Why Are Chinese and American VCs Drifting Apart? | Li Feng Column

"Shifting from Virtual to Even More Virtual" vs. "Shifting from Virtual to Real"

This is the second piece in our 2022 macro series. In this series, I want to explore with you the shifts and turbulence in capital markets in recent years, the landscape and opportunities, and what's behind the divergence between Chinese and American VC.

In last week's first installment, Will 2022 Be a Capital Winter?, I examined the circumstances and trajectories of Chinese and American capital markets this year through short-term, medium-term, and long-term lenses.

Our view is that while both countries' capital markets have experienced turbulence this year, they are not facing the same "winter." If we compare each country's economic cycle to the four seasons, the U.S. is currently in "late autumn heading into winter," while China is more like a "late spring cold snap." Interested readers can click the title link in the previous article to read Part One.

In this second installment, I'll explore another topic closely tied to venture investing — the diverging paths of Chinese and American VC.

"Has Web3.0 emerged in China?" has been a frequently asked question in domestic VC circles this year. Some believe the timing isn't right for Web3.0 in China; others are convinced that Web3.0 is the future, an unstoppable trend.

The heat and controversy that Web3.0 has generated in Chinese VC circles actually reflects a broader trend: the world's two largest economies, which are also the two most favored destinations for international capital, appear to be diverging in their entrepreneurial directions.

A quick look at currently hot investment sectors in China and the U.S. shows limited overlap between the two.

In this article, I'll examine the characteristics of Chinese and American VC today, and what has caused their paths to diverge.

Here are the main arguments up front:

- China and the U.S. are in different economic cycles, and their capital markets have developed different emphases accordingly. Chinese VC is moving "from virtual to real," focused on serving the real economy. American VC is moving "from virtual to virtual," centered on innovation around services and the non-real economy.

- Differences in industrial structure mean that even when facing the same technologies, the two countries apply them differently.

- Differences in how industries develop have created divergent business models.

- The divergence in Chinese and American VC paths results from the combined effects of different industrial structures, different industry development patterns, different capital market conditions, and different financial cycles. Neither is superior or inferior; investors and entrepreneurs need to tailor strategies to their local context.

I hope this offers some useful angles for thinking about these issues.

Reader Giveaway From your perspective, did Chinese and American capital markets face a winter in 2022? Share your thoughts in the comments. The 6 most thoughtful commenters will receive a custom FreeS Fund edition of 2030: How Today's Biggest Trends Will Collide and Reshape the Future of Everything. I look forward to finding certainty amid change, and staying sharp together.

01

From Virtual to Real

V.S.

From Virtual to Virtual

Chinese VC is currently moving "from virtual to real," while American VC is moving "from virtual to virtual." How did we reach this conclusion? Let's look at some conditions in both countries' capital markets — highly relevant to investing.

Under policy guidance, China's financial sector as a whole is moving "from virtual to real." The state advocates that "finance is the lifeblood of the real economy; serving the real economy is finance's duty, its purpose, and the fundamental measure for preventing financial risk." This makes clear that China's capital markets must ultimately serve the real economy.

In Will 2022 Be a Capital Winter?, we noted that in 2021, China's total capital market approached 80% of GDP — completely different from seven or ten years ago. Capital markets have gradually become a significant tool in China's economic development.

For this reason, investment in China today needs increasingly to connect with economic structure; it needs to move from virtual to real. So investment trends have gradually evolved toward "investing in projects tied to economic structure." Hot concepts in recent years like industrial internet and industrial digitization are essentially about using internet models and digitalization to serve real industries.

For example, FreeS Fund portfolio company Hande Technology applies intelligent digital transformation to China's massive logistics industry; another portfolio company, Yiniu Technology, standardizes and digitizes the home repair industry. This is what we mean by "from virtual to real."

Now look at the U.S. As investors, we find many early-stage investment innovations there quite interesting, but we also watch whether these directions are inflated by end-of-financial-cycle froth.

In the first macro piece, we mentioned that after multiple rounds of historically unprecedented quantitative easing, U.S. equities generated substantial end-of-cycle bubbles. The Fed's subsequent rate hikes and balance sheet reductions have left these bubbles on the verge of bursting. Whenever at the tail end of an extended financial cycle, a country like the U.S. — where finance-related industries account for a high share of GDP — typically sees financial innovation detached from the real economy, such as NFTs, Web3.0, or blockchain.

Beyond the influence of end-of-cycle bubbles, there's another reason for American VC's "from virtual to virtual" trajectory: its own economic cycle.

Let's rewind to the last century. Starting in the 1950s, high-tech companies gradually emerged along the southern end of San Francisco Bay. Most were in the semiconductor and computer industries, processing and manufacturing high-precision silicon. This area later became known as "Silicon Valley."

Once Silicon Valley companies clustered, Bay Area VC emerged to help found and expand companies. Nasdaq followed shortly after. At that time, both VC and Nasdaq existed to help emerging real-economy industries grow and expand. The core of these industries was "silicon" — chips, wafers, manufacturing, and computers. Today, these industries are no longer as hot in the U.S. as they are in China.

You could say that in that era, American companies centered on Silicon Valley generated massive technological innovation around real-economy industries, and VC investment was relatively "real-oriented." So why has the U.S. moved "from virtual to virtual" now?

