The Beijing Stock Exchange Sets Sail: A Rational IPO Planning Guide for Startups | Ronghui Practical Insights

CITIC Securities Construction Li Xudong: Key Highlights of the Beijing Stock Exchange Regulatory Framework

On November 15, the Beijing Stock Exchange (hereinafter referred to as the "BSE") officially opened for trading. In its first week of operation, listed companies recorded a combined turnover of 21.2 billion yuan; as of the November 19 close, the total market capitalization of the first batch of 81 listed companies reached 269.596 billion yuan.

The BSE is positioned to serve innovative small and medium-sized enterprises (SMEs), and its institutional arrangements reflect inclusiveness toward innovative companies. It is also seen as "expanding the scope and depth of the registration-based IPO system in Shanghai and Shenzhen in the future." How should we understand the positioning differences between the BSE and the ChiNext board and the STAR Market? What regulatory points should entrepreneurs pay close attention to? How should IPO application timelines be planned?

On November 24, Li Xudong, member of the Investment Banking Committee and Managing Director at CSC Financial, shared his interpretation of BSE policies and offered pragmatic, rational IPO planning guidance for startups at Ronghui's online session. Drawing on his extensive experience with the registration-based IPO system and deep involvement in the New OTC Board (NEEQ) and BSE reforms, Li provided valuable insights. Among the BSE's first batch of 81 listed companies, CSC Financial served as the sponsor for 12 — ranking first.

The following is Li Xudong's presentation (edited for clarity):

First, let's review the BSE's performance during its opening week, which can be described as a "strong start." A total of 81 companies successfully listed in the first batch, including 71 companies transferred from the Select Layer of NEEQ and 10 newly issued companies. Looking at the industry distribution of these first-batch listed companies, they are mainly concentrated in five sectors: industrials, information technology, healthcare, materials, and consumer discretionary.

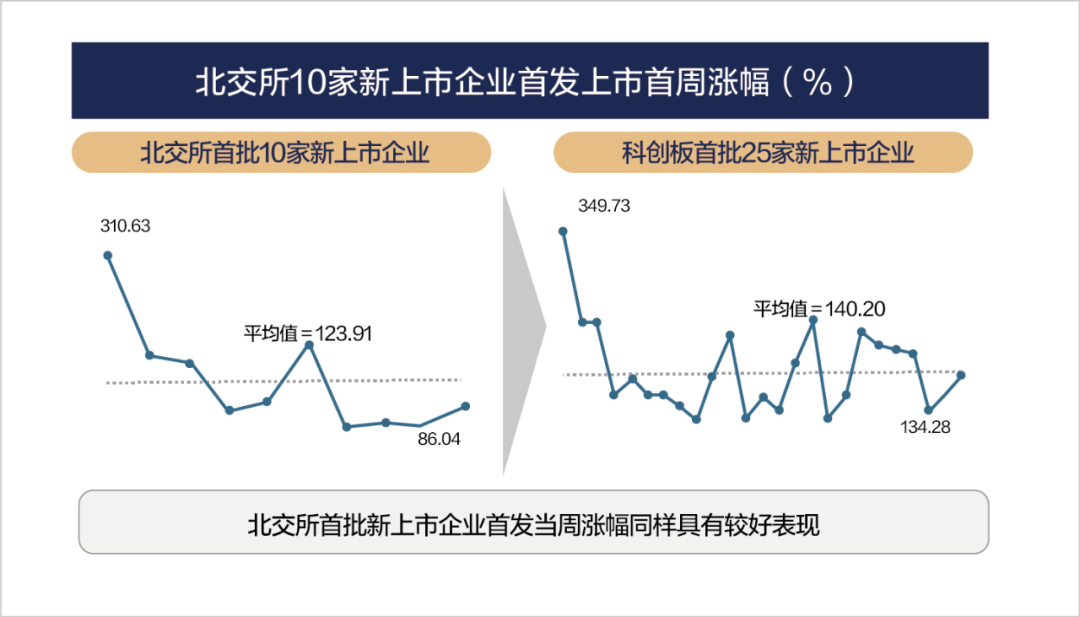

In terms of first-week price performance, the overall results were quite positive. The average gain for the BSE's first batch of 10 newly listed companies reached 123.9%, indicating strong investor interest.

