What Makes the Low-ABV Alcohol Markets in China, the US, and Japan So Different? | FreeS Research

Where does China's unique opportunity lie?

Low-ABV alcohol has been one of the hottest sectors in recent years, drawing considerable interest from entrepreneurs and attracting growing capital inflows. Three months ago, FreeS Fund Report No. 19 looked back at the rise of Suntory and White Claw, and explored the trends in China's current low-ABV alcohol entrepreneurship. In that issue, we focused on analyzing the sociocultural factors behind low-ABV alcohol's market success, shifts in consumer demand, and changes in media and distribution methods.

In today's article, we introduce a new variable: "tax policy." This is an unavoidable factor when examining the development of low-ABV alcohol. After studying the history of alcohol taxation in Japan, the US, and China, we found:

- Changes in tax rates have had a direct impact on the emergence of new low-ABV alcohol varieties and the rise and fall of different categories in Japan and the US. Take Japan as an example: beer's high tax rate, often reaching 40% of its selling price, drove manufacturers to develop low-ABV alternatives to avoid taxes. Interestingly, the government always raised taxes on these new categories after they emerged.

- How significant tax policy's impact is depends on how different countries classify different alcohol types and the foundation of their past tax policies. In the US, for instance, in New York State, the tax rate on distilled spirits is 7 times that of beer. It makes perfect sense that brands like White Claw chose a beer-like fermentation process, because they could be taxed as beer and enjoy that tax advantage. Of course, this was only one of several things White Claw did right.

- Looking at China, its unique alcohol tax system — with spirits, beer, and low-ABV alcohol all taxed at around 10%, with little difference between them — means low-ABV brands cannot benefit from tax rate advantages. Low-ABV entrepreneurs need to forge a growth path with more Chinese characteristics.

FreeS Fund continues to pay attention to investment opportunities in the consumer sector. We welcome business plans sent to bp@freesvc.com, and welcome you to contact Feng Xiaorui (WeChat ID: freesfund).

We'll use 4 short videos

to tell you the biggest differences between low-ABV alcohol in China, the US, and Japan — and why

