What Are Top Overseas Chinese Students Thinking About When It Comes to Entrepreneurship and Investing? | FreeS Fund Dialogue

How do we make sense of the business world and think about the future?

This past summer, FreeS Fund partnered with Chinese student organizations and clubs at several overseas universities for five exchange events:

- "Yale Venture City Tour — Beijing Stop"

- "Penn Quakers Venture Club Gewu Journey — Beijing Stop"

- "Oxford-Harvard-Stanford Chinese Students and Scholars Association Returnee Tour — Beijing Stop"

- "ACE 2023 Summer Startup Trip Entrepreneurship Bootcamp"

- "MIT CEO Entrepreneurship 101 Season 4"

From macroeconomic conditions and frontline investment observations to startup ideas and career planning, students asked questions with enthusiasm and shared their confusions and reflections. Among the FreeS Fund investment team members who participated, there were seasoned "industry veterans" who had navigated multiple cycles, as well as younger investors with backgrounds similar to the students'.

Some of the topics they discussed included:

- How to think about the AI startup frenzy?

- In these uncertain times, how do early-stage investors make decisions?

- How to view the current macro environment and economic opportunities?

- If you want to join the venture capital industry, how should you prepare and plan?

Around questions of shared interest, we've selected some of the more compelling conversations from these events and compiled them here, hoping to offer some useful reference points.

Interactive Giveaway What are your thoughts or reflections on entrepreneurship or investing? We'd love to hear from you in the comments! By 17:00 on September 28, we'll send a book recommended by Feng Shu to the 5 users with the most thoughtful comments (shipped randomly).

/ 01 / AI Is Hot — Should I Get Into Investing or Startups?

Q: How do you evaluate the overall development of the AI industry? With hundreds or even thousands of companies entering AI in China, how do investment institutions assess an AI company's technical capabilities?

Yang Yongcheng (Partner, FreeS Fund): The frenzy around AI entrepreneurship isn't surprising. Objectively speaking, AI is a direction with broad prospects, where both the technology and its applications still have enormous room for growth — it could remain hot for many years. But like most things, AI's development path won't be a straight line. There will be cyclical ups and downs, but the overall trend is forward.

Subjectively, humans are more or less susceptible to herd mentality, and the investment industry is no exception.

From the operating logic of venture capital, a successful early-stage investment requires not only betting on the right direction and an excellent team, but also receiving subsequent recognition from the investment community and the market.

So it's normal for certain directions to receive阶段性追捧, and it's actually a good thing for the AI industry's development. But whether you're an angel investment institution or a team just preparing to start up, merely paying attention to and understanding currently hot directions is clearly insufficient. Ultimate success still depends on whether you can think independently and correctly, and particularly whether you can observe and judge earlier than most in the industry.

As for how to judge AI's development level and potential — that is, what constitutes high versus low AI capabilities — there isn't yet a broadly accepted scientific standard. From what I've observed, the industry's preliminary consensus is to compare AI capabilities with human cognitive abilities. The more human-like, the more intelligent, the more AI. Following this logic, I'll try to refine this evaluative standard into three dimensions from an investor's perspective.

First, things humans can do and AI can also do. AI replaces humans in completing high-volume or even dangerous work, and can also serve as an efficiency tool. For example, AI can converse with people in natural language, serve as intelligent customer service, and recognize and generate images.

Second, things ordinary people can't accomplish, but a small elite among humans can achieve under fortuitous circumstances — can AI do these? For instance, Newton discovered gravity and formulated it mathematically; Einstein derived the famous mass-energy equivalence, laying the physical foundation for the atomic bomb. There are also discoveries in the humanities — say, unearthing an oracle bone script symbol, how do you interpret this character? These all belong to original scientific discoveries or inventions, typically produced by the "flash of insight" of extremely top scholars. We hope AI can increasingly help humans in this regard. In fact, AI has already made many breakthroughs here — for example, AI can now help people predict protein structures.

