Li Xiang x Li Feng: Stripping Away the Emotion, Let's Talk About Economic Variables for the Second Half of 2023 | Li Feng Column

A Conversation About the First and Second Halves of 2023

This column comes from Li Xiang and Li Feng ("Uncle Feng") on the "High Energy" podcast's Macro Chats segment. Li Xiang is the curator of the Detailed Conversations book series and editor-in-chief of Dedao App.

This article synthesizes content from Episodes 26 and 27 of the Macro Chats series. Episode 26 was recorded on June 30, 2023 — a transitional moment. Uncle Feng and Li Xiang connected threads from their first-half discussions, including China's economic recovery, the resilience and divergence of the US economy amid rate hikes, US-China competition, and China's push for technological self-sufficiency. They also looked ahead to the second half of 2023 and discussed the widely watched real estate sector.

Two weeks later, on July 17, China's first-half economic report was released. In Episode 27, Uncle Feng and Li Xiang analyzed the fresh macro data. Grounded in these numbers, the conversation extended and supplemented the previous episode.

Uncle Feng noted on the show that while future variables are many, expectations won't trend downward forever. Stripping away emotion and returning to facts — perhaps this piece can offer you a lens for understanding the causes and implications behind economic data. If any specific topic from these two chats interests you, you're welcome to revisit earlier Macro Chats episodes from the first half of 2023.

Engagement Giveaway

Expectations won't trend downward forever. What new changes have you seen in your industry lately? Share your observations and thoughts in the comments. By 5:00 PM on August 8, we'll give Dedao App recharge cards worth 200 RMB to the 2 users with the most likes and the 3 users with the most thoughtful comments.

/ 01 / First-Half China Macro Review

▎Pessimistic or Optimistic? Two Benchmarks for Measuring Chinese Economic Growth

Li Xiang: Welcome to High Energy. I'm Li Xiang. This episode is another Macro Chat with Uncle Feng. In the last episode, he summarized his understanding of the first-half macro economy. After we recorded that, China's first-half economic report came out. This time, we'll ask him to do some specific analysis and interpretation of that data.

Li Feng: Sure. We're trying to find perspectives or directions that might be overlooked, but still grounded in facts and data. This analysis certainly has subjective positions, but it's more about exploring different angles — which is what we hoped to achieve when we started Macro Chats.

Li Xiang: Looking at the first-half data, including Q2, I think quite a few people were somewhat disappointed. I noticed that several institutions, including JPMorgan Chase and Morgan Stanley, lowered their full-year growth forecasts for China after the first-half GDP release?

Li Feng: Right, basically from 5.5% down to around 5% — though roughly 5% was also the target announced in March. When it comes to this disappointment or optimism about China's economy, I think there are two key bottom lines. One is the pessimistic bottom line: the relationship between China's economic growth speed and world economic growth speed.

What this means is whether China's share or contribution to the world economy will keep increasing. For instance, if 2023 world economic growth is expected to be around 2%, and ignoring exchange rate fluctuations, if China's GDP growth exceeds 2%, logically China's share of the world economy increases.

Then there's the optimistic bottom line — in global competition, the proportional growth relationship between China and the US, the world's two largest economies. The answer depends on both the growth rates and the scale of China-US GDP.

In 2020 and 2021, China's GDP reached over 70% of US GDP. Since 2022, mainly due to RMB depreciation, China's GDP relative to the US has declined in dollar terms. Using that 70% baseline, if 2023 US full-year growth is assumed to be between 1.5%-1.8%, then theoretically, if we grow roughly above 2.3%, at constant exchange rates, our share of US GDP would keep rising.

Whether China's contribution to world economic share can keep rising, and whether China's economic scale relative to the US can keep rising — stripped of individual emotion, the answers to these two questions can serve as a lens for observing China's economy.

▎Half-Year Review: "Strong Expectations" and "Weak Recovery," Plus Some Data Points

Li Feng: Back to our half-year summary, let me roughly recap this year's overall economic trajectory. In short, there's a gap between expectations and reality, specifically "strong expectations" versus "weak recovery." In January and March this year, whether looking at foreign capital, domestic capital markets, the overall economy, or the RMB exchange rate, there was consistent optimism about China's economy. January brought expectations from COVID reopening; March brought suppressed demand bouncing back after the Lunar New Year. Across multiple markets, people started believing in Chinese growth. That's the so-called strong expectations.

What happened afterward: internal and external factors successively affected overall expectations on both fronts. The internal factor was weak recovery. Strong expectations carried in from January and March, with relatively high hopes for post-COVID recovery. After suppressed demand exploded in March, people found the recovery fell short of expectations. From late March through April, May, and June, expectations were downgraded step by step. This reflects the gap between strong expectations and weak recovery.

Looking at the latest first-half macro data: overall, June credit slightly exceeded expectations, exports declined, consumption recovery looked somewhat slower. Additionally, real estate failed to stabilize at a low level and instead stepped down slightly in April-May. The trend in the data does show some challenges overall.

