening in this market now? With Luckin's strong rise and Lightspeed IPO, do we still have opportunities to make new investments?

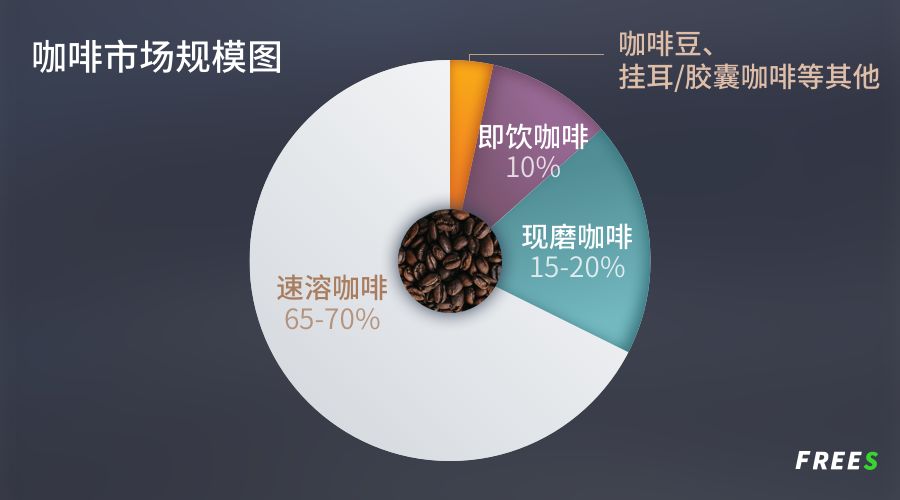

To answer this, let's first look at the overall composition of the coffee market. Based on multiple public sources we consulted, China's total coffee market is over 100 billion RMB[2].

In this market, freshly brewed coffee including Starbucks and other coffee shop chains accounts for only about 15%-20%[3]. Meanwhile, 65%-70% of the coffee market belongs to instant coffee[4]. Ready-to-drink coffee ranks third with roughly 10% market share[5]. The remaining market is occupied by niche consumption methods like coffee beans, capsule coffee, and drip bag coffee.

Let's start with ready-to-drink coffee, which accounts for about 10% of the market. Ready-to-drink means drinking a beverage — we understand it better as "coffee-flavored drink." It tastes relatively sweet, or easy to drink. Its sales scenario is typically convenience stores, where it sits next to iced black tea, fruit juice, and yogurt. This type of product has stronger beverage attributes.

Next is freshly brewed coffee. Abroad, a large portion of this category is home-brewed coffee: using coffee machines and beans, brewing a pot in the morning, pouring a cup for each person, doing the same when guests arrive — the scenes we often see in American TV shows and movies. This scenario is hard to become mainstream in Chinese households, partly because it's troublesome, and partly because small apartment kitchens don't have much space for coffee machines. Additionally, in China, there are convenience stores and delivery services for getting coffee — options that don't exist or aren't convenient enough in the US.

Coffee made in Starbucks stores also falls into the freshly brewed category. When entering China, Starbucks brought along the "third place" concept: a space beyond home and work. Consumers come here not just for coffee, but to wait for people, chat, work, and do business. The "third place" concept was crucial to Starbucks's success in China, possibly even more so than in the US. We've observed that in the US, a higher proportion of users simply grab their coffee and leave.

As analyzed above, our visits to coffee shops have a strong social component. The growth in the number of Chinese coffee shops in previous years didn't represent an explosion in daily coffee consumption. But the third type of freshly brewed coffee — Luckin's delivery model — is indeed strong evidence of the rise of daily coffee consumption.

Although it used substantial subsidies, Luckin's rise at least proved one thing for the industry: if you don't need to sit in a store to chat/socialize, and simply want to drink a cup of coffee, spending 30-plus yuan on Starbucks isn't worth it for many users, because a cup of coffee itself isn't worth that much.

A 35-yuan Starbucks latte actually contains about five yuan worth of coffee, including beans, milk, and packaging. What you're paying 35 yuan for is two services: the five-yuan coffee, plus the comfortable environment Starbucks provides where you can sit and chat for two hours.

