Li Xiang x Li Feng: Key Timelines and Events Worth Watching in 2024 | Li Feng Column

Why is the period after the Two Sessions such an important inflection point?

This column is drawn from the "Macro Chat" segment of the "High Energy" podcast hosted by Li Xiang and Li Feng (Uncle Feng). Li Xiang is the author of the Detailed Talks book series and the host of The Torrential Times.

As we step into 2024, "Will this year be better?" is on many people's minds. Not long ago, Uncle Feng and Li Xiang had an in-depth conversation. They started with consumer and service markets during the 2024 Spring Festival, covering tourism, film, and dining. They also discussed the hot topic of artificial intelligence. At the time, the Two Sessions had not yet convened, and they discussed important timelines and events worth watching in 2024.

Their discussion included:

- How should we view the boom in the Spring Festival box office? Does it reflect current consumer trends and economic vitality?

- Why are "we no longer falling into the consumerism trap"?

- Are we currently overestimating AI's development? As AI technology advances rapidly, why should we pay attention to energy supply?

- Why is the period after the Two Sessions an important juncture?

- If the US dollar begins to cut interest rates this year, what changes will it bring to the country and to each of our individual lives?

We've edited portions of their discussion into this article, hoping to offer fresh perspectives. We invite you to continue observing and exploring with us. You can also find the full episode on Xiaoyuzhou APP / Apple Podcasts / Ximalaya APP by searching for and subscribing to "High Energy."

Reader Giveaway

In consumer and service markets, what innovative opportunities have you observed? By 5:00 PM on March 21, the 5 readers with the most thoughtful comments will receive a copy of Empire of Cotton. This book traces the history of cotton industry connecting six continents, describing the process of capitalist globalization.

01 Observations on 2024 Spring Festival Consumer and Service Markets

Li Xiang: This year's Spring Festival box office, both in aggregate numbers and for specific films, has generated extensive discussion. On pure data, the results are impressive. But some deeper analysis points out that average attendance per screening actually declined. The high grosses came from increased screen counts, or rather from adding more showtimes. Ticket prices, of course, are also a factor.