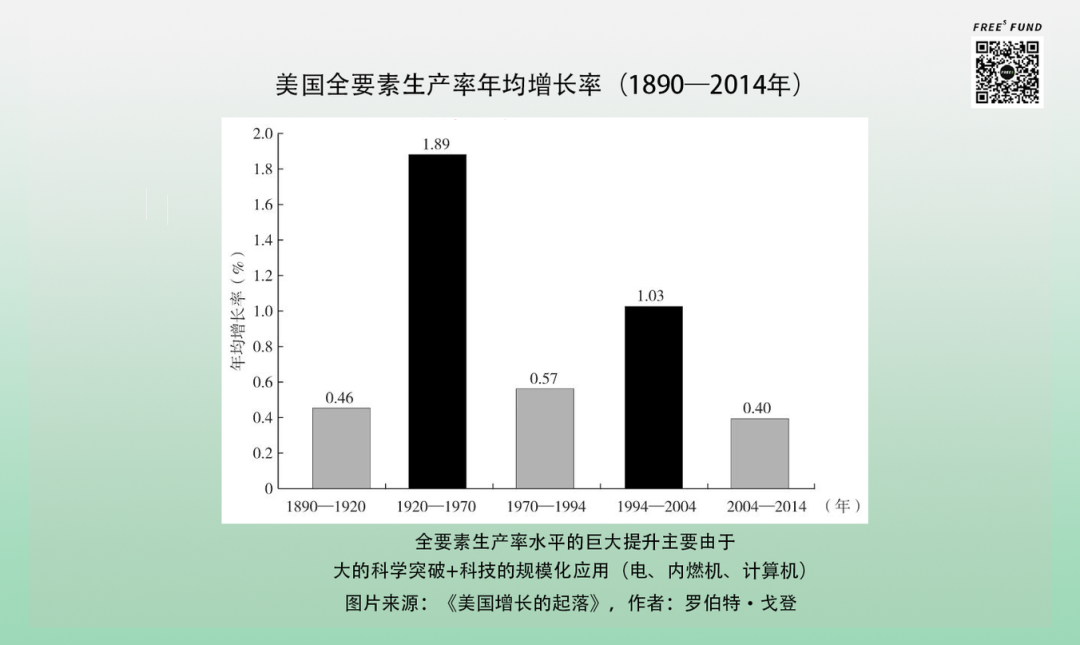

Here we need to introduce a concept: Total Factor Productivity (TFP), which measures the input-output ratio of a system given fixed capital, labor, and resource inputs. It's also the best indicator for analyzing the potential impact of innovation and technological change on economic growth.

Looking back at America's TFP cycles, U.S. total factor productivity saw significant increases in two main phases, both attributable to vigorous innovation and technological change.

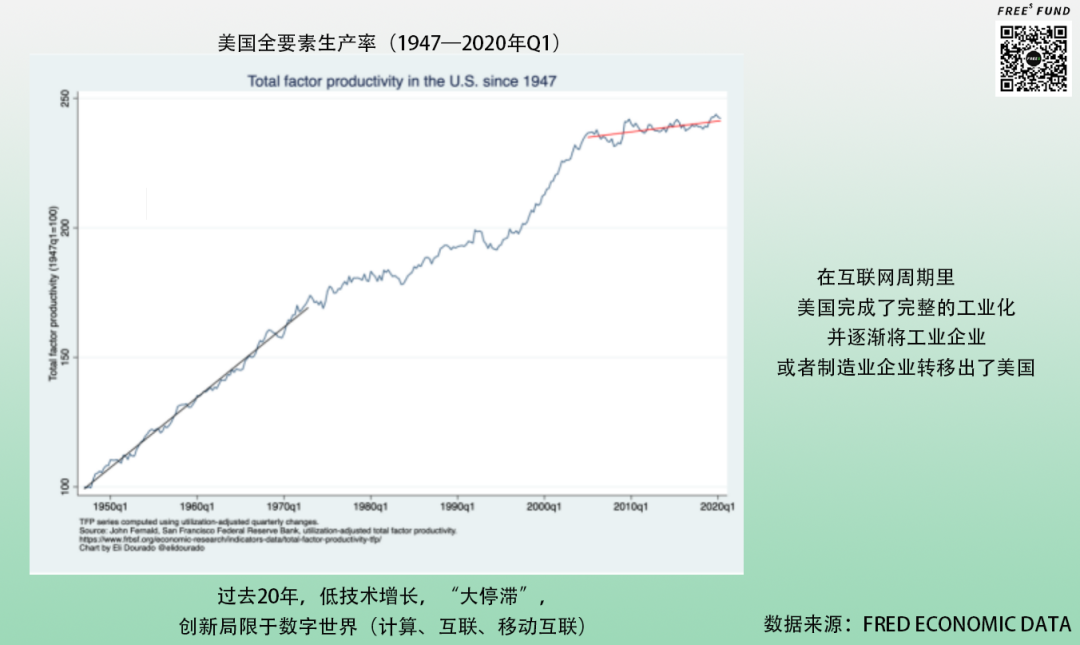

But over the past 20 years, U.S. TFP growth has nearly stagnated. On one hand, technological innovation has hit bottlenecks; on the other, throughout the internet cycle, the U.S. gradually shifted its industry and manufacturing globally, concentrating development in services and non-real-economy sectors like finance.

