Why Robotics Still Comes Down to China | BlueRun Ventures' Cao Wei at 36Kr WISE

China's robotics industry possesses distinctive advantages and unique characteristics.

At the 36Kr WISE2022 New Economy Kings Conference, Cao Wei, Partner at BlueRun Ventures, delivered a keynote speech titled Why We Firmly Believe China's Robotics Industry Is Entering a Golden Age, explaining the firm's logic for betting heavily on early-stage robotics startups since 2014. We hope this transcript will inspire entrepreneurs and industry professionals alike.

Good morning, everyone. I'm Cao Wei from BlueRun Ventures. Let me start with a quick introduction: we manage multiple USD and RMB dual-currency funds in China, with assets under management exceeding RMB 15 billion, making us one of the largest early-stage funds in the country.

Today I want to share why BlueRun firmly believes that China's robotics industry is entering a new golden age.

Why Robotics

Whether you're an investor or entrepreneur, everyone cares about one thing above all: the certainty of long-term value. Compounding matters — putting in five or ten years of steady effort in one direction and earning commensurate returns.

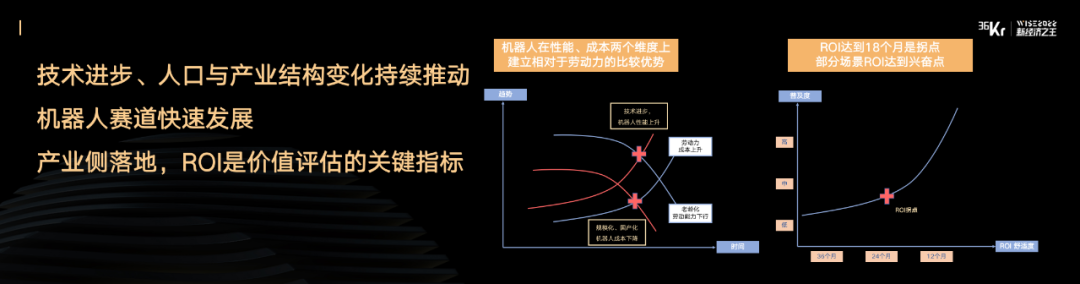

When we first began investing in robotics, we conducted foundational research on macro variables. Globally, not just in China, we found that robots are steadily building comparative advantages against traditional labor across two dimensions: performance and cost.

On the labor side, several long-cycle drivers are pushing costs up: demographic shifts, declining birth rates, and external shocks like the pandemic have all contributed to steady increases in labor costs.

On the technology side, robots' operational capabilities keep improving. Meanwhile, thanks to China's manufacturing scale and mass production, costs are falling rapidly. Looking at 10, 20, even 50-year horizons, the external variables driving this sector have remarkably stable certainty. This is a sector worth committing to for the long haul, for both investors and founders.

Beyond sector logic, robotics has another distinctive feature: robots are universal super-tools applicable across an enormous range of industries and scenarios. With such complexity, timing your investment becomes its own challenge.

We began tracking robotics in 2014, conducting extensive offline demand-side interviews in 2015 and 2016. What we learned early on was that customers viewed robots as super-tools — making ROI absolutely critical. For mid-to-large enterprises, an 18-month payback period generally falls within their comfort zone. For smaller buyers, 12 months tends to work better.

So when we evaluate robotics as a whole, we apply two models: first, assessing long-term value certainty; second, determining optimal timing amid countless scenarios. I share these two frameworks to help you understand why, as a leading domestic early-stage investor, we devote such sustained attention and resources to robotics.

Why China

Robotics is a long-term bet globally. But what gives China distinctive advantages? Let me break it down across several dimensions.

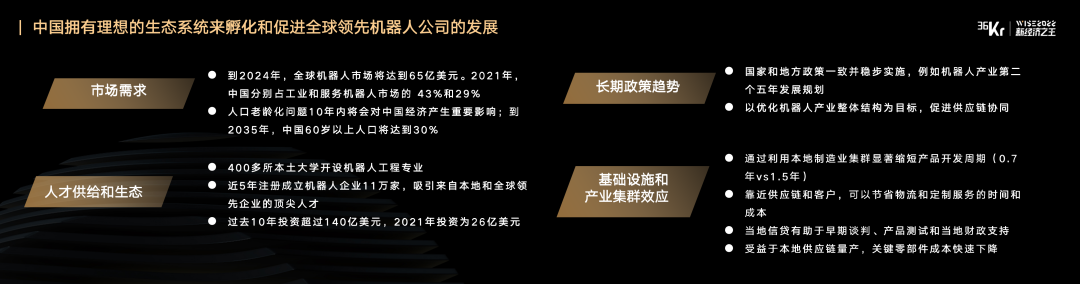

From the demand side, China's market is unique — it is simultaneously the world's largest robotics production base and largest consumption base. China accounts for 43% of global industrial robot purchases and 29% of service robot purchases. As a major manufacturing power, China faces severe demographic headwinds: by 2035, over 30% of the population may be 60 or older, creating enormous pressure on labor supply.