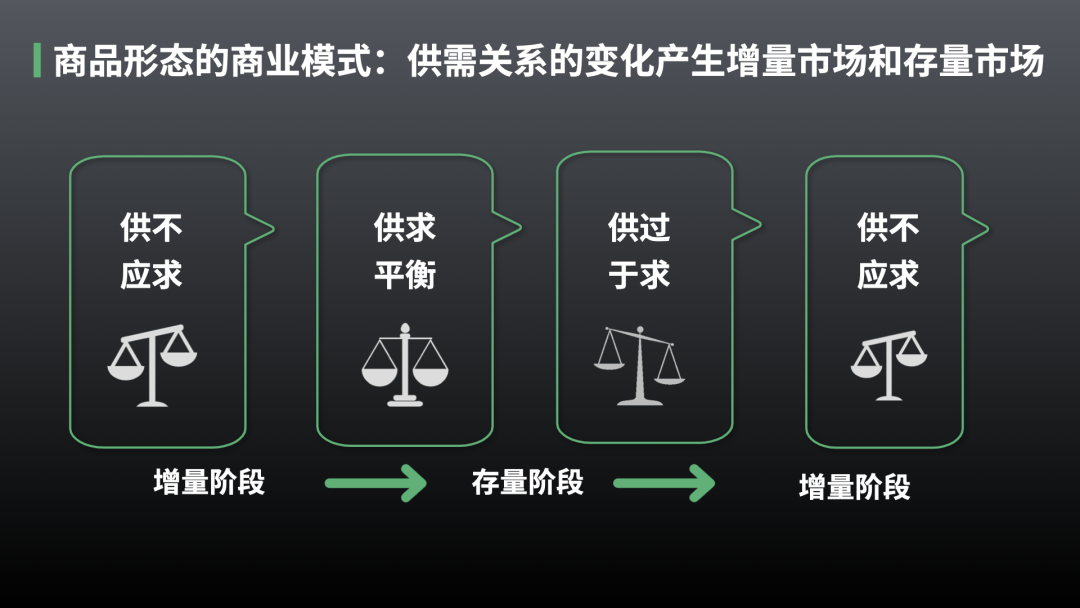

Li Feng: Perhaps this is how it should be. In the US, when people go to see a blockbuster, they don't want to be packed into every corner — if you buy tickets late, you might only find seats in the corner. My understanding is, from a service experience perspective, we don't want to see severe short-term supply shortages. From the perspective of penetration and coverage of goods and services, we want to avoid this too. That's because in a society with diverse goods and services, supply-demand balance is crucial for maintaining market stability and consumer satisfaction.

Li Xiang: Right, achieving high box office through increased showtime supply may differ from achieving it through insufficient supply. One argument is that the latter better proves a film's quality is higher and audience demand stronger.

Li Feng: Not necessarily. I've always believed the service sector will play the most important supporting role in China's future development. Services encompass many areas including cultural tourism, dining, and more. Though people may still be conservative or lacking confidence in spending, broadly speaking, the prosperity and market scale of domestic tourism definitely exceeds what came before.

I think the cultural industry may be undervalued today. It has potential to recover better than pre-pandemic levels. The essence of the service sector is making it easier for people to feel pleasure and satisfaction. Take concerts — the great thing now is that even for stars like Jacky Cheung, with increased show counts, people no longer need connections to get tickets, they can just compete online.

Li Xiang: This shows supply has increased.

Li Feng: Broadly speaking, whether in a goods economy or service economy, as long as it's a commercially developed society, there won't be long-term, severe supply shortages in the end.

Current tourism does have some challenges — for instance, local reception capacity, personnel transport, and accommodation still have room for improvement. But overall, supply and demand will eventually readjust in a commercial society. Just like when we buy things, whether houses or anything else, most go through a process from supply shortage to balance, and now to overcapacity, that is, oversupply.

Li Xiang: I have one observation: the Spring Festival slate was missing that classic sense of a blockbuster, something like Avatar or The Wandering Earth with high production costs and visual spectacle. What we're seeing in the market now are basically dramas.

Li Feng: Whether blockbusters appear in film has similarities to what we discussed about online games. Like well-crafted games, big-budget films costing hundreds of millions typically require decisions made two or more years in advance.

If we work backwards, for a film to release during the 2024 Spring Festival, the production team probably needed to decide whether to invest and shoot before 2022. Given conditions at that time, whether large-scale filming and exhibition would be allowed was a consideration. For example, Creation of the Gods I, released in 2023, had already wrapped in 2019.

In recent years, large-scale investment in the film and television industry may have decreased somewhat. The industry experienced significant investment bubbles from 2015 to 2017, which burst around 2019. Layer on the pandemic, and the industry took a double hit.

As a typical representative of the service sector, entertainment and tourism are now back on a development track. From data and phenomena we've observed, enthusiasm for travel is recovering. Online travel platform Trip.com Group released its 2023 financial report, showing net profit attributable to shareholders of approximately 9.9 billion yuan, up over 600% year-over-year.

There are also macro data showing service sector development exceeding expectations. In 2023, social media carried much news about the restaurant industry's struggles and insufficient consumption. But looking at macro data released by the National Bureau of Statistics in December 2023, total dining consumption first broke through five trillion, reaching 5.289 trillion yuan. Compared to 2022, this was growth of about 20.4%.

Looking at performance of leading restaurant enterprises in Hong Kong and A-share markets, many companies grew beyond expectations. For example, Yum China's financial report shows that in 2023, system sales grew 21% year-over-year, and core operating profit grew 79%. Yum China is the parent company of Pizza Hut and KFC, and both brands have been quite successful in lower-tier markets.

If people consider Yum China's growth to represent consumption downgrading, then some restaurant enterprises targeting mid-to-high-end markets are also worth attention. For instance, time-honored restaurant companies Quanjude and Tongqinglou released 2023 performance forecasts. Quanjude expects to turn from loss to profit in 2023, from a loss of 278 million yuan to profit of 56-66 million yuan. Tongqinglou expects net profit growth of 191.45% to 242.13%. Some smaller companies like Xi'an Catering or Jiumaojiu also performed very well.

