Tian Xuan × Li Feng: How Is Patient Capital Cultivated? | Li Feng Column

Is China's "Patient Capital Era" Here?

Lately, the financial term "patient capital" has started gaining widespread attention. In a special edition of the 2024 Tsinghua PBCSF Global Finance Forum, Feng Shu and Dean Tian Xuan engaged in an in-depth dialogue on the topic of patient capital.

Tian Xuan is the dean of Tsinghua University's National Institute of Financial Research, deputy dean of the Tsinghua University PBC School of Finance, and a chaired professor of finance. He has conducted extensive research in corporate finance, corporate innovation, and venture capital.

They started with the fundamental question of what patient capital actually is, and looked back at how America's path to patient capital unfolded. Turning to China's primary and secondary markets, they explored how key participants can cultivate patience. They also discussed the hotly debated topic of the IPO slowdown: after short-term pain, will there be long-term rewards?

We've edited portions of their discussion into this article, and also produced it as a podcast episode. We hope it offers fresh perspectives, and welcome you to continue observing and discussing with us.

Engagement Giveaway What do you think of "patient capital"? Share your thoughts in the comments.

By 5:00 PM on June 14, we'll give away copies of Dean Tian Xuan's translation of The Power of Patient Capital to the 3 readers with the most thoughtful comments.

/ 01 / Why Patient Capital Is Trending

Tian Xuan: Patient capital is a hot topic right now. Academics have been discussing the concept for some time. The book I'm holding, Patient Capital, is by two Harvard professors, Josh Lerner and Victoria Ivashina. In academic circles, patient capital typically refers to long-term funding — deep pockets, long money. After the April 30 Politburo meeting first proposed expanding patient capital, the concept became especially hot domestically, and this book gained considerable attention. As someone operating on the front lines, what's your view on patient capital?

Patient Capital cover, Citic Press Corporation

Patient Capital cover, Citic Press Corporation

Li Feng: I believe the state's emphasis on patient capital is closely tied to the restructuring of China's economy.