By comparison, China is currently taking technology "half a step down," applying it to the real economy and industries to seek more efficient growth; the U.S. may need to push technology "half a step forward" to create more possibilities for non-real-economy industries and services — hence "from virtual to virtual."

02

Differences in Industrial Structure

Lead to Divergent Thinking

Above, we briefly laid out current capital market conditions in China and the U.S. to demonstrate the path differences in each country's financial sector. Before the next topic, consider this question: What is the essence of investment?

We can roughly summarize the essence of investment as providing resource allocation for economic development — that is, aligning with economic development trends, injecting capital and resources into industries and enterprises that are growing rapidly or receiving focused attention, and helping them grow better. What does this development trend depend on? It depends on a country's industrial structure.

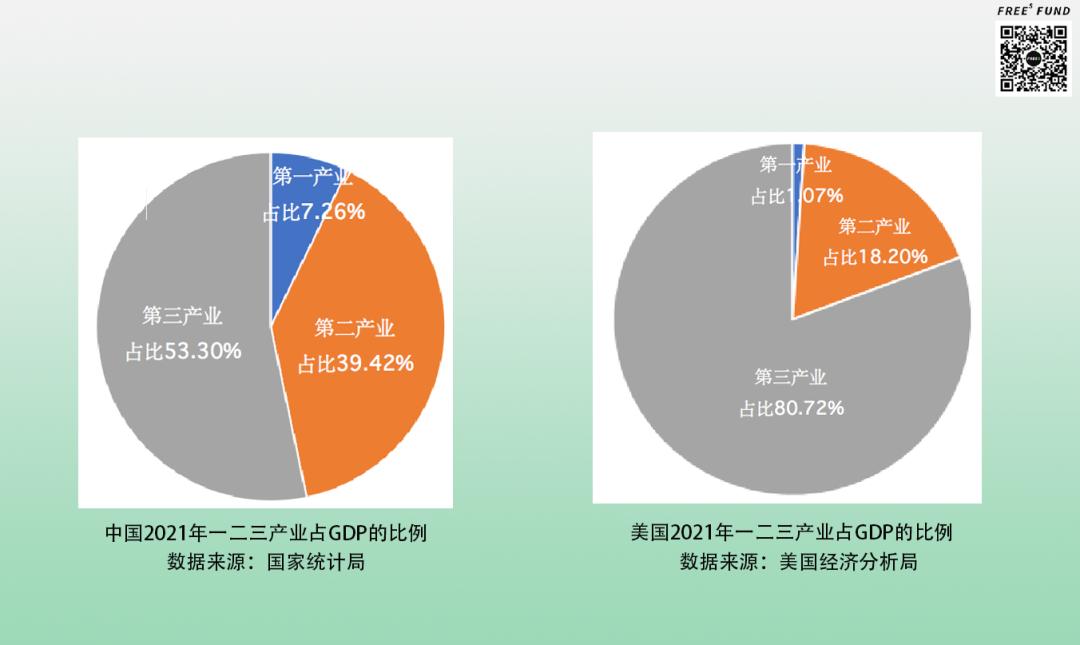

Looking at industrial structure, over the four decades of reform and opening up, China's economic center of gravity has gradually shifted from the primary sector (agriculture) to the secondary sector (industry), and is now moving toward the tertiary sector (services). In the US, since World War II, the primary sector's share has declined year by year while the tertiary sector's share has risen rapidly, with economic growth increasingly driven by commercial services and social services.

In the 2021 GDP composition of both countries, China's three sectors accounted for 7.26%, 39.42%, and 53.30% respectively. It's clear that while the tertiary sector is now the dominant component, the secondary sector's contribution remains significant.

