The Enterprise Services Race Heats Up: What's New for Growth in 2020? | Gaorong Ventures

Eight New Models and Ten Rules for Enterprise Service Growth.

2020 was undeniably a massive inflection point for enterprise services. A wave of companies achieved explosive growth that would have been unimaginable just months before. In early April, Zoom's DAU had surged 20x compared to December 2019, peaking at 200 million. Domestically, products like DingTalk and WeCom also saw unprecedented growth.

But riding a tailwind doesn't guarantee you'll keep soaring. Enterprise service companies still face a "gate" test: with customer conversion and retention unproven, they must cross a resource-devouring "valley of death" — the massive investments in servers, bandwidth, and personnel required to handle traffic surges. Unlike To C growth, To B growth demands both territory and treasure: customer count expansion must be matched by proportional revenue growth.

- As the pandemic's global phase unfolds and beyond, what shifts does To B service growth require?

- How should we understand and apply innovative business models used by high-growth overseas enterprise service companies — consumerization, network effects, SaaS-enabled marketplaces, open-source communities?

- How can growth hacking methods from To C be adapted for To B growth?

- What are the key metrics for measuring enterprise service growth quality?

Liu Xinhua, investment partner at Gaorong Ventures, recently shared insights at the "To B Enterprise Service Growth Online Seminar" co-hosted by Gaorong Ventures and Canjia Academy. Drawing on a decade of observing enterprise service companies and case studies of overseas benchmarks like Zoom, Slack, Salesforce, and Dropbox, he outlined new frameworks and models for enterprise service growth — hoping to inspire founders.

The following is the presentation:

After the 2008 financial crisis, two major categories of tech innovation emerged. One was To C sharing-economy models — Uber, Airbnb, Lyft, and others. The other was To B cloud service companies built on SaaS and PaaS models. Before 2008, not a single cloud service startup had reached unicorn status globally. Now there are over 100 valued above $1 billion, and more than 20 exceeding $10 billion.

As cloud infrastructure has matured, the digitization of business operations and online collaboration has become broadly accepted. A new generation of cloud-based enterprise services has achieved tremendous growth. The 2020 "pandemic of the century," while causing massive social disruption, also created new growth momentum for the adaptable — accelerating slow-moving variables like habits and trust. For a considerable period, physical isolation across entire workforces, supply chains, ecosystems, and even globally caused enterprise operations to rapidly shift online and become digital as a new normal and standard practice. In 2020, enterprise service companies worldwide entered a new explosive growth phase. Discussing enterprise service growth at this juncture requires holistic iteration across growth mindset, product and business models, and data-driven approaches.