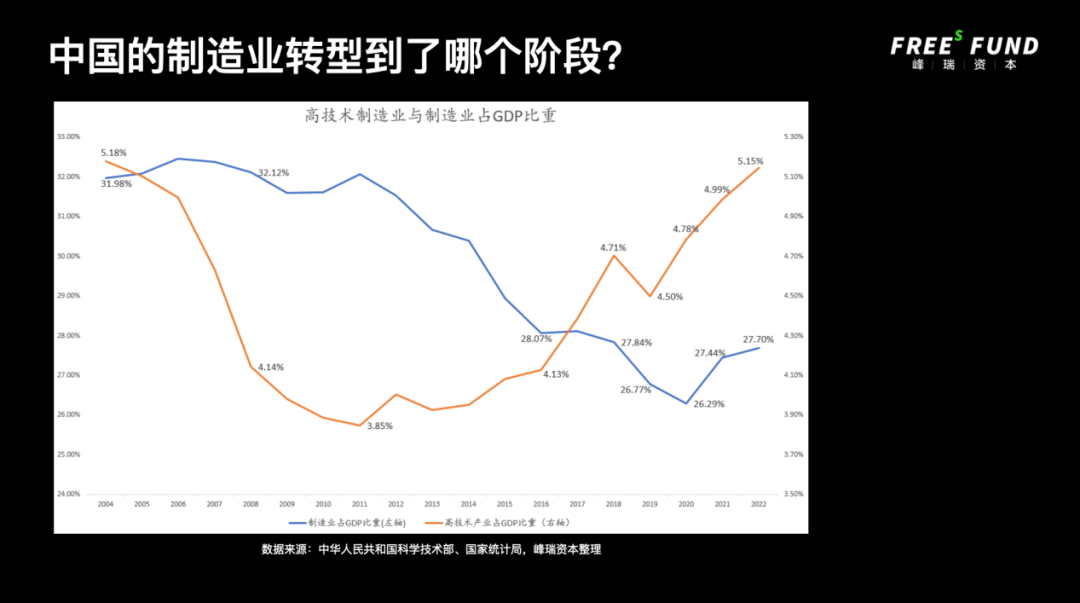

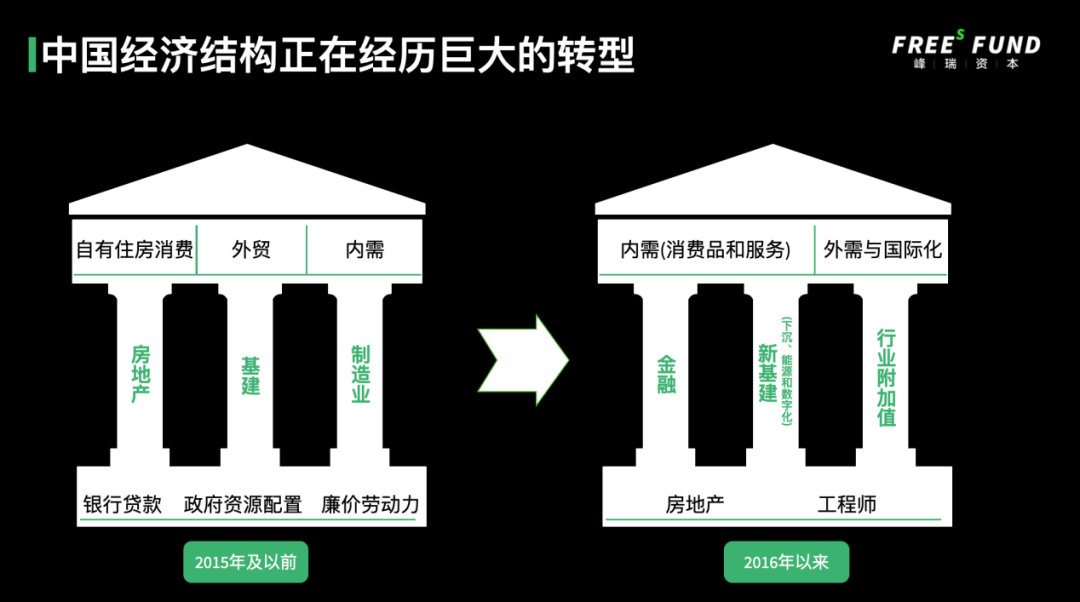

By the numbers, high-tech value-added manufacturing currently accounts for roughly 5.2% of China's GDP, while manufacturing overall represents about 28%. High-tech value-added industries break down into two segments: high-tech value-added manufacturing and high-tech value-added services. One direction of China's economic restructuring is to increase value-added share. This connects to our demographic structure, consumption patterns, and industrial composition.

If the proportion of high-tech value-added industries were to double, reaching 12% or 13%, it might signal that industrial chain restructuring is nearly complete. After all, China can hardly become like the U.S., retaining only the high-value-added segments, since we aim for full industrial chain coverage.

Assuming this reasoning holds, then at the current stage, these typical enterprises representing high-tech value-added industries may still be in early phases, relatively small in scale, and will need time to complete their transformation. Some sectors might require four or five years, others ten or fifteen. It depends on where each industry stands in its development cycle, which also implies that achieving economic restructuring may take a full cycle. This is one reason, from the underlying economic value perspective, why patient capital needs to be emphasized. Another possible reason relates to our secondary market — including capital composition, trading structure, and the institutionalization process, such as the recently issued "New Nine Measures."

Looking at U.S. development, Warren Buffett's success over these 50 years owes much to America's capital market reforms and adjustments since the 1970s.

Before the 1970s, retail investors accounted for as much as 80% of trading volume in U.S. secondary markets, leading to considerable market manipulation and wild volatility. However, during the 1970s to 1980s, with the emergence of new regulatory frameworks — especially the 401K plan, which allowed companies and individuals to invest through annuity accounts with associated tax benefits — these factors drove large-scale institutionalization of U.S. capital markets from the mid-1970s to early 1980s onward. By the 1990s, retail participation had dropped to roughly 50%, and today it's probably around 20%.

In this sense, China's current secondary market development stage, compared to today's U.S. capital market trading composition, still has a long road ahead. This may be another source of patient capital. Notably, after the new "Nine Measures," our secondary market has been encouraging medium- and long-term capital inflows. These initiatives may signal that we're beginning to enter the post-1980s phase that the U.S. experienced.

/ 02 / How Can China's Primary and Secondary Markets Become More Patient?

