Huatai United Securities' Jiang Yu: How Innovative Companies Can Navigate the Path to Listing in the Registration-Based Era | Ronghui

How Can Innovative Companies Seize the Registration-Based IPO Opportunity and Make the Right Capital Strategy Choices?

Since the launch of the registration-based IPO system in 2019, China's capital markets have been undergoing unprecedented transformation, bringing breakthroughs that were once unimaginable: more inclusive listing requirements, more predictable timelines, market-driven pricing mechanisms that give high-potential companies greater valuation premiums, and delisting mechanisms that foster a market ecosystem where the strong thrive and the weak are weeded out.

These breakthroughs have created entirely new securitization opportunities for high-growth startups — to create more value and incentivize more innovation. What are the fundamental conceptual and operational differences between the registration-based system and the previous approval-based system? What transformative trends will shape the next 5-10 years? As companies face more capital market choices, how should they align capital strategy with their business and product-market fit? Recently, at a capital strategy salon co-hosted by Gaorong Ventures and Tsinghua University's PBCSF Global Entrepreneur Leadership Program, Jiang Yu, Party Secretary and Chairman of Huatai United Securities, shared his insights on Navigating the IPO Journey for Innovative Enterprises in the Registration Era, drawing on cross-border capital market comparisons, hands-on STAR Market and ChiNext listing cases, and deep sector knowledge of the new economy.

The following is an edited transcript of Jiang Yu's remarks:

Today I'm delighted to join Gaorong Ventures and all the entrepreneurs here to discuss our understanding of the registration-based system, its impact on capital markets, and how innovative enterprises should craft capital strategy in this new era. Huatai United Securities is an investment bank focused on the new economy. Over the past decade, the transactions we've advised on represent over 1 trillion RMB in market cap. In the past five years, we've maintained a sector-driven approach, providing investment banking services to leading and growth-stage clients in TMT, consumer, healthcare, environmental protection, and advanced manufacturing — and we've participated in the wave of Chinese concept stocks and red-chip companies returning to domestic markets. Though we've helped numerous companies list on A-shares, I think their timing wasn't as fortunate as yours today. This year marks the 30th anniversary of China's capital markets. I believe what the registration-based system has accomplished in just two years, and the value it has delivered to Chinese enterprises, represents a revolutionary leap compared to the previous 28 years.

Truly Understanding the Registration-Based System: Four Major Changes

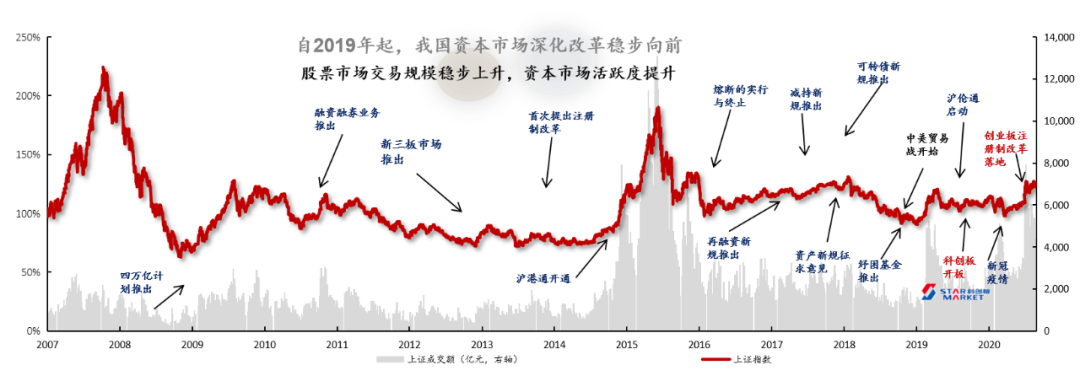

What changes has the registration-based reform actually brought? Since its 2019 launch, A-share secondary market indices haven't moved dramatically, but trading volume has risen significantly — the registration system's impact on market vibrancy has been substantial. What it fundamentally solves is a long-standing problem: outstanding, promising companies were unable to access A-shares for various reasons. As the saying goes, "the well-behaved child doesn't necessarily get good grades; the troublemaker might have the most growth potential." The registration system gives many promising companies a fresh chance.

