Outlook on Hong Kong IPO Opportunities: Uncovering Three Advantages — "Profit Improvement, Globalization, and Sector Leadership" | Ronghui

Embrace innovative mechanisms and leverage corporate strengths.

In April this year, China's securities regulator unveiled five measures to deepen capital market cooperation with Hong Kong, supporting eligible mainland industry leaders to list and raise funds in the city. On August 23, the Securities and Futures Commission of Hong Kong and the Hong Kong Stock Exchange issued a joint announcement lowering the market capitalization threshold for specialist technology companies listing under Chapter 18C.

Hong Kong has long been a key listing destination for innovative and high-growth companies. Despite current market challenges, the Hong Kong IPO market is drawing renewed attention as listing regimes continue to evolve and a wave of mainland companies successfully list or plan their debut on the exchange.

- What policy benefits and latest mechanisms in Hong Kong listings deserve attention?

- For companies in new technology, healthcare, and other sectors, how can they better identify their strengths and highlights to attract investors amid today's market environment?

- How should companies prepare for practical matters like auditing and compliance involved in a Hong Kong listing?

Recently, DFIN, CICC, Gaorong Ventures, Haiwen & Partners, KPMG, and Skadden, Arps, Slate, Meagher & Flom jointly hosted a closed-door session for innovative companies on the Hong Kong listing outlook, sharing insights on these questions. This was also part of Gaorong's 2024 Capital Acceleration series.

Recent Institutional Innovation in Hong Kong's Capital Market

Policy Certainty Bolsters Confidence

In his opening remarks, Kaibang Wang, CFO of Gaorong Ventures, noted, "Despite various objective challenges in the current market environment, we see continuous optimization of policies in Hong Kong's capital market. For example, recent IPO policies supporting innovative enterprises in specialist technology, biotechnology, and healthcare, as well as a series of reforms addressing market efficiency and liquidity. These measures are expected to further enhance Hong Kong's market attractiveness, and we look forward to the Hong Kong IPO market continuing to draw excellent companies and drive long-term industry development."

Xiaoxia Zhang, Vice President of Global Listing Services at Hong Kong Exchanges and Clearing, began by analyzing listing financing and valuation issues that companies care about.

From a financing perspective, "An IPO is not the end of a company's journey, but the starting point of a new chapter in the public markets. Beyond raising capital through new share issuance, the Hong Kong market also provides companies with very convenient and efficient refinancing mechanisms to help them timely secure funds needed for development."

Zhang explained that in recent years, thanks to continuous listing regime reforms by HKEX, a new economy ecosystem has taken shape. Since the implementation of Chapter 18A for biotech companies, 66 biotech firms have completed IPOs, raising over HK$120 billion in total; this has also created an agglomeration effect, attracting healthcare companies that meet traditional financial tests to list in Hong Kong, steadily building a globally leading healthcare fundraising hub.

In 2023, HKEX introduced Chapter 18C, allowing eligible specialist technology companies to list in Hong Kong, covering five sectors: next-generation information technology, advanced hardware and software, advanced materials, new energy and energy conservation, and new food and agricultural technology. Recently, the market capitalization threshold for specialist technology companies under Chapter 18C was lowered — the minimum for commercial companies was reduced from HK$6 billion to HK$4 billion, and for pre-commercial companies from HK$10 billion to HK$8 billion. "This is also a timely rule adjustment made in response to market conditions and company feedback." The amendments will apply temporarily for a three-year period from September 1, 2024 to August 31, 2027.

Zhang pointed out that the Hong Kong market boasts a unique investor structure that attracts global and Chinese capital. Listed companies can access various types of international, mainland Chinese, and local investors through the Hong Kong market, with institutional investors as the dominant and sufficiently diversified force, "including funds from Europe and the US, as well as emerging markets like the Middle East and Southeast Asia." Additionally, the Stock Connect mechanism allows mainland investors to invest in Hong Kong stocks in the most convenient way.

Looking ahead, "policy certainty strengthens investor confidence in the Hong Kong market and lays the groundwork for a market recovery." Zhang also introduced Hong Kong's disclosure-based approval regime, IPO application and review processes, and listing timelines during her presentation. "HKEX will continue to promote innovation and reform, consistently building Hong Kong as the preferred overseas listing venue for mainland enterprises."

