The Rise and Fall of Education, Consumer Bubbles, Carbon Neutrality, Commercial Spaceflight... "Cool" Reflections on Hot Investment Topics | Li Feng Column

Exploring Opportunities Amid "Major Restructuring"

At a recent FreeS Fund "e-Salon · Harvard Special," Feng Shu (Li Feng) sat down with Chinese students from top overseas universities and tech industry professionals for a conversation on entrepreneurship and investing, as always. We've pulled out some of the most interesting discussion topics to share with you:

- Where do opportunities lie for education startups under heavy regulation?

- Under carbon neutrality policies, which types of enterprises deserve attention?

- Why does the consumer sector remain hot for investment despite constant IPO underpricing? Why do some consumer brands see valuation inversions between primary and secondary markets?

- With American billionaires' space ventures heating up, how should we view the prospects for China's commercial aerospace industry?

Before diving in, here are the key takeaways:

- In China, the three most important foundational service industries are finance, education, and healthcare. Internet healthcare and internet finance both experienced explosive growth, faced tightening regulation, and then found long-term development opportunities. Will education follow the same path?

- Most of the "carbon" in "carbon neutrality" comes from steel, cement, and plastic manufacturing — and China accounts for an outsized share of global production capacity in all three. This means one highly promising application for synthetic biology in China is replacing these traditional chemical materials.

- Bubbles exist in consumer sectors for multiple reasons. While countless brands can make the journey from 0 to 1, how many of these new brands can ultimately grow into large brand companies remains an open question.

- Starting in the late 1990s, NASA turned to large-scale outsourcing to adapt to budget cuts. This is the backdrop against which private enterprises developed in America's aerospace sector. China's difference is that we haven't yet seen large-scale "military-to-civilian" conversion at this stage. The upside is that policies now encourage private enterprises to explore technologies in the name of fostering technological innovation.

We hope this offers fresh perspectives.

Event Preview

The FreeS e-Salon is a regular small-scale online closed-door meeting. The first three sessions primarily included Chinese students from prestigious overseas universities and tech industry professionals. At e-Salons, we get straight to the point and speak freely. Topics you care about or raise related to entrepreneurship and investing may well be discussed. The salon is invitation-only, though we reserve a limited number of seats each session — welcome to scan the QR code to register and join Feng Shu face-to-face.

A Token of Appreciation

In this article, Feng Shu shares his thinking on education, carbon neutrality, consumer sectors, and commercial aerospace. We also welcome your observations and thoughts on these topics in the comments below. We'll give FreeS Fund's custom 6th anniversary T-shirts to the 4 readers with the most thoughtful comments. (Deadline: 9:00 PM, September 16)

/ 01 / After a Heavy Regulation Cycle, Education Opportunities Lie in Connecting and Serving Between the Core Layer and Consumers

Question 1: I run an education startup focused on online academic and competition tutoring. The education sector has attracted considerable attention lately, and anxiety is widespread within the industry. I'd like to ask Feng Shu: will recent policy changes affect your investment strategy for the education track? And what types of education companies do you currently favor?

Li Feng: In China, the three most important foundational service industries are finance, education, and healthcare. These three sectors may be at different stages currently, but they've all followed broadly similar paths. So to explore education's future, let's first look at how finance and healthcare developed in China — both experienced explosive industry growth, faced tightening regulation, and then found long-term development opportunities. Will education follow suit?

Let's start with internet healthcare. Here's a brief recap of its policy phases:

- 2011–2015: Riding favorable policy winds, vigorous growth

As internet healthcare entered the mobile era, apps including Chunyu Doctor and Haodf.com launched one after another. In 2015, propelled by policies vigorously promoting "Internet Plus," the internet healthcare industry saw substantial development.

- 2016–2017: Policy chill, tightening regulation

In July 2016, the state ended pilot programs for third-party pharmaceutical e-commerce platforms, shutting down previously approved platforms. That same year, in a draft for comment, the China Food and Drug Administration proposed explicitly stipulating that retail enterprises could not sell prescription drugs online.

- 2018 to present: Standardized development, opportunities emerge

Starting in 2018, industry-related policies began warming up. The National Health Commission issued detailed regulations on market access, practice standards, and supervision for internet hospitals, internet diagnosis and treatment, and telemedicine services. Policies gradually aligned, and the industry outlook clarified. By June 2021, there were over 1,600 internet hospitals nationwide.

