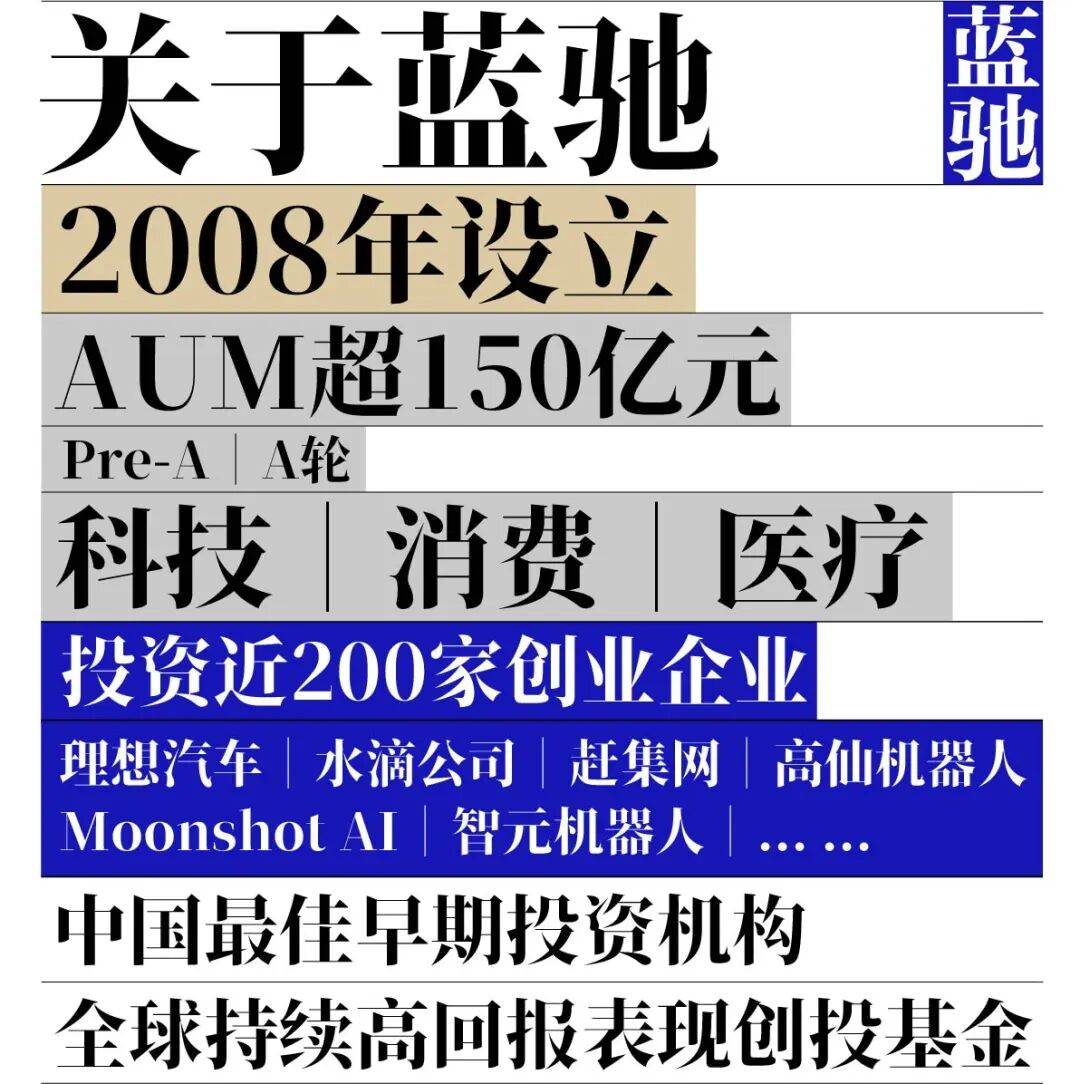

Venture Studio: When Investors Become Startup Producers | He Lan on Entrepreneurship

Step Forward, Step Inside

What do Snowflake, Moderna, and Exowatt have in common? All three were incubated through the Venture Studio model.

