Why Is "New Infrastructure" China's Most Consequential Stimulus Policy for the Next Decade? | Li Feng Column

Two Decades of Chinese Infrastructure: The Evolution of Stimulus Policy and the Industry Chain's Long March

This is the ninth article in our series exploring how COVID-19 is reshaping economic and industrial development. In previous pieces, we analyzed the core factors determining where global supply chains locate and relocate amid pandemic-driven globalization, with a focus on China — reviewing 40 years of structural transformation in Chinese industry and examining the opportunities and challenges facing Chinese supply chains.

Today, we turn to a new variable: "new infrastructure" (新型基础设施). Taking a longer view, we find that looking back at China's stimulus policies following the 1997 Asian Financial Crisis and the 2008 Global Financial Crisis helps answer how the current "new infrastructure" push will shape China's economic trajectory — and for how long.

In hindsight, the three rounds of stimulus China has enacted since 1997 were never isolated events. They nested within one another, gradually forming a larger, more sophisticated system.

After the 1997 Asian Financial Crisis, China used chemicals as industrial "infrastructure" to build out full-factor, full-chain manufacturing. After the 2008 Global Financial Crisis, the "4 trillion yuan" plan created high-speed rail and subway networks that accelerated the circulation of raw materials, products, and labor, making supply chains more efficient. "New infrastructure" now applies new infrastructure layers to these already-formed production and circulation networks, enabling better system-wide coordination and quality improvement. Once completed, China is projected to become the world's most efficient supply chain network.

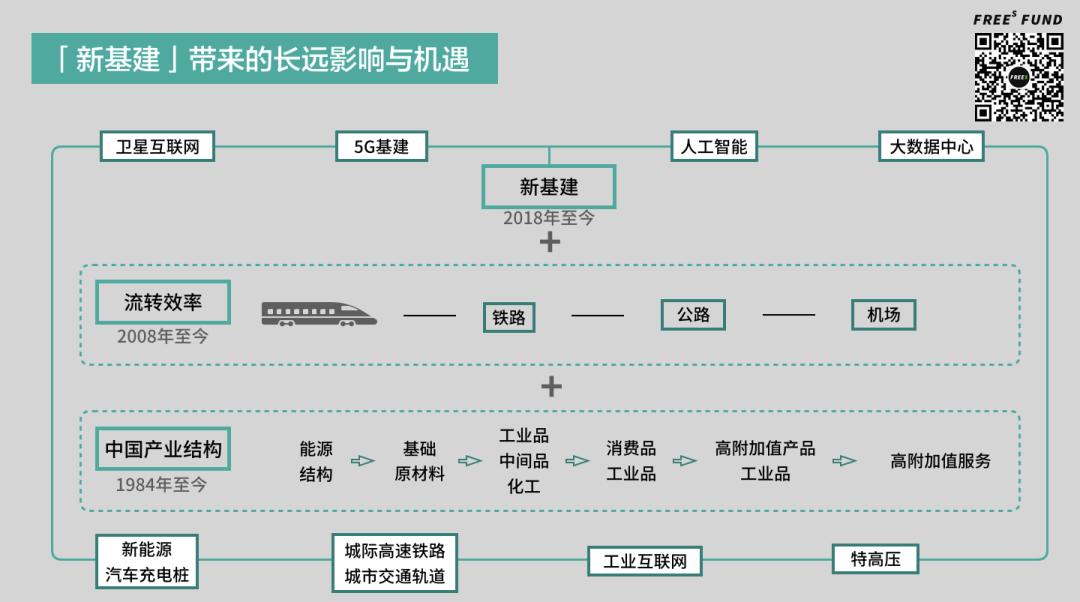

▲ Map any specific direction of new infrastructure to its corresponding link in the production or circulation chain, and that connection will likely represent a major opportunity over the next decade.

In this article, we explore:

- What major stimulus policies did China implement over the past 20-plus years before "new infrastructure," and how did they reshape industrial structure?

- What differentiated each round of stimulus, and what did they share in common?

- Why can "new infrastructure" form a coordination network that orchestrates the entire ecosystem of capacity, output, supply chains, and circulation efficiency? How will it affect China's manufacturing and technology development?

- How much economic activity can new infrastructure generate, and is that enough to meaningfully stimulate China's current economy?

- How will "new infrastructure" and "factor market reform" interact to "counter" supply chain relocation from China?