Choosing Between A-Share and Hong Kong Listing Paths

Comprehensive Assessment of Listing Standards, Valuation Levels, and Predictability

During the event, Guanlei Ren, Executive Director of CICC's Investment Banking Department, analyzed the choice between A-share and Hong Kong listing paths for companies, incorporating the latest market dynamics.

Ren noted that the securities regulator has repeatedly voiced support for eligible mainland industry leaders to list and raise funds in Hong Kong, helping the city consolidate and enhance its status as an international financial center. Currently, the Hong Kong IPO market has a substantial pipeline of pending issuances, with nearly 100 projects having filed A1 applications and advancing their listing plans. From the industry distribution of pending projects, new economy sectors including advanced manufacturing, consumer, TMT, and healthcare dominate.

Based on an overall comparison of listing standards between A-shares and Hong Kong, Ren provided companies with an analytical framework for planning their listing path. The A-share market generally commands relatively higher valuation levels with better liquidity; on the review dimension, Hong Kong listings offer greater predictability and certainty. Hong Kong listings need to meet requirements under Hong Kong regulators and the CSRC filing system, and companies are expected to face no substantive obstacles in the HKEX listing review.

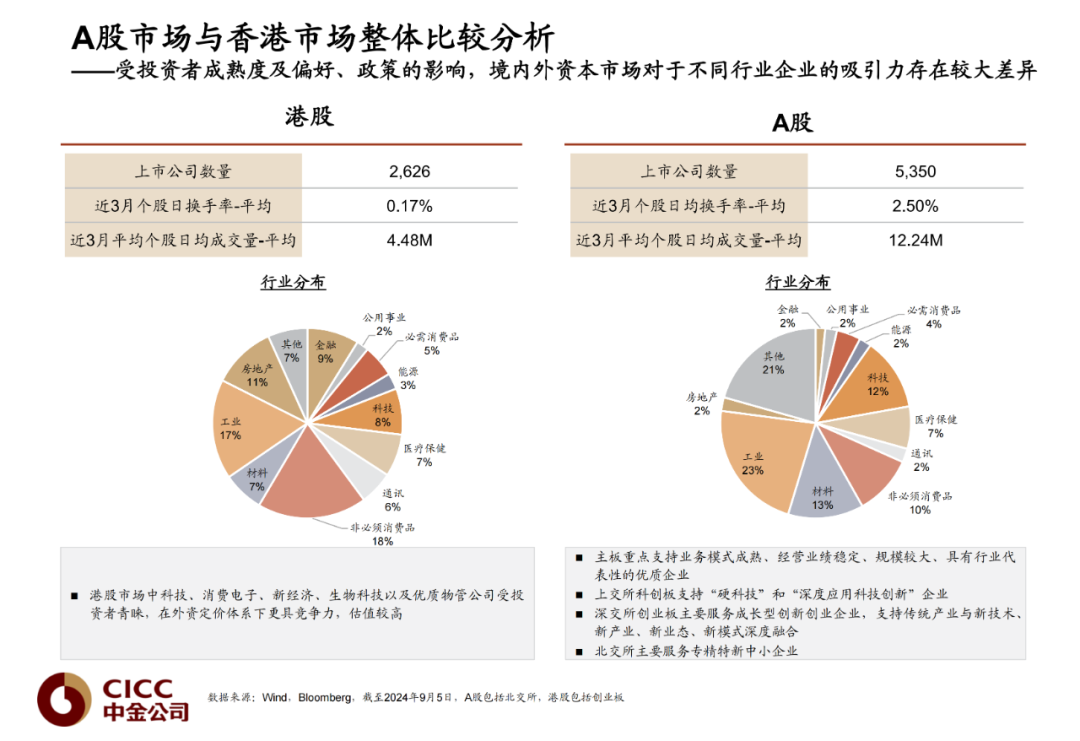

Additionally, Ren pointed out that due to differences in investor maturity and preferences, as well as policy influences, A-shares and Hong Kong have significantly different appeal for companies in different industries — in the Hong Kong market, technology, consumer electronics, new economy, biotechnology, and quality property management companies are favored by investors and more competitive under foreign pricing systems, commanding higher valuations; different A-share boards each have their emphases, such as the main board focusing on supporting quality enterprises with mature business models, stable operating performance, large scale, and industry representation, while the STAR Market supports hard technology enterprises, among others.

