What Will Our Future Elder Care Look Like? | FreeS Fund Report 29

"When one nears the dusk of life, what is needed is not merely medicine, but living."

In a consumer market flooded with new products, elderly users seem like the "marginalized group" compared to the much-discussed younger demographic. While there's always someone young, we can't ignore the accelerating reality of China's aging population. China has become the first country in the world with over 100 million elderly people. What was once a "marginalized group" will become a defining force in the market. At this year's Two Sessions, the government made its position clear on the delayed retirement policy: it will be introduced prudently at an appropriate time after careful study and thorough deliberation. The latest proposal for institutional reform also formally put forward improvements to the aging-related work system, emphasizing the implementation of a national strategy for actively responding to population aging.

For individuals, macro factors such as increased life expectancy, delayed retirement policies, and personal pension schemes are prompting us to think: what kind of elderly life will we lead? Are we prepared for aging? How will we work, consume, and maintain our health when we're old? And most importantly, how will we live through our later years with autonomy, joy, and dignity?

Encouragingly, we're already seeing numerous business innovations with deep humanistic care. For example: elderly people wearing VR devices to immersively revisit places with special memories, thereby slowing cognitive decline; gyms without mirrors where middle-aged and older women can exercise freely without any "gaze"; shopping malls that open at 7 a.m. to match seniors' schedules, with walking paths throughout, dedicated to selling products for elderly consumers...

In this report, we'll explore what impact the silver economy will have on future society. How will it affect consumer markets? How will it shape employment and entrepreneurship? How can we identify and capture innovation opportunities under the aging trend?

If you're also interested in the silver economy, or starting a business in this space, you're welcome to contact the author of this article, Mingwang Fan from FreeS Fund, at kikofan@freesvc.com.

Interactive Giveaway What kind of retirement life do you hope for? What product innovations in the silver economy have you noticed? Share with us in the comments. The 5 most thoughtful commenters will each receive a copy of Being Mortal: Medicine and What Matters in the End.

/ 01 /

The First Country with Over 100 Million Elderly People

Today, we may be paying more attention to population issues than ever before. Discussions around delayed retirement policies, fertility promotion policies, and more have made population a topic closely intertwined with our daily lives.

However, if we look back at the long arc of human history, we'll find that for most of it, population was an inert variable. Human society long maintained a dynamic balance between high birth rates and high death rates. It wasn't until around 1800 that global population finally surpassed 1 billion, and by 1927, it had only expanded to 2 billion.

So when exactly did population become an active variable?

Starting in 1950, humanity entered what Japanese demographer Toshio Kuroda called the "Demographic Century." The world political and economic situation shifted from extreme turbulence to relative stability, and the population landscape changed fundamentally.

What is the Demographic Century? The first 50 years, from 1950, marked the fastest period of population growth in world history. The second 50 years, from 2000 onward, is the period of fastest change in population age structure.

How did population change in the first half of the Demographic Century? In 1950, global population was about 2.5 billion; by 1999, it had exceeded 6 billion. In just 50 years, world population more than doubled — an unprecedented phenomenon in human history. On November 15, 2022, global population reached a new milestone, surpassing 8 billion.

And the era we live in today is the second half of the Demographic Century — the period of most rapid and pronounced change in population age structure.