Third, things humans can do that AI currently cannot do or doesn't do well enough. For example, current AI algorithm architectures and computing hardware consume far more power than the human brain; we're far from "energy-efficient" and "economical." People hope AI algorithms and hardware architectures can further develop — such as photonic computing, or compute-in-memory architectures.

From an investor's perspective, we pay attention to AI's technological development, but care even more about AI's market value in practice. If AI cannot generate actual value, the input-output ratio becomes unbalanced. Whether AI can next accomplish things that humans don't do well — this is what I'm particularly watching.

Q: How do you view "AI+" application-layer startup projects?

Chen Shi (Venture Partner, FreeS Fund): For AI application-layer startups, particularly "AI + (industry)" projects, what I value is that the product must have at least outstanding single-point advantages, sufficient business depth, not be too close to the AI large model itself, and have the ability to form its own closed business loop — these can constitute its moat.

The current rise of generative AI differs from the mobile internet era. Mobile internet applications initially faced massive numbers of new users, mostly people migrating from offline to mobile — the so-called "traffic dividend." The current wave of AI applications, however, is mainly about grabbing users from traditional internet/software companies that have already accumulated certain user bases or business models. There's almost no "traffic dividend" to speak of; the difficulty of scaling user acquisition is very high, while traditional software companies can rapidly catch up through "+AI."

Additionally, if you're doing an AI+ project, the team needs to understand both technology and industry. Experience and accumulated knowledge in a specific industry are very important for entrepreneurs.

Li Feng (Founding Partner, FreeS Fund): Why is AI so hot right now? Probably the biggest reason is that people see it as a productivity tool with huge potential. We can compare AI to a "hammer." Then we need to figure out who can use this hammer, and which nails it can hit. If you only have the hammer, no matter how "good-looking" it is, it's not very useful.

Many young entrepreneurs are interested in "AI+." As an investor, I'll first ask: how was the problem you want to solve addressed before AI existed? Do you understand its business model? These questions are about what the nail looks like. Whether the hammer is better than before — that's a separate matter.

Chen Shi: Exactly. So we say the key to AI application-layer entrepreneurship is "technology first, scenario heavy" — in the end, it still has to land in scenarios.

Q: How should startups enter AI application-layer entrepreneurship?

Li Feng: In the medium to short term, AI applications related to professional services may be more suitable for startups — such as healthcare, education, and so on. These domains require vertical professional knowledge, and the service format is basically conversational, not involving using AI to directly make critical decisions.

In the long term, AI may have the potential to enter various industries with high digitalization. But here, the development situations in China and the US differ somewhat. China's industrial landscape is extremely rich, but its digitalization level is relatively low. The US has relatively higher digitalization, but less industry diversity.

So the direction of AI evolution in the US may be technological progress on top of digitalization, while in China, it may be about raising digitalization levels across enough industries first, then using AI to improve overall efficiency.

Chen Shi: When AI enters industries and the application layer, it's essentially a process of using AI modules to gradually replace traditional code modules. There are two approaches: "+AI" and "AI+". The former is when current industry leaders use AI technology to optimize their existing software; the latter is when new entrepreneurs enter an industry with AI technology to transform it. Given China's current competitive landscape, I'm inclined to believe the former is more efficient and less difficult, though there are exceptions — such as entering a new industry where the newcomer has deep domain expertise, or entering an industry that's easily disrupted by AI.

On technology roadmap selection, I believe the Copilot-style applications (AI-assisted tools) and LLM wrapper apps commonly seen in the industry today aren't suitable for new entrepreneurs, because industry leaders will adopt them too. My advice is to choose more difficult technical routes where no viable consensus has yet formed. It's harder, but your odds of success are higher.

Additionally, when looking for co-founders and building teams, the combination of technical capability and industry experience matters — especially industry experience. I also encourage young people to try boldly. When everyone can't see the direction clearly, that may be precisely the best time to start. (For more on entrepreneurial opportunities in the AI wave, see: Where Does AIGC Go After ChatGPT's Explosion? | FreeS Report 28 A Debate: Two Investors With Different Views on GPT | FreeS Research Institute)

/ 02 / How Do Early-Stage Investors Understand the World and Judge the Future?