2020's pandemic prevention and control measures accelerated the policy framework's refinement for internet hospitals, which is now gradually transitioning from framework establishment to detailed design. According to incomplete statistics from Arterial Network, as of June 30, 2020, 71 internet hospitals had connected to medical insurance during the pandemic — mostly public hospital internet hospitals, but also including enterprise-led internet hospitals from WeDoctor, Ping An Healthcare and Technology Company Limited, and Medlinker.

At the end of 2015 and beginning of 2016, shortly after FreeS Fund was founded, we invested in two internet healthcare-related projects. Our rationale then was that we saw a massive chasm between supply and demand in healthcare.

On one hand, China was gradually advancing universal health insurance, and public health awareness was strengthening as living standards rose. On the other hand, China's core diagnostic and treatment resources were relatively concentrated in the tertiary medical system, and as the "serious illness stays at the county" policy accelerated, the uneven distribution of medical resources became increasingly pronounced. Where supply-demand gaps exist, entrepreneurial opportunities follow.

We saw two layers of opportunity at the time: the service layer and the efficiency layer. In short, it was about how to match patients with appropriate doctors and provide patients with diagnostic and service functions that allowed certain problems to be well addressed without hospital visits. The two internet healthcare projects we invested in aimed to solve these issues. They weathered the policy winter of 2016–2017, eventually waiting out until the 2018 policy thaw, and have been operating quite well ever since.

Why did the "policy thaw" arrive starting in 2018? An important reason is that the two problems we initially identified remained unresolved: the massive numerical imbalance between doctors and patients, and the further amplification of the contradiction between demand and resource allocation as public health awareness improved. The gap between supply and demand couldn't be bridged — whether this gap manifested as triage, referral, general practice consultation, or over-the-counter drug delivery... If tertiary hospitals or community clinics couldn't fully bear the load, it would ultimately be returned to the market, relying on market forces to add more stratification and grading, raising service levels and capabilities. So the market began opening in an orderly fashion.

To summarize, in internet healthcare, the broad trend is liberalization, leaving room for innovation, but implementation proceeds step by step.

The financial sector followed a similar pattern.

Here's a brief recap of internet finance's policy phases —

- 2013–2016: Wild expansion, mixed quality

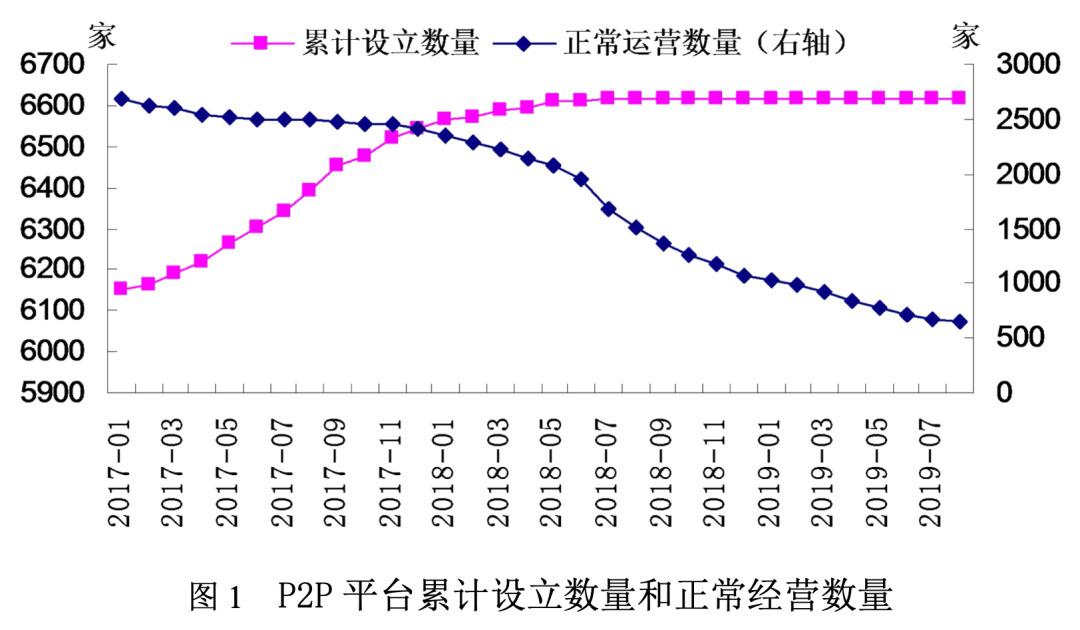

As one product of internet finance innovation, P2P lending platforms began emerging domestically in 2006–2007 and grew explosively around 2013. Citing Hong Kong financial information service provider Finet's reporting, in 2013 there were roughly 800 P2P lending platforms nationwide, but by 2015 this number had surged to 3,844. A report from ICBC City Finance Research Institute showed that from 2013 to 2016, the P2P industry's annual transaction volume growth rate remained above 100%.