Click to watch Episode 1 👆

Welcome to scan the QR code and follow FreeS Fund's video channel

Low-ABV Alcohol and Tax Policy: A China-Japan-US Comparison

By Shao Shili

Low-ABV Alcohol in Japan: A Multi-Round Game with Alcohol Tax Policy

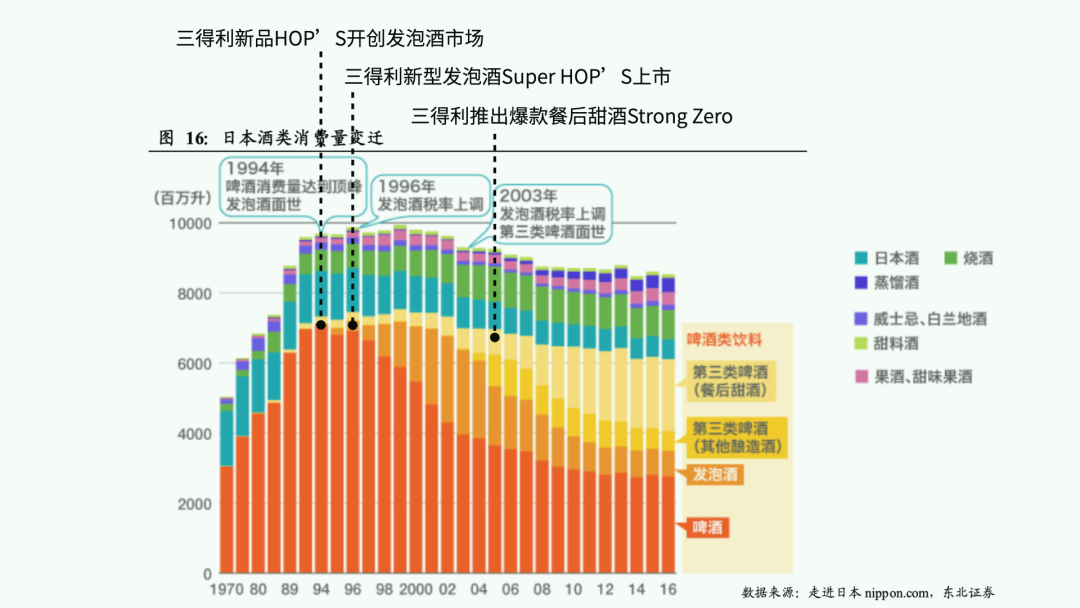

First, the conclusion. From 1994 to 2003, three adjustments to Japan's alcohol tax drove the emergence of many new categories and products. Happoshu (sparkling liquor) and dessert liquor, among others, all followed this pattern.

Japan is a rare major country with an inverted beer tax rate: beer is taxed higher than spirits, and beer also represents the largest alcohol tax base. Beer tax in Japan exceeds 40% of its selling price, even approaching 50%.

According to Japan's tax code definition, initially only beverages with over 67% malt content qualified as beer. This prompted manufacturers to repeatedly develop products with lower malt concentrations to avoid taxes.

In 1994, beer tax was 222 yen per liter, while happoshu with 50-67% malt content was taxed at 152 yen per liter — a third lower. To gain the price advantage from this lower tax rate, Japan saw a boom in happoshu production. From the chart below showing changes in Japan's alcohol consumption, we can clearly see that the orange bars representing happoshu began rising in 1994 and 1995. Also in 1994, Suntory launched its happoshu product HOP'S.

By 1996, Japan revised its tax code to require 50-67% malt content happoshu to be taxed the same as beer. This made the price advantage of 50-67% malt content happoshu less pronounced. The result: manufacturers developed new happoshu with even lower malt content (below 25%), including Suntory's Super HOP'S developed in 1996. The orange section representing happoshu saw significant growth after these two consecutive policy changes in 1994 and 1996, and began capturing market share from beer at a relatively rapid pace.

Around 2003 marked the peak of happoshu's market share (the two years with the longest orange bars in the chart).

The game between manufacturers and policymakers continued. In 2003, to increase tax revenue, the Japanese government raised taxes again on happoshu with below 25% malt content. The result: "third-category beer" — with 0% malt content or mixed with distilled spirits, fruit juice, and other ingredients — began emerging and capturing market share from beer and happoshu. Suntory's Strong Zero, launched in 2005, stands out among these, with annual revenue now exceeding 10 billion RMB from this single product.

Third-category beer comes in two types: one is "other brewed liquor," fermented with alternative bases like peas or corn instead of malt; the second is "dessert liquor" (including what we now commonly call "ready-to-drink cocktails"), made by mixing happoshu with below 50% malt content with distilled spirits and other ingredients. Distilled spirits use a different process from beer and happoshu, and if malt accounted for less of the beverage than distilled spirits, fruit juice, or other ingredients, it wouldn't count as happoshu under Japan's tax code at that time, thus avoiding the relatively higher tax rate.

Corresponding to Japan's alcohol consumption change chart, other brewed liquor and dessert liquor are represented by the light yellow and dark yellow areas; among them, the light yellow area representing dessert liquor has shown clear growth since 2003, becoming a significant player in Japan's alcohol market.

In summary, three adjustments to Japan's alcohol tax brought forth new products across different alcohol categories.

Specifically, how significant can alcohol tax's impact be? Analyzing the proportion of alcohol tax to price gives us part of the answer.

A 350ml can of beer retails for 221 yen in Japan, with alcohol tax plus consumption tax accounting for 45% of the selling price. A 350ml can of happoshu retails for 164 yen in Japan, nearly 40% cheaper than beer. The alcohol tax plus consumption tax proportion is slightly lower, but still reaches 39%. Excluding consumption tax and looking only at alcohol tax, the retail price difference is 57 yen (221-164), while the alcohol tax difference is 30 yen (77-47) — the alcohol tax difference contributes 52% of the retail price difference.

Similarly, non-malt happoshu and blended happoshu (the two types of third-category beer just mentioned) are 56% cheaper than beer, and the proportion of alcohol tax difference to retail price difference is even larger, exceeding 60%.