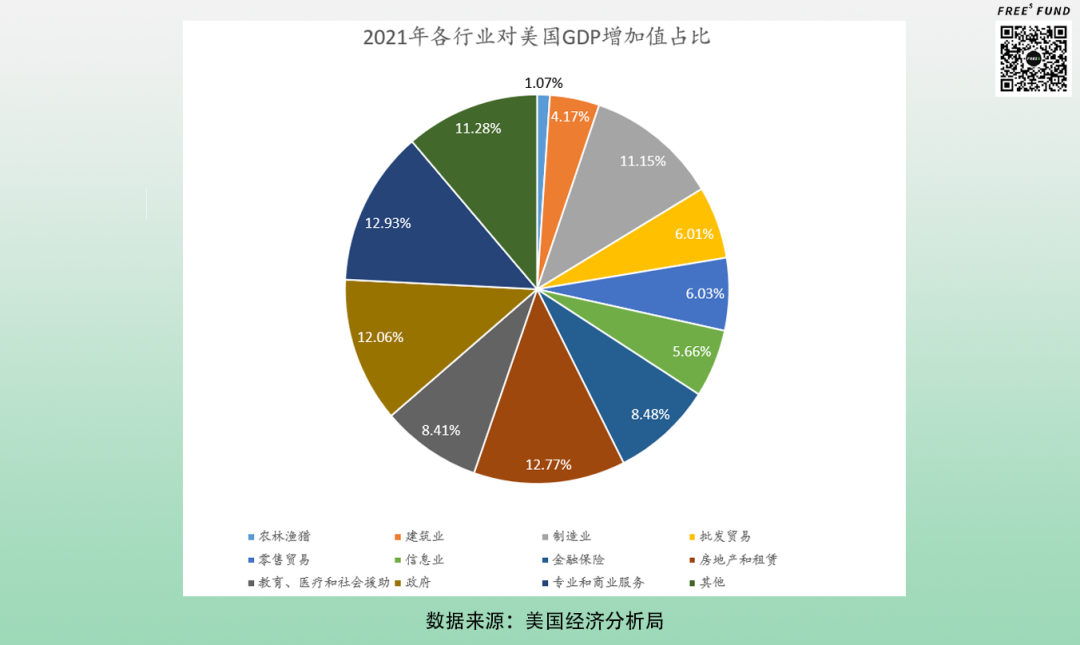

In the US, the tertiary sector far exceeds the other two, comprising over 80% of GDP. The secondary sector accounts for just 18.2%, and the primary sector a mere 1.07%.

Let's analyze the two countries' industrial structures from another angle.

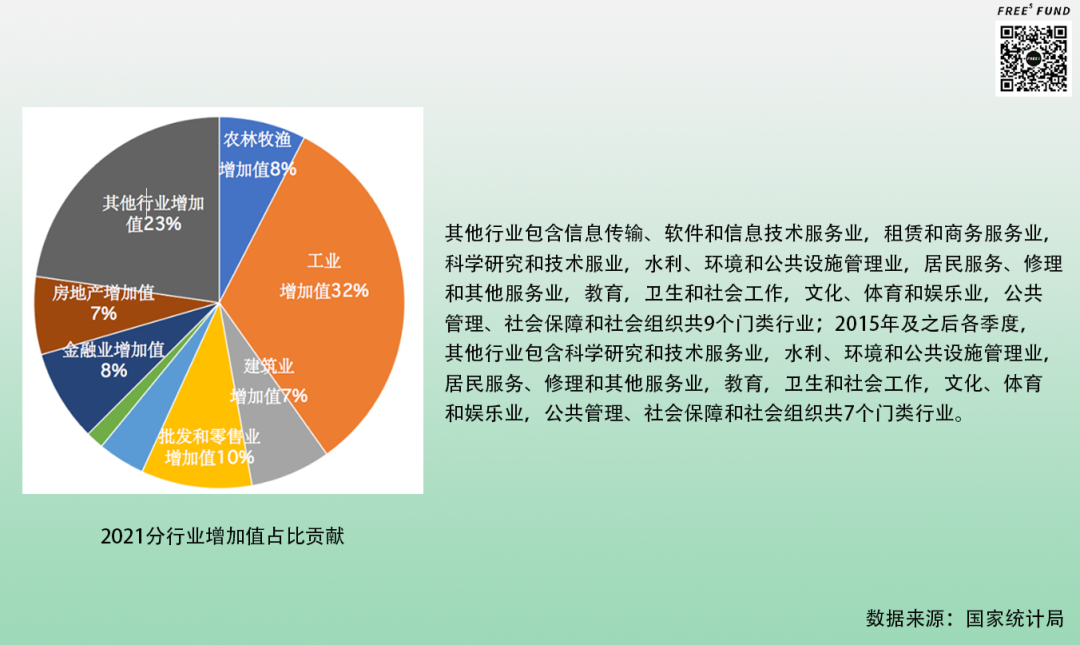

Putting together China's GDP composition above with the sectoral breakdown of GDP value-added contributions below, we can observe two phenomena: the tertiary sector has begun to play a noticeably stronger role in driving China's economic development; and industry still contributes substantially to China's economic growth.

In 2021, China's GDP grew 8.1% year over year. Within that 8.1%, industry — part of the secondary sector — contributed the largest share to GDP growth at 32%. Next came value-added from various service industries, at 23%.

So we can see that many of China's current hot industries are connected to raising the value-added of manufacturing and industry — new energy vehicles, industrial internet, and so on.

Turning to the US: in 2021, American GDP grew 5.7% year over year. The data shows relatively balanced contributions across sectors. Tertiary industries including finance and insurance, professional and business services, and education, healthcare, and social assistance combined for a high contribution of nearly 30%, followed by manufacturing, government, and others. But the total value-added contribution from manufacturing and other secondary industries was comparatively small, with less pull than in China.

So how do these divergent industrial structure trends we've outlined manifest in capital market development paths?

Take synthetic biology — a hot industry in Chinese and American VC circles over the past six months. In the US, synthetic biology technology has largely been applied to biopharmaceuticals, represented by companies like Amyris and Precigen. In China, synthetic biology technology has almost entirely been applied to chemistry and chemical-related industries, represented by companies like Cathay Biotech, Huaheng Biotech, and Bluepha (a FreeS Fund portfolio company).

Why this difference in application? From China's perspective, the country's basic chemical industry accounts for roughly 40% of global chemical industry output. McKinsey & Company projections show that over the next decade, China will provide more than half of global chemical industry growth.

Moreover, as China's economic policy increasingly shifts from investment-driven growth to consumption-driven growth, and as consumption-driven growth turns toward demand for more sophisticated products, the result may be further growth in demand for specialty chemicals. For example, growth in the premium personal care products market may drive demand for more complex specialty surfactants.