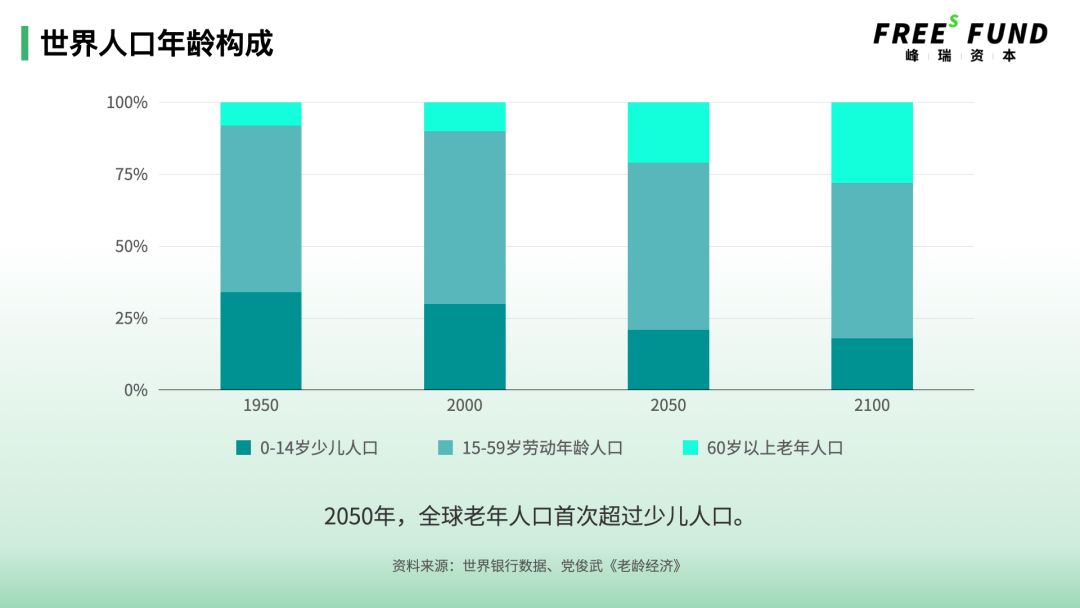

According to World Bank data and figures from The Silver Economy by Dang Junwu, a member of the Expert Committee of the China National Committee on Aging and deputy director of the China Research Center on Aging, globally in both 1950 and 2000, the population under 14 significantly outnumbered those over 60. In 1950, the proportions of global population aged 0-14, 15-59 (working age), and 60+ were 34%, 58%, and 8% respectively. By 2000, these figures became 30%, 60%, and 10%.

But by 2050, this age pattern will shift, with the elderly population reaching parity with children for the first time in history. By 2100, the composition of the three major age groups is projected to be 18%, 54%, and 28%, with the elderly share ultimately and significantly exceeding that of children — forming an inverted population pyramid never before seen in human history.

We need to note that this age distribution includes all countries in the world, especially developing countries with younger population structures. The aging trend may unfold even faster in China.

Why? Let's look at China's aging trajectory.

First, China has a large elderly population.

According to the 2021 National Bulletin on the Development of Aging Programs released by the National Health Commission and the China National Committee on Aging, as of the end of 2021, the population aged 60 and above was approximately 267 million, accounting for 18.9% of the total population; those aged 65 and above numbered about 200 million, or 14.2% of the total. This makes China currently the only country with an elderly population exceeding 100 million — the largest in the world.

Second, China is aging rapidly.

In 2001, China's population aged 65 and above reached 7% of the total, officially entering an aging society. By 2021, China had entered deep aging — a process that took only 21 years. This is far faster than France's 126 years, the UK's 46 years, and Germany's 40 years.

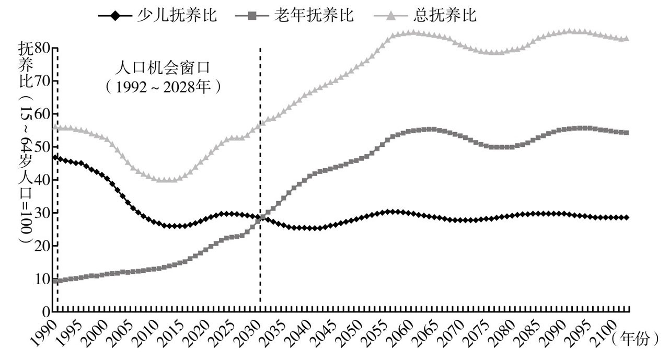

We can also examine structural change from another angle. Demography has a metric called the total dependency ratio: (population aged 0-14 + population aged 65+) / working-age population aged 15-64. When the total dependency ratio falls below 50, it means there are more workers relative to dependents, and the overall age structure is relatively young and healthy. The demographic window of opportunity refers to the period when the total dependency ratio remains below 50.

Image source: Zhu Yong, Smart Elderly Care

According to data compiled in Zhu Yong's Smart Elderly Care, China's total dependency ratio fell rapidly from 1992 to 2010, then climbed just as quickly. It is projected to exceed 50 again by 2028. This means, by this definition, the demographic dividend window we once knew lasted only 37 years.

By 2030, the elderly dependency ratio is expected to surpass the child dependency ratio for the first time, and China will officially enter a social structure primarily focused on supporting the elderly.

Third, rural China is aging significantly faster than its cities.

According to projections from Zhu Yong's Smart Elderly Care, in the 2030s, when national population aging reaches its fastest pace, the gap between rural and urban aging will also peak, with a maximum difference of 12-13 percentage points.

Particularly noteworthy is China's increasingly severe problem of empty-nest elderly. Statistics show that in rural areas, over half of elderly people live apart from their children, surviving alone. According to The Aging Society Research Report (2019), the unmarried elderly population is projected to grow to 105 million by 2030. The Fourth National Sample Survey on the Living Conditions of China's Urban and Rural Elderly found that elderly people living alone or as empty-nests accounted for 13.3% of the elderly population, with the rural proportion significantly higher than urban.

This is the reality of aging in China that we must confront — the world's largest elderly population, one of the fastest aging speeds, and significant urban-rural disparities. These characteristics will make China the world's largest innovation laboratory for the silver economy.

/ 02 /

What Is the Silver Generation Really Like?

When we talk about the silver economy, we can't help but focus on the driving force behind it — the silver generation. What are the characteristics of this generation?

