12 New Trends and 12 New Growth Models in Global B2B for 2021 | Ronghui B2B Growth Camp

A look at the latest trends in the post-pandemic B2B market, and the growth strategies behind high-growth B2B companies overseas.

Despite a noisy, risky, and uncertain global landscape, this may well be the best of times for China's B2B entrepreneurs. Having endured and evolved through the long pandemic, and with the post-COVID acceleration of digital infrastructure on the industry side, China's best B2B founders can not only survive cycles and become friends of time — among them will inevitably emerge world-class B2B enterprises commensurate with China's economic weight. Of course, this doesn't mean the path of B2B entrepreneurship or growth is smooth sailing.

To soar against the headwinds, B2B entrepreneurs must resolve complex and shifting challenges with flexibility. They must be swift as the wind — rapidly evolving in response to technological innovation, cloud ecosystem shifts, and demanding customer experience expectations. Yet they must also be steady as the forest — able to step back from the front lines at any moment amid the sprint, examine critical junctures, and calmly do the hard but right things, focusing on building high-quality growth systems.

In April 2021, Gaorong Ventures launched the 2021 Ronghui B2B Growth Camp, formally assembling 46 outstanding B2B entrepreneurs. Over three months, the camp will focus on key growth links including new business models, enterprise and SMB sales, customer success, and content marketing — helping entrepreneurs gain insights and truly solve growth pain points through industry expert sharing and case study discussions.

In early May, Gaorong Ventures investment partner and former Kuaishou chief growth officer Liu Xinhua, drawing on years of experience in product, strategy, and growth at high-tech and internet companies, joined the camp's entrepreneurs to examine the latest post-COVID B2B market trends and share growth tactics from high-growth overseas B2B companies.

Going forward, we will continue to share the series of practical insights from the B2B Growth Camp's industry experts, in hopes of bringing help to more B2B entrepreneurs.

The following is an edited transcript of Liu Xinhua's sharing:

The impact of COVID-19 on global industry and economic patterns may, in retrospect years from now, prove more profound than people imagine. Some developed countries have seen the dawn of herd immunity, yet localized regions including India and Brazil still face fresh uncertainty.

But great crises beget great remedies. Leading the world out of this disaster requires not only biological herd immunity at the individual level, but also digitalization, intelligentization, automation, and comprehensive cloud migration on the enterprise, industry, and supply chain sides to help the economic supply side develop herd immunity. Whether the digital investments made by nations and companies as stress responses during the pandemic, or the massive digital new infrastructure plans invested in by governments and tech companies post-pandemic — these are all "golden rain" opportunities that B2B entrepreneurs should not miss.

Today's sharing covers 12 new entrepreneurial trends and 12 new growth tactics in the B2B space from a global perspective, hoping to help enterprise service entrepreneurs accelerate supply-side innovation in China's economy.

12 Innovation Trends in the Post-COVID B2B Space

Trend 1: Distributed Remote Work Becomes Mainstream, Spurring New SaaS Tools to Reconstruct Work Scenarios

Outside China, the protracted pandemic has made distributed remote work the new normal. McKinsey & Company's latest survey of over a thousand companies shows that 20-25% of companies will still have employees working from home half the time even after the pandemic. Another interesting fact: in the past nine months, the number of new companies founded globally has exceeded the annual number of new companies founded in each of the past ten years — and most of these are "born remote," meaning they had no office from day one and were globally distributed from the start.

Remote work naturally offers much flexibility, but it brings a host of problems: burnout from sustained work, loneliness, collaboration and communication challenges, cross-timezone coordination, data security management. Even Zoom founder Eric Yuan himself has said, "To be honest, even I sometimes get tired of Zoom."

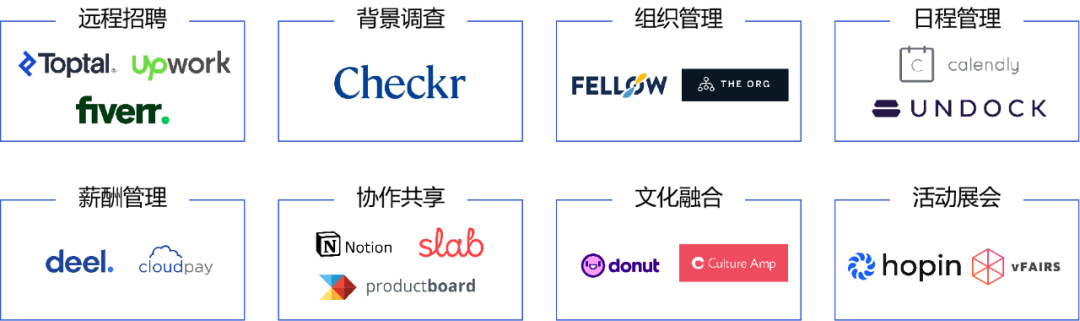

Examined closely, pure distributed remote work poses multifaceted challenges to traditional company organizations: how to conduct remote hiring, background checks, and capability assessments; how to manage collaboration, compensation, and performance after employees join; and more headaches — how to build cultural identity and organizational cohesion.

