The Rise of Crayfish, Latiao, and Pickled Pepper Chicken Feet: Why Mala Took Over China | Frees Fund

"Spicy" is the engine that drives hit snack products.

What's the Next "Mala" Breakout Hit?

You can't escape the heat. Of the 600,000 tons of crayfish China produces annually, the dominant flavor is mala — numbing-spicy. The same goes for internet-famous snacks like latiao (spicy strips) and pickled chili chicken feet. Their core selling point is always "spicy."

This month, Xinliangji — a restaurant supply chain brand in FreeS Fund's portfolio — closed a RMB 120 million Series A+ round, with FreeS Fund continuing to follow on. Among Xinliangji's standardized product lineup, crayfish, spicy crabs, spicy bullfrogs, and finger-licking river snails all share that mala connection.

Why does mala have the power to turn casual foods into runaway hits? Why did duck neck, crayfish, latiao, and chicken feet become the first categories to develop recognizable brands? And beyond these, which other spicy foods hold similar branding potential? This piece might offer some answers.

The Rise of Pickled Chili Chicken Feet, Zhou Hei Ya, and Crayfish: Why Mala Conquered China

By / Longmaojun

Source / New Consumer Insights

Why Does "Spicy" Drive Breakout Products?

Mala's dominance across China comes down to several factors:

▍Easy access to raw materials

Chinese taste theory recognizes five basic flavors: sour, sweet, bitter, spicy, and salty. All can be derived from cultivated plants. Sour comes from fermentation and vinegar production; sweet from sugars in certain roots and tubers.

Chili peppers arrived in China from the Americas, took root in the southwest, and grew without issue. Later, Chinese farmers developed new varieties like Chongqing's Chaotianhong. Large-scale chili cultivation laid the groundwork for spiciness to spread.

▍High mobility in source markets

Without debating which Chinese regional cuisine is most mainstream, it's undeniable that Sichuan food leads in popular appeal — dishes like twice-cooked pork and boiled fish have become national staples. A key reason: Sichuan, the cuisine's home base, is a major source of migrant labor. The seven chili-loving regions — Hubei, Hunan, Jiangxi, Sichuan, Yunnan, Guizhou, and Chongqing — account for over 40% of China's labor outflow.

As workers migrated to Beijing, Shanghai, Guangzhou, and Shenzhen, clustering effects took hold. "Spicy" as a food culture traveled nationwide.

The spread happened in two stages:

- Importing demand for spicy food. In commercial society, demand markets correlate with population density. The influx of spice-loving people naturally drove growth in Sichuan restaurants and related supply.

- Chef migration + dissemination of Sichuan cooking techniques. Sichuan cuisine also happens to be relatively simple and accessible to learn compared to other regional styles.

Rising demand plus expanding supply creates new markets.

▍Spicy preparation is forgiving of ingredient quality

Food lovers widely recognize that the finer the ingredient, the more "original flavor" matters in preparation. This approach prizes bringing out the food's essential taste with minimal seasoning — think high-end Japanese cuisine. But it's also demanding on ingredients, driving up costs. At the other end, cheaper ingredients rely more on seasoning and technique to taste good. Spicy preparation doesn't require peak freshness and can even mask flaws in the underlying ingredient.

These three factors give any spicy product a naturally broad user base — the market needs no education.

Why Did Pickled Chili Chicken Feet, Spicy Duck Neck, Crayfish, and Latiao Become Breakout Hits?