Compared to VC (Venture Capital), a Venture Studio doesn't look much like investing — it's more like being a "startup producer": selecting the direction, assembling the team, even handling the day-to-day operations, then handing over control to the true director of the company — the CEO — once things are on track. The underlying assumption is that by stepping forward, investors can reduce the randomness of entrepreneurship and seek the optimal match between opportunity, talent, and solution.

In the new era after the AI earthquake, the Venture Studio takes on additional meaning: the entrepreneurial veterans who dominated key gateways in the mobile internet era aren't sufficiently AI-native; meanwhile, young people who have already logged their ten thousand hours in AI urgently need to connect with real-world scenarios. Are investors the best candidates to solve this mismatch?

This episode of "What's Blue About Startups" features Terry Zhu, Managing Partner of BlueRun Ventures, as host, joined by tech entrepreneur and investor Xing Meng and MIT PhD Justin to discuss what they know and think about Venture Studios — their various models, success stories, and their value across different industries.

This episode is also a crossover with Xing Meng's podcast "Tech Isn't Boring." As a seasoned venture capitalist with experience in both entrepreneurship and major tech companies, Xing Meng hopes to create a narrative that makes technology anything but boring in his podcast. Follow along!

Below is the full conversation, edited and condensed:

Xing Meng: Let's start with what the venture studio model actually is. Generally speaking, VCs invest in startups and take a small equity stake. But with a venture studio, the investor decides the direction of the company, founds it, and may even serve as CEO managing operations including hiring and day-to-day management. Only after the company finds product-market fit or reaches a certain revenue scale do they bring in a professional team to take over. At some stage, the investor and founder may essentially be the same person.

It sounds quite difficult, but what's exciting about it is the investor's perspective — they can see a broader world. When selecting a direction, they may be more analytical, choosing directions with higher probability of success, and they can mobilize more resources, essentially bringing their own capital to the table.

Some funds have been experimenting with this model for a while, but it didn't attract much attention before. In the past couple of years, because of the success of star companies like Snowflake and Moderna — for example, Snowflake, Moderna... people have gradually started noticing Flagship, which is representative of this model. What do you two know about Flagship?

Flagship Pioneering is a multi-sector innovation incubation platform focused on biomedicine. Its star company Moderna rapidly developed the COVID-19 vaccine Spikevax using its mRNA technology platform during the pandemic, becoming the world's first COVID-19 vaccine to enter Phase I clinical trials. This pushed Moderna's market cap to nearly $200 billion in August 2021. Flagship founder Dr. Noubar Afeyan is a successful entrepreneur and biochemical engineer.

Terry: What I understand is that their team includes people from major companies as well as scientists. They start with ideation, reading papers, and after finding a viable direction, they invest resources to do some testing. Once there's engineering feasibility, they start putting in capital — roughly tens of millions of dollars — which counts as the project's first round of investment.

Justin: Flagship itself focuses on the healthcare industry. I joined Flagship in 2010 as an intern while still a PhD student. Before joining, I thought they were just a regular VC. But day one was a shock: I walked into the office, this huge space, and couldn't find anyone. Everyone was crammed into one room. I looked — the tables were covered with papers spread open. Another PhD student told me our task was to find the best resources from these articles, like treasure hunting. Back then, Flagship mainly found suitable scientists from articles and guided them down the commercialization path.

But today, Flagship develops and discovers science themselves. They form groups of 6-7 PhD students led by a partner, starting from a specific need, with the PhD students finding solutions. Their daily discussions are about technology and the gap between technology and business. During this process, partners participate too — they have over ten years of experience, know the process from zero to one, and understand what drug development entails. During this period, they're doing almost purely paper-based work.

After ideation, they form a Proto Company (which may only have a basic product or service concept). Flagship invests $1-2 million, and they do lab proof-of-concept (Flagship has a shared lab that charges per project). If results match their paper thinking, the team raises a second round of funding from within Flagship, potentially reaching the tens of millions level. Then they do some CRO and CDMO partnerships.