These new challenges in niche scenarios also breed new reconstruction opportunities. Existing HCM tools that relied on office scenarios are now "at their wit's end," while a new batch of SaaS tools has developed rapidly, with greatly improved user growth and stickiness, and corresponding unicorns have emerged. In recruiting, for example, Upwork, Fiverr, and Toptal have seen their stock prices or valuations multiply several times; in scheduling, Calendly; in collaboration and sharing, Notion and Slab; in virtual events and exhibitions, Hopin — all have had notable development.

Trend 2: SaaS Goes "Beyond the Fifth Ring Road," with SaaS for Down-Market Small and Micro Enterprises Rising Rapidly

In overseas cloud service markets today, whether IDC or Gartner data, 60-70% or more of cloud services are purchased by SMEs — a very healthy distribution. Currently China is the opposite: large enterprises are the main paying customers, hybrid cloud configuration dominates, and cloud service potential remains to be unlocked.

The overseas pandemic has further boosted SaaS penetration among SMEs, especially small and micro enterprises. Small and micro enterprises have long been "saline-alkali land" in the eyes of traditional SaaS practitioners — hard to cultivate, yet too costly to abandon. But conversely, they are also an under-competed, under-served market; with customer acquisition model innovation and new traffic support, they may instead be diamonds in the sand.

The ravages of the pandemic have brought three types of small and micro enterprises actively on board, beginning to fully embrace SaaS tools. The first are very traditional offline-dependent small businesses — in catering, field services, event management and other industries, where digitalization and cloud migration have become the final lifeline. The second are small and micro enterprises parasitic on large e-commerce and social platforms — Amazon sellers in cross-border e-commerce, DTC brands leaning on Shopify and relying on social media for traffic. The third are pandemic-spawned "born remote" innovative companies, for whom digital nativity is standard equipment. The surging demand from these three types of small and micro enterprises is transforming a neglected "saline-alkali land" into potentially fertile ground for wealth creation by new SaaS entrepreneurs.

Similarly, the substantial increase in online transaction penetration after the pandemic, combined with the maturation of China's WeCom ecosystem, has also accelerated the emergence of new SaaS companies serving small and micro enterprises. Whether in China or overseas, the trend of B2B going "beyond the fifth ring road" to expand into broader down-markets is becoming a new direction.

Globally, a number of small and micro enterprise service companies that "do not disdain small acts" have developed rapidly thanks to the pandemic. Beyond Shopify with its over $100 billion market cap, Toast, which digitizes the restaurant industry, has reached a $20 billion valuation; Service Titan, which empowers small businesses through field services, is valued at over $7 billion; payroll platform Gusto and project management platform Monday.com have both grown into unicorns.

Trend 3: Dual-A Drive Becomes Essential for New SaaS, Pushing Self-Evolution of SaaS Service Value

Regarding the concept of SaaS — "Software As a Service" — many practitioners only focus on the first S, software. But the second S, service, may be more important; after all, software is the vehicle, while the core value rests in providing service. SaaS differs from traditional software not essentially in business model or delivery model, but more importantly in providing superior service experience that improves with usage time and depth. This experience gap is the most essential advantage for SaaS to prevail over traditional software.

But how to achieve service value upgrades without heavy human investment, and even provide more personalized service to customers? For a large-scale SaaS company, ecosystemization is certainly one answer — to be discussed in detail later.

Another trend is using Automation + AI (dual-A) to enhance the system's "action power" + "brain power," driving service efficiency and experience improvement. In the new generation of SaaS, dual-A capability enhancement will be everywhere. SaaS will no longer be simply efficiency tools and recording tools; SaaS will be more like the helmsman commanding countless "software robots" (such as RPA) and "algorithm robots," continuously pushing service acceleration, personalization, and even evolution.

Trend 4: Cloud-Native, Microservices, Multi-Scenario API Integration, and Multi-Cloud Support Become Standard for New SaaS

China's current SaaS companies are mostly hybrid-cloud-model-dominated, with subscription and customization services running in parallel. But a new generation of SaaS companies, many from their founding, are cloud-native — designed for the cloud. The goal of cloud-native is to enable applications to consider the cloud environment from the very beginning of design, leveraging and exploiting the elasticity and distributed advantages of public cloud, so that applications run in optimal condition on the cloud.

Advances in virtualization and containerization, the steep rise in public cloud penetration and capability, and the mainstreaming of DevOps collaboration have made cloud-native the architecture of choice for a new wave of SaaS companies in the post-pandemic era. The new ecosystem that cloud-native enables is, in the long run, a fundamentally healthy one.

The deeper significance of cloud-native is that it is not merely a forward-looking technical architecture, but an advanced model for development, management, and even ecosystem collaboration. Technically, it encompasses highly decoupled microservices architecture, containerized deployment, continuous delivery, and DevOps operations mechanisms.