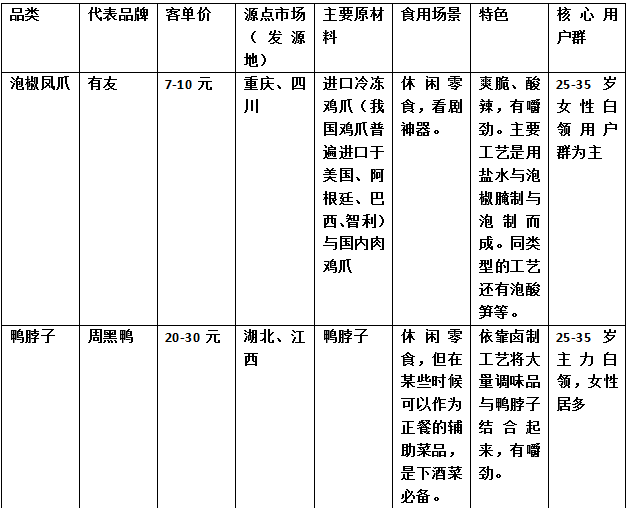

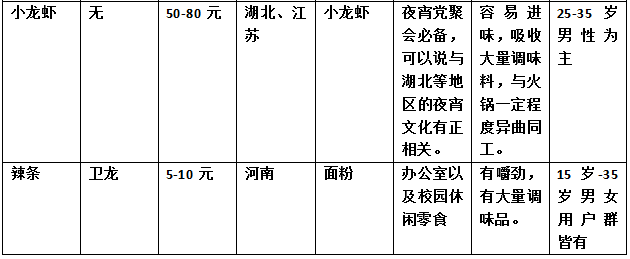

We analyzed these categories across several dimensions: representative brands, average ticket size, place of origin, raw materials, consumption scenarios, distinguishing features, and core user groups:

From this comparison, several key conclusions emerge:

▍These products have remarkably long lifecycles — 10 years at minimum, up to 20

Their recent rise to mainstream awareness stems mainly from social media in the mobile internet era spreading what were once regionally confined products to all demographics. The emergence of prominent brands further amplified these categories.

▍Average ticket prices are generally low

Huangmenji chicken, Shaxian snacks, and Jiangxi clay pot soup — all positioned toward low-income urban and rural workers — sit in the RMB 15 range. Interestingly, Zhou Hei Ya, Weilong latiao, crayfish, and pickled chili chicken feet cluster in the same bracket. Because these come in small individual portions, users often buy multiples or combo packs, pushing actual spending to roughly RMB 50.

Low pricing strategically maximizes the potential user base. For mass consumer goods, the faster you get people to try and understand your product, the easier it is to occupy their mental shelf space. Once users form the impression that "you are the category," competitors face extremely long odds.

Low pricing has another advantage. Once you've built scale and channel barriers, survival becomes difficult for competitors in that price range. The only way to compete is undercutting on price, but first movers generally hold major advantages in channels and production capacity. Rivals need both the capital base and the distribution network to absorb that volume — no easy feat.

▍Core users are 25–35, the prime spending demographic

There's a saying: "Men eat shrimp, women eat feet." Summer evenings with cold beer, crayfish, and conversation represent the preferred gathering scenario for male consumers. Meanwhile, pickled chili chicken feet and Weilong latiao have evolved from elementary school snacks to white-collar treats. The kids who loved latiao grew up, and certain subcultures became mainstream. This hints at the massive opportunity lurking in the casual snack market.

▍Key characteristics: mala and crisp texture

Numbing and spicy create mild tingling; crisp texture comes from food friction against teeth — like tripe soaked in hot pot broth meeting your molars. Chinese palates have an innate preference for this sensation.

Analyzing from external factors, we can examine social trends, user psychology, and business model viability. Social trends create herd mentality; user psychology explains why people choose these products; sound business models ensure these products reach users in viable form.

▍Social trends perspective

Economic pressure and suffocating urban environments drive white-collar workers to stimulate their mental state through spice. Overtime culture and late-night eating culture have also boosted these products.

Late-night eating deserves special attention. It's not just about the food — it's about emotional connection. This requires food that stretches out time. The once-popular sunflower seed culture worked because seeds kill time; you can't finish them instantly. Similarly, crayfish require shelling, chicken feet demand extensive gnawing, and duck neck needs constant nibbling. (One theory for crayfish's social appeal: your hands get too greasy to use your phone, so you're forced to focus on your companions.) Latiao is the exception — it's pure snack culture with little social element.

▲ Shelling crayfish takes time. "Eating slowly" gives the food social properties.

Also, if everyone around you loves spice, you eventually join in or risk social isolation.

▍User psychology perspective

- Emotional transfer and nostalgia. Food isn't just sustenance; it carries special meaning. Many overseas students reach for Lao Gan Ma chili sauce at meals. These products evoke hometown and childhood flavors. Latiao's popularity carries a distinctly retro sentiment.

- Addiction. Sweet, sour, bitter, and salty are relatively mild stimulants, but spice creates slight pain that becomes addictive.

- Spice gives these products long shelf life without spoilage and makes them highly portable. This enables nationwide mass distribution and rich consumption scenarios.

- Urban dwellers release pressure through spicy food. Watching shows is one relaxation method; eating pickled chili chicken feet is another way to trigger pleasure through elevated heart rate and sweating — similar to the dopamine release from exercise.

- Low pricing enables repeat purchase. For mass consumer goods, no repeat purchase means no brand loyalty. Low-priced, addictive products are the categories most likely to drive repeat purchase desire.