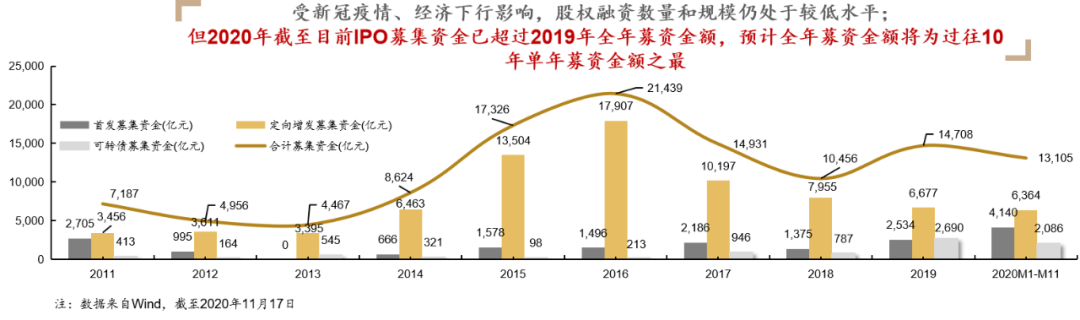

For a long time, China's direct financing has been suppressed. As shown in the chart below, China's total equity financing peaked at over 2.1 trillion RMB in 2016, but IPO fundraising hovered perennially below 200 billion RMB. IPOs were suspended nine times over 30 years, most recently in 2013. Since the registration system's implementation, 2019 IPO fundraising exceeded 250 billion RMB, and 2020 had already surpassed 410 billion RMB by November — a multi-decade record. Though still far from meeting Chinese enterprises' massive financing needs, this represents a future trend: under the registration system's influence, more quality assets will achieve securitization in A-shares, and we believe this trend will continue deepening.

China's registration-based system has now formed a basic institutional framework: with the 2020 revised Securities Law providing foundational legal safeguards; and both the STAR Market and ChiNext having established their own registration-based implementation systems. The 14th Five-Year Plan explicitly calls for "fully implementing the registration-based stock issuance system, establishing normalized delisting mechanisms, and increasing the proportion of direct financing."

A timeline for full registration-based implementation is being developed, with further acceleration expected. Recently, the CSRC announced plans to merge the Shenzhen Main Board and SME Board, after which both the Shanghai and Shenzhen main boards will adopt the registration system simultaneously — marking full A-share registration. This will establish genuine foundational market infrastructure, gradually replacing the visible hand that decides which companies can list and when with market-driven determination. To summarize the registration system: one core principle, three coordinations, and four changes. The overarching principles are marketization, rule of law, internationalization, and institutionalization.

The one core is information disclosure. For years under both the channel system and approval system, regulators made substantive judgments about corporate compliance and sustained profitability. For example, 40% of rejected M&A restructuring applications were due to inadequate disclosure of sustainable profitability — meaning companies lacking sustained profitability risked rejection. Under the registration system, issues of compliance, growth prospects, and future outlook are addressed through full information disclosure, with market participants making the judgments.

The three coordinations are: coordinated differentiated development across boards, coordinated comprehensive supporting reforms, and coordinated reforms for both existing and new boards — with the STAR Market as incremental reform and ChiNext as existing board transformation.

The registration system has brought four important changes to A-share capital markets.

Change 1: More Inclusive Listing Standards

The first change is making listing standards more inclusive. Previously, listing eligibility centered on profitability. Though the main and SME boards had multiple standards, in practice most companies passing CSRC IPO review had profits above 50 million RMB in the year before listing. Under the registration system, both the STAR Market and ChiNext have abandoned profitability as the core criterion, designing instead five and three market-value-centered standards respectively.

