10 Experts on 2025 Overseas Listing Opportunities: "Prepare Well, Execute Firmly" | Ronghui

Ronghui Capital Acceleration Series.

"Keep overseas financing channels open, further improve the efficiency of offshore listing filings, and actively support qualified domestic companies in going public abroad, making better use of both markets and both types of resources." Recently, with policy support and a package of incremental policies driving an economic recovery, Chinese companies' appetite for overseas IPOs has rebounded.

- As 2025 approaches, what trends can we expect across the macro economy and primary and secondary markets, and where will confidence come from?

- Looking back at this year's Hong Kong and Chinese concept stock listings, what lessons can we draw?

- When innovative companies prepare to launch an IPO, what planning should they prioritize?

Recently, Gaorong Ventures joined forces with DFIN and KPMG to host a closed-door session for innovative companies, looking ahead to 2025 opportunities for Chinese companies seeking overseas listings and offering practical "listing playbooks."

Outlook for 2025

From Macro Economy to Primary and Secondary Market Dynamics

Macro Outlook and Equity Capital Market Dynamics

At the event, economists and equity capital market heads from investment banks shared their outlook for China's macroeconomic trajectory in 2025, alongside analysis of equity capital market dynamics and insights from recent new listing transactions.

Since September this year, as high-frequency data has improved, a package of incremental policies has demonstrated resolve and strength, and China's macro economy has shown signs of recovery and upward momentum. Domestic demand is seen as the primary driver of next year's economic growth.

On the equity capital markets front, Greater China equity indices have improved recently (A-shares, Hong Kong stocks, and Chinese concept stocks). Since September this year, Hong Kong trading volumes have climbed noticeably, with northbound capital flows becoming a key driver of the Hong Kong market and an important source of liquidity support.

Market data also shows that overseas hedge funds, passive index funds, and retail investors have become active buyers of Greater China equities. Long-only foreign funds are returning to sectors like consumer goods, and European investors are playing an increasingly important role in Hong Kong and Chinese concept stock deals.

AI Defining the New Tech Wave, With Real Returns in Sight

In his presentation, Shuo Hu, Partner at Gaorong Ventures, shared observations from domestic and international perspectives on recent market investment activity, exit pathways, M&A deal flow, and how the AI wave is reshaping the ecosystem.

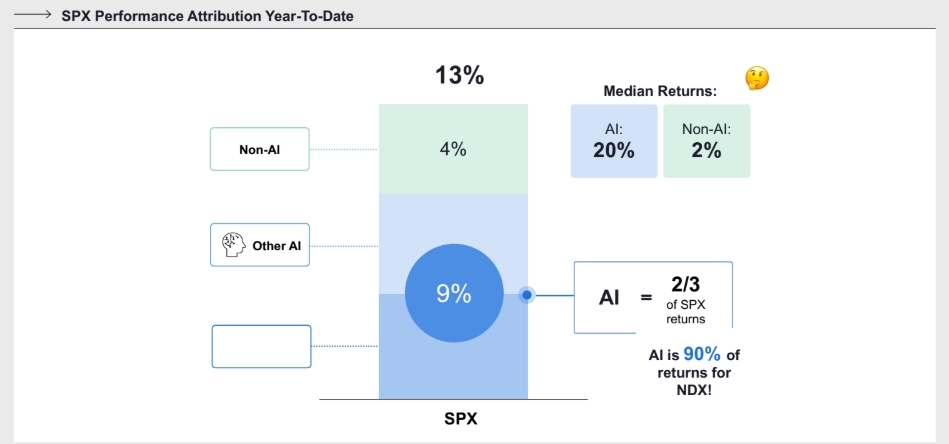

Based on statistics for recent U.S. VC investment deal volume, American VC activity remains below the 2021–2022 peak but has returned to pre-pandemic levels. Large-ticket deals at the top end have rebounded, with AI becoming the strongest capital magnet — "AI projects, compared to non-AI projects, are an order of magnitude higher in terms of deal count, valuation, and single-round funding size." On the domestic front, according to Zero2IPO data, China's investment and financing activity is stabilizing, with deal count and value rising quarter-over-quarter in Q3.

From an exit perspective, a global liquidity shortage is slowing the "capital flywheel." Even in the U.S., a large number of unicorn companies are waiting to go public, driven by capital flowing toward larger companies with greater certainty, valuation inversions between primary and secondary markets, and investors' diversified options. As a result, the market is seeking alternative exit routes — overseas M&A has consistently been one of the most active exit channels. Beyond pursuing IPOs in the U.S., Hong Kong, or other markets, Chinese companies should also pay attention to policy tailwinds and opportunities around M&A.

Hu also noted that AI is defining the new technology wave and has the potential to generate substantial returns — in 2023, AI was the primary driver of S&P 500 earnings; leading AI companies like OpenAI and Anthropic have already generated massive revenue in a very short time. As AI creates more real value, it will continue to reshape the entire ecosystem.