▍Business model perspective

- Low pricing depends on low-cost ingredient selection. Pickled chili chicken feet centers on "pickled chilies + chicken feet" — frozen chicken feet cost almost nothing. Major exporters like the US and Argentina don't eat chicken feet, enabling massive, cheap exports to China. China itself is also a major poultry producer; chicken and duck are among the cheapest meats. Crayfish is the sole exception — inherently low-cost, but demand inflation in recent years has driven up prices.

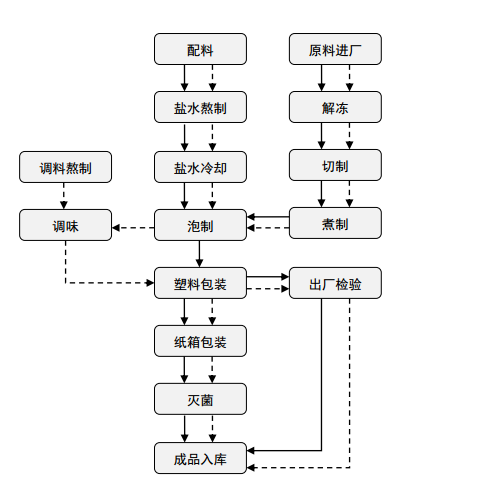

- Production standardization enables mass manufacturing.

▲ Steps in making pickled chili chicken feet.

- Local industrial policy support and clustering effects. In Qianjiang, Hubei and Xuyi, Jiangsu, government promotion and support have scaled and formalized the crayfish industry chain.

- Key figure promotion. Xu Jianzhong, inventor of thirteen-spice crayfish; Li Daijun, who pioneered oil-braised crayfish; Chen Lirong, who brought oil-braised crayfish to Beijing — all were critical catalysts in this chain. Without these ignition points, these products might have remained regional curiosities.

- Leading brands igniting categories. These products existed long before — braised duck neck has deep roots in Wuhan — but only when key brands emerged did the industry standardize, scale, brand itself, and build distribution systems.

- Key preparation method improvements and technical innovation. Zhou Hei Ya's creative "fresh-keeping" packaging, for instance, solved how duck neck could flow nationwide.

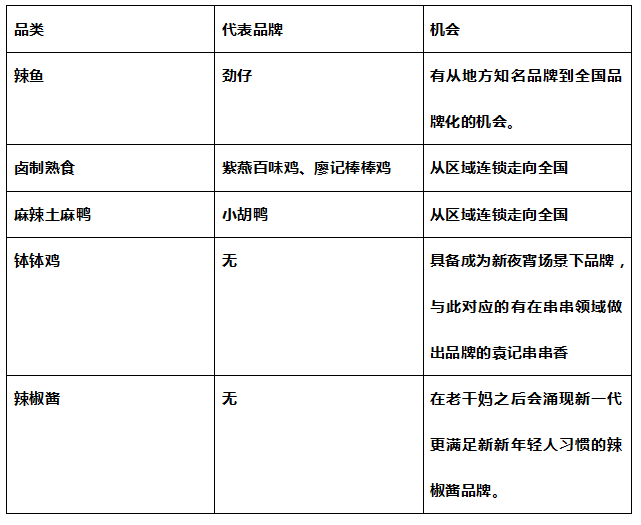

Which Spicy Foods Hold Similar Opportunity?

We'll throw out some ideas on which regionally distinctive "spicy" foods in the casual snack space might hold similar potential.

- Regionally distinctive brands have the potential to become national chains.

- In vertical categories with established demand but no dominant brand, new product opportunities can emerge around consumption scenarios — overtime work, gatherings, social occasions, and others all offer openings for new casual snacks.

- Brands targeting specific demographics and emotional needs hold opportunity. As urban "empty nest youth" multiply, snack brands serving this population will continue emerging.

- New channel opportunities. Bestore's rise validated new channel potential, but dedicated casual food stores or specialty channels focused on mala and other niche segments have yet to appear.

In short, the mala-centered casual food space holds massive, underexplored opportunity.

(This article originally appeared in New Consumer Insights. Feel free to share to your Moments.)

▲ Feng Li x Li Jian: Behind Crayfish's Conquest of China, a RMB 10 Billion+ Business

▲ FreeS Fund Report (10): The Shared Secret of Snack Breakouts That Survived Economic Cycles

▲ Why Hot Pot Trends Change as Unpredictably as Fast Fashion