Where Is the Future of Livestream E-Commerce? Lessons from TV Shopping History for New Brand Opportunities | FreeS Research

What traits make a brand well-suited for livestream e-commerce?

2020 was the year livestream e-commerce exploded: Austin Li, Viya, and other hosts entered the mainstream, and Yonghao Luo's entry made it even hotter. Livestream selling had become an essential new channel for e-commerce.

FreeS Fund has long paid attention to new traffic and new media changes in the consumer/TMT space. In the first half of 2020, we used two articles to explore the two main forms of livestream e-commerce in China at the time — a colorful Juhuasuan, a colorful Smzdm. In today's piece, we look overseas to study the history of teleshopping — the predecessor of livestream e-commerce — in the US, and combine it with the new characteristics of livestream e-commerce to discuss future trends and entrepreneurial opportunities.

Why is teleshopping the predecessor of livestream e-commerce?

Traditional teleshopping and the now-rising livestream selling share many similarities: real-time video as the medium, user demand for immersive content and low prices, and relationships with back-end supply chains. The "only 998" teleshopping model from over a decade ago and Austin Li's "buy it" aren't fundamentally all that different.

Teleshopping in developed countries like the US has already gone through a relatively complete marketization process. Learning from history, we can see the future direction of livestream e-commerce from teleshopping's 40-plus-year history.

This article will explore:

- What is the potential of livestream e-commerce? Is this a real trend that will exist long-term? How large is the market?

- Over 40 years of American teleshopping, what did the successful companies do right? What lessons does this hold for China's livestream e-commerce?

- Under entirely new media forms and traffic environments, what kinds of companies and brands can stand out in China's livestream e-commerce landscape?

Before diving in, three preliminary conclusions:

- Livestream e-commerce is a multi-trillion-RMB market and represents a real, long-term demand.

- From 40 years of American teleshopping history: the traffic advantages brought by scale, and the product selection and supply chain control achieved through vertical integration, were key success factors for teleshopping companies — and likely represent trends in livestream e-commerce's development.

- During this period when livestream e-commerce is emerging as a new medium, brands with storytelling, demonstrability, and novelty that can combine with livestream e-commerce's new characteristics will enter a golden period of growth.

FreeS Fund continues to pay attention to investment opportunities in the consumer sector. Business plans are welcome at bp@freesvc.com, and you can also contact Feng Xiaorui (WeChat ID: freesfund).

The Future of Livestream E-Commerce Through the Lens of Teleshopping History

By Shili Shao

01 Behind the Hype, What's the Real Market Potential of Livestream E-Commerce?

Livestream e-commerce could account for 2 trillion RMB in GMV annually

What is the real market potential of livestream e-commerce?

The current livestream e-commerce market is flooded with news of fake orders and counterfeit goods. We assess the market space by studying the penetration rates of teleshopping, which shares similar characteristics with livestream e-commerce.

First, the conclusion: in the long term, livestream e-commerce will reach a market scale of several trillion RMB, with trillion-level room for growth.