We often discuss the long-term development potential of the tertiary industry. Dining, culture, entertainment, and tourism are the most typical major categories within it, and these categories achieved above-expectation growth in 2023.

I've also noticed that after the Spring Festival, some small shops in places I frequent have closed. I don't know whether these closures mean they're waiting until after the Lantern Festival to reopen, or if they've truly shut down. People's lived experience may not be wrong, but at the macro level, the service sector is indeed growing.

Overall, in 2023 the restaurant industry saw many establishments close, but also new ones open. The total market grew substantially, but branded and leading enterprises benefited more. After the ups and downs of recent years, many service industries show this phenomenon.

02 "We No Longer Fall Into the Consumerism Trap"

Li Xiang: A similar phenomenon to the restaurant industry has appeared in automobiles. In the second half of 2023, I discussed with an executive at a leading automaker that despite the market looking very prosperous, the actual incremental growth was mainly captured by a few companies, while most companies took significant hits.

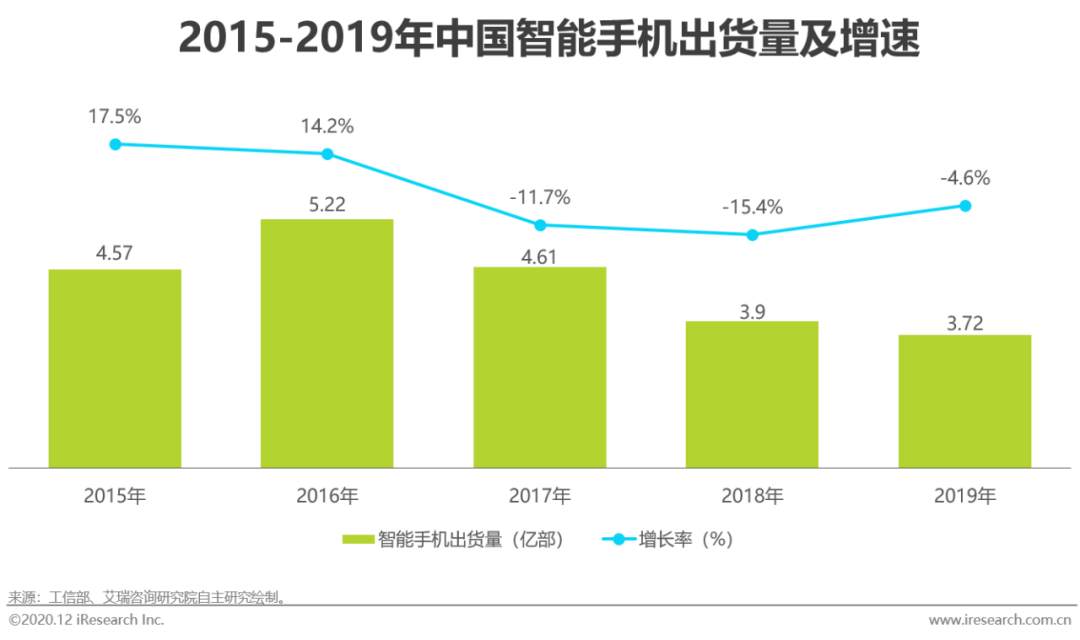

Li Feng: The auto industry is very similar to the smartphone industry. Phones had a blooming period from 2013 to 2016, then went through a brutal elimination round from 2016 to 2019, finally leaving a few leading brands like Xiaomi, vivo, OPPO, and Huawei. If Huawei hadn't been sanctioned, consolidation likely would have continued, just with different market shares among the four companies.

The auto industry in 2023 and before may still have been in that 2013-2016 phone cycle. Starting from 2024, especially for new energy vehicles, it may enter the pattern that smartphones saw from 2016 to 2019.

Li Xiang: In a growing market, who captures the growth is a question. This means not the entire industry shares in that growth.