For example, the STAR Market's five standards: if expected market cap is at least 1 billion RMB, there are corresponding revenue and profit requirements; if unprofitable, market cap must be at least 1.5 billion RMB with revenue of at least 200 million RMB in the most recent year — a higher revenue bar; if expected market cap exceeds 4 billion RMB, revenue requirements can even be waived, as for innovative drug companies. This is a groundbreaking breakthrough — unprecedented in the 28 years before registration-based reform. This inclusivity allows innovative, earlier-stage companies in high-tech, healthcare, and other sectors to access the STAR Market.

ChiNext's three standards follow similar principles. Standard One requires profitability — positive profits in the last two years with cumulative net profit of at least 50 million RMB. The other two standards are market-value-centered with certain revenue requirements. Currently, ChiNext differs from the STAR Market in that loss-making companies cannot list for one year, but this will open up afterward. That loss-making companies can list was previously unimaginable.

Registration-based inclusivity also manifests in two additional ways. First, dual-class share structures are now permitted. For many companies, control rights are a pain point, often addressed through AB shares — previously barred from A-shares, but now allowed on both the STAR Market and ChiNext, subject to market cap and corresponding revenue/profit requirements. This too is historic.

Second, red-chip companies can now list. For decades, only companies incorporated in mainland China could access A-shares — a single provision that drove so many Chinese companies overseas. Now A-shares have opened: sufficiently large market cap allows STAR Market and ChiNext listings. Red-chip companies already listed overseas — including CSPC Pharmaceutical, Geely Auto, and SMIC — now have expanded capital market options.

Change 2: More Efficient, Transparent, and Predictable IPO Review

The second major change is more predictable listing timelines. Previously, one of the biggest pain points was extreme uncertainty in listing cycles. In practice, a year and a half was considered fast. This unpredictability deterred many companies from pursuing A-shares.

Under the registration system, review is more efficient and transparent. In recent years, CSRC average review time exceeded 400 days; under registration, it's basically six months. The entire process is transparent, with companies responding to rounds of inquiries. Compared to the main and SME boards under the approval system, the STAR Market and ChiNext have far fewer questions per inquiry letter — enhancing materiality and specificity while drastically reducing generic questions.

As of November 2, 2020, the STAR Market had accepted 469 IPO applications, ChiNext 423 — with each stage from acceptance, inquiry, approval or deferral, to registration submission and result, clearly delineated.

US and Hong Kong listing cycles are basically 6-9 months, so STAR Market and ChiNext timelines under registration have essentially aligned with international standards. Last year, the STAR Market's first batch was even faster — 25 companies approved in three months. Including Huatai United Securities-advised HYC Technology, the "first STAR Market IPO," which went from acceptance to issuance in just 89 days — "China speed." Under normal circumstances now, a six-month review cycle is predictable.

Change 3: Market-Driven Pricing Enables Efficient Resource Allocation

The third change, which everyone cares deeply about, is that market-driven issuance pricing under the registration system enables efficient resource allocation. For years, A-share IPO pricing was constrained by a "23x P/E ratio" cap for various reasons. Now both the STAR Market and ChiNext have broken this control, letting the market set new issue prices. However, STAR Market market-driven pricing differs from pure market pricing in the US and Hong Kong: institutional investors submit bids, but with price guidance — not exceeding the median and average of valid bids after excluding highest quotes. Even so, relative to the past this represents a historic breakthrough.

We can see that the current average IPO P/E ratio on the STAR Market stands at 69x, and since its launch over a year ago, listed companies have seen their share prices rise an average of 150% from their issue prices. Additionally, 40% of STAR Market companies have raised more than RMB 1 billion — a funding scale that similarly sized companies could not access on the main board or SME board.

Moreover, companies in sectors favored by A-share investors, such as biopharma and internet information technology, are commanding higher valuations. However, we need to recognize that such valuations may not be sustainable.

Change 4: Delisting Mechanisms Reflect Marketization and Rule of Law

The final important change concerns delisting mechanisms. We've discussed the entry points to the A-share market, but a major historical problem has been the blocked exit — no survival of the fittest. Over 30 years, China's capital markets have delisted fewer than 200 companies total. This has created a dysfunctional ecosystem where good companies couldn't get in and bad ones couldn't get out. Under the registration-based system, both the STAR Market and ChiNext have redesigned their delisting mechanisms. First, they established four categories of mandatory delisting conditions: trading-based, financial, compliance-based, and major violation-based. Previously, delisted companies could apply for relisting, but the STAR Market and ChiNext now clearly stipulate that forced delisting under any of these four conditions permanently bars relisting.