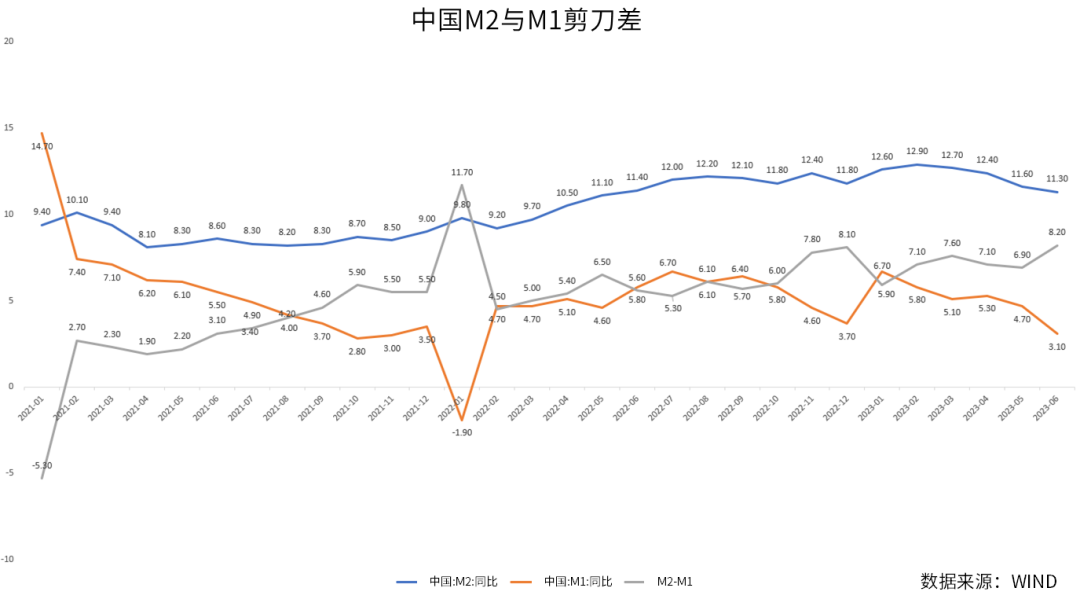

First, credit. In June, the M1 (narrow money supply) and M2 (broad money supply) scissors gap widened again to 8.2%, the highest this year. Economically, every time credit expansion accelerates, this gap typically widens — mainly because increased liquidity isn't immediately absorbed. In the data, this shows as faster M2 growth that M1 hasn't caught up to yet.

The difference between M1 and M2 growth rates can partly indicate whether social capital is being activated to drive the real economy including consumption. Faster M2 than M1 growth, with a widening gap, suggests currently inefficient capital activation — possibly reflecting confidence issues among enterprises and households. Of course, these two data points need further observation.

On credit and social financing, we also noticed: Chinese household medium- and long-term loans added 463 billion RMB in June, a sharp month-on-month rebound from May. But we also found that June transaction area for commercial housing in major and medium cities was 12.3982 million square meters, clearly below the five-year average for the same period — not quite supporting the credit increase. However, June passenger vehicle sales were 2.268 million units, up 10.6% month-on-month and 2.1% year-on-year; it's unclear whether auto and other big-ticket consumption partly drove credit growth. Additionally, Chinese household short-term loans added 491.4 billion RMB in June, up 63.2 billion year-on-year, the highest June on record — possibly due to the Dragon Boat holiday and the usual summer travel peak.