We hope this offers some useful perspective. Share your thoughts in the comments.

/ 01 /

In the decade after the 1997 Asian Financial Crisis,

full-factor, full-chain manufacturing began to take shape

▲ Source: China's Industrial Landscape: Li Feng's Hypothesis course, first released on Dedao app. Click "read more" for the full course. From 03:25 to 19:26, Li Feng discusses how China's three rounds of stimulus nested within each other to form a larger, more complete system.

After the Asian Financial Crisis, China built chemical industry infrastructure, raised industrial concentration, and spurred downstream sectors including textiles, apparel, automotive, and home appliances — creating full-factor, full-chain capabilities. Previously, China's industrial structure had been dominated by primary products.

Before becoming the world's top manufacturing country: primary products accounted for half of exports, and China was once a net oil exporter

In 2010, China's manufacturing value-added surpassed that of the United States for the first time, making it the world's largest manufacturing country. It has held that position ever since. But getting there was no overnight success.

Before developing complete supply chains, China exported large volumes of primary products. In 1985, primary products contributed nearly half of China's total exports; in 1990, they still accounted for one-quarter.

These primary product exports included substantial quantities of oil, coal, and other key inputs for manufacturing. According to the Karamay Yearbook (2010) edited by Chen Genfa: "In 1990, China had net crude oil exports of 21.06 million tons. In 1995, net crude oil exports were 1.74 million tons." China only became a net crude oil importer in 1996.

Because energy carried too little value-added and domestic economic construction increasingly needed energy as foundational support, the room for energy exports kept shrinking.

So, building on its energy industry, China began producing crude-processed goods like steel. In 1996, China's steel output broke through 100 million tons, reaching 101.24 million tons and making it the world's top steel producer. By 2005, China's steel output exceeded the combined total of the US, Russia, Japan, and South Korea.

Behind the "world's top steel producer" title lay accumulated burdens. At the time, China mainly exported low-end steel products with low value-added and high consumption of raw materials, water, energy, and transport capacity.

China used chemicals as a foundation to gradually build full-factor, full-chain manufacturing

In April 1994, the State Council issued the Outline of National Industrial Policy for the 1990s, calling for accelerated development of the petrochemical industry to make it a pillar of the national economy.

Three years later, the Asian Financial Crisis hit. South Korea, Singapore, Malaysia, and other regions with close trade ties to China were severely affected. Meanwhile, China faced domestic deflation and pressure to expand both foreign and domestic demand. To shield Chinese industry from the crisis's impact, China further liberalized foreign trade policy. Starting in 1999, all private enterprises could export independently.

Manufacturing firms' sales channels opened up, and the chemical and other basic industries they depended on developed further.

Moreover, before joining the WTO, to raise industrial concentration and strengthen international competitiveness, China strategically restructured state-owned enterprises, forming China National Petroleum Corporation and China Petrochemical Corporation in 1998. By end-2004, Sinopec's maximum single-set crude distillation capacity had increased to 10 million tons per year, making it Asia's largest refiner.

Using chemicals as a foundation, China gradually built full-factor, full-chain manufacturing.

Take the apparel supply chain: beyond natural materials like cotton, linen, and silk, fabrics like polyester, nylon, and acrylic are all chemical products. In 1998, China became the world's largest producer of synthetic fibers. By 2015, chemical fibers accounted for 84% of China's total textile fiber processing volume. In 2018, China's chemical fiber output reached 50.11 million tons, about 70% of global production.

As one of the three major chemical new materials, engineering plastics are mainly used in electronics/electrical and automotive applications. A September 2019 research report by China Fortune Land Development's industrial research institute noted: "In engineering plastics consumption, the electronics/electrical industry accounts for roughly 40%, automotive manufacturing about 10%." China has long since become the world's largest producer of electrical/electronic products and automobiles.

Beyond promoting other industries, the chemical sector itself moved toward finer specialization. According to a report by Minsheng Securities, in 2005 China's fine chemicals sales accounted for 11% of global sales; by 2010, this share had risen to 16%.

After decades of accumulation in chemicals and related industries, China not only holds the world's largest chemicals market share but also enormous capacity. Citing a September 2019 Xinhua report: "China's chemical industry capacity accounts for 40% of global capacity; by 2030, this ratio will approach 50%."

