Li Feng x Guan Qingyou: What New Opportunities Remain in the Consumer Market for 2025?

How should we view the present and future of China's consumer retail market?

Consumption touches every one of us — because we're all consumers. But mention China's consumer market in 2024, and two phrases seem unavoidable: weak confidence and low sentiment.

What's the real picture? Did macro data and micro-level experience diverge in the year just past? Looking ahead, where do opportunities still lie in consumer retail? Is consumption downgrading or upgrading — which dominates? What factors shape spending behavior across age groups? It's been eight years since "new retail" was coined — has the essence of retail itself changed?

Last month, at the invitation of Ximalaya, Feng Shu (李丰) sat down with Guan Qingyou, president of Rushi Financial Research Institute, for an in-depth discussion on China's consumer market in 2024 and opportunities in 2025.

Here are the key takeaways:

- In the first three quarters of 2024, China's total retail sales of consumer goods grew slower than GDP. But as they say, every cloud has a silver lining — and there were bright spots in Chinese consumption.

- When debating whether consumption is upgrading or downgrading, we need to distinguish: are we being forced to choose cheap, low-quality unbranded products, or are we actively choosing high-value products enabled by more efficient supply chains?

- China's old, middle-aged, and young generations differ in characteristics and behavior, because spending power depends mainly on expectations for the future and balance sheet health. Notably, young people — tagged as "lifeless" on social media — remain the primary creators and drivers of consumer trends.

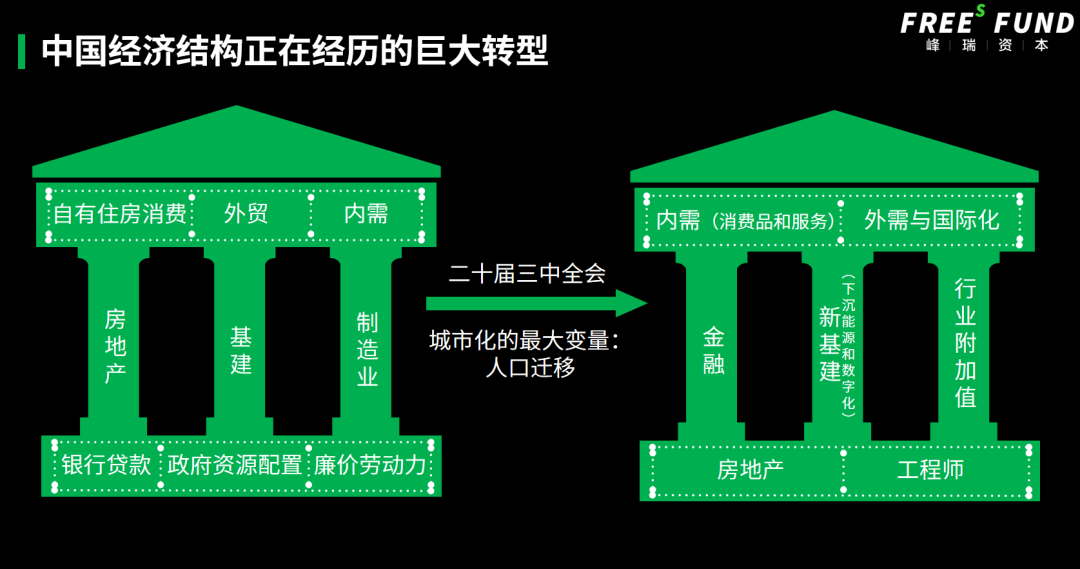

- Long-term policies like consumption tax reform, urbanization, and household registration (hukou) reform are slow-moving variables that will reshape the consumer market.

- Even as globalization itself slows, new consumer species actively expanding overseas have achieved substantial growth over the past year and a half.

We hope this offers one lens for observation. Change is always happening; only through continuous observation, synthesis, and learning from experience can we progress in an ever-changing world. Though the present may not be calm seas and clear skies, if there's winter, spring and summer will surely follow — and opportunities always exist.

Head to the Ximalaya app and search for "Qingyou Living Room · Season 3" to listen to the full conversation.

Giveaway

What do you think of China's consumer market in 2024, or what are your expectations for 2025? Leave a comment below — we'll randomly select 5 readers to receive the latest industry research handbook from the FreeS Fund team.