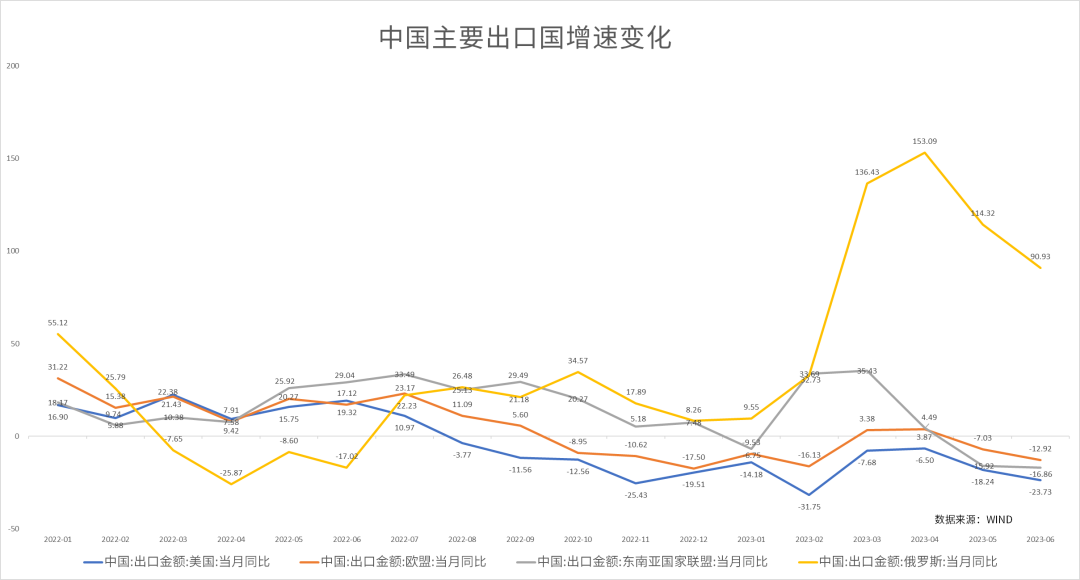

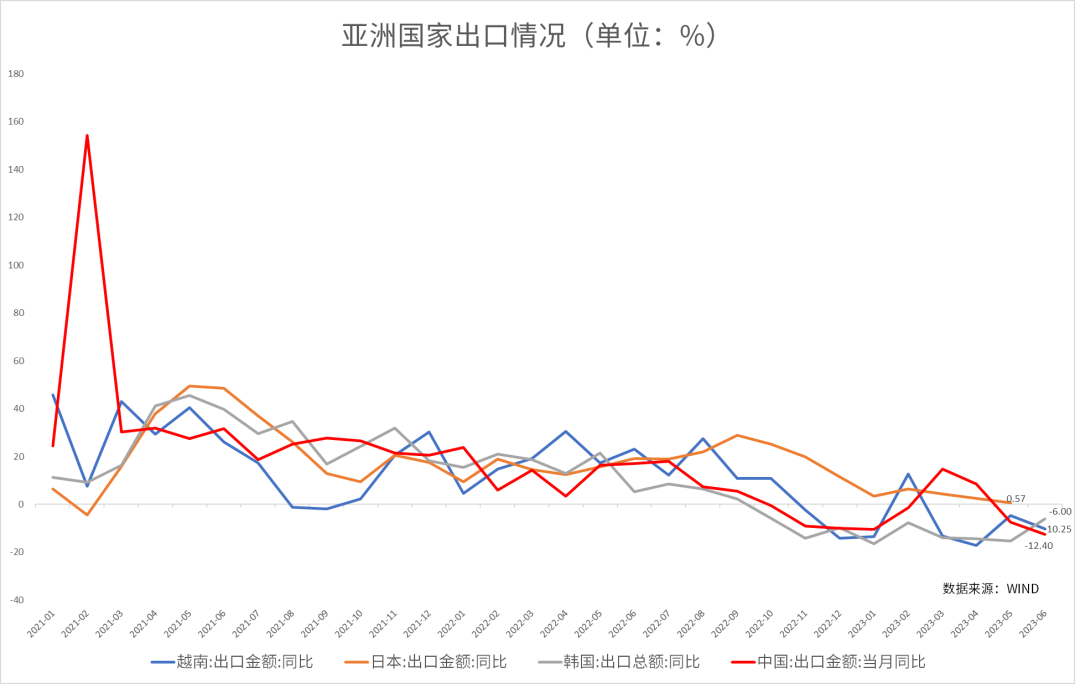

The second relatively challenging area is foreign trade. Since April this year, China's export value growth to major destinations — ASEAN, the US, the EU, Russia — has declined continuously. Exports to the US turned negative after August 2022; exports to the EU and ASEAN turned negative starting May 2023. According to Ping An Securities Research Institute statistics, Belt and Road countries that boosted Chinese exports in March-April saw their positive contribution turn negative from May onward.

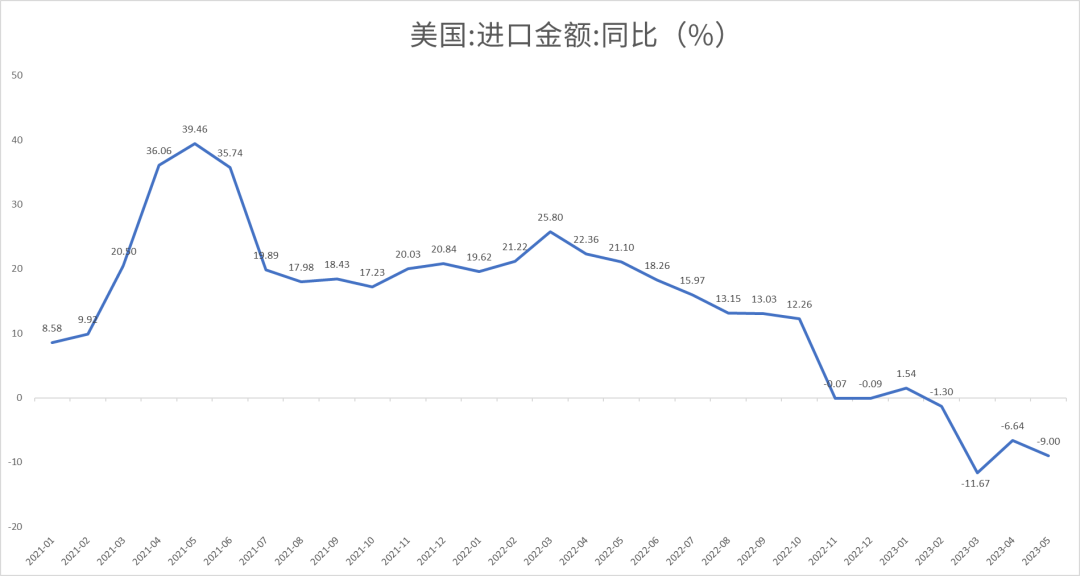

The export slowdown first stems from shrinking global external demand. Major purchasing power in developed economies, after successive rate hikes since last year plus energy price pressures, has begun importing less. Take the US: US import value turned negative year-on-year from early 2023, with a local trough of -11.67% in March due to the high base from March 2022. Data also shows Japan, South Korea, Vietnam and other Asian countries' exports declining since August 2022. Slower exports has become a global problem.

