Silicon Valley's Booming Longevity Economy, Its Commercial Path Is Right in Front of Us

"The first people who will live to 1,000 may already be alive today."

"The first people who will live to 1,000 may have already been born."

This bold prediction came from Max Hodak in a recent interview. In 2016, he co-founded Neuralink with Elon Musk. Now he's started fresh with a new company called Science, also focused on brain-computer interfaces, and widely seen as Neuralink's most credible competitor.

His confidence stems from the non-linear explosion of BCI and frontier biotech. But for sharp-eyed capital markets, while the ultimate vision of "living to 1,000" is undeniably grand, investors are asking a more immediate question: where in this massive Longevity Economy tech revolution can commercialization happen fastest?

The answer isn't the distant brain or internal organs. It's the body's largest and most visible organ — skin.

Skin health and aesthetic medicine are officially crossing from "lifestyle consumption" into the core territory of "serious medicine." Behind this shift lies collective validation from top global investors in the logic of "Skin Longevity." Unlike traditional "skin health" concepts focused on treating disease (acne, eczema), Skin Longevity emphasizes proactive aging delay and long-term maintenance of youthful skin state — aligning closely with Silicon Valley's hottest investment theme.

How closely aligned?

In 2023, Sam Altman personally invested $180 million — half his total liquid assets — in Retro Biosciences, a biotech company whose core mission is adding 10 years to human healthspan through frontier biotechnology. Then in January 2025, without a single Phase I clinical data point, the company launched a $1 billion Series A round targeting a $5 billion valuation based purely on vision. This fully demonstrates capital markets' feverish optimism for the longevity economy track. Its fundraising materials even projected: the company's market cap would surpass Eli Lilly and Novo Nordisk, approaching Alphabet and Microsoft.

In 2022, Altos Labs debuted with $3 billion in launch funding, backed by core investor Jeff Bezos — setting the largest single-round fundraising record in biotech history. The company's sole objective: "reverse human aging." One year post-funding, Altos Labs recruited 4 Nobel laureates, offering "sports-star-level" compensation starting at seven figures plus equity incentives.

Since then, global longevity sector funding has only heated up further. In 2024, funding reached $8.5 billion, surging 220% year-over-year, comparable to peak AI investment bubble levels. More broadly, according to UBS's 2026 outlook report, global longevity economy annual revenue could soar from $5.3 trillion to $8 trillion.

Longevity Economy Sector Funding Overview. Data source: Compiled from public information**

This frenzy isn't limited to the face. Capital has rapidly extended into the blue ocean of "Scalp Longevity." Just this month, KilgourMD, a scalp anti-aging brand founded by a Stanford dermatologist, announced its Series A completion — merely six months after closing a $5 million seed round. The brand's core commercial narrative precisely matches current industry consensus: abandon traditional hair care's "surface-level" approach, and instead pipeline directly into follicle-level repair and even "gray-to-black" hair reversal aging domains.

As Sam Altman and his peers pursue, investments in the longevity economy ultimately never aim simply at "living to 150." The goal is "being as healthy at 120 as at 40." This conceptual shift from "lifespan extension" to "healthspan extension" is precisely why the longevity economy holds fatal attraction for capital markets.

The reason "Skin Longevity" has become such a hot segment within longevity economics is that pure "aging reversal" technology may need 10-20 years to reach clinical application. Investors increasingly recognize skin — the body's largest organ (roughly 16% of body weight, 1.5-2 square meters surface area) and most visible aging marker — as both a validation scenario for longevity technology and the fastest revenue-generating application domain.

To fully understand why "Skin Longevity" has become a new global medical investment focus, we need to examine three dimensions:

First, technological paradigm disruption — from traditional "physical filling" toward cell signal-based precision delivery;

Second, valuation system reconstruction — how medical hard tech enables aesthetic medicine tracks to command premium multiples dozens of times higher, with Korean markets already providing validation;

Third, industrial landscape reshaping — how "Silicon Valley innovation + China manufacturing" will become the new paradigm in this global frenzy.

Below is Peakview portfolio company N1 Life founder Dr. Janice Zang's detailed breakdown of these three dimensions.

Author Bio Janice Zang, PhD in Chemistry from Stanford University, studied under U.S. National Academy member Paul A. Wender, specializing in peptide chemistry and targeted drug delivery systems, with deep expertise in skin drug delivery technology. Founded N1 Life in Silicon Valley in 2019, later established Xinan Biotechnology (Suzhou) Co., Ltd., maintaining long-term research and clinical collaborations with Stanford University and other top international research institutions, with formal partnerships established with over 10 pharmaceutical and health companies. Selected for national-level major talent programs, named Suzhou Young Scientist, among other honors. Reader Giveaway

What efficacy concerns do you have about aesthetic medicine products? Share your thoughts in the comments. By 17:00, April 3, 2026, the most thoughtful commenter will receive a copy of The Secret Life of Skin.

01 Molecular Innovation: The Ultimate Battlefield Is Delivery Systems

From "Filling" to "Signal Transduction": A Paradigm Shift

"Regenerative Aesthetics" has become high-frequency vocabulary. The industry is collectively abandoning "filling mentality" — no longer satisfied with simply "plugging holes" with inert materials like hyaluronic acid, but turning to more fundamental questions: how to send "youth signals" to skin cells, letting cells restore their own youthful state?

Several molecular categories are becoming focal points:

1. Polydeoxyribonucleotide (PDRN) has already secured significant position in Korean medical tourism. This molecule extracted from salmon DNA activates fibroblasts and promotes collagen synthesis. The popularity of products like Rejuran (colloquially "salmon injection") fundamentally validates the viability of the "biological signal molecule" approach.

2. Exosomes represent another frontier direction. These nanoscale vesicles secreted by cells carry signaling molecules capable of regulating surrounding cell behavior. Beauty Independent's 2026 beauty trends report shows exosomes rapidly moving from laboratory concept toward market application.

3. Peptides are the core ingredient in 2026's skincare landscape. Consumers are actively seeking "next-generation scientific skincare" active ingredients, and peptides are reshaping the competitive landscape of premium anti-aging skincare. From La Prairie's thousand-dollar Platinum Multi-Peptide cream, to Augustinus Bader's $1 billion valuation built on TFC8® peptide technology, to Biologique Recherche pushing peptides toward epigenetic regulation — peptides have upgraded from supporting ingredients to core engines driving brand premium and technical moats, with market size projected to exceed $6.6 billion by 2033. What will determine winners in the next phase is no longer "what peptide was used" but "how the peptide was delivered" — encapsulation and delivery technology is becoming the true watershed.