Li Feng: Still using the restaurant industry we mentioned earlier as an example — after leading enterprises benefit, they raise the barriers for later entrants to come into the market.

The "internet-famous" phenomenon we used to talk about is especially typical in the restaurant industry. Influencer-driven brands fall into two categories: those that charge premium prices purely off hype, and those that combine viral appeal with genuinely differentiated products or real competitive moats.

Looking at today's market, whether in consumer goods or services, what we're seeing is the first type getting wiped out — products that are merely internet-famous without being special, without substance. "Not special" here means the product lacks the substance or other barriers to support its value.

We can observe this pattern in restaurants and even apparel brands. There are likely two reasons. First, before the pandemic, we went through a period of rapid diversification in social media. Whether Douyin or Xiaohongshu, these platforms gave brands traffic dividends — opportunities to capture consumer attention. Today, however, social media has become normalized, no longer novel. In trendy terms, it's been "disenchanted."

Second, the growth challenges many businesses face today are less about "consumption downgrading" and more about consumers becoming more rational. We used to talk about "pleasing others versus pleasing yourself" — China has essentially moved through this cycle very quickly. Consumers have shifted from emotional to rational consumption. This rationality doesn't mean not buying; it means that regardless of price point, consumers need clarity on why they like or want to purchase something.

Li Xiang: We're no longer falling into the consumerism trap.

Li Feng: Exactly. At the same time, China also has oversupply and intense competition at the product level — it's brutal out there. The sectors we mentioned earlier — dining, culture, tourism — these are all service industries in rapid development.

Li Xiang: One point you made really interests me. The service industries we just discussed — culture, dining, tourism — they're all growing, but there may be a subtle distinction. Regarding this year's Spring Festival movie season, one interpretation is that we may be moving away from pursuing spectacular visuals and massive budgets, returning instead to more authentic storytelling and emotional resonance. This could be seen as a trend back to fundamentals. Another interpretation is somewhat concerning: despite industry growth, suppliers seem increasingly unwilling to make heavy, long-term investments. The film industry may be somewhat special because it had to make decisions during the pandemic. This means practitioners may be optimizing for the short term rather than long-term, capital-intensive commitments — which could be a troubling signal.

Li Feng: I think this connects to the pandemic. My sister came back before the Spring Festival and described Europe this way: the economy isn't as bad as people make it out to be, but people also don't have the vitality they should. She felt everyone seems more佛系 (Buddha-like), more passive than before.

She believes the pandemic may have had some medium-term effects on people. She explained that due to the pandemic's unique nature, although foreign prevention measures weren't as strict, mobility controls and such still existed. Before the pandemic, people always wanted to "stir things up" from time to time. After the pandemic, that willingness has diminished considerably. Many people may not want to go through the hassle of traveling far during holidays, have lowered expectations for work, and feel less desire to explore what's around them.

Key Issues in Finance and Social Consumption

Li Feng: Before the "Two Sessions," the State Council's executive meetings typically lay some groundwork. Several important topics came up at these meetings. First, stabilizing and attracting foreign investment. Many people are pessimistic about China's ability to attract foreign capital, but actually, according to Ministry of Commerce data, in January 2024, China absorbed 112.71 billion yuan in foreign investment, up 20.4% month-over-month, though down 11.7% year-over-year. Particularly noteworthy: the number of newly registered foreign-invested enterprises in January was 4,588, up 74.4% year-over-year.

Li Xiang: This should be related to our policy changes? Many sectors now allow wholly foreign-owned enterprises.

Li Feng: If we take these foreign investment figures at face value, we can infer that perhaps the number of small foreign enterprises has increased significantly. Because while newly registered foreign enterprises grew over 70%, the amount invested fell 11.7% year-over-year — so the increase likely isn't from BASF or BMW-style projects involving tens of billions in one shot, but rather smaller businesses.

Li Xiang: This could be because many industries, including financial services, are now opening up. There used to be policy barriers.