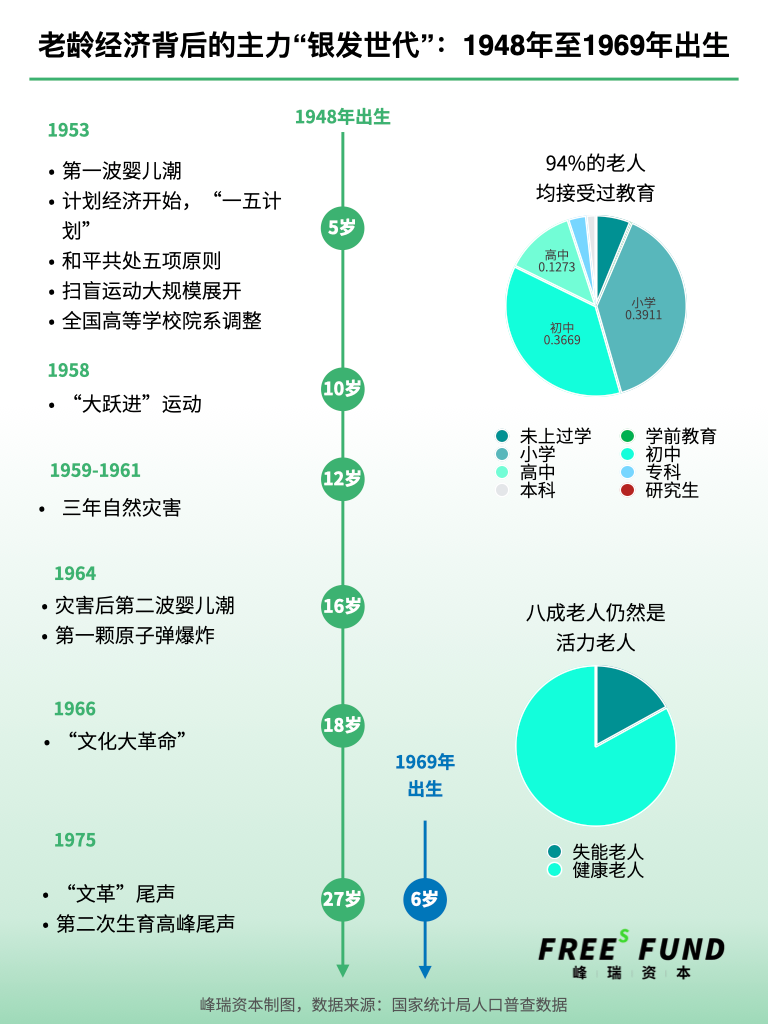

Generations are not simply classified by birth year. A generation is a sociological concept: a cohort that came of age during the same major social, technological, and cultural events, sharing collective memories, environments, and consumption values. Sociology widely holds that the social events and shocks experienced during one's adolescence profoundly shape their life trajectory. We attempt to map the characteristics of the silver generation through two dimensions: critical developmental milestones in the life cycle, and major social events.

Critical Milestones in the Life Cycle

Every life contains pivotal moments. According to cognitive psychology research, ages 5–6 mark when a child begins forming complete memories; 10 is when outlooks on life and career begin taking shape; 12 brings junior high school and the adolescent pursuit of independence and rebellion; around 16, high schoolers start exploring social and romantic relationships; 18 marks official adulthood. On the social events axis, we've selected landmark occurrences since the founding of the People's Republic for comparison.

Overlaying personal and national timelines reveals that China's current silver generation consists primarily of those born between 1948 and 1969. Born during the first and second baby booms, they experienced economic scarcity, the three years of natural disasters, and profound cultural upheaval.

Yet this generation also witnessed many of the PRC's proudest moments. They saw the successful implementation of the First Five-Year Plan, entered school to learn during the literacy campaign, watched the first atomic bomb detonate, and found themselves swept up in the narrative of a rising technological power. They observed the new China's diplomatic face taking shape under the Five Principles of Peaceful Coexistence. Though raised in material deprivation, they emerged as a generation remarkably resilient — and proud — in spirit.

Our definition of the silver generation — those born 1948 to 1969 — encompasses approximately 450 million births, per National Bureau of Statistics data. About 330 million survive today, representing 23.4% of the total population. They are aged 54 to 75, with the vast majority under 69; women slightly outnumber men.

Educationally, the literacy campaign's impact is visible: over 94% received basic education, and roughly 5% attained higher education. In terms of health, more than 80% remain relatively healthy without loss of daily functioning.

▍ Consumption Characteristics of the Silver Generation

The shared experiences of this generation have forged distinctive consumption patterns.

In consumption, the silver generation regards family as central to life's meaning, and they serve as primary decision-makers in household purchasing. The planned economy's lingering influence makes them favor value-oriented platforms like Pinduoduo and Taote. They also prefer centralized, visually intuitive livestream commerce, as well as social commerce backed by personal recommendations from acquaintances. In brand preference, their pride in national honor draws them toward domestic brands.