Xing Meng: One obvious thing about Flagship is they only do pharma-related directions. This is a very vertical, incubation-friendly direction because what they're essentially incubating is assets, even IP. Most pharma companies don't really think about how to sell the drug before it's formulated — they care about how it's developed. They may have already exited by the time the drug is developed.

And Flagship breaks things down very deeply. They don't enter at an already-formed drug stage. Instead, they reverse-engineer from the target disease to its underlying science, then find different labs, even do their own research. Terry, is the venture studio a model that's particularly suited to the pharma industry? Does it have universal applicability?

Terry: I think whether this model works depends on three things:

- Whether there are sufficient numbers of various roles in this industry. Talent density needs to be high enough for the relay baton to keep moving.

- The characteristics of how science and technology in this industry transform into productivity and commercial value;

- To C or To B. The skill sets and team compositions needed, the height of barriers, and the patterns of returns are all different. I believe the pharma industry has this distribution too — the speed and cycle of capital turnover have their own characteristics.

Justin: Flagship didn't actually decide to do biotech from the start. The core reason for choosing this track is that the founder himself had previously succeeded in entrepreneurship in the pharma direction and had positive feedback. But they were also willing to try other areas, like energy. Have you seen their recent news? They've now invested $3.6 billion in sustainability, which may include agriculture and energy directions.

Xing Meng: The short chain, exitability, and assetization of the pharma industry exist because most companies have already formed monopolistic structures, with big pharma having established complete sales channels. For them, the most cost-effective approach is to pay a premium to purchase completed IP rather than fully developing it in-house.

Also, product definition in pharma is very clear — what drug treats what disease. As long as you make it, you can basically sell it. There's not much sales uncertainty; it's mainly R&D uncertainty.

Third, the entire process has clear regulation and value assessment — from preclinical testing to animal trials, then Phase I, II, III clinical trials, and finally market approval. These characteristics aren't easily replicated in other industries. When we do other sectors, we don't have such clear regulation, nor clear acquisition value at each step.

Terry: So maybe discussing Flagship doesn't offer much value for thinking about venture studios. The proposition of venture studios differs across different domains, as do the lead person's experience path and solution. Whether a venture studio succeeds, how efficient it is, how long it takes to produce valuable assets — these all need measurement standards. But maybe a venture studio isn't something that can be done by people who only look at commercial results (laughs). You also need some social ideals — wanting to solve certain problems, and using sustainable commercialization to support your social ideals.

Xing Meng: Justin, you should know something about ARCH Ventures too? Unlike Flagship, they may cover a broader area.

ARCH Venture Partners primarily invests in companies co-founded by scientists and entrepreneurs, focusing on bringing innovation in life sciences to market. It is a leader in successfully commercializing technologies developed at academic institutions and national laboratories. Star incubated companies include genetic decoding company Illumina and RNAi technology developer Alnylam.

Justin: ARCH Ventures could be called the originator of incubation capital. They were already established in the 1980s. At the time, because of the success of companies like Genentech (an American genetic engineering company considered the founder of the biotech industry), people wondered why capital investment, especially R&D capital investment, hadn't produced such good results. This stimulated universities and more people to think about it.

ARCH Ventures founder Steve Lazarus was then Associate Dean at Chicago Booth. He thought of using social capital and university capital to do early-stage project incubation. He raised $9 million — not easy in the 1980s. With the first fund, he did 12 projects. The result: 4 companies went public, 4 were acquired, 4 were written off.

AR represents Argonne National Laboratory, a national laboratory managed by the University of Chicago. CH represents Chicago (University of Chicago). These two institutions have over 700 labs. This was also Lazarus's bold proposal: after the Bayh-Dole Act, why wasn't anyone monetizing the value produced by these 700+ labs? This was his hypothesis. This result allowed him to move beyond the university after Fund II, but that didn't mean he abandoned these two schools — he continued following up on their labs' output.

What's interesting is they weren't limited to biology. Their partner Nelson's first very successful case in the 1990s actually had nothing to do with tech — it was an after-school tutoring program related to school education, but very successful. And one of Arch's most successful projects was a non-biology infrastructure company specializing in internet infrastructure.

