What Did Minister Miao Wei Actually Say About Chinese Manufacturing? | Frees Fund

What Happened to China's "Undervalued" Manufacturing Sector Between 2015 and 2019?

A lecture delivered in November 2015 was recently dug up and reinterpreted, stirring up quite a bit of controversy. According to an article titled "Minister of MIIT: 'Made in China' Is Not as Strong as We Imagine, the Public Is Too Feverish," its central argument was drawn from Minister Miao Wei's interpretation of the Made in China 2025 roadmap at the 13th meeting of the 12th CPPCC National Committee Standing Committee. The article claimed that the minister said, "Made in China is not as strong as we imagine, Western industry has not declined to the point of depending on China. Our manufacturing sector has not yet upgraded, but manufacturers are already starting to leave."

The article seemed to use the minister's words as a reminder that although "Made in China" played an irreplaceable role in producing medical supplies like masks as the pandemic spread globally, people should not be too feverish about Chinese manufacturing.

While sparking widespread discussion, the article was quickly debunked. Aside from the claim that "China is currently in the third tier (of global manufacturing)," which did have a source, the core controversial quote attributed to Minister Miao did not appear in his actual speech. But debunking aside, the fact that this article resonated with some people now precisely shows how uncertain many feel about the real strength of Chinese manufacturing. This pushed the question to a new level of discussion: standing in 2020, what is the actual position of Chinese manufacturing in global industry?

On this, our basic view is that over these five years, whether driven by domestic policy, market forces, and technological advancement, or stimulated externally by factors including the trade war, China's manufacturing sector and the entire industrial chain have seen considerable development. The strength of Made in China has been underestimated, not overestimated.

Since its founding in 2015, FreeS Fund has always prioritized investments in industrial upgrading, including intelligent manufacturing and industrial internet. Based on our investment and research practice from 2015 to the present, we share our thinking in this article on three topics:

- Where did the "third tier" label come from in 2015?

- Compared to the context of Minister Miao's 2015 speech, what macro-level changes have occurred in Chinese manufacturing?

- In the three most challenging manufacturing sectors — consumer electronics, semiconductors, and automobiles — what progress have Chinese companies made over these five years? How competitive are they internationally?

We hope this offers a different perspective. We welcome your thoughts and feedback.

/ 01 /

Where Did the "Third Tier" Label Come From in 2015?

Before analyzing Minister Miao Wei's remarks, let's look at 2015, the year this view was proposed. From a scale perspective, where did China's manufacturing actually stand in global industry?

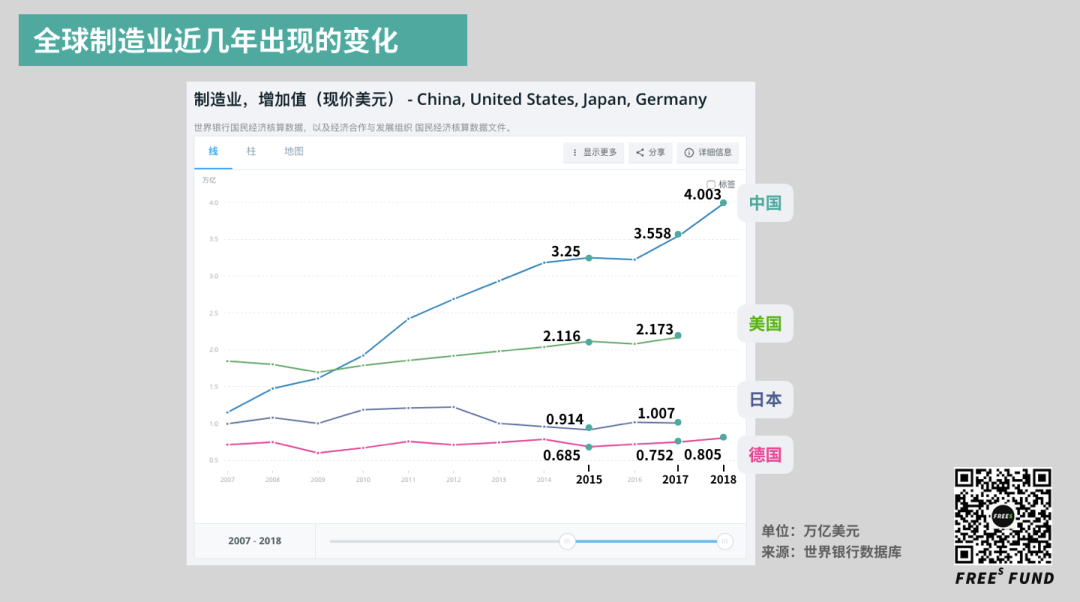

According to World Bank data, in 2015, manufacturing value added for China, the US, Japan, and Germany was $3.25 trillion, $2.116 trillion, $0.914 trillion, and $0.685 trillion respectively. The US, Japan, and Germany's manufacturing value added was approximately 65%, 28%, and 21% of China's.