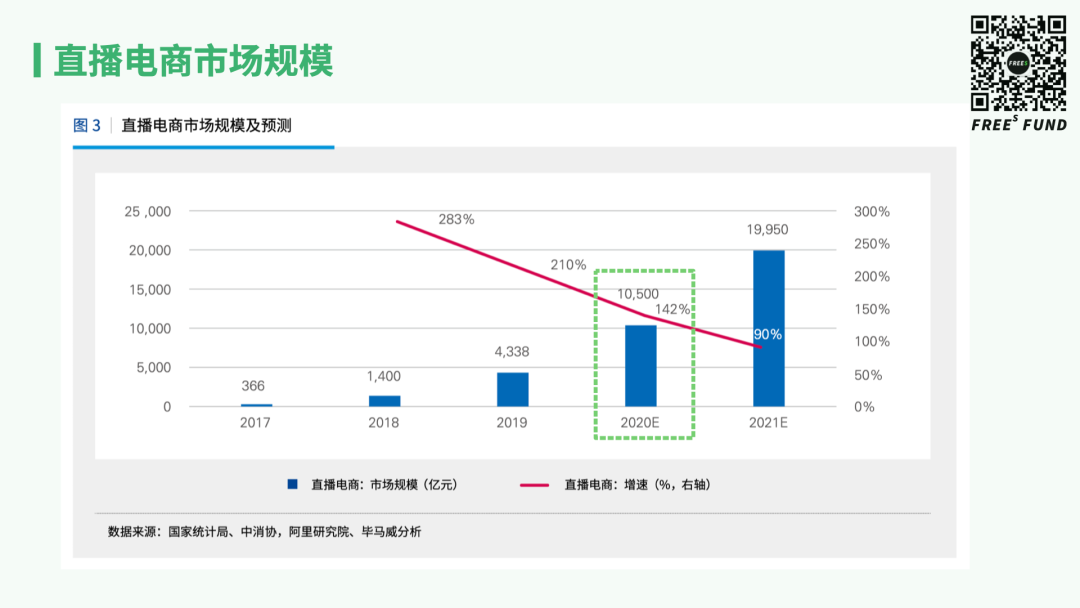

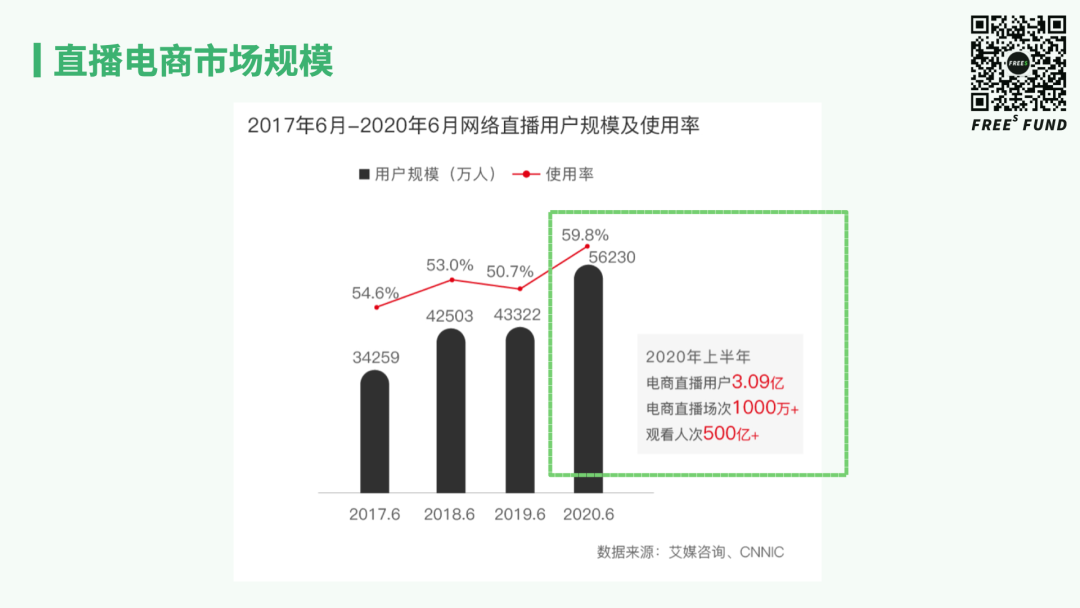

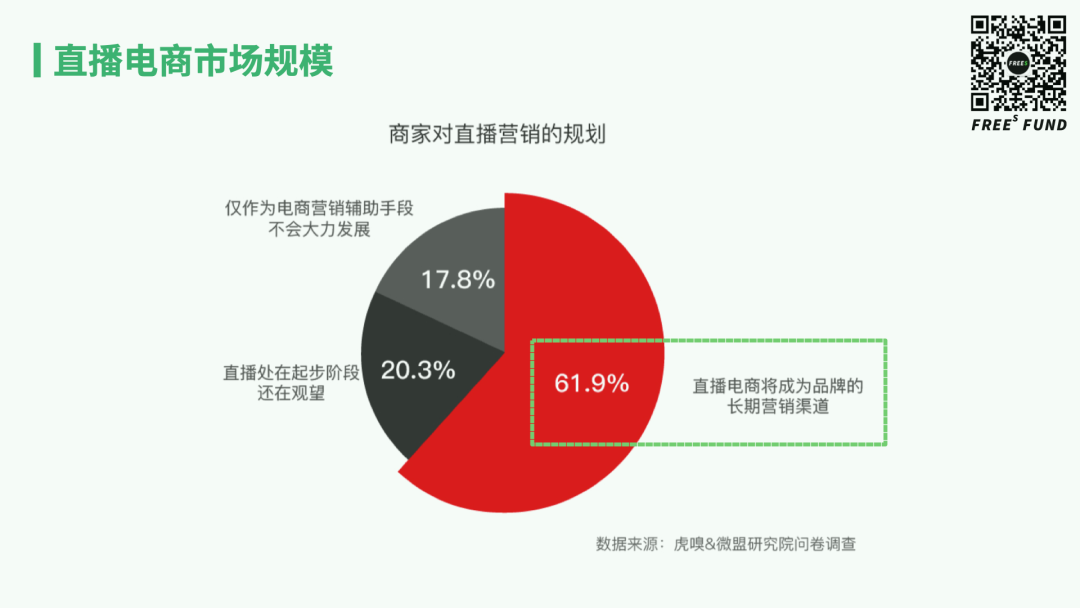

Some public data mentions that the livestream e-commerce market was around 400 billion RMB in 2019, and expected to reach 1 trillion in 2020. Livestream e-commerce also has substantial user numbers — by the first half of 2020, viewing users had reached 300 million. Surveys by Huxiu and Weimob Research Institute targeting merchants also showed that over 60% of merchants believe livestream e-commerce could become a long-term trend.

Behind these impressive numbers, is there false prosperity?

Many recent reports have mentioned fake ordering and high return rates in livestream e-commerce. Jiemian News wrote that return rates often exceed 30%, with women's clothing categories even reaching 50-60% — including top Kuaishou host Simba, who couldn't avoid return rates exceeding 30%, approaching 40%. According to public reports, specialized services for fake orders and fake followers even exist, with systematic pricing ranges covering the entire industry chain.

To reduce interference from this "false prosperity," we estimate livestream e-commerce's development potential by studying relevant indicators from the teleshopping market.

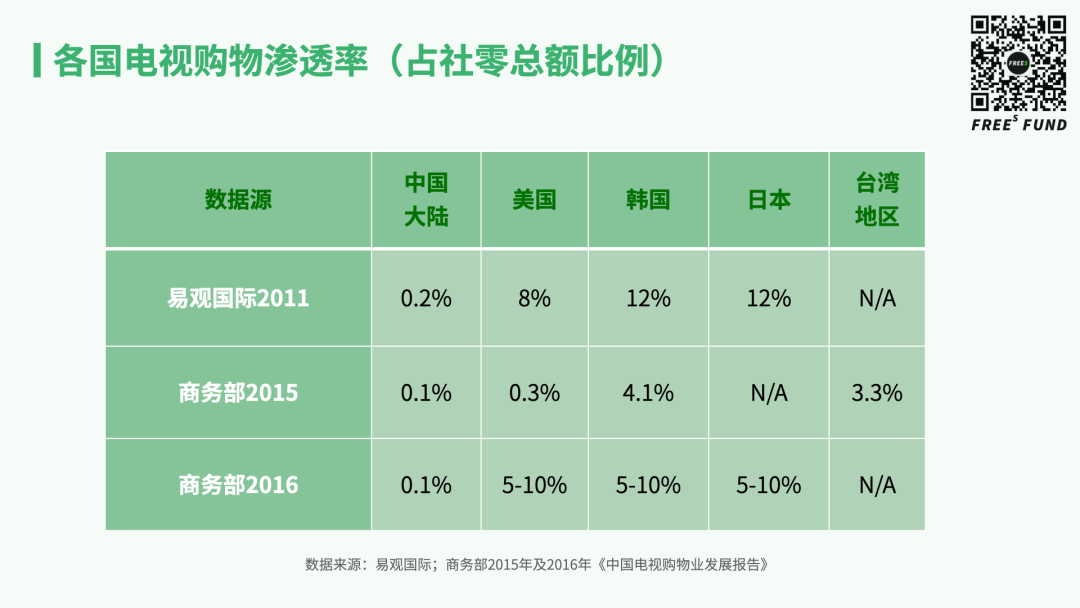

A relatively important indicator is the penetration rate of teleshopping markets in various countries — that is, the proportion of total retail sales accounted for by teleshopping. The penetration rates of teleshopping in developed countries where the industry is fully developed could theoretically represent the development space for similar livestream e-commerce demand. This indicator has different statistical口径:

- An Analysys International 2011 report showed developed countries' teleshopping penetration at around 10%, while China was only 0.2%;

- The Ministry of Commerce's 2015 "China Teleshopping Industry Development Report" was much more conservative, stating the US at 0.3%, South Korea at 4%, and Taiwan at 3% — mainland China still had a large gap compared to these regions, with the US 2.3 times higher than mainland China, and mainland China having 20-30 times gaps with some other regions;

- But the Ministry of Commerce's 2016 report showed different numbers, with European and American live TV shopping penetration at 5-10%, while China's was 0.1%.

So which of these differently-calculated numbers more accurately represents livestream e-commerce's potential penetration in China?

China's total retail sales in 2019 were 41 trillion RMB. Achieving 10% penetration would mean a market size of 4.1 trillion; 4% would be 1.6 trillion. At 0.3%, it would only be a bit over 100 billion.

According to data from the National Bureau of Statistics, China Consumers Association, and other institutions, China's livestream e-commerce market was already over 400 billion in 2019 — even with water content, halving it gives over 200 billion.

So for livestream e-commerce, 0.3% retail penetration should be on the low end; 4-10% retail penetration is probably closer to its true potential. Livestream e-commerce, replacing teleshopping, is likely a small multi-trillion-RMB market.

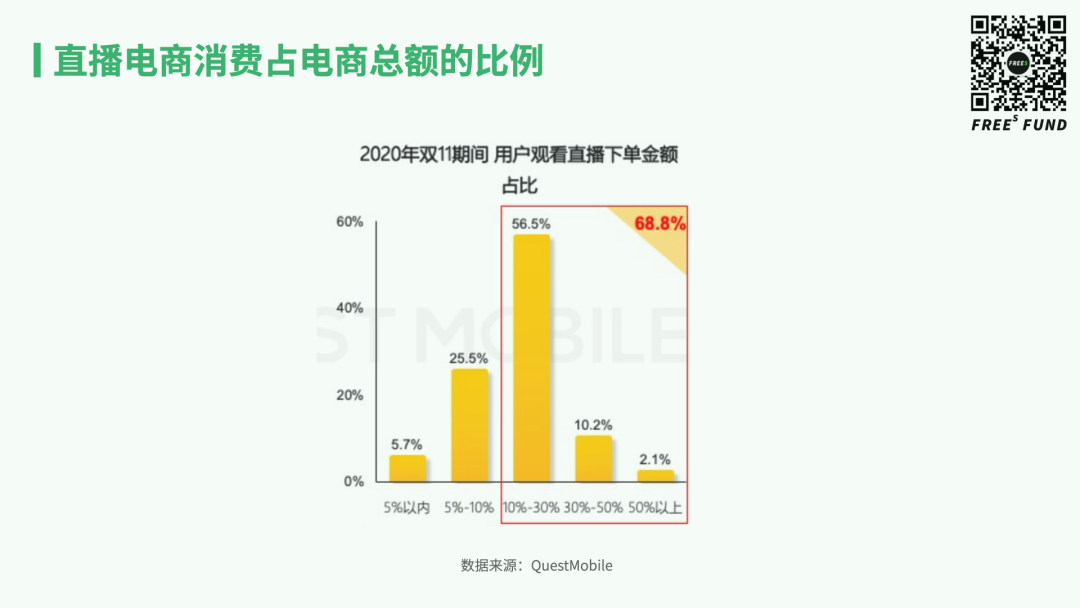

Another indicator can also support livestream e-commerce's potential: during Double Eleven, the proportion of users' livestream-driven purchases relative to total e-commerce spending. According to Questmobile statistics, most people fall in the 10-30% range, with nearly 70% of users above 10%.

