The Road to AGI | BlueRun Ventures' AGI Investment Thesis Updated to Version 2.0

Six takes, posted here for the record. Subject to revision.

In the first half of last year, BlueRun Ventures launched its "The Road to AGI" series, publishing multiple installments that mapped out possible futures for the GenAI era and articulated the firm's AI investment thesis: the triple wave of AI + new interfaces + robotics would catalyze an entirely new age. To date, BlueRun Ventures has executed on this vision across the board:

Over the past year, we've worked alongside the most exceptional founders to sketch the contours of GenAI, experiencing the fiercest battles from the front lines. Our investment thesis has continued to evolve and sharpen in the process. GenAI is still accelerating; the war has yet to reach halftime. We hope to share these reflections with founders at this moment to spark more discussion and accelerate evolution.

There has been much debate recently about open source versus closed source, and whether to build models or applications. Here are our conclusions:

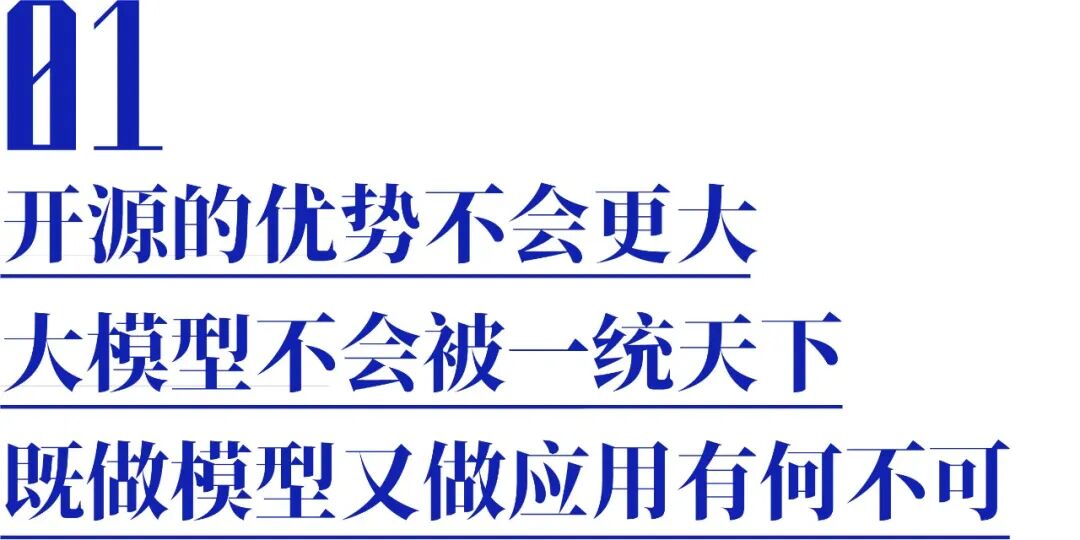

First, models must be affordable to be viable. Therefore, building smaller, verticalized models on top of open-source foundations is an inevitable trend.

But for the commanding heights of AGI — such as logical reasoning capabilities, multimodal models, and video generation — the closed-source trend will likely persist. Even when open-sourced, the crucial "how" — how the model is trained, the configuration of key parameters — will remain undisclosed, making replication impossible for latecomers. Failure to invest aggressively and promptly risks falling behind in the race.

Many draw analogies between large models and operating systems; we disagree, because the two are fundamentally different. An operating system is fundamentally a technology, but for large models, the model is the application, and its iterative development accumulates data. Over the long term, truly general models capable of AGI will be extremely limited, while industry-specific models tailored to different scenarios will flourish. Meanwhile, due to cultural differences, geopolitics, and other factors, different countries may develop their own large models.

We believe the strategy of building both models and applications is logically sound. Only by continuously collecting user feedback and accumulating applied model practice can founders develop deep understanding of their model requirements and how to iterate on them. Today's models are increasingly data-driven in nature; merely opening APIs to external parties makes it difficult to form a user feedback loop — far less efficient than simultaneously building applications like Kimi Chat.

The paths to building foundation models are diverse. Just as there are different ways to build cloud platforms — Amazon first developed a certain market scale through Amazon.com, constructing AWS capabilities in the process before exporting them externally, while other tech companies built cloud platforms directly and exported capabilities to customers — the first path may prove more effective for the China market. When a company has business demands and data feedback, it understands better how infrastructure should be built.

Last year we proposed making money, earning data, and gaining knowledge simultaneously. This year, building data flywheels has become market consensus. We advise founders to further upgrade their understanding of data: pay more attention to data processing and multimodal data.

Three critical layers of questions deserve attention on the data front: 1) Have you secured massive public-domain data or unique private-domain data? 2) Can you identify data that helps models learn continuously and iterate at high quality? 3) Can data be properly enhanced to build higher-quality data structures?