Since China was already first in scale by a clear margin, where did the "third tier" label come from?

Let's revisit the original text.

According to Minister Miao's 2015 classification — global manufacturing had basically formed a four-tier development structure:

- First tier: The US-led global center for technological innovation.

- Second tier: High-end manufacturing, including the EU and Japan.

- Third tier: Low-to-mid-end manufacturing, mainly some emerging economies.

- Fourth tier: Resource-exporting countries, including OPEC, Africa, and Latin America.

Miao stated that China (in 2015) was in the third tier. Although it had become a major manufacturing country, it was not yet a manufacturing powerhouse. Compared to advanced countries, there remained significant gaps. Taking equipment manufacturing as an example, he identified four areas of weakness: weak independent innovation capability; insufficient basic supporting capabilities; product quality and reliability in some sectors needing improvement; and irrational industrial structure.

However, he also believed that facing technological and industrial transformation and major adjustments in the global manufacturing competitive landscape, China faced both major opportunities and major challenges — with opportunities outweighing challenges.

In summary, we can understand these gaps, which were difficult to fundamentally change in the short term, as the reason China was officially classified in the "third tier" at that time.

So, five years have passed from Minister Miao's 2015 speech to now. What changes have occurred in Chinese manufacturing? Have those gaps changed? Are we still in the third tier?

/ 02 /

Five Years On, What Has Changed in Chinese Manufacturing? What Does It Look Like Now?

Let's start with the fundamentals and look at how the relevant data has changed.

▍ Manufacturing Value Added

Manufacturing value added reflects a country's productivity level and symbolizes manufacturing strength. According to World Bank data, measured in current US dollars, China's manufacturing value added first surpassed that of the US in 2010, making it the world's largest manufacturing country, a position it has held continuously ever since. From the curve above, we can clearly see that starting from 2010, the gap between the US in second place and China's industrial value added has generally widened, with China's lead becoming increasingly pronounced after 2016.

▍ Annual Growth Rate of Industrial Value Added

From a growth rate perspective, from 2015 to 2018, China's industrial value added maintained annual growth of nearly 6% on an already high base. According to China's National Bureau of Statistics, national industrial value added of enterprises above designated size grew 5.7% year-on-year in 2019.