/ 01 /

By the Numbers:

How Did China's Consumer Market Fare in 2024?

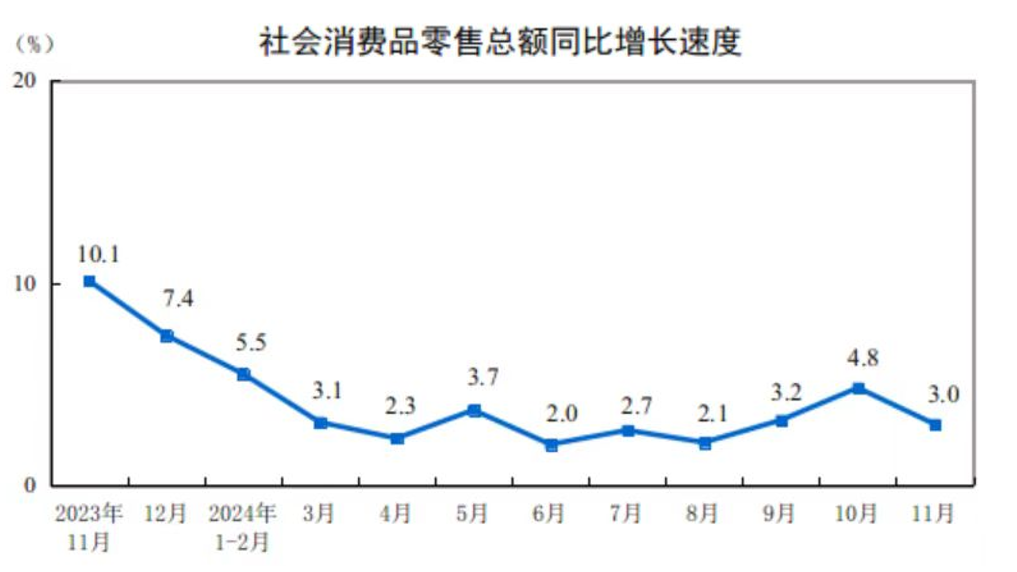

Let's start with two figures from the National Bureau of Statistics: in the first three quarters of 2024, total retail sales of consumer goods grew 3.3% year-over-year, while GDP grew 4.8%.

Source: National Bureau of Statistics

The comparison makes it immediately clear — in the first three quarters, consumption grew slower than GDP. In other words, though much hope was pinned on consumption, it wasn't the main positive contributor to GDP growth.

The counterpoint to consumption data is household deposits. According to the central bank, in the first ten months of 2024, household deposits increased by 11.28 trillion yuan.

Taken together, these macro figures seem to align with everyday social media discourse: the public is growing more cautious, consumer confidence needs a boost, and worried about future income uncertainty, people are more eager to save than spend.

But data shouldn't be viewed in isolation — you need to look both vertically and horizontally.

Vertically: 2023's full-year retail sales growth was quite strong at 7.2%, partly because it was compared against the low base of 2022, when COVID depressed figures. In 2024, the comparison shifted to 2023.

Horizontally: though countries lifted pandemic controls at different times, the common pattern was that experiential consumption — dining, entertainment, travel — recovered to 80-90% of pre-pandemic levels within a year to a year and a half after reopening. China followed this pattern. Notably, China has continuously streamlined travel facilitation over the past couple of years, introducing unilateral visa-free policies for 29 countries including France and Germany, and establishing mutual visa exemption agreements with 157 countries and regions covering various passport types. In the first half of 2024, total inbound and outbound crossings by mainland Chinese, Hong Kong, Macau, and Taiwan residents plus foreign nationals reached 92% of 2019 levels.

Physical goods consumption varied more by country, but broadly also needed about a year to recover to roughly 90% of pre-pandemic levels. China's trajectory was similar, though the general feeling was that consumers had become more cautious and rational.

The "rational mindset" hit "internet-famous" consumption hardest — viral brands, restaurants, hotels, drinks, entertainment venues. What defines "internet-famous" is primarily being famous; whether it's actually good or worth it is secondary.