Therefore, overall, changes in alcohol tax have an enormous impact on product selling prices. This explains why manufacturers continuously research and launch new low-ABV alcohol formats to circumvent high-tax categories, thereby selling new alcohol products with significant price advantages.

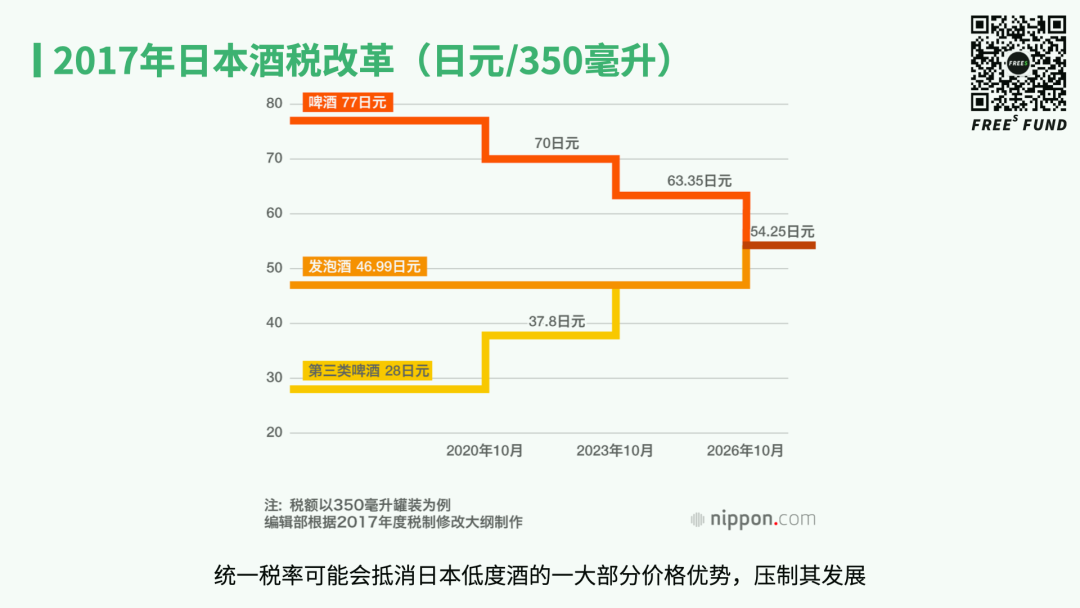

In 2017, Japan's tax rates saw new adjustments. Previously, the base tax rates for beer, happoshu, and third-category beer differed considerably, roughly forming high, medium, and low tiers. In 2017, the Japanese government announced plans to equalize tax rates across these three categories by 2026. Undoubtedly, this means a large portion of low-ABV alcohol's (or rather, non-beer alcohol products') price advantage will disappear again due to tax adjustments. Japan's alcohol market landscape will likely change further.