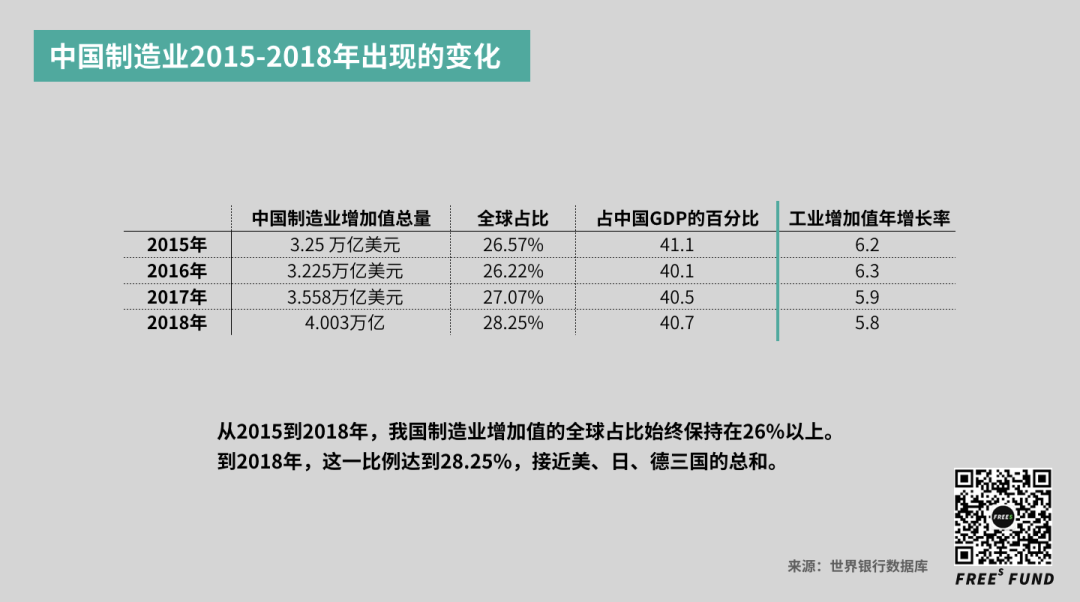

▍ Contribution to Global Manufacturing

From 2015 to 2018, China's share of global manufacturing value added remained above 26%, reaching 28.25% by 2018 — close to the combined total of the US, Japan, and Germany. Additionally, from 2015 to 2018, global manufacturing value added increased by $1.94 trillion in total, with China alone contributing $0.75 trillion of that growth, or 38.8%.

Undoubtedly, from a macro data perspective, over these five years, China's position as the "world's largest manufacturing country" has been further consolidated, providing key momentum for global manufacturing growth. So, have the gaps Minister Miao mentioned changed?

Our basic assessment is that these five years have seen enormous change. China's industrial structure is undergoing significant transformation. We have not simply stopped at driving growth through factor endowments. In some key mid-to-high-end advanced manufacturing sectors, we have made notable breakthroughs. A typical manifestation is that we are now producing products that are increasingly difficult to manufacture (higher technological value-added) and increasingly expensive (greater profit margins).

Below, we examine three widely recognized high-tech, high value-added industries — electronics, automobiles, and semiconductors — to see what changes have occurred in these sectors over the past five years.

/ 03 /

In the "Hardest to Make" Sectors of Consumer Electronics, Semiconductors, and Automobiles, How Internationally Competitive Is Made in China?

▍ Apple vs Huawei: One Migrating Toward China, One Decoupling from America & Localizing

For consumer electronics, let's take the most familiar example: smartphones.

As one of the most valuable technology companies, Apple has always represented the advanced level of global smartphone manufacturing. Because its products are premium and technologically complex, its requirements for supply chain partners are extremely demanding.