Similarly, Chinese consumption trends will create new opportunities. The rapid growth of online food shopping, for instance, may increase demand for new packaging materials, which could in turn increase demand for innovative products like biodegradable polymers.

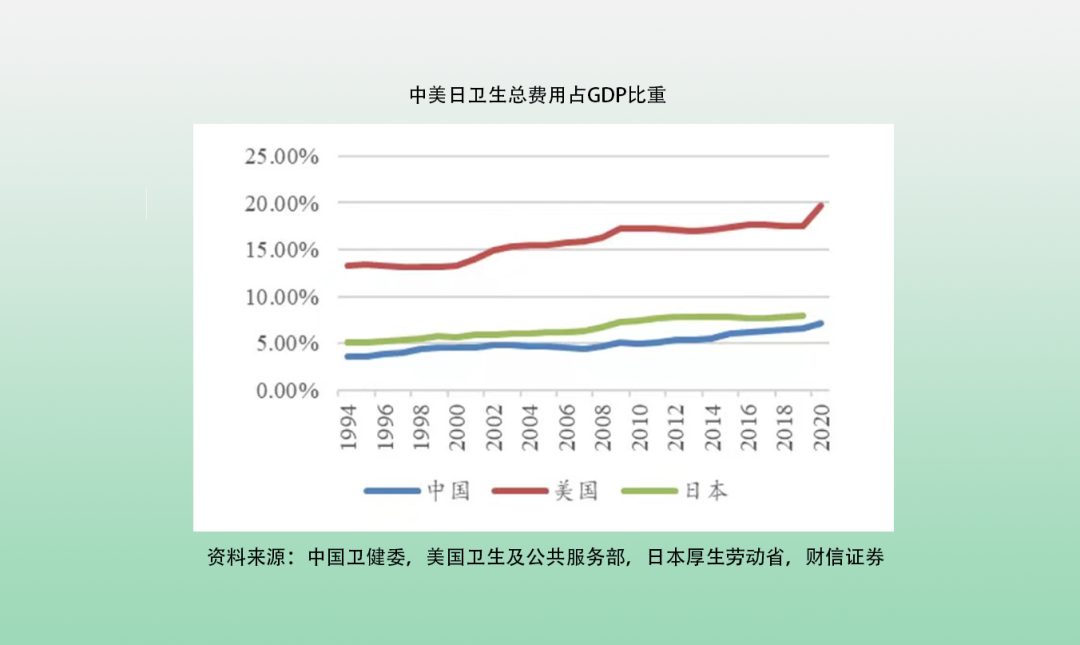

From the US perspective, its chemical industry is far from matching China's scale, but healthcare is a heavyweight industry in America. In 2020, US national health expenditure reached 19.7% of GDP — a historic high — with public and private healthcare spending far exceeding other developed countries and China.

Additionally, US new drug R&D and pharmaceutical spending are substantial — several times the scale of China's industry. While China's healthcare industry is developed, it still lags behind the US: in 2020, China's total healthcare expenditure was about 7% of GDP, and new drug R&D accounted for less than 20% of total healthcare spending.

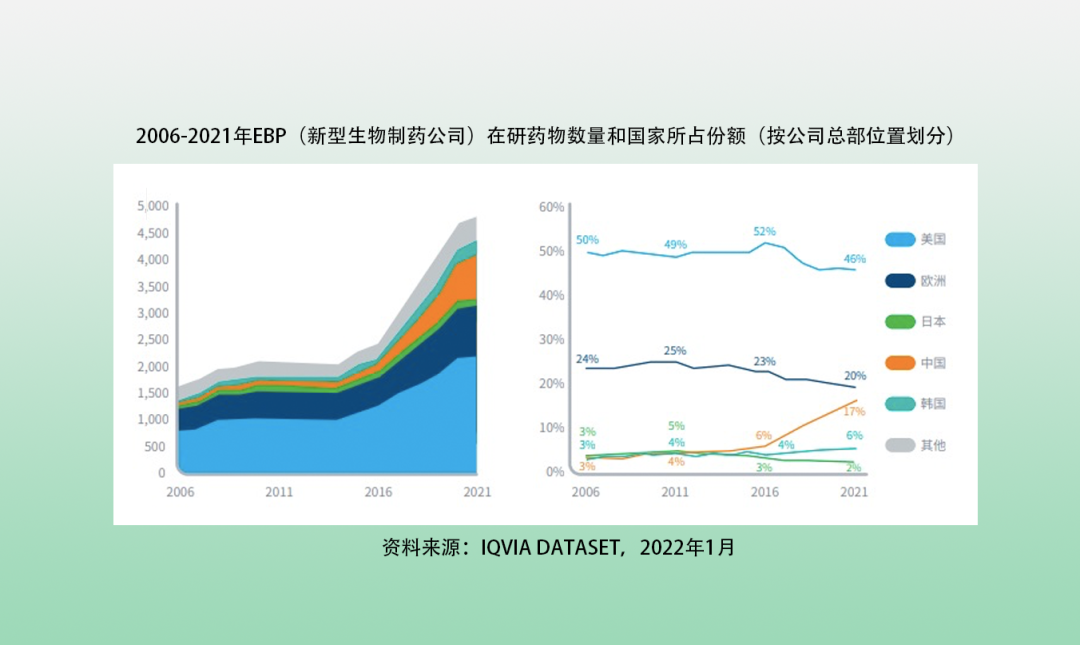

North America, especially the US, has nearly dominated the global drug development market. In recent years, the rising prevalence of various chronic diseases in the US has been a major factor attracting pharmaceutical companies to invest in new drug R&D. CDC data shows that over 90 million American adults have at least one cardiovascular disease, and more than half the population has at least one chronic condition such as cancer, cardiovascular disease, respiratory disease, or neurological disease. This has increased demand for new and innovative drugs, and provided the synthetic biology industry with abundant application scenarios in pharmaceuticals.