This makes the capital market exit much smoother. Mandatory delistings have increased in the past two years, though the gap with international markets remains significant. We believe that on this foundation, the ecosystem will gradually optimize and truly enable survival of the fittest.

Many are also concerned about the positioning differences between the STAR Market and ChiNext — the two are filling complementary roles through market-based development.

Regarding the STAR Market's positioning, official documents specify "three orientations" and "six industries." The three orientations are: facing the global frontier of science and technology, facing the main battlefield of the economy, and facing major national needs. The six industries are: next-generation information technology, high-end equipment, new materials, new energy, energy conservation and environmental protection, and biopharmaceuticals.

In plain terms, the STAR Market has a distinctive feature: "sci-tech innovation attributes," emphasizing "hard tech." To list on the STAR Market, companies need recognition of these innovation attributes. Currently there are three main quantitative standards: R&D investment, patents, and revenue. However, beyond these quantitative metrics, substantive judgment of innovation attributes remains important.

ChiNext complements the STAR Market, emphasizing "three innovations and four new elements." The "three innovations" are innovation, creation, and creativity. The "four new elements" refer to new technologies, new industries, new business forms, and new models. ChiNext also maintains a negative list: traditional industries including agriculture, forestry, animal husbandry and fishery, mining, and construction cannot list. However, traditional industries that achieve integration and innovation with internet, big data, cloud computing and other technologies — especially business model innovators — can list, including some consumer companies.

Differences in IPO Review Focus: Registration-Based vs. Approval-Based Systems

The registration-based system's IPO review priorities differ from the approval-based system. For certain matters, the standard of "principally constituting an issuance and listing obstacle" has shifted to "intermediaries exercising prudent judgment." Specific monetary thresholds or ratio requirements for certain matters have been eliminated, moving away from one-size-fits-all review approaches.

We've summarized 11 notable differences in review focus. Take competing business issues: under the approval-based system, requirements were extremely strict, but the registration-based system is more flexible, emphasizing "substance over form" and focusing on whether material adverse effects exist and potential future competing business may arise.

The approval-based system had higher standardization requirements. For example, fundraising projects had rigid requirements for land acquisition — without the corresponding land certificate, the process couldn't proceed. Under the registration-based system, there's no rigid requirement; companies need only disclose their land acquisition plans, specific arrangements, and timeline.

For spin-off listings, under the approval-based system, assets partially sourced from listed companies couldn't list; "big A wrapping small A" was prohibited, involving definitions of "duplicate listing." Currently, spin-off listings have been liberalized and are more flexible.

Regarding historical evolution: previously, if there were deficiencies such as insufficient or unsubstantiated historical capital contributions, or accumulated unrecouped losses at restructuring, companies had to resolve these and then operate for 36 months — a very long cycle. Now it's different: after making up and correcting these issues, there's no operating period requirement. The shortened A-share listing cycle is actually achieved through these technical breakthroughs.

On valuation adjustment mechanisms (VAM agreements), the registration-based system no longer absolutely prohibits VAM clauses.

The registration-based system shows greater tolerance for litigation. For lawsuits not involving main assets or core technology, and not having material impact on ongoing operations, companies may pass review while litigation is pending.

The "three types of shareholders" issue has also been liberalized — proper information disclosure suffices now, whereas they previously had to be cleared before listing.

For shareholder identification in mergers under common control, VIE structures previously constituted substantive obstacles. Now VIE structures are accepted, with intermediaries required to explain the rationale, reasonableness, authenticity, trusts, nominee arrangements, and control stability.

Previously, if performance declined between approval by the issuance review committee and final issuance authorization, it would materially affect final approval. Now, after passing review, as long as the performance decline doesn't exceed 50%, issuance can proceed.