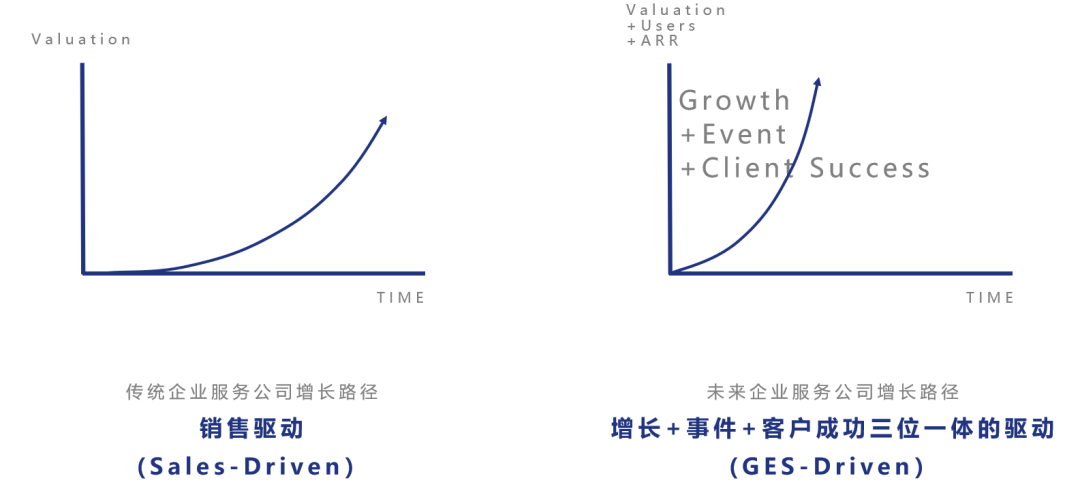

Enterprise Service Growth: From Sales-Driven to GES Trinity-Driven

Traditional enterprise service companies, especially those serving large enterprises, whether selling software, hardware, solutions, or consulting, relied on "Sales-Driven" growth. Multiple decision-makers, lengthy approval processes, on-site and private deployments, extensive training and consulting to shift customer learning curves, high customer concentration — winning, closing, and renewing deals all required massive sales teams. By contrast, rapidly growing modern enterprise service companies demonstrate "Growth + Event + Customer Success trinity-driven (GES-Driven)" growth. Growth-driven means digital precision acquisition and activation based on growth hacking theory — the conventional customer acquisition model. Event-driven means preparing for external black swan events for unconventional acquisition, an antifragile growth model. Growth-driven and event-driven correspond to "orthodox" and "unorthodox" strategies. Customer success-driven means using refined digital operations to manage customer lifecycle and enhance overall value.

1. Growth-Driven Growth

More enterprise service companies now rely on growth-driven growth, including Zoom, Tableau, Slack, Dropbox, Docusign, and DingTalk. Common traits: first, product supremacy — early growth centers on product before sales; second, product iteration optimizes core user experience, improves activation, and achieves product-market fit; third, applying growth hacking models to optimize acquisition efficiency and paid conversion, boost viral growth, renewal, and upsell, reduce churn, and improve customer and revenue growth efficiency across the full chain.

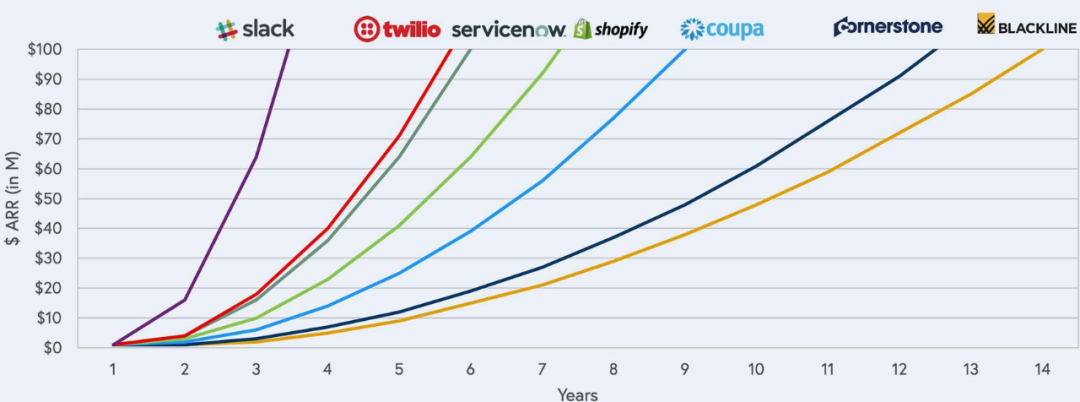

The chart below shows how long several overseas cloud service companies took to grow ARR from $1 million to $100 million. Companies consciously adopting growth-driven approaches typically grew faster — Slack reached $100 million ARR in just three years.

State of the Cloud: Years from $1M to $100M Annual Recurring Revenue (ARR) — Chart source: Bessemer Venture Partners

2. Event-Driven Growth

Event-driven growth is often overlooked. This isn't simply event marketing or pre-planned hype campaigns. It's more about preparing for the unexpected and capitalizing on it. Enterprise security and other adversarial domains particularly emphasize this approach.

As the saying goes, "When all is calm, growth lacks momentum." What unprepared companies see as poison, forward-thinking, adaptive companies treat as honey. Every crisis is a catalyst accelerating performance divergence.