In health, they take personal responsibility for their own wellbeing. A generation accustomed to "cultural troupe" performances and public ceremonies channels youthful aspirations into full expression in later life, finding spiritual belonging in square dancing. Hence step-counting apps with strong social features like Tangdou and "Walking Master" have become favorites among elderly users.

In wealth management, navigating an extended old age and actively managing assets to cushion against economic cycles — thereby securing their later years — has become an urgent need. In recent years, financial education platforms targeting seniors have attracted substantial elderly user bases.

In spiritual life, seniors pursue rich and varied activities. User growth among the silver-haired demographic has surged across short video, music, travel, and more. Meanwhile, content creation tools that lower barriers to entry — CapCut, Meipian — have gained popularity with elderly users. In the silver influencer space, the first creator to surpass 30 million followers has already emerged.

More notably, the post-70s generation is gradually approaching retirement age. Raised during Reform and Opening Up, having experienced rapid economic and cultural growth, and influenced by the internet and younger generations in intergenerational exchange, this more open, inclusive, and trend-seeking cohort will become the fastest-growing segment of the aging economy over the next decade, injecting fresh vitality and new characteristics.

What Changes Will the Aging Economy Bring to Future Society?

Having discussed the silver generation at length, we want to examine an easily conflated concept: Is the aging economy simply the silver economy? When we focus on the aging economy, is it enough to merely layer elderly needs atop existing economic structures? The answer is clearly no.

The aging economy is not merely oriented toward older people. It will fundamentally reshape nearly every aspect of society, primarily through four dimensions: consumption structure, working lifespan, industrial transformation, and social operating models.

Entering an Elderly-Driven Long-Tail Market

Aging's impact on society will directly manifest in consumer demographics and structure.

According to 2022 statistics from Caibao Research Society, roughly 54,000 people in China celebrate their 60th birthday each day, compared to about 12,000 in the United States. Globally, this figure reaches 210,000 and is still rising rapidly.

Many of the new consumer brands that emerged around 2019 targeted primarily the 25-to-35 age bracket. Per the National Statistical Yearbook, this cohort numbered approximately 230 million in 2019 — roughly equivalent to the elderly population at that time. But in the five years since, this core demographic has declined, while the elderly population has grown rapidly.

Following current aging trends, consumer markets will eventually shift to an elderly-dominated structure. Many worry about insufficient elderly spending power, but elderly-driven markets will be long-tail markets. For instance, given current life expectancy trends, when a brand wins over a 50-year-old user, it may well secure 20 to 30 more years of loyalty. Thus, across extended user lifecycles, the total economic value seniors can generate is considerable.

Extended Working Lifespan

Aging will also lengthen working lifespans. As medical technology advances, the period of frailty shrinks as a proportion of total old age — meaning more "active elderly" will emerge, fundamentally affecting education and employment markets.

Consider Japan, already a deeply aged society. Today, Japanese 60-year-olds have an average remaining life expectancy exceeding 25 years — comparable to the time a master's graduate spends before entering the workforce. By 2050, this figure is projected to reach 30 years and continue growing. This lengthening old age will profoundly reshape employment and education markets; compared to ever-fewer young people, the elderly will remain active participants in future labor and education markets.

Since enacting the Act on Stabilization of Employment of Elderly Persons in 1986, Japan has revised it repeatedly to supplement social security in pension receipt, unemployment compensation, gradual retirement systems, and corporate subsidy mechanisms — greatly safeguarding elderly employment rights and boosting employment rates. In 2019, official data showed that among enterprises with 31 or more employees, 99.8% had implemented delayed retirement, continued employment, or age-limit abolition systems; 78.8% of elderly persons expressed work意愿 and ability to continue until 65.

Returning to China: current average life expectancy is 78.2 years, meaning a 60-year-old has over 18 years of remaining life expectancy on average. In the near future, we will witness the historic shift where old age exceeds employment preparation time.

At this year's Two Sessions, the government gave clear signals regarding delayed retirement policy: after careful study and thorough论证, it will be introduced steadily at an appropriate time. The latest institutional reform proposal also formally raised the issue of improving elderly affairs governance. The proposal emphasized implementing a national strategy for actively responding to population aging, relocating the National Working Commission on Aging to the Ministry of Civil Affairs to strengthen its comprehensive coordination, supervision, guidance, and organizational推进 of aging事业 development.

These measures are not unique to China. Globally, employment rates among those 65 and older already exceed 50% in Japan, South Korea, the United States, and Norway. In Norway, the figure surpasses 70% — meaning seven in ten elderly remain actively working.