Li Feng: Financial services is the next topic we'll discuss. The first issue raised at the State Council meeting was stabilizing and attracting foreign investment. The second was a related supporting measure: improving payment convenience. Our WeChat Pay and Alipay are very convenient — provided you have a domestic bank card to link, which is a real headache for many people traveling to China. Now Beijing Capital Airport has added dedicated counters to help solve the problem of how to pay within China. You can clearly feel our overall infrastructure upgrading as well.

The third thing mentioned at the State Council meeting was that local government debt risks have been broadly alleviated, and we need to push forward with making the comprehensive debt resolution package effective. This indicates progress on resolving local debt issues.

Incidentally, in February 2024, China's five-year-plus Loan Prime Rate (LPR) was cut by 25 basis points to 3.95%. A one-time 25-basis-point cut exceeded market expectations, marking the largest single-month decline since the 2019 reform.

This reduction in long-term lending rates will affect many things. The most obvious is its impact on real estate loans.

The five-year-plus LPR is the pricing benchmark for medium- and long-term loans, especially mortgage loans. After the LPR cut, new housing loan rates will follow downward, and existing mortgage rates will also adjust on their repricing dates. For first-time homebuyers with genuine housing needs, repayment pressure is reduced. As for investment properties, many major cities have already begun gradually easing purchase restrictions.

Beyond these topics, the government also discussed promoting large-scale equipment upgrades and consumer goods trade-in programs, and effectively reducing logistics costs across society.

China is undoubtedly a country with a highly developed logistics industry. In 2022, China's logistics costs reached 17.8 trillion yuan, accounting for 14.7% of GDP — a massive total. Compared to 8–9% in developed European and American countries, China's logistics cost ratio is relatively high.

In theory, it's feasible for China's logistics costs as a percentage of GDP to drop to 10%. This doesn't mean reducing the total volume of logistics, but rather reducing logistics costs. When logistics costs fall, many things can circulate more conveniently and cheaply.

Alongside the discussion of reducing logistics costs across society, there's also an implicit important topic: how to leverage the consumption potential of lower-tier markets. In terms of infrastructure construction, we need to pay attention to the most remote villages and townships. In many cases, the circulation cost of goods increases with distance, especially in remote areas — this is primarily driven by logistics costs. Therefore, goods tend to be more expensive in these places.

To address this, while reducing logistics costs, we also need to consider how to improve last-mile infrastructure to stimulate consumption in lower-tier markets. This means we must not only improve logistics efficiency but also ensure that village and township residents can purchase goods at reasonable prices, thereby narrowing the urban-rural income gap.

Li Xiang: Why is "trade-in" being treated as such an important topic for dedicated discussion?

Li Feng: That's a good question. I think it involves two things. First, from the consumer perspective, consider phone replacement cycles. In the early days of smartphones, our average replacement cycle was 18 months. But during the pandemic, with surging demand for remote work, online learning, and video conferencing, many people probably replaced their phones in 2020–2021.

Li Xiang: Demand for PCs and printers was also very strong then.

Li Feng: So at that time, people needed to replace phones in concentrated fashion, or purchase new devices. Even without replacing, they needed additional units. That was one replacement cycle. But starting from 2022, perhaps the market lacked attractive new models, combined with changes in consumer psychology, so replacement numbers may have been low. Market research firm Counterpoint Research data shows that during 2019–2020, China's smartphone replacement cycle was 24–25 months, while after 2022 it reached over 30 months.

Another example: many existing high-speed rail projects began operating over a decade ago — have these reached their replacement cycle? Or hospital diagnostic equipment, which may also need updating.

My understanding is that durable consumer goods lean more toward B2C, while equipment upgrades lean more toward B2B.

Li Xiang: Is our emphasis on trade-in programs coming from a consumption perspective? Does this mean we still have urgent needs in stimulating consumption?

Li Feng: Indeed, many examples we've discussed prove this point. We mentioned before that the ultimate outlets for technological innovation are almost exclusively consumption and military. Military is determined by multiple factors; we ultimately still need to rely on consumption. Whether new energy vehicles or phones, they're all driven this way. We can use technology to upgrade traditional manufacturing, thereby carrying new consumption demand.

