Jui Chan, BlueRun Ventures: Bidding Farewell to the Tumultuous Year of 2022, Anticipating the Next Decade of Sci-Tech Innovation

What we need to resist is the diminishing marginal returns of the Third Industrial Revolution.

Recently, Jui Chan, Managing Partner of BlueRun Ventures, delivered a keynote speech titled "Where Is the Next Decade of Sci-Tech Innovation Heading in an Economic Gear Shift?" at TMTpost's 2022 T-EDGE Global Innovation Conference.

2022 was a year of sudden, dramatic change, but it was also a footnote in a larger era of transition. When we find ourselves at a loss because it's difficult to give a comprehensive, accurate assessment of this year, we might pull the camera back to a more macroscopic view — at the tail end of the Third Industrial Revolution, what exactly are we experiencing? What logic will govern the next ten years?

In his speech, Jui Chan examined the present moment through the lens of having navigated multiple cycles over more than two decades. He also used specific case studies to unpack BlueRun's investment preferences in the hardcore innovation era that has already arrived — favoring companies with self-developed underlying technology, world-class products, interdisciplinary backgrounds, and global market orientation. Below is a transcript of Jui Chan's speech, which we hope offers some answers as 2022 draws to a close:

Hello everyone, I'm Jui Chan from BlueRun Ventures. Today I'd like to share some of my observations and thoughts on the theme Where Is the Next Decade of Sci-Tech Innovation Heading in an Economic Gear Shift?

Before answering this question, we need to understand the past, see what changes the present world is exhibiting, and then judge the future. BlueRun Ventures is an early-stage venture capital fund with an international perspective. Over the past two decades, we've been through many domestic and international cycles. Therefore, we often think about the underlying elements of cyclical change, and I personally strongly endorse analyzing the development patterns of the current world economy through the lens of the "technology-institution" paradigm transformation.

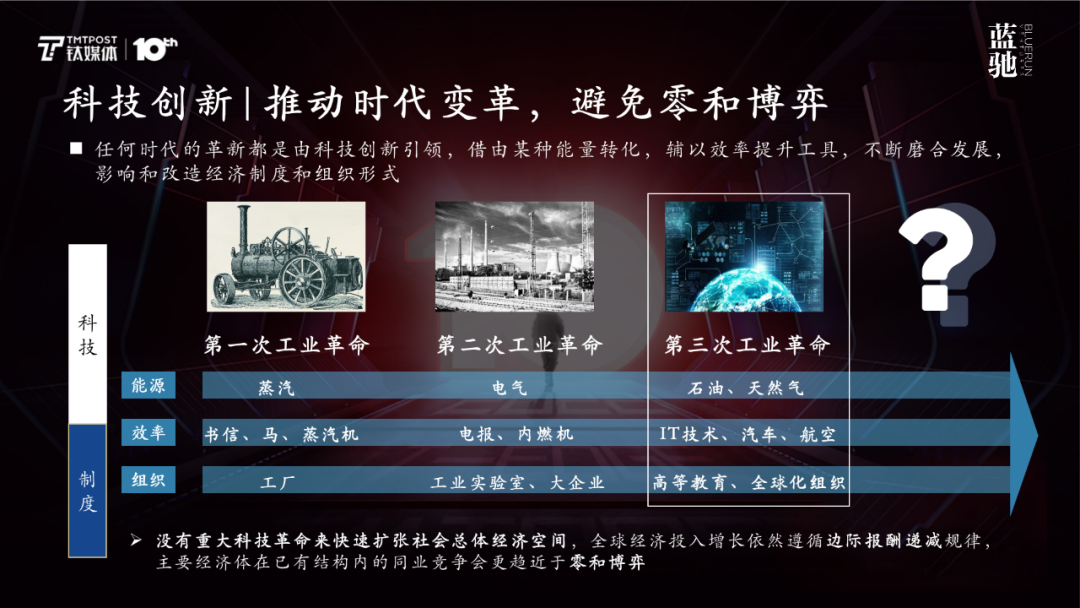

People often use the "economic long slope" to describe the transformation of modern industrial economies. It represents the most fundamental, most basic technological system in an economic society, along with its accompanying set of economic institutions. New foundational technologies will expand the overall economy of society, bringing new growth and new opportunities, while also challenging and influencing the institutional and organizational forms of today's economic society, impacting the technology and institutional paradigms of originally dominant countries, and creating opportunities for emerging nations to leapfrog.

