Jui Chan, BlueRun Ventures: Why We Started Laying the Groundwork for Golden Tracks a Decade Early — And It Wasn't Luck

Where will venture capital opportunities emerge over the next decade?

Where will China's venture capital opportunities emerge over the next decade? Recently, Jui Chan, managing partner of BlueRun Ventures, was invited to serve as a mentor for the ninth cohort of Zero2IPO's Sandhill Institute, where he drew on ten years of industry experience and two decades of early-stage tech investing across China and the United States to share his thinking on technological innovation. With tech investment themes shifting every two to three years, how do investors maintain the capacity for renewal and avoid missing important opportunities? We've edited and shared his remarks below — we hope you find them illuminating.

I spent eight years in Silicon Valley and have been investing in China for over a decade, so I'll approach this from three perspectives: the US perspective, the China perspective, and the industry perspective.

After all, Silicon Valley is the birthplace of venture capital, and learning their methods and experience matters; at the same time, China has its own development trajectory and style, so what's more important is applying what we learn in a grounded way; additionally, investing needs to be closely tied to industry — especially since venture capital combines financial and industrial attributes — so the industry perspective is equally crucial.

01

The Hard KPI of Venture Capital:

Nailing Technological Innovation

Eight Years in Silicon Valley: Witnessing, Participating, Learning

I'm Singaporean, and spent nine years developing my career in Asia-Pacific and Singapore. IBM was my first job, where I was responsible for PC products. Later at Singtel, I mainly worked on internet services and wireless network services.

In 1999, I came to Silicon Valley and joined what was then Nokia Venture Partners — BlueRun's predecessor, which later rebranded and became independent. Those were exactly the years when the internet began surging.

When Netscape launched its browser in 1994, the internet's enormous potential opened the world's eyes. Because of that browser, great companies like Amazon, eBay, Yahoo, and Google later became possible.

While in Silicon Valley, I was fortunate to participate in several significant projects. Among them was PayPal, the earliest online payment system.

When the US internet bubble burst in 2001, PayPal was one of the few internet companies that survived. Companies like Yahoo and Amazon, having been founded earlier with mature foundations, didn't collapse. But PayPal was still a growing company, yet it survived.

A key reason it survived was that the company had two exceptional founders: Peter Thiel, the renowned American investor who wrote Zero to One: Notes on Startups, or How to Build the Future; and Elon Musk, now widely known as the "real-life Iron Man."

Peter Thiel built PayPal; Elon Musk built X.com. They anticipated the crisis before the bubble burst, merged the two companies, and survived. In 2015, PayPal spun off from eBay and went public independently; it's now worth nearly $100 billion.

So we see that the risks of tech entrepreneurship are extremely high, but when done well, it creates genuine value.

Later we also invested in Coupa, a famous American SaaS company; and Waze, which used user apps to provide location information and build maps — the earliest navigation software with social features.

Why mention these three companies? Their concepts were quite ahead of their time. PayPal was founded in 1999 and went public in 2003; we didn't get Alipay until five years later. Coupa was founded in 2006 and listed on NASDAQ in 2016; it was another five or six years before the SaaS concept emerged in China.

Objectively speaking, the United States is still ahead of us in many areas of technological innovation.