The Precision of Delivery Systems and Migration of Pharmaceutical Technology

No matter how advanced the molecule, if it cannot penetrate the skin barrier and reach target cells, it remains trapped at the "in vitro experiment" data level. This is precisely why delivery technology has become the critical bottleneck.

1. Evolution From Passive to Active

Traditional transdermal patches rely on passive diffusion driven by concentration gradients — low efficiency, slow speed. Newer systems employ active push technologies: iontophoresis uses weak electrical current to actively "push" drugs through the skin barrier; microneedle arrays physically penetrate the stratum corneum directly. Research Nester's Transdermal Drug Delivery Systems Market Size and 2026-2035 Forecast Report shows that by 2035, iontophoresis alone is expected to capture 22.2% of the transdermal drug delivery market.

2. Migration of Mature Pharmaceutical Delivery Technologies

What's particularly interesting is that mature delivery technologies from pharmaceuticals are migrating toward skin aesthetics. These technologies have already been validated for drug delivery; the question now is how to adapt them for skin as a special organ:

Liposomes are the most mature nanocarrier system. They can simultaneously encapsulate both water-soluble and fat-soluble active ingredients, improving permeability and bioavailability through fusion with skin lipid bilayers.

Polymer microspheres can achieve sustained and controlled release of active ingredients, extending local drug action time in skin and reducing dosing frequency. This is particularly important for anti-aging ingredients requiring long-term use.

Polymer nanoparticles, through surface modification, can achieve a degree of targeted delivery, increasing active ingredient enrichment in specific skin layers (epidermis, dermis).

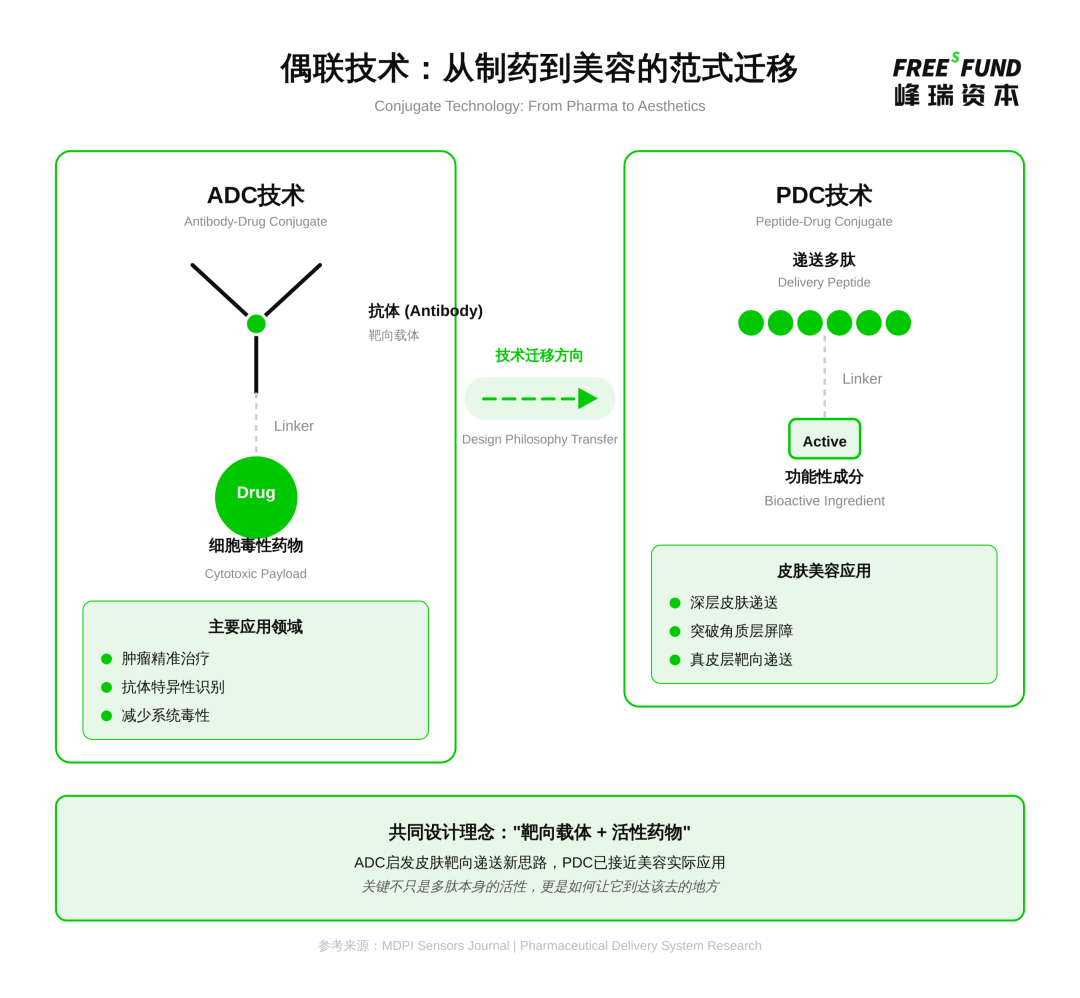

3. Innovative Breakthroughs in Conjugation Technology

Conjugation technologies from pharmaceuticals are opening entirely new possibilities for skin delivery:

Antibody-drug conjugates (ADCs), while primarily used in oncology, are inspiring new thinking in skin-targeted delivery through their "targeting vector + active drug" design philosophy — if skin-specific targeting molecules can be identified, more precise delivery than existing methods becomes possible.

Peptide-drug conjugates (PDCs) are closer to practical application. By covalently conjugating delivery peptides with active ingredients, PDCs can breach the stratum corneum barrier, delivering molecules precisely to deep skin layers and even the dermis. This represents the cutting edge of current peptide aesthetic technology — core competitiveness no longer lies solely in the peptide's biological activity, but increasingly in how to get it precisely where it needs to go.

This technology migration and innovative fusion from pharmaceuticals into aesthetics is opening an entirely new market space. When the precision of oncology drug delivery meets the consumer attributes of skin aesthetics, "medical-grade beauty" will truly move from concept to reality.

Data source: MDPI Sensors Journal | Pharmaceutical Delivery System Research

02 Valuation Recalibration and the Korean Model's Evolution

When an industry acquires pharmaceutical-grade regulation, recurring revenue models, and clinical evidence, its valuation logic undergoes a qualitative leap. This is precisely the transformation aesthetic medicine technology is experiencing.