Conversely, the categories that grew well were precisely those offering strong value-for-money while genuinely enhancing experience. Merchants have been fiercely competing to improve product value — brutal competition. Since most major economies are experiencing inflation while prices in many Chinese consumer categories have actually declined slightly year-over-year, these phenomena are easily interpreted as deflation. Moving up the price ladder, premium "expensive but good" brands recovered somewhat, but not as robustly as the foundational rational consumption tier.

/ 02 /

What Changed in 2024's "Double 11"?

Though e-commerce platforms no longer loudly trumpet GMV (gross merchandise volume), Syntun data shows that during 2024's "Double 11" period, combined sales across comprehensive e-commerce and live-streaming platforms reached 1.4418 trillion yuan, up 26.6% year-over-year.

"Double 11" has now passed its 16th year. With promotional events scattered throughout the calendar, neither consumers nor merchants are as eager to collectively engineer a sudden spending spike — we've moved past the stage of chasing some national consumption frenzy.

Still, 2024's numbers exceeded many expectations. Beyond the rational consumer mindset lowering expectations for "Double 11" results, two contextual factors deserve mention.

First, 2024 set a new record for promotional duration. Douyin's e-commerce platform kicked off on October 8. Taobao, Tmall, and JD.com launched their "Double 11" events on October 14.

Second, government subsidies helped. Starting late September, China saw an unusual large-scale subsidy for physical goods consumption, concentrated in home appliances and automobiles. Categories with subsidy stimulus performed notably well. Syntun data shows that in 2024's "Double 11," home appliances ranked first in sales across comprehensive e-commerce platforms (Tmall, JD.com, Pinduoduo, etc.) at 193 billion yuan, accounting for 16.3% of total sales and growing 26.5% year-over-year.

This round of consumption subsidies merits particular attention. Historically, value-added tax was collected primarily under the "production location principle" — meaning VAT revenue went to wherever goods or services were produced. The alternative is the "consumption location principle," where revenue goes to where goods or services are consumed.

Since 2019, China has been advancing consumption tax reform. In July 2024, the Third Plenary Session of the 20th Central Committee passed the Resolution of the Central Committee of the Communist Party of China on Further Deepening Reform Comprehensively to Advance Chinese Modernization, which in its section on deepening fiscal and tax system reform proposed "advancing the shift of consumption tax collection points further downstream and gradually transferring them to local governments." The "downstream shift" means moving taxation closer to the retail end — from production-based to retail-based collection, with payment responsibility shifting from manufacturers to wholesalers or retailers. By experimentally adjusting local government tax incentives, this encourages local governments to move away from their unbalanced focus on expanding production capacity while neglecting consumption stimulus.

To illustrate: previously, if Region A spent 3 billion yuan subsidizing consumers to buy appliances, under the "production location principle," since those appliances were manufactured in Region B, the tax revenue went to B — giving A little motivation to spend money and effort boosting consumption. Under the "consumption location principle," when A subsidizes consumption, A's residents buy on A's e-commerce platforms with delivery to A addresses, and all the stimulated consumption completes its final tax payment in A — suddenly A is highly motivated.

In September, the National Development and Reform Commission and Ministry of Finance allocated 150 billion yuan in ultra-long special treasury bonds to local governments, supporting tailored implementation of trade-in programs for consumer goods. This helped "unblock the last mile of subsidy distribution, getting tangible benefits into consumers' hands as quickly as possible."

Looking at PMI (purchasing managers' index) and total retail sales data, it's clear that "real money" consumption subsidies at the retail end can produce tangible stimulus effects. With this "national subsidy" pilot achieving relatively ideal consumption-boosting results, fiscal subsidy intensity may increase next year. Indeed, since November, some local governments have already launched local versions of home appliance "national subsidies," continuing the central program while both sustaining market vitality and consumer confidence and further advancing the tax reform from production to consumption.

/ 03 /

How Should We View Different Age-Based Consumer Segments?

An online quip characterizes China's current consumer groups as: "lifeless young people, half-dead middle-aged people, energetic elderly people." Perhaps this resonates.

In my view, even in a highly aged society like Japan, where consumption structures adjust and tiers diverge, young people remain the primary creators and drivers of consumer trends. While people habitually say this generation of youth differs from the last, ultimately every generation's young people are roughly similar at the same life stage. In every era, the then-trendy products were mainly popularized by young people.