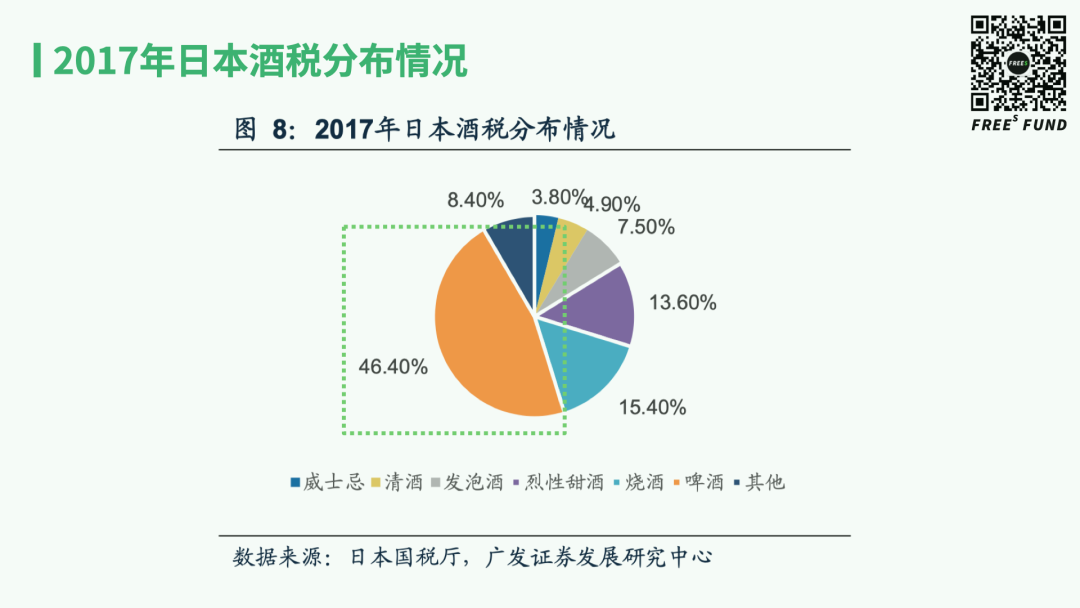

Why has Japan been so focused on beer's tax rate and insisted on maintaining its high rate for so many years? There are historical reasons behind this. During the Russo-Japanese War, Japan raised beer taxes to expand military spending. As beer became increasingly accessible and mainstream, beer consumption became one of the government's important revenue sources. In 2017, beer contributed 46.4% of Japan's alcohol tax revenue. Additionally, Japan's beer raw materials are relatively import-dependent, and high beer consumption would increase Japan's reliance on other countries. Clearly, the Japanese government was reluctant to become overly dependent on foreign countries, so beer taxes were set relatively high.

In 2017, Japan's new alcohol tax policy began unifying tax rates across different alcohol categories, meaning raising taxes on happoshu and third-category beer while lowering beer tax rates. The reasons behind this are worth exploring. One plausible speculation: after nearly 50 years of development, other alcohol categories including happoshu and third-category beer have become incremental markets occupying larger market shares, with consumption far exceeding beer. Raising taxes on these growing categories is a more profitable approach for the government.

Low-ABV Alcohol in the US: Low Beer Tax Rates Drive Malt-Based RTDs to Capture the American Market

The US alcohol tax system classifies alcohol into two categories by manufacturing process: distilled spirits and fermented liquor. Distilled spirits are typically what we call baijiu or whiskey and other spirits; beer belongs to fermented liquor.

