Rui Han of Gaorong Ventures Decodes the Battleground for Future Consumer Giants: Transferable Trust Is What Makes a Brand

Above category, the first way to classify tomorrow's consumer giants is by "scenario and function."

"From an entrepreneur's perspective, every industry is worth rebuilding from scratch. From an investor's perspective, our conviction is that every industry is worth deconstructing from scratch."

On August 26, Rui Han, partner at Gaorong Ventures, delivered a keynote speech titled Some Thoughts on the Consumer Sector at 36Kr's "2020 China Investor Future Summit." Drawing from Gaorong's hands-on investment experience in new consumer brands, Han shared his observations on two fronts: the structural opportunities for VC investment in China's consumer sector, and Gaorong's framework for evaluating the industry's future trajectory.

Key takeaways:

-

The foundational structural opportunity for consumer investment in China lies in generational turnover — specifically, the shifting weights and priorities in decision-making factors as consumers enter new life stages.

-

The accumulation of new demand and the evolution of startups progresses through three phases: incubation, explosion, and maturation. The key to investing lies in "selecting the trend" by observing the emergence of new demographics and directions of unmet demand accumulation, and "selecting the timing" through qualitative leading indicators.

-

Scenarios and functions will replace product categories as the primary label for future-facing consumer companies.

-

New-species companies will seize the opportunity to merge "product and service," "channel and brand" into unified offerings, packaged as complete products presented to consumers. Private-domain tools will represent a revolutionary infrastructure for consumer goods companies on a global scale for the first time in two to three decades — providing channels and overlaying service layers.

-

Transferable trust is what constitutes a brand.

-

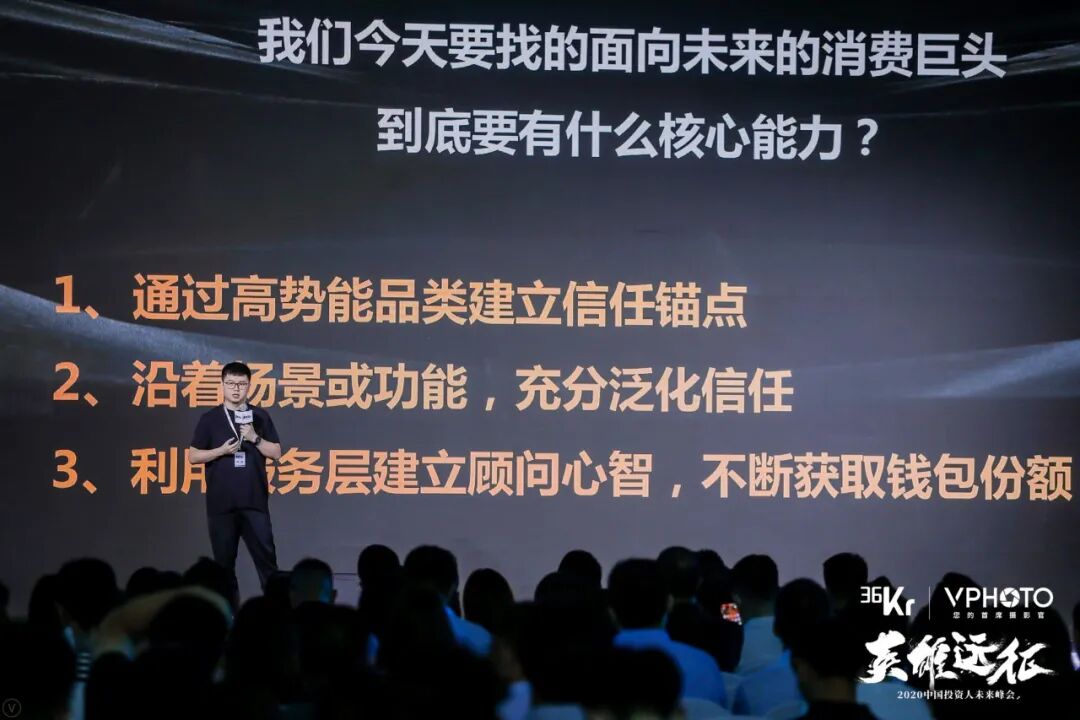

A plausible path to success for future consumer giants: establish trust anchors through high-potential categories; fully generalize that trust along natural scenarios or functions; leverage service layers to build an advisory mindset, holistically solving scenario and function problems, and continuously capture wallet share.