That said, theoretically, since spending power depends on future expectations and balance sheet health, the quip does partly reflect the current state across Chinese age groups.

Among all age brackets, the middle-aged carry the heaviest balance sheet burden. Middle age coincides with peak cash outflows — supporting elderly parents and raising children, both money-intensive. Being middle-aged, one may easily become pessimistic about employment stability and cash income prospects. Meanwhile, as the primary mortgage holders, property price declines have significantly eroded home values, multiplying debt pressure. Faced with enormous balance sheet pressure, middle-aged consumers necessarily become more rational.

The "energetic" elderly are mostly urban retirees with stable pensions, who needn't be pessimistic about future income. Even if they carry mortgages, these are mostly paid off or in their final repayment stages. Particularly for those over 60 who converted public housing to private ownership, property pressure on their balance sheets should be minimal — after all, however prices fluctuate, they likely won't fall below the original conversion price. In this sense, they are indeed the most psychologically stable age group.

Take current tourism: young people trend toward "special forces" travel to atypical cities — spending less money pursuing novel, peculiar experiences. In typical tourist cities, you find more elderly visitors, who usually have ample leisure time and are willing to pay premium prices for better travel quality. This isn't unique to China.

Today's primary elderly consumers were mostly born in the 1950s-60s, having lived through extremely difficult periods. Even with comfortable retirement finances, their consumption mentality remains cautious. Looking ahead, when the post-70s generation retires en masse and becomes the new "energetic elderly," at what point will this group show obvious consumption growth? What product and service types will they favor? How to influence them... These are questions entrepreneurs hoping to serve this direction should consider in advance.

/ 04 /

Will the Mainstream Be Consumption Downgrading

or Upgrading?

My personal view: looking at the medium term (next 5-7 years), consumption upgrading will remain dominant.

For example, people used to drink barrelled water, then moved to bottled purified water, bottled mineral water, then bottled beverages and various innovative drinks. Compared to drinking a 3.5 yuan bottle of iced black tea, drinking a 9.9 yuan cup of Luckin Coffee represents consumption upgrading. Similarly, shifting from pre-mixed drinks to freshly prepared coffee beverages is also upgrading.

Of course, some will object: I used to drink 30-40 yuan Starbucks, now I drink 9.9 yuan Luckin — isn't that downgrading?

This needs case-by-case analysis. When judging downgrading, we must clarify: are we being forced to choose cheap, poor-quality unbranded or white-label products, or are we actively choosing high-value products enabled by greater supply chain efficiency?

Take "Three Squirrels" (三只松鼠), a brand I invested in early on. They frequently mention a concept called "premium value-for-money." Simply put: by extending the industrial chain from nut cultivation through precision processing, using a highly efficient digital supply chain to simultaneously serve online and offline end-to-end product delivery, continuously optimizing costs and margins.

I've also spoken with brands selling on Douyin. In 2022 through first half 2023, certain categories achieved remarkable live-streaming sales there, driven mainly by traffic operators and unbranded/white-label producers jointly creating a wave of low-price-driven sales growth. From second half 2023 onward, the brands capturing Douyin's main traffic红利 shifted to manufacturers with their own supply chains, who used traffic operations to capture market share with products slightly pricier than white-label but still offering strong value-for-money.

So I believe upgrading remains the medium-term mainstream, though its manifestations will differ.

05

Against a Backdrop of Weak Consumption, Where Are Opportunities in 2025?

By total retail sales of consumer goods, China ranks second globally behind the US, with not a huge gap between them. The larger divergence is in service sector value-added. In 2023, China's service sector accounted for 54.6% of GDP, while the US figure was 81.6%, with high-value services spanning law, finance, chip design, biopharma R&D, and more.

Given China's economic and social development stage, its service consumption will also converge with the US in aggregate and per capita terms. From a policy direction perspective, over the past year-plus China has aggressively opened precisely the service sector — allowing 100% foreign ownership of banks and insurance companies, and proposing to permit wholly foreign-owned hospitals in nine locations.