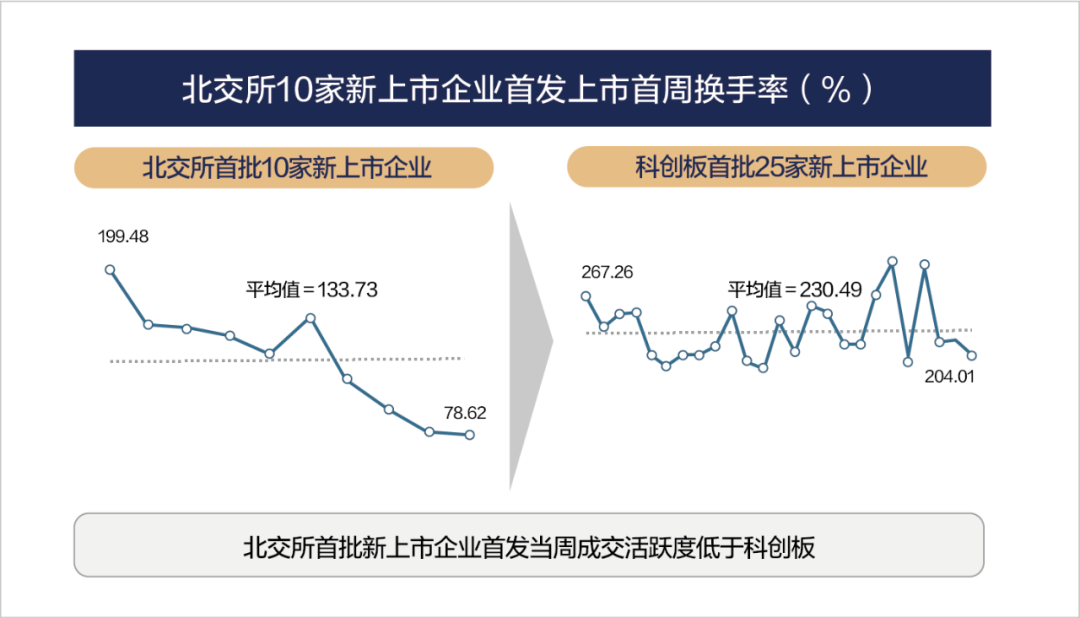

Regarding turnover rate, the average first-week turnover for the BSE's first batch of 10 newly listed companies reached 133.7%. Compared to the average first-week turnover rate of over 230% for the STAR Market's first batch of listed companies, there is still a noticeable gap.

This result stems from a combination of factors: First, investors are still in a process of re-evaluating and understanding the BSE; second, investor account openings are accumulating — currently there are over 4.3 million BSE accounts, compared to nearly 8 million on the STAR Market; third, the proportion of tradable shares also plays a role, as BSE-listed companies have a significantly higher float ratio compared to the STAR Market. The investor composition of the BSE has already converged with that of the STAR Market, encompassing PE and VC firms, public and private funds, and high-net-worth individuals. Going forward, investor participation and market liquidity can be expected to improve.

Before formally introducing the BSE's institutional framework, let's review the overall situation of the A-share IPO market in 2021.

Three Key Characteristics of the 2021 A-Share IPO Market

The 2021 A-share IPO market displayed several notable features:

