Why We're Bullish on Virtual Idols | Frees Fund

A Brief History of Virtual Idols in Japan, and Their Future in China.

(Peter, Vice President at FreeS Fund. Email: chenzhe@freesvc.com. You can also reach him through FreeS Fund's WeChat contact, ID: freesfund. Swipe for more 👉)

Virtual idols have been around in China for years. In 2020, the pandemic-driven surge in livestreaming converged with virtual idol technology, turning virtual idols into a genuine inflection point. What started as a niche within ACG circles rapidly broadened, pushing into far wider audiences. Tencent, ByteDance, iQIYI, Bilibili — major players all piled in. Infinite Kings, QQ Dance, RiCH BOOM — virtual idol IPs and labels kept multiplying.

According to data from vtbs.moe, a platform tracking virtual streamer metrics, subscription and tipping revenue for virtual idols on Bilibili grew 350% year-over-year.

The capital markets have been active too. Recent months have seen multiple funding rounds in the space. Magic Technology closed a Series B exceeding 100 million RMB, providing technical infrastructure and MCN operations for virtual streamers. Wanxiang Culture, a virtual idol technology service provider, and Yishiyi, a virtual idol IP incubator, also raised funding of various sizes.

More intriguingly, the live e-commerce wave has swept up virtual streamers too. Luo Tianyi debuted on Taobao Live. Yichen the Little Monk, Momo Jiang, I'm Not a Glutton — more and more virtual streamers are testing the waters of live commerce. The advantages are compelling: always-on availability, controllable risk, low marginal costs. These factors are accelerating market growth.

Meanwhile, quiet transformations in underlying technology are opening new possibilities from the supply side.

Beneath all this excitement, how do you actually seize the massive opportunity in virtual idols? On May 28, Sansheng hosted an offline salon titled "Virtual Idols: Reality and Outlook." Peter, Vice President at FreeS Fund, gave a presentation exploring the evolution, business models, emerging shifts, and challenges facing virtual idols.

Before diving in, three preliminary takeaways:

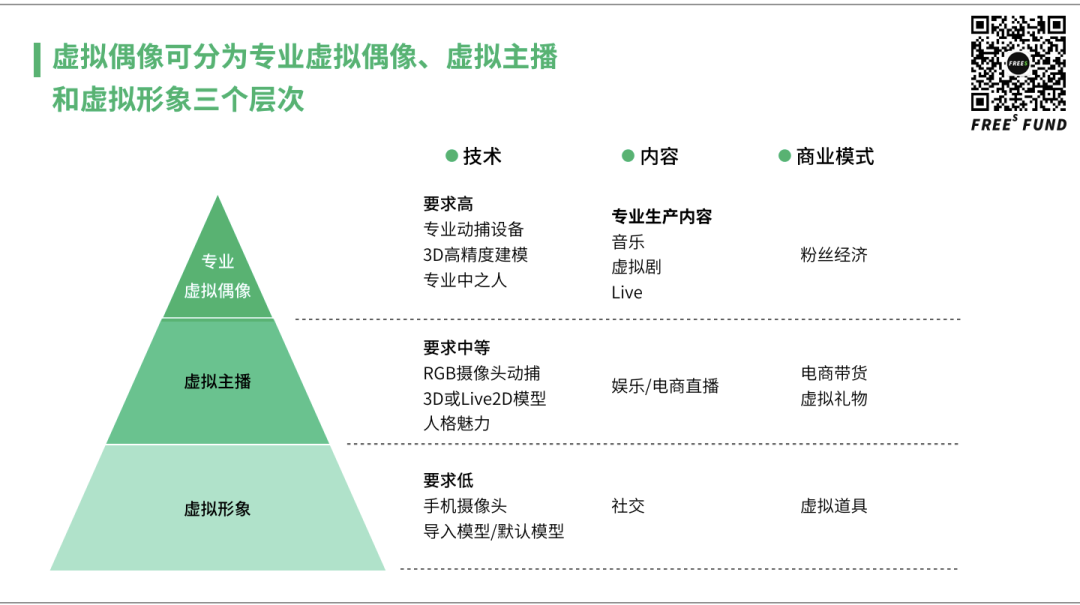

- Virtual idols can be divided into three tiers. At the top are exemplars like Hatsune Miku and Luo Tianyi, built with industry-leading technology to deliver the best audiovisual experience. The second tier comprises virtual streamers, monetizing through e-commerce and virtual gift tipping. The third tier is social networking based on virtual avatars. We believe that following this trajectory of technological and content development, a social platform built around virtual avatars will very likely emerge.