Energy May Be the Core Variable Affecting AI's Long-Term Development

Li Feng: In February 2024, OpenAI released Sora, a text-to-video large model, attracting widespread attention. OpenAI CEO Sam Altman has also emphasized the importance of computing power and energy. I believe that logically, what will ultimately be decisive are these three things: data, computing power, and energy. The application scenarios for data determine its importance. Currently, AI applications are more concentrated in entertainment and media. Some joke that we originally expected AI to handle our daily laundry and mopping — that hasn't quite materialized.

Li Xiang: We did expect AI to do these things.

Li Feng: My colleagues and I discussed this before: looking at the long term, what might be the biggest variable affecting AI technology development?

Is it computing power? But computing power will likely become increasingly cheap — it won't become the core variable affecting AI development. Despite the technological barriers the U.S. has set for China, computing power ultimately won't become the main barrier. In most cases, whether search, cloud storage, or big data, these technologies themselves don't become long-term moats for any company; technology eventually gets cracked and becomes widespread.

Compared to computing power, energy may be one of the biggest variables affecting AI development. Most productivity revolutions increase by an order of magnitude the energy each person can manage and use. Historically, people initially relied only on their own strength, then began using horses. With the advent of steam engines and internal combustion engines, per capita power may have reached hundreds or thousands of horsepower. Entering the electrical age, we gained even more electrical equipment.

Looking ahead, if we assume AI becomes ubiquitous, our currently limited imagination might picture something like this: you put on a pair of VR glasses, and from the moment you step outside, it starts processing all kinds of information for you. It needs to calculate what you want to see and where to go. After getting in a car, it needs to calculate the optimal route, and may even need to drive the vehicle itself. These additional computing and data demands could increase per capita energy consumption by another one to two orders of magnitude. If we continue using horsepower as an analogy, each person might need tens of thousands of horsepower. If these demands keep growing, how should we solve the energy problem?

Li Xiang: Bill Gates's view is that nuclear power remains humanity's most reliable energy solution.

Li Feng: But today's per capita energy demand, like bandwidth, always lags behind our changing appetite for multimedia. Suppose we estimate it will take another 25 years to achieve controlled nuclear fusion. During this period, AI is spreading very rapidly, per capita energy consumption is rising significantly, yet controlled nuclear fusion hasn't been achieved at commercial scale. How should we respond?

Li Xiang: The market economy approach might be to raise energy prices; the planned economy approach might be to impose restrictions.

Li Feng: But what I want to say is that today, major countries globally may be diverging in their energy path choices.

The US is the world's largest crude oil producer, and economic interests determine the importance of fossil fuels to America. One lesson from the Russia-Ukraine conflict for China is that we cannot make ourselves completely dependent on others for energy. Therefore, China is going all-out to develop new energy and undergo an energy transition.

Looking at the ultimate incremental supply and structure of energy, whether fossil fuels or wind, hydro, and electric power, the ultimate source of energy is the sun. If people crack nuclear fusion, it's equivalent to cracking the most fundamental energy source.

Although in the short term China and the US have chosen different paths in energy utilization, if we face the future and consider the rise in per capita energy consumption driven by intelligence, finding large-scale new energy increments may be the better choice.

Li Xiang: The US is indeed a unique country. It has abundant energy resources, such as shale gas, while also leading in algorithms and artificial intelligence — for example, giving rise to companies like OpenAI and NVIDIA.

Li Feng: There's a data point that may surprise us: China has the world's largest shale gas reserves, and China's shale oil reserves rank third globally. But China's shale oil is mainly stored in areas with higher extraction costs — simply put, complex terrain and hard rock. There's a saying in China's petroleum industry: "Developing shale oil and gas is like drawing blood from capillaries, needing to 'squeeze' oil and gas from rock crevices only 1/270 the diameter of a human hair."

From a medium-term perspective, if AI materializes within 10 to 20 years, especially considering the complexity of China's industrial chain, its numerous application scenarios, and rising per capita consumption, China and indeed the entire world will face the challenge of how to find incremental energy.