China's industrial policy choices have won broad recognition. At the 2019 G2 Extraordinary Forum, DigiTimes president Huang Qinyong discussed a survey he had seen in a Korean magazine: "Since 2000, none of the priority industries China has chosen have failed. Since 2003, in steel, petrochemicals, automotive, shipbuilding — every sector — China has had no failures."

Full-factor, full-chain manufacturing helped China "fight the pandemic"

During the pandemic, companies like Yanshan Petrochemical, BYD, and FreeS Fund portfolio company Yifei Automation were able to rapidly pivot to mask production. This reflected a structural advantage in Chinese manufacturing: China has capacity, labor, relatively advanced manufacturing capabilities, and raw materials — the ability to assemble these elements and produce epidemic prevention supplies at massive scale in a short time.

Citing a May 17 Xinhua report, from March 1 to May 16 China exported 50.9 billion masks, 216 million protective suits, 81.03 million pairs of goggles, 162 million COVID-19 test kits, and 72,700 ventilators.

Abroad, the absence of large-scale chemical industry foundations, efficient circulation systems, capacity, labor, and other systemic factors made it difficult to match China's rapid, large-scale production of epidemic supplies.

In March, the US government invoked the Defense Production Act to require Tesla, Ford, and General Electric to produce ventilators and other medical devices. Before producing its own ventilators, Tesla first purchased 1,225 ventilators from China to donate to California hospitals.

On March 21, Foreign Affairs published "How the Coronavirus Could Reshape the Global Order," noting: "China has manufactured the masks, respirators, and ventilators needed to respond to the crisis. The United States has only 1 percent of the required masks/respirators and 10 percent of the needed ventilators. The United States lacks the industrial capacity to meet its own needs, let alone provide aid as the crisis worsens."

Discussion

Q: Why shouldn't we worry too much about some supply chains relocating to Southeast and South Asia? And what does it mean that ASEAN has surpassed the EU as China's largest trading partner? Give us a "like" at the end of this article, and reply "Southeast Asia" in the WeChat official account backend for our preliminary answer.

/ 02 /

After the 2008 Global Financial Crisis,

China built efficient circulation networks centered on high-speed rail

Having developed relatively large, complete, and lengthy supply chains, China began in 2008 to "wrap" a circulation network around this solid industrial core, enabling more efficient interconnection across the supply chain and improving the movement of goods and people.

The "4 trillion yuan" plan, despite controversy, made countless long-term economic outcomes materialize

In 2008, the United States, at the epicenter of the financial crisis, rolled out measures including the "$700 billion Troubled Asset Relief Program" and the "$800 billion stimulus package," with the primary goal of injecting liquidity into America's financial and commercial systems.

That November, in response to the financial crisis, China's State Council introduced ten measures to expand domestic demand and stimulate economic growth. These included accelerating the construction of affordable housing; rural infrastructure; and major transportation infrastructure such as railways, highways, and airports. A State Council announcement stated: "Preliminary estimates indicate that implementing these projects will require approximately 4 trillion yuan in investment by the end of 2010."

More than a decade later, looking back at the "4 trillion yuan" plan, we can see the "long-termism" reflected in this stimulus policy.

At a time when China already possessed the world's largest manufacturing capacity, the "4 trillion yuan" plan yielded assets like high-speed rail and subways that improved circulation efficiency.

Consider China's investment in high-speed rail. Since the opening of the Beijing-Tianjin Intercity Railway in August 2008 — mainland China's first high-standard railway designed for 350 km/h operation — through December 2019, China has put 11 high-speed rail lines into operation, with total HSR mileage reaching 35,000 kilometers, firmly ranking first globally. China's railway transport volume also leads the world.

According to a World Bank report published in September 2019, the average cost of a 350 km/h dual-track high-speed rail line (including signaling, electrification, and facilities) is approximately 139 million yuan per kilometer; 250 km/h lines cost about 114 million yuan per kilometer; and 200 km/h lines run roughly 104 million yuan per kilometer. This means China's investment in high-speed rail over the past decade totals approximately 3.6 to 4.8 trillion yuan.

China's investment in subways is equally staggering. From 2009 to the end of 2019, China's total subway mileage grew from 835 kilometers to 5,187 kilometers — an increase of 4,352 kilometers over 11 years. According to Science and Technology Daily, by 2013 China's urban rail transit mileage already ranked first in the world.