As black swans and gray rhinos become more frequent, leveraging major disruptions for unconventional and supernormal growth will be essential. Huawei, which constantly asked "could we be the next to fall," established its Blue Team Staff Department early on — a core unit systematically studying risks that could destroy Huawei and developing countermeasures. Simply put, the blue team plays the opposing force in military exercises. Huawei's red team proposes standard strategies; the blue team, from competitors' and future innovation perspectives, daily asks "how to defeat Huawei." Huawei's many crisis-to-opportunity turns and avoided strategic errors owe much to this adversarial thinking.

Many overseas tech giants regularly conduct extreme scenario simulations to ensure rapid emergency process switching. As ancient wisdom states: "Use orthodox methods to engage, unorthodox methods to win." Modern enterprise service companies need not only digital-driven orthodox growth but also formal blue teams or virtual groups to think about avoiding black swans and profiting from them.

3. Client Success-Driven Growth

Many overseas enterprise service companies had no sales team before reaching $10 million ARR, instead driving revenue through client success teams. These teams focus on the core post-payment customer journey — new customer onboarding, aha moments, version upgrades, renewals, upsells, and cross-sells — using digital insights for refined operations that improve retention and value. Client success teams don't just ensure renewals; they create upsell opportunities, such as packaging customer support as a client success service offering.

Salesforce pioneered the client success concept, and many Silicon Valley mainstream companies have adopted it for organizational planning. Salesforce's client success operations provide: 1) continuous attention to customer experience — publishing upgrade notices, maintenance announcements, security risks, performance alerts, and API availability, with client success teams communicating accordingly; 2) pre-built template configurations and automation scripts based on usage behavior and statistics, minimizing customer configuration changes, and when necessary, pushing product teams to build these into standard products; 3) operating the online support community Trailblazer, using community experts for online training and peer-to-peer assistance.

Comparing "sales-driven" and "GES trinity-driven" models: the former mostly means "kneeling to earn," or at best "standing to earn" with exceptional technology. Future enterprise service companies, through new growth models, may stand to earn — or even "earn while lying down."

"6 Big, 2 Small" Product and Business Models Driving Enterprise Service Growth

Good growth genes stem from good business model design. Like To C growth, some products naturally occupy favorable traffic positions, more easily accumulating traffic potential and becoming inherent hits. Enterprise services often have their growth trajectory determined from initial product and business model design.

Here we focus on the "6 big, 2 small" models. The 6 big models are both product and business models; the 2 small models are primarily business model designs.

1. Model One: Consumerization

Consumerization (or "To C-ization") of enterprise services centers on whether the product is designed around the core end user. The playbook: build a product with exceptional user experience to win over individual users, then employ a bottom-up sales motion to penetrate the decision-makers at those users' organizations.

Consumerized enterprise services sidestep the burdens that weigh down traditional sales-driven growth. Those burdens typically include:

First, sales-driven products aren't designed around core user pain points—they're designed around what decision-makers perceive as valuable. Enterprise decision-makers span IT departments, procurement, business unit heads, and C-suite executives. They usually aren't the ones actually using the software or cloud services, so they can't truly grasp end users' real pain points. This disconnect leads to complex decision-making processes and protracted sales cycles.

Second, many sales-driven products suffer from over-engineering or even custom-built features, creating an illusion of higher value for decision-makers. In reality, these overbuilt features often see vanishingly low usage, and bespoke products resist standardization—making it nearly impossible to achieve economies of scale or declining marginal costs.

Third, sales-driven products rarely embrace simplicity, carrying steep learning curves. They also seldom account for remote, touchless delivery scenarios, resulting in complex, costly deployments—a model that took a severe beating during the pandemic.

Fourth, sales-driven enterprise services face substantial friction in discovery and distribution.

Several forces are driving consumerization to the mainstream:

First, "To C-ized" products more readily accumulate word-of-mouth and viral spread, expanding TAM (Total Addressable Market).

Second, user-driven rather than purchaser-driven adoption shortens decision cycles and reduces revenue concentration risk.