Li Xiang: It's said that AI algorithms can improve energy use efficiency and thus achieve energy savings?

Li Feng: The cost of AI today is still mainly concentrated in computing power. But even the most advanced technology products follow the inherent laws of industrial products — performance gradually improves while costs gradually decrease. We can manufacture smaller, cheaper chips, making chips more personalized and intelligent. However, if total energy consumption grows substantially while supply remains limited, then the problem becomes thorny.

Li Xiang: So Elon Musk's idea is correct. He says Earth's resources are finite, and exponential growth cannot be supported within a finite space, so we need to colonize Mars.

Li Feng: If in the future the entire digital world revolves around each person, constantly computing for everyone while also processing multimedia information and interactions, then energy consumption will be far higher than our current levels of sitting in air-conditioned rooms and riding in vehicles.

Li Xiang: We'll just have to hope that controlled nuclear fusion technology arrives soon. I have one curiosity about AI: is it being over-anxioused or over-hyped?

There are two levels of observation: First, I've heard some views that US attention to AI may not be as high as in China — it's mainly companies in the San Francisco and Silicon Valley area that are focused on AI, but this attention may be exaggerated in the Chinese context.

Another intuitive feeling is that AI's popularity seems to be entirely driven by OpenAI alone. It keeps releasing new things, generating wave after wave of attention, without other companies effectively pushing the industry's development together.

Li Feng: I think so. Take Google as an example. Its search engine technology formed a high technical barrier in the short term, but over time, these technical barriers were not insurmountable. The key to its success was finding a business model with Matthew Effect in commercialization — namely, paid search ranking and search advertising.

Similarly, Tencent's instant messaging technology is also a technical barrier, but whether QQ or WeChat, the key to their success may lie in the Matthew Effect of social communication itself: once everyone joins this network, it becomes increasingly useful. Even if the second-place player has the same technology, they may not be able to surpass the already-built network.

The cost of developing AI technology today is indeed very high — most likely only large companies and those with substantial funding can afford the corresponding costs. Currently, there aren't enough truly effective AI applications, and even when applications exist, we need to consider whether the technology cost can exceed current human labor costs.

As described in Empire of Cotton, which we recommended earlier, "In 1770, wage levels in (Britain's) Lancashire may have been six times those of India. Even with machine improvements that made British per capita productivity two to three times higher than Indian workers, this was still insufficient to offset the wage disadvantage." Early mechanized production of cotton cloth couldn't compete on price with Indian handwoven cotton.

Today, facing AI technology with limited applications and not yet developed at scale, we need to assess whether the efficiency provided by these technologies is truly superior to traditional methods, and whether computing power and algorithm costs are more cost-effective.

05

In 2024, what important time nodes should we pay attention to?

Li Xiang: In 2024, what important time nodes do we need to watch? What significant events might occur that could serve as benchmarks for our judgment of the Chinese market?

Li Feng: First, the tone set at the Two Sessions is very important. The main topics are the economy, foreign investment, and private enterprises. The economic topic overall reflects economic goals, development direction, key levers, and priorities. The foreign investment component has already been strengthened — for example, we relaxed foreign investment access conditions at the end of 2023. Private enterprises need more confidence, so the private economy promotion law is an important topic.

Second is the external environment's impact on China, including energy and international relations. The US financial cycle — the rise and fall of interest rates — will have significant effects on global markets. Currently, the Fed has pushed back expectations for rate cuts, while we are keeping the market prepared for the possibility of rate hikes.

Third, worth noting, is the situation in Hong Kong. There were previously rumors that 200,000 people left Hong Kong during the pandemic. According to data published by the Hong Kong SAR Government Census and Statistics Department, Hong Kong's provisional population at the end of 2023 was 7.5031 million, an increase of about 30,000 compared to 7.4726 million at the end of 2022, representing 0.4% growth. Over the past few years, through measures such as the "Quality Migrant Admission Scheme," Hong Kong has successfully attracted large numbers of people to return, achieving net growth.