The hardest part isn't collecting data — it's processing it. For startup teams, the ability to filter and process truly scenario-appropriate, high-quality data represents a combined test of technical capability, model understanding, and scenario comprehension. This can ultimately lead to differences of two to three orders of magnitude in training data.

At a higher level, we believe three questions merit careful founder consideration: Does intelligence grow along data, or does data grow along intelligence? What are the respective characteristics of incremental new data versus existing old data? How should scenarios for new data generation be prioritized?

In the internet era, humans processed data in two-dimensional space. But if we view the world as a model, data should not be limited to text. What data underpins Sora and Gemini? What data underpins Li Auto's autonomous driving, Apple Vision Pro, and DJI? From a spatial perspective, perhaps less than 5% of this world has been digitized; how should the remaining 95% be digitized, and at what speed?

BlueRun believes that in the AI era, the acquisition and processing of three-dimensional spatial data will be fiercely contested terrain. This multimodal data will give rise to new super-applications — ones that may no longer live on phones, but instead emerge from the combination of new interfaces and embodied intelligence execution terminals.

This is one reason OpenAI invested in Figure. In the embodied intelligence track, BlueRun Ventures made early investments in AgiBot, GalaxyBot, and other projects.

Based on accumulated insights, BlueRun's underlying logic for tracking AGI is: the triple wave of AI + 3D interaction + robotics, with Web3 as auxiliary. The three waves are essentially three technology drivers, corresponding to different spaces and execution capabilities. Apple Vision Pro's spatial computing and the previously discussed metaverse, when reduced to first principles, represent 3D interaction — a new generation of interfaces — while robotics encompasses embodied intelligence plus execution structures.

In the mobile internet era, applications captured the lion's share of the market, with compute and infrastructure representing a smaller slice. Because the internet's capability was "connection," value had to be delivered through applications: connections between people spawned social apps; connections between information spawned search. But in the GenAI era, the foundation layer commands a larger share, because its capability is "generation" — creating value that is larger and more direct than the internet's.

Meanwhile, GenAI's long tail may prove even more fertile, because each small unit along that tail can create value independently. Take the To B market: for the longest time, highly fragmented scenarios and dispersed data meant numerous personalized needs went unmet. But GenAI may be able to aggregate these niche demands behind a single entry point. The AI Agents, AI Native applications, and Copilots under discussion are all fundamentally AI-powered applications that will dramatically enhance individuals' ability to solve problems autonomously.

We anticipate that as GenAI broadly empowers individuals, business model innovation will follow, and we'll see an increasing number of one-person billion-dollar companies emerge.

Over the past two decades, high-end service industries like law, medicine, and education have seen relentlessly rising costs, constrained by insufficient supply of top talent. But GenAI opens the possibility of "doing more with less": as companies gradually reduce reliance on human labor, the unit cost of value creation drops precipitously. This will catalyze a new generation of companies — no longer software firms empowering vertical industries, but AI model-driven industry players themselves.

For example, an entrepreneur today wanting to build a SaaS company serving retail must first hire people to develop software, then sell the product to retail companies. But in the future, product development may be handled by code generation tools, system maintenance delegated to AI — effectively, the company employs a workforce of retail digital workers. The enterprise itself becomes a retail company, not a "software company empowering retail."

First, choose data-rich scenarios — primarily those with context, or those not yet digitized.