The philosophy of microservices architecture is critical to understanding the advantages of the cloud-native model. Microservices allow enterprise application services to be highly decoupled, enabling small teams of roughly ten people to accomplish development tasks that would have required one or two hundred people under a traditional SOA architecture, with releases possible on a daily or weekly cadence. This efficient use of development resources allows companies to deliver more services for the same investment — in other words, it lowers development costs.

Moreover, under cloud-native and microservices architecture, both internal service modules within a SaaS system and interconnection with external SaaS must be linked through APIs. Where software companies once had to integrate services through partners and systems integrators, APIs now enable far more efficient integration. The flourishing abundance of APIs has greatly catalyzed the rise of the cloud services startup ecosystem, because cloud services inherently depend on ecosystem strength — a single tree does not make a forest. The unique connectivity and enablement characteristics of the API model reduce the redundant reinvention of wheels within the SaaS ecosystem, and have given rise to a class of API service aggregators and specialized API modules. Stripe, valued at nearly $100 billion, Twilio in communications, and Okta in digital identity management all package diverse functions, data, and processes through APIs to become super-service aggregators.

Beyond these characteristics, cloud-native's efficient container orchestration technology gives services high scalability and enables efficient operations with continuous delivery. To prevent lock-in to a single public cloud provider, various operations SaaS, security SaaS, and storage management SaaS offerings that provide multi-cloud support and management have gradually become essential in the cloud-native era.

Trend 5: The Wave of Vertical Industry SaaS Arrives, with SaaS-Enabled Marketplace (SEM) Opportunities

The unique cost-reduction, efficiency-gain, and compliance demands of vertical sectors were further amplified during the pandemic, driving a new wave of vertical SaaS. Because vertical industry SaaS connects upstream and downstream players in an industry, it has the opportunity to evolve from a pure subscription-model SaaS tool into a SaaS-enabled marketplace (SEM). These marketplaces can dramatically improve industrial efficiency and drive supply chain reinvention within vertical sectors.

For example, Procore in construction empowers various roles in the industry while also generating numerous upstream and downstream transaction opportunities. Coupa Software started with spend control in supply chains, then upgraded to a comprehensive enterprise spend management tool, and formed a transaction platform that empowers small and medium suppliers and large customer procurement. Mindbody in fitness, beyond empowering gyms through SaaS tools, also connects gyms with end users to generate transactions. VTS in commercial real estate and Guild in education and training are further representative cases of vertical SaaS advancing to become transaction platforms.

We therefore advise vertical SaaS entrepreneurs that, beyond subscription revenue, they can adopt more flexible models — building generalized transaction and transaction SaaS platforms to generate revenue based on usage or transaction fees.

Trend 6: Ecosystem SaaS Is the Inevitable Path for Large SaaS Advancement

When a SaaS company reaches a certain ARR scale — say, $100 million in the US market — it inevitably begins to consider how to become infrastructure for at least one vertical domain. But as customer types multiply, scale grows, and demands become more varied, the difficulty of pleasing everyone becomes increasingly acute. By building a PaaS-like ecosystem, a SaaS company can maintain continuous product standardization while working with independent developers, value-added channels, and other ecosystem partners to address customers' ever-changing needs and share in the rewards. This achieves not only the perfect combination of standardization and customization, but also strengthens the company's product ecosystem moat and expands its potential market boundaries. In short, once SaaS reaches a certain scale, platformization and ecosystemization become inevitable.

The advancement of Shopify, a $100 billion-plus giant, would not have been possible without its ecosystem of 4,000 certified developers. Shopify pays these developers genuine cash dividends of no less than $100 million annually, and 80% of Shopify customers purchase products from Shopify developers beyond the core Shopify product. This not only reinforces Shopify's product moat but also drives continuous upsell and personalized services. UiPath, the recently listed "automation cloud" RPA giant, similarly leverages its 800,000 developers as a crucial asset for personalized delivery to large customers. Other well-known SaaS giants — Salesforce, ServiceNow, Twilio, Adobe, Autodesk, and Workday — all have distinctive developer ecosystems as well as partner ecosystems of systems integrators and consulting firms.

Trend 7: The Democratization of Developer Tools Is Unstoppable

Although there are approximately 25 million developers globally, this remains woefully inadequate against the surging wave of post-pandemic digital transformation demand. Two pain points have driven the rise of low-code/no-code development tools: helping experienced developers become more efficient and less burdened, and enabling non-coders — product managers, data analysts, and even operations managers — to do self-service development.

Given that experienced developers command premium salaries and are hard to find, the democratization of developer tools represents a massive opportunity. Major overseas tech companies have built or acquired their own low-code/no-code product lines. Among independent startups, overseas leaders include Zapier, Appian, and Mendix, while domestic players like AoZhe lead the field in China.

Trend 8: Open Source Eats the World, Moving from Edge to Mainstream

Open source is consuming traditional closed-source software, gradually moving from a geek-driven fringe to the mainstream of software development and growth models. Over the past two to three years, we have witnessed numerous open source software IPOs and acquisitions, repeatedly shattering valuation records for open source companies. From Red Hat and GitHub being acquired by tech giants at sky-high prices, to independent open source companies MongoDB and Elastic going public and ascending to become $10 billion-plus super-unicorns, the market's 30-year discrimination against, neglect of, and indifference to open source software has been thoroughly washed away.