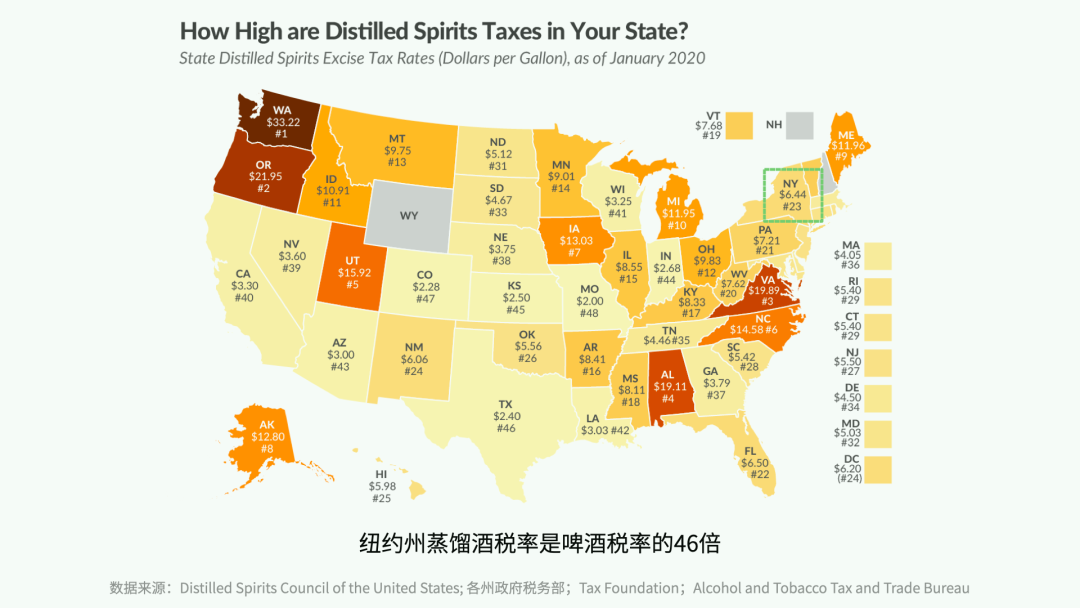

The two charts below show tax rates for beer and distilled spirits across US states. In New York State, for example, the state tax on beer is $0.14 per gallon, while the state tax on distilled spirits is $6.44 per gallon. That makes the latter 46 times the former. This is not an isolated case. The state tax rates on distilled spirits and beer generally differ significantly across the US, by roughly 10 times.

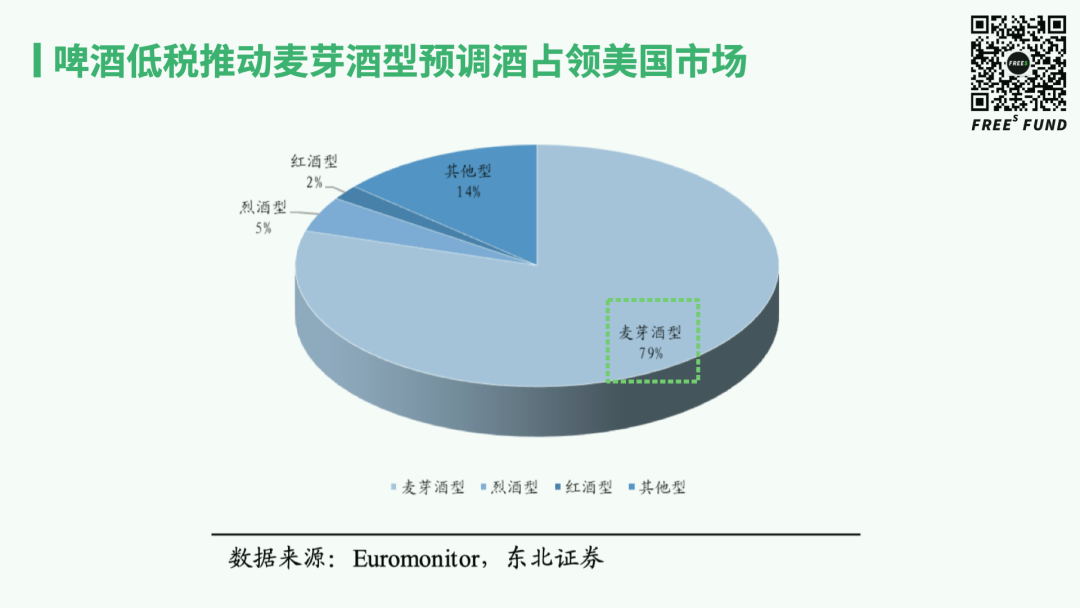

When low tax rates translate to low prices, they stimulate more consumption. As a result, in the US market, malt-based beverages using fermentation processes (typically beer) occupy 79% of the market, more than 3 times the combined market share of spirits-type, wine-type, and other-type alcohol. Among these, numerous American RTD producers have taken advantage of beer's low tax rates to mass-produce malt-based RTDs. White Claw, the popular RTD favored by young people, is one such example.