▲ Image source: "ICBC City Finance Research Institute Report: Viewing the P2P Lending Industry Through the 'Pioneer Group' Incident"

- 2016–2020: Regulatory cycle

The consequences of wild expansion were that the drawbacks of online lending gradually emerged and industry chaos proliferated. According to the "2016 China P2P Lending Annual Report" published by 01 Think Tank, by the end of 2016, problematic and transitioning P2P platforms had reached 3,231, accounting for 67% of the industry's cumulative total. Per reporting by EO Company, in 2018, 580 P2P lending platforms collapsed, with investors suffering heavy losses.

Policies began taking active measures. One important event was the 2017 19th Party Congress report proposing to improve the financial regulatory system and guard against systemic financial risk.

By January 2020, the central bank announced that the 2020 battle to prevent and defuse financial risks had achieved important phased results: P2P platforms had been completely eliminated, and various high-risk financial institutions had been orderly disposed of.

- Third quarter 2020 to present: Return to positive track

Many assumed that after heavy regulation, the private financial industry had disappeared, particularly in internet finance. This wasn't actually the case. Some U.S.-listed internet finance companies, including 360 DigiTech, CreditEase, and FinVolution (PPDAI), while divesting from P2P businesses, continued operating financial-related businesses and are doing quite well.

Take 360 DigiTech as an example. In Q1 this year, net profit reached 1.3 billion yuan, up 6.4x year-over-year; Q2 net profit reached 1.548 billion yuan, up 76.6% year-over-year.

What happened in internet finance parallels what occurred in internet healthcare.

Although at P2P's peak, its annual transaction scale (3 trillion yuan) was still "small potatoes" relative to total assets held by banks, these internet finance platforms possessed scenarios, data, and large customer bases — essentially directly touching the core of the financial system.

Although the state subsequently implemented strict financial regulation on internet platforms, after market education through P2P and internet finance, user demand had actually been cultivated. And the pandemic further drove online demand, with banks increasingly feeling their inadequacy in connecting consumer demand with services.

Licensed financial institutions including banks and insurance companies can provide core system functions like fund aggregation and centralized risk control, but gaps remain between them and consumer needs (including individual consumers, households, and micro/small enterprises). These gaps create space and efficiency for service and connection — which is also the development space for financial innovation.

In recent years, financial innovation developing under regulatory premises has been the main theme. Although internet finance companies face strict regulation on business scope, their efficiency in connecting with consumers and markets remains. They can channel this connection efficiency and service to licensed fund aggregators, becoming loan assistance providers. Previously, when they handled fund aggregation themselves, they bore risk control responsibility; now they don't touch risk control, only doing matching and service between capital and various consumer needs, instead transforming into asset-light companies more welcomed by capital markets. This is why many internet finance enterprises have been able to return to positive tracks with outstanding performance.

Education will most likely follow the same pattern.

In recent years, online education overheated, especially since the pandemic, then plummeted due to recent heavy regulation. If we reference the development patterns of healthcare and finance, we're inclined to believe education will eventually emerge from its "deep winter."

If we view full-time schooling as the core system of the education sector, after experiencing a strict regulation cycle, unbridgeable gaps between the core system and consumer demand — such as service links and specific resource allocation — will still need bridging by the market or innovative enterprises.

What's worth noting is that when entrepreneurial companies innovate and serve at this layer, they'd best avoid interfering with the core layer. Just as fund aggregation is the core layer of the financial system, and hospitals at various levels are the core layer of universal healthcare-related diagnosis and treatment, full-time schooling is the core layer of the education sector. Innovation by education sector enterprises should revolve around connection and service between the core layer and consumers.

In fact, over a decade ago, both New Oriental and TAL Education were doing supplementation and service outside the core layer. However, after 20 years of offline training industry development, 10 years of online education development, and especially the high-speed expansion of the past two to three years and during the pandemic, much extracurricular tutoring actually excessively interfered with full-time stage school education. But consumer habits cultivated during the industry's explosive and expansionary period, and the gap between demand and the core system, won't suddenly disappear completely because of regulation.

So looking ahead, a major opportunity for education startups lies in not interfering with the core layer, but doing the connection layer well. Broken down, this means two things: either you do customer experience and service well; or you further improve the allocation efficiency of educational resources.