Per the Kauffman Index of Entrepreneurship, in 2016, entrepreneurs aged 55–64 accounted for 24% of new entrepreneurs; by 2030, this is projected to reach 50%, making entrepreneurs over 55 the dominant group among new business founders. In other words, we will soon witness a social landscape where the elderly remain active in education, flexible employment, and even entrepreneurship.

From a longer life-cycle perspective, the traditional "social clock" will gradually lose its grip, allowing people to freely explore life's possibilities at ages previously unimaginable.

Industrial Restructuring

The aging economy will also reshape industrial structure. As more elderly remain in the workforce, technology- and experience-intensive industries will better leverage their strengths than labor-intensive ones, with technology playing an increasingly central role.

As the working-age population shrinks relative to total population, and elderly participation extends, the gaps in energy, education, and comprehensive capability between working-age and elderly populations will ultimately influence the direction of industrial transformation. Industries with outsized physical demands — labor-intensive sectors — will feel aging's impact most acutely. Primary and secondary industries will increasingly need to boost productivity through experiential wisdom and technological intelligence, while tertiary industries will see incremental demand for services catering to elderly needs.

Shifting Consumption Preferences

The aging economy will also transform our consumption outlook and money mindset.

Nobel laureate Franco Modigliani, from a life-cycle theory perspective, proposed a framework linking age to savings. Across the life cycle, consumption habits and monetary attitudes shift with age. The theory holds that during working years, people tend to save actively for retirement; in retirement, with reduced income, they draw down youthful savings, rarely or never adding new savings.

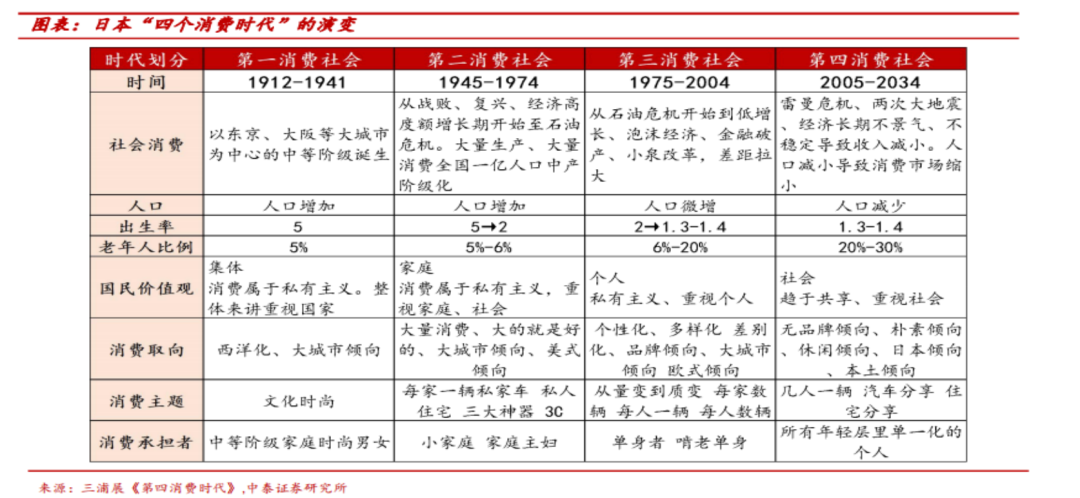

In consumption studies, a famous book titled The Fourth Consumer Society by Japanese author Miura Atsushi divides Japanese consumption history into four stages. The third stage emphasized individuality, differentiation, branding, and privatism; the fourth stage moves toward de-branding, comfort and simplicity, local cultural appreciation, and sharing.

Is this pattern of consumer evolution transferable? To even attempt an answer, we must first ask: what truly distinguishes each stage from the next?

The book divides the stages purely by time, which feels somewhat arbitrary. If we instead use social wealth indicators like per-capita GDP, we cannot adequately explain why similar phenomena failed to emerge in other developed countries such as the United States. We believe that the degree of societal aging — specifically, the proportion of the population aged 65 and above — serves as a more appropriate metric for distinguishing consumption stages. Measured by this standard, China today sits on average in the third consumer society and will continue evolving toward the fourth.

Of course, we must also account for national differences. Japan's current elderly are represented mainly by the "dankai sedai" (baby boomers) and "kanjō sedai" (emotionless generation), born during the postwar baby boom. They accumulated wealth during Japan's economic takeoff in their youth, but in middle age faced the bursting of the economic bubble and the decline of student activism; in old age, they confront challenges to their pensions and health insurance.

Beyond the Silver Generation mentioned earlier, China's post-70s cohort will gradually reach retirement age. Unlike Japan's current elderly, this generation grew up during a relatively open and prosperous era, possesses higher average education levels, has accumulated substantial material wealth, and was deeply shaped by the internet. These factors will make China's future aging economy structurally different from Japan's.