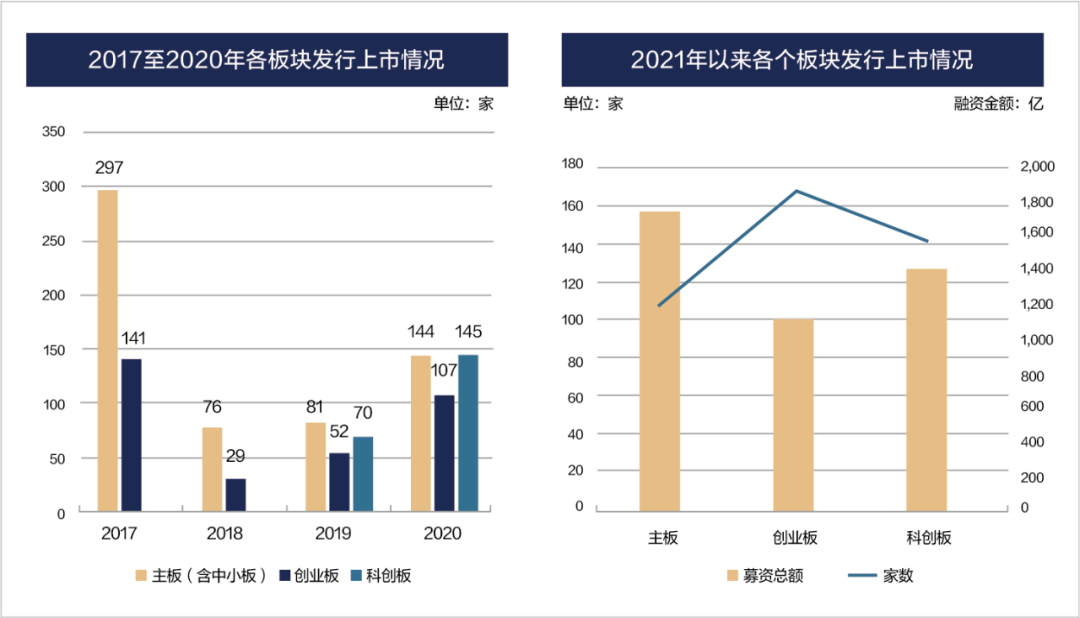

First, the normalization of IPOs continued to advance. As of November 19, the number of IPOs in the A-share market reached 419, with 2021 expected to set a record for the highest number of IPOs in a single year — including 110 on the Shanghai and Shenzhen main boards, 168 on ChiNext, and 141 on the STAR Market. With the addition of BSE listings next year, the total number of A-share IPOs in 2022 is projected to exceed 500.

Second, pricing has become more market-oriented. Under the previous registration-based IPO inquiry system for ChiNext and the STAR Market, there was a phenomenon of deliberately suppressing offering prices, forcing many companies to price "at the floor." After listing, their share prices would frequently surge several-fold. This situation changed after the issuance and underwriting rules reform on September 18. The main direction of the reform was adjusting the maximum quotation exclusion ratio from "no less than 10%" to "no more than 3%," and moderately weakening the regulatory requirement that pricing must not exceed "four values." The fully market-oriented inquiry system has led to more varied price-to-earnings ratios for new issuances, with overall valuation levels roughly doubling. Of course, some companies have also experienced post-IPO price drops. These should be viewed rationally — they represent the growing pains that a market-oriented issuance system must go through.

Third, IPO review has placed greater emphasis on board positioning and industry orientation. Since 2021, the STAR Market has further emphasized its "hard tech" attributes. Whether through the "4+5" standards for sci-tech attributes or the substance-over-form principle, the trend has been toward stricter enforcement. ChiNext reviews have also shown increased attention to board positioning. This places higher demands on investment banks in project selection and on companies in choosing their listing board. In terms of review timelines, the STAR Market generally takes 6-9 months from acceptance to issuance, while ChiNext's review cycle is around 12 months.

Understanding the BSE's Overall Positioning: Serving "Earlier, Smaller, and Newer" Companies

1. Background and Deeper Significance of the BSE's Establishment

The establishment of the BSE carries meaning at three levels. First, from a national perspective, it is an important measure to promote balanced economic development between northern and southern China. The Yangtze River Delta and Pearl River Delta already have the Shanghai and Shenzhen exchanges respectively; establishing the BSE helps leverage agglomeration effects to promote development in the Beijing-Tianjin-Hebei region and the Bohai Rim.

Second, from the perspective of capital market development, the BSE serves to improve the multi-layered capital market system and meet the needs of innovative SMEs. While ChiNext and the STAR Market have played significant roles in supporting sci-tech enterprises, ChiNext currently cannot accommodate loss-making companies, and although the STAR Market can, it primarily targets hard-tech companies with relatively mature business models. For innovative SMEs with leading technology but still in the early stages of industrialization, effective capital market support has been difficult to obtain. The BSE effectively fills this gap.

Third, the BSE is very important for Beijing's development. As the nation's financial management center, Beijing should also take a leading role in capital market reform. The BSE is the third stock exchange established in China's 30-year capital market history and the third board to implement the registration-based IPO system. It must both learn from the best practices of the STAR Market and ChiNext, and innovate and break new ground in the scope and depth of the registration-based system. The establishment of the BSE will also further support Zhongguancun's new round of pilot reforms and drive the development of Beijing's high-precision industries.