Q: Why does FreeS Fund pay so much attention to interdisciplinary startup investing?

Li Feng: First, our current disciplinary divisions are actually the result of mutual influence and joint advancement between the Industrial Revolution and scientific progress itself. So if our technology or production methods change, the logic behind existing disciplinary divisions will adjust accordingly.

Looking at today's tech industry development, two trends are fairly obvious: one is moving toward the micro scale, the other toward the macro scale. Chip manufacturing is an example of micro-scale development — process technology has advanced from hundreds of nanometers, to tens of nanometers, to a few nanometers. Observation and exploration of the universe, weather, environment, and so on belong to macro-scale development.

Our portfolio projects involve more of the micro scale. For this type of technological progress, we divide it into four stages: observation, measurement, control, and manufacturing. First you see what's happening at a more micro scale, then you can accurately measure what you've observed, then you can control changes at that scale, and finally you can precisely control various elements for product manufacturing. This progression can't be solved with single-dimension knowledge or a single discipline — it requires multidisciplinary accumulation and breakthroughs.

We can also think about this from the industrial chain perspective. China's industrial chains are comprehensive and long, with still substantial portions in the low-to-medium value-added segments. Midstream and downstream processing and manufacturing are relatively heavy, while upstream R&D is comparatively insufficient. Now, as industrial chains upgrade and extend toward higher value-added development with increased technological attributes, many new intersection points may emerge. For example, when healthcare digitization accumulates sufficiently, you get computational biology. When gene editing and enzyme engineering develop together, you get synthetic biology.

Additionally, it's currently less likely for individual industries to experience major discontinuous development driven by technological breakthroughs; more likely is gradual development. And the driving force for this may well come from other related industries. For instance, new directions in construction might come from materials science — the invention of some new building material — or from advances in technologies like 3D printing. Paying attention to this kind of multi-industry linkage effect is another reason we choose to invest in interdisciplinary areas.

Interdisciplinary opportunities are relatively difficult to judge. Teams need professional expertise in multiple vertical domains simultaneously, then need to find the connection point. However, once industrial chains extend and form new intersections in the future, this category of startups will show tremendous potential.

Q: How does early-stage investing judge the future, and how do you face "uncertainty"?

Li Feng: One internal investment "discipline" we have is to invest in good projects early, not to invest in "cheap" projects when they're hot. Making investment decisions when industry enthusiasm is low isn't actually easy. To put it abstractly, you need to simultaneously think through three things: Why isn't this direction hot today? Why will it be hot tomorrow? And why will it ultimately become big? Only by thinking through this logic can you dare to make investment decisions when the market is cold.

Additionally, you have to consider the time factor — "tomorrow" and "the future" are two different time horizons. As early-stage investors, our returns are based on project growth, and first and foremost we want the project to survive. So the question to clarify first is "What will happen tomorrow?" Then, perhaps, comes "What will happen in the future?"

Q: In my entrepreneurial journey I've come into contact with some traditional domestic factories, and I've deeply felt how difficult their transformation is. Against the backdrop of the AI-driven intelligentization wave and global industrial chain relocation, where should China's traditional industrial chains go in the future?

Li Feng: This can be divided into two situations: existing industrial chains need to rely on digitalization, while new industrial chains need to rely on technological advancement.

The smartphone industrial chain, for example, was once a new industrial chain. Moving from traditional phone production to smartphone production added considerable technological content — from sensors and chips to displays and cameras — raising the value-added of the industrial chain. Other consumer electronics industries are similar. Take Insta360, which makes action cameras. Through front-end hardware-software integration, image algorithms, camera hardware advances, and so on, Insta360 created new products and elevated the industrial chain's value-added. (On why China needs "chain leader" enterprises, see: Li Xiang x Li Feng: Stripping Away Emotion, Discussing Economic Variables for the Second Half of 2023 | Li Feng Column)

The other portion is existing industrial chains with room for value-added improvement, such as apparel and home textiles. These industries need to improve efficiency through digitalization as much as possible. For example, cross-border apparel e-commerce company Shein created a "small-batch, rapid-response" flexible supply chain model, carrying out supply chain digitalization transformation for its partner apparel factories.