China's total e-commerce GMV is now roughly 10 trillion annually. Calculating at the midpoint of 10-30%, or 20%, livestream e-commerce could account for about 2 trillion in GMV each year. Double Eleven has its special characteristics as a shopping festival, but considering livestream e-commerce's future growth potential, this 2 trillion figure may not be far off.

The main differences between Chinese and American teleshopping markets lie in category composition and repurchase rates

Why is there such a large gap between China and developed countries' teleshopping markets, and can this gap be closed in the livestream e-commerce era?

From a population penetration perspective, Ministry of Commerce 2015 data shows that one-third of households in the US and South Korea are teleshopping members, while Chinese teleshopping members account for only 5% of the population. In average order value, China and the US differ by roughly 10 times: Chinese teleshopping users spent an average of 758 RMB per person (Ministry of Commerce 2017 data), while in the US it was 8,967 RMB per person converted (QVC 2019 financial report).

By analyzing category composition and repurchase rates, we can infer what's driving the gaps in average order value and penetration.

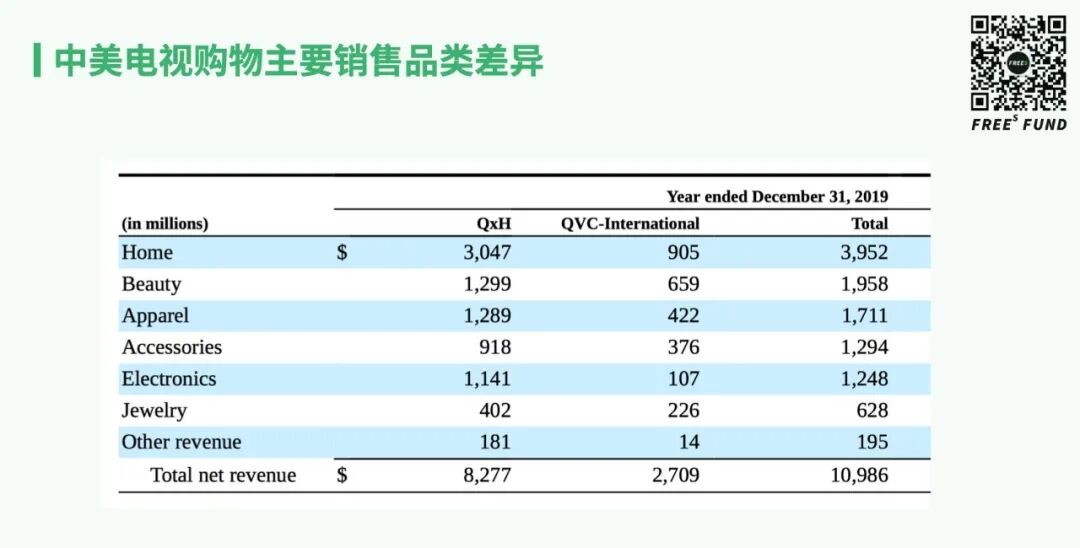

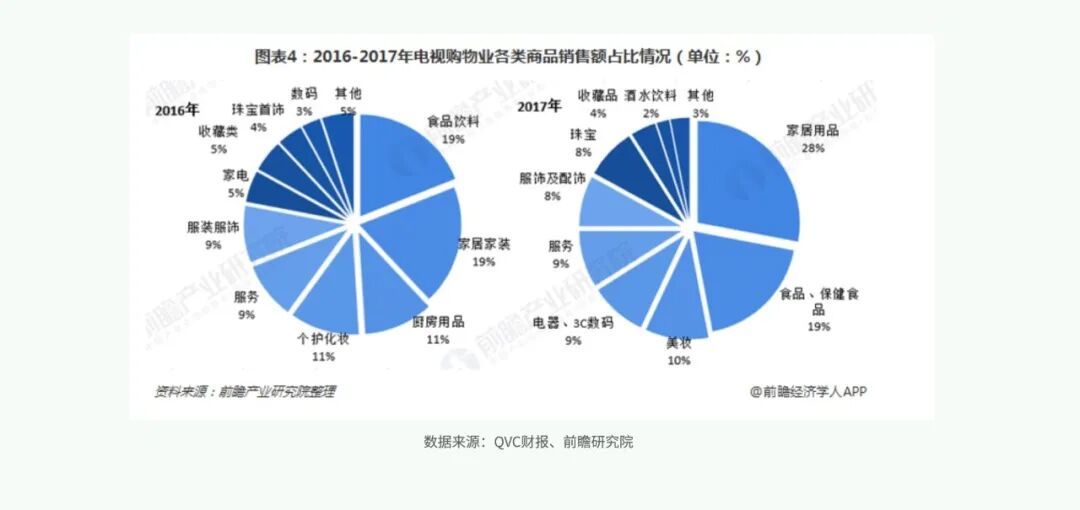

On categories, the US teleshopping market skews toward higher-ticket items. At QVC, America's leading teleshopping giant, mid-to-high-AVV home goods account for roughly 40% of total sales, while relatively premium 3C products make up about 14%. In China's teleshopping industry, home goods overall represent only 20-30% of sales; the dominant categories are lower-AVV items like food and beverages, and beauty products.

Repurchase rates also favor the US by a wide margin. QVC derives 86% of its revenue from existing customers — a staggering figure. By contrast, an AgeClub survey found that among elderly consumers in China's first-tier cities who had tried teleshopping, 77% would not buy again. Their repurchase rate likely sits at just 20-30%, with substantial membership churn.

Later sections will detail how US teleshopping companies achieved high repurchase rates and covered premium categories — through scale to gain traffic advantages, and improved selection and supply chain efficiency to ensure product quality — approaches that China, to some extent, can replicate in the live commerce era.

Live commerce has far greater upside than teleshopping

Whether viewed from demand, supply chain, or transaction efficiency, live commerce's inherent characteristics give it a theoretical ceiling well above teleshopping's.