For example, FreeS previously invested in an education project called "Onion Academy," whose characteristics include: no live teachers, using animation to break down knowledge, with some AI-based personalized content combinations. Two-thirds of Onion Academy's users come from school and teacher recommendations. Because each lesson is very short, with content matching full-time classroom content, it can serve preview, review, and difficult-point self-testing functions, while also stimulating student interest. It doesn't affect the core layer; instead, it does well the connection and service between the core layer and consumer needs. We're inclined to believe such projects will actually see better development after the heavy regulation cycle passes.

▲ Image source: Onion Academy APP

Of course, for the education industry, it's difficult to predict how long this regulation cycle will last, but the story arc will most likely mirror finance and healthcare. When the inflection point arrives, the entire industry will actually see greater efficiency improvements.

However, to survive the current difficult period, vocational education will likely become a red ocean. Because many companies that still hold substantial capital and wish to continue in education may choose vocational education as a transition, waiting for the policy turn.

/ 02 / "Carbon Neutrality" Will Bring Entrepreneurial Opportunities to Synthetic Biology and Other Fields

Question 2: I work in the strategic investment department of a multinational energy company, primarily focusing on smart logistics, energy technology, and the intersection of energy and fintech. Carbon neutrality has been much discussed lately — I'd like to ask Feng Shu how the current policy status and trends around carbon neutrality will affect related field investments?

Li Feng: Let's first look at where the "carbon" in "carbon neutrality" mainly comes from. Bill Gates's book How to Avoid a Climate Disaster mentions that globally, about 51 billion tons of greenhouse gases are emitted into the atmosphere annually. Of this, production and manufacturing total emissions (including steel, cement, plastic manufacturing, etc.) account for the highest share at 31%. Electricity production and storage is second at 27%. Planting and breeding, and transportation rank third and fourth at 19% and 16% respectively.

Looking at China, China's current steel production accounts for 56.5% of world total output, cement production accounts for 58.5%, and petrochemicals account for 40% of global market share. Because China's production capacity share is so high in these three categories — steel, cement, and plastic — although in the short term for carbon reduction we can push on clean energy and new energy vehicles, in the long term, achieving carbon neutrality ultimately cannot bypass these three major items in steel, cement, and plastic manufacturing.

And within this process lie entrepreneurial opportunities — for instance, synthetic biology. Synthetic biology, simply put, uses bacteria, enzymes, or microorganisms to complete carbon chain decomposition and transfer processes. Before gene editing technology emerged, synthetic biology research was very difficult, because even if researchers could calculate what kind of bacteria or enzymes were needed, obtaining them from nature was extremely hard. But in recent years, as synthetic biology paired with gene editing technology has developed, breakthroughs in obtaining bacteria, enzymes, or microorganisms have been substantial — researchers can accelerate strain discovery or even create needed strains, enormously improving synthetic biology's efficiency and developing it into a platform technology.

Currently in China, synthetic biology has several uses: first, material substitution, mainly traditional chemical material replacement; second, synthesizing natural extracts; third, producing pharmaceutical intermediates — certain chemical raw materials or chemical products used in drug synthesis processes.

Combined with carbon neutrality policy, one highly promising market application for synthetic biology is traditional chemical material substitution, and in China there's also a sufficiently large market.

Take FreeS Fund's angel-round company Bluepha as an example. Bluepha is a company based on "biotechnology + industrial internet" engaged in molecular and material innovation. Bluepha has developed industrial production technology for the biodegradable material PHA, systematically reducing PHA production costs. PHA material is widely used in agriculture, environmental protection, biochemicals, microelectronic materials, energy, medicine, medical materials, and other fields, and can spontaneously degrade in natural environments including soil and seawater.

▲ Granular PHA raw material and products. Image source: Bluepha

Notably, there's been a special backdrop these past two years: global monetary oversupply has brought global inflation, triggering commodity price increases. Rising oil prices lead to petrochemical products becoming more expensive. Originally, petrochemical product substitutes manufactured through synthetic biology were priced higher than petrochemical products themselves, but affected by commodity price increases, the "green premium" relatively decreases, even reaching "green price parity." So we can judge that synthetic biology will next welcome an even more special and enormous market opportunity.

FreeS Partner Ma Rui shares breakthroughs and progress at biomedical enterprises including Bluepha

Click to watch 👆

/ 03 / Bubbles in the Consumer Track: From 0 to 1 Is Easier, From 1 to Scale Is Harder

Question 3: I'd like to ask Feng Shu about the primary-secondary market valuation inversion issue. Many projects are highly sought-after in primary markets, yet immediately fall below issue price upon listing. Yet even with numerous cautionary tales, consumer sectors remain hot for investment — some brands are even valued at 100 million per store. How does Feng Shu view this phenomenon?