The latter isn't directly charged for — it's collected through the coffee. Your coffee is essentially you paying Starbucks's rent; fundamentally, you're covering this cost. So even though the direct cost of a cup of coffee is only five yuan, Starbucks's net profit margin is only around 10%.

By saving on environment and service costs, the price per cup can be lowered while still making a profit. That is, if you have no social needs and just want to drink a cup of coffee, the 35-yuan Starbucks can be challenged. Startups including Luckin happened to catch a trend: Chinese consumers' genuine daily demand for drinking coffee has risen.

This demand parallels the tea beverage market. Not many people need to sit and socialize in HEYTEA. You buy a 20 or 30-yuan drink and even queue for it — truly just to enjoy that beverage. Consumers willing to spend this cost to enjoy a high-quality drink is a typical example of consumption upgrade. The evolution of Chinese consumers brings new investment opportunities for investors.

Finally, let's look at the instant market, which still constitutes the main consumption. In instant coffee, Nestlé is the undisputed king. Its most classic product is the "3-in-1" that entered China in the early 1990s — strip after strip of coffee powder packets, mainly composed of coffee powder, sugar, and creamer. Chinese people's earliest understanding of coffee likely came from this, with the function of staying alert. But there's general consensus that it's not very healthy or tasty.

Similar 3-in-1 instant coffee products sell for even less than 1 yuan per strip. Its product characteristics suited China's early coffee market, but also make it difficult to position itself as a consumption upgrade brand in a future new consumption environment pursuing health and fashion.

Currently, some relatively innovative coffee products have appeared on the market, such as FreeS-invested Saturnbird. It's 100% pure coffee with no sugar or creamer in its ingredients. You can pour it into milk or water and drink directly. Another key consumption scenario different from previous instant products: it doesn't need hot water and dissolves instantly in cold water/ice water. (Welcome to participate in the interactive activity at the end of this article to experience Saturnbird's star product)

▲ Pour the boutique coffee powder from the mini cup into ice water, instantly restoring a truly delicious cold brew coffee.

In terms of taste, Saturnbird drinks like cold brew coffee, far superior to traditional instant. It is essentially innovation and upgrade within the instant category against the original 1-yuan 3-in-1 product.

How Can the Coffee Industry Innovate?

Coffee is fundamentally an agricultural product.

As an agricultural product, raw materials determine its quality — coffee beans are essentially grown by farmers, with the core difference being origin. However, general consumers find it difficult to distinguish between origins, so neither Starbucks nor Luckin can emphasize product-level differentiation too much. To some extent, mass-market coffee leans toward being a standardized product. Over thirty years since its founding, Starbucks's hit product is still the standard-made latte, not needing to iterate its product line every so often like industries that emphasize trends.

From this perspective, if we invest in the coffee industry, a major challenge is finding innovation on top of homogenized products. This innovation is relatively difficult because coffee beans are provided by foreign coffee growers — brands can essentially only ensure consistency through selection, with limited room for product excellence.

With product innovation being difficult, Luckin chose to enter the market through business model innovation, a typical capital-driven player. After researching extensively, we found that Saturnbird is one of the few product innovation cases. The freeze-dried powder cold-brew process behind Saturnbird, along with its unique, highly recognizable packaging (Lego-like mini coffee cups), currently remains the only one of its kind, though imitators are expected soon.

So in China's coffee market, every company must find its unique innovation point on the basis of homogeneous raw materials. Luckin切入 from the angle of convenience and accessibility through new business models; FreeS-invested Saturnbird切入 from product and process innovation. Ultimately, innovation沉淀 into brand.

Of course, I don't believe product innovation in the coffee industry can sustain an advantage for ten or twenty years, because consumer goods don't have absolute barriers in the technological sense. Sustainable barriers are like Starbucks — transforming certain enterprise advantages into brand势能 over time. Only brand moats can be sustained long-term.