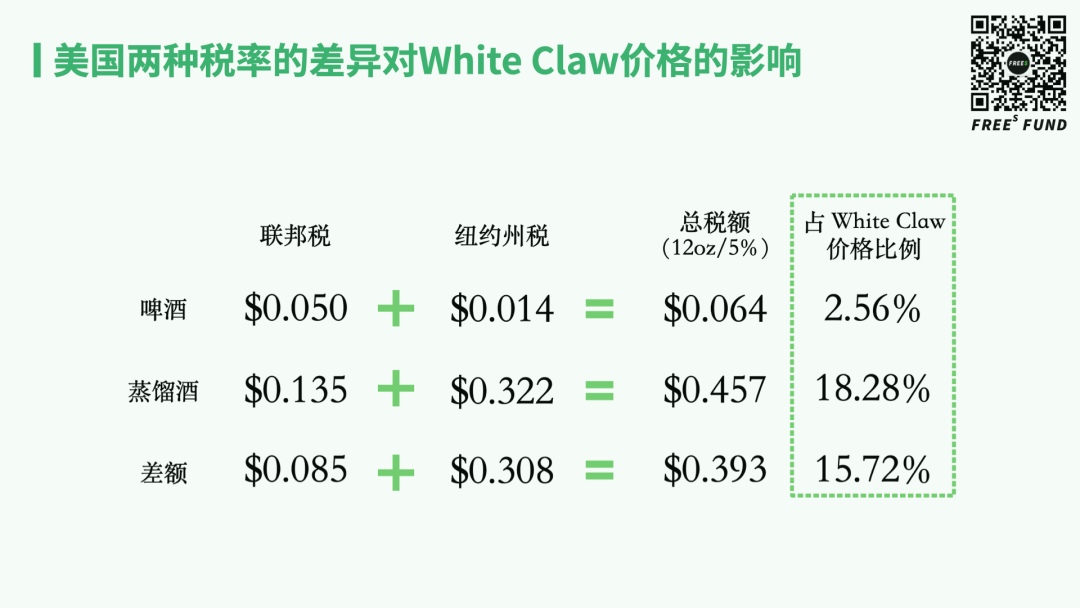

How significant is the impact of tax rate differences on specific products? A single can of White Claw sells for $2.50; with a fermented liquor base, federal tax plus New York state tax combined accounts for 2.56% of its price. If its base were switched to distilled spirits, the combined federal and New York state tax proportion would rise to 18.28% — a difference of about $0.40 per can in alcohol tax. This tax rate difference would affect a single can of White Claw's standalone price by 15.72%.

If buying a 12-can pack of White Claw, the current price is around $16 per case; if switched to a distilled spirits base, the price would increase by nearly $5, about 30% of a case's price.

At the beginning of this article, we mentioned that enjoying the low tax rate on fermented liquor in the US was one of several things White Claw did right. Beyond that, what else did it do right? A crucial point: paying attention to and embracing changes in consumer taste preferences.

Previously, large quantities of American RTDs used beer as a base, adding some sugar and fruit flavors. While this could mask beer's strong malt flavor, the taste was cloyingly sweet, lacking in refreshment, and labeled as insufficiently healthy due to excessive artificial additives. White Claw's innovation was that, also using fermentation processes, it switched the base from malt to cane sugar, resulting in a cleaner, more refreshing taste — no need for additional sugar or other flavorings to remove the beer taste.

This new fermentation process both capitalized on beer's low tax rate and catered to consumer taste preferences, forming an important part of White Claw's success formula. In a sense, it's a drink with spirits-like flavor at beer tax rates.