Customer concentration follows the same pattern: previously there were quantitative thresholds; now proper information disclosure and risk revelation suffice.

For related-party transactions, the registration-based system focuses on completeness, legality, necessity, reasonableness, and fairness of related-party and transaction disclosure, with information disclosure as the primary approach.

These 11 points support our argument for why the registration-based system is more inclusive and can better control listing timelines — these are very important for companies. In summary, the registration-based system makes information disclosure central, delegating more choice to the market and intermediaries.

What Trend Impacts Does the Registration-Based System Bring?

So what trend impacts does the registration-based system bring? Why do we say China's capital markets are undergoing major transformation, bringing tangible benefits to enterprises, technological innovation, and capital exits? When capital market reform has been elevated to national strategy, we believe the following important impacts will follow.

Impact 1: Significant Room for A-Share Securitization Rate Growth; Listed Companies to First Increase, Then Decrease

First, the A-share securitization rate still has significant room to grow. From a macro perspective, China's current securitization rate is only about 60%, compared to roughly 160% in the U.S. — a large gap, equivalent to U.S. levels in the 1970s-80s. This upside represents more opportunities for companies to securitize. Of course, listing is not the end-all; rather, companies have opportunities to seize and grow.

U.S. listed company numbers peaked in the mid-1990s at over 8,000, later falling to around 4,000. A-shares currently have over 4,000 listed companies; we believe under the registration-based system, this number will continue rising in coming years — reaching 10,000 wouldn't be exaggerated. Of course, there will be a pattern of first increasing, then decreasing, with survival of the fittest.

Impact 2: Further Capital Market Differentiation; Market Cap and Liquidity Concentrating in Leading Companies

With market-based resource allocation mechanisms taking effect, China's multi-layer capital market is gradually forming. China has already established a multi-layer structure: below are OTC markets including broker counters and regional "fourth boards"; above is the NEEQ (New Third Board). Exchange-traded markets include the STAR Market, ChiNext, SME board, and main board. After full implementation of the registration-based system, this will consolidate into two tiers — main boards of both exchanges (no more SME board), plus ChiNext at SZSE and STAR Market at SSE.

Future A-share market cap distribution and liquidity will converge toward Hong Kong and U.S. patterns. U.S. and Hong Kong markets have already formed highly differentiated structures where the top 20% of companies by market cap account for over 90% of total market cap and trading volume. I believe this is also the future trend for A-shares: while aggregate scale explodes, structure further differentiates. Currently, A-share companies with market cap above RMB 10 billion account for 31% of listed companies but 84% of total market cap. I believe over time, trading volume will further concentrate in leading companies.

Impact 3: Market Valuation Premium for Companies in Growth Industries

Currently we see that emerging industries supported by national strategy — including biopharma, internet information technology, and high-end manufacturing — command high issuance P/E ratios in A-shares: biopharma averages over 80x, internet over 60x, high-end manufacturing over 40x. We've also seen loss-making or barely profitable companies list on the STAR Market in the past two years, with some exceeding RMB 50 billion market cap — unimaginable just three years ago. This reflects the A-share market's valuation premium for growth industries, which is considerably attractive.

Impact 4: Industry Upgrading, Governance Optimization and Other Factors Driving M&A

We believe genuine market-based consolidation and industrial M&A will occur in A-shares in coming years, driven by industry evolution, technological change, governance optimization, and financial environment shifts. The U.S. had M&A waves triggered by the 1990s information technology revolution, and rising M&A scale driven by continuous interest rate cuts from 2009. We believe A-share industrial consolidation and M&A will further develop. In other words, leading companies will have opportunities to acquire others, and many companies will have opportunities to be acquired by leaders. In the A-share market's ongoing structural adjustment, this will provide increasing opportunities for entrepreneurs with real vision and capability — this is the profound change in future capital markets.

How Should Companies Make Capital Strategy Choices?

Under the new opportunities brought by the registration-based system, how should companies make capital strategy choices? Beyond A-share listing being relatively easier with shorter timelines, companies face more choices when selecting capital markets.