Doing Venture Capital Requires Strong Metabolic Capacity

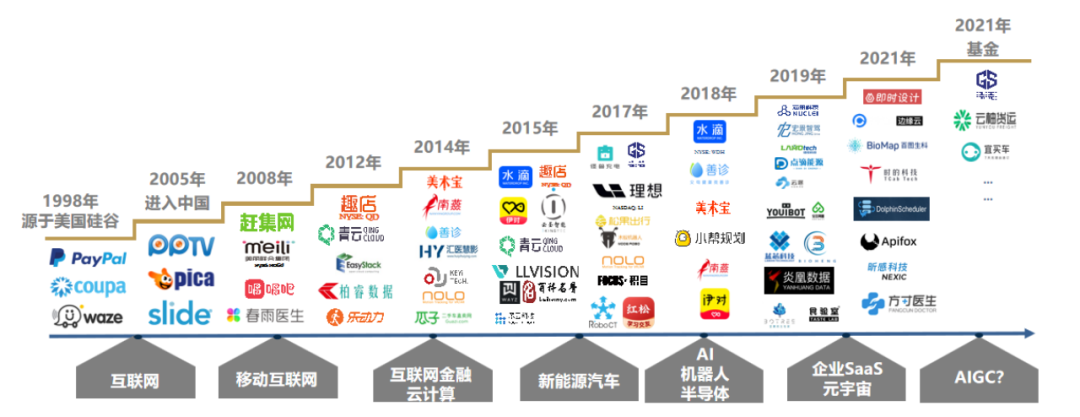

In 2008, I assembled the BlueRun China team, and I've been here ever since — 15 years now. We've invested in over 100 companies, with fund management exceeding RMB 15 billion. As early-stage investors, we've led over 90% of our deals.

At first, we brought new technologies and ideas from the US. Our very first investment was a semiconductor company, but back then hard tech and chips weren't as hot as they are now, talent was scarce, and the company ultimately didn't develop well — the timing was simply too immature.

BlueRun Ventures Investment Timeline

From internet to mobile internet, internet finance, cloud computing, then new energy, AI, then SaaS, metaverse — tech investment themes shift every two to three years, and we've captured exciting projects in every wave, many of which have gone public. The challenge for investors is considerable: you need very strong metabolic capacity to continuously keep up with technological revolutions.

Much Technological Innovation Originates from Marginal Demand

Much technological innovation starts out extremely marginal, attracting little attention.

I remember around 2013–2014, when we were researching new energy vehicles, I asked classmates who were executives at Mercedes-Benz or BMW whether they saw opportunity in NEVs.

Their answers were all "impossible, very difficult, the market is too small." In Europe only dozens were sold; in China, BYD was selling just a few hundred. Battery range was barely 100 kilometers, hardly anyone was buying them — there seemed to be no hope. Even in 2016, when we invested in Li Auto, there were still many voices of incomprehension.

So why did we persist with new energy vehicles? I think a crucial point was returning to demand.

Traditional investing may focus more on current revenue and profit, without needing much future projection. But tech investing requires projection. The demand at that moment may have been marginal, but the key question is whether that demand will evolve over five or ten years.

When we invested in Ganji.com, many people around me didn't understand it — they thought nobody used the site, that it was crude and unattractive. But my judgment was that this site wasn't aimed at executives and elites at all, but at migrant workers and young people coming to big cities to find jobs, housing, and cheap secondhand goods. There was actually a huge market.

So to do tech investing well, you must maintain enormous curiosity, not underestimate marginal demand, and be able to detach from the influence of people around you to understand the real market situation, continuously project, and make independent judgments.

Warren Buffett has a saying, roughly meaning that when everyone reaches consensus, the returns on that project will regress to the mean. So to make serious money, your view must differ from others'. When many people dismiss something as just a trinket, that's when you should pay attention instead.

Building Foundations, Chasing the Frontier: A Long Road Ahead

For the past decade-plus, China has basically been learning from abroad. Why did this work? Because it was the shortest path, the fastest speed — it didn't require much innovation, just good localization to achieve strong results; plus it could fully leverage China's enormous demographic dividend. So investors and entrepreneurs naturally chose the shortest path.

Another important point: Copy-to-China projects were easier for US investors to understand.

But now, the world has changed.

First, the mobile internet traffic dividend has disappeared. I still remember when we started investing in mobile internet in 2009, customer acquisition cost was just RMB 1 per user; now it's over RMB 100, making cost coverage very difficult.

Second, US capital markets' attitude toward Chinese concept stocks has also shifted.

We divide tech investment into three layers: underlying technology, applied technology, and frontier technology.

China has always been particularly strong at the middle application layer. But our investment in underlying technology development and frontier technology R&D has been insufficient. So once we get choked at the neck, problems multiply — relying solely on the middle application layer cannot achieve sustainable development.

Whether investors or entrepreneurs, everyone should push toward hard tech to break through the current predicament.

02

The Era of Hardcore Independent Innovation

What Are the Golden Tracks

Now that China has entered the era of independent innovation, there are still many advantages.

First is the engineer dividend. Many universities now have corresponding talent cultivation programs, and many outstanding overseas talents are returning to China. Overall, while there's still some gap in talent quality compared with developed countries, China is working hard to catch up, and has clear advantages in quantity.