Leveraging its financial influence and liquidity, Hong Kong allows global asset allocation. Similar policies have been piloted for some time, with more openings recently. In February 2024, Hong Kong's market opened a new function allowing Chinese government bonds and other financial bonds purchased with RMB to serve as eligible collateral in Hong Kong for RMB liquidity. Also in February, optimized measures for the Guangdong-Hong Kong-Macao Greater Bay Area's "Cross-boundary Wealth Management Connect 2.0" formally took effect. At that time, banks including BOC Hong Kong and ICBC Asia launched RMB time deposit products in the Greater Bay Area with annual interest rates exceeding 6%, but with terms of only one month — likely more aimed at attracting new users to open accounts.

The three directions I just mentioned all illustrate that China's financial market opening is two-way. On one hand, foreign businesses can wholly own and operate Chinese financial enterprises, including banks and insurance. On the other hand, through Hong Kong as a special offshore center, RMB connects with international assets. These measures are very important for enhancing RMB liquidity.

In the A-share market, we can also see some policies and actions, such as appropriately reducing public fund securities trading commission rates and strengthening regulation of public fund securities trading commission allocation behavior; increasing penalties for capital market financial fraud, fraudulent issuance, market manipulation, and other illegal activities. These measures are essentially about cleaning up the market environment.

After the Two Sessions conclude, everyone can observe what adjustment measures may emerge in the three directions of economy, foreign investment, and private enterprises.

Overall, if the US dollar cuts rates, it may substantially reduce pressure on the RMB exchange rate, and even provide possibility and room for RMB appreciation. As many people are buying Japanese assets, it's not necessarily because of Japanese economic growth.

Li Xiang: This is related to exchange rates.

Li Feng: Yes. Japan's stock market hit new highs, but does this mean Japan's economy is improving?

Japan's economy hasn't grown significantly. Although Japan's economy grew 1.9% in 2023, nominal GDP was $4.2 trillion, less than Germany's $4.5 trillion, ceding its ranking as the world's third-largest economy to Germany.

Yet people are buying yen assets because the yen is cheap — you can use fewer dollars to buy more yen-denominated assets.

Why do other economies' interest rate hikes and cuts affect the confidence of Chinese entrepreneurs or ordinary people?

If the US dollar begins cutting rates, pressure on the RMB exchange rate will decrease, and there will be expectations for RMB appreciation. Even without considering economic growth, RMB-denominated assets may be revalued due to exchange rate movements, leading to rising asset prices and to some extent alleviating pressure on the real estate market.

Overall, the period after the Two Sessions is an important time node. Currently, Goldman Sachs has pushed back its US rate cut expectations to June. The best outcome would be if the matters we just discussed can proceed progressively and in the same direction. If the external environment improves — for example, if US finance enters a rate-cutting cycle, reducing global economic pressure — then signals in the same direction will compound. Once known risks materialize, the remaining situation at least won't get worse.

The most critical node this year is the end of Q1. Second, in Q2 we may need to watch closely for more data as well as changes in the external environment and financial cycle.

Reader Giveaway

In the consumer and services market, what innovative opportunities have you observed? By 17:00 on March 21, the 5 readers with the most thoughtful comments will receive the book Empire of Cotton. This book traces how the cotton industry connected six continents, describing the process of capitalist globalization.

▲ Four Funding Rounds Arriving With Spring | FreeS Family Funding News Vol. 18

▲ Li Xiang × Li Feng: In Waves of Technological Change, Why Is Gaming Usually the First to Cash In? | Li Feng Column

▲ Li Xiang × Li Feng: How We View the Consumer Market in 2023 and 2024 | Li Feng Column

▲ Li Xiang × Li Feng: Setting Emotion Aside, Let's Talk Economic Variables for the Second Half of 2023 | Li Feng Column

▲ Li Xiang × Li Feng: From Purified Water to Unsweetened Tea — A Case Study of China's Consumption Upgrade | Li Feng Column

Star the FreeS Fund WeChat official account for timely business insights delivered straight to you.