Taken together, these figures point to a challenge for processing economies in global supply chains. Countries positioned in the low-to-mid value-add segments with shorter domestic supply chains will feel the impact more acutely. China's relatively complete industrial chain and ongoing adjustments to its trade structure offer some buffer, but even so, it can hardly avoid the demand shock.

China's export decline also reflects the high base from the same period in 2022. In late Q1 2022, the Russia-Ukraine conflict disrupted supply chains for intermediate goods, sending prices sharply higher. China's sources for bulk raw materials differed from others', allowing its exported intermediate goods to be priced below global averages — which produced unexpectedly strong trade performance.

Li Xiang: If it's not just China seeing trade data slip, it's essentially global trade trending downward.

Li Feng: Right, it's as if the overall demand pool is shrinking or stagnating. Everyone's fighting for shares of a fixed pie — much harder.

Li Xiang: On trade, I'm also curious: if the Fed stops hiking rates, could global trade improve in the second half?

Li Feng: Possibly. This is largely dollar-driven pressure. Fed tightening created a strong dollar, which strengthened dollar-denominated assets. Our macro analysis shows many developed economies are flashing consistent recession signals. If the dollar stops rising and other central banks can follow suit, easing currency pressures, global conditions may find some relief. (On July 26 local time, the Federal Reserve announced another 25-basis-point increase to the federal funds rate target range, to 5.25%-5.5%. This marked the Fed's 11th consecutive rate hike, with cumulative increases reaching 525 basis points.)

/ 02 / The Global Economic Environment and Great-Power Competition

▎US Economic Resilience and Divergence Under Rate Hikes

Li Feng: We've briefly reviewed China's first-half economic conditions. Now let's turn to the international landscape, where the most closely watched topic is the US economy and the dollar's rate-hike cycle. After markets began pricing in a US recession last September-October, the economy has shown resilience over the past six months. Perhaps because expectations uniformly worsened, reality proved less dire than imagined.

This resilience shows up mainly in consumption — including services employment within consumption, and services jobs generated by government departments and related sectors as government spending increased. Additionally, the massive direct subsidies to households in 2020-2021, essentially "helicopter money," created "excess income."