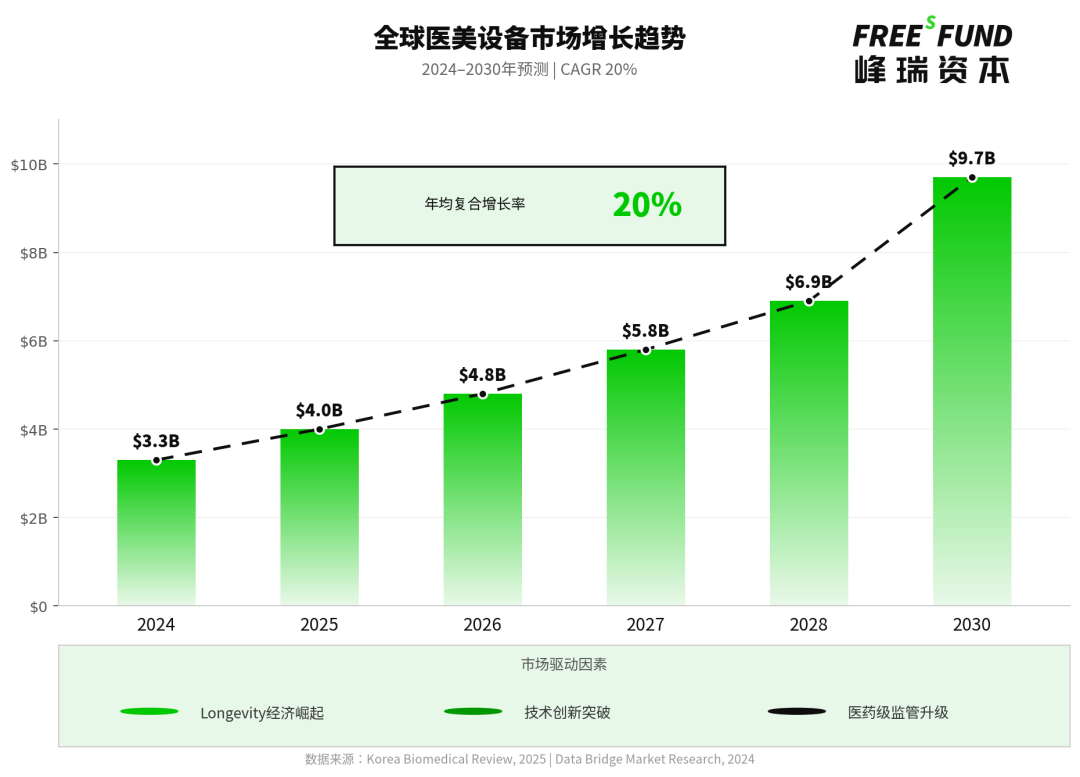

The global medical aesthetic device market is expanding rapidly from $3.3 billion in 2024 to a projected $9.7 billion by 2030, representing a compound annual growth rate (CAGR) of 20%.

Global aesthetic device market growth trajectory. Data sources: Korea Biomedical Review, 2025; Data Bridge Market Research, 2024.

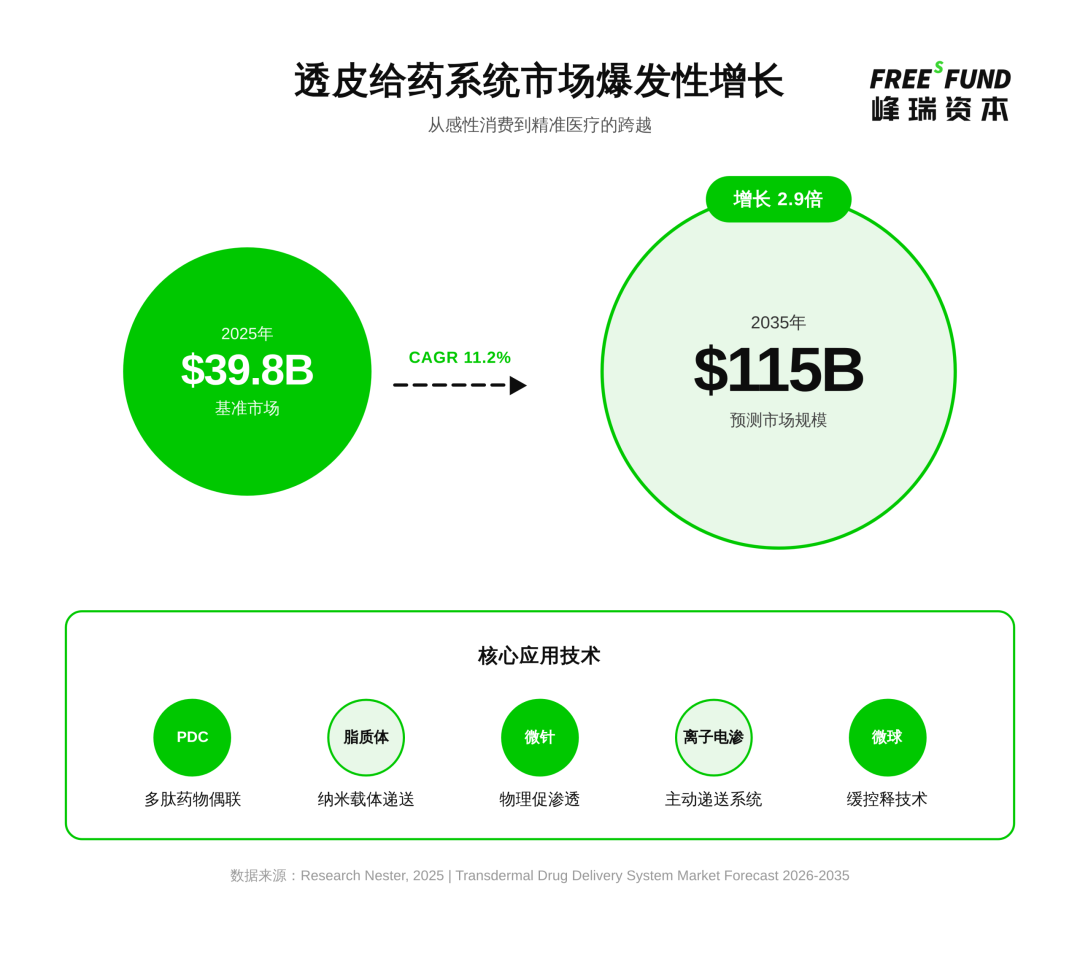

More striking is the explosion on the drug delivery side. Research Nester shows the transdermal drug delivery system market growing from $39.8 billion in 2025 to $115 billion by 2035, at an 11.2% CAGR. The significance of this figure: it is no longer merely a "skincare market," but a genuine drug delivery technology market.

Data source: Research Nester, 2025 | Transdermal Drug Delivery System Market Forecast 2026-2035

But what truly excites investors is not merely absolute growth rates — it is the multiple expansion. Traditional cosmetics companies typically trade at 10-15x EBITDA multiples, while medical device and biotech companies command 30-50x. When the beauty industry acquires pharmaceutical-grade technical moats and regulatory barriers to entry, its valuation ceiling is completely redefined.