The tremendous progress of open source commerce has finally formed open source software into a complete operational闭环. Open source business innovation has also combined effectively with the SaaS model, forming an Open Core free + SaaS subscription paid model. Specifically, this means open-sourcing 95% of core functionality (Open Core), while keeping the remaining 5% of premium proprietary features closed-source and charging for them through SaaS subscriptions to serve demanding large customers. This 5% of proprietary functionality primarily covers multi-user, cross-cloud management and auditing, and security service scenarios, where large customers have strong willingness to pay. Of course, where large customers have needs, developers can also convert some maintenance and support services into subscription-based revenue. This business model design not only helps drive the dual wheels of technology and commerce, but also ensures their coordinated development.

Of course, the Open Core free model is not without flaws. The decision of which code belongs to open source versus proprietary can lead to community fragmentation. The most troublesome scenario is when the community rejects your proprietary code decisions and decides to fork the project, or launch an entirely new project based on the original codebase. Since open source software is rooted in community, staying in sync and alignment with that community is critically important.

A successful Open Source SaaS must achieve three fits: Project Community Fit, Product Market Fit, and Value Market Fit. The first two relate to product success and community growth; the last, Value Market Fit, determines the boundary between open source and proprietary code, as well as the scope of SaaS subscription收费 services. The independent open source super-unicorns that have risen in this wave of open source — Databricks, HashiCorp, Elastic, MongoDB, and Confluent — have all successfully achieved these three fits, particularly Value Market Fit. Open source companies that fail to solve Value Market Fit can at best achieve "popularity without profitability." But when the "profitability" problem is solved and Value Market Fit is achieved, independent open source companies can become high-growth, thoroughly mainstream commercial software companies.

Trend 9: Multi-Dimensional Compliance Becomes a New Growth Engine

Without rules, nothing can be accomplished. To ensure that technological progress interacts positively with industry and societal development, compliance management is everywhere — from internal corporate compliance around finance, legal, tax, and data, to implementing industry standards, national standards, and legal systems in company products and services, to complying with local laws and regulations in cross-border operations. But efficient compliance management has always been challenging: execution costs are extremely high, inefficiencies and loopholes abound, and corruption is a persistent concern.

Yet one can still dance beautifully "with shackles on." Compliance modules within SaaS software, and new SaaS born from compliance needs, not only make compliance management more agile and low-cost compliance possible, but also enable the discovery of more risk scenarios, provide deep insights into rules and compliance processes, fix loopholes, optimize rules, and form a positive interaction where all parties are incentive-compatible and proactively compliant.

For SaaS founders, new features or entirely new software "born for compliance" are emerging as powerful growth engines. In Europe and the US, compliance demands across multiple dimensions are spawning a new generation of compliance unicorns: ESG (Environmental, Social, and Corporate Governance), DEI (Diversity, Equality, and Inclusion), privacy and data protection, vertical industry regulations adapting to distributed remote work / full cloud migration / open collaboration, internal IT operations and security compliance, and financial, legal, tax, and HR compliance.

In China, the two-invoice system in healthcare, government and state-owned enterprise procurement transparency, financial sector banking-securities-insurance compliance, and carbon-neutrality mandates are likewise fueling the rise of industrial internet companies.

One additional point worth emphasizing: beyond merely meeting customer compliance needs, startups can strive to become participants and even shapers of the rules themselves, capturing the dividends of regulatory influence. Ordinary companies are rule-followers. Excellent companies become rule-participants. Great companies inevitably become rule-makers.

Trend 10: Exploring New Data Dimensions for New Opportunities — "Reaching for the Sky and Delving into the Earth," Digital Twins

Today, B2B entrepreneurs are also leveraging new data dimensions to uncover novel demand scenarios and unlock new paradigms of growth. New data dimensions can dramatically expand human cognitive boundaries and give birth to new business models. Software products built on such dimensional data typically face less competition, and if the TAM is large enough, significant opportunities may emerge.

What counts as new data dimensions? Data collection tentacles have expanded enormously: satellite internet development, exponential growth in sensors, nanoscale semiconductor technology, advances in cellular and genetic testing. Our data collection capabilities can truly be described as "reaching for the sky and delving into the earth." Whether it's SaaS companies leveraging satellite remote sensing big data like Orbital Insight, Planet, Descartes Labs, and BlackSky; platform companies utilizing IoT sensor data like Tuya and Samsara; or companies working with biological data at the cellular, genetic, and protein scales like Sema4 and Relay Therapeutics — all are creators of new paradigms.