Wang Mengshu, a Chinese Academy of Engineering academician and tunneling and underground engineering expert who participated in the construction of China's first subway, explained in a 2011 interview with China.org.cn: "In China, subway construction costs approximately 500 million yuan per kilometer." Based on this estimate, China's investment in subways over the past decade totals roughly 2.2 trillion yuan.

Although the "4 trillion yuan" plan faced considerable controversy after its launch, in retrospect it enabled countless long-term economic outcomes to materialize.

On one hand, infrastructure like high-speed rail directly stimulated travel demand, giving rise to highly profitable enterprises such as the Beijing-Shanghai High-Speed Railway, with a market capitalization exceeding 300 billion yuan. According to a Xinhua report from July 2019, the Beijing-Shanghai High-Speed Railway had cumulatively transported 1.03 billion passengers in its eight years of operation.

On the other hand, high-speed rail dramatically improved the efficiency of China's economic circulation — both the movement of people and goods.

In urban clusters like the Pearl River Delta and Yangtze River Delta, different cities have distinct industrial structures: some focus on core R&D, others specialize in small-scale supporting production, while others concentrate on large-scale, single-unit supporting production. High-speed rail connects these upstream and downstream industries into an integrated network, reducing circulation costs and improving overall efficiency.

During the pandemic, because cities in Jiangsu Province had relatively balanced and comparable levels of development, each city operated fairly independently in supporting epidemic-affected areas — earning the nickname "modular Jiangsu" from netizens. High-speed rail happened to be a key enabler of this "modular Jiangsu." The province's manufacturing chains are long enough, and high-speed rail connects all the cities along the route with high speed and low cost, dramatically improving their circulation efficiency.

By the end of 2019, the combined high-speed and rapid rail mileage of Jiangsu, Zhejiang, and Shanghai exceeded 2,800 kilometers — more than 1,000 kilometers beyond Guangxi's 1,751 kilometers, which had the longest HSR operating mileage in 2018.

During the pandemic, freight transport within Jiangsu Province, as well as goods moving between Jiangsu and Shanghai, Hangzhou, and other locations, never stopped. According to a China News Service report from April 1: "Since March, Jiangsu has maintained frequent goods movement both within the province and with Shanghai, Hangzhou, and other areas, with logistics between Jiangsu and Shanghai being particularly tight. The total import and export volume of goods between the two places ranked first among all of Jiangsu's trading partner cities, reaching 8.8% and 10.6% respectively."

Compared to other countries globally, does China's circulation efficiency have sufficient competitiveness?

China has notable advantages in logistics costs and infrastructure. Citing an article by Wang Yangong of the Ministry of Transport: "In 2011, U.S. logistics costs, transport costs, and highway transport costs were 1.62 times, 1.95 times, and 1.79 times those of China respectively."

However, China's comprehensive circulation efficiency still has room for improvement. According to the World Bank's "Logistics Performance Index: Overall Score" (on a scale of 1-5, where 1 is worst and 5 is best), China ranked 35th globally in 2007 with a score of 3.32. By 2018, it had risen to 28th place with a score of 3.61.

As China gradually became the world's factory, and as it improved the physical circulation efficiency of people and goods through networks like high-speed rail and subways, the next challenge to address became "structural adjustment."

/ 03 /

After COVID-19, Accelerating "New Infrastructure"

▲ "New infrastructure" can function like a dispatch system, directing supply and demand, production, transportation, and other links.

After the COVID-19 outbreak, China intensified its commitment and investment in "new infrastructure."

On April 20, the National Development and Reform Commission defined "new infrastructure" as encompassing three areas: information infrastructure, converged infrastructure, and innovative infrastructure. This covers 5G, IoT, industrial internet, satellite internet, artificial intelligence, cloud computing, data centers, intelligent computing centers, intelligent transportation infrastructure, and smart energy infrastructure.

Once China has formed a complete industrial chain and possesses an efficient circulation network, "new infrastructure" can better perform system-wide dispatch on this foundation, guiding production, delivery, and consumption according to supply-demand relationships — making existing production factors and circulation networks more efficient. Additionally, "new infrastructure" will drive technological development in related fields.

▍How does "new infrastructure" allocate resources globally and mobilize supply-demand relationships and energy?

Take the energy industry as an example.

In recent years, China's pressure regarding crude oil has grown daily. In 2017, China surpassed the United States and Japan to become the world's largest crude oil importer. Moreover, China's crude oil imports continue to grow, rising from 420 million tons in 2017 to 506 million tons in 2019.