Overall, for listing venue and board selection logic, beyond considering whether hard requirements are met or acceptable costs of compliance, companies should make comprehensive judgments from perspectives including specific revenue models, R&D characteristics, market liquidity, and shareholder exit needs. On this foundation, when choosing listing venues, market demand needs increasing consideration: where are your customers? Where are your users? Where is your market? Choosing a listing venue close to your business layout and product markets, where investors better understand your commercial story — this is very important. Recently we've also seen many large consumer and internet companies returning to A-shares, all considering their own user bases.

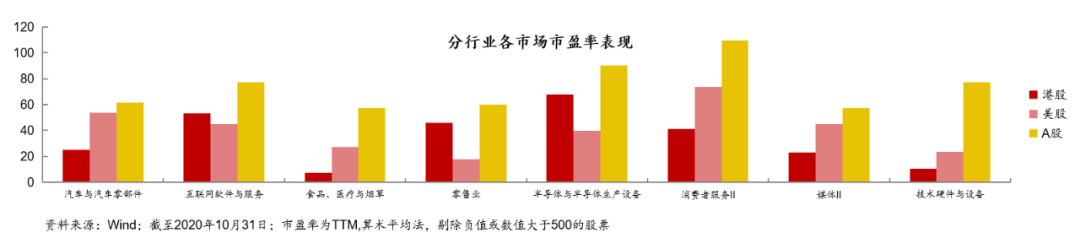

Let's compare Chinese companies' industry and market cap distributions across domestic and overseas capital markets. U.S.-listed Chinese companies are predominantly tech companies; Hong Kong has more even industry distribution; A-shares are dominated by capital goods, materials, healthcare, and consumer products. However, A-share valuation levels for healthcare, high-tech, and services companies are not low. Across A-share boards, the STAR Market leads in both valuation and fundraising capacity, with P/E ratios reaching 100x and ChiNext around 60x. A-share industry P/E ratios generally exceed Hong Kong's; excluding financials and petrochemicals, the overall A-share P/E valuation is 40x.

There's another major opportunity worth noting. Secondary listings, cross-border listings, homecoming listings, and spin-offs are becoming mainstream, giving companies more options to consider A-shares. Today we're seeing many leading companies choose Hong Kong for secondary listings, but in fact both the Shanghai and Shenzhen exchanges are now considering opening up to second listings as well. More and more high-market-cap, high-potential red-chip companies are returning. Quality companies are also making full use of both A-share and Hong Kong markets through A+H cross-market offerings — for example, A-share quality companies like Tigermed going public in Hong Kong. Spin-offs are also increasing, including A-share listed companies spinning off subsidiaries for Hong Kong listings, and the STAR Market providing a channel for Hong Kong tech innovation companies to spin off and return to A-shares. These were all unimaginable in the past, but are gradually becoming mainstream.

For growth-stage companies, equity incentives are a major concern, and the registration-based system provides corresponding tools. Before IPO, companies planning to go public can use direct shareholding by core personnel, employee shareholding platforms, or stock options for equity incentives. In the past, companies with option plans could go public directly in the U.S. and Hong Kong, but not in A-shares — options had to be exercised or exited before IPO. Now that's all opened up. This is an excellent solution the registration-based system brings to growth-stage companies. Both the STAR Market and ChiNext now explicitly allow senior management and core employees to participate in strategic placements through dedicated asset management plans at IPO, which can serve as effective incentives with certain advantages in terms of tax treatment and other conveniences.

Of course, we need to be clear: IPO is a hot topic right now, but against the backdrop of A-share differentiation, even though the channel has widened, it still faces a situation of "thousands of troops and horses crossing a single-log bridge." In the past, we spoke of the "dammed lake" under the approval-based system, with hundreds of companies queuing at the CSRC; under the registration-based system, more than 300 companies have passed review this year, but there are still 700 to 800 companies queuing for the STAR Market and ChiNext. So although more companies are getting listed, more want to list — especially in technology and healthcare, where companies are going public much earlier than in the past. And we see that Hong Kong's listing rules have low barriers, yet only about 100 to 200 companies list there each year. That's the power of market forces, because ordinary companies don't get corresponding valuations. A-shares will be the same in the future.