One heavy on chemicals, one heavy on healthcare. This industrial structure difference produces the result that China applies synthetic biology mainly to chemicals, while the US applies it primarily to biopharmaceuticals.

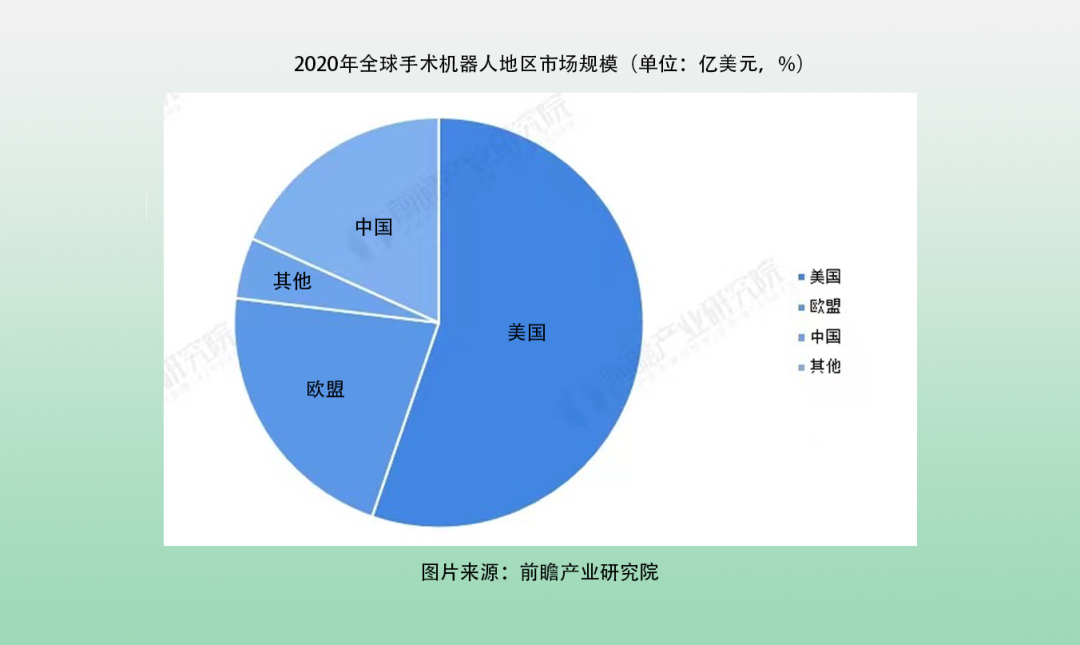

A second example: in robotics. Currently, the US is focused on the surgical robotics market, while China is focused on industrial robots.

But industrial robots were actually born in the US. Around 1961, the US pioneered industrial robots, yet subsequent market share was captured by the "Big Four" from Europe and Japan. Several main reasons explain this:

- After WWII, US unemployment surged; using people was more urgent than using robots, so the government had no policy incentive to support robotics industry development.

- Japan and Germany, as defeated WWII powers, had lost large portions of their populations and faced severe postwar labor shortages.

- Japan's and Germany's auto industries rose in the 1960s and 1970s, generating demand for industrial robots.

These factors combined to shift industrial robot market share from the US to Europe and Japan.

Currently, the main global market for industrial robots has shifted to China. As of 2021, China had ranked first globally for eight consecutive years; in 2020, China's installations accounted for 44% of global total, with sales growth consistently outpacing global growth.

On one hand, China's call for technology to serve real industries creates substantial manufacturing demand, stimulating the flourishing development of the industrial robot sector. The 14th Five-Year Plan also proposed supportive policies for the robotics industry, driving progress from quantity to quality.

On the other hand, after the demographic dividend's pull on economic growth gradually faded, Chinese industry has been seeking transformation toward intelligence and efficiency to improve TFP — factors that have generated substantial demand for the robotics industry.

Looking back at the US: during the internet cycle, America moved its industrial system out of the country and turned to developing the tertiary sector. Thus in industrial robotics, it lacked the strong impetus that Japan and Germany had.

But the rapid development of the US tertiary sector, especially healthcare, created opportunities for medical robots. In 2020, the US surgical robotics market was $4.6 billion, accounting for 55.1% of the global market, while China's surgical robotics market that same year was $400 million — less than 10% of the US figure.

In summary, differences in industrial structure development trends have caused the same technology to develop with different emphases in China and the US, producing divergent VC thinking between the two countries.

How Differences in Industry Development Laws Catalyze Divergence

The industrial structure perspective is relatively macro. Let's go down one level and focus on industry development laws. When entrepreneurs discuss differences in China-US startup directions, they inevitably face this question: if laying out operations in one or both countries, what are the main differences in innovation and entrepreneurship paths between the two?