Third, greater standardization and economies of scale enable potentially declining marginal costs and increasing marginal returns.

Fourth, deployment costs drop through minimized delivery touchpoints and maximum remote/online delivery. Consumerized enterprise services also leverage communities where power users mentor regular users, reducing top-down corporate training investment.

Fifth, products can distribute through higher-traffic, more concentrated app marketplaces like the App Store and Google Play. In the mobile and cloud era, the best enterprise services—including Zoom and Slack, beyond their browser extensions—all have mobile apps. Mobile apps designed with consumer-grade UX can achieve better marketplace distribution. Outperform competitors, and you capture more visibility—Zoom recently topped the App Store charts in numerous regions.

2. Model Two: Network Effects

Network Effects mean a product's value to one user depends on how many other users adopt it. More users, more value; more value, more users. Virtually all breakout products embed network effects into their core design.

Traditional sales-driven enterprise services tend toward linear growth, sometimes even hitting "diseconomies of scale" at certain thresholds. Network effects unlock superlinear growth—network effects propel growth, which in turn amplifies network effects, creating a positive feedback loop.

Network effects fall into four categories. First, direct network effects: connections among similar or homogeneous users where product value increases with user base and usage volume. Common examples include IM, email, and payment tools; Outlook, Square, Dropbox, and PayPal all leverage direct network effects. Here, network value grows at roughly the square of user count—the classic Metcalfe's Law.

Second, indirect network effects: increased usage of an initial product drives consumption of complementary products, thereby enhancing the original product's value. More devices running Windows, Android, or iOS attract more developers and apps, accelerating OS adoption. Many PaaS providers follow this pattern—more users attract complementary SaaS developers to integrate with their APIs, driving PaaS growth.

Third, two-sided network effects: connections between heterogeneous complementary users, or between users and suppliers. More users or higher usage creates greater value for the complementary side, and vice versa. E-commerce and social platforms exemplify this.

Two-sided network effects can be global (Amazon, Alibaba) or local (Uber, Airbnb). Global network effects are stickier and more expansive—ideally, any demand finds unlimited supply with deep market liquidity. Two-sided effects can combine cross-side with same-side effects (LinkedIn), or feature only cross-side effects without same-side effects (heterosexual social networks).

The final category is standards and compatibility. When a product becomes an industry standard—de jure or de facto—it drives growth of compatible products. Software and cloud services integrating with Salesforce, Docusign, Office, or Zoom gain growth advantages. Proprietary PaaS platforms exporting APIs and SDKs to connect broadly with other cloud services aim to establish de facto standards and capture network effects—Twilio and Shopify operate this way. Within the WeCom and DingTalk ecosystems, Application PaaS (low-code/no-code platforms) and Integration PaaS are gradually becoming de facto standards for China's industrial internet. Riding the expanding developer ecosystems of WeCom and DingTalk, these PaaS categories will see substantial growth.

3. Model Three: SaaS-Enabled Marketplace

The third growth-driving model transforms a standalone SaaS tool into a two-sided marketplace (SEM, SaaS-Enabled Marketplace).

Pure SaaS tools face chronic stickiness limitations long-term. Converting that tool into a two-sided marketplace creates a dynamic where more customers attract more suppliers, and more suppliers drive further customer-side growth—building higher barriers and stickiness. Once the marketplace is established, SaaS developers can monetize through take rates; as transaction volume scales, supply chain financing services may emerge as additional revenue streams.

Two cases illustrate this model. First, Zenefits initially offered free HR payroll and performance management software to SMBs, then transformed into an insurance sales platform for SMBs—creating a two-sided marketplace connecting insurance carriers with small-business customers.

Second, Coupa began as procurement SaaS for enterprises, then evolved into a Business Spend Management (BSM) platform. Coupa connects enterprises with suppliers, helping companies manage procurement and supply chains while leveraging accumulated platform data plus AI capabilities to improve spend control. On the supplier side, Coupa also provides direct procurement access to major customers, giving suppliers incentive to partner with Coupa on preferential pricing and reliable supply chain delivery.