Classys: From Hardware Vendor to Infrastructure Layer

Consider Korea, where the aesthetic medicine market is exceptionally developed.

Korean medical aesthetic device company Classys has delivered standout capital markets performance. It has not only maintained operating margins above 50% for multiple consecutive years, but has also projected $1 billion in sales by 2030 with operating margins exceeding 50% — demonstrating earning power far beyond traditional beauty. Based on this commercial and capital markets success, we conducted a deep deconstruction of its evolution, finding that it precisely illustrates the industry's transformation logic. On the surface, Classys is a hardware manufacturer of ultrasound and radiofrequency devices. But careful study of its technology platform reveals it has completed a transformation into an "infrastructure layer."

1. Barriers Built by Pharmaceutical-Grade Certification

Classys CEO Seunghan Baek stated in an interview: Classys's core product portfolio covers the major technical pathways of energy-based devices (EBDs). Its flagship product, Shrink Universe, employs HIFU (high-intensity focused ultrasound) technology. Since its 2014 launch, over 18,000 units have been installed globally, capturing the #1 position in South America's HIFU market. South America ranks as the world's fourth-largest aesthetic medicine market, with Brazil alone representing an $800 million aesthetic device market.

The Volnewmer/Everesse series employs monopolar RF technology, using revolutionary single-pulse energy delivery combined with continuous water-cooling systems to significantly reduce treatment pain and time costs. The Quadsay series' microneedle RF technology represents the next generation of precision treatment solutions.

The common characteristic of these technologies: all have obtained the world's most stringent medical device certifications, including FDA, CE MDR, KFDA, TGA, and ANVISA. This means they have completely transcended the category of "salon equipment" and entered the medical device regulatory system — a realm traditional cosmetics companies cannot approach.

2. Business Model Innovation: The EBRP Platform

More critical is the evolution of the business model. Classys is the world's first company to propose and implement the EBRP (Energy-Based Recurring Platform) model — essentially the "razor and blades" model applied to aesthetic medicine. Seunghan Baek explained in an interview: This model creates highly sticky, predictable recurring revenue streams: consumables sales already account for 43% of total revenue.

Financial data reveals this model's power: from 2018-2023, the company achieved average annual sales growth of 31% and EBITDA growth of 39%. 2024 revenue reached approximately $169 million, up 34.9% year-over-year. More aggressively, the company has set a target of $1 billion in sales by 2030 with operating margins exceeding 50% — a profitability level approaching that of medical technology companies.

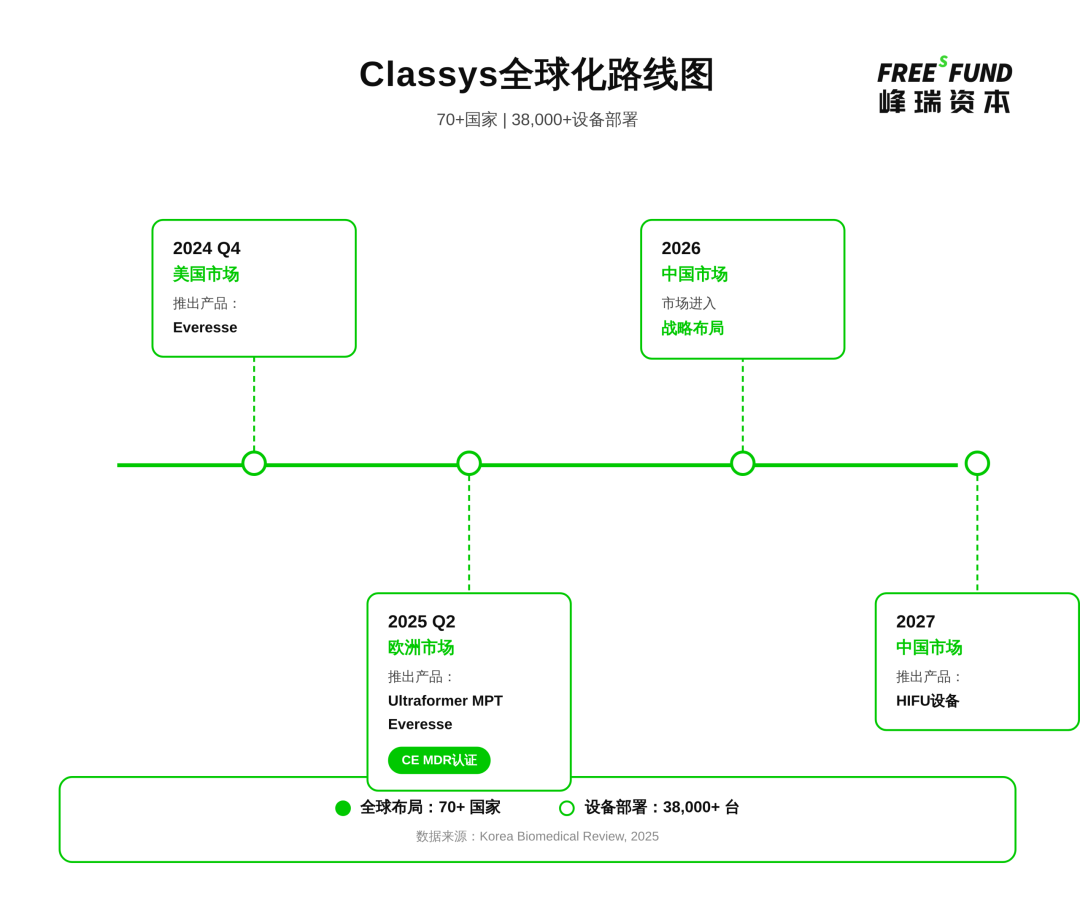

3. Global Expansion Rhythm

As of January 2025, Classys has deployed over 38,000 devices across more than 70 countries. Its globalization roadmap is clear: Q4 2024 saw the U.S. launch of Everesse; Q2 2025 plans European market launches of CE MDR-certified Ultraformer MPT and Everesse; 2026 entry into China; 2027 HIFU device launch.

Data source: Korea Biomedical Review, 2025

4. Re-examination from an Academic Perspective

Stepping outside commercial narrative and re-examining Classys's technology from the academic perspective of skin drug delivery reveals deeper value. The skin's stratum corneum is the natural barrier facing all externally applied bioactive substances — its existence ensures that the "active ingredients" in the vast majority of skincare products remain on the skin's surface.

Classys's energy devices are essentially "precision terminals for physical permeation enhancement." Through precisely controlled thermal injury (such as RF) or physical puncture (such as microneedling), these devices open a "transient window" for subsequent molecular drugs (such as peptides, exosomes, growth factors). This "device paves the way, drug permeates" drug-device synergy model is the critical prerequisite for achieving cellular-level skin repair.