Concluding her presentation, Ren systematically outlined Hong Kong listing structures for companies and compared H-share and red-chip listings on the Hong Kong main board across dimensions including listing timeline, refinancing convenience, major shareholder stock liquidity, valuation, post-listing trading activity, restructuring complexity, equity incentives, listing costs, and subsequent difficulty of A-share listing. "If a company still hopes to list on A-shares in the future, H-share listing is recommended."

Innovative Companies Planning Hong Kong Listings

Identifying Three Key Strengths: Profitability, Globalization, and Sector Leadership

Yilin Xu, Partner at Skadden, Arps, Slate, Meagher & Flom, drew on extensive Hong Kong listing transaction experience to share expectations for Hong Kong's future and how companies can identify their strengths to successfully list.

Xu expressed optimism about Hong Kong's outlook for the next two years. Since 2022, Hong Kong has trended downward due to the confluence of multiple macro factors including US interest rate hikes and geopolitics, with trading volume in particular seeing rapid decline. But as the US enters a rate-cutting cycle, and as other surrounding markets also face macro challenges, "I believe considerable capital will still flow back to Hong Kong, and today we're already seeing growing enthusiasm among companies to launch Hong Kong IPOs."

In today's relatively constrained liquidity environment, Xu summarized that companies with three characteristics stand a good chance of completing an issuance smoothly or achieving strong market performance in Hong Kong.

First, companies with good profit margins or clear profit improvement trends — "compared to top line, investors today are more focused on bottom line."

Second, companies with higher internationalization levels and overseas expansion capabilities tend to achieve better market performance.

Third, companies need to identify their advantages and highlights, and whether they can be recognized as the absolute No. 1 in a given sector.

Regarding Chapters 18C and 18A, Xu also shared practical considerations based on actual experience. For 18C specialist technology companies, the issue of领航资深独立投资者 (leading cornerstone independent investors) requires heightened attention. "Leading investors themselves have high qualification requirements, and they need to cooperate closely throughout the listing process," so a systematic review of leading investors needs to begin on day one of the project or even earlier.

For 18A biotech companies, clinical progress of core pipelines needs attention. "The original intent of Chapter 18A was for IPO proceeds to be invested in R&D. If core pipelines have already reached commercialization, that may actually disqualify a company from 18A."

Practical Analysis

Compliance, Regulatory, and Auditing Issues for Hong Kong Listings

Chao Huo, Partner at Haiwen & Partners, shared insights on structural choices, processes, and common compliance issues for A-share to Hong Kong listings under the overseas listing filing rules. Huo noted that the choice between H-share and red-chip structures for Hong Kong listings requires careful consideration of multiple core factors based on company fundamentals, including future A-share listing plans, foreign investment access restrictions, investor attributes, timeline plans, restructuring costs, share liquidity, and lock-up periods.

Additionally, Huo systematically outlined and shared key focus areas during the CSRC filing process for listing-bound companies, including — shareholder verification, historical equity changes and tax compliance, equity incentives, business operation compliance, data compliance, business independence, and foreign investment access restrictions. He also offered companies recommendations such as proactively reviewing relevant matters before filing and paying attention to compliance requirements during business operations.

Kunpeng Lu, TMT Industry Audit Lead Partner at KPMG China, focused on analyzing several financial issues and differences involved in A-share to Hong Kong transitions.

First is the accounting treatment for terminating VAM (valuation adjustment mechanism) agreements. Lu noted that unlike A-shares, IFRS and Hong Kong regulators have no additional guidance on stipulating "void ab initio." Related investment proceeds received by issuers should be accounted for as financial instruments rather than equity instruments before the VAM arrangement is terminated, "meaning they are treated as liabilities for accounting purposes, though we are increasingly confident this issue will not become a listing obstacle."

Second, new economy companies listing in Hong Kong prefer to use non-IFRS measurements. Companies can select and adjust calculation methods for these metrics based on their business characteristics, operating environment, and specific reporting purposes, with the aim of better demonstrating company performance to investors.

Lu also advised companies to pay attention to the accounting impact of business restructuring, as well as differences between A-share and H-share listings in fiscal year definitions, revenue recognition, R&D expense capitalization, and share-based payments.

For entrepreneurial companies, the Hong Kong market offers opportunities including an international marketplace, a bridge closely connected to mainland investors, and a flexible and efficient refinancing market, while continuously optimizing market structure and listing mechanisms. On the foundation of identifying their own strengths and highlights, companies can examine Hong Kong opportunities from multiple dimensions, plan prudently, and set sail toward their goals.