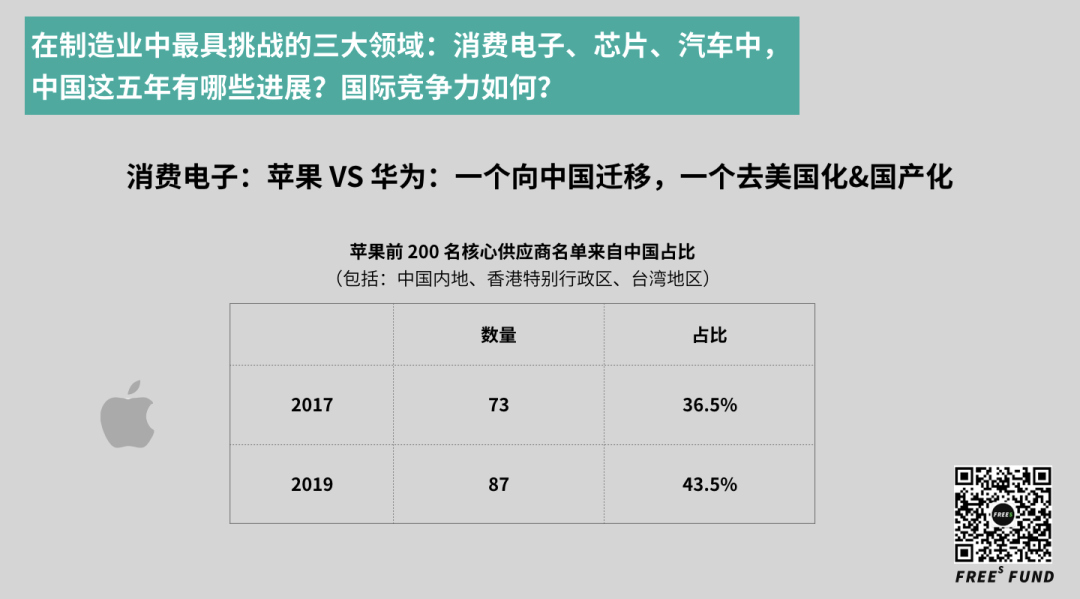

Starting in 2012, Apple has published an annual list of its top 200 core suppliers. These companies provide Apple with materials, manufacturing, and final assembly services. In Apple's 2017 top 200 core suppliers list, companies from mainland China, Hong Kong SAR, and Taiwan totaled 73, accounting for approximately 36.5%. By 2019, the top 200 list included 87 companies from mainland China, Hong Kong SAR, and Taiwan, with the share rising to approximately 43.5%. Among them, mainland Chinese suppliers have grown increasingly important in Apple's supply chain system, breaking through 40 companies for the first time in 2019, accounting for 20% of the top 200 suppliers.

Over these two years, the number of newly added companies from China (mainland, Hong Kong, Taiwan) was comparable to the combined total of Germany (6), Singapore (3), the Netherlands (3), and Finland (2). Meanwhile, China's total number of listed suppliers also surpassed the combined total of the US (38) and Japan (38).

This string of data makes it abundantly clear that within the mobile phone segment specifically, Chinese manufacturing's global competitiveness has been steadily climbing. According to Industrial Securities data, from a CKD (complete knock-down) perspective, roughly 75% of global phone production capacity sits in China, about 10% in Vietnam, about 10% in India, and about 5% elsewhere.

On one hand, we're seeing China's rise in both phone production capacity and high-quality supplier resources. On the other, we're witnessing certain domestic phone brands actively reducing their reliance on American component suppliers, replacing them with domestic parts or diversifying their supplier base.

The emblematic case is Huawei — Apple's main rival in the China market. We all know that over the past two years, and especially since around April or May of last year, Huawei has undergone an extraordinarily pressured supply chain transformation under relentless US sanctions and crackdowns. This was grueling work: the phone industry chain is long, the technology complex, and the interdependencies deep. But Huawei had no choice — it had to fight with its back to the wall. So what do the interim results look like?

At the end of 2019, professional teardown firm TechInsights published its disassembly report on Huawei's flagship Mate 30 and Mate 30 Pro 5G. The report found that Huawei HiSilicon's self-designed chips accounted for more than half of the Mate 30 series' components; meanwhile, the proportion of American components dropped sharply, replaced by suppliers from Japan, South Korea, and China.

TechInsights listed the main self-developed chips adopted: 5G SoC, power management IC, audio codec, LNA/RF switch, PA (power amplifier), RF transceiver, and others. The remaining American components were minimal — including Qualcomm's RF front-end modules, Cirrus Logic's audio amplifiers, and Texas Instruments' MIPI switches. In critical RF domains, Huawei had already found alternatives, eliminating the need for equipment from American majors Skyworks and Qorvo.

By late 2019 and spring 2020, American components' presence in Huawei's new phones diminished further. Teardowns showed that in the Huawei nova6 5G released in late 2019 — out of 1,848 total components — Chinese parts numbered 210, just 11.4% by quantity, yet accounting for a whopping 60.7% of total cost. This meant the nova6 5G had already reached 60% localization. At the same time, components from the US numbered just seven, representing a mere 0.6% of cost. Similarly, the Huawei P40 released in April 2020 contained only two RF chips from the US, with negligible cost impact.

It's evident that Huawei's "de-A" initiative — eliminating absolute dependence on American ("A") components — is bearing fruit. Huawei is pulling through its darkest hour by reshaping its supply chain. In the long run, this push for self-sufficiency will further cement China's domestic high-tech supply chain as a critical node.

Of course, supply chain controllability doesn't mean going it alone. The globalization of the phone industry chain has deep roots, and Huawei still makes extensive use of components from Japan, South Korea, and elsewhere. Technological self-sufficiency solves the "stranglehold" problem in key industries, but it doesn't mean severing globalized supply chains. Partnering with the world's most innovative companies remains crucial for any brand's long-term development.

New Energy Vehicles 2015–2019: China's Sudden Emergence

Like mobile phones, new energy vehicles (NEVs) represent an industry with long, complex, and highly technology-intensive supply chains marked by deep interdependencies. It's another textbook domain for observing China's manufacturing capability gains.