Xing Meng: Another company that left an impression is Atomic Ventures. Founder Jack Abraham sold two companies when he was young. Atomic's first fund was roughly $200-300 million, and they raised their fourth fund last year. Among all venture studios, they were the first to explicitly state they "absolutely don't do vertical directions." Mark Andreessen was their LP, and he told them that in any given year, there won't be more than 15 meaningful new companies, and he couldn't bet that all 15 would appear in one track — possibly none at all. Interestingly, their first breakout company was Hims & Hers Health, a pharma company. Relevant patents had just expired, they made a generic drug and brought it to market. It succeeded.

Atomic Ventures was founded in 2012 by Jack Abraham. Star companies incubated using the venture studio model include: Hims & Hers Health, a healthcare company that reached a $1 billion valuation in just 15 months; OpenStore, which provides fast sales of e-commerce businesses for Shopify entrepreneurs; and marketing technology company Zenreach. They cover high-potential innovation areas including healthcare, fintech, and consumer technology.

Another example is Sutter Hill, known because of Snowflake, but before Snowflake, their investment in Pure Storage was also a major company. Before 2008, Sutter Hill didn't do incubation at all — it was a normal investment company. After Mike Speiser joined in 2008, he transformed the entire company's style to focus on incubation. He proposed the "80% CEO" concept: the investor spends 80% of their time being CEO, handling everything unrelated to product and technology, letting the team focus on product.

Sutter Hill Ventures is a long-established Silicon Valley venture capital firm. After Mike Speiser became a partner at Sutter Hill Ventures, he began incubating a batch of star companies using methods distinct from traditional VC, including Snowflake, all-flash storage solution provider Pure Storage, and real-time log management and analysis service provider Sumo Logic.

Sutter Hill Ventures Managing Partner Mike Speiser

So when does the investor let go? When they find PMF. Before that, company size stays at 5-10 people. If a product needs more than 10 people in the process of finding PMF, they won't do it. Once PMF is reached, such companies scale far faster than any competitor — extremely small before PMF, then heavily invested after. They mentioned one software company that spent roughly $200 million on scaling alone in one year; another grew from 100 to 1,000 people in a year.

Terry: Did they have pipeline cases first and then the Evergreen Fund, or the other way around?

Xing Meng: They started incubation on the basis of the Evergreen Fund. When Sutter Hill did Snowflake, it should have been with the Evergreen Fund.

Terry: What problem does venture studio essentially solve? It should be solving capability and resource mismatch problems in the entrepreneurial process. It could be the mismatch of scientists wanting to do commercialization but lacking go-to-market capability, or mismatches in timing, rhythm, and resources caused by macro environment — not sure if Mike Speiser joining Sutter Hill in 2008 had anything to do with the financial crisis.

So what mismatch points are we facing right now with AI or hard tech cycles that venture studios could help produce results? Because essentially VC also solves mismatch problems, but venture studios go deeper. Different verticals may have different mismatch propositions. For current VCs, there are some opportunities they want to invest in but can't pull the trigger on — should they be putting deals together?

Xing Meng: Many incubation funds were established in eras when capital was relatively cheap. Valuations were high then, and people were passively pushed earlier stage, and earlier stage meant angel stage — many incubators emerged this way. But today's situation is the opposite.

Terry: So what do you think is good timing for doing a venture studio? Or are there more opportunities today to use the venture studio model?

Xing Meng: Many factors influence this, such as whether it's a rate-hiking or rate-cutting cycle, platform shifts, especially the rise of AI technology — this may be a major paradigm shift — and the abundance of mature managers in corresponding application market domains. The permutation and combination of these factors forms the judgment. For example, if you want to do an AI-centric incubator in the education sector, the above two conditions are met, except for the rate-hiking cycle.