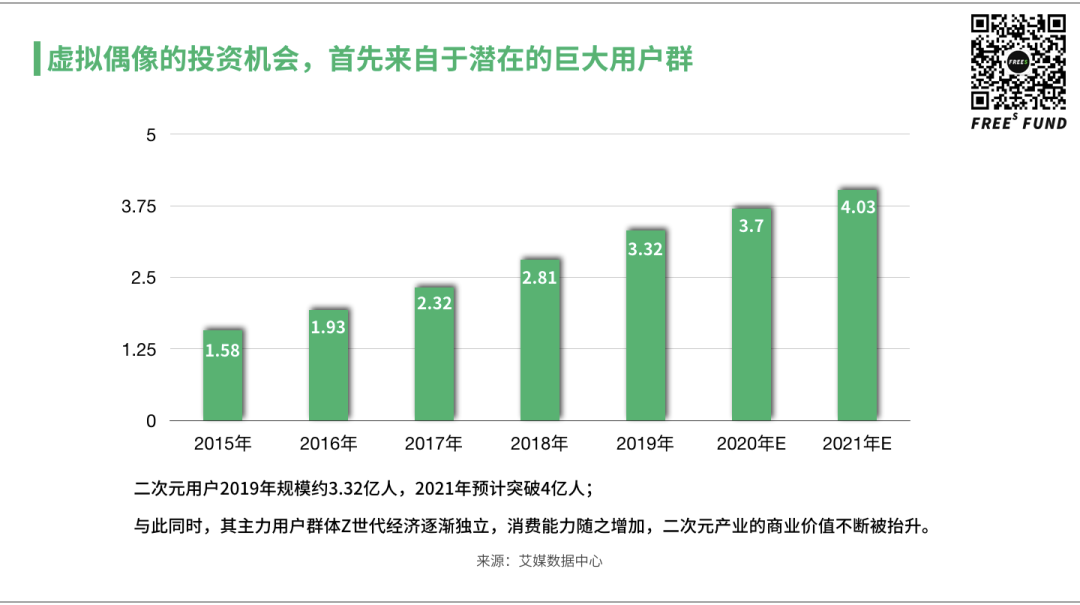

- The virtual idol market is large enough, because the audience skews younger with higher interest and enthusiasm for new things. Compared to human idols, virtual idols have irreplaceable advantages in lifecycle length, controllability, and interactivity. At the level of fundamental user needs, virtual idols serve the need for companionship and belonging exceptionally well.

- We are at an inflection point of technological transformation. For virtual idols, appropriately priced technical solutions will emerge for each tier, increasing content supply.

Before joining FreeS Fund, Peter worked at NetEase Games' overseas division and ByteDance's strategic investment department. He has long focused on investment opportunities in entertainment and culture. His email is chenzhe@freesvc.com, and you can also reach him through FreeS Fund's WeChat contact (ID: freesfund).

Below is Peter's presentation, which we hope offers fresh perspective.

Peter, Vice President at FreeS Fund: Virtual Idols in China — A Major Opportunity at the Intersection of New Technology and New Content

Source: Sansheng

Author: Sansheng Editorial Team

/ 01 / Three Tiers of Virtual Idols and Their Evolution

Virtual idols can be divided into three tiers.

At the top, following the first-generation apex virtual idols represented by Hatsune Miku and Luo Tianyi, second-generation virtual idols incorporate more advanced technology. These include motion capture and 3D modeling — necessarily industry-leading, since the core goal is delivering the best possible audiovisual experience. Beyond the high technical demands, the voice actors behind the avatars (known as "nakano-hito" or "the person inside"), and the derivative content built around the virtual idol — music, virtual dramas, live performances — must all be produced with top-tier technology. The business model ultimately resembles that of traditional idol economies, monetizing through fan spending.

The second tier, more numerous and the fastest-growing part of today's market, consists of virtual streamers. Technical requirements are relatively lower here. Product and content manifestations center on entertainment and e-commerce livestreaming. Revenue models are primarily e-commerce sales and virtual gift tipping.

The third tier — we believe, following this trajectory of technological and content development, a social platform built around virtual avatars will very likely emerge.

A brief history of virtual idols.

In Japan's Showa era, the earliest form: figures appeared on television as real people, but these real people were actually personas engineered around the aggregate preferences of target audiences. The crafted image would never date, never marry, never be embroiled in scandal — a perfect princess or prince fulfilling audience fantasies.