Since becoming the world's largest NEV market in 2015, China has held onto that top spot. From 2014 to 2017, China's NEV sales were 75,000, 331,000, 507,000, and 777,000 units respectively. Based on the Ministry of Industry and Information Technology's industry projections, total NEV sales for 2018–2020 were estimated at 1 million, 1.52 million, and 2.14 million units.

As one of China's seven strategic emerging industries, NEVs benefited enormously from a suite of policies rolled out around 2015: exemption from license plate lotteries and purchase restrictions, consumption tax waivers, subsidy programs, and more. These dramatically stimulated industry growth. So how has China's car-making capability evolved over these past five years?

Compared to conventional vehicles, NEVs' core technologies are battery, motor, and electronic control. These three also represent the bulk of an NEV's cost. According to Digitimes estimates, the battery accounts for 40–50% of total vehicle cost, while the drive system (including motor and electronic control) makes up 15–20%.

Next, we'll examine China's technological progress in NEVs over these five years through the lenses of battery, motor, and electronic control.

- Battery: Domestic power battery makers now rank in the global top tier

Lithium-ion batteries are currently the most popular power source for NEVs, dubbed the "lifeline" of new energy vehicles.

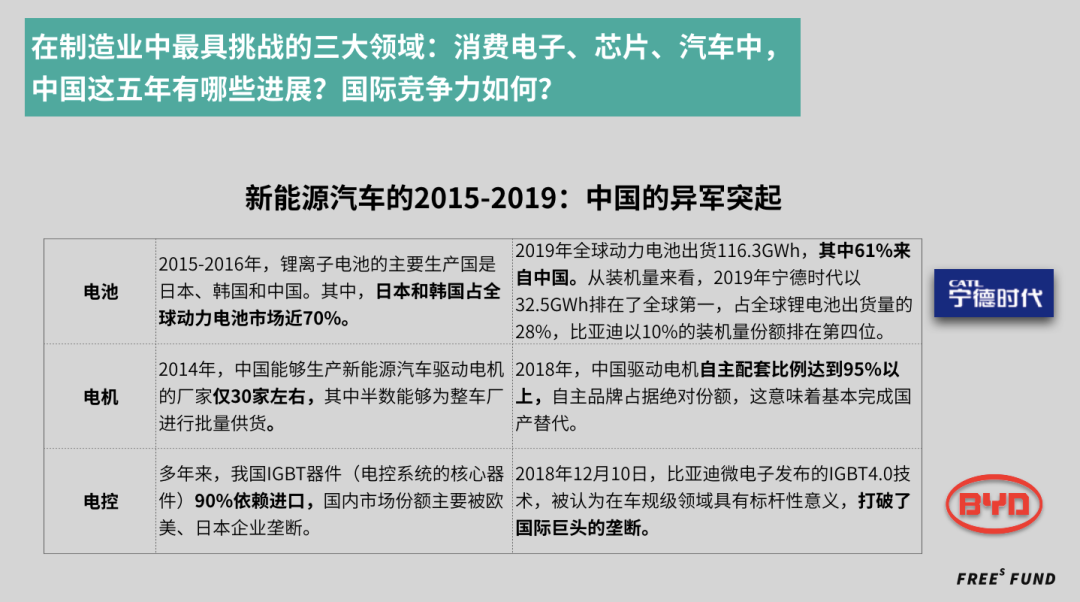

According to Zhiyan Consulting data, in 2015–2016, the main lithium-ion battery producers were Japan, South Korea, and China. Japan and South Korea together held nearly 70% of the global power battery market. Through subsequent years of development, China's power battery industry chain has become relatively complete. By 2017, China's power battery output reached 44.5 GWh, basically satisfying domestic demand. Over the following two-plus years, the Japan-Korea-dominated lithium battery landscape gradually broke apart, and China entered the global top tier — accompanied by intensifying market competition and rising industry concentration.

Per SNE Research data, in 2016 the top ten global power battery makers held 73.6% market share, with domestic brands occupying six spots and a combined 44.8% share.

By 2019, again according to SNE Research, global lithium-ion power battery shipments reached 116.6 GWh, up 16.6% year-over-year. Among the top ten manufacturers, domestic brands held five positions: CATL, BYD, Envision AESC, Gotion High-tech, and Lishen — together accounting for approximately 45.1% of global market share. By installed capacity, CATL led the world again in 2019 with 32.5 GWh, representing 28% of global lithium battery shipments. On both growth rate and shipment volume, CATL was widening its gap over second-place Panasonic.