In investors' eyes, Classys is not a company that sells equipment, but the infrastructure layer of the entire "skin longevity" ecosystem.

If Classys represents the "hard tech + medical device" path, then other players in Korea's beauty industry demonstrate entirely different evolutionary directions.

APR Corp: Dimensionality-Reduction Strike Through Drug-Device Integration

APR Corporation (parent company of Medicube) pursues another path: downgrading laboratory-grade technology to home-use scenarios.

According to Business of Fashion, 2025 was an explosive year for APR. 36-year-old founder and CEO Byunghoon Kim became one of Korea's youngest billionaires in July, with the company's stock price surging over 200% since the beginning of the year. This explosion was no accident — in the first half of 2025 alone, APR's global sales reached $423 million.

APR's core strategy is a closed loop of "bioactive ingredients + home-use photoelectric permeation." While traditional beauty brands still compete on ingredient concentration games like "5% or 10% niacinamide," APR is already competing on "transdermal penetration rate" — using proprietary home beauty devices to alter the skin microenvironment, enabling accompanying molecular formulations to truly cross the stratum corneum.

This model essentially pulls beauty from "emotional consumption" into "data-driven" medical tracks. When a skincare product acquires the delivery logic of a "drug" and the immediate feedback of a "device," its substitutability for traditional luxury brands becomes structural — this is not a gap marketing can bridge, but a generational technology gap.