From a policy perspective, national and local governments alike have developed implementation roadmaps for industrial automation and intelligence, from macro frameworks down to granular targets — all with explicit timelines and concrete goals. Compared to other regions, China offers a uniquely founder-friendly, ecosystem-friendly external environment.

On entrepreneur community vitality: over 400 undergraduate institutions now offer robotics engineering programs, growing at more than 10% annually. Over the past decade, robotics-related investment has exceeded $14 billion, with $2.6 billion in 2021 alone. In the last five years, roughly 110,000 robotics companies have been registered.

Finally, China has excellent industrial clustering. Whether in the Yangtze River Delta, Pearl River Delta, or Beijing-Tianjin-Hebei region, these clusters provide startups with superb upstream and downstream business environments — access to customers, supply chains, local financing, product testing cycles, and more. All of these advantages ultimately translate into faster iteration and better product quality.

This echoes 36Kr's conference theme: we firmly believe China has an ideal ecosystem to incubate and propel globally leading robotics companies.

Underlying Technology and Scenario Innovation

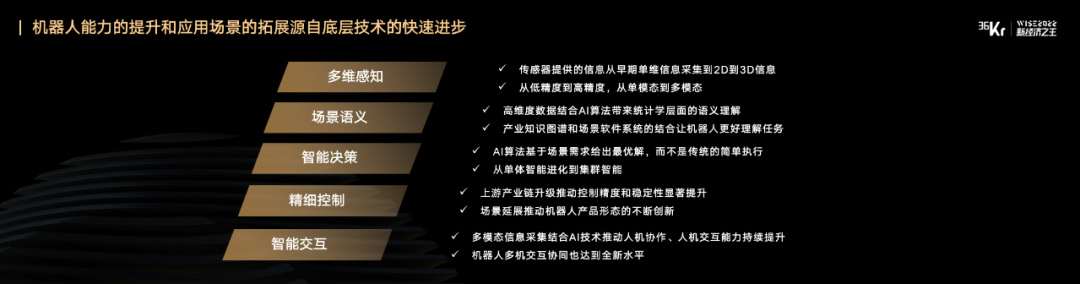

Next, let me share how BlueRun thinks about robotics. We believe that as intelligent agents, robots are fundamentally shaped by core underlying technologies. Advances in these technologies drive performance improvements, which in turn unlock commercial value by addressing scenario-specific pain points. And it all starts with technology and product innovation.

Robot capabilities break down into perception, decision-making, fine control, and interaction. In perception, we've progressed from single-modal to multi-modal sensing, from traditional 2D to 3D perception. In control, we're extending from traditional rigid arms to soft arms and novel interaction forms. In intelligence, beyond single-robot intelligence, we're increasingly seeing cloud-based swarm intelligence. These are all areas entrepreneurs and industry participants should watch closely. The key question is: is your work genuinely driven by underlying technology, and does that drive create scenario-specific value innovation? This is crucial.

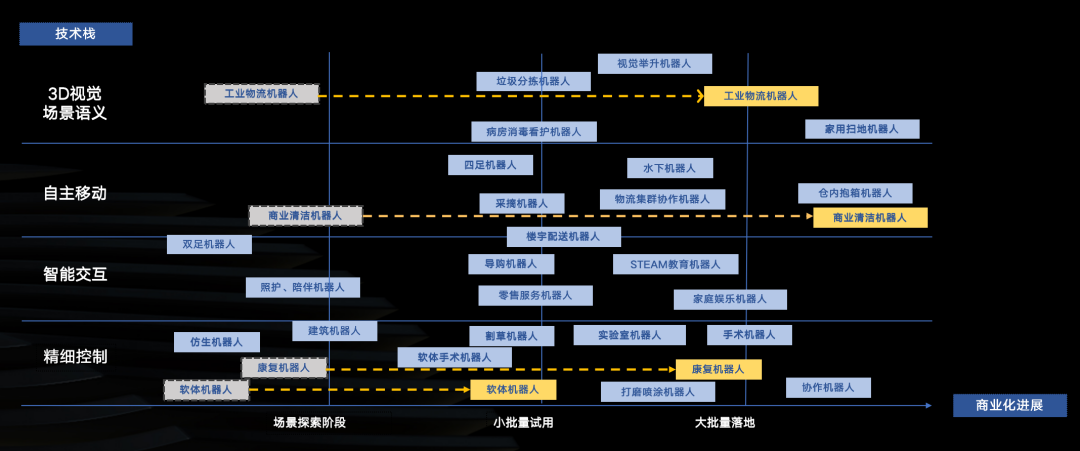

Here's our industry radar for tracking the sector. We've divided robotics deployment into three phases: scenario exploration; small-batch piloting; and large-scale deployment.