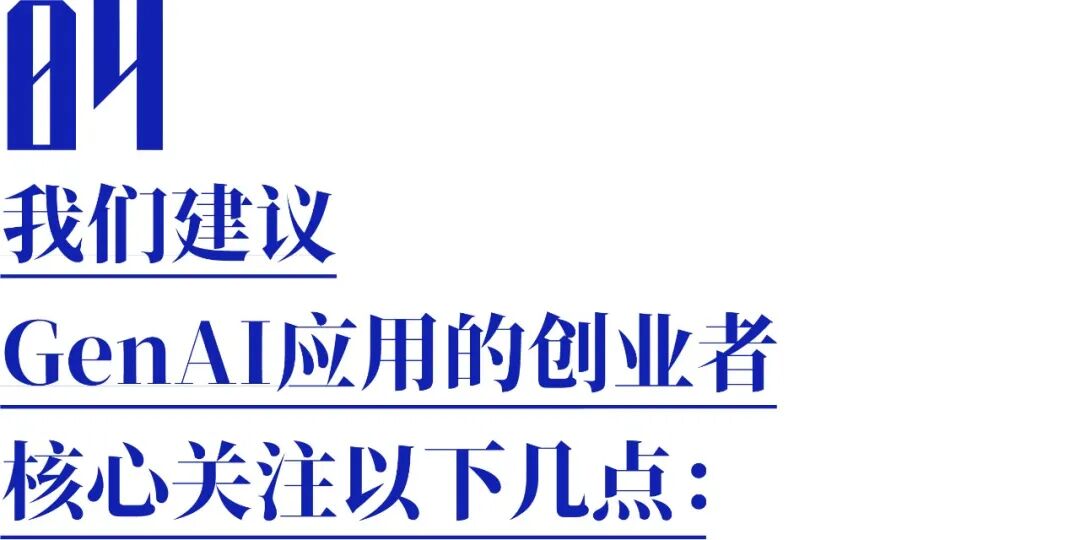

Second, make money, earn data, and gain knowledge simultaneously to form a data flywheel. For founders, the first hurdle is achieving product-market fit, but PMF in the GenAI era differs from before. At this stage, product definition must be grounded in technical constraints. Founders who either fail to understand the technology or over-define their product risk being eliminated instantly. Founders must consider: for the relevant technical category, does scaling law apply / still apply? Where is the technical ceiling? What fundamentals will not change with technological iteration? Based on these technical assessments, founders must make key decisions: what technology to adopt? Whether to chase the technical ceiling or capture the technical floor? How to iterate?

Thus, AI-savvy product managers are precious during the PMF phase of GenAI products. The feedback mechanisms they construct must enable users to generate further data through usage — this is ultimately what builds moats. These individuals have typically experienced several waves of AI technology iteration, participated in model training and alignment during GenAI's development, and attempted to build products from zero to one based on AI capabilities.

Third, focus on cost reduction. On the model front, founders must understand the core capabilities of different models and how to efficiently and cost-effectively match differentiated model capabilities to appropriate scenarios. At the same time, leverage the data flywheel formed through PMF to increase revenue. Believe in large models' scaling law, but also believe in the rapid pace of cost reduction. So founders must consider: under the new Moore's Law, what should their business model look like in two to three years?

To C and To B products should hit different milestones at different stages. Our thinking is as follows:

To C Products

[Exploration] Have niche scenarios and niche features; achieve retention and payment from core users

[Validation in Progress] Layer on top of existing scenarios and features; generalize user base; revenue covers model inference costs

[Validated] Product and scenarios converge; user scale grows exponentially; customer acquisition costs drop substantially

To B Products

[Exploration] Have product, have scenario, small number of trial customers; continue to explore broadly

[Validation in Progress] Have product, have scenario, small number of paying customers; attempt convergence, continuous customer success

[Validated] Product and scenarios converge; have commercialized customers, have scaled revenue (upscale from customer renewals), have some renewal customers

While geopolitics will remain an unavoidable theme, AI entrepreneurship requires a global perspective from day one. We must continuously absorb global knowledge, bring in world-class talent and resources, and observe all countries — including the United States and China — with an unbiased, neutral, pragmatic lens, weighing their pros and cons to think through our own opportunities, challenges, and how to navigate this landscape. We can think openly: whatever challenges China faces, what are its comparative advantages? Whatever lead the United States holds, does it have an Achilles' heel?

Thus, as we consider the next phase of AI applications, another important question arises: where will markets expand next. Whether Chinese or overseas founders, one must find one's position and capital market exit within the global landscape. BlueRun has always examined China's comparative advantages from a global perspective. Building on years of deep roots in China, we hope to create opportunities for AI founders to become global top-tier companies.

We believe the model capability improvements driven by scaling law are far from reaching their limit, and we can continue pushing forward along this path. While some worry about data scarcity, in reality vast quantities of data remain untapped for model training — private-domain data, and more importantly, physical data. Both categories will unlock further possibilities for models.

Some academics and founders are exploring AGI through smaller, edge-side models. We believe this path does not contradict scaling law — it aims to achieve steeper intelligence improvement curves at lower cost and faster speed. It's as if we've discovered an alchemy furnace that produces results, and now want to run it more efficiently.

This path severely tests team capabilities, touching on the data processing and selection, hyperparameter configuration, and other factors discussed above. We believe the difficulty of this route will gradually increase; as noted earlier, publicly available information about high-end model training will only diminish, making replication and fine-tuning progressively harder.

As investors, we maintain an open mind and stay attentive to possible alternative paths. Humanity's exploration of AGI remains in its early days, and the emergence of new approaches cannot be ruled out.

The Road to AGI | AI + 3D Interaction + Web3: The Triple Wave Ignites a Productivity Revolution

The Road to AGI | With Large Model Support, Robotics Approaches a New Generation

Zhilin Yang: Advancing Toward the Unknown Snow-Capped Mountains | BlueRun Ventures Family Spotlight