Li Feng: Bubbles certainly exist in consumer sectors, and there are multiple reasons behind this.

First, affected by the pandemic, many offline stores had to close due to operating difficulties. Large numbers of vacant shops faced re-leasing. Those entering the market at this time were often people just starting chains, or those who'd received funding and wanted to expand. Because supply increased substantially and rents decreased, many brands encountered favorable expansion opportunities.

Second, from an investment perspective. Before the pandemic, after several rounds of "trend" baptism, people generally felt there was nothing left to invest in the internet industry, and many began turning back to consumer sectors. (Welcome to click the blue link to revisit "Li Feng: Will Consumer Investment Continue to Be Hot in 2021? | FreeS Research Institute") One very interesting phenomenon: in just two months recently, seven or eight chain noodle shops received investment from well-known investment institutions — several Lanzhou noodle brands alone successfully raised funding.

Third, the consumer track's popularity also relates to the rise of online new brands. Since 2019, starting with Douyin, platforms' traffic distribution mechanisms began shifting from search to recommendation. The result was that user tags became more numerous and more granular, also causing products or brands to become increasingly niche to adapt to new traffic distribution mechanisms — the closer your product aligns with user tags, the easier you can precisely reach effective users.

But for brands, this change has pros and cons. The pro is that going from 0 to 1 is relatively easy; the con is that continuing to scale from 1 onward becomes much harder. To achieve scale requires category expansion, user demographic expansion, brand promotion and marketing expansion — facing greater challenges and burning through substantial cash.

So this explains why many small, beautiful brands suddenly emerged, attracting capital attention. However, while countless brands can achieve 0 to 1, how many new brands can ultimately incubate into sufficiently large brand companies remains an open question.

Of course, we've always said that looking long-term, China will birth many world-class brands representing China. What needs consideration is which brands can ultimately break out. From our current investment observations, those rising new consumer brands that sustain their ascent all leverage China's supply chain characteristics and advantages, all seize market demand changes and make rapid responses relying on supply chains, and all can evoke higher emotional value from users.

Feng Shu interprets consumer brands' path from 0 to 1, from 1 to 100

Click to watch 👆

/ 04 / Commercial Aerospace: China and America's Commercial Aerospace Development Contexts Are Completely Different

Question 4: Recently Branson and Bezos successively experienced suborbital flight, with American billionaires' space venture competition heating up — how does Feng Shu view space travel and the development prospects for China's commercial aerospace?

Li Feng: Commercial aerospace is quite an interesting direction. However, relatively speaking, China's commercial aerospace and America's commercial aerospace have completely different development contexts.

Let's briefly review American commercial aerospace's development. In the 1950s–60s, the U.S. and USSR launched the "Space Race." To counter the Soviet space program, America increased investment in space-related technology, and NASA developed rapidly after its 1958 establishment. However, with the 1991 Soviet collapse, the 40-plus-year U.S.-Soviet arms race ended. NASA's fiscal allocations subsequently declined. Starting in the late 1990s, to adapt to budget cuts, NASA turned to large-scale outsourcing. This is precisely the backdrop against which private enterprises developed in America's aerospace sector.

China's difference is that at this stage, we haven't yet seen large-scale "military-to-civilian" conversion. The upside is that, out of encouraging technological innovation, policies now encourage private enterprises' technology exploration. FreeS Fund's angel-round company Jiuzhou Yunjian was founded against this broad backdrop.

▲ Image source: Jiuzhou Yunjian official website

Jiuzhou Yunjian focuses on liquid oxygen methane rocket engine design and R&D, assembly testing, and full-process supporting flight services. From a team composition perspective, most have "national team" industry backgrounds and full-process development experience, having received many awards including National Defense Science and Technology Progress Awards and Military Science and Technology Progress Awards. From a customer composition perspective, including aerospace and military industry research institutes, universities, and machinery/chemical central state-owned enterprises are all important customers for its engines and component parts.

A Token of Appreciation

In this article, Feng Shu shares his thinking on education, carbon neutrality, consumer sectors, and commercial aerospace. We also welcome your observations and thoughts on these topics in the comments below. We'll give FreeS Fund's custom 6th anniversary T-shirts to the 4 readers with the most thoughtful comments. (Deadline: 9:00 PM, September 16)

Star-follow the FreeS Fund WeChat official account — first-hand industry research to share with you

Li Feng: Will Consumer Investment Continue to Be Hot in 2021? | FreeS Research Institute