If the past decade-plus saw China mainly achieve rapid growth in physical goods, to the point where its consumer goods retail market now nearly rivals America's, then following the path of social and economic development, healthcare, education, finance, experiential entertainment and other service industries could become China's fastest-growing sectors by aggregate value over the next decade.

Having addressed services or service consumption opportunities, let's return to physical goods consumption with four observations.

First observation: Among FreeS Fund's portfolio companies, those in the tens of millions to hundreds of millions yuan revenue range who launched overseas operations in 2023 have, over the past year and a half, seen revenue scale and profitability growth that has more or less exceeded our and their own expectations.

These companies fall into two categories.

One category comprises products that cleverly fuse both China's manufacturing chain and tech chain advantages. Examples include new musical instruments and medical devices built with sensors, chips, and motors. Once these consumer goods, refined through countless iterations in China's supply chain, enter overseas markets with far less intense competition than China, they can command higher prices than domestically, yielding better margins while achieving multi-fold sales growth — quickly becoming overseas industry leaders.

The other category involves using technology plus hardware supply chains to rebuild existing products from scratch. Examples include robot vacuums, robotic lawn mowers, AI glasses, and AI earbuds. Once these enter developed Western markets, they too can rapidly become brands with both sales volume, influence, and strong profitability.

Moreover, recall that Jack Ma first proposed the "new retail" concept in 2016. Per that definition, "new retail" meant being consumer-centric, breaking online-offline boundaries, and digitally connecting consumption scenarios with supply chains.

Eight years since the concept was introduced, having experienced many ups and downs, the past year and a half — perhaps because domestic market competition grew so fierce, or perhaps because domestic internet applications have become so developed — has clearly seen China's online-offline supply chain digital connectivity capabilities rise a major notch.

Second observation: If established-scale enterprises fail to achieve good online-offline supply chain digital connectivity, they're easily eliminated; if they do it well with considerable scheduling flexibility, they at least won't lose the race; if they add innovation on this foundation, they're more likely to win — examples include MINISO and Pang Donglai (胖东来).

Third observation: Starting from coffee and tea.

Recall that from mid-2020 through end-2021, a roughly 16-month period, nearly everyone in the coffee/tea track told the same story: Japan's annual per capita coffee and tea consumption far exceeds 100 cups, while mainland China's figure was under 10, implying China's coffee and tea market held at least several-fold growth potential. Based on this, many argued that though consumer investment bubbles were huge, coffee and tea surely weren't among them — the massive latent growth space would rationally materialize.

Looking back, four years ago coffee's main consumers may have been fashion-conscious youth in tier-one cities. Though per capita consumption hasn't reached 100 cups, thanks to brands including Luckin pushing the market, coffee has largely achieved popularization and下沉 in China. These brands mainly did three things well: low prices, efficient online-offline supply chain digital integration, and beverage-ification. Milk tea followed a similar pattern, with brands like HEYTEA driving market popularization.

Extending the view to broader physical consumer goods: during the past decade-plus of rapid economic growth, nearly all consumer goods crossed the market popularization phase. Entering the next phase, consumers won't necessarily stick with the same category of popularized products — they'll make rational choices based on their age, preferences, and other factors. Using milk tea as illustration: some prefer tea-heavy, others milk-heavy, ultimately segmenting — whether they choose HEYTEA, CHAGEE, or another brand.

Fourth observation also connects to a major policy formulation change from the Third Plenum: "Implement a basic public service system based on habitual residence registration, ensuring that eligible agricultural migrant populations enjoy equal access to social insurance, housing security, and compulsory education for their children as local registered residents, accelerating the citizenization of agricultural migrant populations."

Simply put: provide equalized public services to those employed and residing in cities — wherever you live, work, and pay taxes, there you receive education, healthcare, and other public services and social security.

National Bureau of Statistics data shows that at end-2023, China's permanent resident urbanization rate reached 66.16%. Compared to developed countries, while this can continue rising toward roughly 80%, there's only about 15 percentage points of room. The corresponding figure is the household registration (hukou) urbanization rate. Ministry of Public Security data shows that at end-2023, the national hukou urbanization rate reached 48.3%. The roughly 20 percentage point gap translates to over 200 million people — those living and working in cities without local hukou.