Gasoline is one of the main products of petroleum refining, with a yield rate of approximately 25% of crude oil. This means one ton of crude oil produces 0.25 tons of gasoline. By this calculation, refining all of today's imported crude oil into gasoline would yield just over 100 million tons of gasoline — roughly equal to or slightly exceeding our current gasoline consumption. According to a report from the China Petroleum and Chemical Industry Federation, China's apparent gasoline consumption (annual production plus net imports) in 2019 was approximately 125 million tons.

While facing challenges in energy structure, China still has considerable room for growth in automobile consumption. In 2019, China's vehicle ownership exceeded 260 million, with 173 vehicles per 1,000 people. If in the coming years China's vehicle ownership per 1,000 people quadruples to approach Japan's level (591 vehicles per 1,000 people), the gap in China's gasoline production would be enormous.

This partly explains why the rollout and promotion of new energy vehicles has received encouragement.

At this point, we can also understand the significance of including "ultra-high voltage" (UHV) — a direction that seems distant from most people's daily lives — in new infrastructure.

UHV refers to power transmission technology with AC voltage levels of 1,000 kV and above, and DC voltage levels of ±800 kV and above. It offers advantages including long transmission distances, large capacity, low losses, and high efficiency.

Li Lichuan, a Chinese Academy of Engineering academician who organized the construction of the world's first ±800 kV DC transmission project, stated in a 2018 interview with Economic Information Daily: "The UHV ±800 kV DC transmission project has 2-3 times the transmission capacity of ±500 kV DC projects, with economical transmission distance increased by 2-2.5 times, operational reliability improved by 8 times, per-unit transmission distance losses reduced by 45%, per-unit capacity line corridor land use decreased by 30%, and per-unit capacity construction cost reduced by 28%."

Next, let's compare the efficiency differences between UHV and traditional gasoline resource dispatch through two scenarios.

The gasoline consumption cycle follows this path: due to insufficient domestic production capacity, we mainly import crude oil from abroad, transport it to various ports, refine it into gasoline nearby, then distribute it to gas stations within a certain range for sale to gasoline-powered vehicles.

If we develop new energy vehicles and use UHV for power transmission, the entire process changes fundamentally. Whether from wind, hydro, or solar power, once electricity is generated and the generation process is digitized, UHV can then transmit it to various charging stations — with high efficiency and low losses.

Furthermore, with the development of "new infrastructure" such as IoT, cloud computing, AI, and industrial internet, all information related to supply-demand and production conditions can be aggregated. The "overall supply-demand relationship" within industrial chains can then be mapped out — including who produces what, how much, and where it should go. As a result, "new infrastructure" can function like a dispatch system, directing supply and demand, production, transportation, and other links.

Specifically in the new energy vehicle market, UHV changes the form of energy, making power supply and delivery more intelligent. Meanwhile, IoT and data-related "new infrastructure" makes it possible to monitor electricity consumption in different regions at different times in real time and allocate supply according to demand. In the long term, it can also address the imbalance between energy demand and distribution, and promote the development of the new energy vehicle industry.

▍How will "new infrastructure" drive the development of key technologies?

Having explored new infrastructure's system-wide dispatch capabilities, let's examine how it drives the development of key technologies.

Based on the experience of the previous two rounds of infrastructure development, although these large infrastructure investments were controversial at the time, in retrospect their timing played a significant role in enabling the next wave or the following decade of growth. From the results, once infrastructure is built, technologies and applications related to it — and urgently needed for economic development — become easier to integrate into industrial chains.

When we developed the chemical industry in the 1990s, we may not have fully anticipated the vigorous growth of fine chemicals, or the driving effect of China's chemical industry on electronics, electrical appliances, and the automotive sector.

Before China accelerated construction of high-speed rail, subways, and other infrastructure in 2008, there may not have been such large-scale intercity transportation demand. But once high-speed rail and similar infrastructure were built, people gradually grew accustomed to and dependent on this mode of transport. Once it carried enough goods and people, the economies of scale of the high-speed rail network became apparent. The takeoff of high-speed rail in China also drove advances in high-voltage power lines and rail transit technology.

New infrastructure may similarly influence the development of related and critical technologies. Take 5G as an example — it's easy to imagine that all technologies and applications connected to 5G will see substantial growth.