2. Overall Approach and Distinctive Features of the BSE

Let's briefly review the reform history of the NEEQ. In 2006, the share transfer system for Zhongguancun Science Park was established — this was the earliest version of the NEEQ. In 2014, with State Council approval, the share transfer system was upgraded from a regional market to a national market. From this point until 2016, due to the slow pace of IPO approvals, many companies used the NEEQ as an important financing venue, and the number of listed companies rapidly exceeded 10,000. As listings increased, companies varied significantly in quality, scale, and regulatory compliance, leading to calls for tiering to establish differentiated institutional arrangements. In 2016, the NEEQ introduced the Innovation Layer, but without substantive institutional improvements. Some quality companies chose to pursue IPOs, while others delisted, and the NEEQ fell into difficulty. However, NEEQ reforms never stopped. In 2020, the NEEQ established the Select Layer and introduced public issuance and continuous auction mechanisms, forming the market structure of "Select Layer, Innovation Layer, and Base Layer."

The overall approach for establishing the BSE follows the principle of "step-by-step implementation, gradual progress," broadly transferring the foundational institutions of the Select Layer. NEEQ Select Layer companies were transferred to the BSE to become BSE-listed companies. Going forward, to list on the BSE, companies must first be listed on the NEEQ for 12 months and enter the Innovation Layer before applying for a BSE IPO. This creates a tiered, progressive market structure.

The BSE's core positioning is "serving innovative SMEs." What are innovative SMEs? In six words — earlier, smaller, and newer: earlier stage of industrial development, relatively smaller operating scale, and newer technological level. Such companies have promising prospects but relatively unproven business models, not yet fully realized operating performance, and greater development uncertainty — yet they urgently need capital market support. Aligned with these company characteristics, the BSE's institutional arrangements demonstrate strong inclusiveness — accommodating the immaturity, uncertainty, and certain regulatory imperfections of innovative SMEs during their development process. Of course, malicious fraud and lack of integrity are absolutely not tolerated.

The BSE must also properly manage "two relationships." On one hand, it must differentiate and complement the Shanghai and Shenzhen exchanges, while retaining the transfer mechanism — BSE-listed companies can choose to transfer to the STAR Market or ChiNext after 12 months of listing. Retaining the transfer mechanism both maintains institutional continuity and eliminates concerns about listing on the BSE, giving companies choice in their listing venue. As investor thresholds are lowered and market trading becomes more integrated, the transfer mechanism will level out differences in liquidity and valuation between the BSE, ChiNext, and the STAR Market. The second relationship involves coordinated planning and institutional linkage with the existing NEEQ Innovation Layer and Base Layer, maintaining balance in the market structure.

With the establishment of the BSE, we now have three coexisting exchanges: the SSE (Main Board, STAR Market), the SZSE (Main Board, ChiNext), and the BSE. Each exchange has its own clear positioning, with differences as well as slight overlaps between them, providing companies with more space and options for listing. As the multi-layered capital market improves and registration-based reforms advance, the inclusiveness and flexibility of issuance and listing mechanisms will further increase, better adapting to the development patterns and characteristics of innovative companies and allowing them to enjoy better capital market services.

3. Comparison of Market Positioning: STAR Market, ChiNext, and BSE

Let's compare the positioning differences between the BSE and ChiNext and the STAR Market. The STAR Market emphasizes sci-tech attributes, targeting six industries: new-generation information technology, high-end equipment, new energy, new materials, energy conservation and environmental protection, and biomedicine. It has "4+5" indicators for sci-tech attributes, with emphasis on supporting "hard tech" listings, and in practice stresses substance-over-form judgments.

ChiNext is positioned toward "three innovations and four new elements" — innovation, creation, and creativity — supporting the deep integration of traditional industries with new technologies, new industries, new business forms, and new models, with a negative-list management approach. The industry distribution of applications is relatively diversified.