Looking back at history, the steam era of the late First Industrial Revolution represented a stage where steam power served as the technological foundation, and this industrial technological system developed over half a century to constitute an economic system. Next came the Second Industrial Revolution, centered on electricity and steel. Electricity replaced steam as the primary energy source, production relied more on internal combustion engines than steam engines for transport power, and the telegraph became a new communications tool, improving the efficiency of information dissemination in the process. By the Third Industrial Revolution, oil and natural gas became the main energy sources, with automobiles and aviation serving as efficiency-enhancing tools.

From this we can draw a conclusion: the innovation of any era is led by technological innovation, which leverages some form of energy conversion combined with efficiency-enhancing tools, continuously磨合发展 [developing through磨合 — this phrase is awkward in Chinese too, meaning iterative refinement/adaptation], influencing and changing the forms of economic institutions and organization.

If we apply the above theory of technology and institutions to locate where the world stands today, how we find breakthroughs within the Third Industrial Revolution is the challenge we face next. We must compete for subsequent leadership based on the diminishing marginal returns of the Third Industrial Revolution. This means that in the positioning of macro-historical trends, we need to dig deeper into what the driving factors are, thereby discovering new opportunities.

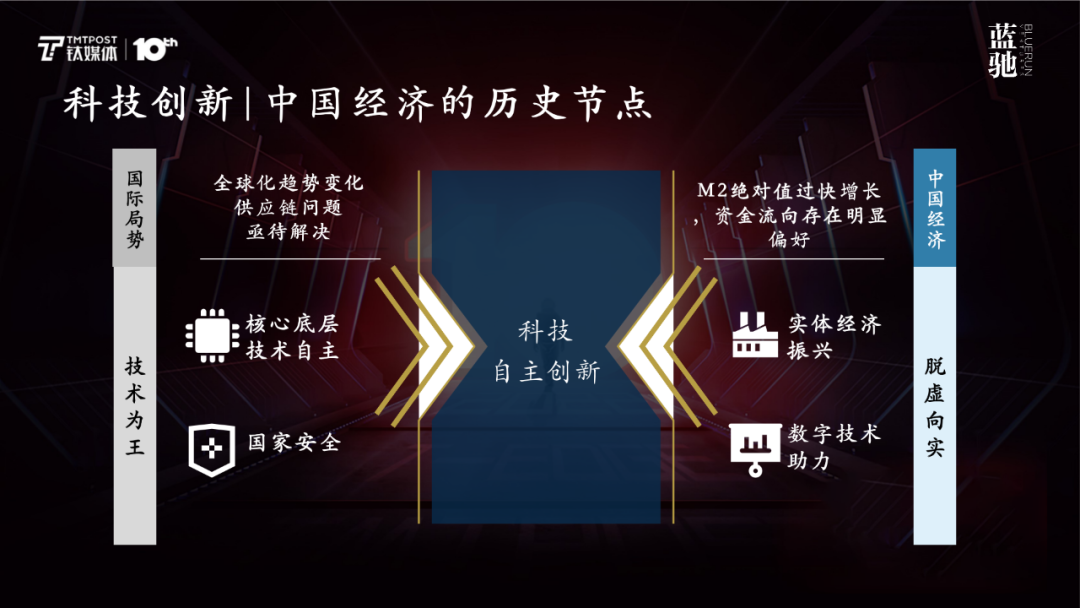

Based on the model I just introduced, BlueRun remains bullish on China and believes investing in China is the best choice. Three decades of reform and opening up have built two major advantages: first, talent reserves, and second, a strong manufacturing foundation. Although China's past development came through integration into the globalized system and cooperation with the United States and other Western developed countries, our market and technology were still "two ends abroad" [dependent on external markets and external technology]. To seek breakthroughs, we must pursue independent innovation in technology. We cannot continue using previous approaches to capture existing markets, or else we will face diminishing marginal returns from the Third Industrial Revolution.

China is actually in the midst of this transition. Recently we've also seen the state placing great emphasis on technological innovation, proposing development of the domestic circulation [dual circulation strategy], internationalization of the RMB, with a focus on revitalizing the real economy. This transition will necessarily be lengthy and challenging. I also want to emphasize one point: in an era of inflation and monetary oversupply, we must accumulate greater competitiveness in manufacturing, informatization, and other areas.