Going forward, aside from a few megacities, if most Chinese cities implement the Third Plenum's directive, the impact will be enormous. Imagine when over 200 million currently non-local-hukou people can more easily obtain local home-buying qualifications, their children can attend school beside them, and their parents can access local elderly care and medical services — this substantially relates to how China's consumer market will transform. For consumer enterprises, this is also a long-term trend worth watching and contemplating.

06

Revisiting the Essence of Retail

Technology keeps iterating — so is the essence of retail itself changing?

Retail formats are indeed products of environment and era. Take the US: during WWII, America was virtually the only major combatant whose homeland escaped devastation, and massive wartime armaments demand enormously stimulated American manufacturing. For comparison, today China's manufacturing value-added accounts for roughly 30% of global share, while post-WWII America's industrial output exceeded 50% of the capitalist world. This was the backdrop against which iconic American retail models emerged.

In other words, because of overcapacity, the US consumer market was intensely competitive. Meanwhile, with super-developed manufacturing, manufacturing transformed every industry. McDonald's, for example, used automated hamburger-cooking equipment to enable standardized chain operations; Starbucks leveraged "La Marzocco" industrial espresso machines to stand out with high-value freshly ground coffee.

Beyond McDonald's and Starbucks, a cohort of famous consumer retail enterprises including Walmart and Dunkin' Donuts were born in the 1950s-1970s post-WWII period. After winning their home market, these consumer retail companies began crossing oceans with America's globalization process. One result: America got the world to absorb its overcapacity.

Today many say China also faces overcapacity, and China's consumer market is also intensely competitive. In my view, where China's market competition goes a step further than America's is in the online-offline full-chain digitalization we mentioned repeatedly. This owes to China's highly developed internet applications — Chinese consumer retail enterprises' digital connectivity capabilities and efficiency have risen a major notch.

Additionally, China's retail industry differs from America's in another way.

Two to three years ago, I conducted small surveys at various occasions: are HEYTEA and Luckin more like service industries, or retail? At the time, people felt HEYTEA was more service-oriented, especially its large city flagship stores with strong customer experience; Luckin was more retail-oriented — basically grab-and-go, or direct delivery.

Now a trend has become very clear: retail is becoming service-oriented, while services are becoming retail-oriented.

Therefore, if you've been doing pure retail, you need to consider how to add experiential dimensions across your product and sales chain. Supermarket brands are all striving to add service experiences to previously pure retail scenarios — whether opening large food courts in stores, or having chefs prepare king crabs on-site after purchase, everyone's experimenting with various service scenarios. Another FreeS portfolio brand, "Saturnbird" (三顿半), opened an offline experience space on Shanghai's Yuyuan Road, aiming to make consumption a comprehensive experience — no longer just drinking coffee, but holistically addressing users' flavor preferences, emotions, aesthetics, spatial experience, while communicating the brand's circular values.

Such business model fusion isn't very typical in America — for them, service is service, retail is retail. Though Starbucks emphasizes "service from the heart," it faces challenges before Chinese competitors who have pushed full-industry-chain digitalization to the extreme.

Corresponding to retail's service-ification is services' retail-ization. In services, the hardest part is efficiency improvement. Services are delivered by people — how to standardize management of people while requiring them to provide high-experience service is quite challenging. Digitalization is one viable solution path. Haidilao, for example, has done exceptionally well in restaurant retailization, supported by high-level digitalization and supply chain elasticity. While high digitalization is certainly important, services' retail-ization is also an inevitable trend amid China's intensely competitive market.

Giveaway

What do you think of China's consumer market in 2024, or what are your expectations for 2025? Leave a comment below — we'll randomly select 5 readers to receive the latest industry research handbook from the FreeS Fund team.

▲ eVTOL: China's Next Opportunity to Overtake on the Curve

▲ From "How the World Got Here" to "Where We Go From Here" | FreeS Fund 2024 Annual Investor Summit Recap

▲ Li Xiang x Li Feng: What Might We Experience in 2023? | Year-Ahead Outlook

▲ How We View the Consumer Market in 2023 and 2024 | Li Feng Column

▲ Li Xiang x Li Feng: Stripping Away Emotion, Discussing Second-Half 2023 Economic Variables | Li Feng Column

Star the FreeS Fund WeChat Official Account — timely business insights delivered to you