For industrial digitalization, the needs in China and the US also differ somewhat. After deindustrialization, the US has more domestic high value-added production and service enterprises, chip design being one example. Their main demand is using SaaS to improve enterprise management efficiency. China's industrial chains are long and still retain many low-to-medium value-added segments. What these traditional industries want to solve is how to reconnect every link in the industrial chain through digitalization to improve overall efficiency. (On industrial digitalization, see: Li Xiang x Li Feng: Why Did ChatGPT Emerge Today? What Happens Next? | Li Feng Column)

Q: Regarding the current macroeconomic environment, how do you as an investor judge and think about it?

Li Feng: On the macro front, I've shared in articles and podcasts that regarding future economic development, I believe there are two key bottom lines. One is the pessimistic bottom line — the relationship between China's economic growth rate and the world's economic growth rate. The meaning behind this is whether China's share or contribution to the world economy will continue to increase. The other is the optimistic bottom line — the proportional relationship in economic growth between China and the US, the two countries ranked first and second in GDP globally. The answer to this relates to both the GDP growth rates of China and the US, and to the scale of China-US GDP. (On how to understand variables related to the macro economy, see: Li Xiang x Li Feng: Stripping Away Emotion, Discussing Economic Variables for the Second Half of 2023 | Li Feng Column)

Based on these two lines, how the market judges Chinese assets and how capital liquidity is affected are more concrete questions. Though I'm often teased by podcast listeners for being perennially optimistic, my intention isn't to give my own predictions, but rather to try hard to provide a relatively rational analytical perspective.

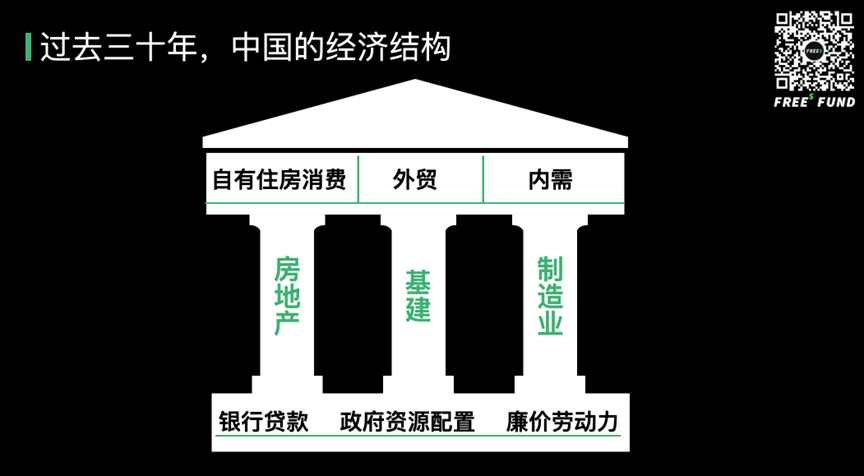

We drew two diagrams to summarize our understanding of China's structural economic transformation. The first illustrates the economy's composition over the past 30 years. At the center are three pillars representing the primary growth drivers: real estate, infrastructure construction, and manufacturing capacity expansion. All three are production-factor-intensive industries, requiring substantial upfront inputs of capital, land, or cheap labor. The foundation beneath these pillars supported their development: bank lending, government allocation of production factors such as land, and cheap labor—drawn from the migration of workers from primary to secondary and tertiary industries, as well as from urbanization. The roof held up by these three pillars comprised domestic demand, foreign demand, and owner-occupied housing consumption.