In terms of company screening orientation, the BSE primarily serves innovative SMEs with good growth potential, including but not limited to "specialized, refined, distinctive, and innovative" (专精特新) companies. BSE-served companies can be small in scale (though not necessarily low in market cap), but they must have a future and potential — areas like artificial intelligence, intelligent driving, biotechnology, commercial aerospace, integrated circuits, and SaaS are particularly well-suited for the BSE.

Detailed Analysis of BSE Rules: From IPO to Refinancing and Ongoing Supervision

Let's first summarize the core content of the BSE's rule system.

Financing and admission. Loss-making companies are permitted to list, with diversified listing conditions set across profitability, growth, market recognition, and R&D capabilities. Inclusiveness is the BSE's most core characteristic, and also where it hopes to boldly advocate and achieve breakthroughs — truly giving choice and pricing power to the market, allowing innovative companies with core technology but still refining their business models to grow and develop with BSE support.

Trading system. A frequent criticism of the previous NEEQ was its poor liquidity. In this reform, investor thresholds for the BSE, Innovation Layer, and Base Layer have been adjusted to 500,000, 1 million, and 2 million yuan respectively — the BSE threshold is now aligned with the STAR Market. Based on the BSE's first-week performance, liquidity issues have improved significantly. More importantly, the BSE must attract truly high-quality, future-oriented listed companies that gradually gather and create atmosphere — then trading activity will naturally increase. And accommodating these companies depends on maintaining inclusiveness in admission criteria; the two reinforce each other.

Ongoing supervision. Compared to the Shanghai and Shenzhen exchanges, the BSE has made some differentiated arrangements based on the principle of "appropriately strict and appropriately lenient." There are more flexible institutional arrangements in corporate governance, information disclosure, equity incentives, and share reductions — well-suited to the characteristics of SMEs.

The exit mechanism is also well-designed. BSE listing is tiered and progressive; delisting is similarly a risk mitigation process — "in and out," "can enter and can exit." Companies that no longer meet BSE conditions can retreat to the Innovation Layer or Base Layer to continue trading, avoiding the harm to investors from direct delisting.

The BSE's market connectivity also demonstrates openness. Beyond retaining the transfer mechanism, innovative layer companies that have been listed on the NEEQ for one year maintain open choices for their listing board — they can pursue a BSE IPO or an IPO on the Shanghai or Shenzhen exchanges.

Next, let's examine several regulatory points that entrepreneurs are particularly concerned about.

1. IPO Conditions

Issuance conditions. A BSE IPO requires prior listing on the NEEQ for 12 months; after entering the Innovation Layer, companies may apply. During this period, companies can conduct IPO tutoring, filing, acceptance, and prepare application materials. The average BSE IPO review time is 3-4 months. If time is used efficiently, the BSE can provide companies with earlier listing opportunities.

Asset scale requires that the issuer's net assets at the end of the most recent year be no less than 50 million yuan. Public float requirements include: public issuance of no less than 1 million shares, no less than 100 subscribers, total share capital of no less than 30 million after issuance, no less than 200 shareholders after issuance, and public shareholders holding no less than 25% or 10% of total share capital (for total share capital exceeding 400 million).

One point deserves emphasis. At the Shanghai and Shenzhen exchanges, all existing shareholders are classified as non-public shareholders, with major shareholders subject to 36-month lock-ups and other shareholders to 12-month lock-ups. The BSE only classifies controlling shareholders, actual controllers, directors/supervisors/senior management, and shareholders holding more than 10% as non-public shareholders, with a 12-month lock-up; all other shareholders are public shareholders with no lock-up restrictions after listing. The BSE's share lock-up arrangements approach mature market standards — for minority shareholders (including most PE shareholders), shares become tradable immediately upon listing. Additionally, since the proportion of public shareholders is relatively high at listing, the initial issuance ratio need not be strictly limited to 25% or 10%; companies can more flexibly set issuance ratios based on funding needs, avoiding excessive dilution from large-ratio issuance at lower valuations.