Another point is that China has built relatively strong infrastructure over these two decades, including logistics, factories, and so on — what we in venture capital like to call supply chain advantages — with accelerated urbanization, improved public services, and optimized business environments all supporting this advantage.

Over the past five years, national policy has also provided substantial support. On industry policy, there's strong support for real economic development, moving from virtual to real; on macroeconomic policy, many national funds have begun deploying into technology, advanced manufacturing, and other investments. When we do early-stage investing in strongly innovative companies, they later need continued financing and will also take strategic national funds — this is quite helpful for startups.

Of course, many fields and sub-tracks simply have enormous markets in China.

Four Promising Tracks for the Future

- New Energy

New energy isn't just about electric vehicles and photovoltaics — opportunities exist throughout the entire chain.

For example, 90% of EV components are imported, especially power semiconductors with very high demand — there's definitely opportunity there.

Beyond passenger cars, many commercial environments have different vehicles: mining trucks, port cargo ships — these will all become electrified, creating many investment opportunities.

New materials R&D that can help new energy be used more stably, safely, and efficiently is also something many investors and companies are examining.

Beyond that, new energy production, transport, storage, including recycling — these are all tracks with strong development prospects within new energy.

- New Efficiency

New efficiency can be understood as the deep application of everything that can be digitized, automated, and intelligenized.

More and more scenarios and services in our lives will be transformed by artificial intelligence.

In manufacturing, for instance, increasingly simple repetitive labor will be done by robots. This is closely related to demographic structure — population aging is a trend, and fertility rates are declining.

Currently, many Chinese enterprises still have digitalization rates below 10%, so future development space is large.

Also in services, logistics — dispatch algorithm platforms, logistics robots; and of course, applications in biomedicine. These are all future development trends.

- New Interaction

Regarding new interaction, a superficial understanding is that optical technology and rendering computing power continue strengthening, dramatically improving VR and AR experiences.

But a deeper understanding is that the deep development of human-machine and machine-machine interaction will support new applications, new scenarios, satisfy new demands, and even advance new industrial revolutions, forming new economic models.

When you first encountered a PC, didn't you find the keyboard interesting? Later came the mouse, and the feeling was different; when you first touched an iPad, the touchscreen was exciting; more recently with the wildly popular ChatGPT, many people have already tried it personally — it can chat, write programs, suddenly pushing interaction to new heights.

- New Science

At bottom, whether making next-generation robots or next-generation new energy, all technological breakthroughs originate from underlying innovation. So we need to pay special attention to where underlying science and frontier technology intersect and concentrate — these fields and tracks will definitely be full of opportunity.

And innovations must be implemented in applications and commercialization — things we often discuss lately like brain-computer interfaces, controlled nuclear fusion, these will also see major development in the future.

What Kind of Venture Team Will Be the Mainstay of the Future

There's certainly no shortage of excellent talent, but to achieve genuine innovation breakthroughs, what we need more are entrepreneurs with outstanding innovation capability, international vision, and long-term perspective. Because innovation in these fields may require enduring hardship for ten or twenty years — completely different in nature from traditional business.

We're finding that China's innovative businesses are increasingly shifting from data and operations model-driven to research and technology-driven. Correspondingly, startup teams have shifted from internet entrepreneur-dominated to being led by serial entrepreneurs, professors, scientists, and algorithm experts.

Many tech domain companies, to develop rapidly, need far more than one or two hundred million yuan — some projects need at least RMB 1 billion in the first round. Only serial entrepreneurs have the ability to integrate various resources and sufficient industry knowledge; otherwise, investors will find it hard to invest with confidence.

At the same time, everyone will find that innovation and entrepreneurship focused solely on the domestic market is no longer enough. Internet development previously relied relatively heavily on local culture, but now developing underlying technologies like AI, hard tech, and new energy all require considering international markets and having sufficient competitive strength globally.

Let's take the OpenAI team as an example. Their team has many people who understand underlying computing power technology; many mathematicians who deeply understand data model construction — essentially a very strong team supporting algorithms and data, with intelligence built on these foundations; on the capital side, they may have raised several billion dollars, persisting all the way to reach where they are today.