Furthermore, the expansion of digital twins across domains is reconstructing a new virtual world, vastly extending humanity's ability to transform industries and industrial processes, and improving transaction and collaboration efficiency in every vertical niche. Physical-world assets at every scale — spatial assets including buildings, structures, factories, and land; as well as vehicles, bridges, apparel, jewelry, and assets at even finer granularity — will not only be digitized but ultimately digital-twinned, providing true-mirror 3D visualization and multi-dimensional data accumulation. Analogous to how Google indexed human information and knowledge, digital twin companies are now indexing the real world from every dimension. Matterport has fully digitized 5 million commercial spaces; Autodesk drives design and delivery efficiency in architecture, engineering, and construction (AEC) through digital twin tools; domestically, Lingdi Technology digitizes apparel through its digital sample library. Once assets are digitized, especially digital-twinned, possibilities for design, collaboration, and transaction emerge, nurturing abundant opportunities.

Of course, digital twin opportunities are not limited to the physical world we can observe. They can extend deep into microscopic scales invisible to the naked eye. AI drug and materials discovery company Schrödinger, for instance, builds high-fidelity digital twin models of molecular worlds, enabling efficient screening of new drug and material molecules from vast compound spaces.

Trend 11: Traffic Anxiety and Digital Existence — Brand Enablement Tools Take Center Stage

The DTC philosophy is increasingly taking root, digital channels have become brands' primary sales channels, and the reality that digital traffic is increasingly concentrated on oligopolistic platforms — all of this is intensifying traffic anxiety among brand owners globally. Brands must care about traffic quality and efficiency while deepening user operations, yet also adapt to new traffic dynamics and seize new growth opportunities. Brand enablement tools have proliferated post-pandemic, helping brands grow across multiple dimensions.

In China, for example, the rise of livestreaming and short video has spawned numerous tools to help brands improve content production and KOL distribution efficiency. The maturation of the WeCom ecosystem has also given birth to private traffic management tools for brands. Overseas, many new SaaS tools focus on helping DTC brands manage fan engagement across multiple social platforms, comment management, intelligent product selection, intelligent content splicing and distribution, influencer marketing, and more.

Moreover, brands have evolved from traditional user and fan management to experience management. Experience management tools help brands better manage the health of customer relationships and improve transaction conversion efficiency.

Trend 12: New Manufacturing (On-Demand Manufacturing, Automation, 3D Printing) and Global Supply Chain Restructuring (Small Batch, Fast Response, Customization, Proximity-Based Resilient Supply Chains) Driving Industry 4.0

We've discussed many software and data-driven entrepreneurial trends, but opportunities in manufacturing deserve attention. Innovation in new materials, new processes particularly in 3D printing, new collaboration and transaction models represented by smart factories and on-demand manufacturing, and vertical industrial MRO on-demand procurement platforms — all represent important innovation directions in new manufacturing.

Furthermore, global supply chains are being restructured. Small batch, fast response, customization, and proximity-based resilient supply chains are becoming the new norm. Global supply chains, disrupted by the pandemic, now face enormous pressure as economies restart — particularly in Europe and the US. The recent attention on rising copper, oil, and lumber prices, and inflation's compression of growth stock valuations, partly stems from supply chain shortages. Chinese entrepreneurs, leveraging China's supply chain advantages alongside digitalization and intelligentization trends in logistics and warehousing, are building new efficient, low-cost, digital supply chain networks — also worth watching as entrepreneurial opportunities.

12 New Growth Models in B2B

Regarding growth systems, I've previously shared an 8-character principle — Clarify the Way, Seize the Momentum, Refine the Method, Know the People. Today I'll focus on 12 new growth models at the "refine the method" level. The direct sales, channel sales, and online display/search advertising lead generation models previously standard in B2B are now mature and won't be discussed further.

Model 1: Product-Led Growth — Experience First, Free Trials, Consumerization of B2B Products

First, product power is the first principle of growth. This is universally accepted in B2C, but in enterprise services, product power doesn't equate to monetization power, so its importance is often overlooked. Combined with the traditional top-down sales model typical of enterprise services, customer relationships, direct sales teams, and channel partners receive far more attention than product experience itself.

With the rise and full penetration of SaaS and cloud service models, and the continuous downward market expansion, product-led growth has become increasingly important. As enterprise software moves toward lower ACVs and flatter procurement decisions, individual end-users within teams now have more voice in product purchasing than before. When products build internal usage momentum and word-of-mouth, they increasingly trigger organizational procurement decisions — what we call the consumerization of B2B. The customer purchase path is bottom-up, but for products with natural network effects like Slack, Zoom, Docusign, and Figma, once they reach sufficient organizational penetration, B2B procurement decisions become simple and efficient.

Some ask whether product-led growth strategies only work for SMB markets. Actually, for products targeting enterprise customers, adopting B2B consumerization strategies, optimizing product experience, and reducing trial costs is also sound strategy. Snowflake, focused on large customers, offers first-class experiences whether in free trial features or self-service products and tools. Twilio — even at $10 per month — delivers the same clean, fluid interface experience as customers spending millions monthly, differing only in usage volume, seat count, and feature breadth. Products with natural word-of-mouth, low learning costs, and high self-propagating characteristics naturally achieve higher conversion and renewal rates, with upselling becoming easier.

As shown below, starting from 2018, an increasing number of successful enterprise service companies have achieved significant growth through product-led strategies.