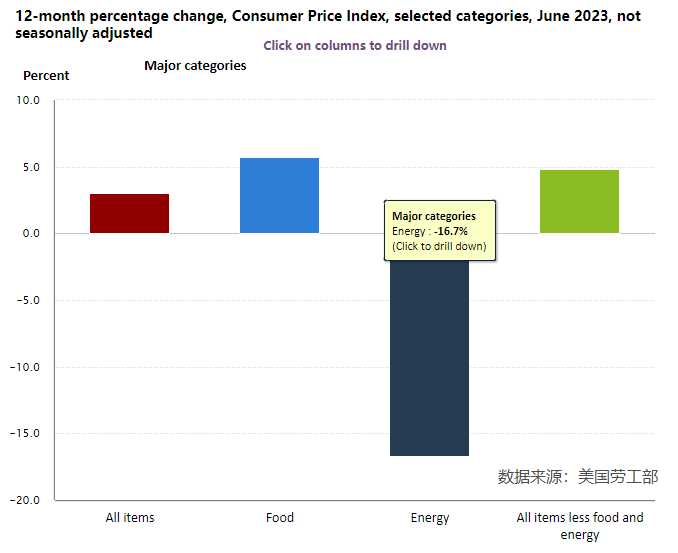

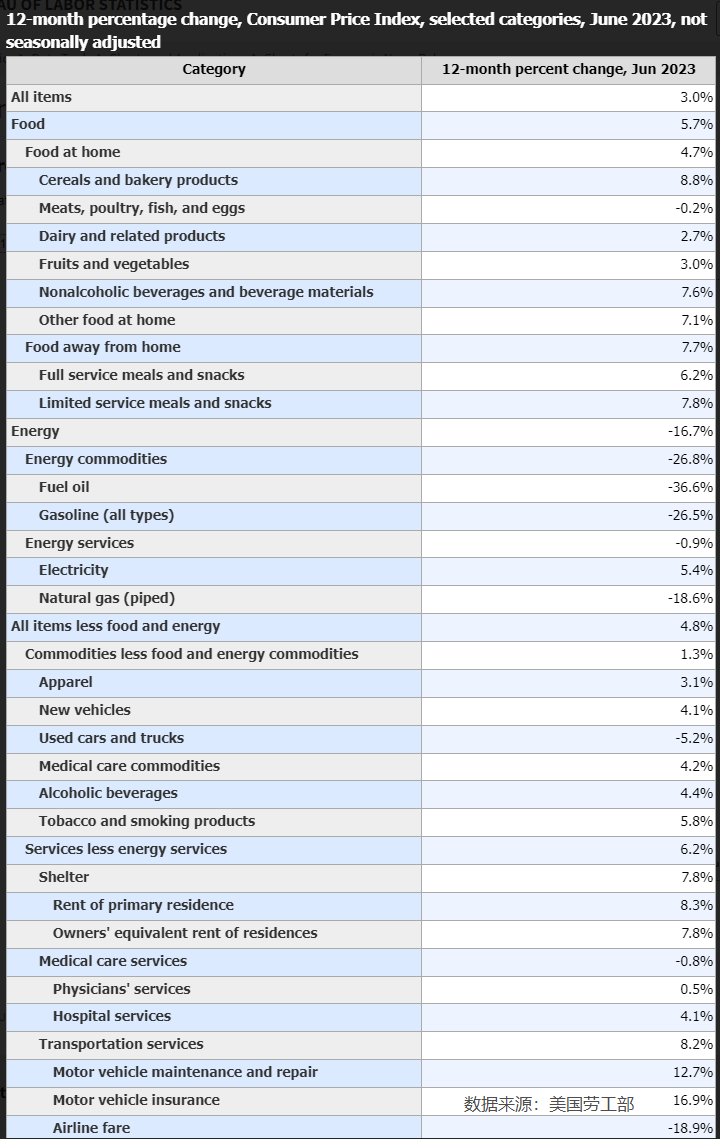

Full employment in services, government investment-supported jobs in related public sectors, and excess household income — these factors substantially supported US consumption. And consumption is the main pillar of the US economy. According to CNBC, on June 29 the US sharply revised Q1 GDP growth upward from 1.3% to 2%, driven by this consumption support. In June, US CPI inflation eased further to 3% year-on-year from May's 4%, below the 3.1% expected — the 12th consecutive monthly decline and the lowest since March 2021. Breaking down this better-than-expected inflation data by sector reveals so-called "inflation stickiness." Looking at June 2023 CPI changes by category, important services components, particularly rent and housing-related services, maintained sticky prices. The overall inflation surprise came mainly from energy prices' 16.7% decline.

▲ Image source: https://www.bls.gov/cpi/ This US economic resilience also shows in equity markets: the S&P 500 has rebounded 24% from its October 12, 2022 closing low, entering a technical bull market.

At the same time, US growth is polarized. According to Moody's Analytics, from November 2022 through June 2023, US PMI (Purchasing Managers' Index, reflecting procurement, production, distribution and other processes across manufacturing and non-manufacturing sectors) remained below 50 for over eight consecutive months, with gradual weakening. Correspondingly, we've all seen layoffs in tech and financial sectors.

Moreover, the US Treasury yield curve inversion has persisted for 12 months. So how long US economic resilience lasts is something to watch in the second half.

Let me briefly digress: why hasn't China shown similar resilience at this stage?

One possible reason lies in substantial structural differences. For China, external demand matters enormously. Consider: China has roughly 1/6 of global population, yet its manufacturing value-added in 2022 accounted for nearly 1/3 of the world total. That is, 1/6 of humanity produces 1/3 of global output. Meanwhile, taking a relatively high-GDP-growth year, in 2021 exports contributed 21.9% of economic growth, while consumption contributed 58.3%.

So if external demand faces genuine challenges, other sources must compensate — such as consumption. The data shows that with export growth declining, consumption contributed 77.2% of the 5.5% first-half GDP growth. This may feel somewhat at odds with perceptions. Consumption growth included rebounds in culture, tourism, leisure and entertainment services from last year's low base.

▎From US "Decoupling" to "De-risking": What Does It Mean?

Li Feng: Turning to the US, China-US competition is unavoidable. Many experts and scholars have noted that US containment of China shifted last year from "decoupling" to "de-risking." Over the past year, the US has both escalated unilateral restrictions on China's tech sector and used media and political channels to amplify "China threat" narratives around Russia-Ukraine, Taiwan Strait, and South China Sea issues.

On supply chains, since 2017 the "Indo-Pacific Strategy" has become central to US global strategy. The US has shifted portions of its high-tech supply chains from China toward Japan and South Korea, while moving lower value-add, labor-intensive industries to India. This explains many events we've discussed in previous macro conversations.

How are we responding to all this?

First, we're working to participate in building new trade systems and adjusting trade partner structures — from the previous US-Europe-centric pattern with other regions supplementary, toward roughly the inverse. This is a long-cycle but certain adjustment.

▲ Image source: DATA Jushi, National Bureau of Statistics

Second, in international relations, we've consistently played the role of peace-maker, hoping to facilitate more trade and economic development within a stable, peaceful framework. In March, China helped broker Iran-Saudi Arabia diplomatic normalization. We've also addressed energy import security through cooperation with Central Asia and Russia. Beyond this, numerous diplomatic initiatives with Southeast Asian and Western European countries are visible.