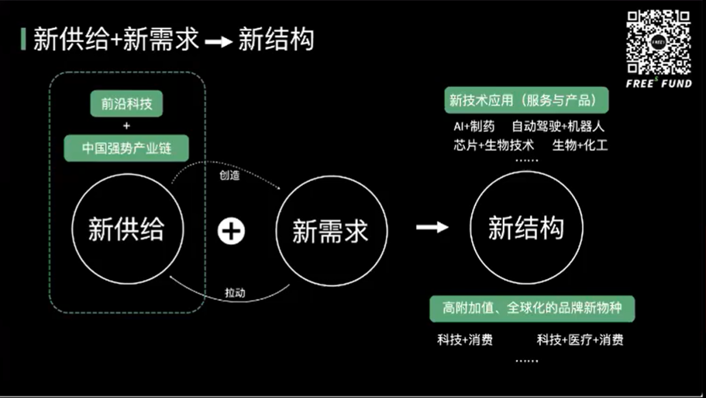

Today, China's economic structure is undergoing significant adjustment. The diagram above represents the new configuration. In the foundation, first, as the demographic dividend gradually fades, cheap labor is being replaced by better-educated workers—the so-called engineer dividend.

Another shift: real estate, formerly one of the pillars, has moved to the foundation. Once a powerful engine of Chinese growth, even if it no longer sees simultaneous price and volume surges, it will remain a stabilizer for economic development.

The most dramatic changes are in the three pillars themselves. First, we are adjusting the financial structure to control further growth in leverage. Where we previously relied mainly on bank loans for indirect financing, recent policies increasingly point toward direct financing. Building out a direct financing system and raising its share is a major directional shift for capital markets.

The central pillar—infrastructure—will likely develop along two paths. One is further下沉 of roads, bridges, and similar infrastructure into townships and rural areas. The other is digitization, or datafication, across industrial chains: for example, digital power systems capable of real-time monitoring and supply-demand balancing.

As the cheap labor advantage diminishes, China's industrial chains must either upgrade in quality or improve in efficiency. Digitization is a crucial lever for efficiency gains. Quality upgrading corresponds to the pillar on the right: developing mid-to-high value-added segments of industrial chains, such as advanced consumer electronics and new energy vehicle supply chains.

So how will the top layer of this new structure change? One segment is domestic demand. We are the world's second-largest consumer market. According to data from the NDRC and National Bureau of Statistics, China's total retail sales of consumer goods reached 43.97 trillion RMB in 2022. In the first eight months of this year, that figure grew 7% year-over-year.

My observation: because supply chain efficiency in consumer goods is already exceptionally high, the sector will likely tilt toward zero-sum competition. Services, having passed through the pandemic-suppressed phase, should see relatively rapid growth in coming years—incremental expansion. Consumer goods and services are the two major components of our domestic demand. As for foreign demand: with roughly one-sixth of global population, we produce 30% of global output. Even with a sizable domestic market, foreign demand remains important. Chinese products and brands are also shifting toward "active internationalization"—companies adding technological value atop existing industrial chains to create globally competitive new products.

Leaving Campus: How to Start Your Own Business?

Q: In the early stages of entrepreneurship, how do you cultivate interdisciplinary capabilities and build a team with interdisciplinary backgrounds?

Marui (Partner, FreeS Fund): First, many entrepreneurs already have interdisciplinary backgrounds. Take Haokian Zhang, CEO of Bluepha: he graduated from Peking University's physics department while also winning a gold medal in the biology iGEM competition. His research field was essentially engineering biology. Another example is Xin Zhao, founder of Xinsu Technology. During his PhD at MIT, he worked on semiconductors. Later, he recognized the potential of applying semiconductor technology to biology, so he pivoted his research in that direction during his doctoral studies. So for students, it makes sense to consciously study across disciplines.