4. Model Four: Open Source

Open source represents the core spirit of the internet. Skeptics argue it "gains users but not revenue"—popular but unprofitable. Yet evidence shows open source can deliver both fame and fortune: Red Hat, built on supporting open-source Linux, sold to IBM for $34 billion; GitHub was acquired by Microsoft for $7.5 billion; Elastic and MongoDB grew rapidly through open source, went public, and reached $10 billion-plus market caps.

Open source communities essentially abandon narrow proprietary R&D in favor of broad public crowdsourcing. They harness the hacker innovation and altruistic contribution of community technical leaders to evolve an innovative technology framework into a shared technological path. For enterprise service entrepreneurs aiming to disrupt established tech giants or introduce novel technology frameworks, leveraging open source communities for growth is a remarkably efficient strategy.

Before open-sourcing, founding teams should define core architecture and map out division of labor between the team and community. This enables deep community operation around open-sourced core technology. The growth fulcrum for open source technology: either provide an innovative framework for entirely new scenarios and problems, or deliver technology with disruptive cost and efficiency advantages—either way, attracting like-minded technical talent to participate. Under open source, technology iterates faster, drawing more developers to contribute and deploy proactively. Once a de facto standard forms, a substantial customer base and passionate technical following follow naturally.

Mature commercial models exist: free open-source versions with paid stable enterprise editions; revenue from hotfixes and maintenance subscriptions; or monetization through custom development/consulting, or even converting software into proprietary chips or hardware.

Open source communities serve not only startups but also large companies incubating new products, recruiting technical talent in emerging domains, and building technical brand influence. Open source also functions as competitive strategy—Android's open-source challenge to iOS, and Alibaba Cloud's open-source challenge to the IOE (IBM, Oracle, EMC) stack, both represent classic cases of massive ecosystem and commercial growth.

5. Model Five: Vocational Certification

The fifth model cultivates external "evangelists" through vocational certification, using socialized methods to drive product adoption and viral spread. Enterprise service deployment differs fundamentally from consumer businesses—it typically requires technical门槛 and accumulated learning curves. By externally certifying enterprise software development and usage capabilities, companies essentially cultivate "trust agents" and evangelist ambassadors for socialized promotion. More enterprise customers create demand for more certified developers and operations specialists; more certified professionals accelerate broad deployment. A well-functioning certification system and enterprise service deployment form a mutually reinforcing positive feedback loop.

Tableau initially pursued a sales-driven model with mediocre results, because decision-makers and core users were disconnected. Tableau then launched extensive tutorials and certifications. Today Tableau boasts 150,000 certified analysts, forming a massive ecosystem network. Microsoft and Cisco ecosystem growth also correlates closely with their MCSE/MCSD and CCNA/CCNP certification systems.

DingTalk has spent recent years cultivating external "digital management specialists"—a profession that became one of 13 new occupations officially recognized by China's Ministry of Human Resources and Social Security in 2019. In 2018 alone, DingTalk trained and certified 200,000 digital management specialists through its programs; that number has now approached 2 million. The growing ranks of digital management specialists give the much-discussed enterprise digital transformation more concrete touchpoints for implementation, while helping DingTalk strengthen product promotion, deployment, and implementation capabilities.

6. Model 6: Boosting Visibility Across the Traffic Ecosystem

There's another angle: increasing the visibility of enterprise services within the broader traffic ecosystem. First, search remains an underappreciated but critical traffic source for enterprise service growth. Companies must prioritize SEO and improve page rank. Slack, for example, places heavy emphasis on search traffic.

Second, optimize for app store search (ASO) to boost app rankings.

Third, consider whether your product can improve API rank by integrating with enough mainstream products. Both Slack and Zoom connect with thousands of products through API integrations.

7. Model 7: Milestone-Based Pricing

Two smaller models focus more on business model innovation. The first is milestone-based installment charging. Some enterprise services carry prohibitively high upfront costs; consider charging a base software fee, then collecting phased fees at critical junctures where massive value is generated. Schrodinger, a molecular simulation technology and enterprise software solutions company, employs this model: it charges a software usage fee upfront, then collects separate fees for initial research, clinical trials, and success fees when molecular drugs gain approval.