So the current market situation places higher demands on investment teams as well. Previously, teams only needed to connect with internet talent and have people who understood applications, able to communicate with these talents. Now teams need industry experts who also understand different technologies, with interdisciplinary knowledge reserves.

For example, on our team, we have several PhDs who know robot and new energy equipment parts inside out, while also understanding software, applications, and logistics; several others with deep expertise in computing power and algorithms. This is how BlueRun's team has continuously upgraded and iterated over these dozen-plus years.

This also shows that whether in entrepreneurship or investing, having just one skill is no longer enough.

Hard Tech Investment

Finding the Right Entry Point Amid the Boom

For case sharing, I'll focus on pre-investment thinking and research — this should be more valuable for everyone.

Gaussian Robotics. Around 2016–2017, through researching various industry data, we inferred that the demographic dividend was about to disappear, aging was rising rapidly, and around 2023 there would be a crossover point where fertility rates fell below mortality rates — you've probably seen related reports recently; our inference from five or six years ago has now been confirmed.

This conclusion made us realize that supply of low-end labor would definitely experience cliff-like decline.

Following the same logic, we believed that AI should also be applied in low-speed scenarios. For example, picking robots, cleaning robots — these are essentially low-speed versions of autonomous driving.

At this point we asked ourselves: If by 2023 these robot technologies are relatively mature, what problems will still exist?

A very important component of robots is LiDAR, used to detect obstacles ahead. But back then, LiDAR was extremely expensive — over RMB 10,000 each — which would limit large-scale robot deployment and application. So we researched further and found that LiDAR costs would likely decline as more entrepreneurial teams entered and R&D processes advanced, dropping below RMB 1,000.

Indeed, five or six years later, prices have come down.

Gaussian Robotics was founded in 2013; we led their Series A in 2017. We paid attention to Gaussian Robotics very early on, when the company was still exploring ROI improvement. By 2017, we judged that the demographic dividend was ending, 2022–2023 would be an inflection point, LiDAR costs would drop low enough by then, and supply and supply chains would further catch up — so we moved decisively.

Looking back, my judgments were largely correct. Gaussian Robotics now holds 60–70% global market share in unmanned cleaning machines, with domestic and overseas shipments at a 1:1 ratio. Their products are not only low-cost; I believe their functional software is world-class, able to quickly acquire service space networks, with multiple machines able to achieve intelligent dialogue when working together.

The key point to emphasize here is that hard tech is indeed hot, but you must find the right timing to enter. Too early or too late makes it hard to achieve expected results.

ChatGPT has recently attracted widespread attention. What we can see is that hard tech still has many application scenarios in the future, and can truly realize many of humanity's wild imaginings.

Whether it's a nation's rise or the advancement of human technological enterprise, more talented and ambitious people are needed to devote themselves wholeheartedly to tech entrepreneurship and tech investment.

Originating in Silicon Valley, BlueRun Ventures was established in 2005 and is a venture capital firm focused on early-stage startups.

Currently, BlueRun Ventures manages multiple USD and RMB dual-currency funds in China, with assets under management exceeding RMB 15 billion, making it one of the largest early-stage funds domestically. Its investment stage focuses on Pre-A and Series A, covering hard tech and innovative interaction, enterprise technology, new consumption, and healthcare, with cumulative investments in over 150 startup companies including Li Auto, Waterdrop, QingCloud, Guazi Used Cars, Qudian, Songguo Mobility, Ganji.com, Energy Monster, Yuntu Semiconductor, Machenike, CloudSaints Intelligence, Anxin Network Shield, BioMap, and others.

BlueRun Ventures has been ranked #1 on Zero2IPO's "China Top 30 Early-Stage Investment Institutions," #1 on ChinaVenture's "China Best Early-Stage Venture Capital Institutions TOP30," and among Preqin's Top 10 VC Fund Managers Globally for Sustained High Returns.

Additionally, BlueRun Ventures has for consecutive years received honors from Forbes China, 36Kr, Cyzone, Caixin Media, CBNweekly, Jiemian, and other media organizations for "China Best Early-Stage Institution of the Year," "China Top Venture Capital Firm," "Most Entrepreneurur-Friendly Early-Stage Institution of the Year," and "Most Influential Early-Stage Institution of the Year."