From Aspirational Consumption to Daily Consumption

China's coffee market has entered a period of rapid development. Over the past several years, on a market scale exceeding 100 billion, China's coffee market has maintained about 20% annual growth[6], yet per capita annual coffee consumption remains at a low level of 6-7 cups[7]. The scale is not small, growth is relatively fast, but per capita levels are still low — meaning large room for growth. This is also the point coffee industry practitioners love to make most.

The reason foreign per capita coffee consumption is high is that coffee has evolved into daily consumption. Everyone has a coffee machine at home and in the office; freshly brewed coffee has become part of life. Whether in Europe, America, Japan, or Korea, this is the case. I believe China's coffee industry will also gradually evolve from social spaces and aspirational experiences into basic daily consumption.

When a demand evolves from novelty-driven/aspirational consumption (both psychological satisfaction) to daily consumption, users start doing the math — on price on one hand, and convenience on the other. Both need to be suitable for coffee to become daily consumption.

To illustrate with an example: Freshippo was very popular in its first two years because the novelty-seeking population was huge — everyone went to Freshippo to consume lobster and crab, so business grew quickly. But after the freshness of novelty/aspirational consumption passed, the question Freshippo faced was: can it become daily consumption? Freshippo needed to adjust on price and product selection to face/address this challenge.

Returning to the coffee market, we hope to capture the time window of the shift from novelty/aspirational consumption to daily consumption in our positioning.

Category Selection Logic for Consumer Goods Through the Lens of Coffee

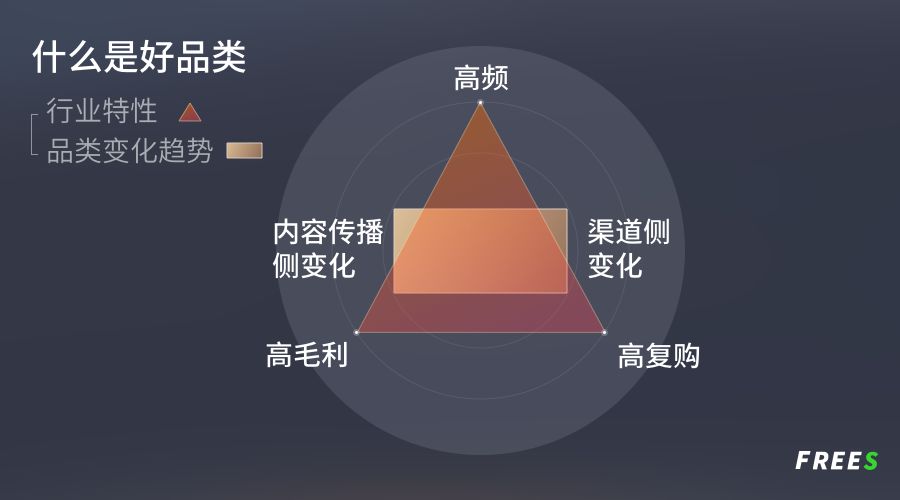

The above discussion of coffee also reflects a general analytical framework for various consumer goods categories. A question we often consider is: in the consumer goods field, what makes a good category? In other words, how do we find areas worth paying attention to and digging deeper into, then discover good companies within them?

We can analyze from two dimensions: industry characteristics and changing trends.

Industry characteristics are the unchanging parts of category attributes. The long-term advantages of the coffee category, as analyzed above, are its high frequency, high margin, and high repurchase characteristics.

High frequency and high repurchase differ slightly. High frequency means the consumption frequency in this category is high. High frequency determines that marketing in this industry will be very efficient — of ten people who see this product's promotion, eight can order immediately. Besides coffee, high-frequency categories include beauty; low-frequency categories include home furnishings. I also pay close attention to the home furnishings industry, but its low-frequency attribute确实 creates certain customer acquisition difficulties, because when consumers see an advertisement, they may not be in a purchase period for home furnishings. By comparison, beauty product user conversion rates will be higher than home furnishings.

High repurchase means a single SKU in this category can be repeatedly purchased and consumed, so the ceiling for a single SKU is high, and blockbusters can emerge. For example, Starbucks's best-selling product for decades has been the latte, which consumers frequently purchase without getting tired of, without worrying that the product's fashion attribute will quickly fade — this is high repurchase.