- Motor and electronic control: Motors largely domestically substituted; IGBT for electronic control achieves domestic breakthrough

Another core component that long constrained China's NEV mass production was the motor drive system. Comprising the drive motor and motor controller, it determines the vehicle's primary performance characteristics.

The NEV market's growth acceleration also drove development of the NEV drive motor market. According to public reports, in 2014 only about 30 Chinese manufacturers could produce NEV drive motors, with roughly half able to supply vehicle makers in volume. By 2018, China's drive motor self-supply ratio exceeded 95%, with domestic brands holding absolute share — meaning domestic substitution was largely complete.

As domestic motors developed rapidly, so too did motor controllers — the control center of the entire power system. Taking the IGBT module, the core device in electronic control systems, let's examine the data changes in recent years.

Demand-side growth. According to Zhiyan Consulting, the 2018 global IGBT market was $5.836 billion, growing 11.06% with a five-year CAGR of 13.84%. China's 2018 IGBT market was 16.19 billion RMB, growing 22.19% with a five-year CAGR of 18.77%.

China's domestic market now accounts for roughly 40% of the global market, with faster growth than the global average. China has become the world's largest IGBT demand market.

Supply-side breakthrough. IGBT technology barriers manifest in three aspects: high design thresholds, difficult manufacturing, and large capital requirements. Previously, about 90% of China's IGBT devices relied on imports, with domestic market share dominated by European, American, and Japanese enterprises. In recent years, though imports still predominate, cracks have appeared in this monopoly — with BYD as the representative player.

According to public information, BYD began assembling an IGBT R&D team in 2005, formally entering the IGBT field. After more than a decade of development, on December 10, 2018, BYD Microelectronics released its IGBT 4.0 technology, considered benchmark-setting for automotive-grade applications and breaking the international giants' monopoly.

Currently, BYD Semiconductor has become China's largest independently controllable automotive-grade IGBT manufacturer, with a complete IGBT industry chain spanning IGBT single crystal, epitaxy, chip design, packaging and manufacturing, module design and manufacturing, high-power device testing application platforms, and power supply and electronic control. This has laid groundwork for the domestic substitution of NEV IGBTs.

In summary, we can see that when the world's largest consumer market meets a relatively long industry chain, supplemented by appropriate policy guidance, it creates fertile soil for NEV industry chain upgrading. Across the three core technology domains of NEVs, China's domestic power battery makers now rank in the global top tier, motor production has largely completed domestic substitution, and IGBT for electronic control has achieved domestic breakthrough. This is what has happened over these five years.