Model 2: Community-Driven Growth — From Passerby to Fan, User to Customer

As mentioned earlier, the open-source software model has been evolving for 30 years and is now at its peak. Its core has never been the technical code itself, but community building. Beyond accumulating leads through free products for later conversion, SaaS companies can build community ecosystems that mobilize and support users, encourage sharing of tips and playbooks, and provide pathways for power users to rise through the ranks and even monetize their expertise. Through the network effects of community, this approach can freely aggregate massive amounts of leads and opportunities, converting them via the "passerby to fan" journey. UiPath, Discord, Tuya, and Unity are all masters at leveraging community for customer acquisition.

Model 3: Content-Driven Growth — From Text to Short Video/Livestream, From Official Broadcasts to Customer Showcases and Community Sharing

Historically, enterprise service companies approached growth and branding the same way they approached sales: top-down, with everything being an "official announcement" — official presentations, official videos, official guides, official conferences. But customers trust other customers more. User-generated content based on real experience — "buyer showcases," "player showcases," "tutorial videos," "explainer posts" — often carries more weight than official messaging, especially for lower-ACV products.

To B companies used to pour significant resources into annual ecosystem conferences and brand events, generating various officially licensed content. But the pandemic changed things: through audio and video tools like Zoom, Hopin, and even Clubhouse, companies could now interact with customers in lightweight, ongoing ways, continuously producing valuable content for distribution.

"Decentralized" content marketing is not only more persuasive and diverse, it's also extremely helpful for search-driven growth. Search has long been an overlooked growth tool in enterprise services. And the prerequisite for search optimization is feeding crawlers enough rich text content — so the more diverse the content, the more varied the angles, and the richer the formats, the better the search results.

Model 4: KOL-Driven Growth — Gartner/Forrester Endorsements; Lighthouse Customers Defining Features, Setting the Pace, and Making Referrals

Enterprise service companies rely on two types of key opinion leader endorsements above all: first, top-tier industry rating and research firms like Gartner, Forrester, and IDC; second, CIOs at major customers — though depending on the product, this may also include CFOs, CHROs, and CTOs.

Analyst relations with rating agencies has always been a crucial tool for Western enterprise service companies to build brand and drive growth. Many companies, like SAP, maintain dedicated teams for industry analyst relations. Being placed in the upper-right quadrant of Gartner's Magic Quadrant or Forrester's Wave is equivalent to reaching the pinnacle of industry recognition, and is critical to winning major deals. Lighthouse customers with industry representativeness, along with testimonials from their CIOs, can also provide outsized leverage for growth.

What makes a good lighthouse customer? A lighthouse customer is one with high influence and exceptional loyalty — even willing to publicly endorse the company or make referrals. They aren't necessarily the biggest-budget users, but rather super-users with the strongest needs and the most internal users, making their testimonials more compelling. Their demand scenarios tend to be both forward-looking and broadly applicable: the forward-looking needs help inform future product planning, while the universal needs serve as decision templates for other customers, guiding industry purchasing decisions.

KOLs are the business influencers of the enterprise service world — their word carries enormous weight. So I advise enterprise service entrepreneurs: by the time you reach Series C, you should have at least one team dedicated to managing KOL communications. These KOLs include analysts at industry rating and research firms, CIOs, and well-known industry bloggers.

Model 5: Mobile-First Growth — App Store and Mini-Program Distribution

Many SaaS products are built around web or desktop software, with little attention paid to the mobile experience. A mobile-first product strategy has become increasingly important post-pandemic, particularly leveraging app stores and mini-programs for low-cost distribution and growth.

Mobile strategies also expand usage scenarios, helping reach users who were previously inaccessible. One key lesson from Adobe and Autodesk's cloud transformations was using mobile to successfully convert former piracy users, individual users, and micro-business users to paid, legitimate customers.

Model 6: API/SDK Integration-Driven Growth — Scenario Distribution, Mutual Traffic Exchange

Under the cloud-native trend, a product's API capabilities are an important pathway to improving usability and driving growth. Through API integration, products can connect broadly with other entry-level SaaS or PaaS products, expanding usage scenarios and driving customer acquisition growth. Many well-known SaaS products have grown this way — for example, Slack integrated via APIs with mainstream platforms and adjacent-scenario products to improve usability and increase exposure and conversion opportunities. Beyond APIs, if a product's core functionality can be packaged as an SDK and embedded in partner products, such product alliances become traffic alliances that facilitate growth and enrich usage scenarios.

Just as Google proposed the PageRank system, using hyperlinks to measure a webpage's authority, perhaps public cloud app marketplaces could develop an "API Rank" as the cloud-native trend accelerates — with an API's influence determined by call frequency and which APIs call it. APIs with broad request volume would be more likely to be algorithmically pushed to the top of indexes, gaining more traffic.

Currently, enterprise service APIs in China aren't particularly developer-friendly, and the ecosystem isn't robust enough. I hope that under the software ecosystems led by major platforms like Tencent and Alibaba, Chinese developers will come to trust APIs more, API integration will become more commonplace, secure data exchange will be more universal, and we'll see more super-API companies like Stripe, Twilio, Agora, and Okta emerge.