The following is a transcript of the speech, edited by 36Kr:

Thank you to 36Kr, and to the many industry veterans here today. I'll take 15 minutes to share some of Gaorong Ventures' thinking on the consumer sector. I'll divide this into two parts: the first part is more inductive, addressing why we believe there will always be VC opportunities in China's consumer sector; the second part is more deductive, offering our judgments on the new consumer landscape.

China's Consumer Sector Will Always Offer VC Opportunities

Gaorong Ventures began investing in new consumer brands quite early. We've been fortunate to accompany the growth of a number of outstanding companies, including Pinduoduo, Gaotu Techedu, Roborock, Perfect Diary, Genki Forest, Dingdong Maicai, Pupu Supermarket, Qian Damai, and Dewu App. In fact, consumer-focused VC as an asset management category is relatively uncommon worldwide. The explosive emergence of consumer VC in China over the past five years demands that we examine whether this opportunity represents a "one-time event" driven by the convergence of multiple tailwinds, or a "structural opportunity" that will persist for two to three decades or longer. How we characterize this opportunity and analyze its sources determines how we deploy capital and formulate our strategy. If the window is only three to five years, we move fast and strike fast; if it's a long-term opportunity, we commit to deep, sustained cultivation.

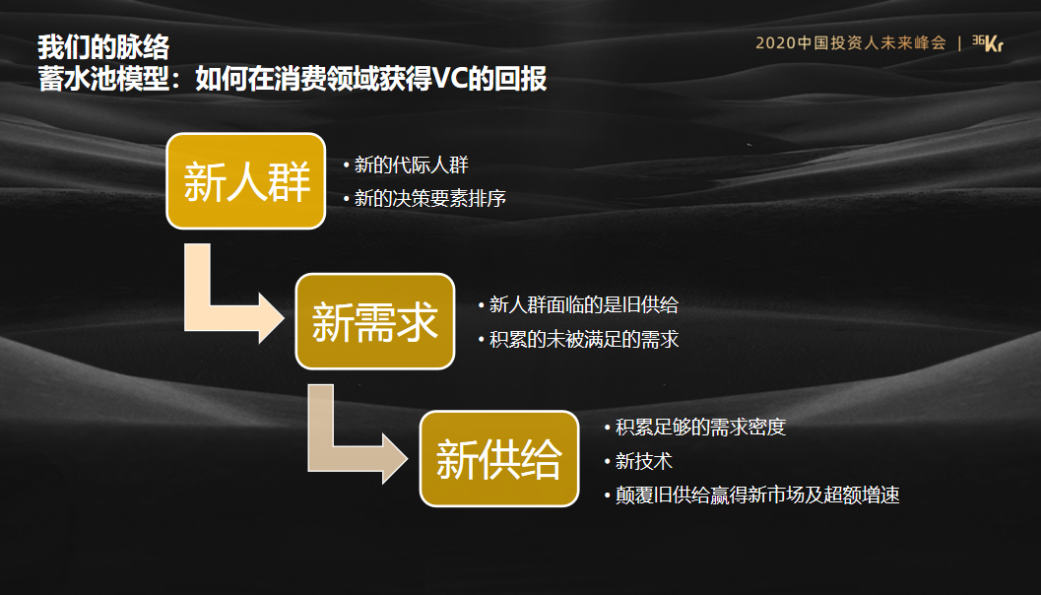

Regarding how to generate VC returns in consumer, we've developed a model — the reservoir model. Its three key elements: new demographics, new demand, and new supply. These terms are no doubt familiar to everyone; I'll briefly share our thinking on them.

If we call all new services or products in the market "new supply," these are undoubtedly driven by certain new demands. New demand can be deconstructed along infinite dimensions; for our purposes, we'll categorize it as one-time, cyclical, or structural.