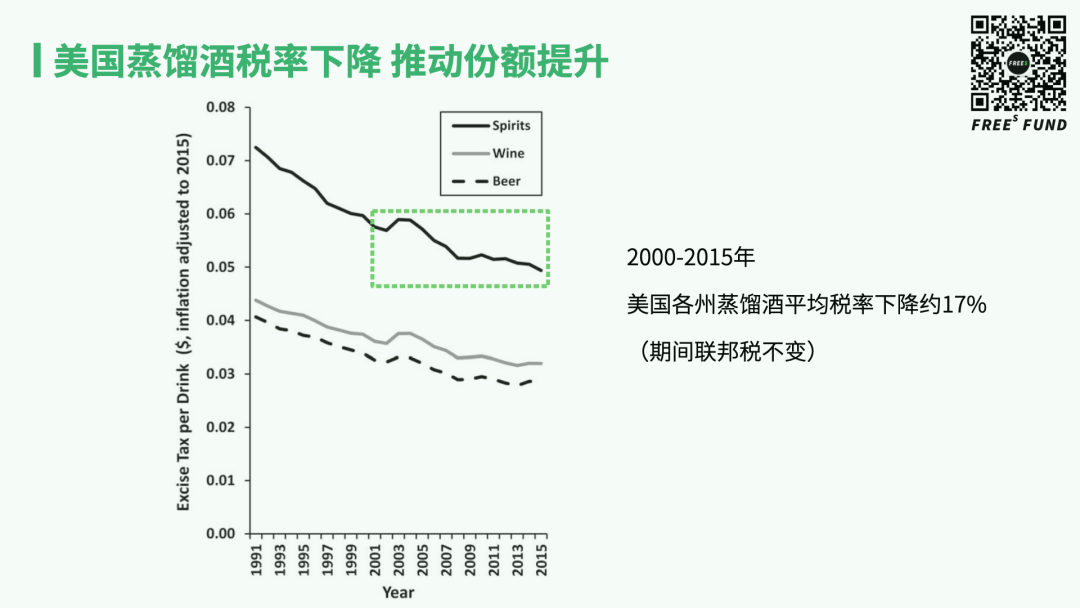

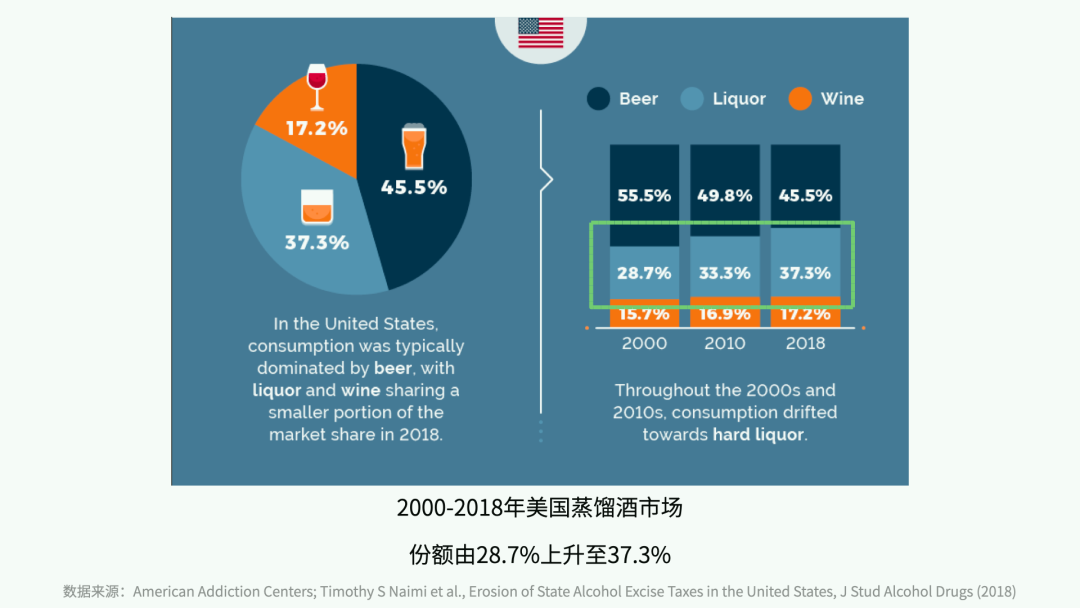

Tax rates' impact on alcohol consumption can also be observed from a more macro perspective. Extending our timeline, looking at changes in US distilled spirits tax rates and market share since 2000, we can clearly perceive the connection between the two. Compared to 2000, by 2015 the average distilled spirits tax rate across US states had dropped by about 17%. Correspondingly, since 2000, US distilled spirits market share began rising; by 2018, distilled spirits' market share had increased from 28.7% in 2000 to 37.3%. Put simply, after distilled spirits (spirits) tax rates dropped by nearly 20%, their market share rose by about 10%.

/ 03 / China-Japan-US-Europe Comparison, and Opportunity Analysis for China

As mentioned earlier, Japan's alcohol tax has certain particularities — tax rates are relatively high, with beer, shochu, and happoshu tax rates typically reaching 30-40%, while sake's tax rate is about 20%. This higher tax base motivates manufacturers to develop new categories to achieve tax savings.