By the Heisei era, idols emphasized documentary realism or participatory engagement. No longer merely perfect constructs from talent agencies, they became co-created with fan involvement. One example: Japanese entertainer Ijuuin Hikaru, on his radio program, collaborated with listeners to build a virtual character through language and collective imagination.

Not until 2007, with advances in digital technology, did the virtual idols we now recognize emerge — Yamaha's Hatsune Miku. Later came VTubers (Virtual YouTubers; the term refers to virtual idols who stream and upload videos on YouTube, also called virtual streamers on other platforms).

We've observed that top-tier virtual idols modeled after human idols — like Hatsune Miku — haven't actually proliferated that quickly, because content costs are high and risks substantial. But VTubers, combining newer business models with lower production barriers, have grown explosively. By end of 2019, Japan had nearly 10,000 VTubers. This likely reflects Japan's strong ACG cultural foundation, with the market adapting to this model very rapidly.

By 2019, Japan's virtual idol industry chain had reached considerable scale — production, marketing, monetization, even media coverage and investment. The ecosystem was quite mature.

This maturity showed up in capital markets through numerous funding events. Japan's VC industry isn't particularly developed, given relatively weak entrepreneurial drive among Japanese. For a vertical sector like virtual idols to attract so many investment cases is quite remarkable.

But like all entertainment subsectors, virtual idols ultimately consolidate toward the top. Among content providers (CPs), only six companies managed to launch over 50 virtual idols. The three largest: Nijisanji, COVER, and Activ8 (which operates Kizuna AI).

Let me introduce the two most prominent: COVER and Nijisanji. Both operate in China, both focus on VTubers, but their models differ significantly. COVER pursues a premium IP route — every VTuber launch is carefully planned to ensure quality.

Nijisanji's model resembles AKB48 — cast a wide net, recruit all kinds of VTubers, then create an ecosystem through their interactions. Like the CP-baiting that fan circles love, this builds an atmosphere that keeps users within the ecosystem, with fans following relationship threads from one VTuber to the next. In Japan there's a well-known term, "hako-oshi" (box-pushing) — selling you the whole roster, betting you'll find at least one you like.

Both companies have succeeded. COVER built a closed loop covering production and distribution, with sufficiently high content quality. They developed proprietary underlying technology called Hololive. Using this tech, they segment their label by target demographics. Initially focused on the female market, they expanded into male groups and music units as that market saturated, ensuring broad audience coverage. On this foundation, they launched user-facing apps encouraging fan-created derivative works, further amplifying VTuber reach.

With this business model established, they turned to overseas expansion — establishing Hololive China and Hololive India, and launching China operations through partnership with Bilibili.

Most top UP hosts on Bilibili today are actually exports from Hololive. Their development follows the steady, methodical approach VCs prefer. Their funding history reflects this — four rounds from 2017 to 2020, with the latest bringing in strategic investors like Hakuhodo.

Nijisanji's promotion model boils down to three pillars: wide recruitment, CP-baiting, and ecosystem-building.

Founded May 2017, Nijisanji has now operated 141 VTubers, with 99 in the Japanese domestic market. They took some detours along the way. The company was founded by a Japanese university student with no resources or background. Unable to push many VTubers at launch, he recruited a batch and let them run free, seeing who would break out.

Early content quality wasn't particularly high. What to do? They suddenly discovered one tactic worked especially well: having VTubers ship with each other, drawing fans into discussion and analysis of these relationships.

But this approach wasn't sustained. Once the company had money, they tried to emulate COVER. They categorized second-generation and subsequent VTubers into three labels — gaming, female-oriented, and another — grouping VTubers for cross-promotion between groups.

Within two years, they'd essentially killed what originally made them successful — VTuber collaboration and joint content — and found the results disappointing.

So at end of 2018, they reverted to dispersing all VTubers into 2-4 person groups, forming combinations and CP relationships based on debut timing and character settings. These CP relationships ultimately became products.

Meanwhile, intra-group CP dynamics combined with inter-group collaborations. Beyond cross-promotion, they used games like Minecraft for scenario-based interaction. They embedded VTuber avatars into Minecraft, letting users watch their gameplay live. This was powerful — essentially turning VTuber relationships into content. Audiences ate it up, and Nijisanji's scale grew very rapidly, with cumulative funding exceeding COVER's.

Japanese ACG users tend to be relatively loyal, so top content in Japan enjoys very long lifecycles. We can see top VTubers remaining on the charts for over two years.