One-time opportunities carry enormous fashion risk — last year's The Big Band, this year's Sisters Who Make Waves — and don't systematically suit VC investment. This is straightforward to understand. Cyclical opportunities, meanwhile, present two challenges: first, timing cycles is extraordinarily difficult for anyone; second, the best way to profit from cycles requires high liquidity — getting in when the wave comes, getting out when it recedes. So in practice, the pursuit of long-term returns isn't really a multiple-choice question for us. We have no alternative but to seek structural opportunities.

Where does structural new demand come from? The most reliable source is new demographics. It's important to emphasize that by "new demographics" we don't mean only young people; anyone entering a new life stage qualifies — newly retired, new second-child parents, new homeowners, newlyweds, new job holders... When a new generation enters a new life stage, and the weights and priorities in their consumption decision-making factors undergo significant change, opportunity is embedded within that shift.

How does the reservoir model operate? For new demographics entering new life stages, only old supply is available to serve them early on — and this old supply appears before them precisely because it served the previous generation of consumers so well. These new demographics' new demands aren't well-satisfied in the early stages. Under this mismatch, unmet demand begins to accumulate. As this unmet demand accumulates, it's like pouring water into a cup: initially nothing seems to change, but as more is poured, the center of gravity rises higher. At a certain point, whether because density or quantity reaches a critical threshold, or because of external stimuli such as technological progress, the cup tips over. That moment when the cup tips — releasing a flood of unmet demand — enables new supply to achieve excess growth, thereby meeting the return requirements of VC.

The pace of generational turnover in China is extraordinarily rapid. In the US or Japan, a term describing one generation might span ten or twenty years — Millennials, Baby Boomers, the Heisei generation. In China, we classify cohorts in five-year intervals or even shorter. As long as this rhythm of generational turnover persists, structural opportunities for VC investment in China's consumer sector will continue to exist.

From an investment perspective, the trends we seek should be directions that neither capital nor policy can easily alter. We select trends by observing changes in demand, observing which generational characteristics and which unmet demands are accumulating. For example: grocery shopping is a classic case — my mother, my grandmother, and I each make three different choices. Each generation has different channel preferences.

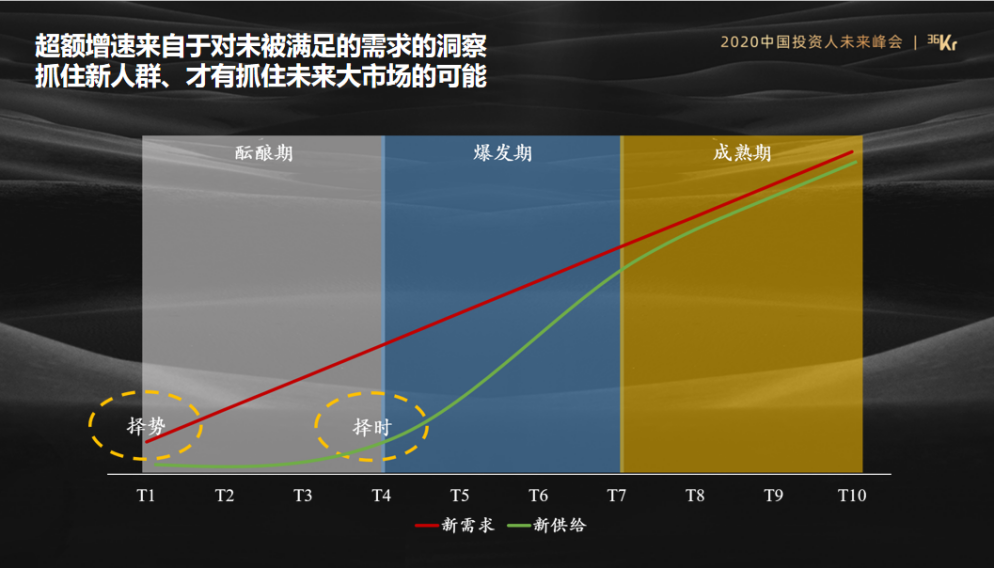

The greater challenge, we believe, is timing selection, which we approach by observing changes in supply. On one hand, we wait for unmet demand to accumulate to sufficient density to support new businesses; on the other hand, we wait for new technologies to emerge that make new supply more universally applicable. Whether through leading demand indicators or new technologies, transitional supply will appear that allows us to more preemptively detect the signal that "the building is about to collapse."