Product Innovation Cases in the Aging Economy

Based on market demand arising from the aging economy, we have mapped out the following categories, encompassing spiritual needs, health needs, livability needs, and service needs — each containing significant entrepreneurial opportunities.

- Spiritual needs: educational and training programs for seniors, travel and leisure, content products, and more.

- Health needs: beyond serious medical care, we can look to more diverse health therapies and derivative products, such as medical foods, functional footwear and apparel, and wearable devices. We must also pay attention to the increasingly severe mental health challenges facing the elderly.

- Livability needs: a range of opportunities arising from seniors' needs for safety and convenience in aging-in-place, including smart home products, home health monitoring devices, and mobility assistance equipment.

- Service needs: home care and nursing, financial advisory services, senior shopping centers, and more.

From these four categories, we have selected several cases to explore noteworthy innovations in the global aging economy.

Spiritual Needs: More Human-Centered, Exclusive Content Services

Rendever is a company primarily providing VR hardware and age-appropriate content for the elderly. It helps alleviate cognitive decline and prevent Alzheimer's by allowing seniors to immersively revisit places holding special memories. Currently, most AR and VR startups target young people, but as Rendever demonstrates, applying these technologies to the elderly reveals vast market potential.

Another company worth noting is Artifact, whose main product is audio-format family biographies. It combines freelancers with intelligent automated tools to interview family members, then produces roughly 20-minute professional audio pieces from the material, creating an editable, shareable family history page where users can upload family photos.

Since launching in 2020, Artifact has gained over 10,000 paying users in Spanish- and French-speaking countries. Similar market opportunities exist in China — platforms like Meipian or CapCut use professional tools and services to lower the barrier to content creation. Seniors can use these tools to satisfy social needs and reduce loneliness.

Health Needs: Human-Centered Models and Product Innovation

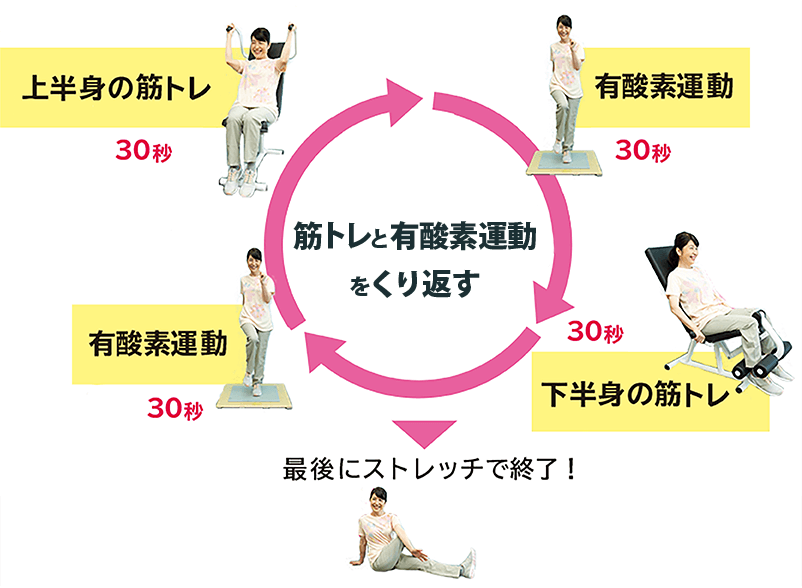

First, let us introduce Curves, a typical example of human-centered innovation arising from elderly health needs. Curves was the world's first gym chain designed around female users and remains one of the largest fitness franchise brands globally. In Japan, Curves serves over 950,000 middle-aged and elderly users across nearly 2,000 locations. In 2018, the Japanese franchisee acquired its American parent company — how did it achieve such success?

The core lies in Curves Japan's sharp focus on middle-aged and elderly women, with extensive product and service upgrades tailored to this demographic: all staff are female; plate-loaded training equipment unfriendly to older women was replaced with specially designed hydraulic machines; a 30-minute circuit workout was developed specifically for this group. A crucial model innovation: no mirrors in any location, eliminating any "gaze" that might trigger anxiety about body shape or age.

An elderly person working with powered assistive clothing. Image source: Innophys

Another company achieving product innovation, also from Japan, is Innophys, which offers a wearable "air muscle suit." Unlike motor-driven exoskeletons, Innophys's product requires no external power — it uses compressed air as its power source. The "air muscle suit" helps seniors continue working in sorting, care services, and agriculture.

The product retails for around RMB 7,000, with rental prices of roughly RMB 400 per month. Because it aligns with Japan's policies promoting elderly re-employment, purchasers or renters receive subsidies covering about 50% of the cost. The affordable pricing combined with lightweight, simple wearability has enabled the product to accumulate over 10,000 continuous paying users in Japan.