Model 7: Cloud Marketplace-Driven Growth — Using IaaS and PaaS for Software Distribution and Cross-Selling

The普及 of cloud-native architecture brings another trend: public cloud marketplaces becoming the primary channel for SaaS software distribution. Public cloud marketplaces are both an important future revenue growth engine for the clouds themselves and one of the most important future customer acquisition channels for SaaS companies. Currently, AWS and Azure marketplaces lead SaaS growth internationally. For example, approximately 260,000 customers already use ecosystem developer software on AWS. Azure has two marketplaces: Azure Marketplace has built an ecosystem of over 100,000 developers, while AppSource markets and distributes SaaS applications to business users.

Today, leading global SaaS companies like PagerDuty and HashiCorp derive 30% of their revenue growth from public cloud marketplaces. As Azure and AWS bundle application distribution with public cloud sales and functional integration, public cloud marketplaces could become as important to SaaS future growth as Google Play and Apple's App Store.

Domestic public clouds are also gradually improving their marketplace ecosystems. For example, Alibaba Cloud already supports software subscription management, contract management, and rapid cloud deployment. As the marketplace ecosystems of Alibaba Cloud, Tencent Cloud, and Huawei Cloud mature, domestic developers can also tap into the traffic dividends from this emerging channel.

Of course, beyond major cloud providers' public clouds, other super-SaaS PaaS platforms also have high-value distribution capabilities. Salesforce and Shopify's app stores, for instance, are channels worth taking seriously for relevant SaaS distribution.

Today, overseas companies like Tackle.io — a fast-growing startup focused on public cloud marketplace agency operations — have even emerged, indirectly signaling the major trend of cloud marketplaces becoming a new pathway for SaaS growth.

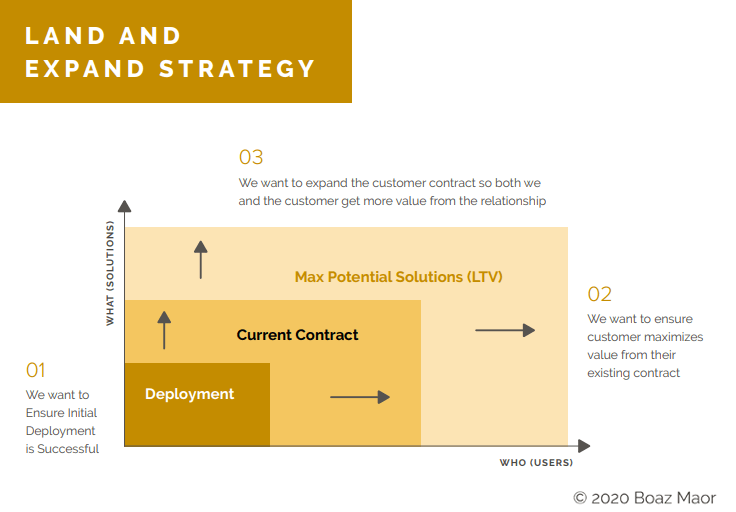

Model 8: Land & Expand Growth — Expansion Across Scenarios, Industries, and Geographies

Overseas publicly traded enterprise service companies almost universally discuss the Land & Expand growth strategy. The essence is to start with a single-point solution for a core customer's pain point scenario (Land), then gradually expand (Expand) to adjacent scenarios, similar industries, other regional markets, and higher-tier product solutions for upselling.

Model 9: Black Swan-Driven Growth — From Regulatory Shifts to Unpredictable Shocks

In reality, anything from a new regulatory rule to a full-blown black swan event can become a catalyst for enterprise service growth. Huawei's "Blue Team Staff Department" is a core unit within the company that systematically studies every conceivable risk that could bring Huawei down and develops countermeasures. This kind of organizational mechanism allows enterprise service companies to adapt to sudden disruptions, building inherent antifragility — and when external conditions shift dramatically, it can even help the company rapidly capitalize on the momentum.

Opportunity favors the prepared. In an era of frequent black swan events, companies should consider building strategic management teams modeled after the "Blue Team Staff Department" — not only establishing risk mitigation protocols, but also developing rapid-response capabilities to accelerate growth from unexpected crises.

Model 10: Value-Added Channel and Ecosystem-Driven Enterprise Growth

Enterprise software companies have two ecosystem models. The first is the developer ecosystem, similar to what Salesforce and Autodesk have built — typically providing a set of development tools, UI components, APIs, and an integration platform to create an app marketplace and deployment environment where developers build value-added and industry-specific applications.

The second is the traditional SAP ecosystem model: SAP provides standardized ERP products and platforms, while consultancies like IBM handle pre-sales solutions and overall project contracting, managing hardware and software integration. Companies like Accenture then implement the ERP system and provide ongoing maintenance support. Value-added channel ecosystems composed of consultants and solution providers like IBM, alongside implementers and operators like Accenture, are essential for heavy-delivery enterprise customers.