From these high frequency, high margin, and high repurchase characteristics, when we observe the consumer space, e-cigarettes and color cosmetics each meet at least two of the three, and they are also the hottest consumer sub-sectors in the past two years.

Changing trends, on the other hand, are the evolving attributes of category characteristics — the opportunities for rapid rise.

This splits into two aspects. One is changes on the content distribution side — whether new media formats are emerging that can most effectively drive the rise of certain categories. I analyzed this point in my previous article "Startup Brand Breakthrough: From Traffic Thinking to Content Thinking." The other is changes on the channel side, typically opportunities from offline to online. Specifically, it's when category demand is growing, but existing offline giants haven't heavily covered the category — then the space is large enough.

Jiangxiaobai is a typical case for both points. On distribution, you can see Jiangxiaobai achieved "product as content" — it was the first to make the liquor bottle itself into content, with golden phrases covering the bottle body. On channel change: baijiu is a large category, but previously it targeted middle-aged social business dining scenarios, focusing on mid-to-high-end restaurants. Jiangxiaobai made a baijiu product for young people, capturing food stalls and small restaurants.

Saturnbird Coffee is the same. Instant coffee's original consumption scenario leaned offline, with weak internet attributes. Saturnbird chose to切入 through planned consumption scenarios on e-commerce, where consumers buy 24 or even 36-cup combo packs online to meet their monthly coffee needs.

So on the product positioning side, our investment logic is: when a category is rapidly rising, find a differentiated entry point from existing giants.

Data Sources and Notes

[1] Many companies have membership points and discount activities; coffee prices mentioned in this article refer to original prices

[2] Data source: Mintel

[3] Data source: Qianzhan Industry Research Institute, Mintel. Data is estimated; because coffee shop sales aren't entirely coffee products, a more reliable calculation method is to work backward from coffee bean usage.

[4] Multiple versions of relevant data exist, but without exception, all point to instant coffee occupying the largest proportion of the coffee market.

[5] Data source: Qianzhan Industry Research Institute, Mintel

[6] Data sources: AskCI, Qianzhan Industry Research Institute, International Coffee Organization, USDA. Specific data varies across sources; FreeS Fund adopted the most credible values through research.

[7] Data source: Luckin Coffee prospectus

Article Summary

-

Coffee is fundamentally an agricultural product, leaning toward standardized goods. In China's coffee market, every company must find its unique innovation point on the basis of homogeneous raw materials.

-

Most of the business happens beneath the surface. The relatively unremarkable instant coffee occupies 60-70% of market share.

-

Coffee in China is evolving from aspirational consumption to daily consumption.

-

Good consumer categories feature industries with high frequency, high margin, high repurchase, and other characteristics. Additionally, they ideally catch changes on the content distribution side and can leverage changes on the channel side.

Today's Thinking

-

We analyzed potential investment opportunities in the coffee market's shift from novelty/aspirational consumption to daily consumption. In the consumer space, what other sub-markets have similar time windows?

-

In China's tier-3 and tier-4 markets, does this time window theory同样 apply? What opportunities might it bring?

Welcome to share your thoughts and observations in the comments. By 9 PM on September 25, the 3 most thoughtful contributors will each receive the star product from FreeS Fund portfolio company "Saturnbird Coffee" — super instant boutique coffee 3.0 (36-cup bucket). Ice/hot water, milk, sparkling water; home, office, travel... Good Coffee, Anywhere.

(Welcome to read, share, and like. For reprinting to other official accounts, websites, or mobile apps, please reply "reprint" to learn reprint rules, and contact "Frees Xiaorui" (id: freesfund) for authorization. Copyright belongs to FreeS Fund.)

▲ Startup Brand Breakthrough: From Traffic Thinking to Content Thinking

▲ Li Xiang × Li Feng: 200 Million New Urban Residents' Consumption Awakening — Who "Harvests" It?

▲ Deep Dive into Tier 3-6 Markets: Shima Chuxing Announces $20 Million Series A | FreeS Funding News