The US also shows clear tax differences between distilled spirits (typically spirits) and low-ABV alcohol, giving manufacturers strong motivation to develop low-ABV alcohol to enjoy lower tax rates. The EU situation is similar.

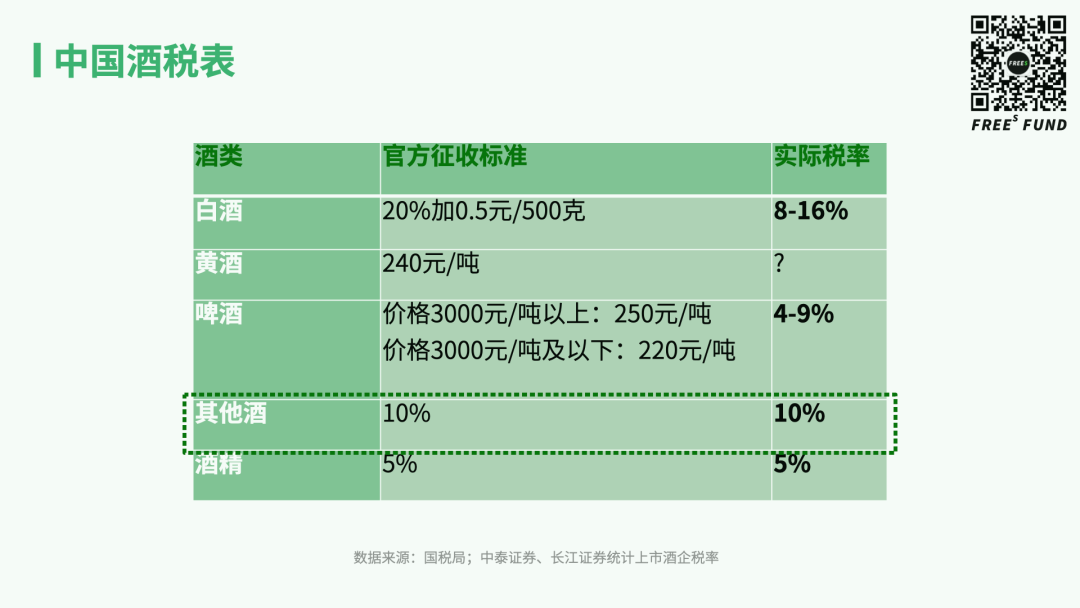

In China, calculating from the proportion of alcohol tax to price, most alcohol categories are taxed at around 10%. Baijiu's actual tax rate falls between 8-16%, beer is 4-9%, and many low-ABV alcohols including RTDs and blended liquors are taxed as "other alcohol" at about 10%. In other words, China's low-ABV alcohol tax rate is higher than beer's, and not much different from baijiu's concentrated rate of around 12%. Therefore, Chinese RTD or common low-ABV alcohol brands have no obvious tax rate advantage. China's unique alcohol tax policy cannot serve as a key variable driving low-ABV alcohol development as it does in Japan and the US.

Comparative Research Summary

Japan: Beer dominates the market with high tax rates (40-50%), and its initially narrow definition of beer repeatedly prompted manufacturers to develop lower-ABV alcohol to reduce tax burdens. The government also consistently brought new categories back into high-tax brackets after their emergence.

US: Distilled spirits tax rates are several times higher than beer's, forming the soil from which White Claw emerged — allowing it to use beer's fermentation process (enjoying beer's tax advantage) while developing a product with spirits-like clean flavor (matching consumer demand).

China: Compared to Japan and the US, alcohol taxes are lower, with little difference in tax rates between categories. As new market entrants, low-ABV alcohol brands have no tax rate advantage, making tax-avoidance-motivated low-ABV product development relatively unlikely. China's low-ABV entrepreneurship needs to focus on other macro and micro variables to achieve greater development.

Discussion

What unique development opportunities exist for low-ABV alcohol in China? Welcome to share your thoughts in the comments.

▲ Surpassing Nestlé and Starbucks During 618 to Become #1 in Instant Beverages: What Did Saturnbird Do Right? | FreeS Research Institute — Learning from Investment