One more point worth mentioning: going public is not the only ultimate path to capitalization for startups. Industry-based M&A is also an important channel. For American entrepreneurs and investors, selling control to PE firms or listed companies is a more common exit channel than IPOs or reverse listings. I once saw a survey pointing out a huge difference between Chinese and American entrepreneurs: 80% of American entrepreneurs consider selling a success; but 80% of Chinese entrepreneurs consider being acquired not a success — only ringing the bell at an IPO is success. This may reflect cultural differences between China and the U.S. But from a rational perspective, with structural changes in A-shares, survival of the fittest is an objective law. If a company can achieve a good acquisition while still in a growth phase, that's also a favorable channel for realizing enterprise value.

What Are the New Capitalization Trends in New Economy Sectors?

Finally, let's share some capitalization trends across major new economy sectors, with a focus on what institutional investors care about. Under the registration-based system, more discretion has been handed to the market and to institutional investors. Currently A-shares are colloquially a "retail investor market," with retail investors accounting for 40-50% of the entire market, but in overseas capital markets institutional investors account for roughly 60-80%. The institutionalization of A-share investors is a major trend going forward. Currently primary market pricing is dominated by professional institutional investors; after listing, institutional investors also lead due to "herd effects." We've also summarized what kinds of companies in major new economy sectors can win institutional investors' favor.

1. Consumer Sector

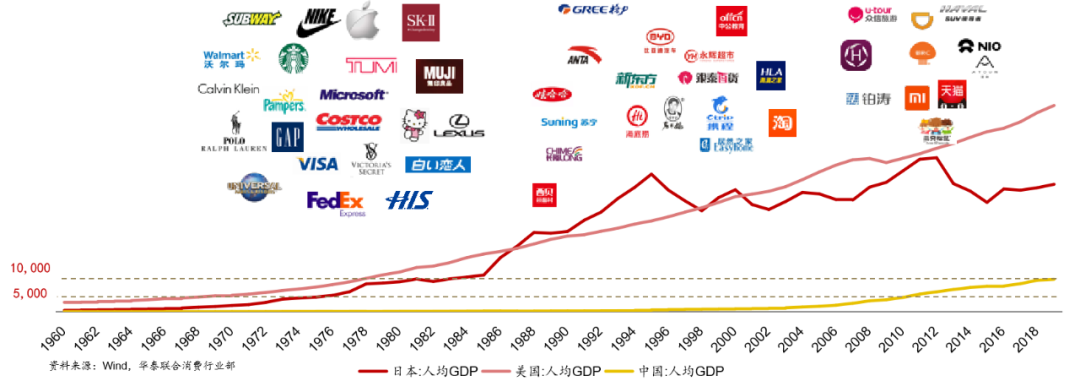

In the 1970s in the U.S. and 1980s in Japan, when per capita GDP entered the $5,000-$10,000 range, a wave of new brands emerged to capture consumption upgrades. Today China's per capita GDP has also reached roughly $10,000, ushering in a golden era for Chinese consumer brands. We believe three categories of brands will continue to attract capital: first, heritage brands with accumulated prestige, such as Moutai and Wuliangye; second, consumer products and channel brands that have grown rapidly through technological and channel revolutions, such as Alibaba and NIO; and third, brands filling market gaps as the market upgrades, such as Huazhu Hotels, Haidilao, and Easyhome.

In recent years, the market capitalization of China's listed consumer companies as a percentage of GDP has risen year by year, currently exceeding 23%. Compared to the U.S. at over 33%, there's still about 10 percentage points of upside. Combined with China's vast consumer market and the evolution of niche sectors, and against the backdrop of the registration-based system rollout, consumer companies are expected to find more capitalization opportunities in A-shares. And although the absolute P/E ratios of A-share consumer companies are lower than healthcare and TMT, A-share consumer listings still enjoy valuation advantages compared to U.S. and Hong Kong stocks, with average P/E ratios exceeding 41x.