Compared to China's current elderly rehabilitation market, where exoskeleton products mainly focus on simulating and optimizing human skeletal joints — making them relatively complex and heavy — there is a gap for Innophys-style products emphasizing lightness, flexibility, wearability, and lower barriers to use for seniors. With delayed retirement and policies encouraging elderly employment forthcoming, flexible exoskeletons like Innophys's point toward another possible market direction.

Livability Needs: Smart Technology Enabling Aging-in-Place Upgrades

When considering livability or aging-in-place needs, people may first think of AI-related smart assistive or monitoring devices. In fact, smart upgrades can permeate every aspect of home-based elderly care.

For example, Panasonic launched a smart soft-food rice cooker precisely targeting elderly people with chewing and swallowing difficulties, helping them easily and conveniently eat appropriate soft-textured food. Currently priced above RMB 2,000, users are still willing to pay to address seniors' swallowing challenges.

Another American company, MedMinder, primarily provides smart pillbox services, offering not only medication monitoring but also entertainment interaction, health alerts, and other integrated functions.

Its most distinctive innovation lies in capturing the characteristic separation of medicine and pharmacy in the United States, integrating at the foundational level with pharmacy delivery services. Through the MedMinder app, pharmacists at smart pharmacy terminals can access elderly patients' prescriptions and track their medication adherence. Based on patients' medication cycles, they automatically ship new replaceable medication trays to seniors on a regular schedule.

To date, MedMinder has secured numerous B2B clients and raised over $80 million in funding. According to data from MedVille Medical Center in the US, MedMinder's intelligent approach has improved elderly medication adherence (the degree to which patients follow their prescribed treatment regimens) from 40% to over 90%. Using intelligent means to enhance aging-in-place livability and humanize home-based elderly care, such innovation opportunities will have even greater potential in the Chinese market.

Service Needs: Sticky, Warm Services

When it comes to services, we must mention Aeon Kasai G.G Mall in Japan. Called "a miracle among shopping centers," this single location generates over $80 million in annual revenue, serving more than 1.1 million middle-aged and elderly customers per year. Seniors spend an average of three hours in the mall — how does it achieve this?

The secret lies in its service philosophy: everything starts from the elderly population. This principle permeates every aspect of the shopping center. To accommodate seniors' early-rising schedules, the mall opens at 7 a.m. The 1.8-meter-wide walkways throughout the mall are designed to facilitate walking exercises for elderly visitors.

The mall also houses a series of service centers for seniors, including rehabilitation centers, exercise centers, and financial planning outlets. In the retail area, easy-to-eat foods suitable for the elderly are clearly labeled and arranged by softness level, helping seniors quickly identify products appropriate for them.

Another company innovating in elderly-oriented services is Sagewell, an American firm providing exclusive financial advisory services for seniors. Through fixed monthly membership fees, it offers comprehensive post-retirement financial solutions, including tax optimization consulting, healthcare service consulting, and pension consulting, helping seniors avoid financial fraud.

Whether Aeon Kasai G.G Mall or Sagewell, both place the elderly at their core, continuously providing sticky, warm services — and winning the market as a result.

China-Japan Comparison: What Stage Is China's Aging Economy In, and What Unique New Opportunities Exist?

After examining global aging economy innovations, we return finally to China: what stage is China's aging economy currently in, and what new opportunities does it present? To answer this, we studied the history of Japan's aging economy and found it can be divided into three stages:

- Stage One (1980–2000): The Rise of Institutions

In just two decades, growing elderly care demand in Japan drove the rise of nursing institutions. Chain nursing homes emerged in large numbers, and industry concentration continuously increased. Ultimately, three giant nursing home groups appeared, led by Nichii Gakkan. Nichii Gakkan's 1999 IPO became the landmark event of this stage.

- Stage Two (2001–2010): The Rise of Consumer Spending

During this decade, the market saw a surge of consumer brands targeting seniors — clothing, cosmetics, food, and more. The elderly consumer market matured rapidly.

- Stage Three (2010–present): Zero-Sum Competition

The consumer market grew increasingly segmented, channels matured, and channel brands began to emerge. The Kasai G.G Mall mentioned earlier exemplifies this trend.

Where does China stand today?

Comparing China's elderly population share with Japan's three stages, we found that during Stage One's institutional rise, the 65+ population ranged from 10% to 18%. In Stage Two, the figure was 18% to 24%, and in Stage Three, 24% to 30%.

According to National Bureau of Statistics data, in 2021, China's population aged 65 and above exceeded 200 million, accounting for 14.2% of the total population. This means China has only just entered the first stage of the aging economy — the phase of rising demand and institutional growth. We've already seen parallel trends: in 2019, the government liberalized the market access negative list and removed approval requirements for elder care institutions. That same year, over 60 listed companies entered the elder care institution and wellness real estate sectors.

When will China enter Stage Two, the phase of consumer market growth?

Based on China's current aging trajectory, we will likely enter the explosive growth phase for elderly consumer markets around 2025–2030. Referencing Japan's experience, we may witness the birth and IPO of numerous consumer goods companies targeting seniors.