On the application side, we've seen 5G communications and related technologies drive widespread adoption of live streaming, video conferencing, traffic operations monitoring, agricultural IoT, and more. Behind this application growth comes massive data expansion, which in turn fuels development in artificial intelligence, cloud computing, and data centers.

On the technology side, 5G base stations require baseband chips, FPGA chips, and optical communication chips — so 5G's expansion will generate significant new demand for the semiconductor industry.

Here's another example. As 5G base station construction accelerates, the energy storage battery industry is also getting a boost.

According to Ministry of Industry and Information Technology data, as of end-March 2020, China had built 198,000 5G base stations nationwide. Driven by the new infrastructure wave, the three major carriers planned to build 500,000 5G base stations in 2020.

To ensure stable operation of 5G communications equipment, macro base stations typically maintain 3-4 hours of reserve power. As China Energy News reported: "Compared with 4G base stations, 5G base stations have roughly doubled energy consumption, and with their trend toward miniaturization and lightweight design, they require energy storage systems with higher energy density and demand upgraded power systems."

Going forward, base station construction's demand for energy storage batteries could exceed that of new energy vehicles for power batteries. According to GGII data, China's power battery shipments reached 71 GWh in 2019, up 9.4% year-on-year, while energy storage lithium battery shipments hit 3.8 GWh, up 26.7%. Orient Securities estimates total 5G base station demand for energy storage batteries at 161 GWh, with 14.4 GWh of new demand in 2020 alone.

This demand for base station energy storage will benefit many companies, including QingTao Development, a solid-state lithium battery R&D manufacturer backed by FreeS Fund. QingTao built China's first solid-state lithium battery production line in 2018 and has since become the first domestic company to achieve mass production of solid-state lithium batteries.

▍ How much economic activity can new infrastructure drive, and is this volume sufficient to provide meaningful stimulus to China's current economy?

As we discussed earlier, new infrastructure can make existing industrial chains and circulation networks more efficient.

So drawing a line from any specific direction of new infrastructure to the relevant links in industrial chains or circulation channels — that connection will likely represent a major opportunity over the next decade.

Beyond the ultra-high voltage + new energy vehicle example we mentioned, big data + healthcare, AI + finance, AI + logistics... wherever new infrastructure connects with a sufficiently large segment of the industrial structure, enormous innovation opportunities lie in wait.

So how much economic activity can new infrastructure actually drive? And can this volume provide adequate stimulus to China's current economy?

The economic activity generated by new infrastructure falls into two main categories: first, the investment scale directly stimulated by new infrastructure; second, the economic value created by efficiency gains in industrial chains or circulation channels.

Let's start with the investment scale.

In its "New Infrastructure" Development White Paper published this March, the China Center for Information Industry Development estimated that by 2025, direct new infrastructure investment will reach approximately 10 trillion yuan, with cumulative induced investment exceeding 17 trillion yuan — equivalent to 10% to 17% of China's 2019 GDP (99.08 trillion yuan).

On March 27, Beijing News surveyed investment plans across 26 provinces totaling 50 trillion yuan, finding "new infrastructure" had become a hotspot for major cities. Just six provinces and direct-controlled municipalities — Guangdong, Beijing, Henan, Jiangxi, Shanghai, and Jiangsu — had 444 "new infrastructure" related projects, accounting for 13.7% of their announced project totals. Shanghai led with 50 "new infrastructure" projects representing 32.9% of its total; Jiangsu had 63 such projects at 26.2% of its total.

Now for the economic value from efficiency gains in industrial chains.

Take 5G alone. Back in 2018, Wei Leiping, then executive deputy director of the Ministry of Industry and Information Technology's Communications Science and Technology Committee, noted in a speech that the 11 industries most benefiting from the 5G era would include infrastructure, agriculture, finance, retail, public safety, utilities, transportation, media and gaming/health, manufacturing, and automotive — with 5G driving industrial output on the order of 4 trillion yuan.

We can also examine the economic effect if Tesla's Model 3 achieved 100% domestic production in China.

According to a research report from Guolian Securities, Model 3's domestic suppliers are concentrated in body, chassis, and interior/exterior trim — roughly 20% of total cost — while the "three electrics" (battery, electric drive, electric control) and automotive electronics account for 50% and 30% respectively.