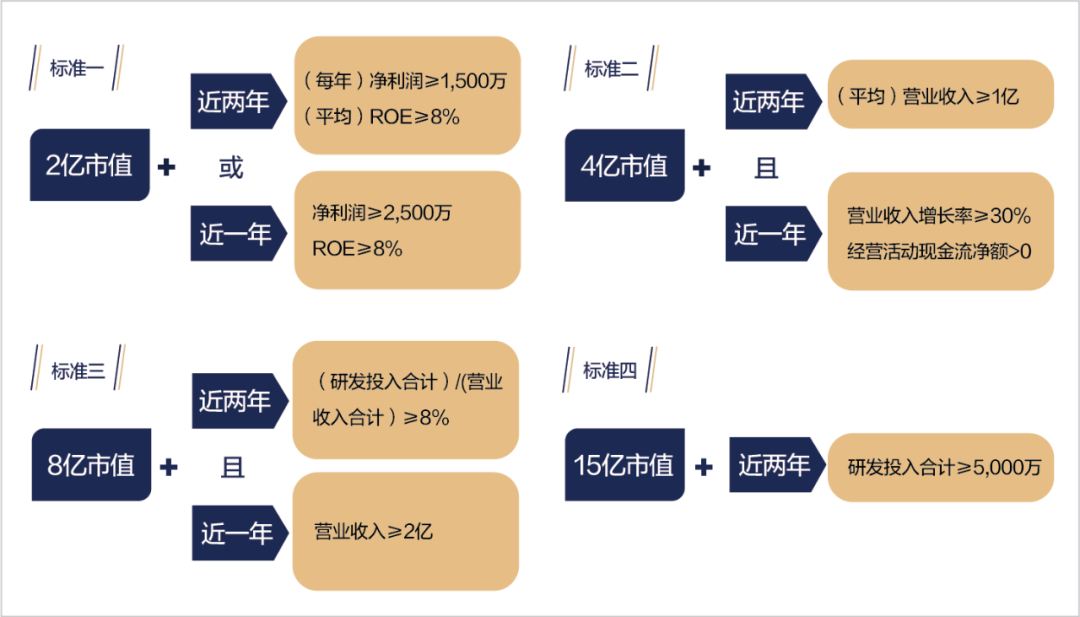

Financial requirements. The BSE has established four sets of standards, all market-cap-based, with financial indicator requirements noticeably lower than ChiNext or the STAR Market.

Standard 1: 200 million market cap, focusing on profitability with relatively high ROE requirements. Requires net profit of no less than 15 million yuan in each of the past two years, with average ROE (return on equity) of no less than 8%; or net profit of no less than 25 million yuan in the most recent year with ROE of no less than 8%. Standard 2: 400 million market cap, focusing on revenue and growth. Requires average operating revenue of no less than 100 million yuan over the past two years, with revenue growth rate of no less than 30% in the most recent year, and positive operating cash flow. Standard 3: 800 million market cap, examining revenue and R&D investment. Requires R&D investment as a percentage of operating revenue of no less than 8% over the past two years, with operating revenue of no less than 200 million yuan in the most recent year. Standard 4: 1.5 billion market cap, disregarding revenue and focusing on market cap, with total R&D investment of no less than 50 million yuan. Mainly applicable to strategic emerging industries such as advanced manufacturing, new-generation information technology, and biopharmaceuticals.

Some may ask: since BSE listing thresholds are relatively lower than ChiNext and the STAR Market, does that mean any company can list? I strongly disagree. The BSE is like a "young talent class" in the capital market — although admission thresholds are lower, the requirements for industry cutting-edge positioning, technological leadership, and potential and growth prospects are very high. BSE investors are primarily institutional investors and high-net-worth individuals, who will be even more demanding about company quality.

From the review and registration process perspective, the BSE is broadly consistent with ChiNext and the STAR Market, requiring both exchange review and CSRC registration. Currently, the BSE review process shows higher efficiency, shorter timelines, and better coordination between review and registration.

Issuance and underwriting. Pricing methods include direct pricing, online auction, and offline inquiry. Currently direct pricing is the more commonly used method for BSE listings, while inquiry-based issuance will gradually be adopted by more companies.

2. Refinancing and M&A Restructuring System

For refinancing and M&A restructuring, the BSE also implements a registration-based system with flexible institutional design. Refinancing issuance establishes authorized issuance, shelf registration, and self-managed issuance systems, reflecting characteristics of "small amounts, fast execution." For issuances within 12 consecutive months not exceeding 10% of total share capital with total financing not exceeding 20 million yuan, no sponsor documents or legal opinions are required — companies can conduct self-managed issuance. This is a distinctive arrangement carried over from the NEEQ system.