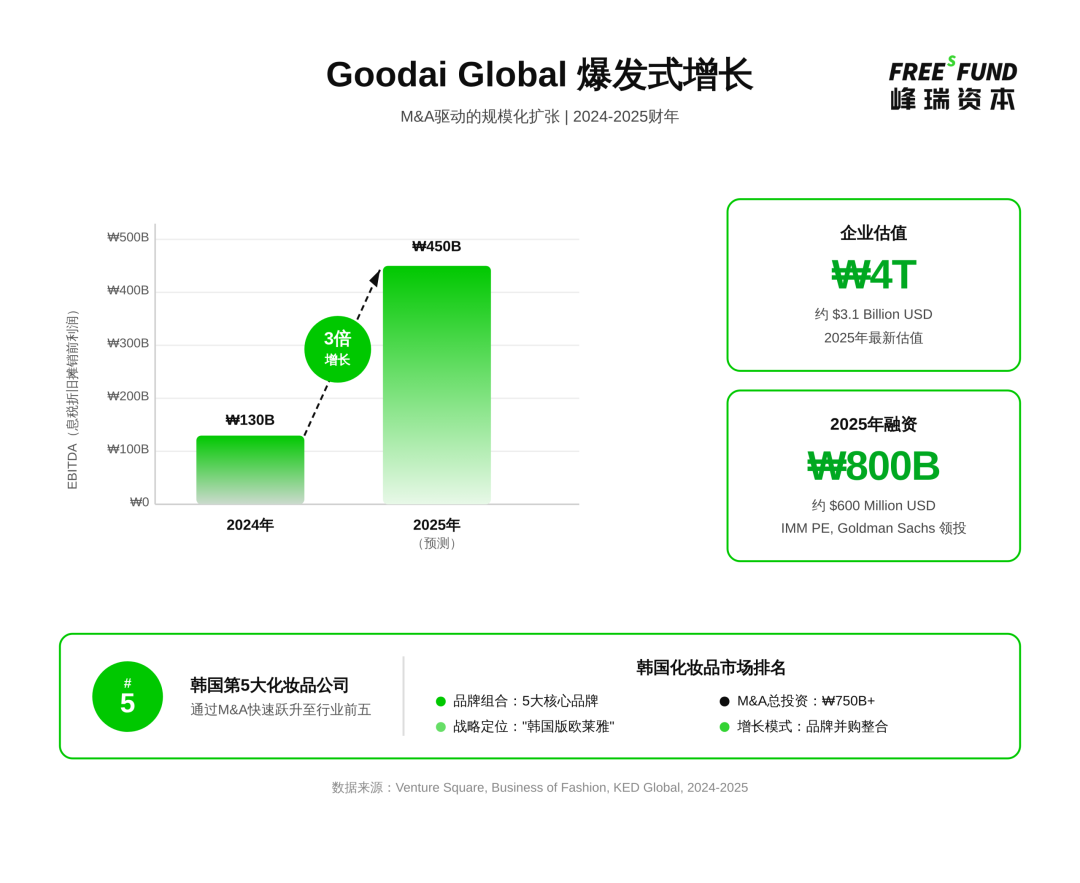

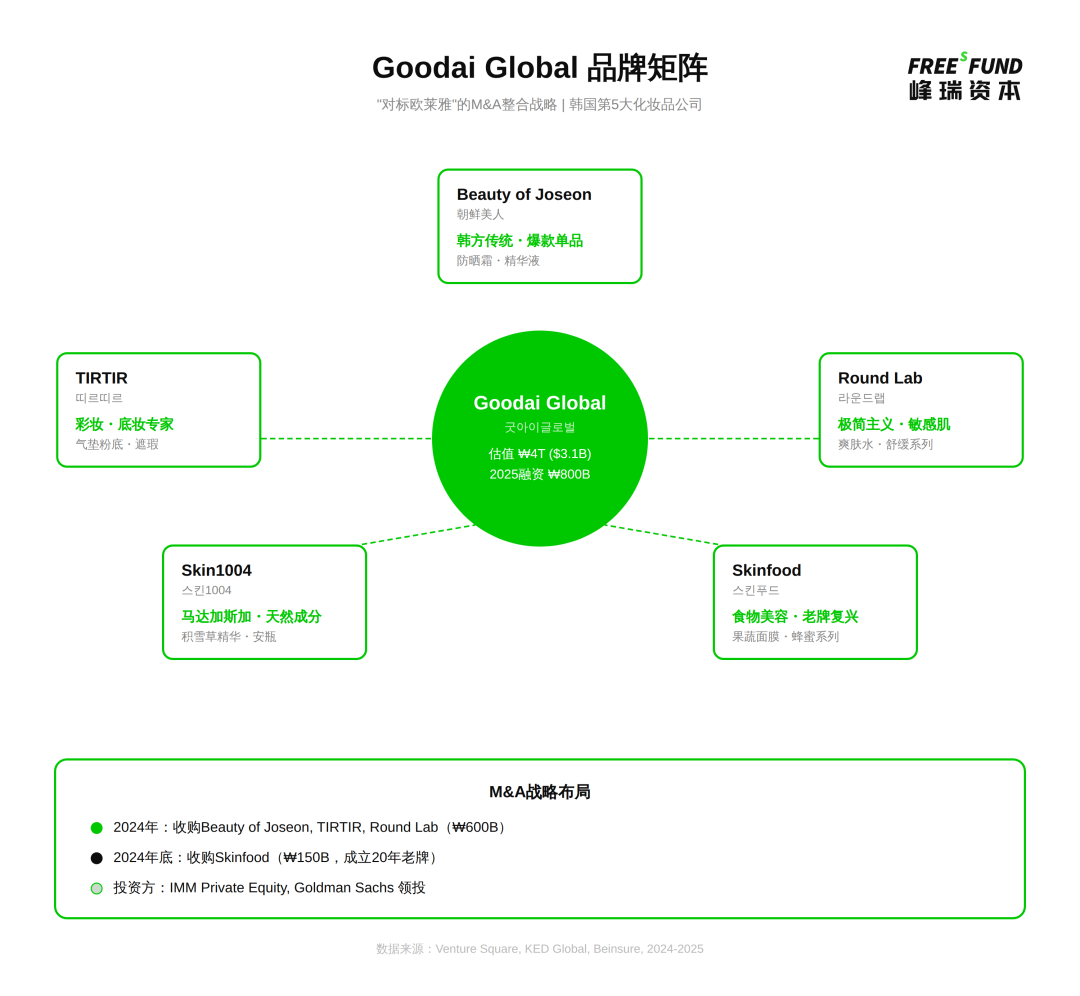

Goodai Global: The M&A Machine Benchmarking L'Oréal

The underlying logic of the longevity economy is: people are beginning to incorporate every organ of the body into "anti-aging management." As the human body's largest organ, skin is naturally the earliest point of entry for the longevity economy and where consumer perception is strongest. This explains why capital players like Goodai are frantically consolidating skincare brands — they are betting not merely on "beauty," but on "skin as organ-level anti-aging" as the consumer entry point of the longevity economy.

Founded in 2016, this company pursues an explicit "benchmark L'Oréal" strategy — building a brand matrix through rapid M&A. In the process of downgrading from serious medicine to consumer medicine, platforms like Goodai that control global channel traffic (such as TikTok and Amazon) often become the ultimate acquirer and global distributor of hardcore biotech. This is why capital assigns them such extraordinary cross-sector valuation premiums.

The explosive numbers are staggering. According to the Korea Economic Daily, in 2025 Goodai completed approximately $600 million in financing, reaching a valuation of $3.1 billion. Its 2024 operating revenue was $226 million, with operating profit of approximately $98.3 million — both metrics roughly doubled year-over-year. Even more dramatic was EBITDA growth: from $86.68 million in 2024 to a projected approximately $300 million in 2025 — a tripling. 2025 projected sales are expected to reach $1.2 billion.

Behind this growth rate lies an aggressive M&A strategy. According to the Korea Economic Daily: Goodai has assembled a collection of Korean brands that have exploded in overseas markets: Beauty of Joseon reconstructs traditional Korean ingredients through modern scientific research, precisely hitting global "ingredient-obsessed" consumers; TIRTIR holds a position in color cosmetics; Round Lab's Dokdo Toner became a blockbuster product, with its parent company Seorin acquired by Goodai in 2025 for approximately 600 billion won; the portfolio also includes Skin1004, House of Hur, and Laka Cosmetics. In September 2025, the company also formally completed the acquisition of Skinfood, Korea's first-generation independent beauty brand, for approximately 150 billion won.

Data sources: Venture Square, Business of Fashion, KED Global, 2024-2025

Goodai's capital backing is equally impressive: top Korean private equity firms including IMM Private Equity, JKL Partners, Premier Partners, Kiwoom Private Equity, and Company K Partners, plus Goldman Sachs.

As of 2025, Goodai has become South Korea's fifth-largest cosmetics company, trailing only Amorepacific, LG Household & Health Care, Kolmar, and Cosmax. What's notable is that this ranking was achieved despite an extremely high overseas revenue share — Goodai's main battlegrounds are Amazon and TikTok Shop, not traditional Korean domestic channels.

Data sources: Venture Square, KED Global, Beinsure, 2024-2025

Beyond Silicon Valley's underlying technology innovation and Korea's proven business models, the longevity economy is attracting capital across other major global markets. In Europe, for instance, research institutions in Switzerland and the UK are drawing significant venture investment focused on cellular anti-aging and regenerative medicine; in Japan, biotech companies specializing in extending healthy lifespan are becoming darlings of the Tokyo capital market, driven by demand from its aging society.

Four Interlocking Investment Drivers

Why is global capital suddenly pouring into medical aesthetics? Four mutually reinforcing forces are at work.

Driver 1: The Longevity Economy Explodes — A Trillion-Dollar Investment Opportunity

Global population aging creates demand not just for elder care, but for a trillion-dollar market in "healthy aging" and "skin longevity." This generation of consumers is no longer satisfied with surface-level cosmetic coverage — they want medical-grade anti-aging solutions backed by clinical data, with quantifiable, trackable improvements.

The core cognitive shift: from lifespan to healthspan.

Global healthy life expectancy is only 63.7 years, while average life expectancy is 73 — meaning people spend their final 9-10 years in illness. The longevity economy addresses how to live longer, healthily.

Why is skin the first inflection point?

From an investment perspective, skin longevity has three distinctive advantages:

-

Quantifiable results — skin aging is visible and measurable, unlike internal organ health that requires complex testing.

-

Clear regulatory pathway — "reduce wrinkles" and "improve elasticity" are clinical endpoints recognized by the FDA/CE, far easier to approve than "extend lifespan."

-

Strong willingness to pay — consumer anxiety about "looking old" drives high payment propensity.

Market size overview. Data source: compiled from public information.

More critically, consumer demographics are shifting: in China, those earning RMB 10,000-20,000 per month account for over 40% of medical aesthetics consumers; in the US, millennials are starting preventive treatments in their 30s. This is no longer exclusive to the wealthy — it's middle-class necessity.

This explains Classys's rapid growth: it is not a "beauty device company" but a "skin longevity infrastructure provider" — 70+ countries, 38,000+ devices, managing the "skin healthspan" of tens of thousands daily.

Technology breakthroughs, regulatory clarity, market scale, and consumption upgrades — all four elements have matured simultaneously. The ignition point for a trillion-dollar track has arrived.

Driver 2: The Recurring Revenue Business Model

Classys's EBRP model proves one thing: medical aesthetics is not a one-time transaction but an ongoing service. The "device + consumables" model creates high-stickiness, predictable cash flow — precisely the business model characteristics capital markets favor most.

Why is the "device + consumables" model a perfect match for the longevity economy? Because longevity management is not a one-time surgery but lifelong intervention and maintenance. Devices provide periodic energy stimulation or delivery channels, while consumables (such as peptides, exosomes, and other active ingredients) need to be replenished as high-frequency consumer goods. This "hardware opens the door, consumables drive repurchase" combination perfectly aligns with the long-term nature of anti-aging.