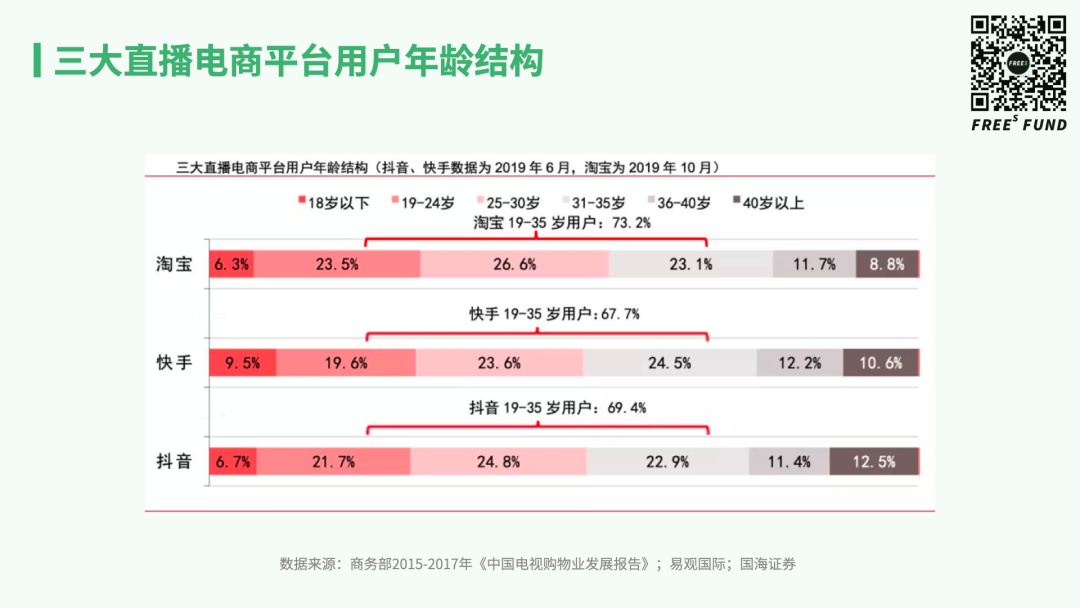

On the demand side, live commerce reaches a far broader population. Teleshopping airs during daytime hours when young people are unavailable; its core audience skews elderly and homebound — 63% of Chinese teleshopping members are over 46. Live commerce, meanwhile, draws 70% of its users from the 19-35 age bracket, capturing younger consumers in their prime earning years.

Nearly everyone now carries a smartphone and uses it constantly, but not everyone watches TV for extended periods daily. In 2020, 300 million people already watched live shopping streams, compared to teleshopping's peak of just 80 million members in China in 2017.

On supply chain and overall transaction efficiency, live commerce's infrastructure — payments, logistics, and e-commerce platforms — is more developed. Real-time interaction, big data-driven precision targeting, and private traffic operations all make the supply side more efficient, raising live commerce's theoretical ceiling further.

From the perspective of teleshopping's penetration of total retail sales, live streaming's share of e-commerce consumption, and efficiency comparisons between live commerce and teleshopping, live commerce appears to be a multi-trillion-RMB market. If live commerce reached the projected trillion-RMB scale in 2020, trillion-level growth space still lies ahead. The long-term trajectories of teleshopping in developed countries and China suggest that live commerce, as teleshopping's successor, will likely persist as a market over the long term, even if it experiences some fluctuations along the way.

The Rise of American Teleshopping Giants

Taking the US as our example, let's examine how teleshopping developed in a mature market.

America is teleshopping's birthplace. As a whole, US teleshopping ranks behind only Amazon and Walmart in scale, even surpassing eBay — effectively the country's "third-largest e-commerce" player. What did American teleshopping companies get right, and what lessons does this hold for China's live commerce?

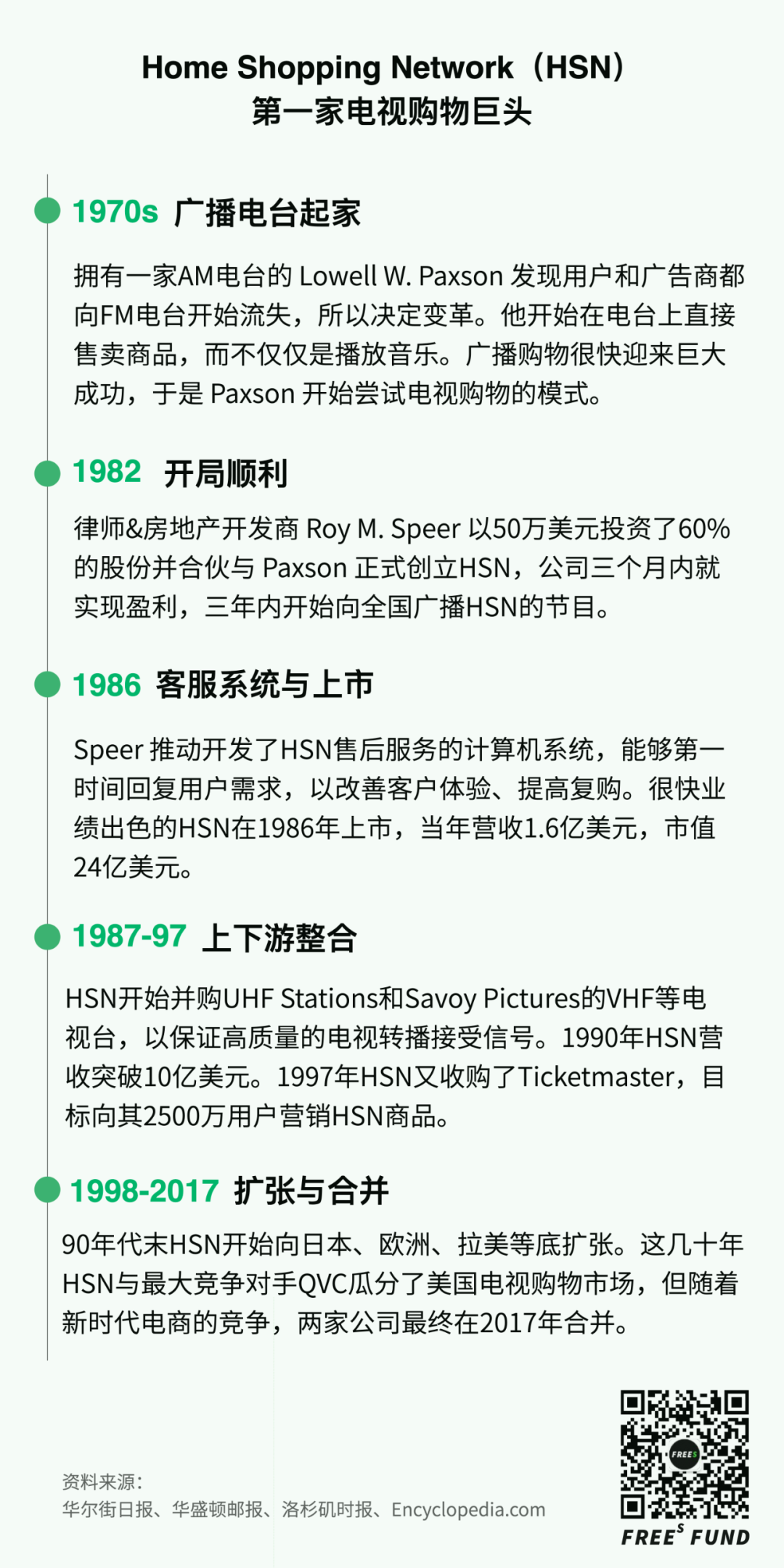

HSN: America's First Teleshopping Giant

Any discussion of American teleshopping must begin with Home Shopping Network (HSN). It seized the opportunity of shifting media formats, established first-mover advantage, and became the first teleshopping giant to rise in America.

Before founding HSN, Lowell W. Paxson ran an AM radio station.

In the 1970s, competition from emerging FM stations threatened Paxson's company with listener and advertiser attrition, prompting him to innovate. He began selling products directly on air — a pure-audio shopping model that attracted substantial audiences.

Television as a new medium was then gaining traction in America, and Paxson decided to bring his approach to TV.