That's why larger SaaS companies today build both types of ecosystems — a developer ecosystem and a value-added channel ecosystem that provides implementation and delivery support — to drive growth across different customer segments.

Model 11: Customer Success-Driven Growth — Maximizing Full-Lifecycle Customer Value

The customer success journey moves from closed-won customer, to satisfied customer, to deeply engaged customer, and finally to loyal customer. Each stage has corresponding metrics: satisfaction is measured by renewal, deep engagement by expansion purchases, and loyalty can even manifest as customer-assisted referrals. Different management and engagement systems apply to customers at each stage.

Customer success is tightly linked to growth because growth fundamentally comes down to acquisition, retention, and churn prevention. Customer success directly impacts retention and churn intervention, as well as increasing the total contribution of individual customers to the business.

Model 12: M&A-Driven Growth — Customers, Data, Scenarios, Channels, Industries, Organizational Capabilities, and TAM Expansion

Today's cloud-native software architecture makes cloud service M&A considerably easier, since products can be seamlessly integrated through APIs and microservices — typically the most headache-inducing aspect of any merger.

In enterprise services, the best acquisitions create multiplication, not simple addition. Strong M&A usually happens between products in adjacent scenarios where one party has substantial scale and a large customer base. Post-acquisition, this effectively adds leverage and a multiplier to the acquiring company, creating amplified effects through cross-selling, data integration, and channel consolidation. When two products with high customer overlap merge, it's mostly addition — buying revenue — and typically does little to enhance competitive moats.

Of course, some acquisitions are subtraction — "buy to kill," eliminating competitors. There's also the "marrying into wealth" style of M&A, where a related asset is injected into a new company and spun out for independent development.

These are some of the latest growth tactics we've observed among overseas B2B companies in recent years. We hope they offer some inspiration for founders.

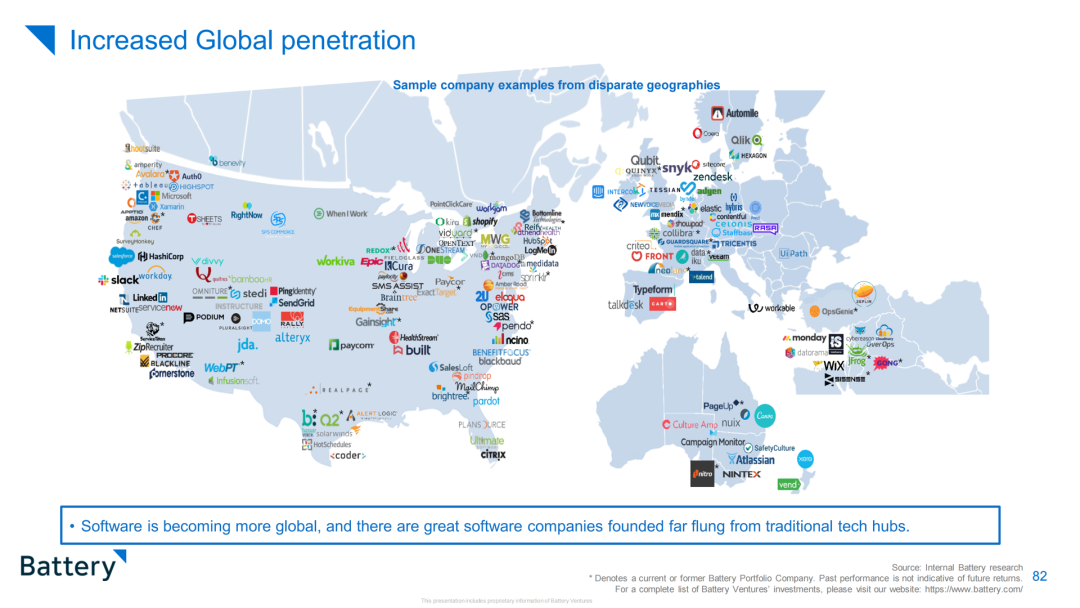

Finally, we want to emphasize that B2B entrepreneurship has entered the Age of Exploration. SaaS unicorns used to come almost exclusively from Silicon Valley, New York, and Seattle. But post-pandemic, more and more unicorns are distributed globally. UiPath is from Romania; Zendesk originated in Europe; Monday.com, Wix, and JFrog are from Israel; Aftership is from Hong Kong; Atlassian, Canva, and Afterpay are Australian. China, too, has seen several SaaS companies achieve rapid growth with customers both domestically and internationally over the past year.

As global cloud-native penetration accelerates and distributed remote work becomes mainstream, outstanding B2B founders can configure teams globally and acquire customers worldwide through new growth models. Enterprise service unicorns no longer have a particular geographic advantage — entrepreneurial teams everywhere have a shot.

Chinese entrepreneurs have spent the past decade riding the wave of mobile internet's unified global distribution, going through phases of utility software export, content app export, gaming export, and e-commerce export. We believe SaaS export and China supply chain export represent particularly large opportunities ahead. We hope to see more globally competitive enterprise service unicorns emerge from China.