Tian Xuan: I think you're absolutely right. Patient capital is certainly connected to the current transformation and upgrading of industrial chains, including what's now being promoted as "new quality productive forces." The core of new quality productive forces lies in innovation, which is characterized by long cycles, high uncertainty, and high failure rates. Therefore, what must match it is inevitably long-term funding.

The secondary market you just mentioned is also very important. I noticed that the April 30 Politburo meeting had two sentences placed together: the first was about actively developing venture capital, followed by expanding patient capital. I suspect this patient capital refers to the secondary market. This includes one provision in the Nine Measures about introducing long-term capital. In China, the secondary market is currently dominated by retail investors, and even institutional investors display retail characteristics, since they're mainly fund manager-driven.

| Can Primary Market Fund Lifespans Be Extended?

Tian Xuan: On another front, this patient capital likely also relates to venture capital — that is, the primary market. Chinese fund lifespans are considerably shorter than in the U.S., where they're typically 10 to 12 years, whereas here we see 3+2, 5+2 — as short as three years, or as long as seven at most.

This difference in fund lifespans means we need to exit within three to five years due to LP (limited partner) pressure. This makes it difficult for us to do what the U.S. does — investing from the earliest stages, at small scale, in hard tech: maybe the company has just an idea, one or two people, two or three computers, and you start investing and accompanying its growth. That's quite hard in China. So we end up investing more in mid-to-late-stage projects.

This proposal of patient capital, as I understand it, hopes to extend investment horizons in primary market venture capital, and even earlier angel investing. For example, can our funds reach 10 or even 12 years? How to achieve this? I believe it's closely tied to how LPs commit capital. Take the U.S. as an example: their LPs are overwhelmingly institutional investors, with only a tiny portion from wealthy families and individuals — just 2%. Of the 98% that are institutional investors, a substantial portion, say one-third, are corporate pension funds. They actually seek long-term stable cash flows, so they're willing to put money into venture capital funds and wait 10 to 12 years. Their investment cycles are long; they're truly patient capital.

Then there are U.S. university endowments, like those of Harvard and Yale — educational institution endowments that are also long money. Because they similarly pursue long-term stable cash flows. Of course they invest in real estate, and they also like investing in so-called alternative assets, including venture capital, hoping for stable returns over 10, 15, even 20 years.

So from the primary market perspective, the patient capital we're talking about probably requires more corporate pension funds, pension funds, retirement funds, and some family office capital to enter the primary market. That way we can extend fund lifespans and better invest early, invest small, and invest in hard tech.

| On Institutional Investor Evaluation Mechanisms

Li Feng: Capital sources are indeed a critical factor. Of course, individuals typically have higher liquidity needs, whereas institutional investors tend to be more patient. However, institutional investors sometimes face issues with their evaluation mechanisms.

Take the insurance industry. Although insurance capital is inherently long-term money — especially pension-related insurance, with cycles potentially spanning 20 to 30 years, far exceeding all equity investment cycles — it was previously difficult for insurance companies to invest in VC, because they expected a certain degree of annualized cash returns. In other words, they cared about cash-denominated returns and didn't really recognize temporary markdowns in book value; this was determined by their accounting systems.

Over the past year, this situation has shifted somewhat, partly thanks to adjustments begun in early 2023 to internal accounting standards for the insurance industry.

Looking long-term, if we want to better channel this long money into VC or secondary markets — like the opportunity Buffett once encountered — we may need policy support on two fronts.

One is that when the insurance industry makes alternative investments or asset allocations, evaluation metrics and accounting systems could see some changes. For example, when an insurance company invests in an early-stage firm like ours, the book gains we generate — even accounting for liquidity discounts since it's not immediately realizable — perhaps could be recognized at a discount, or in some form, as current book returns on that investment.

The other front may require some related institutional design. For instance, in theory there could be better tax incentives, or even tax deferrals, deductions, or exemptions to encourage long-term holding.

Combining these two approaches can help capital owners make money, make long-term money — with the result that their capital becomes more patient.

| How Did Patient Capital Rise in America?

Tian Xuan: I agree with your point. In fact, American venture capital originated in the 1940s. I once translated a book called The Power Law: Venture Capital and the Making of the New Future. It discusses the first venture capital firm, American Research and Development Company, founded in Boston in 1946. For a long time afterward, even by 1972, when firms like Kleiner Perkins and Sequoia were established along Sand Hill Road in Silicon Valley, venture capital hadn't attracted much attention in the US — though of course they would later grow into remarkable institutions.