8. Model 8: Value Bundling

The final business model innovation is value bundling — essentially making software feel more like hardware to enhance perceived value. Many mid-to-large enterprise owners undervalue standalone software. Bundling with hardware products builds trust and willingness to pay. This pattern appears frequently in financial and security software. Bloomberg has its terminal; security vendors Palo Alto Networks and FireEye bind software to hardware to elevate product value. Many chip startups follow similar logic: turning software into chips to boost perceived value, improve customer acquisition, and drive revenue realization.

Data-Driven Enterprise Service Growth

1. The Prerequisite for Paid Growth: Validating Product Value Hypotheses, i.e., Achieving PMF

Product model and business model design help a product more easily capture traffic momentum, but the precondition for large-scale paid growth is achieving PMF (Product-Market Fit) — matching the product to the market and satisfying core user needs.

How to measure PMF? Beyond retention metrics, one commonly used key indicator is Net Promoter Score (NPS) — the likelihood that a customer will recommend a company or service to others. Both Zoom and Slack heavily prioritize NPS. According to Gartner Peer Insight data, Zoom's NPS stands at 72%, far above the industry average — the most important foundation for Zoom's superior organic growth rate compared to competitors.

2. Growth Must Center on a Clear North Star Metric

In the growth hacker framework, cross-departmental coordination requires a unified metric: the so-called "North Star Metric." This is the single most important metric for a product, with two core characteristics: first, it reflects the frequency and stickiness of core product usage; second, it serves as a leading indicator of revenue. Optimizing the North Star Metric naturally drives revenue growth. Salesforce's North Star Metric is "customer data volume recorded per account"; Adobe's is "cloud user subscription volume."

Slack's North Star Metric has evolved through several iterations. Initially it was "New Accounts." When Slack began pushing paid products, this shifted to "New Business Accounts." Six months later, while user quality improved, activity levels hadn't materially changed — sometimes they were even lower — so the metric changed to "New Activated Business Accounts." Later, to align acquisition and retention team goals, Slack adopted "Activated Business Teams" as its new North Star Metric.

3. Optimizing Enterprise Growth Levers and Finding the "Aha Moment"

In consumer growth, we often talk about breaking down growth levers and optimizing each separately. For enterprise services, three levers matter most: first, acquisition — winning and retaining new customers; second, effective activation — completing actions like customer renewals; third, churn prevention, focusing on optimizing customer experience. During rapid growth phases, acquisition takes priority over activation and churn prevention; during high-growth and mature phases, activating and retaining existing customers and preventing churn become more significant.

Consumer growth methodology also emphasizes data-driven discovery of the "aha moment" — that instant when product usage makes users' eyes light up or sparks genuine surprise, when they discover the product's core value: why it exists, why they need it, what they gain. Why does Zoom cap free accounts at 40 minutes? Because user cohort analysis revealed that a customer's first continuous 45-minute Zoom meeting represents the product's "aha moment" — after experiencing a 45-minute meeting, customers convert from skeptics to fans with strong willingness to pay. Similarly, Slack made the first 2,000 messages free because it found that paid conversion willingness rises substantially once an active business account sends over 5,000 messages, and accounts reaching 10,000 messages highly likely become paying customers. So 10,000 messages sent by an enterprise team represents Slack's aha moment for paid accounts. By identifying quantified aha moments, growth teams can guide customers to reach them faster, completing the free-to-paid conversion.

Enterprise service companies can also apply the pirate metrics framework from growth hacking, optimizing across customer acquisition, activation, retention, referral, and revenue stages.

4. Driving Brand Marketing and Perception Management for Enterprise Services

In today's competitive landscape, B2B enterprise service companies must also invest in brand marketing and perception management targeting key customer segments. Examples include brand building through developer communities or conferences; endorsements from Gartner Magic Quadrant and Forrester Wave rankings are crucial; seize event marketing opportunities; leverage major platform or third-party awards for credibility; and for certain B2B companies, diverse content formats — documentaries, tutorial videos, white papers, explainer posts — prove critical for elevating awareness.