Newer VTubers can only capture incremental traffic. This incremental flow isn't enough to feed all the new entrants, so many of those 10,000-plus VTubers actually lose money. But China's circumstances differ considerably from Japan's — including potential market size and how quickly users tire of things — so the market may accommodate more VTubers.

Discussion

Q: Is live commerce the path forward for virtual idols in China? Tap "Like" at the end of this article, and reply "虚拟偶像" in the WeChat official account backend for our preliminary answer.

02 Business Models in Japan's Virtual Idol Sector

Let me introduce the overall business model of Japan's virtual idol sector, since the industry there is relatively mature. Livestreaming, live performances, merchandise tied to performances — business models validated by traditional idols — all perform reasonably well. Advertising revenue, by contrast, has been somewhat underwhelming.

Even top VTuber Kizuna AI earns only about 1 million RMB annually in advertising, against 433 million views. Live tipping revenue clearly exceeds advertising. This indicates that livestreaming generates substantial revenue in Japan.

A recent shift: platform migration. As TikTok's penetration in Japan has increased, VTubers have gradually moved there. TikTok has been welcoming to them — its distribution logic and entertainment positioning suit virtual idol promotion well. Kizuna AI has roughly 2.6 million YouTube followers; on TikTok, after limited effort, she's approaching 1 million.

So Japan's virtual idol sector is developing rapidly with mature business models, but faces several challenges:

The core challenge is high investment costs. This is difficult to solve in Japan, where the content industry's professionalism and division of labor are extremely refined, making rapid cost reduction hard. Quality requirements, combined with overheating in recent years that drew too many competitors chasing content resources, have ultimately driven costs up.

A typical Japanese virtual idol requires upfront investment approaching 10 million RMB, with cultivation cycles exceeding six months. The entire process carries enormous uncertainty. So most virtual idols struggle — annual tips often can't sustain one virtual idol. Kizuna AI's parent company, for instance, reported heavy losses in its Q3 earnings last year.

03 New Shifts in the Virtual Idol Market

Japan's virtual idol landscape may not look that optimistic, but we've identified recent changes that offer fresh hope — especially when combined with China's specific market conditions, where significant opportunity lies.

First, we are at a technological inflection point. The two core technologies — motion capture and modeling. Traditional mocap uses optical or inertial systems, extremely expensive at several hundred thousand to millions of RMB per setup, plus requiring large studio space for optical capture. These costs are prohibitive for most startups, even unaffordable.

But with companies like Apple entering the field, using AI algorithms, future mocap may eventually be achievable through ordinary smartphone cameras. That endpoint remains somewhat distant, but affordable solutions already exist that let VTubers achieve motion capture at very reasonable prices.

So we anticipate appropriately priced technical solutions for each of virtual idols' three tiers, increasing content supply. For virtual streamers, mocap costs will drop significantly while quality improves through algorithm and data accumulation. Ultimately, toward virtual social networking, perhaps just a smartphone will suffice.

Beyond technological transformation, let's examine China's current situation.

China's virtual idols trace back to 2011's Dongfang Zhizi on Tianjin TV (a virtual singer created by Tianjin Television Station, debuting at the "First China Culture and Art Animation Awards Ceremony"). Subsequent years saw sporadic new virtual idols, with Tencent, NetEase, Giant, Bilibili, Happy Elements, and iQIYI all launching offerings.

But across China, virtual idols remain in an embryonic stage.

We judge this on two dimensions: First, no localized virtual idols have yet emerged. On Bilibili, for example, among the top 15 virtual idols, 9 are from Japan. In scale, Bilibili VUPs (virtual UP hosts) number perhaps around 1,000 — compared to Japan's roughly 10,000, China remains very early.

From an industry chain perspective, many companies have entered the market, but CPs remain scarce. Despite major players joining, teams that can actually execute well will likely still be startups.

Technologically, the emphasis is on lowering barriers. This segment emerged earliest — companies like Chaociyuan and Wanxiang integrate, package, and optimize existing mocap, 3D modeling, and livestreaming technologies, then provide them to companies interested in virtual idol projects, enabling faster deployment.

Platform-wise, Bilibili is unquestionably the main battlefield, but short-video platforms like Douyin represent new opportunity — especially with this year's e-commerce livestreaming surge. Additionally, across the industry ecosystem, one piece remains missing: derivative licensing and development. This is the role that truly connects virtual idols from content to monetization, yet we haven't seen many players here.