HSN officially launched in 1982, turning profitable within its first three months — an auspicious beginning. Within three years, the company began broadcasting teleshopping programming nationwide. In its fourth year (1986), HSN went public. In its first year as a listed company, HSN posted revenue of $160 million and achieved a market capitalization exceeding $2.4 billion.

Before its IPO, HSN made one critical move: developing what was then a relatively advanced computerized automated customer service system, enabling rapid response to customer needs, improved user experience, and consequently higher repurchase rates.

Over the decade following its listing, HSN pursued vertical integration on a massive scale. It acquired multiple television stations to ensure high-quality broadcast signals, and purchased Ticketmaster — then a phone-based, now internet-based movie ticket seller — to capture traffic entry points and acquire users. By 1990, HSN's revenue surpassed $1 billion.

▲ HSN leveraged first-mover advantage to secure prime TV real estate.

The subsequent two decades marked HSN's international expansion phase. In recent years, however, the rise of new competitors like Amazon has posed significant challenges to the teleshopping industry. In 2017, HSN merged with QVC, the other teleshopping giant.

Across HSN's history, its emergence as a dominant force in early American teleshopping rested on three pillars:

- HSN was the first company to seriously pursue the teleshopping opportunity, possessing first-mover advantage and securing favorable time slots and positions across television channels early on. The founder's radio background also provided HSN with an initial user base and traffic advantage.

- HSN's prices were low. Similar to live commerce in China today, it attracted customers through pricing. For example, in 1987, 60% of HSN's merchandise came through manufacturer exclusives rather than other purchasing channels, bypassing numerous supply chain intermediaries, avoiding additional costs, and improving efficiency.

- HSN prioritized service. As early as 1986, it developed computerized automated customer service. Later, it acquired television stations to guarantee broadcast quality for its shopping programs. HSN was also among the earlier teleshopping companies to implement no-questions-asked return policies, cultivating user trust.

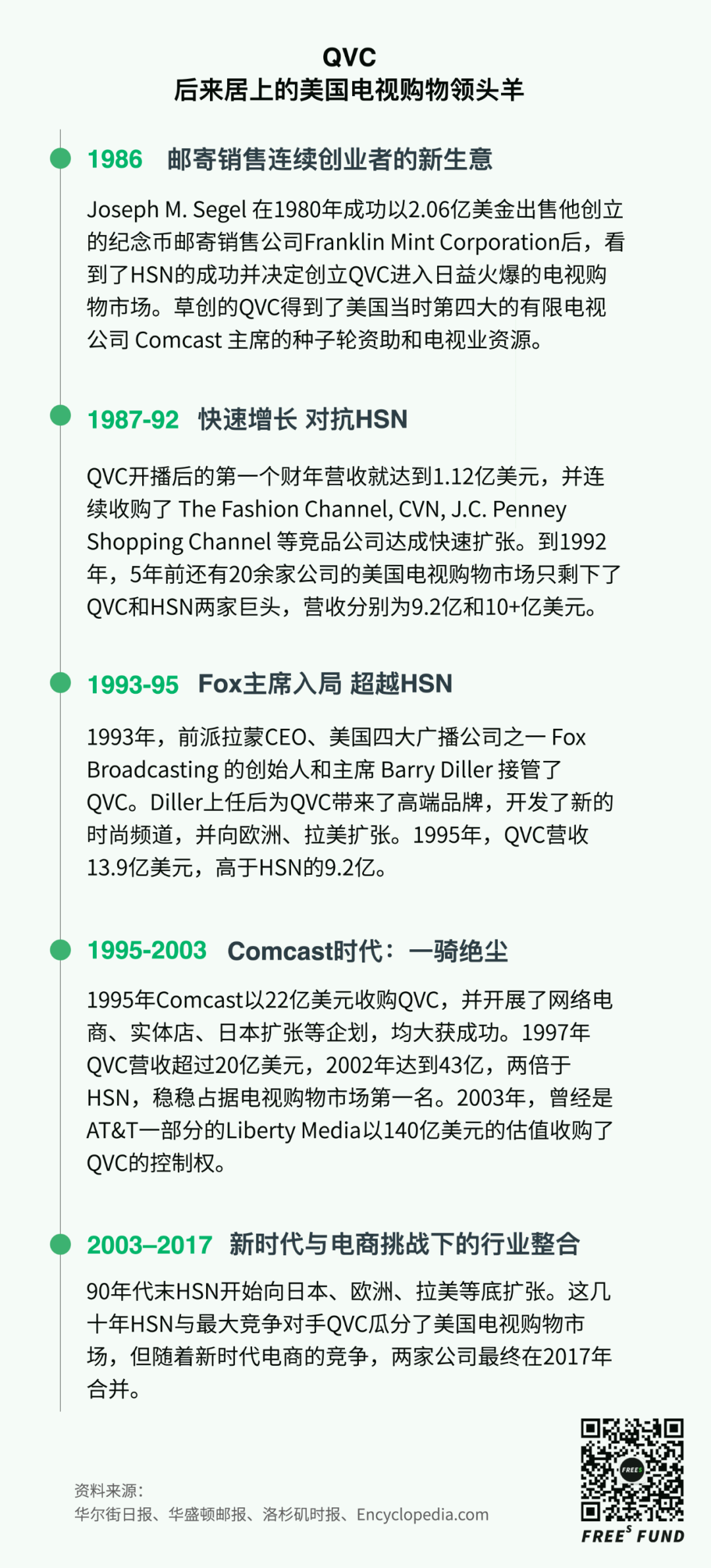

How QVC Came from Behind to Take the Lead

The second representative American teleshopping company is QVC. Founded in the same year HSN went public — 1986 — QVC gained support from TV industry traffic sources, offered differentiated products and services to users, and pursued aggressive M&A and expansion to achieve scale effects on both traffic and supply chain. Thus it came from behind to not only become America's current teleshopping leader, but to ultimately acquire HSN.

QVC stands for "Quality, Value, Convenience" — the name itself signaling how heavily the company weights product quality, with Quality as its first namesake.

▲ QVC's style resembles casual conversation among friends, with homey settings.

Founder Joseph M. Segel was already a successful serial entrepreneur before QVC, skilled in marketing. He had previously founded a commemorative coin company that sold through mail order, which he sold for $200 million. Seeing the opportunity that HSN represented in teleshopping, he entered the industry.

Segel possessed exceptional network resources. The chairman of Comcast — then America's fourth-largest cable company, now the industry leader — was a seed-round investor in QVC and helped connect the company with extensive television industry resources.

With backing and endorsement from industry heavyweights, QVC grew rapidly, exceeding $200 million in revenue in its first fiscal year. Through successive acquisitions of competitors including The Fashion Channel, CVN, and J.C. Penney Shopping Channel, it achieved rapid expansion.

By 1992, QVC's fifth year, the teleshopping industry — which had previously comprised over 20 companies — had essentially consolidated down to two giants: QVC and HSN, with revenues of roughly $900 million and $1 billion respectively.

Beginning in 1993, QVC came under the leadership of Barry Diller, former founder and chairman of Fox Broadcasting. Diller had previously served as CEO of Paramount, the American film production and distribution company, and Fox Broadcasting — where he had worked — ranked among America's four major broadcast networks. Leadership by a figure of Diller's stature substantially elevated QVC's brand recognition.

After taking the helm, Diller pursued a new expansion strategy that included developing premium brands, launching new fashion channels, and expanding internationally. Under the guidance of this seasoned media veteran, QVC continued to grow, reaching $1.4 billion in revenue by 1995 — substantially outpacing HSN's $900 million.