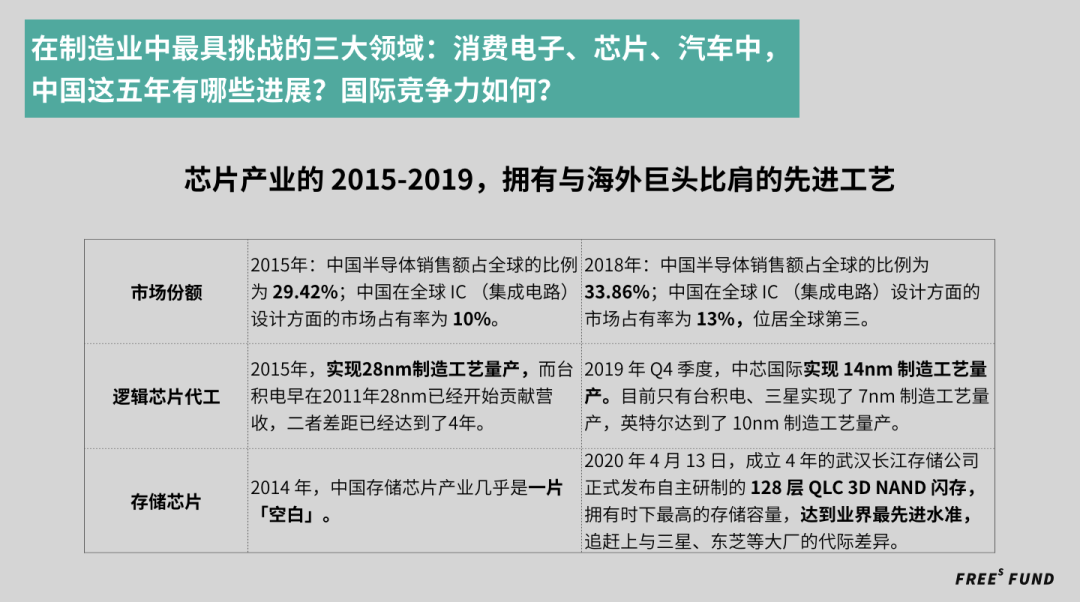

The Chip Industry 2015–2019: Advanced Processes on Par with Overseas Giants

Whether measured by Chinese semiconductor products' share of global market, or by Chinese companies' mastery of key technologies like wafer fabrication and memory chips, China's chip industry has been achieving leapfrog development in recent years.

China's share of the global semiconductor market has been steadily climbing. From 2015 to 2018, Chinese semiconductor sales as a percentage of global sales rose from 29.42% to 33.86%. China's share of global IC (integrated circuit) design grew from 10% to 13%, ranking third worldwide.

In the logic chip foundry sector, Chinese companies currently trail the established chip giants by roughly one process generation.

In 2015, SMIC achieved mass production at the 28nm node. TSMC's 28nm process had already begun generating revenue back in 2011 — a four-year gap.

In Q4 2019, SMIC achieved mass production at the 14nm node. This process technology could satisfy 95% of domestic chip production needs and had already begun contributing $7.69 million in revenue, accounting for 1% of total quarterly revenue.

In the logic chip foundry space where SMIC operates, only TSMC and Samsung had achieved mass production at the 7nm node, while Intel had reached 10nm. Due to the massive R&D investments required for advanced nodes, other players like GlobalFoundries and UMC had already announced they would halt development of processes beyond 14nm.

In the memory chip sector, China's memory industry was virtually a "blank slate" in 2014. By 2018, memory chips accounted for 34% of the global semiconductor market by major product segment.

By 2019 and 2020, Chinese memory companies had achieved technology on par with overseas giants. On September [date], 2019, ChangXin Memory Technologies (CXMT) in Hefei announced mass production of DDR4 memory, becoming China's first domestic memory supplier.

On April 13, 2020, Yangtze Memory Technologies (YMTC), founded just four years prior, officially released its independently developed 128-layer QLC 3D NAND flash memory — featuring the highest storage capacity available at the time and reaching the industry's most advanced standard, catching up to major players like Samsung and Toshiba.

/ 04 /

Minister Miao Wei's View of Made in China, 2016–2019

Finally, returning to Minister Miao's 2015 speech, let's examine how "Made in China" evolved in his eyes over the subsequent four and a half years. Below are excerpts from his public remarks:

- 2016: "Stabilizing after slowing, improving amid stability, enhancing quality and efficiency"

"For 2016's industrial performance, three phrases capture it: stabilizing after slowing, improving amid stability, enhancing quality and efficiency. Industry reversed the sharp decline in production growth and profitability seen the previous year. High-tech manufacturing accounted for only 12.4% of total manufacturing value-added at year-end — meaning over 80% remained traditional industries. In fact, these too are accelerating their development. At the same time, we must pay even more attention to that 80%-plus of traditional industries, upgrading them through transformation to become emerging industries. We must not completely separate or oppose these two categories." From "MIIT Briefing on 2016 Industrial and Telecommunications Development"

- 2017: "Steady progress, improving stability, with quality and efficiency rising in tandem"

"The accelerating integration of internet and production is helping transform and upgrade the real economy. Currently, nearly 40% of China's digital production equipment is networked, over 30% of manufacturing enterprises have achieved collaborative networking, and over 20% have adopted service-oriented manufacturing. In 2017, high-tech manufacturing value-added grew 13.4% year-on-year, 6.8 percentage points faster than overall industrial enterprises above designated size. Electronics manufacturing grew 13.8%, equipment manufacturing 10.7% — together contributing 3.2 percentage points to overall industrial growth. Standout products include industrial robots, with output up 68.1% from the previous year, and new energy vehicles, up 51.1%." From "MIIT Briefing on 2017 Industrial and Telecommunications Development"

- 2018: "Overall stability, steady progress, with some moderation"