Finally, facing escalating US tech containment, we're pushing for self-sufficiency in various "chokepoint" technology areas. As mentioned when explaining batteries and new energy, we need many new "chain-master enterprises." What are chain-master enterprises? Let me cite two companies: BYD and Huawei. These are typical chain-masters — positioned at critical supply chain nodes with strong core competitiveness, capable of shaping industry ecosystems and resource integration. A key reason the US can use consumer markets and technology to influence and contain China is their abundance of chain-masters like Apple and Tesla. When Apple acts on US policy to shift supply chains, it affects our consumer electronics and precision manufacturing.

▎All Technology Export Is Ultimately Consumption

In this sense, China's response to tech competition ultimately requires many products with full-chain technology innovation — products with at least world-frontier capabilities.

Whether electric vehicles, smartphones, or smart home appliances, we need so-called new products built on core new technology mastery, recognized globally, forming new international brands and leading enterprises — "new chain-masters." Only then can we proactively manage, arrange, and shift supply chains, as Apple does today.

Li Xiang: How does technology self-sufficiency connect to ordinary consumers?

Li Feng: In the near-to-medium term, solving security and chokepoint issues requires all-out breakthroughs in key areas. But ultimately, for technology to achieve sustained development and competitiveness, demand must pull it forward — terminal consumer products pulling it. Behind this lies ordinary consumers' demand satisfaction.

Because new technology products, like new energy vehicles, must first rely on domestic demand to pull and iterate them to efficiency. Once this efficiency achieves international competitiveness on the new technology/product, they can "roll out" globally. As we've cited with EVs, robot vacuums, and other examples that have rolled out.

Apart from military applications, the endpoint of all technology is ultimately demand. Even basic energy like wind, solar, hydro, and power supplied to industrial enterprises mostly ends up serving consumer markets. Simply put, as we've discussed in macro conversations: without China having over half the world's NEV market, our new energy-related technology might not attract major auto-producing nations, especially European countries, to invest in China as it does today.

So to sum up, today's tech countermeasures and self-sufficiency efforts, as well as building external trade systems — all of these ultimately point to one thing: we need to solve our own consumption problem.

Beyond that, we need to use these new technologies, combined with demand and manufacturing capability, to redefine more and more new products. Not just consumer electronics, but also new-style tea drinks, apparel, and so on. Through full-chain digitization — like SHEIN — these can become new chain-leading enterprises.

Second-Half Macroeconomic Outlook

▎How Expectations and Reality Interact

Li Feng: Having summarized all the observations from the first half, what are some variables worth watching in the second half?

The first question is when exactly China will bottom out. I mean bottoming out of expectations, not the economy itself. Expectations include our expectations for the economy, foreign capital's expectations for China, and foreign capital's expectations about the impact of US containment strategy — when will these three negative expectations hit bottom? Expectations don't fall forever. Both China and the US will each develop in their own ways.

The concept of expectations bottoming out is this: at some point, reality is probably already better than expected, and it's hard to imagine things getting worse.

On how expectations and reality interact, our colleague at FreeS Fund drew a chart.

Let's crudely plot the roughly 5% growth target set at the beginning of 2023 as a straight line (green) — distributing the full-year 5% target evenly across each month, assuming average monthly growth of 5%. The red line records our actual monthly economic growth rate, the real operating results. The gray line attempts to simulate how domestic events affect investor sentiment — what people call the "felt experience."

The expectations curve and the actual economic performance curve also influence each other. For example, after the growth target was set in early 2022, actual growth declined month by month, compounded by pandemic factors, and the expectations curve also trended downward continuously.

There's another line (blue): foreign capital's expectations for Chinese assets themselves. This relates both to China's economy and to international events including US-China relations. Because evaluating Chinese assets requires considering not just growth, but also security and certainty.

The purpose of this chart is to try to step back and see, from an observer's perspective, how people's emotions and expectations were affected during specific periods — whether they accelerated away from or made volatile adjustments to actual economic data.

Of course this chart may not be correct. Because aside from the economic data, the other lines are drawn using qualitative rather than quantitative methods. Simply put, emotional fluctuations are hard to quantify. We can only make a schematic diagram to help everyone feel this upward and downward process and momentum. It doesn't mean each of us in the real world follows the line's trajectory exactly. It just attempts to show how different political and economic events, real economic development, and expectations connect and resonate.

Li Xiang: Understood. In general, sentiment tends to be amplified.

Li Feng: Yes. Both good and bad get amplified. Perhaps the most typical situation is: GDP fluctuates around the expectations line. If it deviates systematically, like in 2022, expectations will gradually amplify that deviation. If it's volatile, expectations will fluctuate more dramatically too. These are the various possible deviations between people's felt experience and real economic conditions.

Regarding expectations, one observable thing is the RMB exchange rate, because it basically integrates expectations for all these matters — China's economic recovery, how foreign capital views China's economy, and how the world views the impact of US strategy toward China. So we can observe exchange rate fluctuations.

▎The Dual Tasks of Growth and Structural Adjustment

Li Feng: Specifically for second-half growth: first, on the pure financial side, people may hope for stronger stimulus measures. Going forward, it's worth watching how we'll mobilize remaining policy space, how we'll design specific policies, and continue driving growth.