We divide the accumulation of new demand and the development of startups into three phases: incubation, explosion, and maturation. The red line represents the continuous accumulation of "new demand" — "selecting the trend"; the green line represents the emergence and evolution of "new supply" — "selecting the timing." During the incubation phase, there's no real opportunity for startups: even if everyone in this room were willing to pay a premium right now for some fish from Antarctica, the density of demand wouldn't be sufficient to sustainably support a startup. What we're waiting for is the moment "the cup tips over."

Take the pet industry — we love this sector, but haven't invested yet. The macro indicators all point in the right direction, including the usual suspects: urbanization rates, later and fewer marriages, shrinking living space, and so on. But why now? Why not ten years ago, or ten years from now? Some might prefer quantitative indicators for judgment, such as per-capita GDP reaching $10,000. But nature doesn't play in base-10 with humans; it's not as if people watch the evening news, hear that per-capita GDP has crossed $10,000, and decide to do something special. That isn't how factual logic works. Placed in historical context, similar quantitative indicators carry too much noise. What we seek are more qualitative indicators. For example, one key qualitative indicator we've hypothesized for the pet industry is: in China's super-first-tier cities or economically developed provincial capitals, has commercial pet funeral service emerged? The appearance of this business model indicates, first, that enough pets are dying, and second, that pet owners remain willing to pay after the pet has lost its key function — companionship. Sufficient demand density, sufficient willingness to pay — for us, the investment timing is more likely to have arrived. Finding such qualitative leading indicators for timing selection is extremely important for our investment deployment in any given sector.

What Do Perfect Diary, Dingdong Maicai, Pupu Supermarket, and Genki Forest Have in Common?

Next, I'd like to share some of our judgments on the future of the new consumer sector — more deductive in nature.

What do Perfect Diary, Dingdong Maicai, Pupu Supermarket, and Genki Forest have in common? In our view, these are all highly scenario-driven companies. Is Perfect Diary's core battlefield best described as Tmall, WeChat, or some kind of shelf? Our answer is that Perfect Diary's core battlefield is the vanity table — tightly surrounding women's desire to become beautiful, becoming their beauty advisor, and solving as much of the vanity table purchasing demand as possible. Dingdong Maicai's core battlefield is the dinner table: hard-to-brand demands like meat, fish, eggs, and vegetables are satisfied through Dingdong, and then condiments, rice, oil, and semi-finished products can ultimately be entrusted to Dingdong as well — trust accrues to the channel. Beyond defining Genki Forest as a sparkling water company or tea beverage company, a more accurate understanding is "sugar-free specialist" — any demand related to zero sugar and zero fat can be satisfied, with functionality as the primary label.

In the future, the association of "water" with Nongfu Spring or "chili sauce" with Lao Gan Ma will certainly persist. But we may need some new classification terms that emerge more naturally and align more closely with factual logic to define future-facing consumer companies. We believe scenarios and functions will replace categories as the primary label for future-facing consumer companies. Following this logic, we can consider whether new giants will emerge in physical scenarios such as the bedroom, the break room, the bathroom, the coffee table, or on the road, as well as around certain psychological scenarios — that is, functional classifications. These represent consumers' natural selection logic, and we believe this perspective will reveal many interesting opportunities.