Whether you're supplementing your own knowledge or assembling a team, I'd suggest "following the map" across a few dimensions. First, technology fields with major growth potential—materials and computing, for instance, are particularly important. Another major direction is domain expertise in your specific industry. (For more on frontier technology and interdisciplinary entrepreneurship, see Opportunities and Challenges for Frontier Tech Entrepreneurship in a New Cycle)

Q: Is it still suitable to start a business when the market cools?

Li Feng: Market downturns are inevitable. Even Tesla faced a financial crisis during the 2008 financial crisis and struggled to raise money. For startups, whether you enter an industry during a hot or cold market, there's always a path to success.

A core challenge for early-stage startups, simply put, is having insufficient resources while needing rapid growth. Facing this dilemma, the ideal is to avoid ineffective competition. To use an analogy: being the first to step into a pit may be better than stepping into one that countless others have already trampled—because the more a pit is stepped in, the deeper it gets, and the harder to climb out. But once a market heats up, ineffective competition becomes unavoidable. So from this perspective, starting up during a hot market presents its own challenges.

Yang Yongcheng: Overall, current consumer demand hasn't kept pace with supply growth, and the market lacks foundational technology revolutions on the scale of the internet or mobile internet. In this environment, employment and entrepreneurship have indeed become harder.

As individuals, we can't change consumer demand, but we can cultivate and improve our own innovation capabilities. Historically, major technological innovations have mostly begun with individual creation before diffusing to broader groups. So if you can treat innovation as a responsibility and goal during your school years, that's tremendously meaningful.

Moreover, from a long-term perspective, China still has vast market space waiting to be explored, and we encourage everyone to return and develop here after graduation. We will always experience cyclical fluctuations, but entrepreneurship is forever something worth looking forward to.

Q: How should startups respond to competition or even "copying" from large companies?

Chen Shi: Entrepreneurship and investing are similar—I believe both are fundamentally about finding non-consensus opportunities, seeing half a step further than most. Competition from tech giants is hard to avoid, but if you can find a non-consensus opportunity and work on something that giants can't clearly see or commit to, you're much better positioned.

Here's a real case: I was involved in the founding of UC Browser, started in 2004 with the positioning of making browser software for mobile phones. This was the non-smartphone era, wireless networks were slow, and the direction was unclear. Plus, a company called Netscape had already failed at PC browsers, perhaps for two reasons: not finding a viable business model, and operating system companies entering directly—Microsoft launched IE, for instance.

So from 2004 to 2009, we barely encountered competition from major players, winning precious development time. We later concluded that flaws in the early business model can sometimes be a good thing. Of course, you also need to think through whether you have a path to turn that non-consensus into consensus—remaining non-consensus forever doesn't work either.

Li Feng: This reminds me of a book I read a few years ago: Ronald Coase's How China Became Capitalist. Regarding Chinese reform, Coase proposed a theory called the "marginal revolution." He argued that China's successful reforms were driven by forces at the "margins" of the system. Applying "marginal revolution" to innovation and entrepreneurship is entirely valid.

Career Planning for Entering VC After Graduation

Q: I'm a PhD about to graduate. How should I think about the choice between industry and investing?

Yang Yongcheng: The difference between entrepreneur and investor can be illustrated through driving. If you choose entrepreneurship, you're in the driver's seat, hands on the steering wheel.

When you first start in investing, you're like the front-seat passenger—you're young, probably lacking work experience, but you can help the driver read the map, occasionally hand them a water bottle, provide resources and suggestions.

As you gain seniority and experience, you become more like a driving school instructor, able to offer more advice and resources to the driver.

But no matter what, the instructor can't touch the steering wheel—they don't get the thrill of driving or the lived experience. In other words, investing and entrepreneurship are two different lifestyles, with different feelings, inputs, and returns. Which to choose depends on your life pursuits. Of course, practical considerations matter too: career choice should align with your personality traits, capabilities, and resource reserves.

Xie Da (Vice President, FreeS Fund): I've worked with many PhDs and academically trained founders. If you choose industry and aim to translate lab research into commercial ventures, several things are different.