Currently, the three Model 3 variants on Tesla's official site average about 345,000 yuan. With Tesla's Q1 2020 automotive gross margin at 25.5%, we can roughly estimate per-vehicle cost at about 257,000 yuan. Tesla's Shanghai Gigafactory has an estimated annual capacity of 200,000 Model 3s, putting annual production costs at approximately 44.7 billion yuan (257,000 yuan per vehicle × 200,000 vehicles).

If Model 3 were completely domesticized, core components representing the bulk of costs — AI chips, motors, motor controllers, battery management systems — would all be produced in China. This would raise the share of Chinese-produced components from roughly 20% to 100% of total cost. The result: Model 3 production would generate approximately 35.76 billion yuan in additional annual economic effect for China (44.7 billion yuan × the 80 percentage point increase).

That's over 30 billion yuan from just one Model 3 production line. Undoubtedly, as new infrastructure acts on more links in industrial chains, the output potential expands enormously.

Taking all this together, once new infrastructure is completed, China is projected to become the world's most efficient supply chain network. China already has the world's largest and most complete supply chain, is poised to become the world's largest single consumer market, and has low-cost, efficient logistics networks. Add globally efficient coordination of circulation networks and industrial chain links, and other countries will struggle to match this combination of advantages.

/ 04 /

How will new infrastructure affect the relocation of China's industrial chains?

▲ Source: China's Industrial Landscape: Li Feng's Hypothesis course, first published on Dedao APP. Click "Read More" for the full course. From 00:00 to 12:14, Li Feng discusses how new infrastructure and factor market reforms interact to help industrial chains upgrade and transform. From 12:14 to 13:47, Li Feng discusses the long-term impacts of new infrastructure.

Some relocation of China's industrial chains to Southeast Asia and similar regions is inevitable, particularly for manufacturing with somewhat lower value-added. In our view, new infrastructure will affect this outward migration in two ways:

First, by empowering industrial chains to increase their value-added, retaining higher value-added industries and their upstream/downstream suppliers;

Second, by interacting with the "factor of production" document (Opinions on Building a More Complete System for Market-based Allocation of Factors of Production) to reallocate production factors freed up by outward migration toward higher value-added domestic industries.

As we noted in "One Chart to Understand Changes and Opportunities in China's Industrial Chain": China's industrial structure is climbing toward higher value-added segments, and developing high value-added consumer/industrial goods alongside high value-added services is the top priority now and going forward.

"New infrastructure" will act on China's existing industrial chains, drive critical technology development, and elevate industrial value-added. To use an analogy: industrial chains provide the soil for new infrastructure to take root, while new infrastructure serves as the shelterbelt preventing that soil from eroding.

Returning to our earlier example, 5G-related technology development will drive China's chip industry forward — a long-term positive for Huawei, which faces US sanctions and constraints in core RF chips. And precisely because Huawei remains, enough key mobile phone component processors stay in China rather than being relocated abroad.

Moreover, the interaction between new infrastructure and factor market reforms will reallocate freed-up production factors to high value-added industries, achieving industrial chain upgrades.

On April 9, the CPC Central Committee and State Council issued the "factor of production document," proposing reforms to advance market-based allocation of land, guide rational and orderly flow of labor, and promote market-based allocation of capital.