One additional suggestion: use social media to make B2B products break into mainstream consciousness. During Spring Festival, DingTalk's "DingTalk begging for mercy online" meme video spread widely on Bilibili — such user-proximate approaches effectively shape perception and drive growth.

5. Key Growth Quality Metrics Silicon Valley VCs Watch

Below are key growth metrics Silicon Valley VCs heavily emphasize when investing in enterprise service companies. They may not fully apply to China, but serve as useful reference.

Silicon Valley VCs typically divide high-growth enterprise services into two categories. First, growth-stage companies with ARR between $10 million and $100 million, with seven trackable metrics corresponding to good, excellent, and exceptional quality standards. The seven metrics are: ARR growth rate, gross margin, logo retention, net dollar retention, CAC payback period, quick ratio, and composite growth rate (combined ARR revenue + profit rate).

Data source: Signalfire Internal Data

Additionally, growth-stage enterprise service companies face different key metrics depending on customer type.

Data source: Bessemer State of Cloud 2017; Tomasz

Second, companies in rapid expansion with ARR exceeding $100 million. At this stage, calculate your "GRIT Score" using the framework below. Weight and score four dimensions: ARR growth rate, net customer retention rate, cash runway duration, and capital efficiency.

Chart source: Bessemer State of Cloud 2019

For G and R, the ARR growth rate and net customer retention percentage directly become the score — 50% equals 0.5. For I, the score equals cash runway in years — one year of runway equals 1. For T, the ratio itself becomes the score: if net new customer ARR divided by net spend equals 0.8, this component scores 0.8. Adding the four scores yields the GRIT score: 3–4 indicates solid operations, 4–6 represents excellent operations, and above 6 signals exceptional performance. The GRIT score captures an enterprise service company's overall growth quality and resilience — an excellent metric for measuring growth quality.

10 Rules for Enterprise Service Growth

To conclude, here are ten rules we believe enterprise service companies must prioritize for growth today.

-

Product is the primary growth engine; product reputation, not sales force, determines market success.

-

Enterprise service growth demands both territory and treasure — customer count growth must be matched by equivalent revenue growth.

-

The DNA of product growth depends on sound business model and growth model design.

-

Different company stages demand different growth priorities. Early on, new customer volume matters most; in later growth and maturity phases, customer renewals, expansion revenue, and reduced churn become more critical.

-

Different ARR scales require different growth strategies. Enterprise service ARR typically falls into three tiers: single-digit millions, tens of millions, and over $100 million. Lower ARR should correlate with faster growth velocity. Reaching $100 million ARR represents a coming-of-age milestone for enterprise service companies. Maintaining 40% ARR growth while reaching or approaching cash flow breakeven typically meets IPO standards, usually implying unicorn valuation at the $1 billion level.

-

ARR growth rate is a vital indicator of growth capability. The industry has a "T2D3" rule for high-growth SaaS companies: triple ARR annually for the first two years, then double ARR annually for the next three.

-

Pursue high-quality, lean growth. Lean growth means balancing growth rate against burn rate. For companies below $30 million ARR, new customer ARR divided by net new spend exceeding 1.5 represents a healthy benchmark. For larger companies, ARR growth rate plus free cash flow as percentage of ARR exceeding 45% serves as an important metric for excellent public enterprise service companies.

-

Evaluate revenue growth quality through the 5 Cs. First, CARR — Contracted or Committed ARR. Second, Cash Flow. Third, Customer Acquisition Cost (CAC). Fourth, Customer Lifetime Value (CLTV); a CLTV/CAC ratio above 3 indicates healthy customer acquisition. Fifth, Churn.

-

Defining a North Star metric and breaking down its linked growth-lever metrics is essential for successful growth.

-

The GRIT score is a critical measure of an enterprise service company's antifragility.