Note the highlighted examples. Gaussian Robotics, which we invested in back in 2018, had only a product prototype and no commercial revenue at the time — squarely in scenario exploration. Different companies choose different scenarios; Gaussian chose commercial cleaning. After roughly four to five years, it has become the dominant player in its vertical, with annual revenue exceeding RMB 1 billion, products sold across 40 countries and regions, and extensive service scenario coverage.

Another portfolio company, soft robotics startup Wanxun Technology, represents a fascinating, cutting-edge direction. Unlike commercial cleaning robots, it remains in the lab-to-small-batch-piloting transition phase.

This map helps illustrate different robotics products: which capabilities matter most, what phase you're in, how to staff accordingly, how to build relevant business capabilities, and how to capture market opportunities.

Our core takeaway — regardless of robotics category: your understanding of scenarios, pain points, and technical bottlenecks, combined with mastery of underlying technology, will enable you to define innovative products. I hope this framework offers some food for thought for entrepreneurs working across robotics scenarios.

Who Can Define Innovative Products

Finally, with sector and industry logic clarified, I want to share what we believe high-potential robotics entrepreneurs should bring to the table.

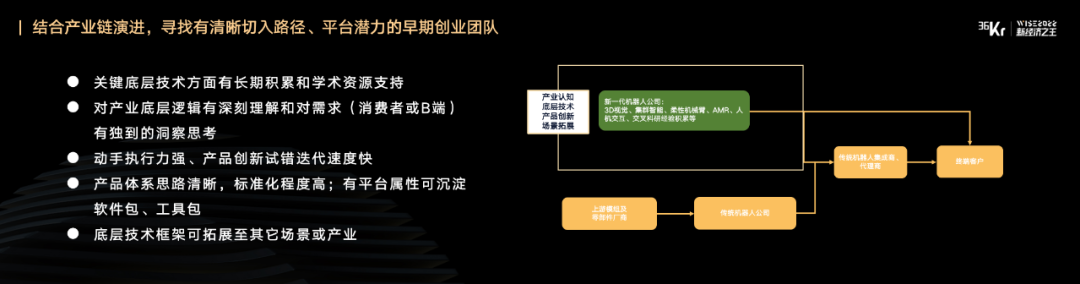

At the most basic level, since this is technology and product-driven innovation, we look for teams with deep, long-term accumulation in underlying technology — whether academic or at the hardware module level.

Second, robots are super-tools that must embed in industries. Beyond robotics specialists, having industry experts on the team is critical. These experts genuinely understand industry fundamentals, with deep insight and independent thinking about sector pain points. When technical talent and product/demand-side talent combine, maximum energy gets released. Only the collision of technical and industrial thinking produces great products.

Another distinctive feature of robotics entrepreneurship: it involves complex software-hardware integration, so teams need strong hands-on execution capabilities. Software innovation cycles are relatively short, but hardware cycles are slower, so execution must be strong enough to enable rapid product iteration.

Two more points: first, product strategy and thinking must have medium-to-long-term perspective, not just short-term focus. Second, platform attributes and technical accumulation need structured frameworks, so that products and technologies can extend from initial scenarios to new innovative scenarios — enabling you to become a platform company with truly unique, core underlying technology.

That concludes my presentation. Let me summarize briefly:

We are deeply bullish on robotics and its deployment across industries. We hope to see entrepreneurial teams with sufficient accumulation in underlying technology, making sustained innovations and product iterations around scenario pain points. We also hope entrepreneurs and industry chain partners will find opportunities to collaborate. Let's build from zero to one, redefining future technology and life together.

Founded in Silicon Valley in 2005, BlueRun Ventures is an early-stage venture capital firm.

Currently managing multiple USD and RMB dual-currency funds in China with over RMB 15 billion AUM, BlueRun Ventures is one of the country's largest early-stage funds. It focuses on Pre-A and Series A investments across hard tech and innovative interaction, enterprise technology, new consumer, and healthcare sectors, with over 150 portfolio companies including Li Auto, Waterdrop, QingCloud, Guazi.com, Qudian, Songguo Mobility, Ganji.com, Energy Monster, Yuntu Semiconductor, Machenike, Yunsheng Intelligence, Anxin Network Shield, and BioMap.

BlueRun Ventures has been ranked #1 on Zero2IPO's "Top 30 Early-Stage Investment Institutions in China" and ChinaVenture's "Top 30 Best Early-Stage VC Firms in China," and named among Preqin's Top 10 VC Fund Managers Globally for Sustained High Returns.

The firm has also received consecutive honors from Forbes China, 36Kr, Cyzone, Caixin Media, CBNweekly, Jiemian, and other media outlets, including "China's Best Early-Stage Firm of the Year," "China's Top Venture Capital Firm," "Most Entrepreneur-Friendly Early-Stage Firm of the Year," and "Most Influential Early-Stage Firm of the Year."