Overall, American and Chinese industry development laws differ considerably.

Before the internet entered various industries, many US industries had already fully competed offline and matured. In China, the internet typically entered industries during their high-speed growth or rapid expansion phases, growing together with the industry. This difference also produced many divergent business models between China and the US.

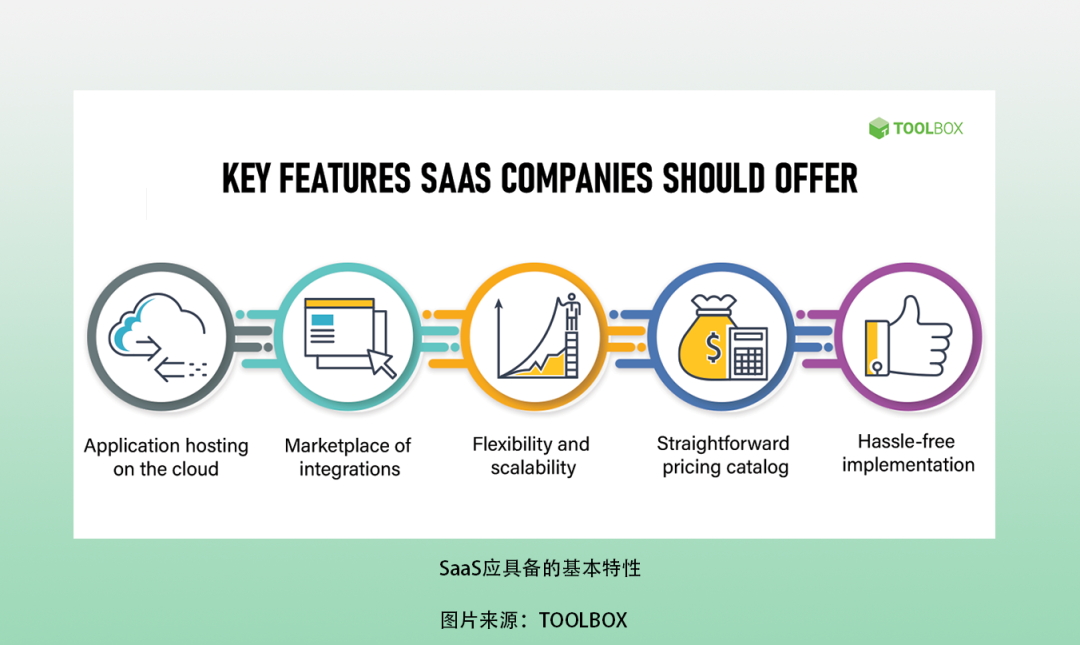

Take SaaS, which has attracted considerable attention in recent years. According to a ReportLinker report, from 2021 to 2025, the global SaaS market will expand by a staggering $99.99 billion. The US SaaS landscape already contains numerous public companies and industry unicorns, such as Google, Amazon, and Salesforce — both consumer-facing and enterprise-facing products.

Looking domestically, around 2011 and 2012, people began saying that spring had arrived for Chinese SaaS. After that, every year or two, this "spring" would be mentioned again.

In recent years, Chinese SaaS public companies have indeed grown rapidly. On the consumer side, there are Tencent, Alibaba, and others, whose market caps can compete with America's top players. But on the enterprise side, China still hasn't produced a SaaS leader with a market cap exceeding $30 billion (comparable to Zoom or Salesforce). I once chatted with a SaaS entrepreneur who said that rather than calling it spring for Chinese SaaS, it was more like they'd reached Spring Festival.

Why this difference? As mentioned above, before the internet arrived, American industries had largely formed complete, relatively mature supply chains through adequate competition. When internet technology began entering American industries, it was roughly during the "stagflation" period of the 1970s. At that time, upstream resource industries (mining, agriculture, forestry, animal husbandry, and fisheries) and monopolistic industries (oil, tobacco) performed relatively well, while finance and tech manufacturing lagged behind, with consumer industries at the bottom.

To improve efficiency in difficult conditions, many enterprises widely adopted software productivity tools on top of already mature offline industrial chains. Companies deployed application software on their own servers to serve customers. This was the overall foundation for American SaaS development. By the late 1970s, America's high-tech industry experienced a noticeable wave of growth.

Entering the modern internet era, American enterprises successively went through three stages: software going online, online going mobile (mobile development of software), and mobile going intelligent (big data and AI applications). American SaaS typically has a rich, complete foundation of enterprise service chains. Each industrial upgrade creates more application demand, driving multiplicative growth in the number of service chains, so numerous enterprise service opportunities usually emerge. Therefore, in the US, SaaS functions more like an efficiency tool for mature industries.

China's original internet business models, while appearing similar to America's, are actually quite different. Take Alibaba as an example. China's total retail sales began rapid growth in 2001, and the retail industry started booming. Taobao launched in 2003 — meaning Taobao and China's retail industry developed almost in sync.

Rather than being an industry efficiency tool or information transmission medium, platforms like Taobao more closely resemble the industry itself. Their division of labor, expansion, and efficiency upgrades all happen on the internet platform, not by maturing offline first and then migrating online. This may answer a question: why doesn't China have a Shopify? Because Shopify's service nature is helping merchants transfer their mature offline retail chains and customer resources online. In China, these chains and resources often formed during the period of online development and expansion.