This model has been repeatedly validated globally. Intuitive Surgical's da Vinci surgical robot derives most profit from disposable instruments and annual service contracts; in medical aesthetics, Allergan's Botox and hyaluronic acid fillers require regular repeat injections, creating exceptionally high customer lifetime value. The core logic is consistent: initial sales establish the foundation, ongoing consumption generates rich cash flow.

Driver 3: The Regulatory Moat of Medical-Grade Standards

Medical devices that pass stringent certifications like FDA and CE MDR possess extremely high technical and regulatory barriers. This is not an advantage replicable through marketing or distribution channels, but a moat requiring years of R&D investment and clinical validation.

But what exactly do "years" mean? Let's look at a real timeline.

Classys's Ultraformer MPT took over five years from initiating R&D to obtaining CE MDR certification. During those five years, the company had to complete: preclinical animal studies, human safety testing, multi-center clinical trials, technical documentation preparation (typically tens of thousands of pages), third-party audits, and regulatory review. Any single step could be restarted from scratch if one data point fell short.

More brutally, the costs. According to FDA data, a Class II medical device (such as a HIFU device) requires average investment exceeding $30 million from R&D to approval, with regulatory-related costs accounting for 30-40%. For Class III high-risk devices, this figure can exceed $90 million. This doesn't include failure costs — the FDA's first-time approval rate for Class III devices is only 22%; most companies require 2-3 applications to gain approval.

From an investment perspective, this regulatory barrier creates a very interesting phenomenon: market concentration will continue to increase.

When entry barriers are sufficiently high, latecomers either choose costly head-to-head competition (rarely successful) or exit through acquisition. The medical device industry's consolidation trend is clear: giants like Johnson & Johnson and Medtronic build product portfolios through M&A, while smaller companies either become acquisition targets or dig deep in niche segments.

Classys's current strategy is clever: completing triple certifications (FDA/CE/KFDA) across three core technologies — HIFU, radiofrequency, and microneedling — creating a "technology platform + multi-market access" portfolio advantage. This means even if a single product faces competition, the company can still sustain growth through other product lines and markets — this resilience is precisely why investors are willing to assign higher valuation multiples.

Simply put: when others are still struggling for one certification, you already hold three passports. You're no longer playing the same game.

Driver 4: Crossover Valuation Premium — Standing at the Intersection of Three Trillion-Dollar Markets

The medical aesthetics industry sits at the intersection of medical technology, consumer goods, and biotechnology: it combines medical-grade technical depth (high barriers), consumer goods market scale (high ceiling), and biotechnology innovation potential (high growth). This "trinity" attribute enables it to command valuation multiples far exceeding traditional cosmetics.

Consider this comparison.

Traditional cosmetics: L'Oréal, for example, with a $200 billion market cap, trades at 30-35x P/E, with 4% growth in 2025. Mature, stable, but with a clear ceiling — how much face cream consumers buy annually is largely predictable.

Pure medical devices: Intuitive Surgical's da Vinci robot trades at 60-70x P/E, but serves the hospital market, constrained by health insurance policy and procurement budgets, with limited expansion speed.

Medical aesthetics technology, however, can capture upside from all three markets.

Dimension 1: Medical technology depth — building defensibility

Medical aesthetics requires FDA/CE certification, clinical data, and patent protection — advantages traditional cosmetics cannot quickly replicate, requiring building clinical trials, applying for certifications, and establishing physician training from scratch at enormous cost. This is why in August 2024, L'Oréal acquired a 10% stake in global medical aesthetics giant Galderma and established a strategic scientific partnership, seeking to cross barriers at maximum speed and rapidly enter the injectable aesthetics and therapeutic dermatology track. And in December 2025, L'Oréal, through its industry fund, made a major investment in Chinese dermatology pharmaceutical company Zhiyuan Pharmaceutical. This technical barrier gives medical aesthetics a "medical technology"-grade moat.

Dimension 2: Consumer goods market scale — opening the ceiling

But medical aesthetics, unlike medical devices, is not constrained by hospital budgets. Its customers are the billions of consumers globally pursuing beauty.

The key shift is from "hospital decision" to "consumer decision." Allergan's Botox, though a prescription drug, follows a consumption logic more like luxury goods — consumers ask about it proactively after seeing results, with doctors acting more as "service providers." This B2C attribute enabled Allergan's $63 billion acquisition in 2019, at a valuation far exceeding traditional pharmaceutical companies. APR/Medicube goes further: home beauty devices + patented serums, bypassing hospitals to reach consumers directly. First-half 2025 sales of $423 million, stock price up over 200%, P/E exceeding 50x — the growth speed of consumer electronics, the barriers of medical devices, the market of beauty products, at the intersection of all three.

What investors see is medical-grade barriers, but the ceiling is not "number of hospitals" — it's "number of global consumers."

Dimension 3: Biotechnology innovation potential — unleashing imagination

Most exciting is medical aesthetics becoming the fastest commercialization scene for cutting-edge biotechnology.

Peptide-drug conjugates (PDC technology) were originally developed for tumor-targeted therapy, finding a faster commercialization path in medical aesthetics. The technical sophistication is equivalent, but monetization is 3x faster (dermatology clinical trials 3-5 years vs. oncology drugs 10-15 years).

Stem cells and cellular reprogramming are also penetrating. After Altos Labs raised $3 billion, the most likely near-term commercialization is not "making 70-year-olds 40," but "restoring youthful state to skin cells" — lower regulatory barriers, higher consumer acceptance. Medical aesthetics is the vanguard testing ground for longevity technology.

When a company simultaneously possesses all three attributes, the evaluation framework changes: traditional cosmetics' ceiling is how many people globally buy face cream; pure medical devices' ceiling is how many surgeries globally; medical aesthetics technology's ceiling is how many people globally pursue youth × medical-grade premium × repeat consumption frequency.

This explains the "unreasonable" valuations:

Goodai Global: With EBITDA of roughly $100 million and a valuation of approximately $3 billion, it trades at 31x — far above the 10-15x typical for traditional cosmetics. The premium rests on a simple logic: capital markets recognize not just the consumer appeal of its five brands, but the medical credibility of its medical aesthetics pipeline and the innovation potential from prospective biotech acquisitions.

APR/Medicube: Less than ten years old, it briefly neared a $2 billion market cap with a P/E exceeding 50x. Under conventional "beauty device sales" logic, it would merit roughly 20x. But by building medical moats through patented RF technology, signaling biotech credibility through customized formulations, and layering consumer advantages through its direct-to-consumer model, it achieved a valuation leap across dimensions.