The Power Law book cover, Zhejiang Education Publishing House

The real rise of venture capital, or patient capital, began in the late 1970s. Particularly in 1979, the US Department of Labor reinterpreted the so-called "prudent investor" rule, allowing insurance funds — including pension funds and other long-term capital — that had previously been barred from the venture capital market to enter the space. So I believe the importance of national policy speaks for itself.

Additionally, as you mentioned, the evaluation mechanism is crucial. The LP composition in the US differs from China's. In China in previous years, individual and family investors made up the majority. But if we look at committed capital, in recent years government investment platforms, government guidance funds, and central and large state-owned enterprises have become major forces.

How Can Government Capital Become Patient Capital?

Tian Xuan: Government capital is inherently patient capital, but in practice, government guidance funds and pension funds don't seem patient enough. I believe this is mainly because their objectives as LPs differ from those of market-oriented LPs. They focus more on investment attraction and recruitment — they emphasize reverse investment ratios, hoping to boost local employment, tax revenue, and GDP.

For large institutional investors like government guidance funds, the frequency and methodology of evaluation are critical to enabling them to support VC as patient capital.

First, we should extend evaluation cycles. Annual evaluations make patience difficult. Early-stage investing differs from the secondary market, where performance can be assessed quarterly or even monthly. The primary market requires long-term accumulation — it may see explosive growth after reaching a certain threshold, but the early stage is necessarily a very slow accumulation process.

Second, and more importantly, evaluations should consider the entire portfolio rather than individual projects. Venture capital has a high failure rate. As the English title of the book I translated suggests, The Power Law — we should focus on the small number of projects with enormous growth potential that may ultimately deliver tenfold or even hundredfold returns, covering the majority of failed investments.

However, current government guidance funds or government financing platforms sometimes don't evaluate in a bundled manner but rather project by project. This can lead to distortion and misalignment. If we review projects individually, even if 9 out of 10 early-stage projects succeed (which is nearly impossible), the one failure could face accusations of state asset loss. The result is that government officials and investors dare not invest in early-stage projects, making so-called patient capital impossible to form.

Li Feng: Every fund we raise includes state capital, though the proportions vary. Roughly from 2018, the proportion of state capital accelerated, and this has become more pronounced in the last two years. I also have some observations relevant to our discussion.

First, looking at the risk appetite of state capital itself, some economically developed cities prefer to be LPs in early-stage funds, allowing professional GPs (fund managers) to bear the risk of investment decisions rather than making project-by-project decisions themselves.

On the other hand, there are two interesting parallel factors related to state capital. One is our country's cadre system — roughly every five years there is an evaluation and rotation. Therefore, since the tenure may not cover the full fund cycle, unless they serve two consecutive terms, funds often encounter changes in the leadership structure of government investors. This involves issues with their internal evaluation mechanisms. At these junctures, there may be some minor changes and challenges in coordination, communication, and continuity.

Another is China's financial reform, roughly once every ten years, from 1994, 2004, 2014, to 2024. In the evolution and institutional arrangements of China's entire financial industry, there is a cyclical iteration. These periodic factors are also a particular phenomenon in the development of state capital.

Tian Xuan: I completely agree. Our country has an official rotation system; officials typically serve 3 to 5 years, and staying too long in one place or department isn't ideal. This rotation system indeed makes it difficult for one leadership term to cover a cycle as long as fund investment.

Let me add — I recently visited a district in Wuhu, Anhui for research. They mainly develop the low-altitude economy and are doing quite well. This sector has also become very hot recently. The local party secretary told me that despite several secretary changes over ten years, they have consistently supported the low-altitude economy. This is a good example, but quite exceptional.

To make government capital patient, we may need some institutional and mechanism safeguards to prevent new officials from disavowing their predecessors' work, focusing only on making their own mark. This is very important.

China's Financial Structural Reform Helps Cultivate Patient Capital

Li Feng: Between state-owned investment platforms and patient capital, China is undergoing a transformation. On one hand, the economic structure is changing, with high-tech, high value-added manufacturing and services developing rapidly. On the other hand, there are interesting changes in the financial sector. By 2024, Chinese finance has undergone reform roughly every ten years.