Terry: Right, when a mismatch is particularly prominent — like with compute, talent, or data supply right now — if a platform can provide support to projects incubated through its venture studio, that's also a very good timing. Looking at GenAI now, there's this feeling: models activating and empowering scenarios may be okay, but are truly native model capabilities fully ready? If everyone has to wait, that's a gap. How does a venture studio harvest the value of this gap?

And in China, to have the conditions for doing a venture studio, talent supply is especially important — people who can skillfully go from 0 to 1, 1 to 10, 10 to 100. There also needs to be a relatively mature culture where people are willing to pass the baton. Like Flagship's CEOs who have sold companies several times — they're very mature CEOs themselves. So when there's no CEO, who serves as CEO? These are very practical challenges.

There's also an important question: is venture studio reward high enough to justify such large investment?

Xing Meng: For example, during the 2010-2012 rise of mobile internet, paradigm shifts gave birth to a batch of new companies. YC truly achieved massive returns during the O2O and sharing economy wave, then in 2012 mobile internet had another wave of returns. But during the periods between these cycles, returns may not have been that high.

Why did it appear in this period? Because it allowed young people with very strong ideas, not much experience, but willing to try various directions to come out and start companies. In more standard cycles in the past, usually only those who were older and had deep accumulation in the industry could leave their original companies to continue doing micro-innovations in the same industry, continuing to serve their original customers.

Terry: That's very well put. I think AI faces this problem right now — there may be many young people who are more AI-native, who may have accumulated their 10,000 hours in AI earlier, but they lack entrepreneurial experience. On the other hand, there are many entrepreneurial veterans who very much hope to catch this AI entrepreneurial cycle, but their sensitivity and feel for AI may not match the young people's. Can this mismatch also be well integrated through this approach?

Xing Meng: Right, I think this is a very good point — it's equivalent to the talent structure needed for a new company having changed, and the market happens to have such a talent structure.

Terry: Right, it must be structural opportunity. What you said about big platforms, big transformations — these are all structural opportunities.

Xing Meng: So whether VC or venture studio, as capital matching parties, besides matching capital, they also have a talent matching function. But I think this layer is still more like angel investing — idea generation and day-to-day management aren't actually directly done by the capital side.

Justin: What is the real value of venture studio? It actually creates a batch of opportunities that wouldn't appear under normal investment logic. I may think more about deep tech, because much deep tech research involves basic scientific discovery and the application exploration after discovery. Venture studio hopes to intervene at the stage where scientific foundations have been discovered but application directions aren't fully clear.

In many cases, scientists actually don't understand the series of judgments needed around applications, including understanding market needs, need segmentation, and how to help them establish engineering-level milestones between science and needs. Scientists or professors aren't so sensitive at this level and often easily take detours, thinking they can find some friends or spend more time themselves to do it. But this is where problems most easily arise.

The venture studio's role is to bring industry cognition and industry experts needed in the process into the team, providing very good feedback before the team is fully formed, so that the engineering built between science and product follows the correct path, providing a very accurate, targeted team.

Terry: Actually, this is already quite granular. What it solves is the problem of how to correctly choose the path from basic scientific research to engineering. This kind of experience is actually scarce, but if it can be platformized like Flagship and provided to more startups, it can solve this problem of social resource use efficiency.

Xing Meng: And I think there actually aren't that many fields where finding the right person can bridge the gap from science to product or PMF. Most of the time, even if you find very strong people, you can't solve it, because it's a large industry problem involving time and coordinated efforts from upstream and downstream parties — not something one right person can solve.

The healthcare industry may be a viable field; some materials industries and other industries may also apply. Now what people may be looking for more is which fields can achieve effective connection and transformation through this approach. The AI Terry mentioned earlier is one example — science has already achieved transformation to the application layer in this regard. So how to use an "amplifier" to expand application impact and make it more sensible is something that needs thinking.

Zhiyuan Peng: The Wild Iron Man, Starting a New Adventure | What's Blue About Startups

I Deliver Packages, Giving North America a Little Tech Shock | What's Blue About Startups

Moonshot AI Explorer Edition Is Here — The Best Search Is the Search You Don't Have to Do | BlueRun Ventures Headlines