At the national level, there have also been quite a few new policies supporting technological innovation. The core point is to let everyone see the importance of technological innovation, and to see that regardless of geopolitical competition or market changes, the shift toward technological innovation is certain to happen.

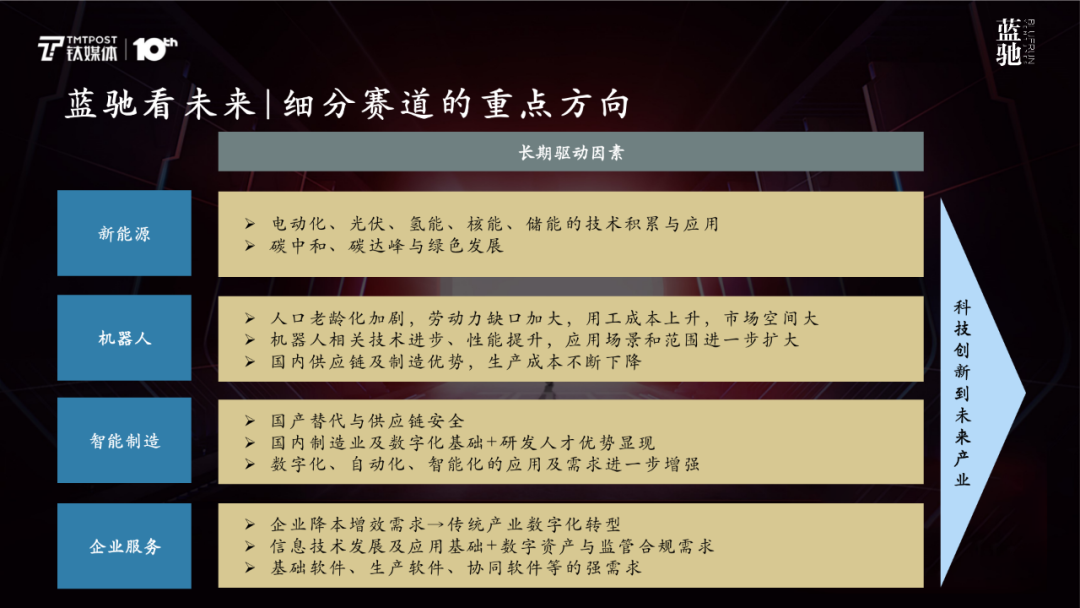

Next, from an investment perspective, let me talk about which sectors we should pay attention to. BlueRun believes there are four major sectors worth watching:

First is new energy. New energy is closely tied to carbon neutrality. As many of you know, there's photovoltaics, lithium batteries, hydrogen energy, and so on. Beyond these, more innovative energy technologies will emerge one by one in the next 5-10 years. These new energy sources, combined with upstream and downstream industrial elements, will create massive industries, so this is something we're very bullish on.

Second is robotics. Currently most of the world is facing the challenge of disappearing demographic dividends, which also means the aging problem will become more severe. How do we ensure productivity gains while maintaining or even further improving our population returns and wage returns? This definitely requires robots to replace some repetitive work, ensuring we can maintain or even increase productivity.

Third is intelligent manufacturing. After the Third Industrial Revolution, how do we ensure China still holds the advantage in technology and doesn't face the challenge of diminishing marginal returns? The domestic substitution and supply chain security we often mention are both important levers. Our country has consistently emphasized improving manufacturing quality and is committed to advancing toward high-end manufacturing.

Fourth is enterprise software, or enterprise-level services. As Chinese companies grow, coupled with accelerating internationalization, management can no longer rely purely on human labor. Impacted by the pandemic, enterprise digitalization and the electronification of upstream and downstream partners have become particularly important, which is closely connected to enterprise software.

Our fund began paying attention to the internet and mobile internet twenty years ago, and recently many of our projects revolve around new energy, intelligent manufacturing, robotics, and enterprise software to create new technological value.

I've just spoken about macro-level changes and sectors that investors should pay attention to. Now at the micro level, I've categorized several shifts:

First, we've seen that many startups previously built core competitiveness through data and operations. Going forward, core competitiveness should be research-driven, which is also driving the shift from model innovation to technological innovation. From an investor's perspective, this has produced different requirements for project attributes and founding teams, because founders who prioritize data and operations and founders who emphasize underlying scientific research and technology have completely different profiles.