The 2014 reform specifically proposed increasing the proportion of direct financing, and this was emphasized again in 2024. This relates to patient capital as we discussed. The main reason is that the high-tech, high value-added enterprises needed by the new economic structure, especially in their early development stages, rely much less on production factors like land and factory buildings, and have much greater need for direct financing. This requires financial structural reform — increasing direct financing rather than indirect financing represented by bank loans.

This reform has also brought another phenomenon occurring in many provinces and cities. This phenomenon resembles what happened during the bank structural reform. After stripping non-performing assets in 1999, bank structures began adjusting, from state-owned banks to joint-stock commercial banks merging nationally, to city and provincial commercial banks merging into city commercial banks or provincial commercial banks — a process that lasted about 10 years.

If we analogize the National Integrated Circuit Industry Investment Fund to the state-owned banks of that era, with direct financing corresponding to the National Integrated Circuit Industry Investment Fund and indirect financing to state-owned banks, today some economically developed provinces are merging various provincial and municipal or city-level investment platforms into one or two large investment platforms for unified management, serving as the main entities for fund-of-funds investment, direct investment, M&A, or major project funding.

From a medium-term perspective, this is good for state capital platforms becoming patient capital, because once integration is complete and they become one or two comprehensive management platforms, policy consistency on how much to allocate to fund-of-funds, who to invest in, what kind of GPs are needed, and how to coordinate with direct investment will be stronger, and continuity will be much improved.

Currently, it appears that most cities and provinces in economically developed regions like the Yangtze River Delta and Pearl River Delta have completed this reform, with new platforms beginning to function. Some places are still in the reform process. This adjustment, because it involves personnel changes and redistribution of management authority, has some volatile impact on capital deployment — after all, questions of who is responsible, who has final say, how much to invest, for what purpose, and how to coordinate with direct investment still need to be worked out.

Since 2022, this phenomenon has been very interesting and pronounced. Perhaps drawing on the experiences and lessons from the bank reform process over 20 years ago would make for an interesting research topic on the changes happening today in direct financing platforms.

Tian Xuan: Our discussion today has also provided new ideas for my research. So we are basically in a transition period, accompanied by some minor friction and rough patches during integration. But your observation and prediction is that if integration succeeds and forms a larger unified platform, it will have a positive impact on long-term capital deployment, investment continuity, and stability, correct?

Li Feng: Yes. Let me explain with a social phenomenon. I remember there was a period when news reports said many GPs were going to county-level cities to raise funds. These reports also reflected the economic structural adjustment we discussed earlier.

Due to economic structural adjustment, many high-tech enterprises or light-asset companies in their early stages don't rely heavily on land and factory buildings, and many cities need such enterprises but lack effective means to attract them. Everyone knows these enterprises need equity financing, so the result is that many institutions became LPs, and whether at the provincial, municipal, or county level, everyone was doing this.

This was somewhat like the banking system before 2005–2006, where we had different city commercial banks, rural commercial banks, and rural credit cooperatives in different cities. Later, these banks underwent a round of merger and integration.

Starting from 2023, as we discussed, something similar has happened in the direct financing field. To prevent every county or small city from doing the same thing, like the city commercial banks back then, they are now being consolidated into a few large platforms, with large platforms managing funds uniformly for allocation and coordination. Behind this may be issues with the sustainable capital deployment capacity of lower-tier cities, or constraints on the GPs they choose and the conditions they can offer, beginning to pose ongoing challenges.

I believe after these adjustments are completed, the sustainability and patience of government money will improve.

Tian Xuan: So what you're describing is a process from decentralization to centralization. Concentrating resources to accomplish major tasks — after centralization, the cycles will be longer, goals more aligned, and coordination better.

Is CVC Patient Capital, and What Changes Has This Sector Undergone?

Tian Xuan: So, what is your view on corporate venture capital (CVC)? In recent years I have been conducting academic research and surveys on CVC, and I have found that many enterprises invest directly in early-stage and venture investments. Their models vary — some do direct investment, some co-establish funds with traditional venture capital, and the loosest form is simply acting as a fund-of-funds. Regardless of the model, we have found that compared to traditional venture capital, CVC is "more patient capital" — with longer investment cycles and greater willingness to invest in earlier, smaller projects.