First, good technology doesn't automatically mean good product. Academically trained teams generally have solid technical foundations, but often struggle with commercialization. So making the transition from technology to product is crucial.

Second, some technologies viable in lab conditions can't scale to mass application. Many biotech research results, for example, may not directly apply to actual drug development. Additionally, scientists-turned-entrepreneurs need to deepen their understanding of financial markets.

Q: I'm an undergraduate in basic sciences and want to work in investing. How should I plan my career?

Li Gang (Early-stage Project Lead, FreeS Fund): I studied physics in college. Personally, I found it quite helpful for investing. The habit of thinking from first principles, for instance, helps me quickly learn new fields. However, basic science majors may have limited exposure to industry during school.

So I'd recommend accumulating some industry experience after graduation before moving into investing. Especially for early-stage investing: if the entrepreneur lacks experience and you as the investor also lack industry accumulation, putting you two together creates a disadvantage.

Ma Rui: I'd suggest participating in entrepreneurship-related activities outside of class and proactively building your network. Drawing from my own student experience — I was student body president at Carnegie Mellon University and also ran CMU Summit, an annual event where we invited many investors from China to speak on campus. Those opportunities helped me connect with numerous domestic investors, including my current boss, Li Feng. Because of that "connection," he offered me a job even before I graduated and returned to China.

Q: Do humanities and social sciences students have any advantages in entrepreneurship or investing?

Li Feng: I come from a science background, but over the past two years I've read extensively in the humanities and social sciences, particularly history. I've tried to combine historical perspective with my scientific lens to think about the role of technological factors in societal development.

For me, knowledge from the humanities allows us to engage in abstract thinking across larger scales of time and space. Many outstanding investors also come from liberal arts backgrounds. For example, the well-known venture capitalist Michael Moritz graduated from Oxford University with a degree in history and even worked as a journalist.

Q: In investment work, how do you learn an entirely new field?

Li Feng: My habit is to first identify the most fundamental variables in this new domain, then transplant the universal patterns I've abstracted from different industries to see which parts might apply. After that, I'll think one or two levels deeper, combining past patterns with the new variables of this industry to test my conclusions. If the conclusion doesn't hold up, I look for other factors and try again.

Take the new energy sector as an example. I first examined whether there had been fundamental innovations in chemistry, materials science, or other underlying technologies. If no such technological breakthroughs were apparent, then new energy might be following a gradual development path. If it's gradual, why is new energy so hot right now? I considered other angles and hypothesized that one factor could be China's push to reduce energy import dependence. Of course, there are many other important variables and dimensions to consider as well.

Special Thanks

We have always looked forward to ongoing exchanges with more partners interested in innovation and entrepreneurship, jointly weaving a vibrant global innovation network.

Our thanks again to the student organizations and clubs that organized and supported these exchange events:

- Yale Venture Club

- Penn Quakers Venture Club

- Oxford Chinese Students and Scholars Association

- Harvard University Chinese Students and Scholars Association

- Stanford Chinese Students and Scholars Association

- ACE Berkeley Chinese Entrepreneurs Association

- MIT Chinese Entrepreneurs Organization

(Listed in chronological order of event organization)

Engagement Giveaway

What thoughts or reflections do you have about entrepreneurship or investing? We'd love to hear from you in the comments! By 17:00 on September 28, we will mail one book recommended by "Uncle Feng" (random selection) to the 5 users with the most thoughtful comments.

FreeS Fund's 8th Anniversary: We Welcome You to Join Us on the Longer Road Ahead

Best Time in Early Autumn: 6 Early-Stage FreeS Family Companies Raise Nearly 1 Billion RMB | FreeS Family Funding News Vol.15 A Trip to the US: 6 New Opportunities in Consumer Sub-Segments We Discovered | FreeS Research Institute "Pain Comes from Identifying Problems, Joy Comes from Solving Them" | FreeS 5th Open Day Recap

Follow & star the FreeS Fund WeChat Official Account for timely business insights