In 1995, Comcast acquired QVC for $2.2 billion. As mentioned earlier, Comcast's chairman had provided seed funding and resources from QVC's founding. Later, seeing the company's strong performance, Comcast simply bought it outright. This acquisition stands as a classic case of a TV channel — the upstream traffic source — integrating downstream into the teleshopping business.

Between 1995 and 2003, QVC expanded into e-commerce, physical retail, and Japan. The results were positive across the board. By 1997, QVC's revenue hit $2 billion. In 2002, it reached $4.3 billion — double HSN's revenue — firmly establishing QVC as the teleshopping industry's leader.

In 2003, QVC was acquired by Liberty Media, then a subsidiary of AT&T, at a valuation of $14 billion — seven times its 1995 sale price.

Over the following two decades, QVC kept pace with the times, introducing high-definition video, offering digital broadcast television, and quickly integrating with Facebook and Instagram as social media rapidly developed. It also acquired several e-commerce companies. For instance, in 2015, QVC acquired Zulily, a母婴产品电商, for $2.4 billion.

But by 2017, challenged by Amazon and numerous new e-commerce companies, the teleshopping industry faced further consolidation. QVC acquired a 62% stake in HSN for $2.1 billion. After the two giants merged, they became the sole dominant player in American teleshopping.

QVC's success factors can be summarized in three points:

- Traffic-side advantages. QVC consistently had the backing of television industry heavyweights. From Comcast at the beginning to Fox later on, they provided capital and resources that helped QVC secure prime-time slots on TV channels and gradually capture consumers' mindshare.

- Differentiated products and services. QVC's style differed considerably from HSN's, evident in the environment and atmosphere of their programs. HSN more closely resembled the traditional Chinese teleshopping model — telling you this product is incredibly cheap and will be gone in ten seconds if you don't buy now. QVC's style was closer to chatting with friends: several hosts in a home-like setting discussing whether food tastes good or furniture works well. This warm, approachable atmosphere enabled product differentiation and established a more premium, more trustworthy brand image in consumers' minds.

- Scale effects in traffic and supply chain through M&A and expansion. A series of acquisitions and expansions ran throughout QVC's development. Remarkably, some acquired companies were larger than QVC itself. For example, when acquiring CVN between 1987 and 1992, CVN was roughly more than twice QVC's size at the time. Overall, thanks to formidable capital operation capabilities and funding advantages, QVC achieved scale effects on both the traffic and supply chain sides, firmly maintaining traffic dominance while realizing category expansion, channel expansion, and business model iteration.

A Key Secret to the Rise of American Teleshopping: Scale

From the histories of HSN and QVC, scale emerges as a key secret to the rise of American teleshopping.

The American teleshopping industry showed clear consolidation trends. In the 1980s, over 30 teleshopping companies competed; later only two giants remained, which further merged into one by 2017.

We can see the concrete impact of scale effects from data released at the time of QVC and HSN's 2017 merger. QVC believed the merger could improve performance by over $300 million — a considerable figure representing roughly 43% of the two companies' combined pre-merger profits. In other words, integration could boost profits by 43%.

A major variable affecting profits was television slot fees. These can be understood as the traffic costs of the internet era — teleshopping companies paid television channels substantial fees to secure prime-time positions.

Before the merger, the slot fees paid by QVC and HSN as a percentage of their respective revenues differed significantly. QVC's slot fees accounted for roughly 5% of revenue; HSN's ratio was 10%. With net profit margins in teleshopping around 3-7%, a 5-percentage-point gap could mean the difference between profitability and loss.

After the merger, because QVC was larger (its revenue was roughly 2.4 times HSN's at the time) and had consistent support from television giants, it could capture market share at lower traffic rates. Assuming the merged company paid QVC's 5% traffic rate, it would save $124 million annually.

Beyond slot fees, scale effects could also improve logistics and transportation efficiency. QVC's initial estimate was that the merger would enhance bargaining power with logistics companies and reduce duplicate logistics facility investments, saving millions to tens of millions of dollars in logistics turnover costs.

On the revenue side beyond cost savings, the QVC-HSN merger could cover broader user bases and product categories. The two companies' customer bases had low overlap: of QVC's 8 million customers, 6 million didn't shop at HSN. Their product categories also differed — QVC excelled at electronics and health and fitness products, while HSN focused on fashion and beauty — creating room for revenue growth as well.

Given the many benefits of scale and integration, why hasn't Chinese teleshopping shown clear consolidation trends?

Indeed, from a market share perspective, the Chinese teleshopping industry is relatively fragmented, with half the market split among 7-8 companies, compared to just two in the U.S. In China, teleshopping has particular characteristics. It's a heavily regulated industry with licensing requirements. Many teleshopping companies are backed by television stations, and mergers between television stations are relatively uncommon domestically.

However, Chinese consumers' attention is relatively concentrated. An Analysys International survey found that over 90% of teleshopping consumers shop only on specific channels, with 80% of shopping behavior concentrated on a small number of shopping channels.

▍Integrating upstream and downstream to improve product selection and supply chain management efficiency

Integrating upstream and downstream to achieve efficient product selection and supply chain management is the second secret to the rise of American teleshopping.