We believe the reasons for this difference are:

First, the goals of corporate venture capital and traditional venture capital differ. The latter focuses more on financial returns — put bluntly, making money for LPs. But for CVC, there are more diverse considerations: strategic alignment, upstream and downstream positioning, even industrial transformation and upgrading. When I talk to people doing strategic investment at corporations, they tell me that before making an investment, they'll first ask their business colleagues whether the project offers any integration or complementarity with their operations, or whether it could bring customers, technology, or traffic. In other words, CVC does more strategic thinking, not just financial returns.

Second, CVC mostly uses its own capital rather than raising from LPs — meaning it doesn't face exit pressure. As a result, CVC tends to have longer investment cycles and is naturally more patient.

Third, CVC often has strategic synergy support from its parent company. Traditional VCs can't possibly understand every technology; if a portfolio company needs relevant technical talent, the investor can only help recruit from the market. But CVC tends to invest in areas related to its core business, so the parent company's own technology, patents, and innovation can help its portfolio companies; conversely, the portfolio companies' innovation can also help the CVC's parent company. This is what we mean by "strategic synergy."

For these reasons, we've found that CVC is also "patient capital," and better able to support portfolio companies' innovation — or what we might call developing new quality productive forces.

However, looking at the data, corporate strategic investment rose from 2014, peaked in 2021, but has declined year by year in 2022 and 2023. I'm curious how Uncle Feng views this: if CVC is patient capital, why has it dropped so much in the past two years?

Li Feng: That's a particularly interesting observation. I can share my gut feeling. Over the past decade, the earliest CVCs in China fell into two categories. The first was A-share-related. Between 2014 and 2016, China saw a proliferation of M&A funds — typically structured around a single listed company as the main sponsor, establishing a smaller affiliated fund to serve as a pre-investment reserve for intended acquisition targets, which would then go public — the "listed company + PE" structure. This first phase, we can say, has more or less concluded, and overall there haven't been particularly successful cases.

The reason, in a nutshell, relates to the inherently short-term nature of this approach and capital market valuation mechanisms. Using M&A for market cap management is relatively short-term. The challenge with China's capital market evaluation is that it used to focus more on profitability metrics — namely the P/E ratio. And the P/E ratio of an acquisition target must certainly be lower than the acquirer's current P/E.

From a "patient capital" perspective, fund sponsors with explicit M&A needs may not actually be all that "patient." This was really just a story that sounded beautiful on both sides — projects get an exit, and listed companies can supposedly create value through M&A.

Perhaps after some time, when China's capital market shifts its evaluation and pricing mechanism for listed companies from profitability to growth orientation, or at least gives equal weight to both, the story of acquiring emerging targets might work out slightly better. After all, you can't demand that something new be good, profitable, and cheap all at once — it's hard to satisfy more than two of these simultaneously; you have to compromise on at least two.

The other type of listed company CVC emerged after 2013, when Baidu spent nearly $2 billion acquiring 91 Wireless, toppling the domino of major internet companies doing strategic acquisitions, mergers, or takeovers. From this event, BAT and other internet giants began large-scale investments, takeovers, or acquisitions. This continued for quite a long time, until after 2020, when Chinese concept stocks faced challenges in the U.S. over audit working papers, while at the same time, the enormous agitation and wealth effects of mobile internet began to fade. These two developments running in parallel caused that wave of CVC to shift and diverge.

From my perception, some large internet platform companies' needs and thinking around strategic investment have changed from before. Previously, their approach was roughly: with full business synergy as the goal, finding targets for control, M&A, and business coordination. The shift happening now is that beyond pursuing financial returns, they're paying more attention to what new technologies and directions are emerging across various sectors and industries, to "broaden their horizons." At this point, CVC becomes more "patient."

Tian Xuan: What's the logic behind these companies "broadening their horizons"? Is it pure curiosity, or do they hope that once these portfolio companies grow bigger, they can absorb their technology, talent, or even the whole company?

Li Feng: They really want to know what changes are happening at the frontier beyond their core business. If you read that The Power Law you translated, American CVC similarly divides into these two types. One is the "broaden horizons" type — for example, Google. Its Google Ventures arm invests in innovative cross-disciplinary and interdisciplinary emerging fields, making investments and positioning in the latest technological frontiers that may be temporarily unrelated to its core business. Of course, Google also has somewhat later-stage investments that may relate to its core business.