Second, regarding trade system adjustment. Trade system adjustment is certainly a long-term process, but all our diplomatic efforts will accelerate this system's transformation at different points. For example, changes in relations with Southeast Asian countries, with Middle Eastern and Central Asian countries, and commercial changes with major EU economic powers like Germany and France that the Premier visited — these are also variables for observing China's position in the global commercial system going forward.

Third, how demand is stimulated. Beyond the significance of domestic demand for domestic growth, if China wants to push for building a new trade system, we must be a buyer — we explained this carefully in previous Macro Chats. Being a buyer means we must push our consumer market to become a relatively important or even the largest purchaser in the entire trade system, and what we purchase must be end products, not intermediate products.

Overall, today we're facing a situation where three things need adjusting simultaneously. First, we need to adjust the trade system — this isn't done overnight. Beyond trade itself, it involves the currency system, related financial and banking systems, and so on. Second, we're adjusting our domestic economic structure — from one driven mainly by real estate to one driven by other sectors.

The third simultaneous adjustment is that we also need to adjust part of the financial structure. Originally focused on infrastructure, real estate, and manufacturing capacity expansion, we're now shifting to a different economic structure. Correspondingly, the original bank-driven, debt-based leveraged financial model will also be adjusted, so that direct and indirect financing drive in parallel.

Li Xiang: Listening to all this, at least for the second half of 2023, if we want to maintain relatively good economic growth, consumption is almost still the village's only hope. But speaking of domestic demand, many people online are concerned about weak consumption. Is weak consumption because households no longer have money to spend, or because we lack the confidence to spend?

Li Feng: I suspect both — challenges with employment, income, and future expectations, as well as having money but being afraid to spend. Both probably exist. On one hand, China has historically been different from the US. China's savings rate has consistently been high in East Asia, and East Asia itself has higher savings rates than Europe and the US.

Since the pandemic, people have accumulated large amounts of precautionary savings. Counting just the excess portion, households probably have roughly two to three trillion in excess savings. If we stratify consumers by income level — from below-middle, middle, upper-middle to high income — it's very hard to disaggregate which income tier mainly contributed this excess savings.

So, as mentioned earlier with US excess income converting to excess consumption: when will China activate consumption? This is hard for me to answer today, because I don't know the composition of excess income sources, nor which groups will be first to activate their deposits for consumption.

For example, for upper-middle income groups, perhaps they took money out of real estate investments but haven't found better investment vehicles temporarily, and combined with expectations, they just parked the money in savings first. This group might spend some on consumption — for family or enriching life experiences — but the total consumption they can stimulate is limited. For the relatively broader middle-income group, perhaps consumption gets activated after expectations and confidence turn upward. For lower-income households' precautionary deposits to become activated, it requires not just confidence, but also stabilization and recovery of the economy and employment.

Besides high savings rates, we have another characteristic: a "mesh-like social structure." Unlike the atomized societies of the US and other Western countries, Chinese family relationships are relatively larger and tighter, forming a mutually supportive kinship network.

This relatively tight mesh structure, to some extent, provides a safety net when families and individuals face temporary challenges. To put it simply: although today's young only-child generation may not live with their parents after growing up, in principle, if young people occasionally "nibble on the old" or, as reported, become "full-time children," this may be discussed as a phenomenon, but parents typically won't refuse.

Real Estate Market Summary and Outlook

▎A Difficult Problem

Li Xiang: This half-year, the real estate market has gone through ups and downs. I understand housing prices affect many people's judgments about economic prospects, and I'd like to hear Uncle Feng's overview of the first half's real estate situation and his predictions for the second half.

Li Feng: Real estate is indeed relevant to everyone, and it's also most relevant to most families' balance sheets, because two-thirds of Chinese households' assets aren't in cash but in real estate. And the GDP scale that real estate directly affects or that Chinese real estate can influence is roughly about one-fifth.

We've mentioned real estate many times in Macro Chats. In Episode 26, "Half-Year Economic Review and Outlook," we discussed real estate in detail and made an expectation judgment that there probably wouldn't be major stimulus policies for real estate — that expectation may need slight adjustment.

From today's perspective, there are real estate stimulus policies with both volume and price rising together. However, how to stabilize volume, enable some effective release of demand, while preventing prices from rising too quickly, is a key concern. Previously I tended to think real estate could probably stabilize at a low level, but after looking at June's data and Q2 trends, it seems some policy adjustment space may still be needed.

The next step may require getting volume up, or at least stabilizing it, while simultaneously not overstimulating and bringing back investment demand. Because large-scale new investment demand would create other long-term problems. I can only speculate that there will probably be some adjustments within existing policy space, but how to adjust may be as cautious as "walking a tightrope."

Based on current data, if we hold home prices constant, the floor for transaction volume is probably around 16–17 trillion RMB — and that's counting only pure刚需 (rigid demand). But real estate in every country is never purely刚需; it always carries both usage and investment attributes. It's just that the ratio between the two shifts at different stages.

The rational transaction scale for real estate would strip out both completely bullish and completely bearish expectations, with both volume and prices stabilizing. In theory, this scale should build on the pure刚需 base and add some investment demand — probably expanding the transaction volume by about 10–20%.