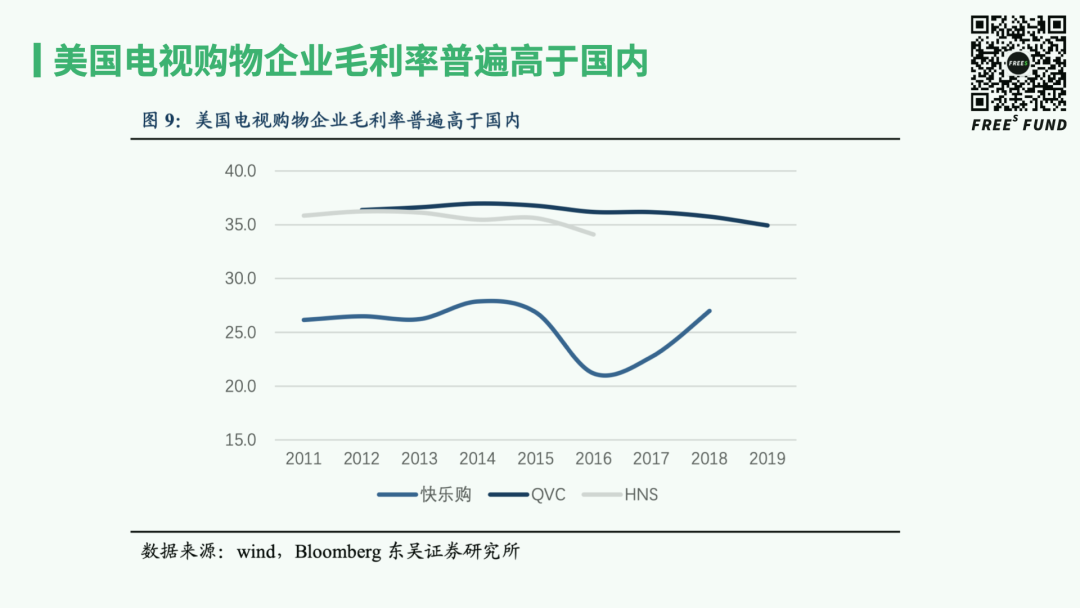

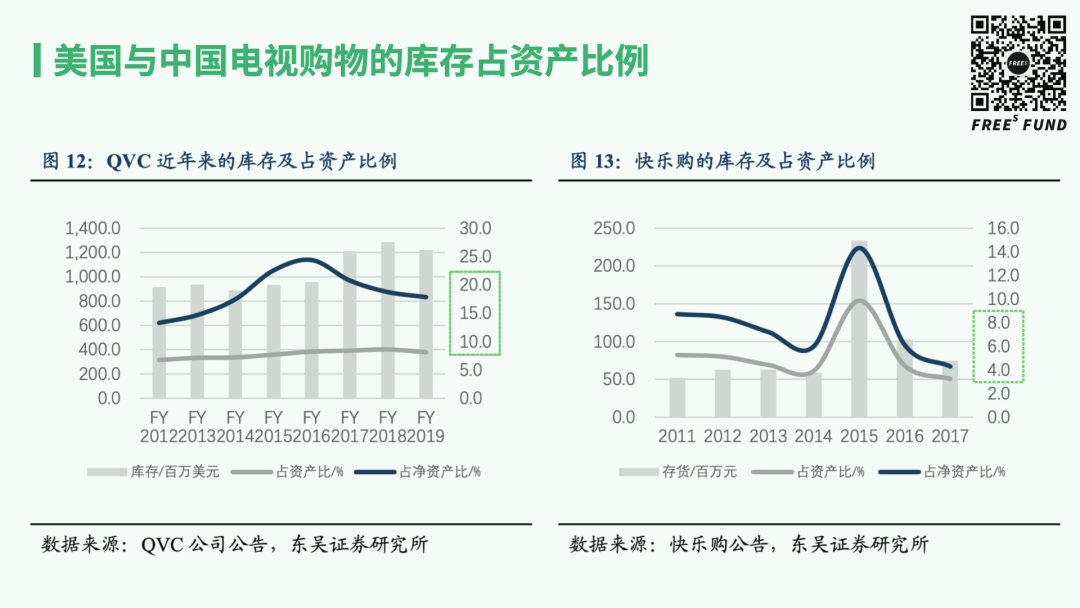

QVC and HSN maintained gross margins of roughly 30-40% over the long term, considerably higher than domestic Chinese counterparts. According to data from Wind, Bloomberg, and Soochow Securities Research Institute, Happy Go — a Chinese teleshopping company — had gross margins around 20-30%, noticeably lower than QVC.

The key to QVC's high gross margins lay in controlling many links itself — sourcing, product selection, procurement, and inventory — thereby increasing bargaining power with suppliers.

This is evident from QVC's inventory as a percentage of assets. The higher the ratio of inventory to net assets, the more goods a company manages itself. QVC's inventory-to-assets ratio was around 20%, while Happy Go's was roughly 4-8% — a considerable difference.

By controlling product selection, sourcing, and merchandise flow itself, QVC could better optimize its categories, selecting higher average-selling-price, higher-margin products. Among categories sold on QVC, home products accounted for the largest share of sales, with jewelry and electronics also representing substantial proportions.

Domestically, whether in teleshopping or current live-streaming e-commerce, products generally have lower average selling prices and margins. For example, the main products in live-streaming sales are food and beverages, personal care, and clothing, with many products priced below 50 RMB.

/ 03 / What entrepreneurial opportunities exist in China's live-streaming e-commerce market?

Having examined the history of American teleshopping, we turn to the question: in China's current live-streaming e-commerce landscape, what kinds of players can succeed? What entrepreneurial opportunities will emerge? Particularly in the brand space we focus on, will new brands rise that adapt to new media formats?

Our preliminary thinking is that in China's current live-streaming e-commerce landscape, scale — or the traffic advantages brought by head-of-market effects — and control over supply chains (including product selection and sourcing management) remain critical elements. New brands that can rise from live-streaming e-commerce as a new media format will need to possess storytelling, demonstrability, novelty, and combine these with the new characteristics of live-streaming e-commerce.

▍Traffic advantages from head-of-market effects in live-streaming e-commerce

Head-of-market effects have already become pronounced in the live-streaming landscape. From the composition of streamers, research by the AliResearch Institute and KPMG in Live-Streaming E-Commerce: Toward a Trillion-RMB Market found that head streamers representing only about 2% of the total by number captured nearly 80% of GMV market share.

Looking more specifically at the sales performance of head streamers across different platforms, according to data from Syntun and other institutions, during the 2020 Double 11 period, Taobao platform streamers Viya and Austin Li achieved GMV of 12.3 billion and 9.8 billion RMB respectively, Kuaishou head streamer Simba achieved 2.8 billion, and Douyin head streamer Yonghao Luo's result was roughly 360 million RMB.

Although Taobao, Kuaishou, and Douyin are all leaders in live-streaming commerce, their platforms' head streamers demonstrate sales capabilities at the hundred-million, ten-billion, and billion RMB levels respectively — with pronounced Matthew effects.

Similar to teleshopping giant QVC in its era, these head streamers attract substantial user attention.

However, individual streamers are difficult for entrepreneurs to replicate or invest in, because in the long run, the sustainability of individual creativity and charisma is uncertain. One promising direction is institutionalized content production — operating multiple IPs, producing relatively replicable content, and thereby achieving scale.

A scaled traffic entry matrix may help live-streaming e-commerce achieve greater volume development. Recently, leading MCN agency Dayu Network completed a Series A financing round of several hundred million RMB. It specializes in building anime IPs; its IP "Little Monk Yichan" has over 40 million followers on Douyin, with at least 5 additional million-follower-plus influencers in its portfolio.

When it comes to content approaches, two directions are worth considering. One is QVC's signature friend-chat format — companion-style content. The other is the currently popular Japanese model, where trained professionals lead product demonstrations and drive sales. Rather than spending heavily on top-tier influencers, many brands are now turning to beauty consultants, sushi chefs, sommeliers, and other specialists to explain product details and attract customers. This is a more readily replicable content production model.

▲ Informational live-streaming commerce in Japan.

▍Upstream supply chain integration is inevitable

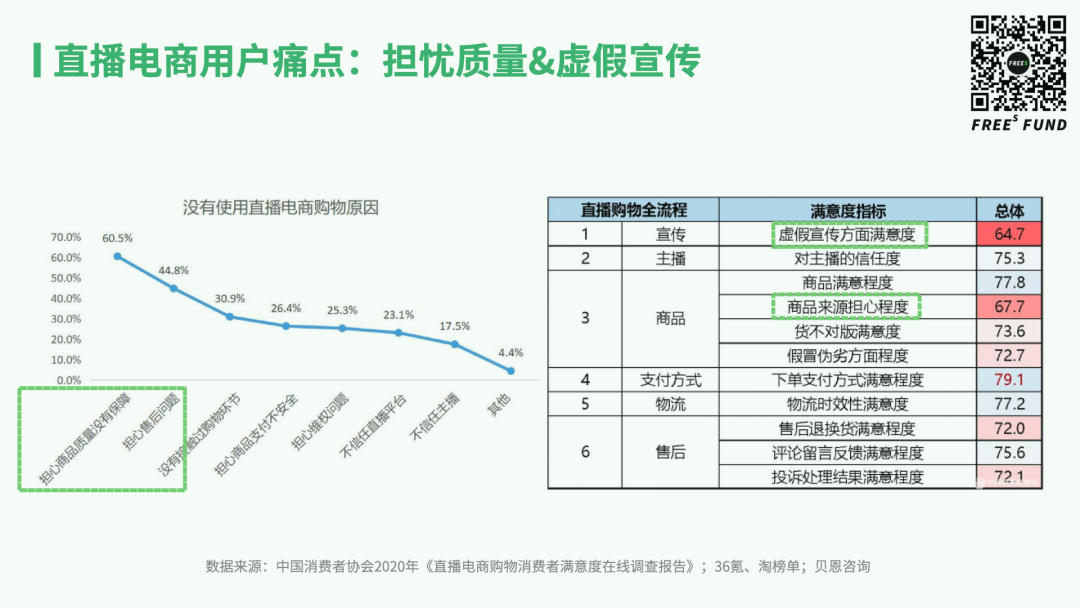

A major pain point for live shopping users is concern over product sourcing, quality, and false advertising. The recent fake bird's nest incident involving influencer Simba sparked significant controversy, and even after his public apology, many remained dissatisfied.