Tian Xuan: Very interesting, so this has happened in the United States. There's nothing new under the sun. In China, my understanding is that these companies are absolutely not "broadening their horizons" out of pure curiosity — they're still making strategic moves. Because companies may feel a sense of crisis; perhaps after some time an entire industry will decline, or new business formats will emerge to affect them, so companies want to understand the most cutting-edge technologies in advance, to prepare for future transformation and upgrading or entering a new field, and therefore invest in projects that may appear unrelated to their current core business.

For example, Xiaomi, as a smartphone company, later entered the car-making industry. I suspect from its decision-makers' perspective, if Xiaomi can transform and upgrade into the new energy vehicle sector, this could play an important role in its continued position at the market frontier.

How to View the IPO Slowdown: Short-term Pain and Long-term Returns

Tian Xuan: On IPOs and exits, I'd also like to hear your thoughts. Domestic listings face considerable short-term challenges right now. After this year's Spring Festival, there were three consecutive months with no IPO companies undergoing review by the listing committee. It wasn't until May 16th that IPOs and refinancing resumed, with normalized review processes restored. In fact, since August of last year, the pace of IPOs has dropped dramatically. How do you view the current situation?

Li Feng: There are definitely challenges in the short term. One impact is that we early-stage investors may be forced to seek more interim management and exits — that is, selling portions of our stakes while companies still have growth potential, before they go public. But if everyone thinks this way, interim management and exits become much harder than before.

Tian Xuan: It's essentially forced patience.

Li Feng: That's the short-term impact. The medium term, I think, is relatively okay. Because during these months when IPOs were slowed — or when the "floodgates" weren't opened — a tremendous amount of supply-side cleanup and adjustment was done, and with considerable force: cracking down on insider trading, illegal share reductions, false financial disclosures, violations of disclosure rules, and strictly enforcing delisting systems, among other things.

We can use an analogy: rather than rushing to add water to the pool or introduce new fish, first let the sediment settle and sort through the fish already in there. Over the past year-plus, all these capital market reforms — as I understand them — have mainly aimed to improve the water and fish in this pool, to make the structure more rational and healthier. This may be preparation for shifting more social capital toward direct financing in the future.

Rationally, we can expect that when capital market activity and trading volumes recover, we'll see more reasonable IPOs for good companies. From an evaluation mechanism perspective, after the "floodgates" reopen, if there's a better balance between companies' growth potential and profitability, that would theoretically be favorable for our exits.

Because nurturing an emerging industry to the point of explosive, high-growth scale takes roughly 5-7 years; nurturing it to meaningful profitability can easily take 10-15 years. This undoubtedly requires more patience. If the capital market can become structurally healthier overall, and if the evaluation mechanism can gradually tilt toward companies' growth potential — or at least give equal weight to profitability and growth — that would be more beneficial for exits of good companies.

Tian Xuan: Recently I've discussed the IPO slowdown with many people, and I think Uncle Feng, you're the most optimistic and positive among them.

Let me summarize your view: during this period, the CSRC is actually making institutional adjustments and reforms, trying to make the mechanisms more sound, the water in the pool clearer, and the fish in it better. After these adjustments, we'll reopen the floodgates and add new blood. In the future, the evaluation mechanism will shift from focusing on profitability to focusing on growth potential, striving to let truly high-growth companies stay domestic rather than all going overseas for listings. And you think this process may involve short-term pain, but is good in the long run, right?

Li Feng: Right. A short-term IPO pause is the easiest thing to affect sentiment. But if I were a disinterested, detached observer looking at what happened in the capital market during the past months of IPO suspension, I could understand why these things happened at this stage.

To use an analogy: in the late 19th century, when the American economy was developing rapidly and seemed to produce massive monopolies, it was instead called the "Gilded Age" — the era that "looked good on the surface." Yet the early 20th century, when American economic growth was mediocre, was called the "Progressive Era."

We might wonder: why didn't Americans call the era of rapid economic growth the "Progressive Era"? In fact, when Americans wrote their own history, they saw that earlier stage as merely superficially glamorous; the subsequent adjustment period, when antitrust and various other measures addressed many accumulated problems, was what they considered the true "Progressive Era."

By the same logic, we're now making supply-side adjustments. The previous regulatory approach was perhaps: when things look bad, quickly open the floodgates; when things overheat, quickly cut off the water entirely — leading to all sorts of dramatic volatility, like the US stock market before 1970 that we discussed earlier. So compared to the dramatic ups and downs caused by short-term adjustments, I think it's better to make longer-term changes that improve the structure.