"In 2018, national industrial enterprises above designated size saw profits grow 10.3% year-on-year, outpacing the 6.2% value-added growth rate, indicating that profitability improvement exceeded value growth. Particularly worth noting: industrial investment steadily rebounded, growing 6.5% in 2018, accelerating 2.9 percentage points from the previous year. Manufacturing investment grew 9.5%, the fastest since July 2015, rising for nine consecutive months. The input-output relationship in industry means today's investment invariably brings tomorrow's output. The sustained growth in manufacturing investment strengthens our confidence in future development. Of this manufacturing investment, nearly 50% went to technological transformation — not capacity- or scale-expanding extensive investment growth, but rather investment to improve product structure, industrial structure, and upgrade toward the mid-to-high end of the value chain. The supporting role of new drivers strengthened continuously: high-tech manufacturing value-added grew 11.7%, significantly outpacing overall industrial growth of 6.2%; equipment manufacturing grew 8.1%, also above the 6.2% overall rate — all results of industrial restructuring." From "State Council Information Office: 2018 Industrial and Telecommunications Development"

- 2019: "Seeking progress while maintaining stability"

"In 2019, withstanding pressures large and small, we stabilized industry as the 'ballast stone.' Our industry possesses the world's most complete industrial system, ultra-large-scale market advantages and domestic demand potential, vast human capital and talent resources, competitive new infrastructure, and deepening reform and opening-up with ample policy space — all of which will further enhance the resilience of industrial economic development. Particularly, we have institutional advantages: under the centralized and unified leadership of the Party, we unify understanding and work together toward common goals. We also have the distinctive advantage that 'socialism can concentrate resources to accomplish major tasks,' all of which strengthen our resilience and room to maneuver in responding to internal and external shocks and challenges. I said at this same time last year that 5G, beyond solving communication between people, will to a greater degree solve communication between things, and between things and people. Roughly estimated, about 20% will be used in traditional consumer IoT, 80% in IoT particularly industrial internet." From "State Council Information Office Press Conference on 2019 Industrial and Telecommunications Development"

So you see — the world keeps changing. From Minister Miao's 2015 speech to today, our manufacturing sector has undergone five years of rapid development. At this critical juncture of climbing uphill and transitioning from large to strong, we face both major opportunities and major challenges — but the opportunities certainly outweigh the challenges.

(Sun Qianhui and Shan Chengchao also contributed to this article.)

Key Takeaways

1 From a macro perspective, over these five years, China's position as "world's largest manufacturing country" has been further consolidated, providing crucial momentum for global manufacturing growth.

2 2015–2019 was a period of tremendous change. China's industrial structure is undergoing significant transformation. We have not remained stuck relying purely on production factor advantages. In certain key advanced manufacturing sectors at the mid-to-high end, we have achieved notable breakthroughs. One telling indicator: we are increasingly producing products that are harder to manufacture (higher technology value-added) and more expensive (greater profit margins).

3 What happened over these past five years: whether measured by Chinese semiconductor products' share of global market, or by Chinese companies' mastery of key technologies like wafer fabrication and memory chips, China's chip industry has been achieving leapfrog development. In the three core technology areas of new energy vehicles, domestic power battery manufacturers now rank in the global top tier, electric motors have essentially completed domestic substitution, and IGBT power modules have achieved domestic breakthroughs. Additionally, in the smartphone industry, we have witnessed China's rise in production capacity and quality supplier resources, while also seeing top domestic phone brands reduce their reliance on American supplier components and simultaneously increase localization levels.

Discussion Question

Q: Minister Miao Wei repeatedly mentioned industrial restructuring. In your view, can China become a country capable of developing high-tech manufacturing? Welcome to hit "Like" at the end of this article, then reply "high-tech" in our backend to receive our answer.

(Welcome to read, share, and hit "Like." For reprint requests, please reply "reprint" to learn our reprint policies and contact FreeS Xiaorui [ID: freesfund] for authorization. Copyright belongs to FreeS Fund.)

A Visual Guide to Globalization vs. Deglobalization | Li Feng Column 2020: The Travel Industry's Reset and Restart | Frees Fund After the Pandemic: Education's Survival Tournament | Frees Fund After the Pandemic: The New Landscape for Fresh Produce, Restaurants, and Food | Frees Fund After the Pandemic: A New Era for "Good Companies" | Frees Fund Li Feng Column 16 | Fresh Retail: Learning Early-Stage Investing from the Secondary Market Li Feng's New Year Outlook | A Visual Guide to China's Opportunities in 2020