2. TMT Sector

The TMT sector has several cutting-edge niche tracks, including intelligent manufacturing, semiconductors, 5G, IDC, and cloud computing, with numerous companies in these industries listing on the STAR Market. Currently among the more than 400 companies accepted by the STAR Market, TMT accounts for nearly 60%: 68 related to 5G, 46 to semiconductors, 39 to IDC, and 57 to intelligent manufacturing. Among the more than 400 companies accepted by ChiNext, TMT accounts for nearly 40%: 18 related to 5G, 8 to semiconductors, 18 to IDC, and 12 to intelligent manufacturing. It's fair to say these major industries are broadly recognized by market participants.

3. Healthcare Sector

We believe healthcare services will similarly have opportunities for chain-based scaling, much like consumer brands. With policy encouragement, private healthcare institutions are seeing rapid development opportunities outside the public hospital and community health systems, with the internet also enabling consumer healthcare services. Currently in specialized fields such as medical aesthetics, gynecology, and ophthalmology, private healthcare institutions have developed replicable chain models. We believe these healthcare services will present many securitization and capital operation opportunities going forward.

Additionally, domestic innovative drugs have remained a persistent hotspot in the pharmaceutical industry in recent years, with some blockbuster innovative varieties beginning to emerge, accompanied by a wave of quality companies listing on the STAR Market and ChiNext. From early last year to now, A-share healthcare valuations have risen steadily, with P/E ratios at one point exceeding 60x, substantially above both the overall A-share valuation level and U.S. and Hong Kong healthcare market valuations during the same period.

Going forward, China's pharmaceutical industry — including pharmaceutical manufacturing, medical devices, pharmaceutical distribution, and healthcare services — will give rise to high-growth companies. We believe these enterprises will be highly sought-after after entering capital markets.

To summarize, we believe today truly is an exceptional era. Overseas, we see the highly developed U.S. capital market, where capital markets have become a key that unlocks solutions, supporting the high-speed growth of strategically important industries across different eras over the past several decades — including software, high-end equipment manufacturing, and healthcare. Today, China's capital markets have been elevated to the level of national strategy.

For entrepreneurs, everyone is engaged in highly creative, enormously challenging work, pursuing entrepreneurship and customer value creation with tremendous passion. Without sustained capital companionship, it would be difficult to maintain sustainable momentum. The same is true for capital: without active capital markets, there are no exit channels, which means no genuine long-term capital willing to enter industries and sustain the capital cycle.

China's capital markets today face an entirely new strategic opportunity. Only through capital market reform can we truly unlock vitality, truly achieve effective incentives for innovation, and allow capital that accompanies enterprise innovation and entrepreneur growth to obtain relatively satisfactory returns through capital markets — thereby forming a positive cycle. As practitioners, we feel deeply honored, and look forward to accompanying more new economy enterprises to achieve greater growth in this great era!

About Huatai United Securities

Huatai United Securities Co., Ltd. ("Huatai United") is a specialized subsidiary pioneered by Huatai Securities Co., Ltd. ("Huatai Securities") within the industry, focused on providing investment banking services. It is committed to providing comprehensive financial services to governments, enterprises, and institutional investors. Leveraging the strong capabilities of parent company Huatai Securities, Huatai United has established a "specialized division + systematic collaboration" large investment banking business model. Oriented toward the human resources goal of "client manager + product specialist + industry specialist," it provides clients with efficient and targeted investment banking professional services through a full-service-chain system. Huatai United consistently ranks among the industry leaders in equity underwriting and sponsorship, M&A restructuring, and bond underwriting.

Huatai United maintains offices or liaison institutions in Beijing, Shanghai, Nanjing, Shenzhen, Hangzhou, and Hong Kong. Adhering to a "client-centered" business philosophy, Huatai United focuses on industry concentration, regional layout, and client depth cultivation, strengthening cross-market collaboration across domestic and overseas, exchange and over-the-counter markets, increasing support for technology and innovation enterprises, and comprehensively enhancing full-product service capabilities and rapid comprehensive service response capabilities.