Then there's the price inversion between new and existing homes. Simply put, in the same district, older homes cost more than new ones. Resolving this inversion could happen either through modest declines in existing home prices, or through new home prices rising gradually and rationally, until both converge at a reasonable market price.

Would falling existing home prices affect Chinese household consumption, especially for刚需 homeowners? We can think through several scenarios. For investment-driven demand, a price drop means damaged investment returns. Like stock fluctuations, if we treat real estate as a risky asset class, price volatility is reasonable — it's an investment loss, not an asset loss for owner-occupiers.

If owner-occupied existing home prices fall, what gets affected is your next upgrade purchase — what people call the balance-sheet-damaged household sector. If you sell one existing home and buy another, you can theoretically hedge. But if you're selling an existing刚需 home and buying a new upgraded刚需 home, there might indeed be some loss.

If existing home prices fall rapidly in specific cities, it could potentially push local governments to adjust their economic structures faster. Which places can make that adjustment and which can't may become a topic going forward.

Li Xiang: Is the stabilization or even decline in real estate prices positively correlated with domestic demand not being that strong?

Li Feng: Home buying is an extremely long-term consumption decision. You might be taking on 10 to 15 years of debt, so you need expectations about your own future development. The confidence and stability expectations required for this kind of long-term decision are typically very high — they're what support the purchase.

Short-term socioeconomic fluctuations do affect the real estate market. But for刚需 housing, this short-term impact is less significant than the 10-to-15-year long-term expectations.

This also connects to the dense grid-like social structure we discussed earlier. For young people's first刚需 home in a new city, beyond their own payment capacity, the purchase decision is also influenced by the entire family's financial support — and that part is affected by current economic conditions.

▎Comparing China, US, and Japan Real Estate Markets

Li Xiang: Are there examples where real estate functions mainly as a consumer good rather than an investment vehicle?

Li Feng: The best-controlled cases are actually some European countries, including Germany. Fluctuations in the US real estate market mainly come from the owner-occupied housing segment, not primarily from investment attributes. During the American Dream era of the 1970s, everyone wanted a big house with a yard, and this cultural influence cut across all social classes. Meanwhile, the US has many immigrants — new residents with purchasing power — and immigration also drives expansion on the demand side.

The ideal is that everyone has a big house, but not everyone has the ability to pay. So US real estate cycles, like the 2008 financial crisis, mainly depend on how far risk is expanded — that is, how many people are enabled to achieve this dream.

Li Xiang: Real estate probably contributes a relatively high proportion to China's overall GDP. I recall that economist Richard Koo (Richard Koo: Chief Economist at Nomura Research Institute, proponent of "balance sheet recession" theory.) mentioned in a speech this June that one difference between China and Japan might be that China's entire construction sector contributed as much as 26% of GDP, which Japan didn't have at the time. Koo also discussed, including the geopolitical influences we face, the so-called middle-income trap, and our potential negative population growth — all problems that 1990s Japan didn't face.

Li Feng: Regarding real estate's contribution to GDP, if this portion's share in the real economy declines, other industries will need to fill the gap. For example, Japan's current economic structure is mainly consumption-driven, and by the primary-secondary-tertiary industry classification, it's the tertiary service sector that has grown more.

As for the other differences between China and Japan he mentioned, I actually think these were all problems that Japan began facing in the 1990s. Like the exchange rate we discussed — it relates to a core autonomy in the economy. After 1985, Japan's exchange rate changed passively, causing yen purchasing power to increase endlessly. Japan's capital market once inflated to 1.5 times that of the US, and yen-denominated assets including Japanese real estate were overvalued in a short period. This wasn't a gradual process caused by internal and external troubles or economic restructuring, but rather泡沫 (bubbles) added to the economy out of thin air in a short time — that should have been considerable pressure on Japan at the time. China's situation is somewhat different. Our GDP is about 70% of the US's, but our capital market capitalization is still less than half of the US's.

Of course, for the same event or data, people can hold different opinions and interpretations. We're just providing one or two small angles, and will continue to observe and observe.

Engagement

Expectations won't trend downward forever. What new changes have you seen in your industry lately? Welcome to share your observations and thoughts in the comments. By 17:00 on August 8, we'll give out 200 RMB denomination recharge cards for the Dedao app to the 2 users with the most likes and the 3 users with the most heartfelt comments.

- FreeS Fund Open Day returns, welcome to register | On the road to the future, there are always fellow travelers

- Li Xiang x Li Feng: From purified water to pure tea beverages, a research sample of China's consumption upgrade | Li Feng Column

- Li Xiang x Li Feng: Institutional reform, Silicon Valley Bank, GDP targets, the flow of money... Discussing recent China-US macro hot topics | Li Feng Column

▲ Li Xiang x Li Feng: The "Monopolistic Success" and "Gradual Dilemma" of the US Dollar | Li Feng Column

▲ Expansion or store closures, re-examining offline opportunities | Li Feng Column

Star the FreeS Fund WeChat official account for timely business insights