For example: raising average company quality, raising the cost of illegal and non-compliant behavior, increasing public participation, and adjusting corresponding fiscal policies and even fee structures. Once these things are in place, theoretically there won't be such dramatic volatility — like the institutionalization reforms in US capital markets after the 1980s, or like the 50 years that Warren Buffett rode.

Tian Xuan: It's like our original approach was: when there's too much flour, add water; when there's too much water, add flour — or treating the headache by addressing the head, the foot pain by addressing the foot. We often say: short-term relies on policy, medium-term relies on institutions. What we're doing now is hoping to truly build a sound, stable environment institutionally. For example, our transition from the approval-based system to the registration-based system aims to exclude those "bad apples" from our listings.

Recently the CSRC has also emphasized implementing "accountability upon filing." It's not that you only get punished if financial fraud is discovered after listing — rather, as soon as you've submitted documents and signed, if problems are found, you bear responsibility. And the corresponding intermediaries, securities firms, lawyers, and accountants all bear responsibility too. This is about kicking out those "bad apples" at the entry point. This is ex-ante regulation.

Then there's in-process regulation: trading systems, including financial intermediaries, reduction systems, and M&A restructuring systems are also undergoing a series of adjustments and reforms, while increasing the cost of illegal and non-compliant behavior, forming a virtuous cycle.

We say capital market development must adhere to "building institutions, non-intervention, zero tolerance." Relative to this goal, I think the secondary market is currently in the process of "building institutions" or "perfecting institutions."

Once institutions are perfected, the market should be "each in their proper place," operating on its own. Listed companies, as market entities, should improve their corporate governance and quality, improve profitability, and bring returns to investors; as investors, we can't have infantile entitlement — we can't say "I'm amazing," "I'm awesome," "I'm a stock god" when we make money, then go complain at the CSRC's door when we lose money. Other market participants, such as intermediaries, accountants, lawyers, and securities firms, should fulfill their role as so-called "gatekeepers." I think this would be a relatively sound, mature, and well-functioning capital market.

The third term is "zero tolerance," meaning if everyone operates within the red lines, however you operate doesn't matter; but as soon as you cross the red line — fraudulent issuance, insider trading, financial fraud, market manipulation — then we need both administrative penalties and criminal penalties, plus civil liability, forming a combined punch against such serious illegal and non-compliant behavior. I think this would make for a better capital market.

Li Feng: Indeed, but the short term is definitely quite painful. Especially given how "invincibly well" the Fed has managed expectations around rate hikes and cuts today. The result of this "invincibly well" performance is that countries worldwide have all suffered losses to varying degrees. The RMB is under pressure now; when the RMB is under pressure, RMB-denominated assets are under pressure. Under today's pressured conditions, doing painful short-term things just hurts more. It's like scraping the bone to treat a wound while salt rains down from the sky.

Tian Xuan: Right, nonetheless, this still needs to be done. I checked — "patient capital" recently appeared for the first time in policy documents at this high level. I think in developing new quality productive forces, encouraging long-term technological and industrial innovation, accelerating the cultivation of strategic emerging industries, and promoting the transformation and upgrading of traditional industries, patient capital will play a particularly important role.

Interactive Benefit

What do you think of "patient capital"? We welcome your thoughts in the comments.

By 17:00 on June 14th, we will select the 3 most thoughtful commenters to receive a copy of Dean Tian Xuan's translation of The Power Law: Venture Capital and the Making of the New Future.

▲ Liu Run × Li Feng: In the Future, What Kinds of Companies Will Thrive? | Li Feng Column

▲ The Road to Embodied Intelligence | FreeS Report 37

▲ How Far Is Embodied Intelligence from Reality: Hype, Bubbles, Technological Frontiers, Commercialization | FreeS Research Institute

▲ Li Xiang × Li Feng: Behind the Rise and Fall of "May Day" Tourism Data, Long-term Trends That Are Easily Overlooked | Li Feng Column

▲ Li Feng in Conversation with Lian Wenzhao: The Imagination and Bubbles of Large Models, the "Impossible Triangle" of Robotics, and the Future | FreeS VC Dialogue

Star the FreeS Fund WeChat Official Account for timely business insights