3. Ongoing Supervision System

For ongoing supervision, the BSE also has several distinctive institutional arrangements. Share reduction, as mentioned above: except for major shareholders, directors/supervisors/senior management, and shareholders holding more than 10%, other shareholders face no lock-up periods. This has certain positive effects on secondary market valuation and liquidity, differentiating from the Shanghai and Shenzhen exchanges.

Equity incentives. The BSE's institutional design is also relatively flexible. For core business personnel of listed companies, they can be included in equity incentive plans as long as proper procedures are followed. Incentive pricing is flexible — prices can be below 50% of market price. Equity incentive shares can reach up to 30% of total share capital, and shares granted to a single incentive recipient can exceed 1% of total share capital.

4. BSE IPO Path: Two Steps or Three Steps

Innovative companies have two paths to the BSE:

Three-step path: First enter the Base Layer at listing; after 12 months of listing and meeting Innovation Layer conditions, automatically transfer to the Innovation Layer upon annual report disclosure without review; then apply for BSE IPO. Two-step path: Simultaneously issue shares and enter the Innovation Layer at listing; after 12 months of listing, apply for BSE IPO. The advantage of entering the Innovation Layer at listing is that when subsequently applying for BSE IPO, there is no need to wait for the fixed May window for layer transfers, saving 3-6 months.

So what conditions are needed to enter the Innovation Layer? For financial and market cap indicators, there are three standards: Standard 1, focusing on profitability, requires net profit of no less than 10 million yuan over the past two years, weighted average ROE of no less than 8%, and total share capital of no less than 20 million; Standard 2, focusing on growth, requires average operating revenue of no less than 60 million yuan over the past two years with continuous growth, compound annual growth rate of no less than 50%, and total share capital of no less than 20 million; Standard 3, focusing on market cap, with no revenue or profit requirements, market cap of no less than 600 million yuan, total share capital of no less than 50 million, and for market-making transactions, no less than 6 market makers — this is a relatively special requirement. For example, biotech companies without revenue that want to enter the Innovation Layer typically need to adopt market-making transactions, find 6 market makers, and achieve a market cap of over 600 million yuan.

Beyond these financial indicators, there are two hard requirements for entering the Innovation Layer to note. First, cumulative stock issuance financing since listing must be no less than 10 million yuan; second, for public float, the company must have no less than 50 qualified investors.

IPO Planning Recommendations for Startup Companies

Every company has its own choices for capital market planning. There is no inherent better or worse among different boards — what matters is choosing the right timing and listing venue. If a company is sufficiently mature, going directly to the Main Board, STAR Market, or ChiNext is certainly fine, provided it maintains smooth financing capabilities in private markets to ensure it doesn't fall behind in its track. The BSE provides companies with a more forward-positioned, earlier-stage listing platform. If competitors choose public platforms while you remain in private markets, whether you can maintain leadership in fundraising speed and development speed is something companies need to consider.

My personal view is that if competition in a niche track is relatively intense, companies may choose to enter public markets earlier to gain more visibility and leverage the listing platform to secure competitive advantage. During the listing period, companies can also drive standardization and cultivation, improve corporate governance and internal controls, and deepen familiarity and understanding of capital markets.

A reminder: if listed on the NEEQ, the "rules of the game" change because the audience of investors changes. After entering the NEEQ, financing targets include not only PE and VC firms but also public funds, private funds, and other financial investors. Different investment institutions have varying requirements for due diligence, valuation adjustment mechanisms, etc., and companies must learn to adapt and communicate.

I believe the significance of the BSE lies not merely in adding another stock exchange, but more importantly in pushing the registration-based system to further reform in both scope and depth through the forward extension and expansion of its service targets, meeting the needs of the national innovation-driven strategy and stimulating the innovative development vitality of SMEs.

Regarding the BSE's development, continue to observe but don't doubt it. Not all companies need to go to the BSE — companies should combine their industry, scale, and development stage to choose the suitable board. If you feel the BSE suits you, don't hesitate, and don't worry about liquidity and valuation. Truly excellent companies will not be overlooked regardless of which board they are on. The BSE will allow companies with potential and a future to connect with capital markets earlier, driving faster and better development.