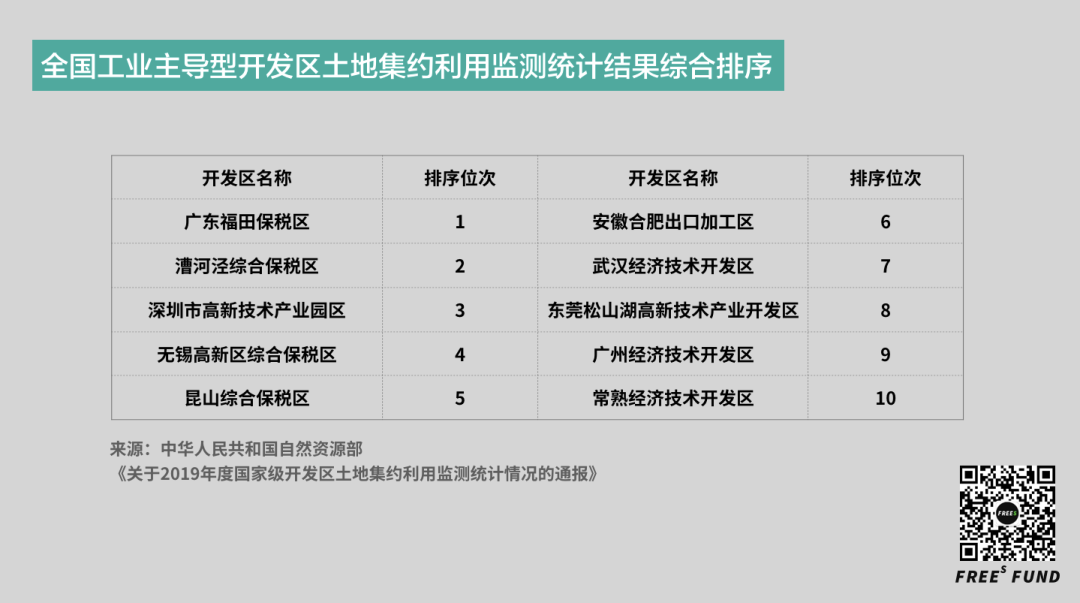

As shown below, the government monitors and publicly reports on intensive land use, with a value assessment system including metrics such as industrial land GDP per unit area and tax revenue per unit area, to guide and drive regional economic and social development and advance industrial restructuring.

▲ On January 8, 2020, the Ministry of Natural Resources released its 2019 report on intensive land use monitoring in national-level development zones.

When lower value-added industries relocate abroad, the vacated industrial land will likely be used by local governments to attract higher value-added or more technology-intensive manufacturers — for example, companies focused on IoT, industrial internet, satellite internet, AI, and cloud computing connected to "new infrastructure." Indeed, on the same piece of land, on the same production line, workers producing higher-tech automobiles versus somewhat lower-tech industrial intermediate goods generate different value-added. And manufacturing workers previously trained in basic industrial skills can be retrained to meet the demands of higher value-added industrial and end-product manufacturing.

Of course, this tests local governments' governance capacity and wisdom — what preferential policies, financial support, and land resources they can deploy to mobilize existing production factors (land, people, capacity, data, capital, etc.) for more efficient reallocation, and to attract and aggregate more excellent factors and resources to improve quality and efficiency, helping local industrial structures upgrade in value.

Summary

1 Looking back, stimulus policies China has issued over the past two decades may have faced considerable controversy initially, but ultimately played major roles in driving subsequent economic growth. What seemed "ahead of its time" at first may, in retrospect, have been well-timed.

2 These stimulus policies have been layered and iterative over time. After the 1997 Asian financial crisis, China built out chemicals as industrial "infrastructure," creating full-factor, full-chain manufacturing that would, more than two decades later, help China fight the pandemic. After the 2008 global financial crisis, the "4 trillion yuan" stimulus ultimately produced physical infrastructure like high-speed rail and subways that supported the real economy and improved scheduling and circulation efficiency across manufacturing supply chains. "New infrastructure," by contrast, can allocate, coordinate, and circulate across entire networks and every link in industrial chains.

3 On one hand, "new infrastructure" can form coordination networks that orchestrate the entire ecosystem of capacity, output, supply chains, and circulation efficiency — more efficiently matching supply and demand and allocating production factors, thereby raising the efficiency of existing supply chains and circulation networks. On the other hand, "new infrastructure" will drive technological development in related fields.

4 By stimulating investment and helping supply chains and distribution channels become more efficient, "new infrastructure" will likely generate stimulus on the order of tens of trillions of yuan for China's economy in the years ahead. Once completed, it is expected to make China the world's most efficient supply chain network — an advantage that other countries will find difficult to match.

Food for Thought

Q: Why shouldn't we worry too much about some industrial chains relocating to Southeast and South Asia? And what does it mean that ASEAN has surpassed the EU as China's largest trading partner? Give this article a "Like" and reply "Southeast Asia" in the WeChat official account backend for our preliminary answers.

(You're welcome to read, share, and like this article. For reprint permission, please reply "Reprint" to learn the rules and contact Feng Xiaorui [ID: freesfund] for authorization. Copyright belongs to FreeS Fund.)

One Chart to Understand Changes and Opportunities in China's Industrial Chain | Li Feng Column Where Is E-Commerce Livestreaming Headed? | Frees Fund From the Rise to the Calm: Is E-Commerce Livestreaming a Feature or a Business Model? (Part 1) | Frees Fund What Did Minister Miao Wei Actually Say About Chinese Manufacturing? | Frees Fund One Chart to Understand Globalization or Deglobalization | Li Feng Column After the Pandemic, a New Era for "Good Companies" | Frees Fund