Classys: 2024 revenue of approximately $187 million, margins above 50%. By traditional medical device standards, fair value would sit at $3-4 billion. Yet factoring in its expansion potential to consumer markets and the possibility of future "drug-device combination" R&D, valuation headroom could widen another 50-100%.

The most telling comparison: Allergan commanded $63 billion in its acquisition, while Avon North America — a pure cosmetics play — fetched just $125 million. Both pursued "improving appearance," yet the valuation gap reached 500x.

In investors' eyes, medical aesthetics technology is not one industry but the intersection of three trillion-dollar markets. Whoever builds advantage at that intersection captures "crossover premium."

Why the Longevity Economy's Capital Wave Must Flow to Chinese Manufacturing

Classys has already designated China as its 2026 strategic priority. CEO Baek Seung-han's reasoning is direct: "China is a market with extremely high demand for medical aesthetics, at prices above Korea and the US. The licensing threshold is high, but the technology gap will be our opportunity."

But China is far more than a "market" — it is the destination for core technology transfer.

The "Skill Spillover" from Pharmaceutical CDMOs

This longevity economy wave must flow to China because of an unexpected convergence with Chinese pharmaceutical manufacturing capacity. Over the past five years, China's pharmaceutical CDMO sector underwent explosive expansion. Global orders for GLP-1 weight-loss drugs (semaglutide, tirzepatide), PD-1/PD-L1 immunotherapy, and ADC antibody-drug conjugates drove WuXi AppTec, Asymchem, Porton Pharma Solutions, and other leading CDMOs to rapidly expand capacity.

But after 2024, as global biotech financing tightened and major pharma companies cut R&D pipelines, CDMO order growth decelerated. The high-end capacity built for innovative drugs — peptide synthesis workshops, aseptic filling lines, nanotechnology platforms — did not vanish. It began searching for new applications.

The medical aesthetics technology boom arriving at this moment became a critical recipient, because the underlying technologies are strikingly similar:

-

The peptide synthesis that pharmaceutical CDMOs master is precisely the core of peptide-drug conjugate (PDC) transdermal delivery

-

GLP-1 drug sustained-release technology can be directly applied to continuous release in medical aesthetics products

-

ADC conjugation processes mirror the "drug-device combination" approach in medical aesthetics

-

Aseptic filling capabilities from biopharma are equally essential for medical aesthetics injectables

More critically, talent is migrating. Formulation scientists released from pharmaceutical companies, clinical researchers cultivated by CROs/CDMOs, and returning overseas talent from multinational pharma are entering medical aesthetics in large numbers — their experience with nanoemulsions, liposomes, and microsphere formulations is precisely what medical aesthetics technology needs most.

China's Distinctive Advantage: Abundant Capacity + Deep Industrial Chain Foundation

While Silicon Valley develops PDC delivery technology and cellular reprogramming, China possesses the complete ecosystem to rapidly industrialize these innovations:

1. Capacity abundance without redundant investment: China has become the global core manufacturing base for peptide APIs. Looking at overall API capacity, China handles over 60% of global manufacturing; in custom peptide synthesis specifically, China accounts for roughly 65% of global capacity. The massive expansion driven by the GLP-1 boom, combined with demand falling short of expectations, has pushed utilization rates below 60% at smaller peptide CDMOs while leading enterprises maintain around 85% — clear bifurcation, with substantial capacity urgently seeking new applications.

- ADC conjugation platforms and pre-filled syringe lines can both take medical aesthetics orders. Most critically, these are FDA/NMPA-standard GMP-certified facilities, ready for direct conversion.

3. CRO capabilities covering the full process with cost and efficiency gains: Domestic CROs span pharmacokinetic studies (PK/PD), skin irritation testing, preclinical safety evaluation, and Phase I-III clinical trial management. Compared to Europe and America, costs are 50-60% lower, speed 50-70% faster, with clinical trial center networks covering the entire country and high subject recruitment efficiency.

4. Extreme supply chain completeness: From hyaluronic acid, collagen, and other medical aesthetics raw materials, to microneedle patches, syringes, and other devices, to packaging materials and cold-chain logistics — no second country globally can complete every step from R&D to mass production of a medical aesthetics product within a two-hour high-speed rail radius. Take the Yangtze River Delta as an example: Suzhou has CDMO clusters (peptide synthesis, formulation development), Shanghai has CROs and clinical research centers, Zhejiang has medical device production bases, Jiangsu has API suppliers — a PDC transdermal product can move from concept to clinical batch production entirely within a 200-kilometer radius.

Synthesizing the trend analysis above, I believe "Silicon Valley innovation + Chinese manufacturing + global markets" is emerging as the new paradigm in the "skin longevity" space. This synergy represents deep integration of innovation ecosystems:

-

Silicon Valley excels at 0-to-1 breakthroughs — molecular design at Stanford and MIT, cellular reprogramming research at Retro/Altos, and so on.

-

China's ecosystem handles 1-to-100 scale-up — CDMO process optimization and mass production (cost reduction of 50-70%, cycle compression of 30-40%), rapid clinical validation through CROs, and cost control through complete supply chains.

-

Global markets handle validation and monetization — FDA/CE/KFDA triple certification, covering markets in Europe, America, Japan, Korea, and China.

From this perspective, China in the global "skin longevity" race has every opportunity to complement Korea's equipment-side advantages: Korea provides FDA/CE-certified energy devices (such as Classys's HIFU, RF), China provides GMP-standard bioactive formulations (peptides, growth factors, nanocarriers), and together they form "drug-device combination products" that jointly define next-generation global medical aesthetics standards.

This is not the old narrative of "China can only do contract manufacturing," but a new pattern of "Chinese capacity absorbing Silicon Valley innovation." When pharmaceutical CDMO overcapacity meets the commercialization demands of longevity technology, a new trillion-dollar industry is quietly taking shape in China.

Conclusion: Where Are the 100x Returns?

The longevity economy is no longer a "nice to have" consumption upgrade story, but a "must have" medical technology track.

From Classys's energy device infrastructure, to APR's drug-device closed loop, to Goodai Global's brand empire; from molecular innovation in transdermal delivery, to AI-driven precision diagnostics, the medical aesthetics industry is undergoing a paradigm revolution driven by technology, capital integration, and regulatory upgrading.

For global investors, the question is no longer "whether to invest in medical aesthetics," but "how to identify the next 100x return target across dimensions of devices, molecules, brands, and channels."

The endpoint of medical aesthetics is no longer marketing concepts, but clinical evidence and serious medicine. As the first barrier against aging, skin will prove: the depth of science ultimately determines the length of beauty.

This article represents the author's personal views only, not the position of FreeS Fund, and does not constitute investment advice.