Beyond retail, other industries' internet business models are similar. Take finance. American financial innovation was more based on migrating offline formats online and upgrading efficiency. But China's financial innovation, after going online, became part of the industry itself — such as mobile payment-driven internet finance.

Or take the restaurant industry. America's typical review platform is Yelp; its typical food delivery platform is DoorDash. The former follows the path of efficiently transferring offline restaurant formats online as an information medium. The latter follows the food delivery route. China's Meituan developed into a comprehensive platform with both reviews and food delivery, also building out industrial chains to support delivery operations. Citing The Paper, in 2021 China's online food delivery already accounted for 21.4% of restaurant consumption — more than one-fifth. This phenomenon shows that platforms like Meituan made themselves part of the restaurant industry.

From this perspective, whether in retail, finance, restaurants, or education, healthcare, and technology, internet involvement in China typically came quite early — often before formats had adequately competed — and became integrated. These platforms represent not just media efficiency but also became the business itself. And from initially being one part, they gradually developed into mainstream forces, even gaining the power to set industry rules.

Now when we look again at why Chinese SaaS, despite experiencing several "springs," still hasn't produced large-scale companies, it becomes easier to understand. Because for many industries, software-ization, online-ization, and mobile-intelligentization were typically compressed into a single cycle, with extremely high demands for competition and iteration. Because of these persistent high demands for competition and iteration, our enterprises' requirements for enterprise services are also generally more dynamic — currently still in a process of rapid growth and formation.

Case Studies of China's Unique Innovation Models

Finally, I'll add one more small topic. Earlier we discussed how China's entrepreneurship and innovation path is determined by industrial structure, capital markets, and industrial development paths. Today's investment path, whether in primary or secondary markets, needs to align more closely with China's economic structure itself and its structural adjustment. On this foundation, China will also produce many innovative models.

If we say America excels at innovation in information transmission media and models, China also has information media platform innovations like Bilibili and TikTok. How did such innovations emerge?

For example, ten years ago I participated in investing in Bilibili. At that time, quite a few teams were trying to build "China's YouTube." Of course, we later learned that Bilibili was the one that survived.

Why did Bilibili survive in the market rather than YouTube's Chinese disciples? Because in the process of localizing YouTube in China, an important condition was missing — the popularization of handheld home video cameras. Most people didn't have portable devices for shooting video (smartphones), let alone creating their own video content and uploading it.

Bilibili's strategy at the time was similar to online video sites like Youku and Tudou: it took already digitized anime films and video content as supply and put it on its own platform. However, unlike other content platforms, Bilibili added a layer of text information on top of this ready-made supply — bullet comments (danmu) — effectively creating new content supply simultaneously.

Text information collided with digitized information, producing information convergence. This is Bilibili's characteristic and culture. It thus gradually grew into a platform gathering ACG (anime, comics, games) subculture communities, and subsequently broke out to attract broader audiences.

So why did a product like Douyin later emerge in the domestic market, and successfully evolve into the internationally known product TikTok? The main reason is the widespread popularization of smartphones. Starting from Q2 2013, China became the world's largest smartphone consumer market, and after 2015, the market with the highest penetration rate.

High penetration brought an increasingly massive base of mobile video shooters, and round after round of rapid popular content iteration, which repeatedly trained the market and audience. So subsequently we had short video products like Kuaishou and Douyin. In short video production methods, we led a worldwide innovation trend, which is closely related to our rapidly developing smart mobile device industrial chain.

Whether Bilibili, or the later SaaS service provider Shangyue, or Douyin and TikTok, all are innovations combining China's distinctive industrial structure, capital market environment characteristics, and other features.

Overall, the fact that China's capital market or investment market size is beginning to approach its GDP is something worth celebrating in the venture capital circle. It means that investment will increasingly relate to our country's economic structure, becoming an important tool for China's economic development.

Additionally, when we say China and America's entrepreneurship and innovation paths are diverging, this doesn't express negativity toward either side. China's economic structure differs from America's. What we're doing today is investment aligned with China's current economic structural adjustment cycle. America also experienced similar economic structural adjustment cycles — like Silicon Valley, VC, and Nasdaq, which emerged successively some fifty or sixty years ago. America today may be at the tail end of a financial cycle, when large amounts of "from virtual to real" conceptual innovation or financial and asset category innovation may appear. This doesn't mean these innovations are unreasonable; although they may appear at the tail end of a bubble, they also represent typical cyclical phenomena.

From these perspectives, we can see that China's current entrepreneurship and investment path has, to some degree, embarked on a different road from America's. This is the result of the two countries' different industrial structures, different industrial development patterns, different capital market development conditions, and different financial cycle conditions at this point in time.

Reader Giveaway From your perspective, did Chinese and American capital markets experience a winter in 2022? Welcome to share your thoughts in the comments. The 6 most thoughtful commenters will receive a custom FreeS Fund edition of Trends 2030: Eight Megatrends That Will Shape the World. We look forward to finding certainty amid change and staying sharp together.

▲ Will 2022 Be a Capital Winter? | Li Feng Column

▲ Understanding the Birth of New Platforms in One Chart | Li Feng Column