Second, as we advance into the Fourth Industrial Revolution, whether it's electric vehicles, robots, or some highly innovative enterprise software, interdisciplinary capabilities are required. For example, an electric vehicle is software, hardware full of sensors, and also a consumer product. This means the barrier to innovation is rising, requiring founding teams with sufficiently diverse composition — no longer the single-background teams of the internet and mobile internet era.

Third, the shift from domestic market to global market: to create world-class products, internationalization strategy becomes particularly important. In fact, many members of new startup teams are post-90s generation. Compared to the previous generation of entrepreneurs, they have a more complete global vision, already factoring international competitors into their product strategy when building it.

Following what I just introduced, let me briefly introduce a few companies BlueRun has invested in, to give you more intuitive feel for what I've shared. First is Li Auto. Many of you have heard of this brand. Li Auto is a leading domestic new energy smart vehicle company with extremely strong product definition and R&D capabilities. Since product launch, it has ranked first in China for mid-to-large new energy SUV sales for multiple consecutive quarters. At the early investment stage, we were very bullish on Li Auto for three reasons: first, it aligns with the new energy trend I just mentioned; second, the team has excellent insight into user needs; third, product design is measured against international standards to ensure world-class product quality.

Another is Gaussian Robotics, a domestic robotics company with full-scenario intelligent cleaning capabilities, commanding 80% market share in China's cleaning sector and exporting to over 40 countries. Cleaning robots combine artificial intelligence, sensors, and multiple other technologies, along with insight into cleaning scenarios — it's entirely a new species, and it has its own supply chain, so costs can be made lower than machines that previously required human drivers. This is also an innovation, and one that can face the international market.

The third is Raymo Tech, which uses 3D printing technology to solve industry pain points in traditional manufacturing production molds, and is a company that integrates quality production capacity and reconstructs the mold industry landscape. We invested in Raymo at a very early stage. At the time, we were bullish on its deep insight into 3D printing technology, and at the same time, it also combines innovation in metal powder materials, significantly improving mold functionality while reducing costs. This innovation is also the interdisciplinary combination I mentioned earlier — materials science, hardware, 3D printing, intelligent manufacturing — so Raymo Tech has quite a few major domestic and international clients, including Apple, Huawei, and others.

Finally, I'd like to introduce Anxin Network Shield [安芯网盾]. They have developed China's first hardware-virtualization-based memory monitoring technology targeting enterprise clients' data security needs. In the past, much security software targeted the application layer. As enterprise software becomes more complex and diverse, many intrusions occur at the operating system and underlying hardware level. How to protect against these intrusions is what Anxin Network Shield aims to solve. Their clients include Huawei, Baidu, and some international clients.

These four cases share several characteristics: they all have self-developed underlying technology, products that reach world-class levels, interdisciplinary backgrounds, and are not limited to the domestic market but also have potential to face international markets. These dimensions map to BlueRun's criteria for evaluating projects.

The industrial changes of the past decade have been full of ups and downs, and at this moment we are in a gear-shift period of ecological reshaping. For the next decade, BlueRun will continue to adhere to a global perspective and deep insight, continuously supporting the vigorous development of technological innovation. Thank you all.

Originating in Silicon Valley, BlueRun Ventures was established in 2005 and is a venture capital firm focused on early-stage startups.

Currently, BlueRun Ventures manages multiple USD and RMB dual-currency funds in China, with assets under management exceeding RMB 15 billion, making it one of the largest early-stage funds in the country. Its investment stage focuses on Pre-A and Series A, covering hard technology and innovative interaction, enterprise technology, new consumption, and healthcare. It has cumulatively invested in over 150 startup enterprises, including Li Auto, Waterdrop, QingCloud, Guazi Used Car, Qudian, Songguo Mobility, Ganji.com, Energy Monster, Yuntu Semiconductor, Machenike, Cloud Saint Intelligence, Anxin Network Shield, BioMap, and others.

BlueRun Ventures has been ranked first in Zero2IPO's "China Top 30 Early-Stage Investment Institutions," first in ChinaVenture's "China Best Early-Stage Venture Capital Institutions TOP30," and was named among Preqin's Top 10 Global VC Fund Managers for Sustained High Returns.

Additionally, BlueRun Ventures has for multiple consecutive years received honors from Forbes China, 36Kr, Cyzone, Caixin Media, CBNweekly, Jiemian, and other media institutions, including "China's Best Early-Stage Institution of the Year," "China Top Venture Capital Institution," "Early-Stage Institution Most Welcomed by Entrepreneurs of the Year," and "Most Influential Early-Stage Institution of the Year."