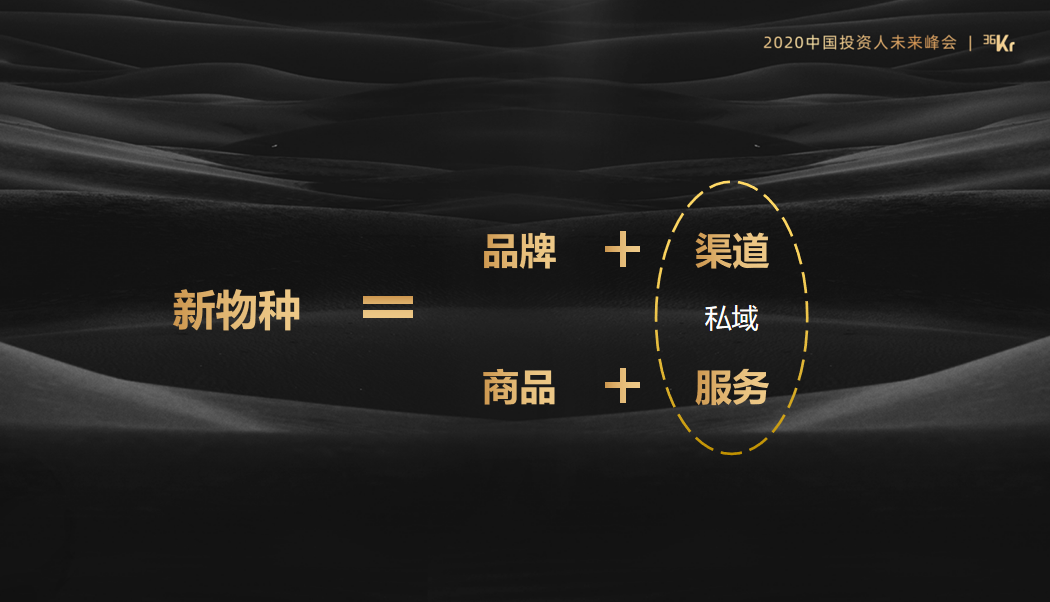

Furthermore, we see the boundary between products and services becoming increasingly blurred. Mention "vertical e-commerce," and many investors might even treat it as a negative term — believing opportunities in this track are slim under the "shadow" of e-commerce giants. Yet we still see Dewu and Weipaitang growing extremely rapidly. Providing very heavy service layers beyond the product itself will build moats that giants cannot easily reach due to inertia, as well as strong connections with consumers.

So, can we really clearly define today's new consumer companies as product or service, channel or brand? In the future, the convergence of product and service, channel and brand, will occur on a massive scale — packaged as complete products presented to consumers by new-species companies. If we express this as a formula, it looks like the following:

One point we want to emphasize: private-domain traffic for consumer companies is not merely an opportunity on par with Xiaohongshu, Weibo, or Douyin in the past. It represents a revolutionary infrastructure for consumer goods companies on a global scale for the first time in two to three decades — capable of providing consumer goods companies with direct channels to consumers and overlaying service layers. WeChat's private domain gives today's Chinese consumer new-species the opportunity to realize this formula.

With such an opportunity in hand, what battlefield do consumer companies face? We have a relatively pessimistic judgment here. Whether channel stratification, mental stratification in communication, or extensive decentralization — these are all familiar trends. Under these trends, today may not offer the same opportunity that existed over the past hundred years or decades to build businesses serving 80% of people, like Procter & Gamble or Coca-Cola. Today, for the vast majority of consumer startups, the opportunity may only be to serve 20% of people; to grow large, one must go deep — to capture 80% of the wallet share of that 20%. And this will inevitably involve extensive cross-selling. Our definition of brand: transferable trust is what constitutes a brand.

So, what core capabilities must the future-facing consumer giants we seek today possess? First, we hope these new species can establish trust anchors through high-potential categories. What is a high-potential category? A category that can accumulate transferable trust. A counterexample: toothpicks — even if we use a toothpick perfectly, it's difficult to pay attention to or remember its brand, let alone buy that brand's toothpaste or toothbrush. In fact, within each specific scenario and functional classification, we can identify categories that have historically been relatively difficult to trust or decide upon — these are also characteristics of high-potential categories. Second, future new species need to fully generalize trust along scenarios or functions. Third, leverage service layers to build an advisory mindset, holistically solving scenario and function problems, and continuously capturing wallet share. This is what we believe to be a plausible path to success for future-facing consumer giants.

A phrase that has become popular recently: from an entrepreneur's perspective, every consumer industry is worth rebuilding from scratch; from an investor's perspective, our conviction is that every industry is worth deconstructing from scratch. Whether future consumer giants can be discovered through past classification systems — we have substantial doubts. We look forward to more primary classification terms emerging that can more sharply help us identify revolutionary companies: what we call "old matters, new dimensions."

Gaorong especially hopes to work with all of you to seek out and support China's future-facing new consumer giants. Thank you, everyone!

When Traffic Is More Expensive Than Gold, How to Achieve Traffic Growth? | Gaorong Hub