Often, whether it's false claims or user anxiety about product quality, the root cause lies in influencers' lack of control over their supply sources. Integrating upstream into the supply chain can better address quality control issues.

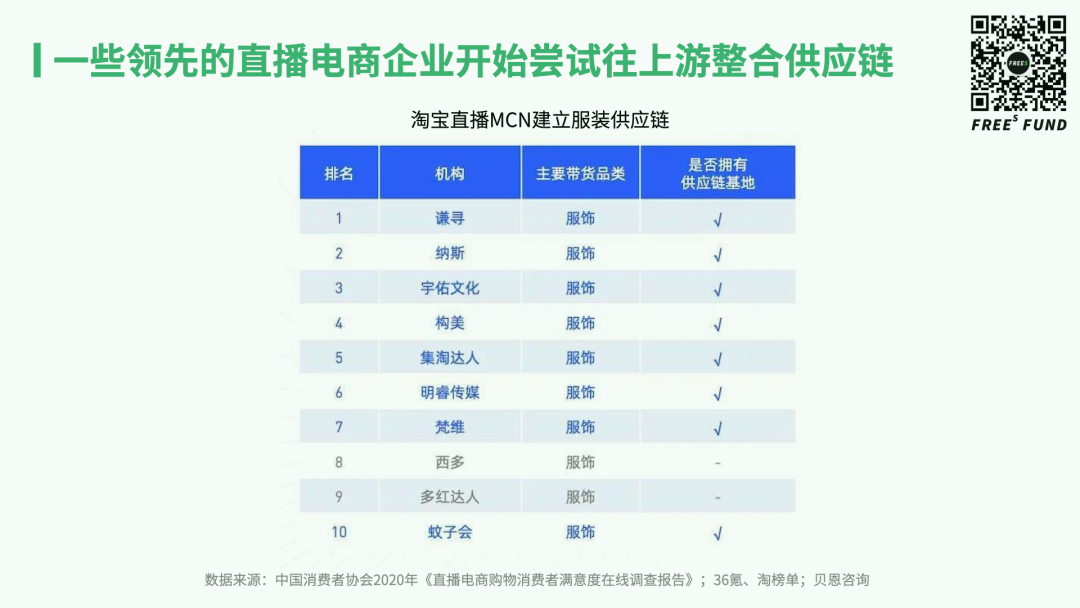

Some leading live e-commerce companies are already experimenting with upstream supply chain integration — this may represent another future trend for the sector. Currently, 8 out of 10 top domestic apparel-focused live-streaming MCNs have begun building their own clothing supply bases.

▍Traits "broadcast-native brands" might possess: storytelling, demonstrability, novelty

FreeS Fund has long tracked the development of new brands. As live-streaming e-commerce enters a new phase of growth as both medium and channel, will fresh brand opportunities emerge?

We can infer potential characteristics of new brands in live e-commerce by examining the history of TV shopping and the nature of new media.

As noted earlier, one key to QVC's success was its rigorous product selection. What principles from QVC's curation might apply to new brands in live e-commerce?

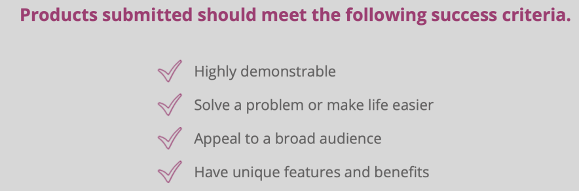

First, QVC places heavy emphasis on the stories behind brands and products. Through televised live streams, QVC aims to tell compelling, relatable brand narratives — does your product solve a problem, fill a gap, or make consumers' daily lives easier?

A crucial element of QVC's internal host training is conveying "attainable aspiration" — giving consumers brand stories that feel within reach yet still inspire desire. For example, through before-and-after beauty transformations, viewers are led to imagine themselves in that improved state. QVC's experiments in the 1990s have since become standard practice for cosmetics brands.

▲ Diagram from QVC's internal training on the "attainable aspiration" concept.

Only through such storytelling can brands forge genuine connections with consumers in the highly visual, strongly interactive live-streaming environment, rather than merely selling products.

Recently, live e-commerce has seen growing traction for non-standard, low-frequency, high-ticket items like secondhand luxury goods, collectibles, and jewelry — categories well-suited to storytelling. Their information asymmetry and relatively premium positioning give them depth of product narrative. The friend-chat live format, similar to QVC's approach, works well for telling these products' stories.

Second, QVC's curation emphasizes product demonstrability. Video streaming's multi-sensory stimulation is ideal for real-time demonstrations of complex product features — showing home appliances in use, makeup before-and-afters, or home decor items staged in simulated living spaces.

The fact that home products rank as QVC's largest category owes much to live streaming's sensory-rich, demonstration-friendly nature. Viewers drawn in by live demos both pass time through entertainment and gain better product understanding.

▲ QVC's product selection criteria.

Finally, QVC pays close attention to novelty and distinctiveness. Sufficiently fresh products capture attention and drive impulse purchases within relatively short broadcast windows. Chinese TV shopping hits like back braces and electronic learning devices largely followed this playbook.

TV shopping and live e-commerce share strong similarities across these three dimensions: storytelling, demonstrability, and novelty. In the live e-commerce market, new brands with comparable traits will likely emerge.

Of course, live e-commerce as a new medium has its own particularities — stronger user interaction, more precise user data, and diverse private traffic strategies, among others. Numerous brands have already begun embracing live e-commerce, whether by partnering with top influencers or launching their own streams. In 2020, brand self-streaming already accounted for 60% of Taobao's Singles' Day live GMV, with major beauty and apparel brands regularly drawing millions of viewers during their broadcasts.

As live streaming becomes standard equipment for brand sales, we believe that amid the broader trend of consumption upgrading, new media and new channels will catalyze new supply and new brands. However, we care about innovation not just in traffic and content, but equally in supply-side innovation and product strength. Thus, new brand entrepreneurship today has become a full-chain efficiency competition, testing founders' comprehensive capabilities.

To summarize, live-streaming e-commerce shares many parallels with TV shopping's 40-year history. Looking to the past, we can discern several directions for live e-commerce's future:

After comparing TV shopping's penetration of total retail sales, the coverage scope and operational efficiency of live e-commerce versus TV shopping, and live streaming's current share of e-commerce GMV, we find that live e-commerce is likely a multi-trillion-RMB market representing genuine, enduring demand.

From the history of American TV shopping, the traffic advantages of scale and the product selection and supply chain control enabled by vertical integration were critical success factors — and may represent trends in live e-commerce's evolution.

In this period of new development for live e-commerce as a medium, brands possessing storytelling, demonstrability, and novelty that can combine with live e-commerce's distinctive characteristics will enter a golden period of growth.

Closing Question: Within the live e-commerce ecosystem, beyond storytelling, demonstrability, and novelty, what other traits do brands need? What specific types of new brands might emerge?

Share your thoughts in the comments.

Where Does Live E-Commerce End Up? | FreeS Research

From the Rise to the Calm: Is Live E-Commerce a Feature or Business Model? (Part 1) | FreeS Research

Li Feng Column 15 | How Long Can Live E-Commerce Stay Hot?

FreeS Report 19 | The Tipsy Era: Where Are the Opportunities in Low-Alcohol Entrepreneurship?

Understanding the Instant Food Boom in 4 Minutes | FreeS Daily Business Thoughts