Source: Coatue, EMW 2024

Hu concluded by emphasizing that in today's market environment, a sense of urgency is critical for both entrepreneurs and investors. "Whether in primary or secondary markets, the focus has shifted from growth alone to unit economics models, free cash flow, and profitability metrics — ultimately pointing to a company's ability to sustain operations."

Offshore Listing Regulatory Focus

Filing Practice

"Identify Early, Act Specifically, Communicate Proactively"

Ran Li, Global Partner at Davis Polk & Wardwell, provided a systematic overview of regulatory review trends for offshore listings. This included U.S. regulatory developments such as SEC review priorities, as well as Hong Kong regulatory developments covering HKEX listing focus areas, SFC enforcement priorities, and annual report review points.

Li noted that Hong Kong regulators have sent many positive signals this year. On October 18, the SFC and HKEX issued a joint statement announcing optimized timelines for new listing application reviews, accelerating the approval process for "qualified A-share companies," and enhancing transparency in the overall new listing application review process.

For companies with IPO plans, Li offered advice and an action guide, emphasizing the need to align with the latest listing regulatory rules: "Identify early, act specifically, communicate proactively" — develop practical work plans targeting review elements and regulatory guidance, and actively seize the window and benefits of new regulations.

CSRC Filing Review Priorities for Offshore Listings

Chao Huo, Partner at Haiwen & Partners, focused on key points in the CSRC's filing review process for offshore listings. Since the new offshore listing rules took effect through November 22, 2024, 184 companies have completed filing — 81 for U.S. listings, 102 for Hong Kong, and 1 for Singapore; 49 direct offshore listings and 135 indirect offshore listings; covering TMT, lifestyle/enterprise services, automotive and mobility, biotech and healthcare, consumer, manufacturing, and other sectors. Huo also noted that the CSRC has stated it will "further improve the efficiency of offshore listing filings," suggesting more positive signals ahead.

Huo walked through the rule standards and basic procedures for offshore listing filings using case examples, emphasizing that the determination of indirect offshore listings by domestic companies follows a "substance over form" principle. He also highlighted common legal issues in filings, including foreign investment access, compliance of restructuring processes, compliance of historical equity changes and shareholder verification, compliance of equity incentives, business operation compliance, and data compliance and personal information protection.

Panel Discussion:

Challenges and Breakthroughs in U.S. and Hong Kong IPOs

At the event, speakers from KPMG China, the Hong Kong Stock Exchange, Nasdaq, and Gaorong Ventures shared their perspectives on offshore listings, moderated by Ke Li, Business Director for DFIN China.

Yunjing Huang, Assistant Vice President of HKEX's Global Listing Services, described how Hong Kong has actively introduced timely listing regimes and market enhancements in recent years — further lowering barriers for innovative and technology companies to list, accelerating listing approval efficiency, strengthening connectivity with global investors to promote liquidity, and providing convenient refinancing mechanisms to support listed companies' ongoing development.

Among these, HKEX introduced Chapter 18C in 2023 and further optimized it in September 2024, allowing more qualified specialist technology companies to list in Hong Kong. Huang noted that companies with high growth potential, strong technology attributes, and global expansion strategies have "promising futures" in the Hong Kong market — as companies achieve positive financial cycles, investor confidence will continue to build.

Yusheng Hao, Chief Representative of Nasdaq China, shared that companies in the U.S. listing pipeline over the next one to two years are concentrated in technology, fintech, consumer, and biotech/healthcare sectors.

Hao emphasized that listing in the capital markets is a starting point, with refinancing opportunities following as companies grow. "Companies with solid enough fundamentals will demonstrate excellent growth and profitability — or a clear path to profitability — gain market recognition, improve stock performance, and gradually restore investor confidence in Chinese concept stocks."

"Companies planning their listing path should also pay attention to the financial metric requirements and rules of different listing venues," noted Kunpeng Lu, TMT Industry Audit Lead Partner at KPMG China, explaining that financial metrics reflect underlying business and commercial models. He stressed that once a company initiates an offshore IPO, management's control over the timeline is a critical success factor — "prepare well, commit fully, execute firmly."

Kaibang Wang, CFO of Gaorong Ventures, also offered three IPO planning recommendations for companies: tell a compelling story; manage finances well; find the right people and do the right things. "From a startup to a pre-IPO company, I recommend building your 'DNA' early — improving corporate governance across finance, organization, compliance, and other dimensions to better navigate the challenges of the IPO journey."

"Don't lose confidence when markets are volatile, and don't get carried away when markets are overheated." Listing is a new beginning. Beyond policy tailwinds, timing windows, and market conditions, the ultimate focus must return to the fundamentals of a company's own value.