FreeS Fund's portfolio company Methuselah exemplifies this opportunity. Positioned in the aging economy, Methuselah is a leading medical nutrition brand addressing the chronic disease prevention and nutritional management needs of health-conscious populations, particularly the elderly. The company has developed a comprehensive medical nutrition product line spanning foods for special medical purposes, low-GI products, and energy-controlled weight management, entering over 500 tertiary hospitals and serving more than 10 million patients.

Currently, we can identify several trends in the aging economy through early-stage investment activity:

First, significantly increased funding scale.

In 2022, both in terms of funding rounds and amounts, early-stage investment in China's aging economy saw substantial year-over-year growth. Meanwhile, capital attention to the senior-focused track notably increased.

Image source: AgeClub

Second, rehabilitation assistive devices, elder care services, and chronic disease management have become hotspots.

Following the 2019 liberalization of elder care institution approvals, the 2021 pilot expansion of long-term care insurance (a system arrangement focused on providing care protection and economic compensation when insured individuals lose daily living capacity, grow old and fall ill, or pass away), and the 2022 introduction of private pension plans, new opportunities have emerged in chronic disease management, rehabilitation assistive devices, and elder care services — becoming current investment hotspots in the aging economy.

Third, chronic disease investment concentrates on brain science-related conditions.

Within chronic disease management, investment concentrates on brain science diseases, with particular attention to neurodegenerative conditions such as Alzheimer's and Parkinson's. Beyond demand drivers and policy tailwinds, the active investment in brain science diseases is inseparable from breakthrough research by domestic scholars in neurodegenerative conditions.

Fourth, overseas aging economy investment is more diversified, with clear digitalization trends in home-based care.

Foreign investment in the aging economy covers more diverse sectors, with elder-focused food, financial management, and senior fitness all flourishing. Among these, the hotspot is digital transformation of home-based care. The core reason is that European and American countries encountered the problems of caregiver shortages and high costs earlier than China, driving them to use various digital approaches to improve the allocation efficiency of care resources.

Summary

Finally, let's summarize the new opportunities we're observing in China's aging economy:

First, mine consumer product opportunities for elderly users.

Based on mature market experience, food, footwear and apparel, and personal care products remain the categories most frequently purchased and most heavily consumed by seniors in deeply aged societies. A familiar saying from the new consumer sector may still apply in the aging economy — for elderly users, every traditional consumer product deserves to be rebuilt from scratch.

Second, pay attention to urban-rural differences in aging.

We must still attend to China's urban-rural aging disparities, particularly the possibility that both high-tier cities and lower-tier rural areas may simultaneously enter deep aging. Differences in asset levels, education, and digital adoption may create entirely different opportunities and unexpected synergies between urban and rural areas at comparable aging levels. For example, online channels may offer greater scale effects, while offline channels may present more differentiated competitive landscapes.

Third, use technological innovation to comfort empty-nest elderly.

We must also address the increasingly severe empty-nest elderly phenomenon. The home-based elder care needs of empty-nest seniors will give rise to unique innovation opportunities that will disrupt traditional industries. For instance, today's pet market, dominated by young people, may in the future count empty-nest elderly — who similarly need emotional companionship — as a core demographic, potentially transforming the underlying logic of pet products.

Fourth, long-term capital management industries such as private equity face new opportunities.

The aging economy will also bring changes to the investment industry itself. In mature markets like the US, government-led pension funds represent one of the primary forces behind private equity funds. As consumer capacity rises and industrial upgrading releases new investment opportunities, long-term capital management industries including private equity and trusts will welcome new development.

In his endorsement for Being Mortal, Oliver Sacks wrote: "We have medicalized aging, frailty, and death, treating them as if they were no more than clinical problems. Yet what people want in their final stage is not merely to be kept alive, but to live — a life with meaning, as rich and full as possible under the circumstances."

We hope to witness more combinations of technology and humanity, working alongside entrepreneurs who care about social value, to help more elderly people live lives as rich and dignified as possible.

Engagement

What kind of retirement life do you hope for? What product innovations in the aging economy have you noticed? Share with us in the comments. The 5 most thoughtful commenters will each receive a copy of Being Mortal: Medicine and What Matters in the End.

▲ After ChatGPT's Explosion, Where Does AIGC Go? | FreeS Report 28

▲ Trends 2023 | FreeS China-US Venture Capital Summit Open for Registration

▲ Join FreeS to Discover New Changes and Opportunities

▲ What Will Humans Eat in the Future | FreeS Report 27

▲ China's Dietary Structure and Food Investment | FreeS Report 25

▲ How Will Humans Work in the Future? | FreeS Report 26

▲ FreeS Report 24 | Embracing the "Smartest" Opportunity: Investing Boldly in Brain and Neuroscience