In China's virtual idol market, we've also observed one major change this year that may be unique to China: livestreaming. Taobao Live, which previously had virtually no connection to ACG, has given substantial traffic support to virtual idol commerce this year. One virtual idol, with zero prior market recognition, attracted over 1 million concurrent users in a 4-hour debut stream through Taobao's traffic扶持.

Then there's Luo Tianyi's livestream — her appearance fee was 900,000 RMB, higher than many human celebrities. Results were strong: 2 million in tips and 2.7 million peak concurrent viewers.

This suggests market acceptance of virtual idols may exceed our expectations. Meanwhile, virtual idols' overall buzz has been directly elevated through several e-commerce livestreams. Beyond directly addressing the anxiety of content that initially generates no revenue, e-commerce livestreaming has indirectly pushed virtual idols into mainstream awareness.

04 An Investor's Perspective on Virtual Idols, and Three Major Challenges

Why is FreeS Fund interested in this space as an investor?

First, virtual idol audiences skew younger, with higher interest and enthusiasm for new things. So we believe the market is large enough. Compared to human idols, virtual idols have irreplaceable advantages in lifecycle, controllability, and interactivity:

First, lifecycle length. Human idols age; virtual idols can persist indefinitely. If we consider Doraemon or Pikachu as virtual idols, they've "lived" for decades and will foreseeably continue.

Second, human idols make mistakes; virtual idols offer stronger controllability with lower scandal risk.

Third, interactivity. Normally you can't ask Wang Yibo to change anything for you, but with virtual idols, you can co-raise them through sustained tipping and positive interaction. Meanwhile, you can't turn a trainee into a Zhou Shen-level singer in a month, but virtual idols can achieve this.

Fundamentally, from the perspective of unchanging underlying user needs, virtual idols serve the needs for companionship and belonging exceptionally well.

Now let's examine current challenges facing virtual idols.

First, localization. We haven't yet seen virtual idol content that truly meets Chinese user needs. Only localized content can break through the niche ceiling.

Second, mainstream adoption. Virtual streamers remain fundamentally a core ACG circle hobby, far from becoming a genuinely mass-market content category. Top UP hosts on Bilibili have followers in the tens of millions, but top virtual UP hosts like Lingyuan have only around 2 million-plus followers.

Third challenge: monetization — how to connect content with commercial realization.

Livestreaming may partially alleviate virtual idols' monetization challenges. We can see that overall subscription and tipping for virtual streamers on Bilibili grew 351% year-over-year, indicating Bilibili users have adopted virtual streamer tipping very quickly, with strong payment willingness.

But beyond live e-commerce, we hope to see more monetization models emerge, enabling the virtual idol ecosystem to become fuller and more complete, making industry growth healthy and sustainable.

Entrepreneurs in entertainment and culture are welcome to contact the author Peter for discussion. His email is chenzhe@freesvc.com, and you can also reach him through FreeS Fund's WeChat contact (ID: freesfund).

Summary

-

We are at a technological inflection point. Appropriately priced technical solutions will emerge for virtual idols, increasing content supply. For virtual streamers, mocap costs will drop significantly while quality improves through algorithm and data accumulation. Ultimately, toward virtual social networking, perhaps just a smartphone will suffice.

-

In China, virtual idols face three challenges: localization, mainstream adoption, and monetization. Livestreaming may partially alleviate monetization challenges. But we hope to see more monetization models emerge, enabling the virtual idol ecosystem to become fuller and more complete, making industry growth healthy and sustainable.

-

We believe that following the trajectory of virtual idol technology and content development, a social platform built around virtual avatars will very likely emerge.

Discussion

Q: Is live commerce the path forward for virtual idols in China? Tap "Like" at the end of this article, and reply "虚拟偶像" in the WeChat official account backend for our preliminary answer.

Giveaway

Tap "Like" at the end of this article and share your thoughts on virtual idols in the comments. By 21:00 on June 23, the 6 most thoughtful commenters will each receive a custom FreeS Fund notebook.

2020: Consumer Brand Entrepreneurship Enters an Era of Multiple Simultaneous Drivers | Frees Fund

Double 11 at Halftime: What Did Chicecream, Saturnbird, Botaniera, and Huasheng Haoche Get Right?

The Category Logic Behind the Hype — Coffee Industry Investment as Case Study

Breaking Through as a New Brand: From Traffic Thinking to Content Thinking | Frees Fund

Where Is the Endgame for E-Commerce Livestreaming? | Frees Fund